Accenture (ACN)

Q1 Results

We looked at the latest quarterly results for Accenture (ACN) for a couple of reasons.

The first was to consider whether it makes an attractive, relatively defensive investment.

Secondly, we are interested in the implications for a smaller company in the same sector called Infosys (INFY). The latter is an India-based technology outsourcing company. My past articles about Infosys can be found here, here and here.

Accenture (ACN) is a professional services company serving clients in various industries globally. ACN is a large company. Some key statistics will illustrate this.

ACN has 799k employees at the end of 2024 (50% are in India).

The Annual Revenue run-rate is now $68bn.

ACN has offices and operations in 200 cities in 50 countries.

The current scale means it is difficult to grow fast going forward.

ACN originally was the Consulting Arm of US accounting firm, Arthur Andersen. It competed with the likes of McKinsey, Bain, BCG, LEK and so on. The latter more prestigious firms were involved in strategic consulting interacting at Board and CEO level. Accenture was focused on business transformation with a more detailed operational focus, having a close relationship a dialogue with the CEO, CTO and senior operating managers.

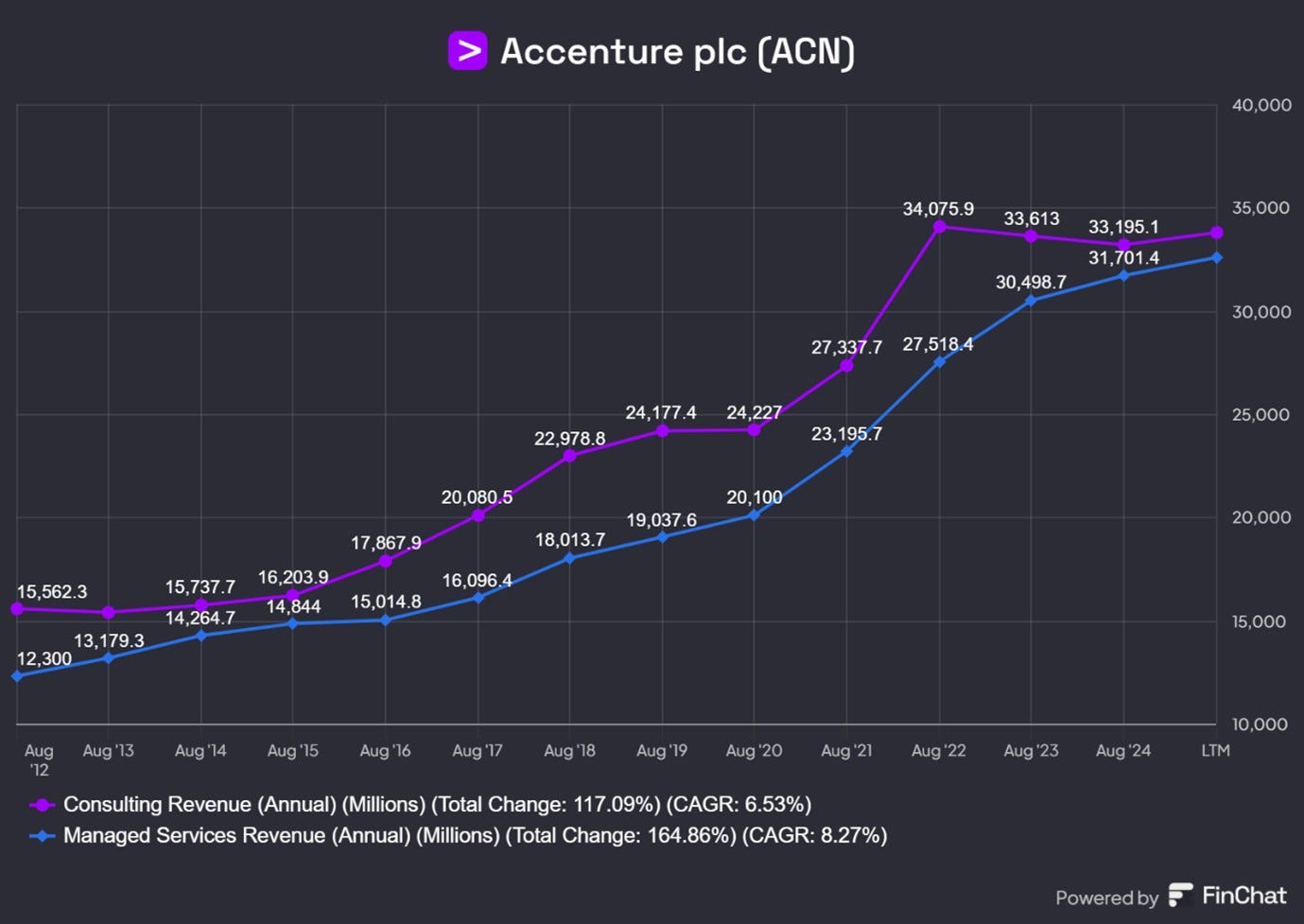

ACN has grown strongly in the last few decades in large part by taking on the non-core and back-office operations of companies, including the clients’ employees. They enabled their clients to outsource non-core operations. Today, revenues are equally split between Consulting and Outsourcing.

Consulting – 51% of Revenues

Outsourcing or Managed Services - 49% of Revenues

ACN serves the following segments.

· Communications,

· Media and Technology;

· Financial Services;

· Health and Public Service;

· Products, and

· Resources.

ACN works with 91 of Fortune Global 100 companies.

Accenture consultants have become indispensable to their clients over time. Very few firms have Accenture’s broad scope of capabilities including technology & back-office capabilities.

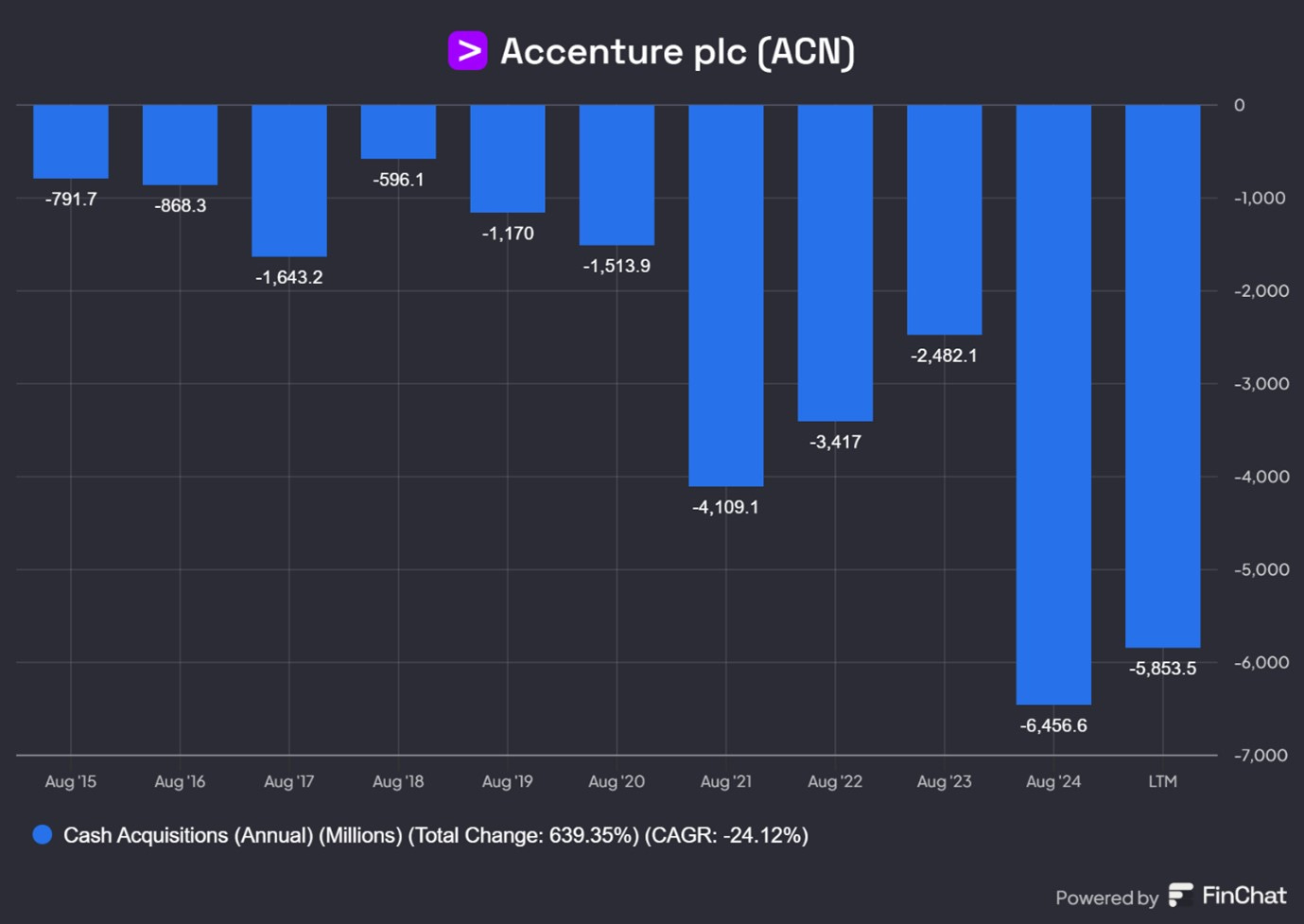

ACN done a relatively large number of small acquisitions. These are mostly of companies with niche development solutions which ACN can integrate quickly, and offer to their large client base.

In recent years, ACN has seen significant growth as its clients have shifted workloads to the cloud. It helps clients migrate integrating their systems with cloud-based operating platforms. ACN is recognised as the leading systems integrator for each of AWS, Azure and Google Cloud platform.

ACN has a broad range of capabilities.

“No other company in our industry can simultaneously do operations that help a company redo their supply chain and a finance function and reduce costs and digitize, at the same time we're helping them migrate to the cloud.”

In the last two years, it has been trying to boost revenues from the AI revolution.

Technology is the single biggest driver of change in companies today and the depth,

breadth and scale of our technology capabilities across our services is unmatched.Vast majority of companies are early in their transformation and whether digital

leader, leapfrogger, laggard or in between, all face multi-year journeys ahead.Ongoing exponential technology change that is accelerating and will create new opportunities, disruptions and change for our clients.

We will present a financial profile of the company before evaluating the most recent quarterly results.

Financial Profile

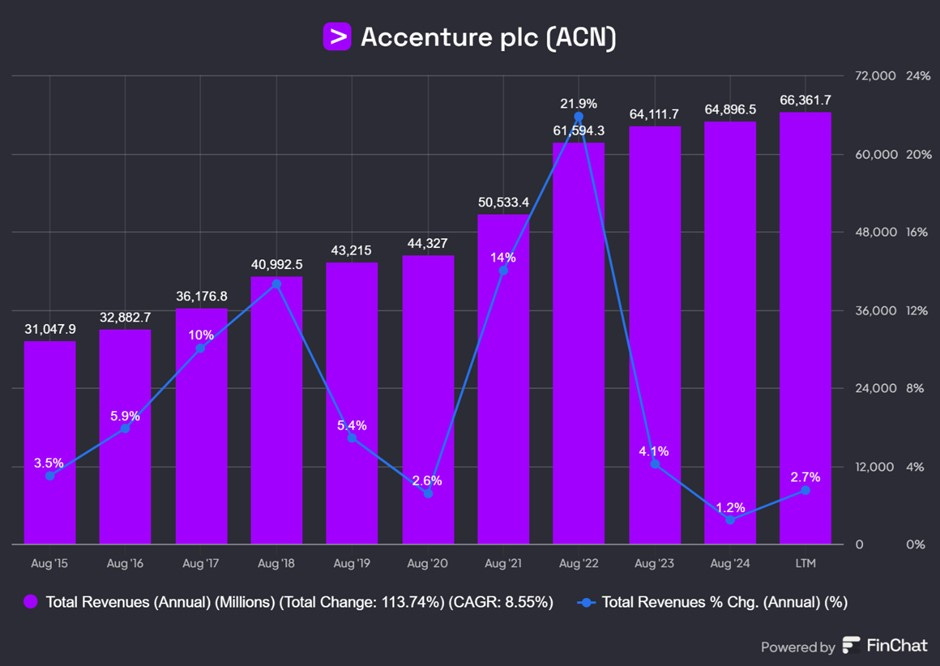

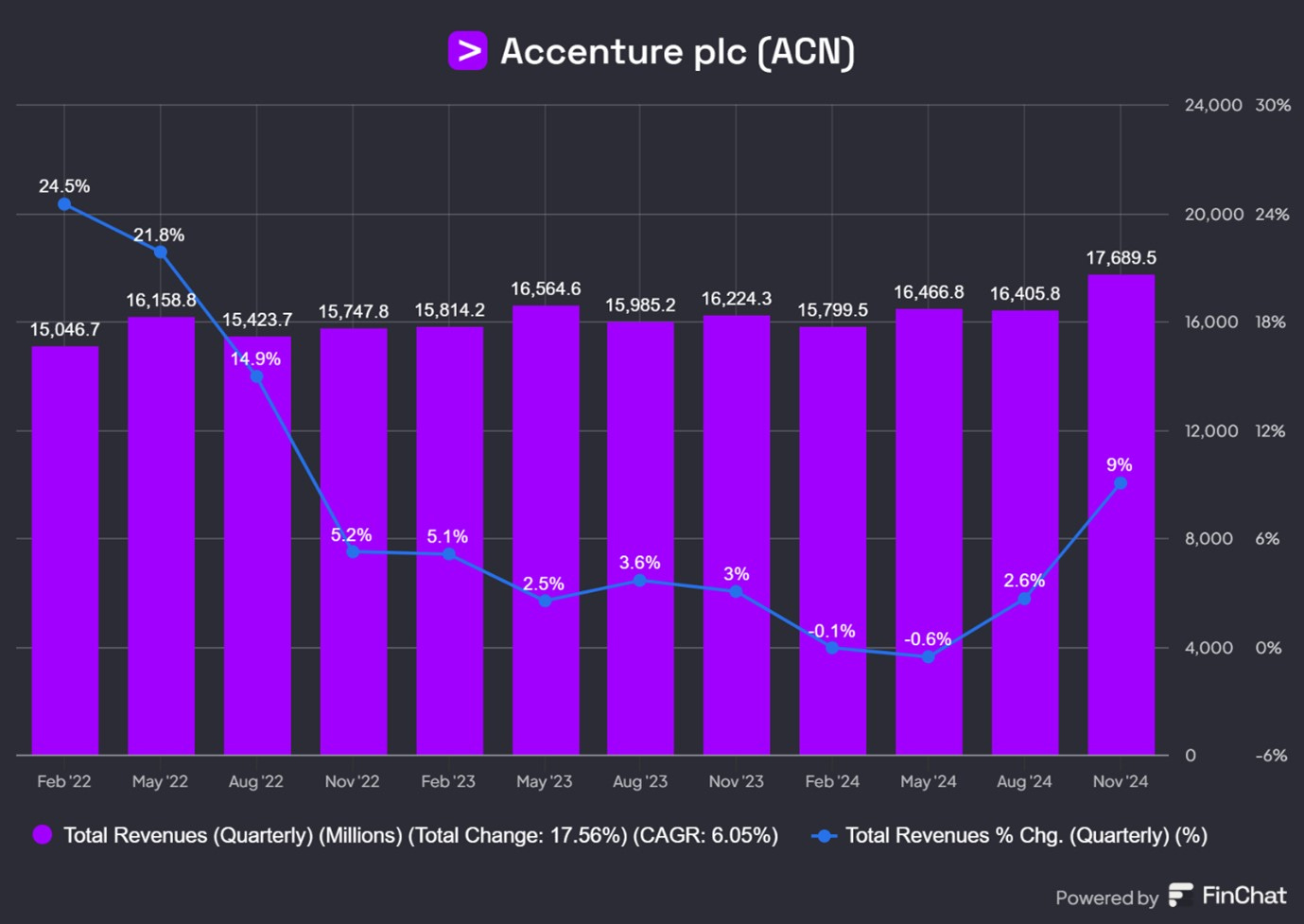

Total Revenues recovered strongly after the Covid-19 pandemic but revenue growth has been subdued in the last three years. Total Revenue for FY 2024 was $66.3bn and has grown at a CAGR of just 8.6% in the last five years.

Total revenues are almost equally split between Consulting and Managed Services. In the last twelve years, Consulting Revenues has grown at a CAGR of 6.5% while Managed Services have grown faster at 8.3% CAGR.

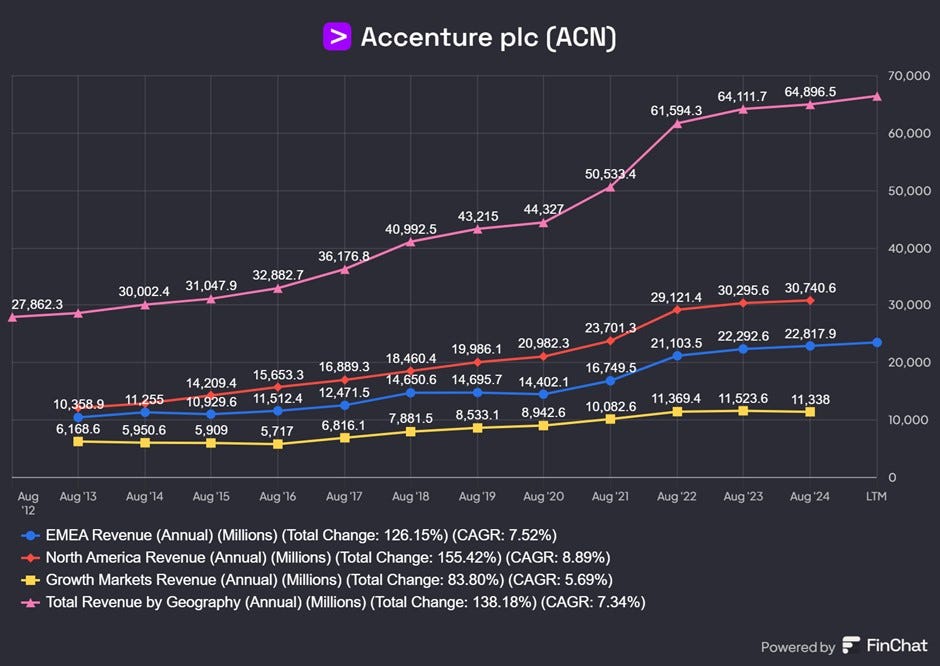

ACN’s revenue is geographically diversified and Americas is the largest and fastest growing region.

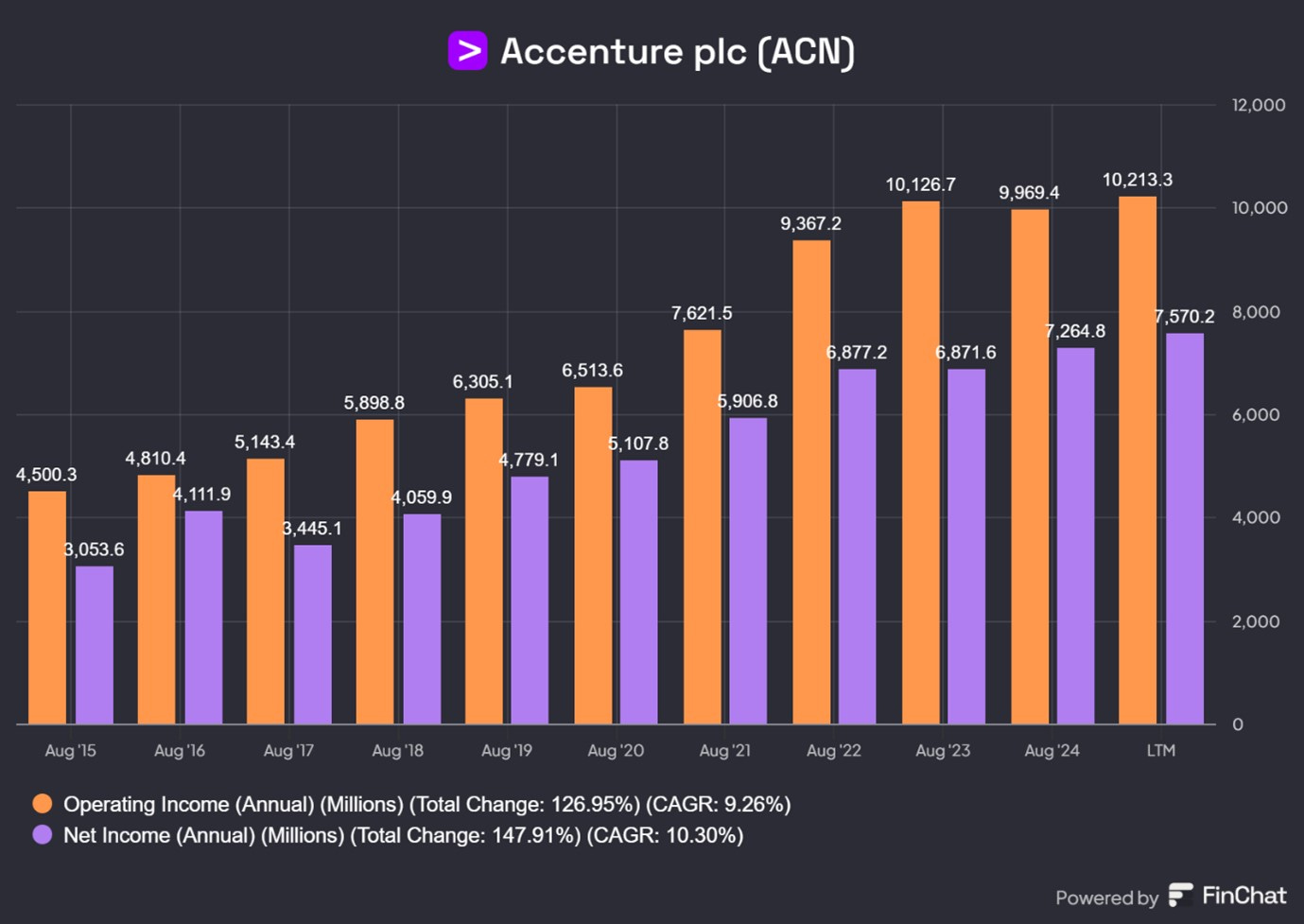

In the last five years, Operating Income and Net Income have grown at CAGR of 9.26% and 10.3% respectively. This is not much higher than the revenue growth rate of 8.6% and suggests that ACN’s business model offers little operating leverage. In order to boost revenues, you have to hire more people, so costs broadly grow in line with revenues.

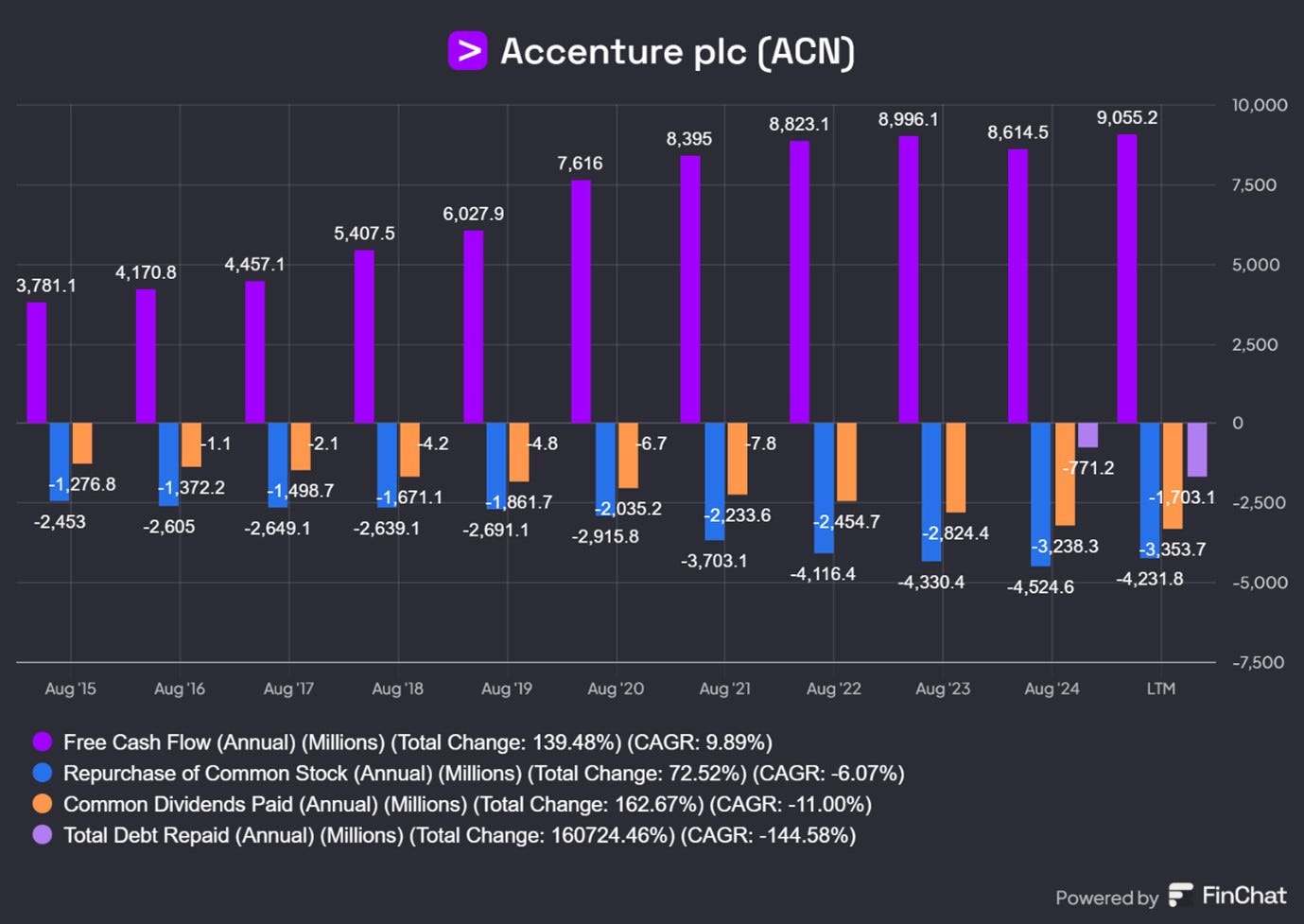

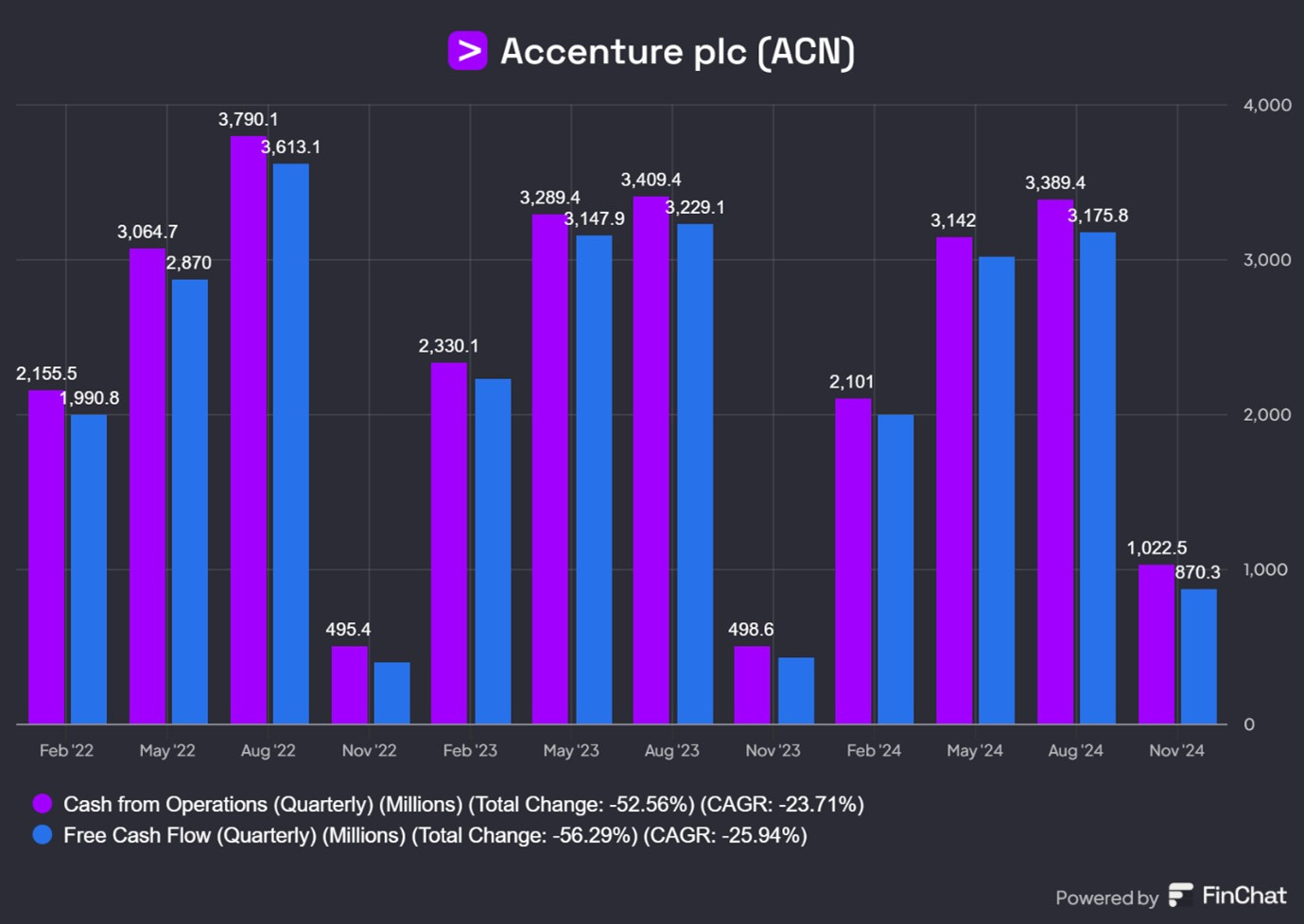

ACN has been a strong generator of Operating Cash Flow and Free Cash Flow. These have both grown by a CAGR of 9% over the last five years. There is little difference between the two as ACN has relatively low capital expenditure.

While capital expenditures are low, ACN does spend heavily on acquisitions - in FY24, these totaled an outflow of $6.5bn (about 70% of Operating Cash Flow). These are a series of small, niche acquisitions of companies which have developed some unique leading- edge product or service. ACN quickly integrates the acquisitions and offer the product or service to their clients.

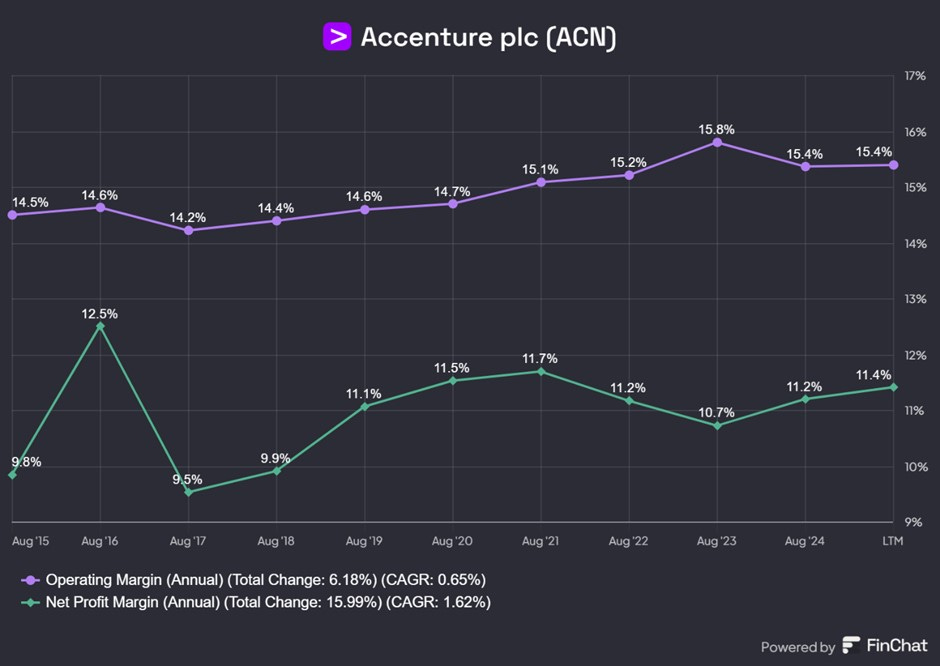

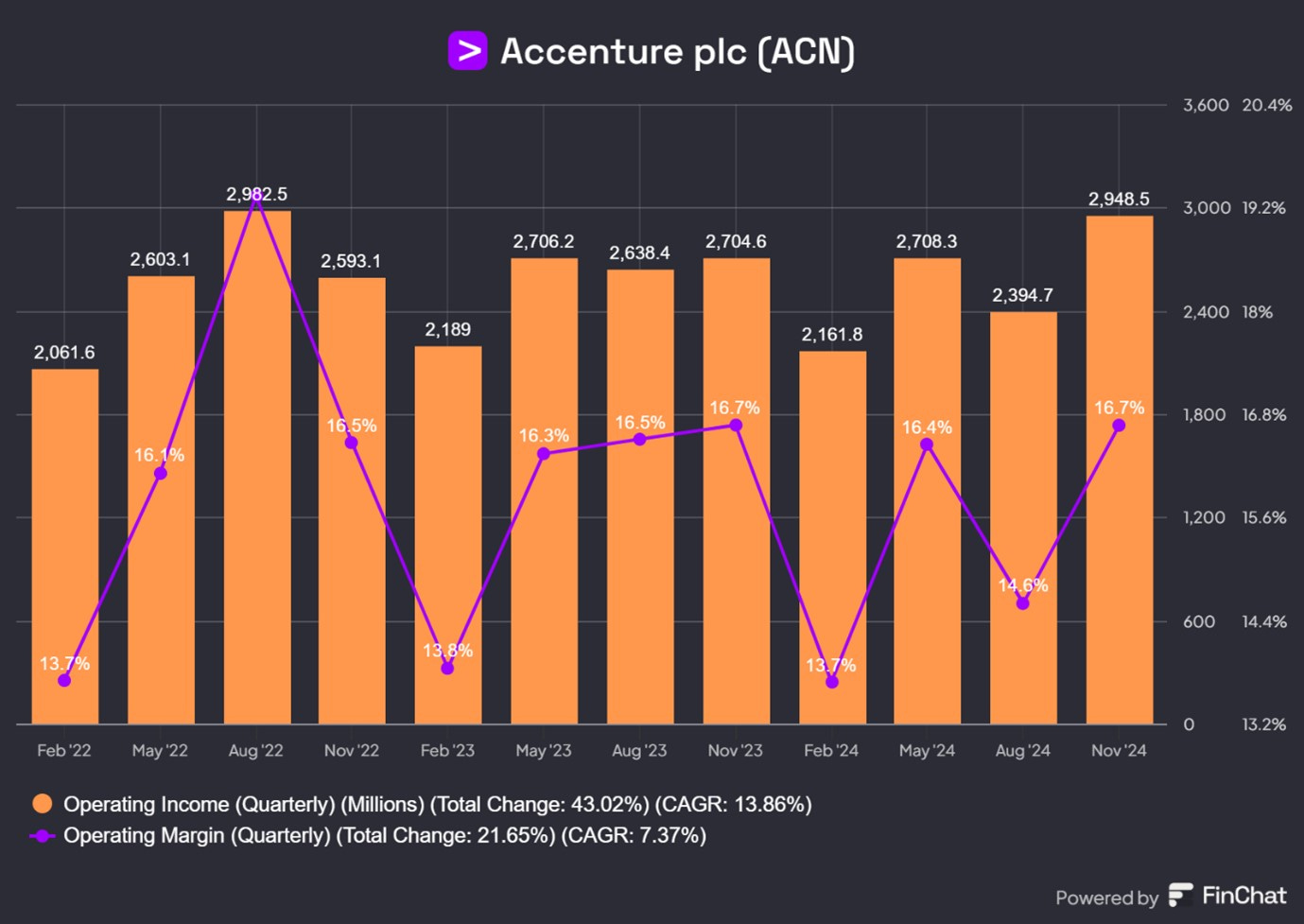

Margins have been stable, with Operating Margins at about 15% and Net Profit Margins at about 11%.

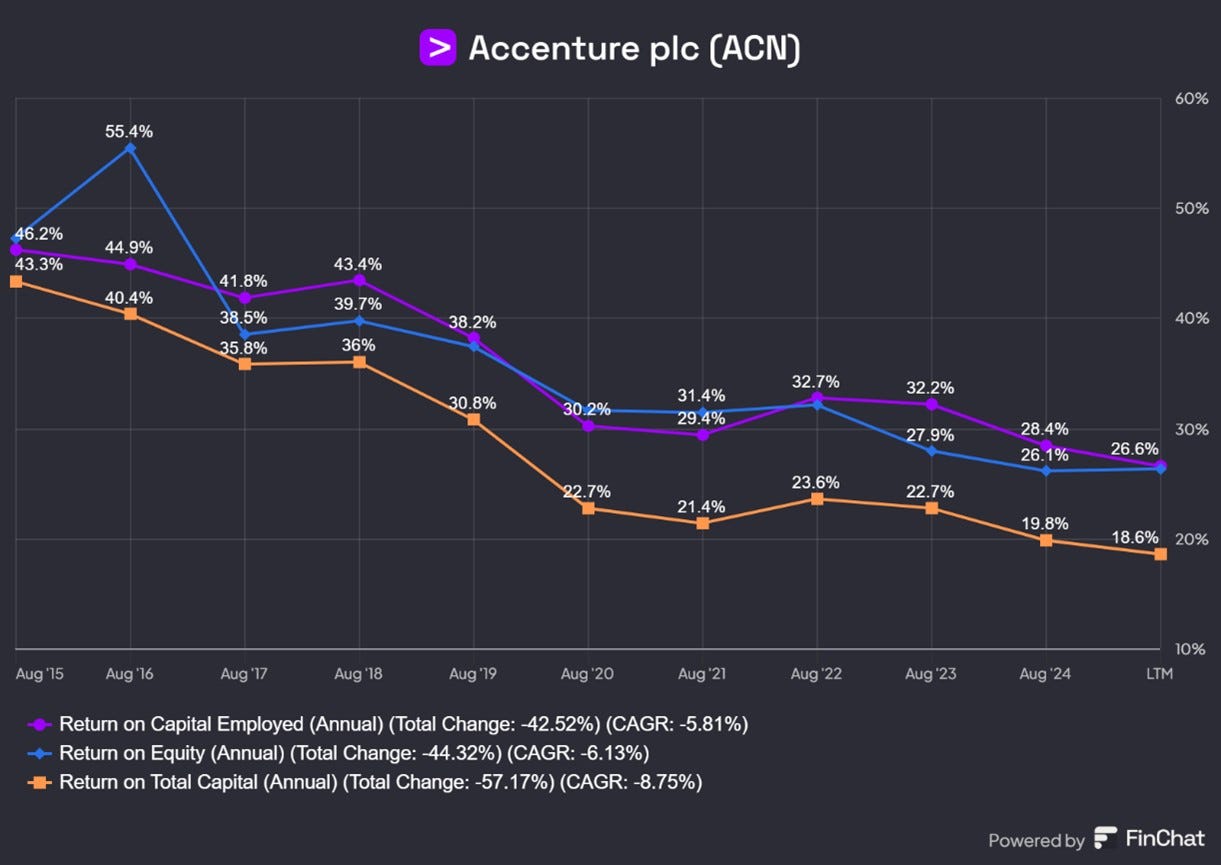

Profitability has declined steadily in the last ten years with the ROE (Net Profit/ Average Equity) and ROCE (Operating Profit/Capital Employed) are both at 26%. This is clearly a negative trend.

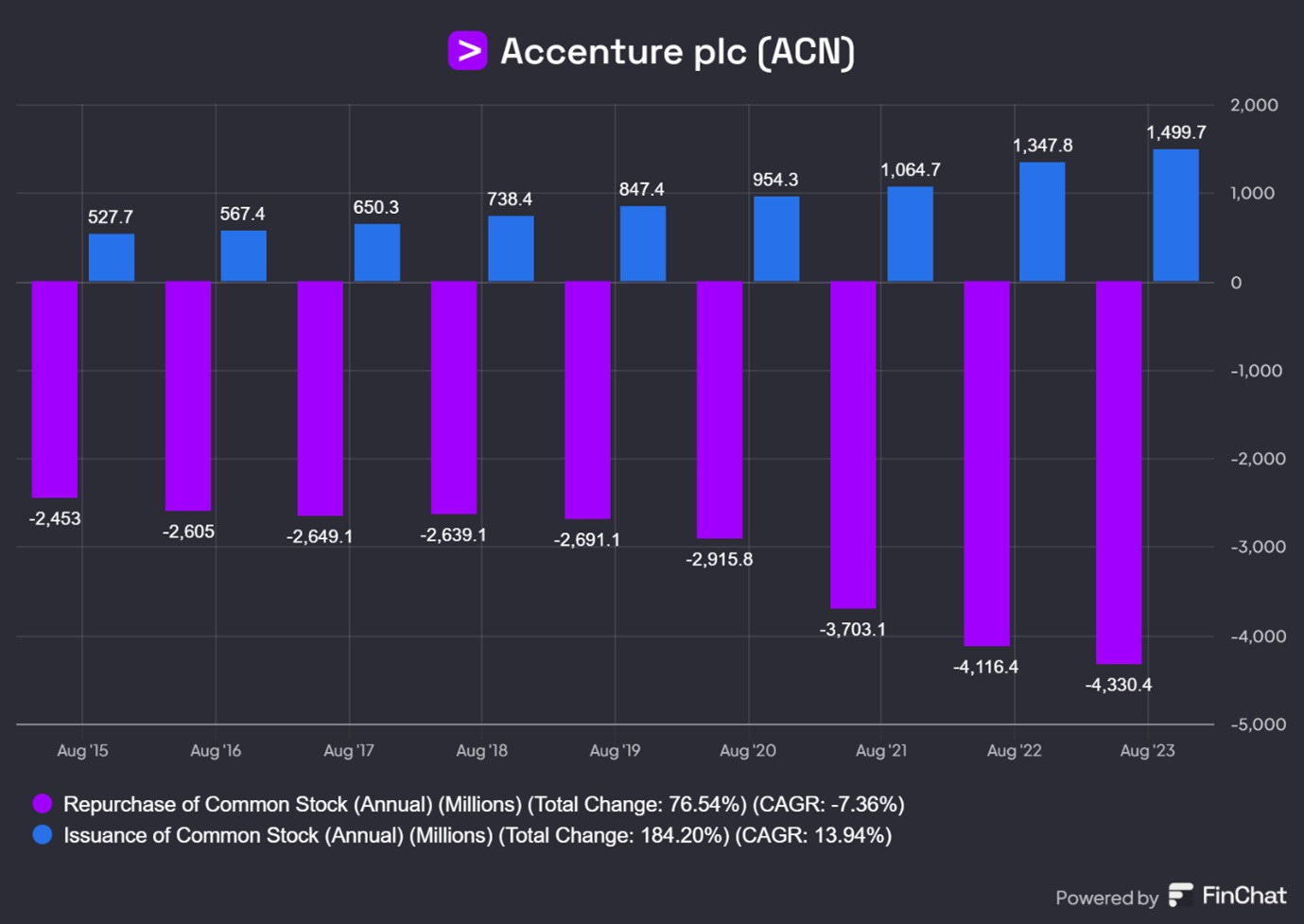

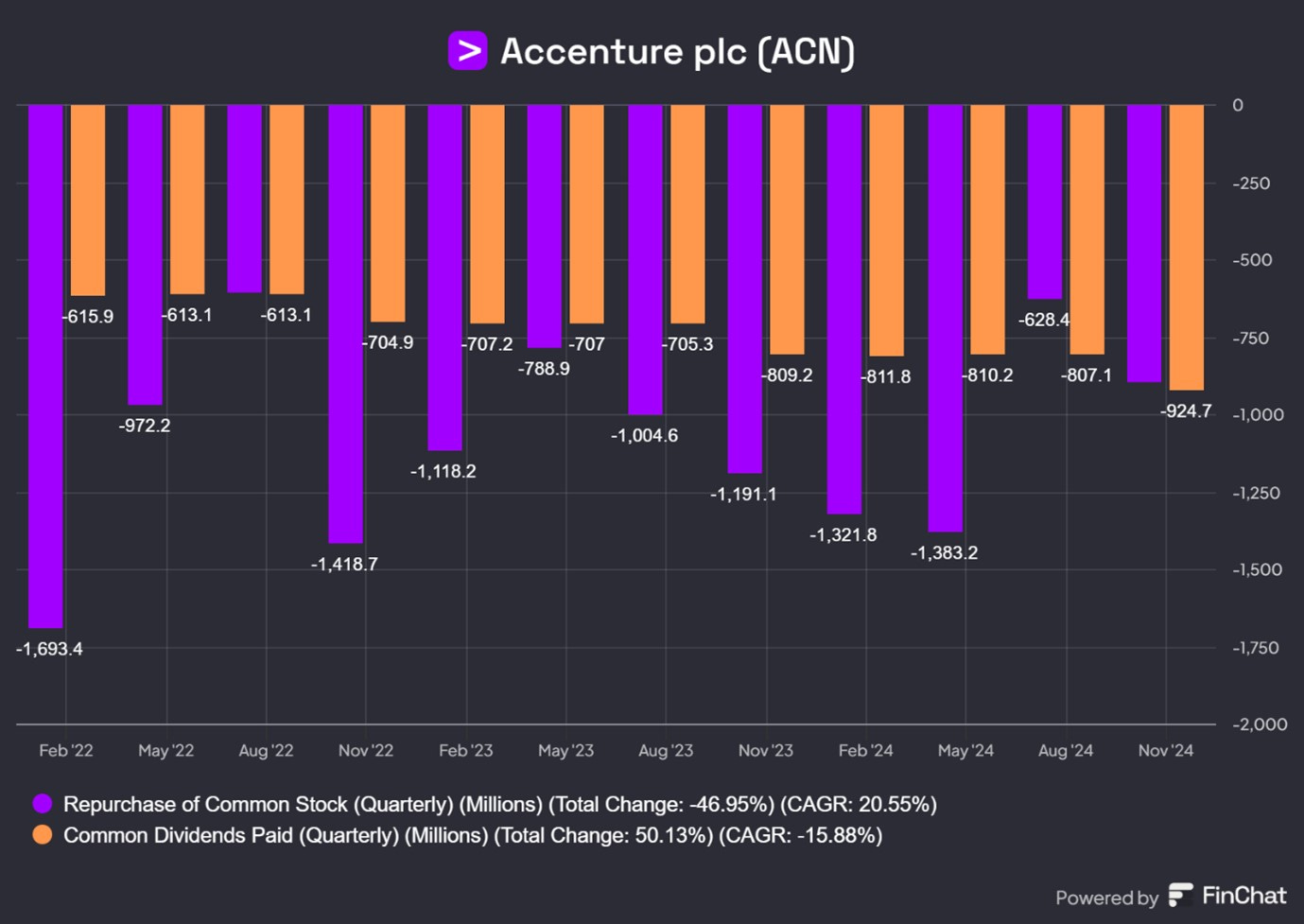

The company uses Free Cash Flow to repurchase stock (about 45% of Free Cash Flow) and pay common dividends. In the chart above, stock repurchases, dividends and debt repayments are shown as negative bars as they are cash outflows.

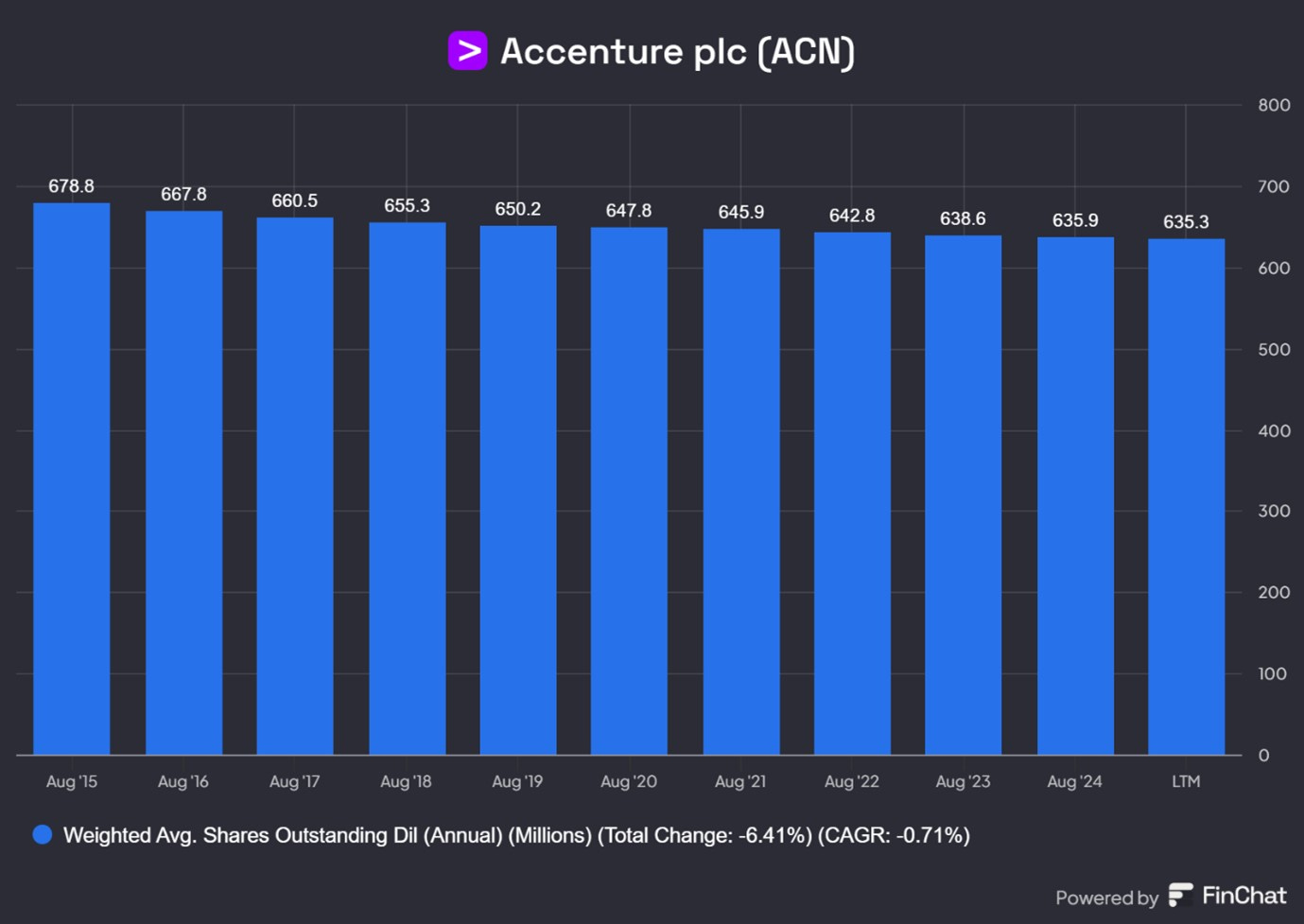

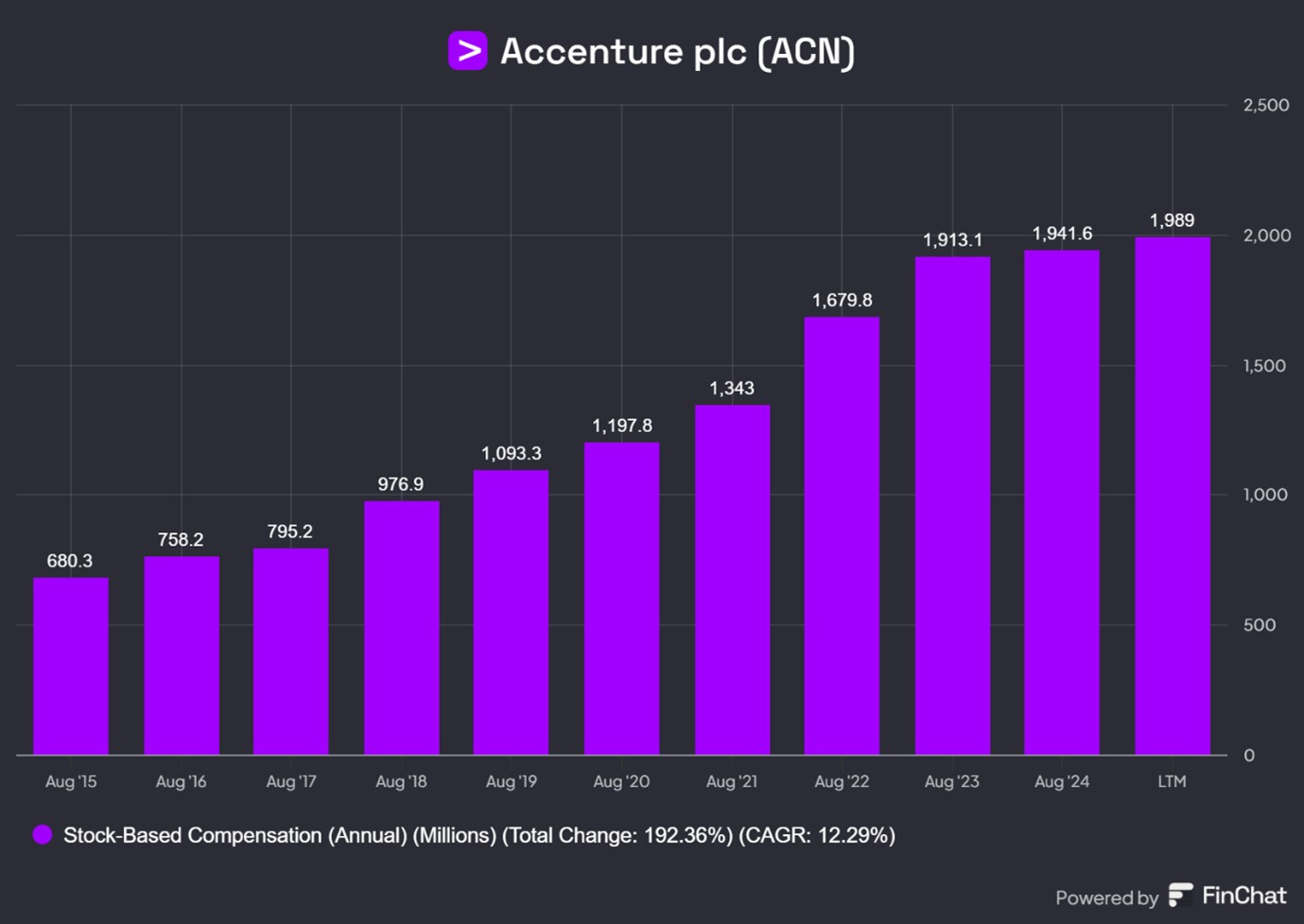

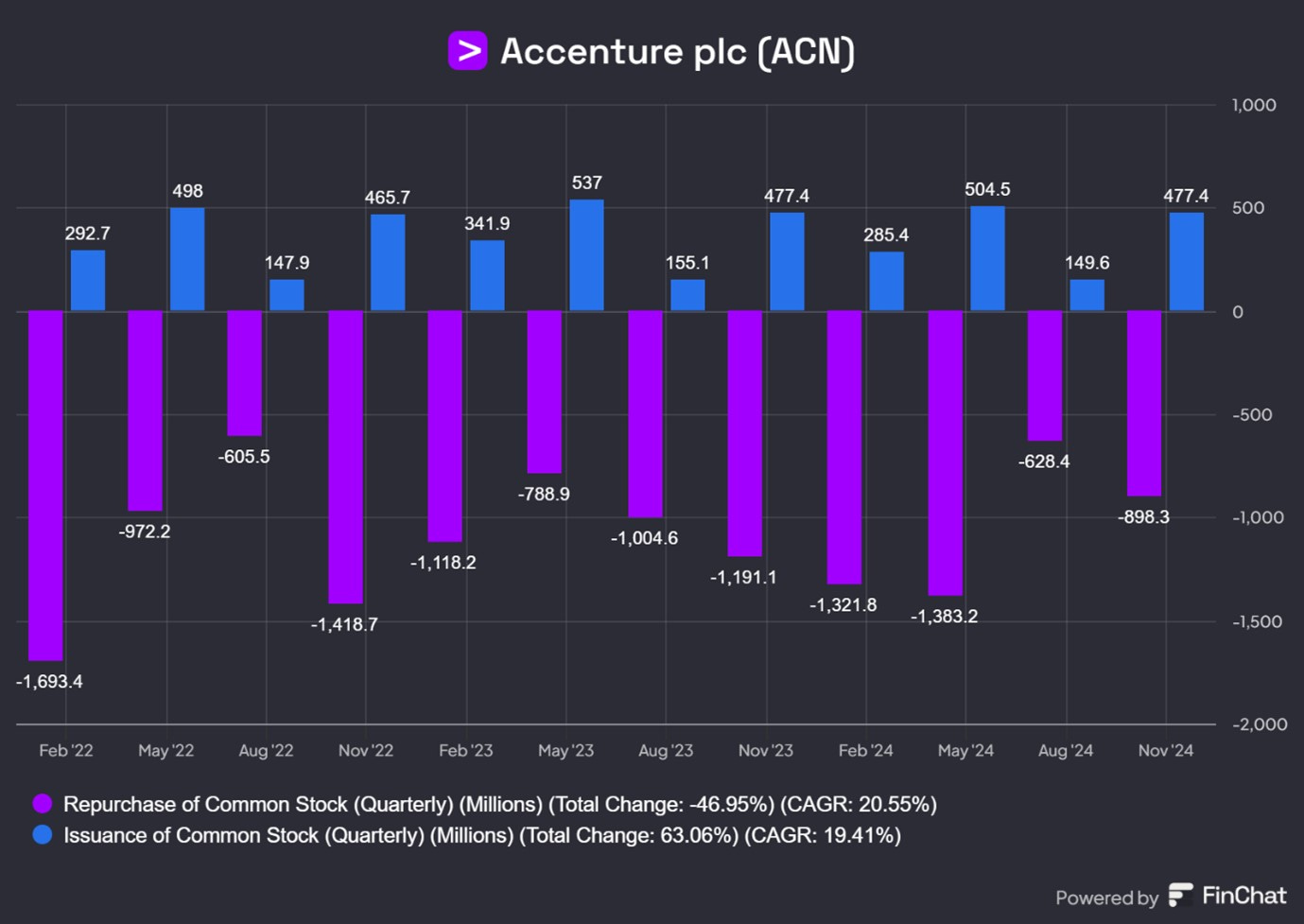

The numbers of shares outstanding have not declined by as much as one might have expected, given the scale of share repurchases. This is due to Stock-Based Compensation (SBC) which leads to new stock issuance, as employees are granted new shares, or as stock options granted in the past are exercised.

New stock issuance has been equal to about 35% of the total shares repurchased by the company. Shareholders are only getting a partial benefit from the stock repurchase undertaken by the company.

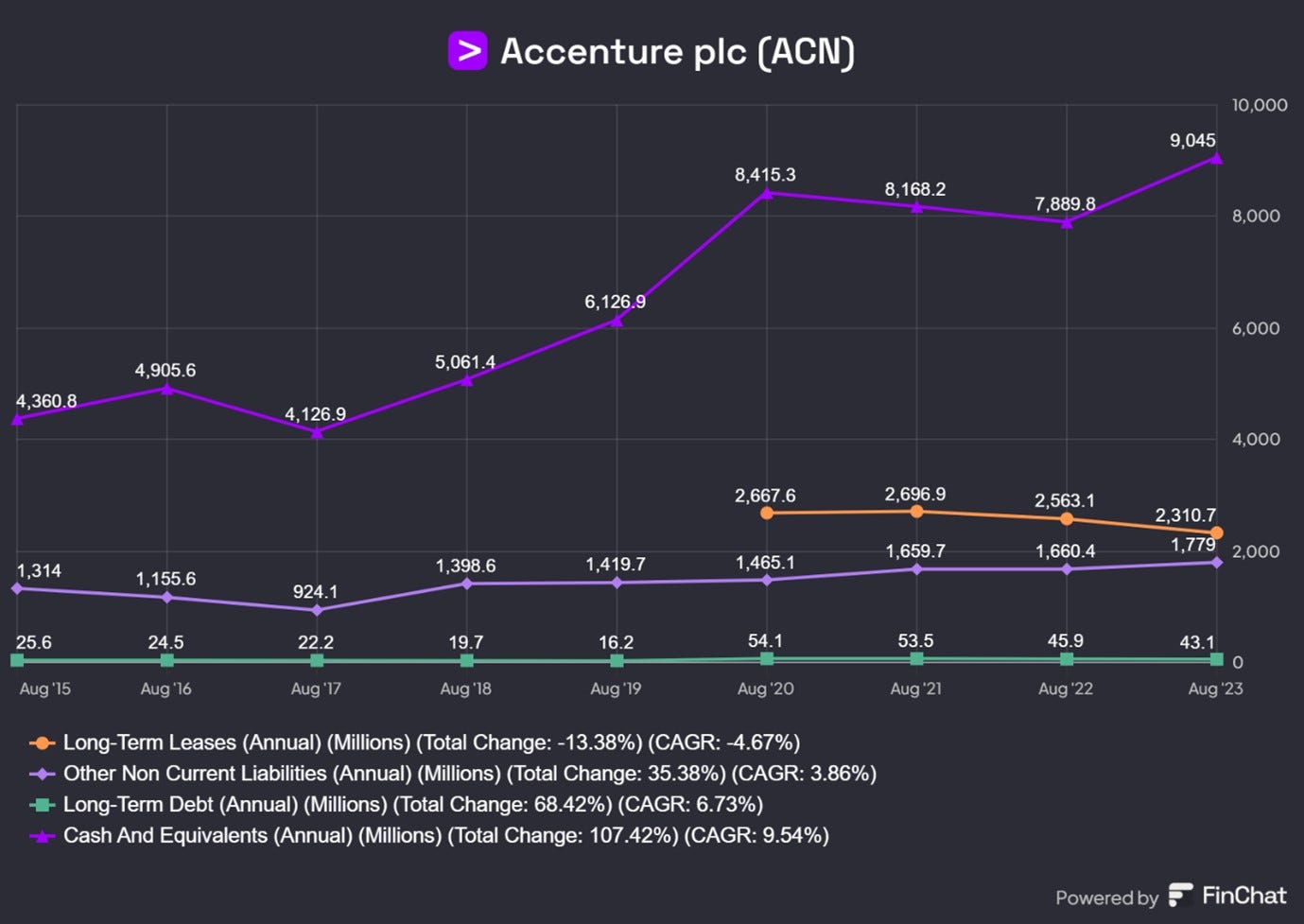

Company has always operated with a conservative balance sheet with Cash and Short-term investments much greater than non-equity long-term liabilities.

The chart above shows Cash and Equivalents have been much greater Long-Term Debt and other non-current liabilities.

Long term returns from the ACN stock:

· In the last 17 years, the stock has given a total return of CAGR of 15.93%

· In the last 5 years, the stock has given a total CSGR return of 15.85%

These are creditable and consistent but not spectacular returns.

Review of most ACN’s recent quarterly results

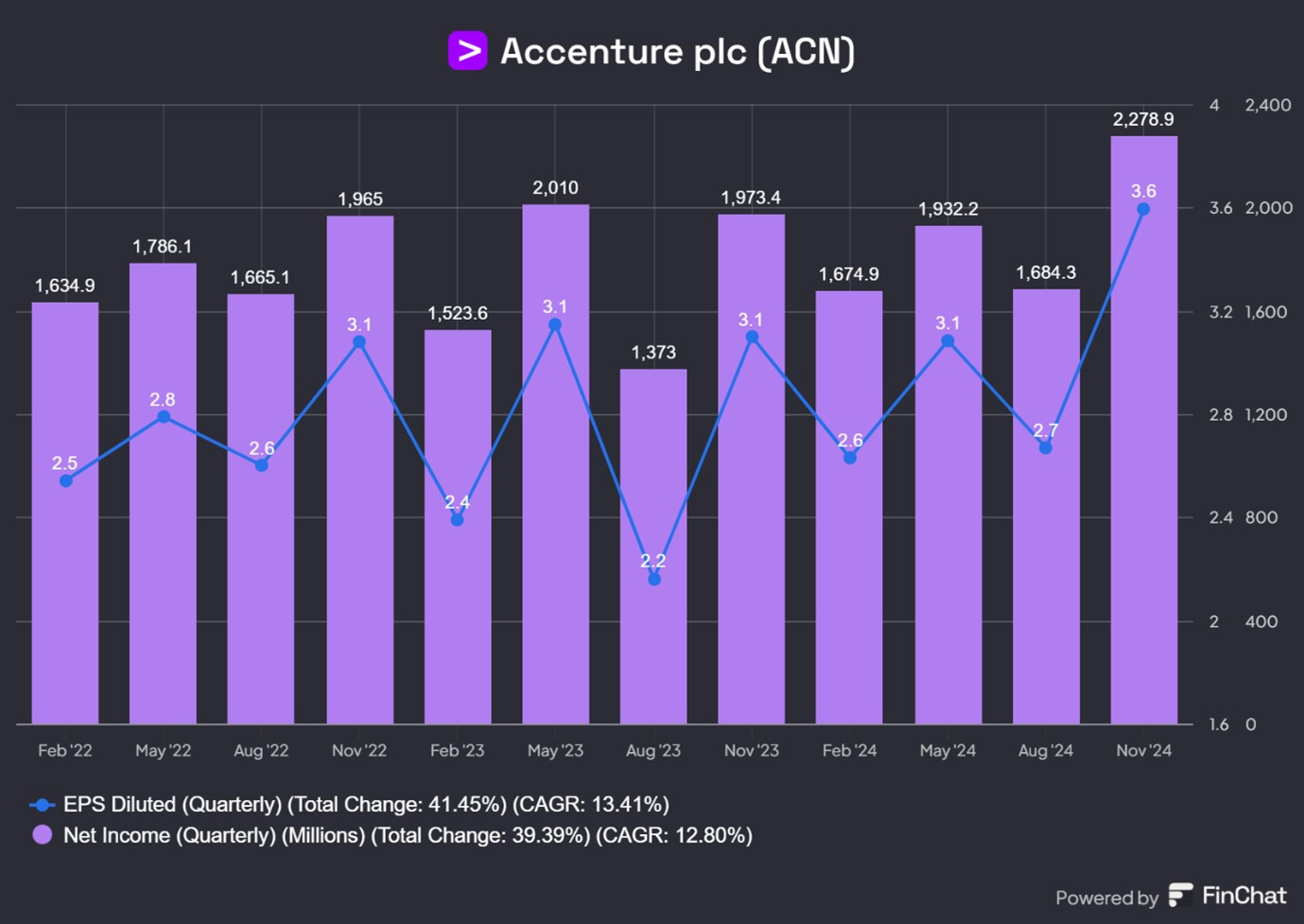

In the most recent quarter, revenue growth accelerated to 9% (y/y). Net Profit and EPS grew 15.5% (y/y) and 16.1% (y/y) respectively.

In the last three years, Total Revenues have grown at a CAGR of 5.7% while Net Profit growth has been 8.4% and 9.0% respectively. Revenue growth in the most recent quarter was higher than the recent trend.

Operating margin was flat compared to adjusted operating margin last year.

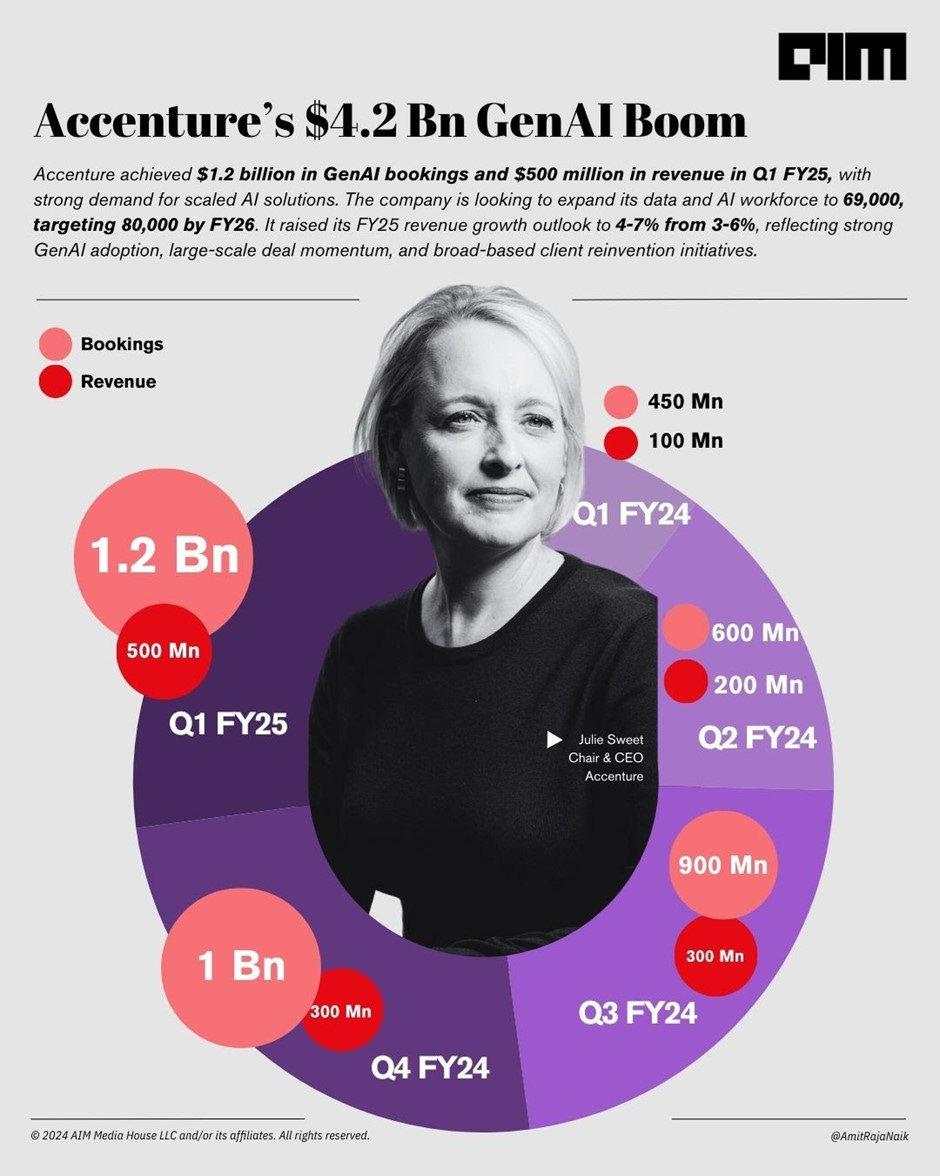

One key important statistic on the trends in demand driven by Gen AI. We had another milestone quarter in GenAI with $1.2bn in bookings and approximately $500mn in revenue. This compares with bookings of $400mn in bookings and $ 100mn in revenue a year earlier.

Picture from Aim Media House featuring Accenture CEO Julie Sweet and illustrating growth in GenAI bookings and Revenues.

Highlights from the Earnings Conference Call

Revenues grew 9% in local currency above the top end of our guided range with six of our 13 industries growing double digits, and we continue to take market share.

EPS grew 10% over Q1 adjusted FY24 EPS ($3.6 vs $3.1)

Operating margin was 16.7% for the quarter, consistent with adjusted Q1 results last year and includes significant investments in our people in our business.

While we continue to invest in our business and our people with $242mn deployed primarily across five acquisitions and with approximately 14mn training hours this quarter designed to help us bring the latest in solutions and technology to our clients, provide our people with marketable skills, and reinvent our services using GenAI.

Finally, we delivered free cash flow of $870mn and returned $1.8bn to shareholders through repurchases and dividends.

The quarterly stock repurchase of $898mn was offset by new issuance of shares of $477mn.

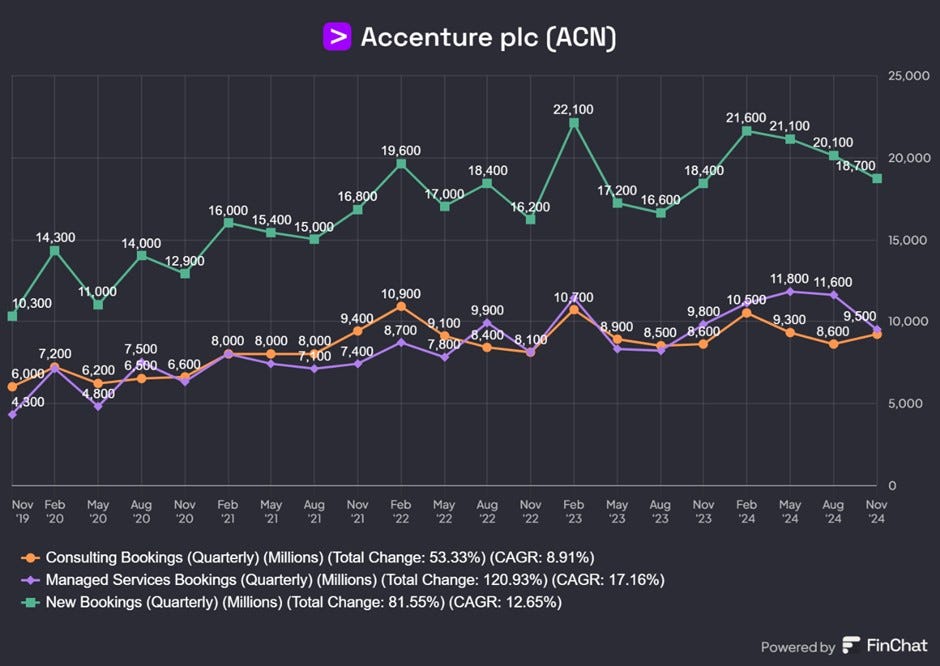

New bookings were $18.7bn for the quarter representing 1% growth in both U.S. Dollars and local currency with an overall book-to-bill of 1.1.

Consulting bookings were $9.2bn with a book-to-bill of 1.0.

Managed services bookings were $9.5bn with a book-to-bill of 1.1.

Our clients are focused on reinvention, which means large-scale transformations.

We do not currently see an improvement in overall spending by our clients, particularly on smaller deals.

When those market conditions improve, we will be well-positioned to capitalize on them, as we continue to meet the demand for the critical programs our clients are prioritizing.

As expected, building the strong digital core required for reinvention was a strong driver of our growth this quarter.

Gen AI continues to be a catalyst for reinvention across the enterprise and building out the data foundation necessary to capitalize on AI, as an increasing part of that growth.

We are helping our clients build their digital core, including in the cloud, which saw double-digit growth this quarter.

Our managed services will modernise the IT platform and migrate applications to the cloud, enhancing resiliency, stability, and service quality.

We will also consolidate (clients’) data and build an integrated cloud platform for advanced analytics and AI, strengthening their digital core.

GenAI will be applied to increase internal IT efficiency and reduce customer response time on digital interaction channels.

We will expand (clients’) digital offerings, employee onboarding, and payments using our suite of shared finance services solutions.

Security is an absolutely essential component of every company's digital core, and we again saw very strong double-digit growth. We are the partner-of-choice in part because we bring both the understanding of cross industry threats and industry specific threats with our deep experience across 13 industry groups.

Industry X grew double digits this quarter. Industry X is one of their strategic initiatives along with Cloud and SONG. In Industry X, they combine industrial and manufacturing expertise with digital know-how. A concrete example of Industry X efforts was given where they worked for a global tyre company.

We are continuing to evolve our long-time partnership with a global leader in tyre manufacturing to revolutionize the way factories operate and to reduce time-to-market for new products, accelerating innovation.

We will build a hybrid data foundation in the cloud, integrating millions of data points. We will also implement advanced analytics, AI, and digital twin technologies to optimize operations processes such as quality checks.

What will be the benefits for the tyre company?

This will enable the company to trace the root cause of a failed batch of tires back to a machine or process in minutes instead of days.

And predictive maintenance will pinpoint what parts of their process or machinery may be impacting quality and productivity, preventing costly down times.

Engineering teams will benefit from machine learning and simulation tools to generate and optimize the design of new products.

We will also implement new ways of working to attract tech-savvy talent and cultivate a learning culture where employees in over 100 factories are upskilled on the AI powered tools.

SONG is another strategic initiative for ACN. Through SONG, ACN seeks to help its clients to create compelling customer experiences. A concrete example of SONG Industry X efforts was given in their work with Spotify Technology.

We are reinventing all things customer through SONG, which grew high single digits this quarter. Song. We have the ability to integrate creative, data and AI, tech and strategy while leveraging our industry and operations expertise to unlike marketing as a growth enabler for our clients while delivering efficiencies.

We are helping Spotify optimize its advertising business by finding opportunities to drive efficiency as it scales globally.

Our marketing operations managed services support their ad operations under a single roof, touching a significant amount of their ad revenue across 150 markets.

We've infused automation across their operational workflows to help significantly reduce the time and effort required to launch advertisers' campaigns, getting them to market more quickly to help ensure revenue realization and advertiser satisfaction.

We continue to expand beyond ad operations, actively launching new capabilities across analytics and insights, data integrity and enrichment, customer support, and more.

Our partnership helps Spotify to focus on its core competencies so it can achieve long-term relevance and growth in an increasingly competitive market.

ACN continued its strategy of small acquisitions.

This quarter, we acquired Camelot, an international SAP-focused management and technology consulting firm from Germany with specific strengths in supply chain, data and analytics and Joshua Tree Group in the U.S., a supply chain consulting firm specializing in distribution center performance.

Outlook for FY 2025

For the full FY 2025, we now expect our revenue growth to be in the range of 4% to 7%

We continue to expect to invest about $3 billion in acquisitions this fiscal year.

For operating margin, we continue to expect FY 2025, to be 15.6% to 15.8%, a 10 to 30 basis point expansion over adjusted FY 2024 results.

We now expect our full year diluted eps for fiscal 2025 to be in the range of $12.43 to $12.79 or 4% to 7% growth over adjusted fiscal 2024 results, reflecting the raise in our revenue outlook.

We did add about 24,000 people in the first quarter, which is really reflective of the momentum that we see in our business.

Current staff utilisation is high so they need to hire more people to grow. They are seeing some growth (4%-7%) but the overall spending environment is little changed. They will get a key indicator in January and February when company’s will determine their 2025 budgets.

And what you see is the continued high utilisation rates at around 90%. Looking ahead, we'll continue to hire for the demand that we see and skills that we need.

it is a positive sign that we're hiring and some of it is coming from acquisitions, but we are seeing organic momentum in our business.

The overall spending environment is the same, that those who really want to go into -- in AI are more prioritizing spending as opposed to spending more… generally feels more like a prioritization within current budget. And so we'll see what happens in January and February.

The hiring that we saw this quarter, similar to last, was that it was concentrated in India.

a lot of our companies are global….they really are looking for optimization of right skills because a big piece of why people, for example, use India is about skills,- 10 years ago, it was about labour arbitrage… Today, it is about like the ability to get these skills at scale.

The Business Processing Outsourcing (BPO) market remains very competitive, no doubt due to companies in India, Philippines and South Africa etc.

BPO is a very competitive market, -we did see lower pricing across the business, which has been pretty consistent. clients have constrained spending, particularly on small deals and so you'd expect it to be constrained.

Summary

Accenture is a large company focused on providing management consulting, technology consulting and outsourcing. It has grown steadily over the years and has given creditable returns to investors over two decades

The company has a long track record of making operating profits and generating operating cash flow and free cash flow. Though profitability has fallen in recent years, ROE is still at a creditable 25%

The company has low capex needs.

The size of ACN means significant growth is difficult to achieve and revenues growth is unlikely to exceed 7% to 9% per annum.

The business model does not demonstrated operating leverage, and therefore it is difficult for Net Profit growth and EPS to grow much faster than Revenue.

The company utilises a lot of its Free Cash Flow for repurchases of stock. However, the benefits of this for investors are significantly offset by level of new stock issuance due to stock-based compensation.

The company’s strategy requires the acquisition of small niche companies and funding these requires a significant cash outflow which constrains the company’s ability to build significant cash reserves.

Valuation

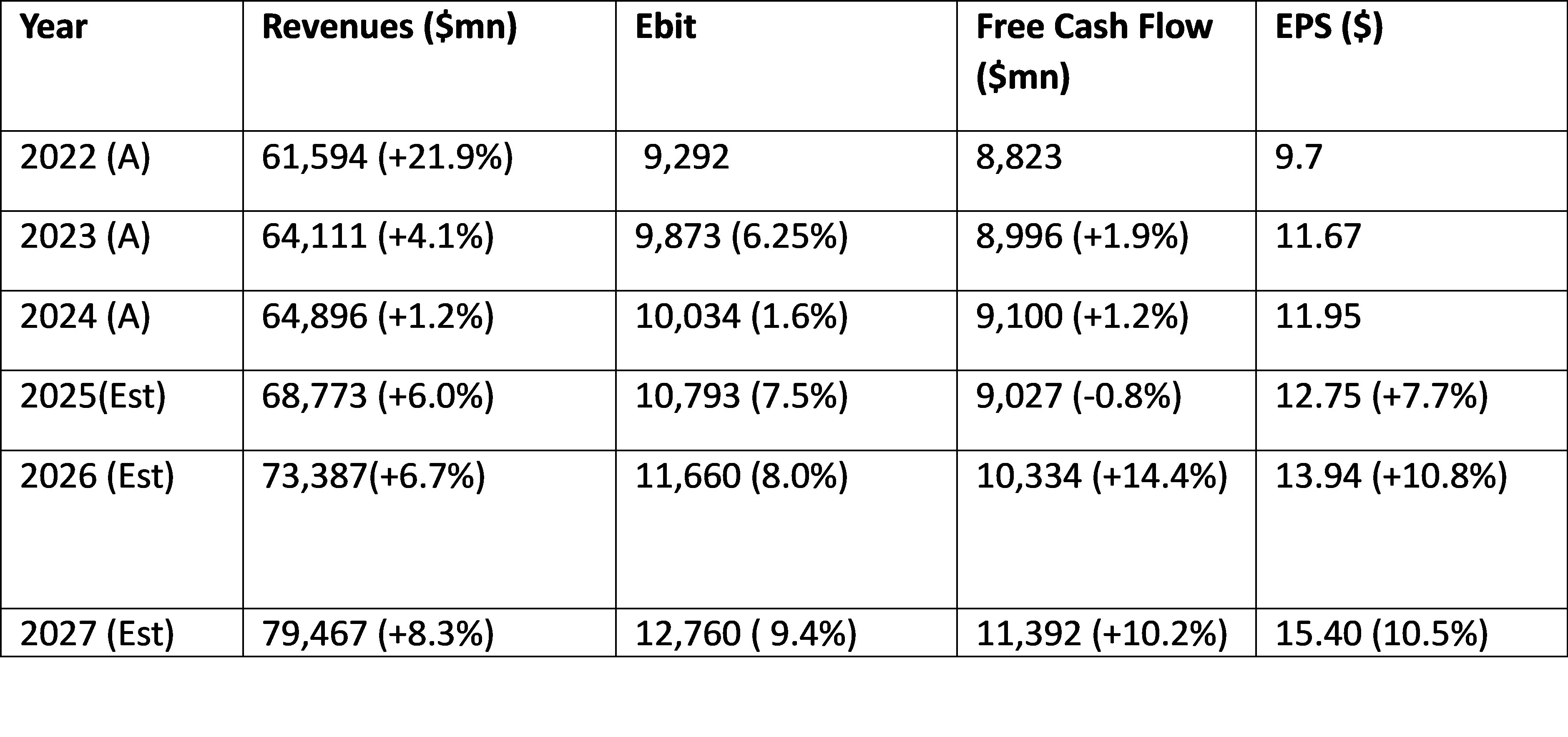

The consensus analysts’ forecasts for Revenues, Free Cash Flow and EPS are as follows:

The analysts’ consensus estimates show that revenue growth will return but only at rate of 6%-8 % per annum. This will translate to annual EPS growth in the range 8% to 11%. In addition, operating margins are expected to be maintained at 15-16%.

At the current price of $360 the ACN stock is trading at a two-year forward P/E Ratio of 25.8X.

At a current market capitalization of $243bn, the two- year forward Price to Free Cash Flow ratio is 23.2X.

These numbers imply a two-year forward Earnings Yield of about 3.8% and a two-year Free Cash Flow Yield of 4.3.%.

These valuations suggest a fair valuation given likely earnings growth of 10% and ROE of about 25%. It is hard to argue the stock is cheap, though that is a big ask in current market conditions.

We conducted a Discounted Cash Flow (DCF) Calculation.

For the DCF calculation, we had to make some additional Revenue growth and Net income Margin in FY 28 and 29.

We assume Revenue growth in FY 2028 and FY 2029 at 9% and Net Margins of 12.1%

We also assume a risk-free rate of 4.4% and a Market Risk premium of 4.5%. The Stock Beta is 1.2. These numbers result in a Weighted Average Cost of Capital (WACC) of 9.8%.

Finally, we assume that in FY 2029, the terminal exit multiple for P/E at the end of FY 29 is 27.5X.

With these assumptions, we calculated a theoretical ACN stock value of $354 -about the current share price

If the terminal exit P/E is (reluctantly) increased to a much more aggressive 32X, we get a theoretical value of $402 which is the 12% above the current share price.

These terminal exit P/E multiples of between 27.5X and 32X look a little high considering the modest growth prospects for the company and the current profitability.

As we have noted before, the problem with all such valuation models is they are highly dependent on the inputs. If one makes small changes in the assumptions, there can be a wide range in the outputs. Therefore, all valuation estimates must be taken with a lot of salt.

It is however difficult to say the stock is valued at an attractive level. Our best guestimate is that shareholders are likely to make 12% to 15% a year

Conclusions

ACN is long established large company

However, its size and the lack of operating leverage in its business model, means that Revenues, Profits and EPS are unlikely to grow much faster than 10% per annum.

ACN business model also requires a significant and consistent outlay of cash

The company is well known and it valuation reflects its likely prospects.

ACN might prove to be a good defensive investment but we will not allocate capital to it in our portfolio

We will not commit capital to ACN as we believe stock currently in out portfolio offer better prospects.

Annexe 1. Implications for Infosys (INFY).

We have written about Infosys (INFY) in the past as noted at the beginning of this article. The most comprehensive note on Infosys can be found here.

Infosys is an Indian ITES (Information Technology Enabled Services) company and trades on the Nasdaq as an ADR with the ticker INFY. The two largest ITES companies in India are TCS and Infosys. The third and fourth ranking companies are HCL Technologies and Wipro. The latter also has an ADR listed in the USA which trades under the ticker WIT. Much of what we say about Infosys will also apply to TCS, HCL and Wipro.

These companies were engaged in global labour arbitrage. India has a huge supply of software workers, and the companies grew by employing software engineers to provide IT services for global clients in the B2B space. They maintained legacy mainframe systems, wrote software code, helped companies transform and monitor IT systems. They got a significant boost due to Y2K issues in the late 1990s when companies had to overhaul IT systems to deal with the Millennium Bug. The large banks who have been among the larger spenders on IT in the last three decades have been important customers for the Indian ITES companies.

For decades, the ITES have earned 70% of their revenues from US companies and institutions, with the balance coming from the rest of the world. Indian customers account for a negligible share.

The ITES companies grew very strongly in the last three decades. They had high sales growth, and high margins and generated huge free cash flows. They gave excellent returns for shareholders over the decades. In the last 30 years they have given CAR return of 30% in INR terms and ~27% in US$ terms.

They have become major recruiters of students in STEM subjects in India and have had to pay well as they battled high levels of attrition. The ITES sector employs 4mn young professionals and has created huge wealth through high salaries and share price appreciation.

The success of these companies was widely applauded. They were seen a symbol of the new capitalist India and India’s first globally competitive industry.

Their success encouraged large global companies such as Accenture (ACN), IBM, Cognizant (CTSH) and many others to establish large operations in India. IBM and ACN employ about 300,000 people each in India. CTSH has 200,000.

INFY has recognised the vast change in the technology landscape and have changed their self-description. They describe INFY as “a global leader in next generation digital services and consulting. They claim they enable clients in more than 56 countries to navigate their digital transformation powered by AI and cloud.”

INFY was established in 1981 from a capital of $250 and has grown to market capitalisation of $ 94bn. It has 317k employees and has over 1882 clients. 300k were professionals involved in service delivery to clients, including trainees. In the 2024 Annual Report, they noted that 250,000 + employees are AI aware.

Differences between Accenture and Infosys.

Accenture is much larger than Infosys.

ACN Market cap of $243bn vs $ 94bn for Infosys (2.6x)

Annual sales run rate of $ 68bn for ACN vs $18.5bn for Infosys. (3.8x)

Infosys is more focused on outsourced technology operations and has a very smaller consulting business. For ACN, as we noted above the split is closer to 50/50.

Historically, ACN had more extensive and deeper client relationships than Infosys. ACN would have much greater contact with CEOs and the board while Infosys’s engagement with clients usually peaked with senior management and the CTO /CIO. In the last two to three decades, Infosys has built a global network of global offices to make up some of the ground on ACN.

ACN has 799k employees of whom 400k are based in India. Infosys has 317k and more than 90% are likely to be based in India. This gives Infosys a cost and margin advantage over ACN.

Infosys earns in USD, Euro, GBP and other “hard” currencies while most its costs are in Indian rupees. This too gives them a general advantage as the latter tends to depreciate against the former, on average by a rate of 3% per annum.

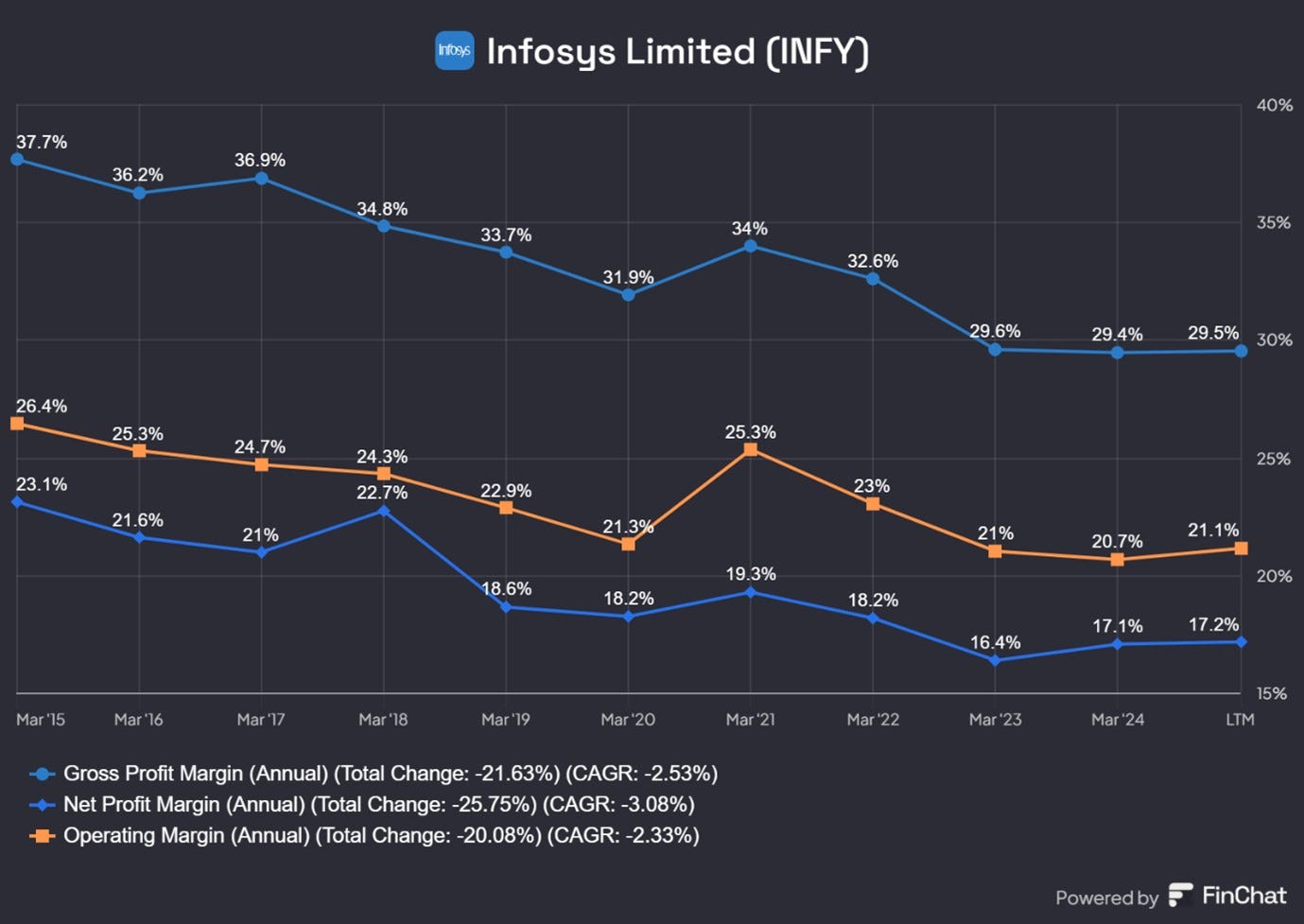

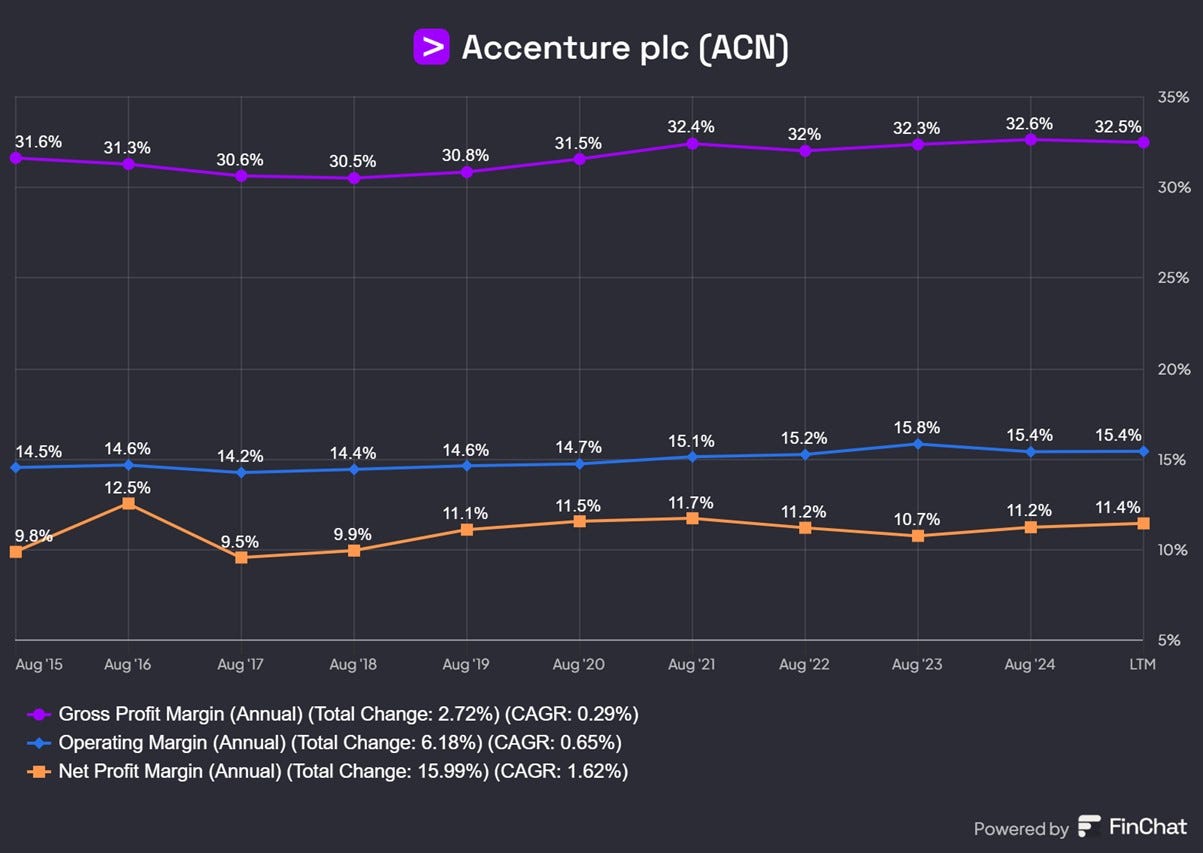

Accenture Gross Margins are 3% points higher (32.5% vs 29.5%) as it commands a “premium” price.

However Accenture Operating Margins at 15.4% vs 21.1% for Infosys (a 570 bp difference).

Accenture Net Profit Margins at 11.4% are lower than Infosys’s 17.2% (a 580bp difference) .

Infosys’s cost advantage is decisive in delivering higher operating and net profit margins. ACN also benefits from the lower costs in India as 50% of its employees are based there. In fact, in absolute terms, ACN has more employees in India than Infosys. In the earnings conference call, ACN management suggested that most of the incremental recruitment is happening there and therefore ACN will benefit from lower India costs going forward.

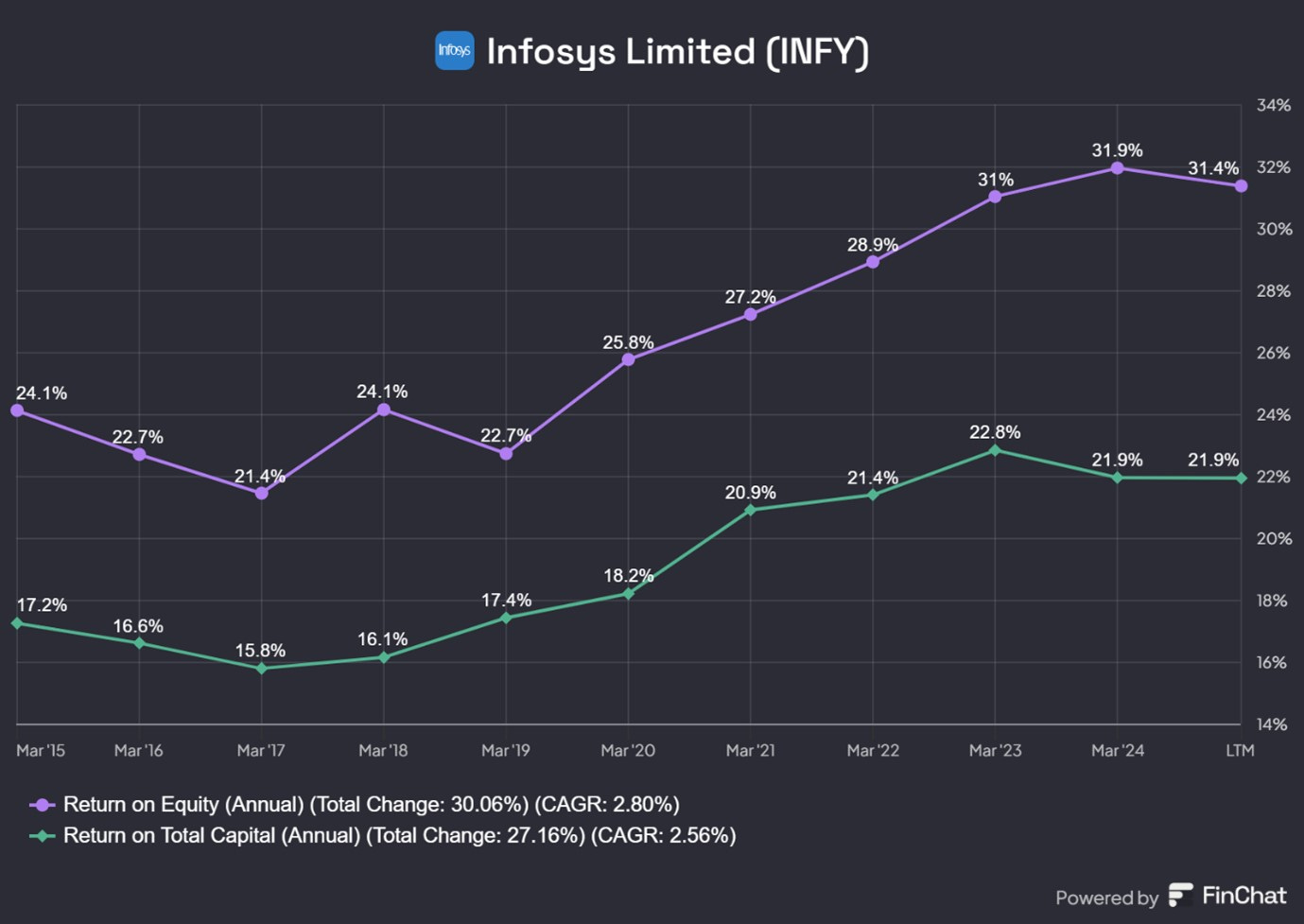

Infosys also wins on profitability as we can see in the charts below.

Infosys’s ROE is 31.4% compared with 26.3% for Accenture despite having lower elves of leverage (a difference of 510bps)

Infosys Return on Total Capital (ROTC) is 21.9% vs 18.6% (a difference of 340bps)

There are two other differences we would like to highlight.

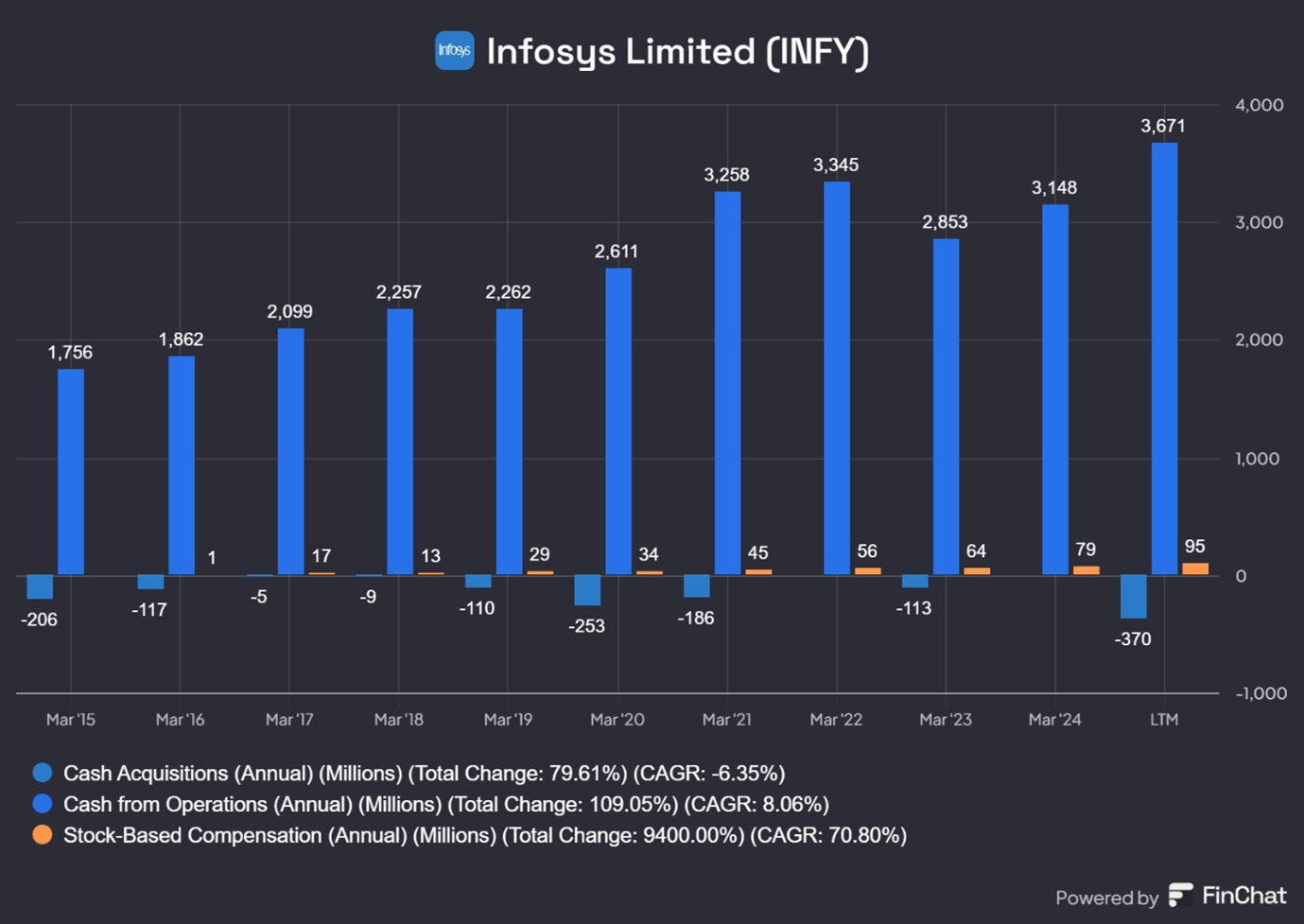

Infosys growth strategy is based on organic growth and both cash spent on acquisitions and SBC is a negligible percentage of operating cashflows. In contrast, for ACN, the two items are a significant part (75%) of the operating cash flow. This means that Infosys has a much greater capacity to generate cash and incurs significantly less dilution due to stock-based compensation.

Stock-Based Compensation (SBC)

Infosys SBC was zero until 2016 and was just $79mn in FY 2024. For ACN, SBC was nearly US$2bn in FY 2024. These differences are huge given the companies are in the same sector and deserve some comment.

Infosys’s business model, strategy and operations do not need SBC. ACN cannot operate without SBC.

This difference reflects cultural factors. Virtually all of the senior management of INFY are of Indian origin and India-based. They seem loyal and willing to work without significant SBC. On the other hand, most of ACN ‘s senior management is in the US where (high) SBC is part of the remuneration practice and ACN(presumably) believes that SBC has to be at current levels to attract and retain senior staff.

ACN has 50% of its workers in India and presumably, a relatively high percentage of senior management are of Indian-origin. Given this, it is difficult not to believe the level of SBC at ACN is too high and that it can and should be lower.

Acquisitions

ACN strategy relies on a large number of acquisitions. These are usually tech start-ups who have developed some innovative products or service. We do not have any evidence they overpay for acquisitions but extensive academic evidence indicates that companies generally overpay for acquisitions.

Infosys growth strategy is organic. They build capabilities in-house by hiring students and training them. They have made a few acquisitions over the decades, namely small consulting firms outside India (mainly in US) which had good end-client relationships, but the scale of this has been negligible.

It is likely Infosys develops technological capacities at a much lower cost than ACN and this difference is likely to continue.

In the last 24 odd years, Infosys has given INR-denominated total return CAGR of about 24%. In US $ terms this fall to about 21%.

On the other hand, over the same period ACN has given a return of 16.2%.

Over 24 years, ACN underperformed by about 480 bps per annum and INFY shares have grown 2.5X more than ACN.

INFY has a better, more profitable business than ACN. Competitive pressures will likely force ACN to be more than INFY than the other way round, though it may take an activist investor to accelerate the change.

ACN and INFY trade at similar valuations right now. 1-year forward P/E of about 27X for both. INFY dividend yield is 2.74% compared with 1.76% for ACN.

Infosys looks a significantly better investment than ACN.

Comments in the ACN conference call which gives some insights for Infosys

ACN noted that they are seeing strong demand for AI work. They are responding to this by recruiting heavily, almost exclusively in India.

Looking ahead, we'll continue to hire for the demand that we see and the skills that we need. The hiring that we saw this quarter, similar to last was that it was concentrated in India.

A lot of our companies are global…they really are looking for optimization of right skills because a big piece of why people, for example, use India is about skills - 10 years ago, it was about labour arbitrage, right? Today, it is about like the ability to get these skills at scale.”

This is positive for Infosys and other Indian ITES companies. In the 2024 Annual Report, they noted that 250,000 + employees are AI aware as a result of training that has been given to them. Therefore, they will be in a good position to meet the increased demand for AI-related work and hire new people in India.

We looked at the Infosys ADR valuation in a previous note which can be found here. The broad numbers have not changed since then.

28/12/2024