Advanced Micro Devices (AMD)

Ready for the AI Opportunity?

Advanced Micro Devices (AMD) was founded in 1969 and went public in 1972. It supplies products such as microprocessors, chipsets, Graphics, Video and Multimedia products. These are manufactured by 3rd party foundries. AMD got out of manufacturing after it spun out its own operations, now called GlobalFoundries.

In 1982 AMD inked a deal with Intel that let AMD make exact copies of Intel's x86 microprocessors, used in IBM compatible PCs. The OEM PC manufacturers did not want Intel to be the sole supplier as the IBM-clone PC market started a three-decade long phase of high growth. The era made fortunes for the “Wintel” combination- Microsoft Windows Operating System and Intel chips.

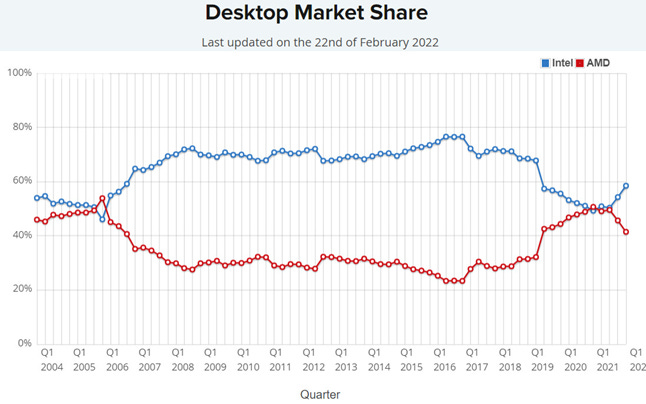

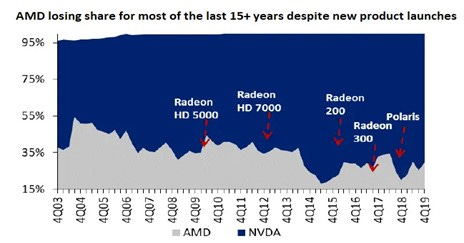

By the mid-1980s, AMD was developing its own chips. For nearly three decades it was seen as a poor also-ran behind Intel as a supplier of Core Processing Units (CPUs) where market share fell to almost 20% in 2016 while Intel’s was almost 80%.

In 2005, Intel was distracted by mobile and AMD captured market share but lost it over the next 8 years. AMD was constrained by losses and financial leverage. Their execution was crippled by gross mismanagement.

AMD’s fortunes started turning around after Dr Lisa Tsu was appointed CEO in 2015. The company has gained desktop market share rapidly since then (see chart above). The company almost failed in 2015 and many analysts expected to be out of business by 2020.

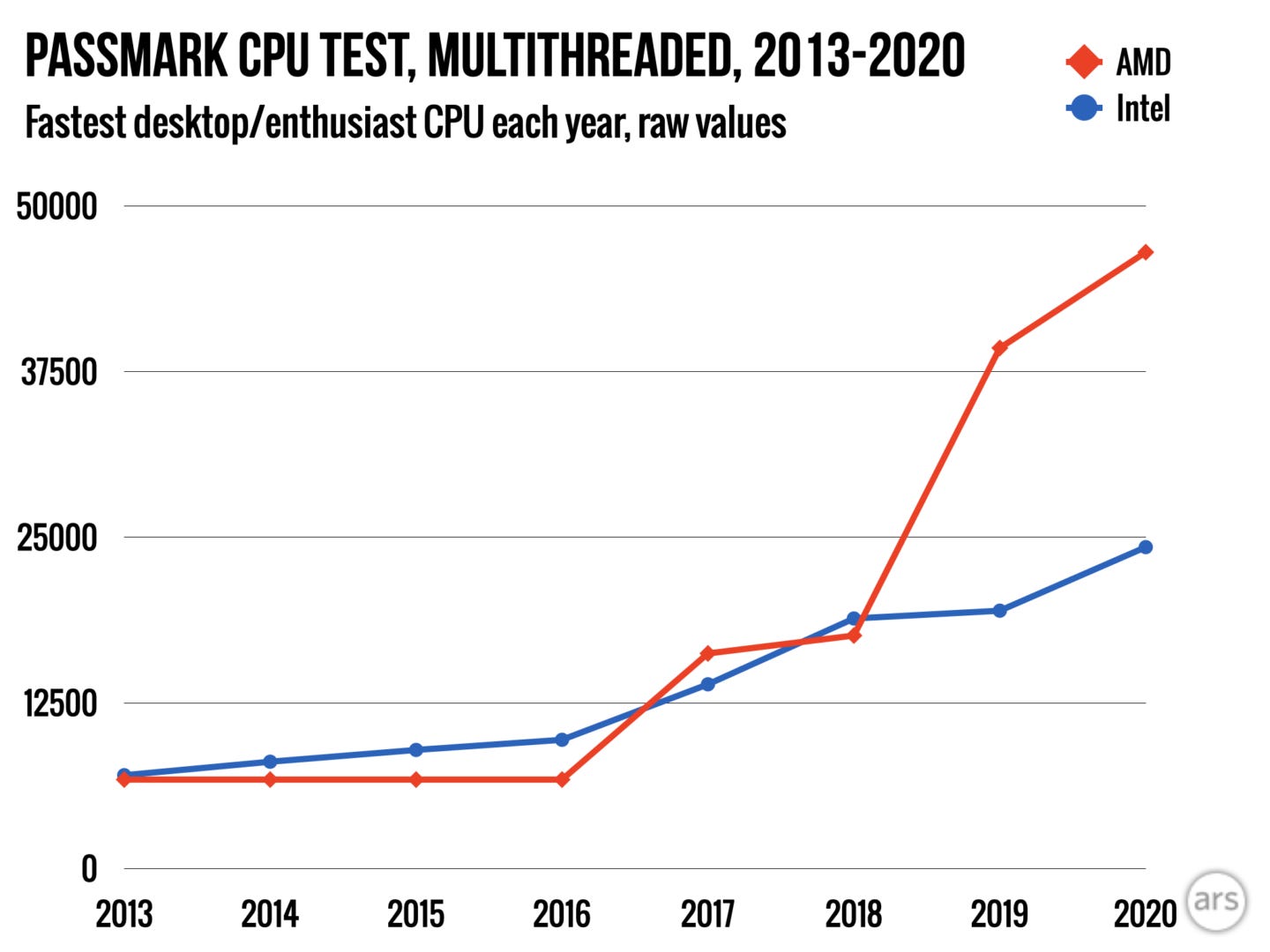

In 2018, AMD released the Zen chip microarchitecture and hardware. It is now in its fifth iteration, Zen 5, and support the new Ryzen CPUs . Ryzen hardware has been a great success, significantly bolstering performance per dollar. It offered consumers a series of budget offerings that were not previously available from other companies.

At the same time Intel stumbled and failed to produce 10nm chips on time in 2015. You can read about the history of the AMD Intel rivalry here and one aspect of this is illustrated below.

The combination of Intel’s complacency, AMD’s technical prowess, AMD made progress and the gap with Intel in CPUs was closed.

- YouTube")

AMD re-entered the market for datacentres in 2017, delivering impressive performance per US$ improvements in Server Chips on successive Zen architectures under the EPYC brand. Successive chips were named after Italian cities- e.g. Naples, Rome, Milan, Genoa – expanding their footprint with each generation.

AMD has gained “low-teens” percentage share of server chip system shipments vs. single digits pre-COVID. These gains would have been even more impressive if AMD chips had not been limited by manufacturing supply constraints. Intel remains the leader in Server CPUs but AMD has gained a foothold in this market. Nvidia is the dominant player in the Server GPU market and AMD currently has a negligible presence.

AMD was, for many years, a poor number two in a consumer facing market. Since 2015. it has greatly improved its standing in the consumer space and gained such credibility with Enterprise customers that is invited to have long-term strategic conversations.

AMD used to report through two segments:

Computing and Graphics, and

Enterprise, Embedded and Semi-custom.

Computing and Graphics accounted for around 55% of sales. This segment includes include desktop and notebook processors and chipsets (CPUs), Graphics Processing Units (GPUs), and chip-related development services.

Enterprise, Embedded and Semi-custom segment account for about 44% of sales. This is a higher margin segment and AMD has grown this rapidly in recent years. It includes Server and Embedded processors, semi-customised System-on-Chip (SoC) products, development services and technology for game consoles.

Geographic Reach

The geographic breakdown of sales is as follows:

North America: 46%

EMEA: 30%

China: 18%

Other: 6%

Sales and Marketing

AMD markets its products through a direct sales force, as well as through a network of independent distributors and sales representatives.

Microprocessor customers consist primarily of

Original equipment manufacturers (OEMs) such as Lenovo, Dell, HPQ etc

Large public cloud service providers such Amazon, Microsoft and Google

Original design manufacturers (ODMs) such as Sony, Tesla, Apple and Samsung

System integrators and independent distributors such as Cap-Gemini or Arrow Electronics

The company is focused on R&D aiming to improve product performance and enhancing design. AMD’s main area of focus is on delivering the next generation of CPU and GPU IP, and designing that IP into its SoCs for its next generation of products, with, in each case, improved system performance and performance-per-watt characteristics.

In CPUs, Intel is the main competitor especially formidable still in Enterprise.

In GPUs Nvidia and Intel are the main competitors

Waves in the Computing Industry

I like to think of the industry as a series of new waves where new waves emerge, but old ones continue to progress. A stylised timeline of these is given below:

The market is currently excited about the prospect of demand from the large cloud hyperscalers (Amazon AWS, Microsoft Azure, Google Cloud Platform, Oracle, Alibaba, IBM, Meta etc) as they invest for the increased workload driven mainly by Artificial Intelligence (AI) and Machine Learning(ML). AI/ML workload requires replacing Server CPUs with GPUs. Nvidia, as the dominant player, is likely to capture the lion’s share of this demand but AMD should benefit as well.

AMD Product Portfolio

Ryzen - Desktop and Mobile Processors –CPUs- Company claims -world’s fastest gaming leadership performance and advanced battery life. The Chips are based on the Zen Architecture which was introduced in 2017.

Radeon - Family of GPUs for PCs, game Consoles, IoT etc

EPYC - x86-64 microprocessors specifically targeted at the Server and Embedded system markets- Company claims they offer performance and TCO advantages. Chips released under this architecture are names after Italian cities – Milan, Genoa etc.

Instinct - High performance GPUs for Datacentres. AMD claims it offers large- scale use Computing for the exascale (super high performance server-farm computing) era. Instinct chips are driven by AMD CDNA architecture .

AMD CDNA- CDNA stands for Compute DNA for the Datacentre. It is designed to deliver ground-breaking acceleration to fuel the convergence of HPC and AI in the era of Exascale. AMD hopes this combined with a new generation of GPU chips such as the Instinct MI100, MI250, MI300 will help them fight with Nvidia in Datacentre.

AMD describes the Instinct MI100 as follows: “AMD Instinct™ MI100 accelerator is the world’s fastest HPC GPU, engineered from the ground up for the new era of computing. Powered by the AMD CDNA architecture, the MI100 accelerators deliver a giant leap in compute and interconnect performance, offering a nearly 3.5x the boost for HPC (FP32 matrix) and a nearly 7x boost for AI (FP16) throughput compared to prior generation AMD accelerators.”

The latest iteration of this line is the MI300. It is the first datacentre chip that comprises a CPU, GPU, and Memory into a single design, delivering 8x more performance and 5x better efficiency for HPC and AI workloads compared to AMD’s MI250 accelerator currently powering the world's fastest supercomputer. MI300 chip is due to be launched in the second half of 2023. If it can get traction with Datacentre/HPC buyers, it will give a significant boost to AMD and help support the current valuation

In recent years, all customers have been demanding higher performance which means more expensive chips and higher margins. The average selling price (ASP) of CPUs and GPUs aimed at consumer have increased by 50%.

One driver is Gaming. Many games now have the ability to be played at super-high frame rates with high fidelity. That gives the broad customer base a good reason to upgrade to the higher-performance products.

Beyond gaming, another driver of demand come from creators and broadcasters. People in Engineering, doing CAD or graphics, editing, movie production, etc or other producers of content. This base has grown rapidly in recent years and they need high performance chips to save time.

In addition, in the Enterprise space, Datacentre has boomed driven by the migration of data and work to Cloud. This is now being boosted by the growth of AI workloads. Datacentre will continue to be a significant driver of demand for high performance and high value chips.

In 2017, AMD had to ask itself the question “Would I make a chip for USD 300 for a notebook or desktop, or would I make a chip for USD 4,000- 6,000 for a server? They decided to move up the value chain and gradually changed their production mix.

Recent Acquisitions

In late 2020, AMD acquired Xilinx via an all-stock transaction worth US$35 billion. This is one of the largest acquisitions in tech. Xilinx develops flexible processing platforms that enable rapid innovation across a variety of technologies - from the Cloud to Edge Computing. Xilinx's main customers are electronic equipment manufacturers in a variety of industries, including:

Aerospace and defense: Xilinx's products are used in a wide range of military applications, including radar, communications, and weapons systems such as Boeing, Lockheed Martin, Raytheon

Automotive: Xilinx's products are used in a variety of automotive applications, including infotainment systems, driver assistance systems, and powertrain control. Customers include Audi, BMW, Daimler.

Data center: Xilinx's products are used in a variety of data center applications, including cloud computing, machine learning, and artificial intelligence. the Cloud hyperscalers are the main customers.

Industrial: Xilinx's products are used in a variety of industrial applications, including factory automation, medical devices, and test and measurement equipment. ABB, Emerson Electric, Siemens

Consumer: Xilinx's products are used in a variety of consumer applications, including networking equipment, gaming consoles, and smart TVs. Cisco, Sony, Samsung are among the customers.

In addition, Xilinx also has customers in a variety of other industries, including telecommunications, networking, and medical devices. So Xilinx has further helped AMD to diversify away from consumers and toward Enterprise.

In May 2022, the Company completed the acquisition of Pensando Systems, Inc. a leader in next-generation distributed computing, for a total purchase consideration of US$1.7 billion. The small acquisition expands the Company’s ability to offer leadership solutions for Cloud, Enterprise, and Edge Computing customers. AMD is able to offer high-performance data processing units (DPUs) to Enterprises.

It may be useful to state AMD’s stated aims here as a summary of its current strategy

The company’s aims are as follows:

We invest in high-performance CPUs for cloud infrastructure, enterprise, edge, supercomputing, and PCs.

We invest in high-performance GPUs and software for markets such as gaming, compute, AI, and virtual reality (VR) and augmented reality (AR).

With the acquisition of Xilinx, Inc. (Xilinx) in February 2022, our product portfolio now includes FPGAs and Adaptive SoCs used in the data center and embedded markets.

With the acquisition of Pensando Systems, Inc. in May 2022, we offer high-performance DPUs and next generation data center solutions.

New Financial Reporting Segments

Starting with second quarter 2022 results, AMD changed its financial reporting segments to align better with its strategic end markets: the segments are now

Datacentre: Including server CPUs, datacentre GPUs, and the portions of Xilinx revenue related to the datacentre business

Embedded: Including the Xilinx embedded business plus the AMD embedded business

Client: Including the traditional desktop and notebook PC business

Gaming: Including the discrete graphics gaming business and the semi-custom game console business.

Total Addressable Market (TAM):

We always have to be sceptical when companies give estimates of their TAM as they have every incentive to overstate it both in absolute terms and relative to their current turnover.

In 2020, AMD estimated their TAM was approximately US$79Bn. They also estimated the 2025 TAM. AMD claims the acquisition of Xilinx is opening up new opportunities and AMD is now looking at a ~US$300Bn TAM in 2025. The increase is driven by expansion in traditional PC, datacentre, and gaming markets bolstered by new market opportunities in communications, automotive and embedded.

Gaming and PCs: AMD see this as a US$ 37bn and US$ 50bn market opportunity respectively.

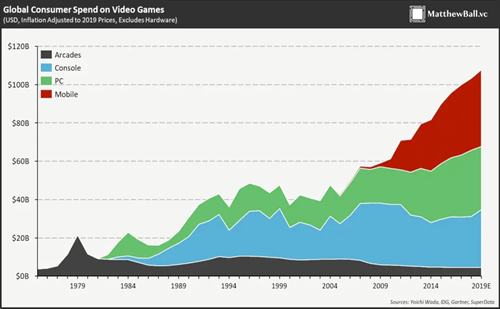

AMD will continue to benefit from the growth of gaming which has grown strongly in recent years as seen below .

Source: Matthew Ball

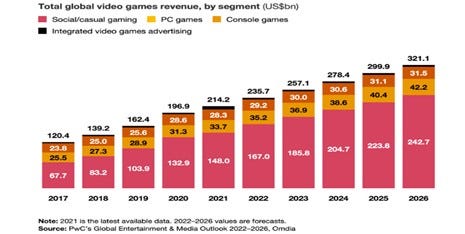

Globally, global gaming industry revenues are anticipated to surpass $320B, growing at a 8% CAGR in between the 2022 and 2026 forecast period:

Source: Total Global Video Game Revenue Projections - PwC

GPU performance is key for gaming. AMD has played number two to Nvidia in PC GPUs space despite new product launches.

Source: Punchcardinvestor.substack.com

AMD has a better share in console gaming. The Sony PlayStation® 5 and Microsoft® Xbox Series S™ and X™ game console feature AMD’s RDNA graphics architecture. PC Chips will continue to be large market. It is a mature market and showed huge increase in demand during the Covid-19 Pandemic which brought forward a lot of demand. Growth is likely to slow significantly and the estimate of a US$ 50bn TAM by 2025 looks optimistic but AMD could make good progress due to better relative (to Intel) technical performance.

Datacentre: AMD estimates the Datacentre TAM at US$ 125bn

Modern data centers require high-performance, energy-efficient, scalable and adaptable compute engines to meet the demand driven by the growing amount of data that needs to be stored, accessed, analyzed and managed. Different combinations of CPUs, GPUs, DPUs, FPGAs, and Adaptive SoCs enable the optimization of performance and power for a diverse set of workloads

The growth in Datacentre is the largest and most important trend in technology in recent years. Growth has been seen Cloud, AI, HPC, Data Analytics and Video Streaming.

Cloud is the most important with applications and use-cases touching almost every company and industry. Gartner anticipates that Cloud expenditures are expected to reach nearly US$600B in 2023, a 50% increase from 2021. The so-called hyperscalers (AWS, Azure, and GCP) are still growing at 20% to 30% despite significant deceleration in growth rates compared to two or three years ago due to base effects.

AI is clearly the current buzzword and front of mind idea – it can reshape almost every industry and there are some high growth forecasts out there.

Can AMD compete? It is far behind Nvdia in technology aimed at deploying and training AI models. However the opportunity is large, Nvidia will not able to supply all demand and customers will support AMD as they do not wish to become solely dependent on a single supplier.

High Performance Computing (HPC) is a part of the Datacentre segment. HPC empowers engineers, data scientists, etc. to solve the largest and most complex problems in the shortest amount of time - maximizing resources at a greater rate than traditional computing. AMD currently powers the world’s most powerful supercomputers, with EPYC CPUs and AMD Instinct Accelerators are currently achieving number one spots in various independent tests. AMD should be able to capture significant value in this space going forward.

The Datacentre is a huge opportunity for the next decade and AMD should be able to grow strongly.

Embedded, Automotive, Communications. Nvidia estimates the TAM here is US$ 33bn for Embedded and Communications respectively and US$ 27bn for Autos.

The Embedded Segment primarily includes embedded CPUs, GPUs, APUs, FPGAs, and Adaptive SoC products. Embedded products address computing needs in automotive, industrial, test, measurement, emulation, medical, multimedia, aerospace, defense, communications, networking, security, and storage markets as well as thin clients, which are computers that serve as an access device to a network.

Embedded systems play a role everywhere from ensuring the general functionality of connected home appliances to powering interactive kiosks and medical devices. AMD Ryzen embedded processors will play a central role in industries ranging from Aerospace to Networking.

In Autos, the future car is/will be a “computer on wheels” with entertainment and connectivity are becoming important parts of the in-vehicle experience. In addition, there is a huge push to develop assisted driving followed by autonomous driving. Tesla’s Model S and Model X feature Ryzen Embedded APU and RDNA-2 GPUs, respectively. In communications, with the spread of 5G, AMD EPYC systems are becoming increasingly sought in the Communications sector.

Income Statement

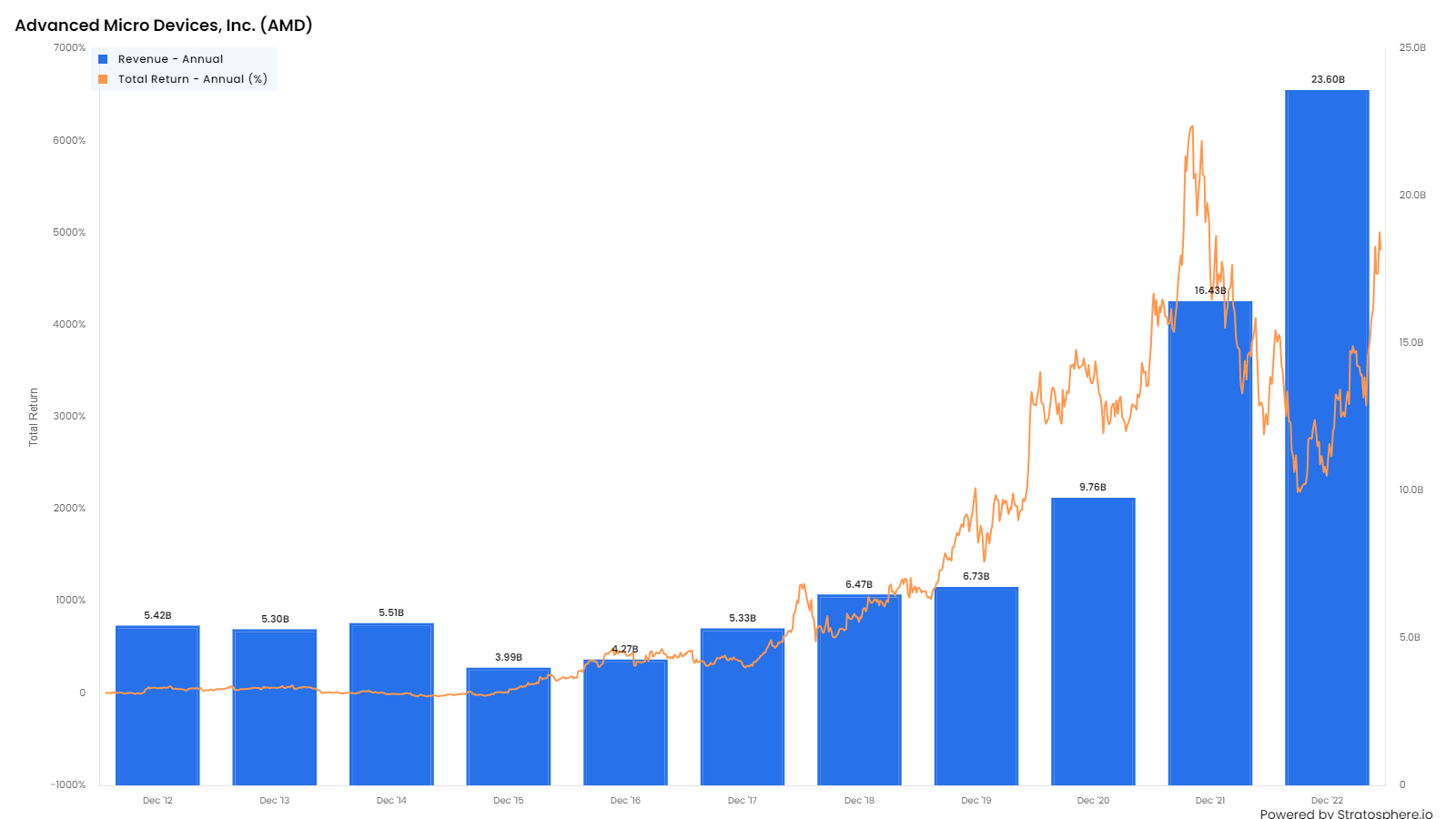

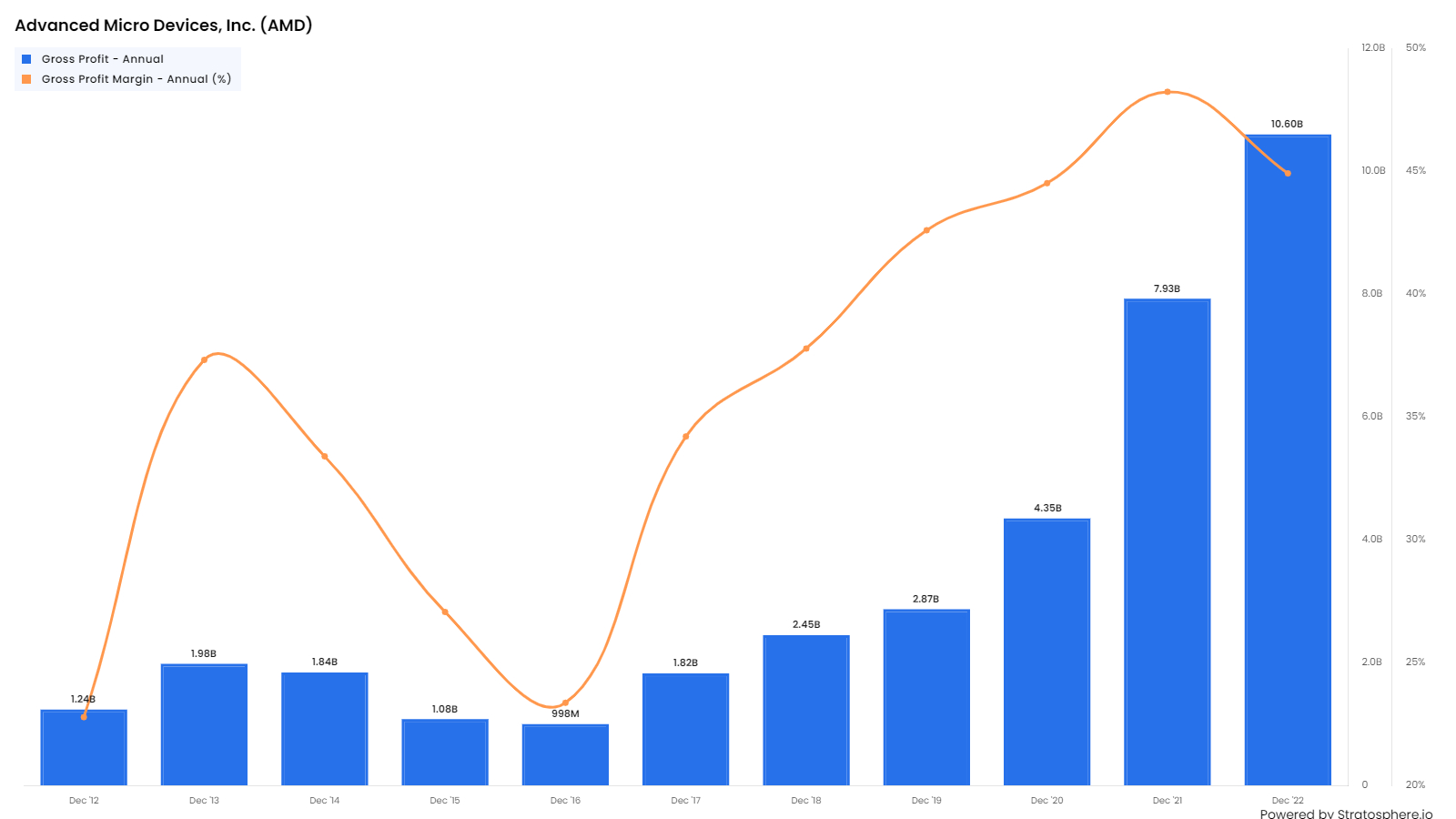

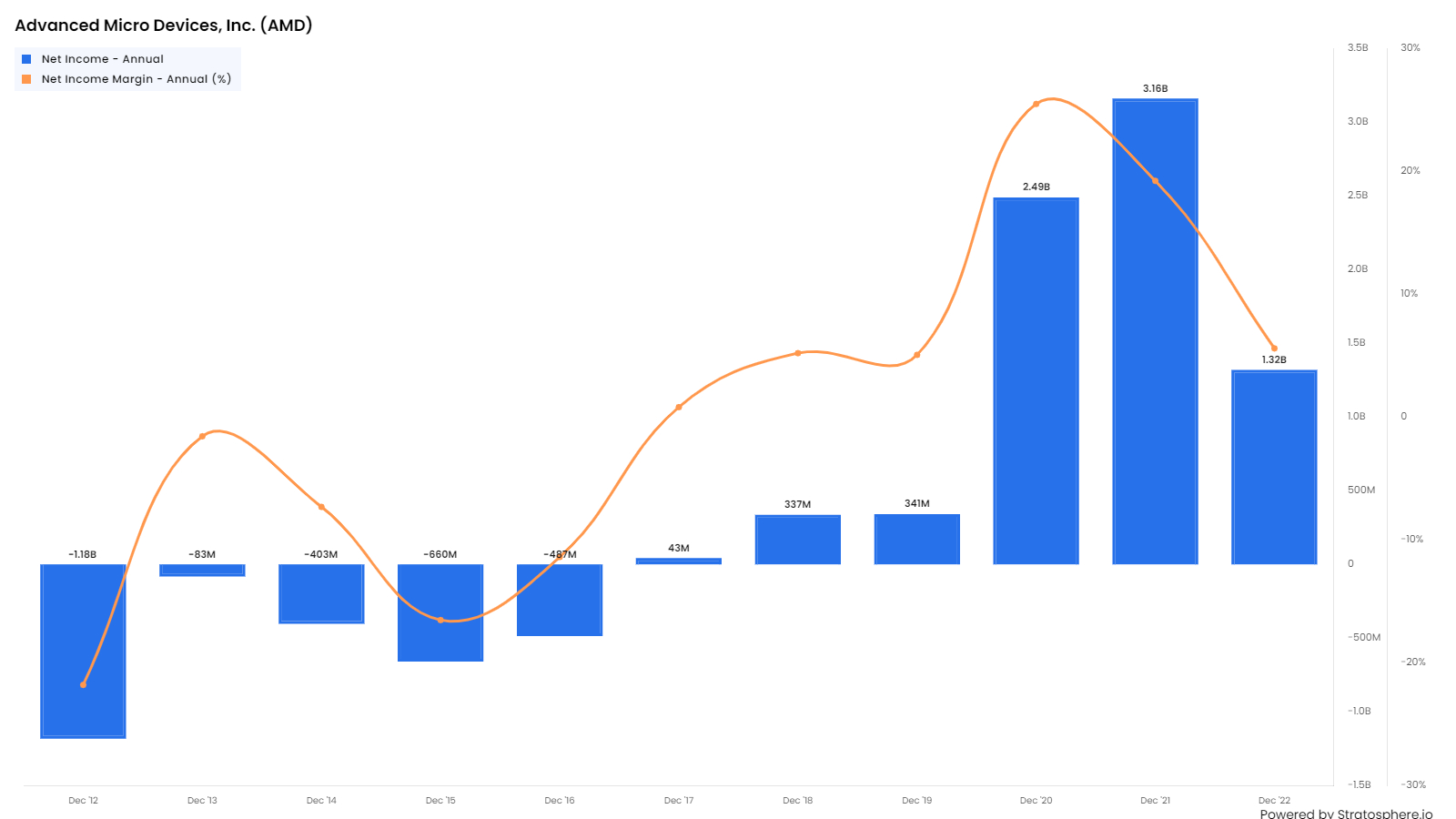

AMD’s total revenue has grown strongly: it has risen from US$ 4bn in 2015 to US$ 23bn in 2022. A 35% CAGR growth from 2017 to 2022, driven by acceleration across all business segments, with particularly noticeable growth in datacentre revenue. The stock has given a nearly 20X return in the last ten years.

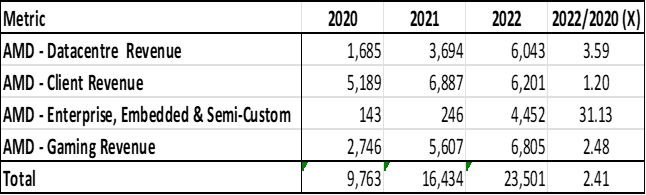

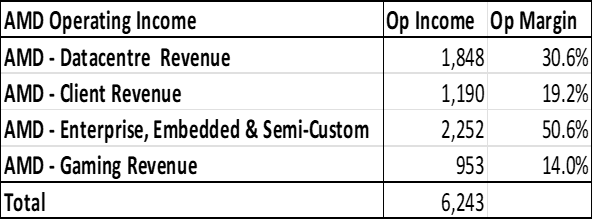

In 2022, the company changed the breakdown which shows breakdown into Data Center, Client, Gaming, Embedded and Other Business segments have been performing in recent years.

AMD Segment Revenues and Operating Income (US$ Million)

Datacentre revenue has grown from US$ 1.7bn in 2020 (17% of total revenue) to US$ 6.0bn in 2022 (25% of total revenue). In contrast, client revenue only grew marginally over this period. The growth in Embedded reflected the acquisition of Xilinx Inc. This increase in Datacentre Revenue was driven by strong EPYC CPU demand, from Cloud and Enterprise customers.

In 2022, Datacentre, Client and Gaming all recorded revenues of about US$ 6bn each. It is a different story when it come to Operating Income and Operating Margins as shown above. Datacentre and Embedded Operating Revenue and Operating Margin is much high than Client or Gaming.

So, if AMD continues to grow much faster in the first two segments it will have outsized effect on future profitability.

Financials

Income Statements

Cost of Revenues has risen but less than total revenue and so Gross Profit Margins have increased from about 25% in 2016 to 45% currently (See above).

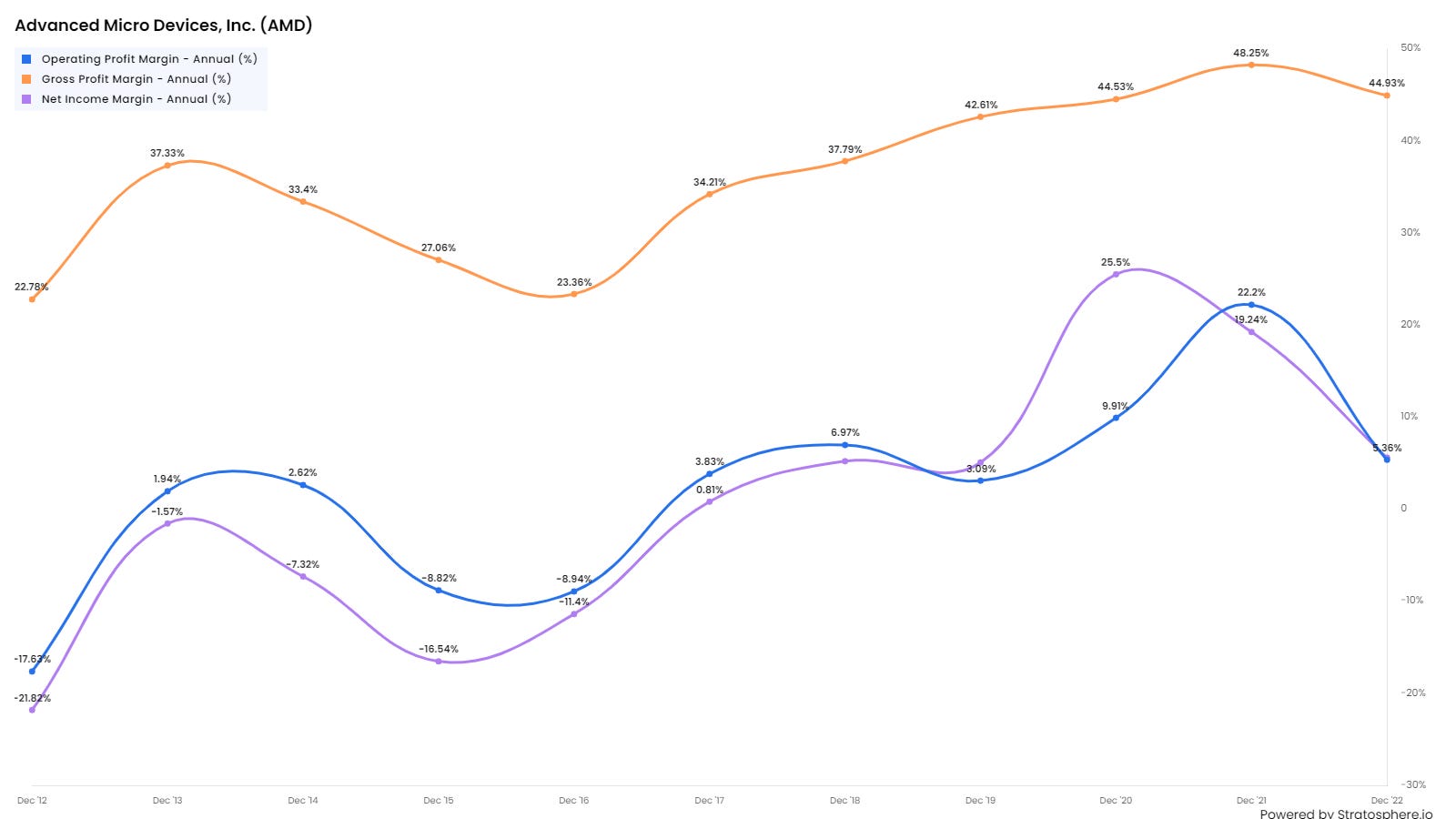

Profit and Margins have increased noticeably over the last few years expanding to 48% (at the Gross Margin level) in FY’22 in comparison to 23% in FY’16. Operating and Net Margins were at about 20% in 2021.

Higher margins reflects cost controls and business mix changes as datacentre and embedded business segments have become a larger part of AMD’s business - they account for more than 40% of Total Revenues currently and are likely to rise to 50% in the next few years.

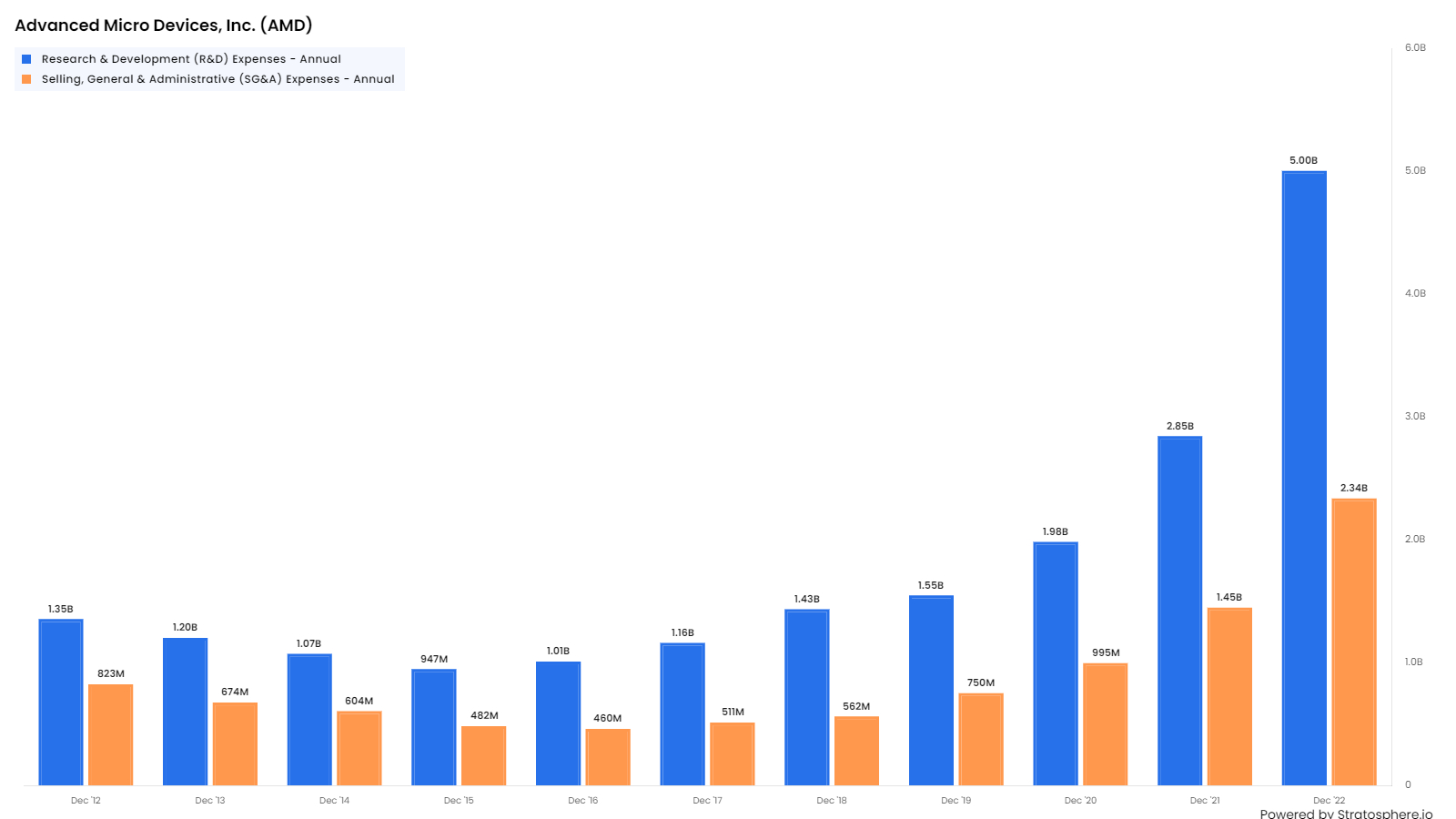

Operating Expenses

The largest two categories of operating expenses are Research and Development (R&D) and Selling, general & Administrative (SG&A) and this have grown about 5X between 2017 and 2022. Total revenues have risen more than this and therefore operating margins have improved.

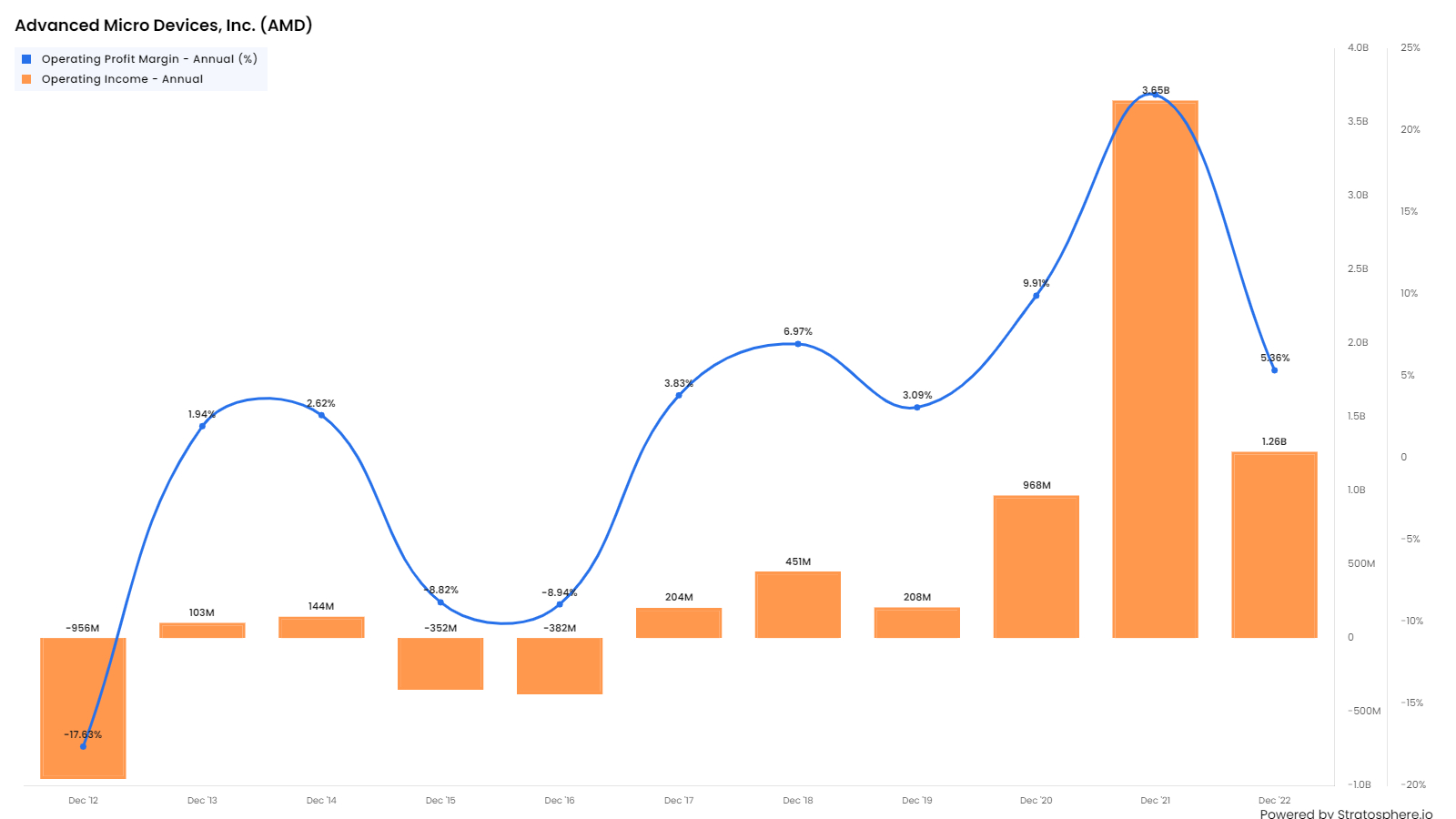

The fall in Operating profit in 2022 from US$ 3.6bn to US$ 1.2bn needs to be explained. According to the AMD 10-K, the company took two write-offs of USD 2.1bn and US$ 1.4bn. In the absence of this, 2022 Operating Profit would have been about US$ 4.7bn ( ~ 30% higher than in 2021).

The information we have suggest that the US2.1bnbn write-off related to inventory of semi-custom chips used in gaming consoles and other devices. In addition, there was US$ 1.4bn write off which many have been a general impairment charge against the intangible assets been built up after the acquisition of Xilinx.

The write-offs had a significant impact on AMD's financial results for 2022. Both Operating and Net profit fell and there was a decline in Operating Profit Margins, Net Profit Margins and ROE. However, as these write downs are non-cash items, they had no impact on the Operating Cash flow or the Free Cash Flow.

Margins and Profitability

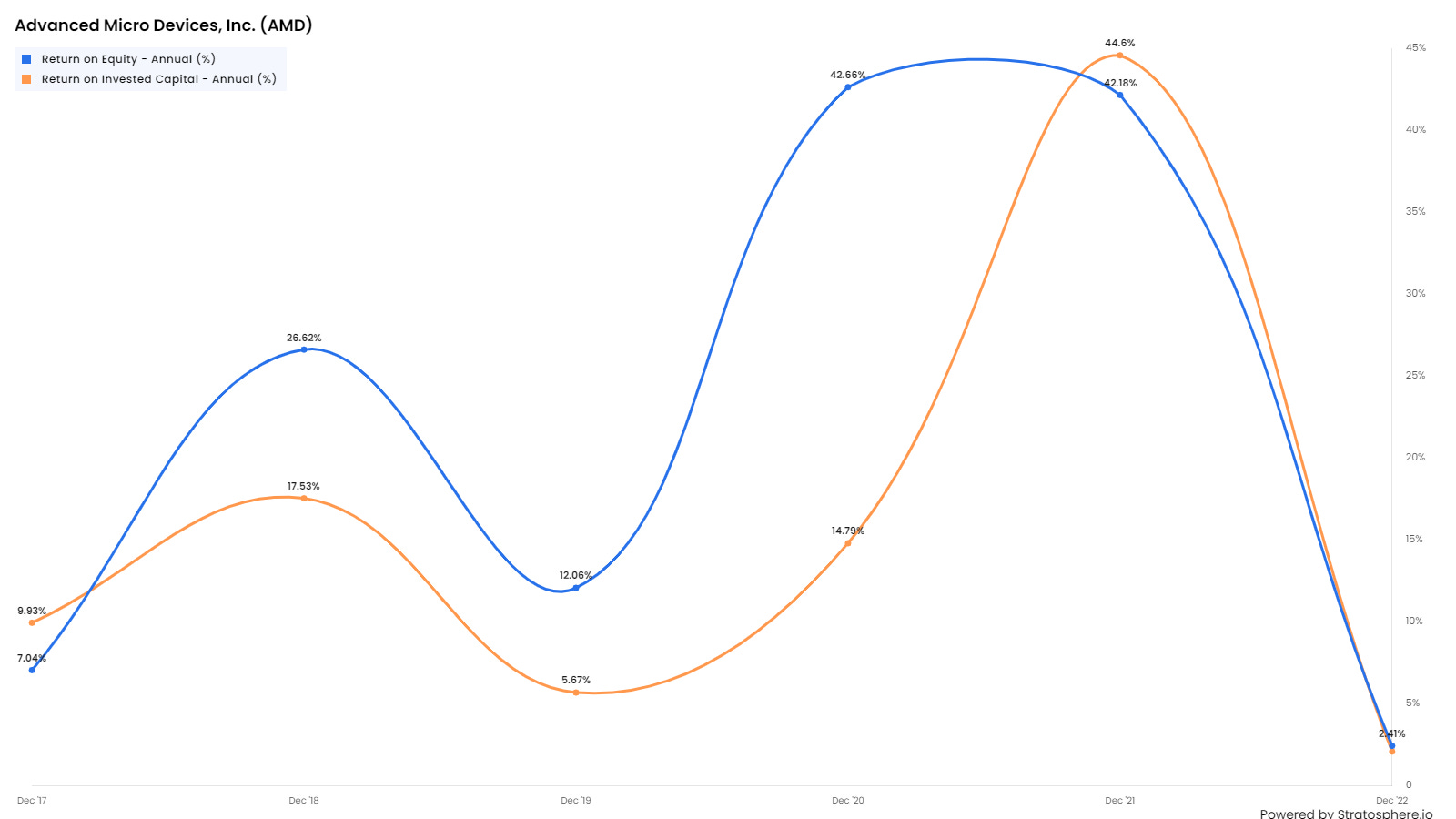

Profitability has improved strongly since Lisa Tsu became the CEO. AMD has really turned itself into a different animal, maintaining a high degree of profitability on an Operating, Net Income and EBITDA Margin basis.

Margins which had been on an upward trend for five years fell in 2022 due to the write -offs discussed above. However they should rise to above 20%-25% in the next few years.

Profitability has increase greatly since 2017 with ROE rising to 42% to 44% in 2021. In 2022, ROE fell due to the decline in Net Profit (due to write offs) and the significant increase in the Book Value of Equity due to the Xilinx acquisition.

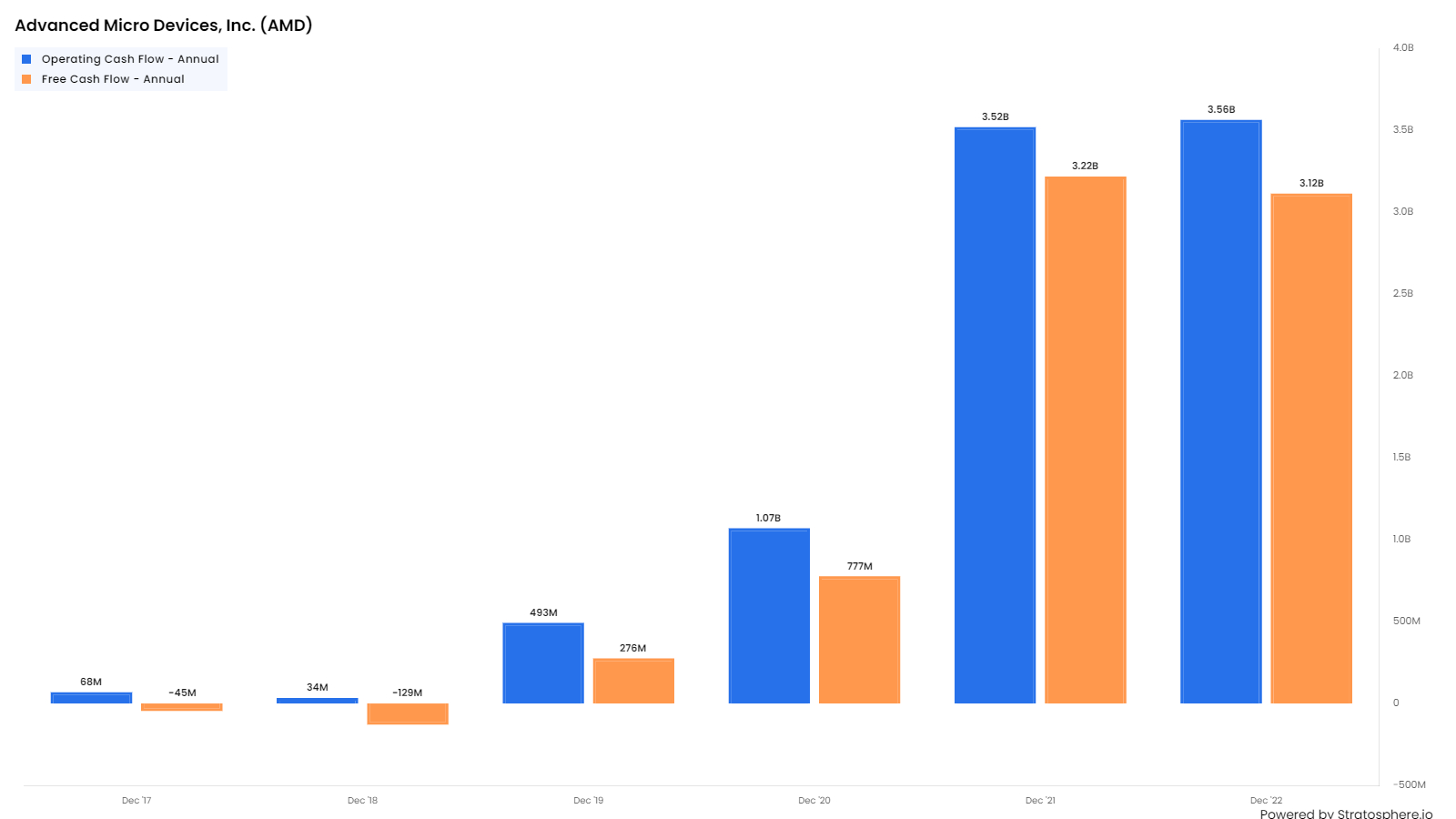

The Operating and Free Cash Flow profile has improved strongly in recent years and is on a run rate of ~US$ 3bn per year. The Free Cash Flow has helped fund R&D expenditure, stock buy-backs and let to steady increase in Cash and Short-term investments.

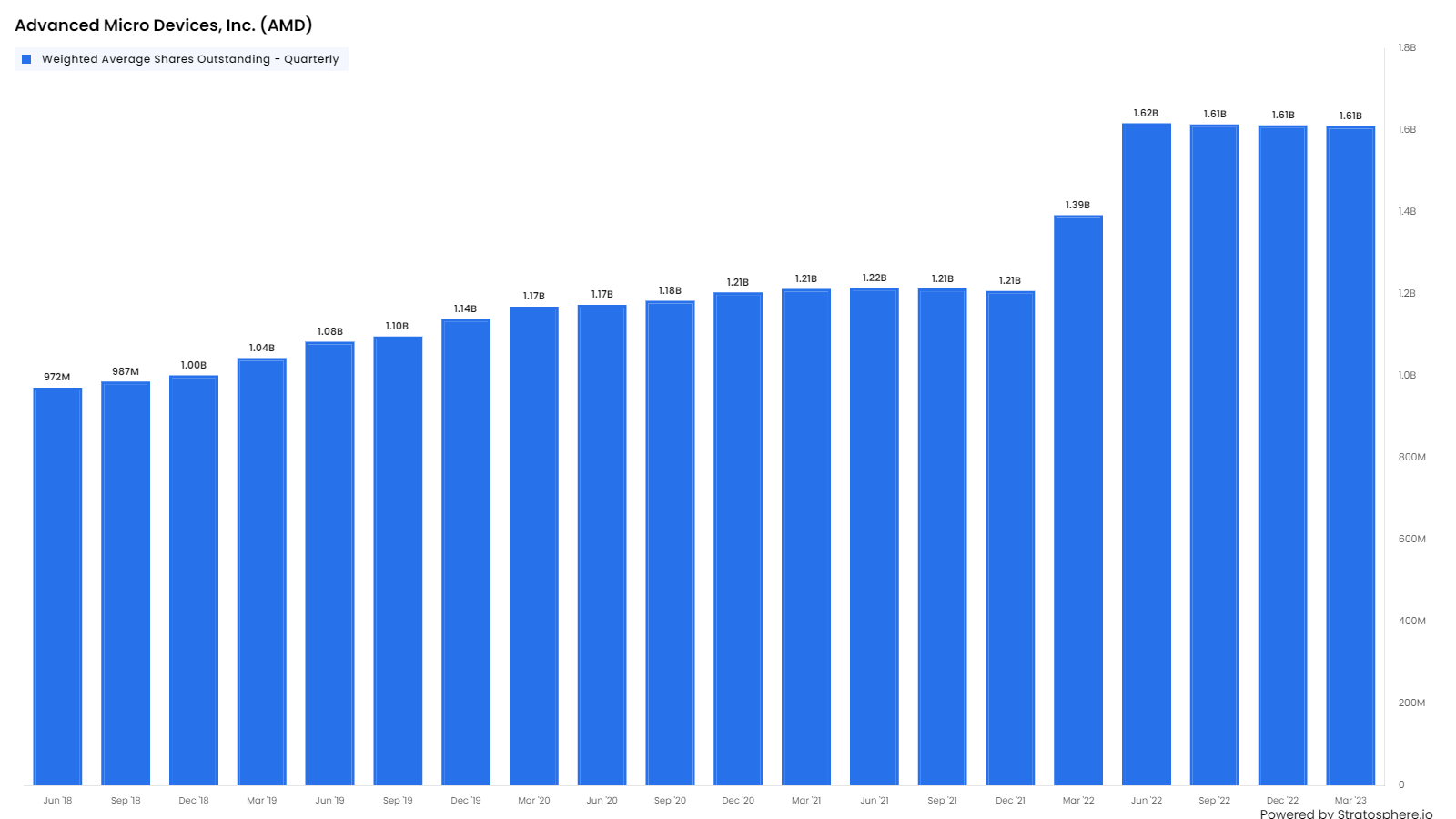

Historically, the company has gradually increased its share count. However, as cash flows have improved in the last two years, the company has started to buy back shares and this likely to continue.

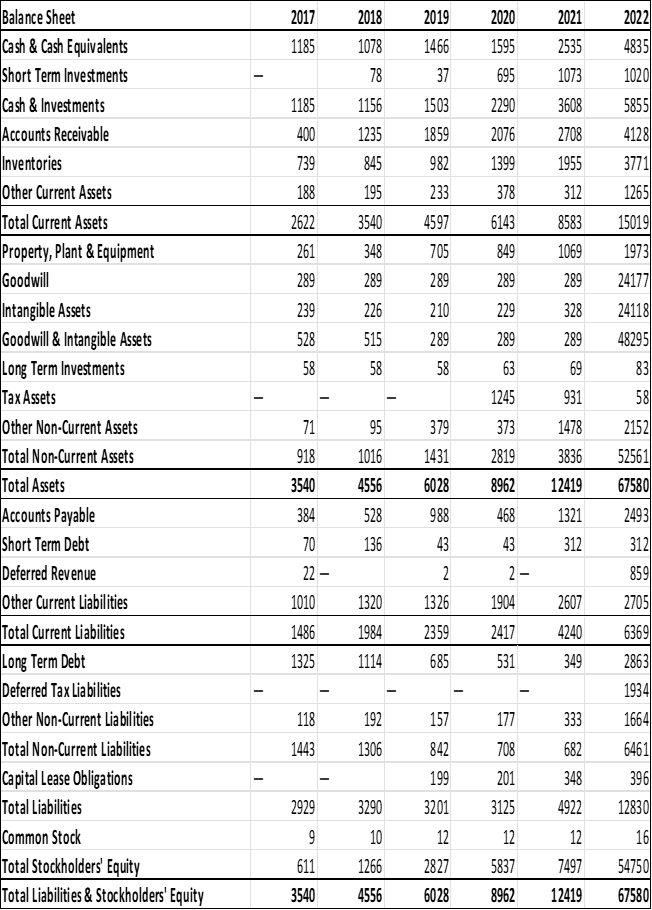

Balance Sheet

The structure of AMD’s balance sheet can be seen below:

Current Assets are approximately US$15bn, coming in at 20% of total assets. Long- Term assets are approximately 80% of Total Assets, at $53B and comprised primarily of Intangible Assets and Goodwill. This reflects acquisitions such as Xilinx and Pensando among others. Property, Plant and Equipment is only US$ 2bn which reflects the fact that capital-intensive manufacturing is outsourced,

Valuation

For the valuation, we ran a simple DCF model - These should come with a heatlh warning as the result is very sensitive to the input. A small change in the latter can lead to a very small change in the former.

Our assumptions included the following :

Revenue growth slowing from 24% growth to 20% over five years.

Weighted Average Cost of Capital (WACC) is at 9.3%

The EBIT Margin is constant at 18% over the next five years

The 5-year DCF give the following value ranges for a range of values for the long-term growth of the company.

Medium to Long-term Growth Assumption (%) /Estimate Fair Value of the stock (US$) from DCF Model

3% - US$ 91

4% - US$ 105

5% - US$ 126

In this case, Medium to Long-term means Year 6 onwards.

These estimated values compare with the current stock price of US$110.

For what it is worth (and it may not be very much), this DCF analysis suggests that the AMD stock is currently overvalued by 10%-20% and conservative long-term investors should be wary of buying at current levels and look a a discounted price of around US$85-US$90 per share .

Summary

AMD has transformed itself from a poor consumer-facing Chip business, that was always seen as inferior to Intel, to a broader consumer/ enterprise business with leading edge technology and products.

In the last few years, AMD has become more profitable in part by changing the business mix towards high-margin Enterprise/Embedded segment and away from low-margin consumer-facing businesses

Like many other companies they are focused on the opportunities presented by the growth of generative AI. They have a concrete target to aim at, namely the 80% -90% market share that Nvidia GPUs has in AI workload.

AMDs MI300 chip is the latest weapon in its fight against Nvidia in AI. It is due to be launched in the second half of 2023. If it can get traction with Datacentre/HPC buyers, it will give a significant boost to AMD and help support the current valuation

Concluding Remarks

The AMD share price has risen from ~US$ 80 to US$100 in the last two months in part due to the excitement relating to Generative AI. This may prove to be premature and/or overstated.

Our analysis suggests that the stock is currently slightly overvalued.

However, if there is evidence of strong demand for the new MI300 then the current value may well prove to be justified.

We will keep an eye on the stock price and await early news on the success of AMD MI300.

Annexe 1 : Summary of AMD Products.

Processors

AMD offers customers and enterprises access to processors for server, workstation, embedded and semi-custom, laptop, desktop and Chromebook applications

For servers, EPYC processors are the world’s highest performing x86 server processors, of which can be incorporated with Cloud Computing, Database and Analytics, HCI and Virtualization and High Performance Computing applications.

For workstations, AMD’s most up-to-date offerings are the Ryzen threadripper pro processors, which contain best-in-class core counts for multi-threaded workloads, the threadripper series for creators, which allow for artists, engineers, architects etc. to create expansive visual experiences much more efficiently than the nearest Intel Xeon W-3275 competitor.

Mobile Processors which power the likes of the Lenovo ThinkPad.

Embedded and semi-custom processors at a series of industries and use-cases through their EPYC Embedded, Ryzen Embedded, R-Series Embedded, G-Series Embedded and Semi-Custom CPUs which power devices within the Aerospace, Automotive, Digital Casino Gaming, Networking and Communications, Medical Imaging, POS kiosks, and Console Gaming spaces, as examples.

AMD powers a series of personal computers with their hardware.

Laptops, these include the Ryzen Mobile Processors, Athlon Mobile Processors and AMD powered laptops for students and teachers.

Desktops. The Threadripper PRO, Ryzen PRO, Athlon PRO, Ryzen Threadripper, Ryzen and Ryzen with Radeon, and Athlon with Radeon Graphics processors power desktops for higher end of the Consumer range, all the way to hardware operating within demanding business environments.

Chromebooks. AMD has Ryzen and Athlon processors geared at powering Chromebooks for enterprise, personal and educational end use-cases.

Graphic Graphic Processing Units (GPUs)

Technical Applications. AMD offers a series of graphics cards and associated drivers and software for a variety of end cases. Most notably these include the likes of AMD Radeon Pro graphics, focused on powering both mobile and desktop workstations, supporting raytracing, intensive workloads etc., embedded GPUs, with the likes of the Radeon E9170 Series powering high-end casino gaming machines, medical imaging devices, aerospace applications, mobile signage, HMI etc.

Gaming. AMD offers customers semi-custom graphics hardware, which most notably has been applied with Xbox and PlayStation consoles leveraging multi-core CPU and graphics technology within a single chip, and Nintendo consoles using custom AMD graphics tech to power their experiences. Lastly, AMD gears Radeon Graphics cards at both desktops and laptops to allow for gamers to immerse themselves in the latest experiences.

Accelerators.

AMD Instinct are professional GPUs geared at the acceleration of the capabilities of deep learning, artificial neural networks. AMD has GPUs supporting scale from single server solutions all the way up to the world’s largest supercomputers, allowing for scientists and engineers to tackle some of the most pertinent problems.

AMD Pensando Infrastructure Accelerators are the industry’s only fully programmable software-in-silicon Data Processing Units (DPUs), allowing individuals and enterprises to execute a software stack that delivers cloud, compute, network, storage and security services, at a large scale.

AMD offers Alveo accelerator cards, which provide optimized acceleration workloads for end-users working on financial computing, machine learning, computational storage, video streaming etc. Alveo was developed by Xilinx.

AMD offers the world’s only computational storage drive (CSD), of which provides compute services and supports persistent data storage such as NAND flash or other non-volatile memory, of which can help runtimes, libraries, APIs and drivers be built into the data application systems, accelerating their capabilities by up to 10X.

AMD’s SmartNIC Network Accelerators are geared towards cloud providers looking to boost performance and adaptability. These products help associated users navigate a vast array of complex applications and adapt acceleration and resources across multiple workloads. These network accelerators help to deliver scalable and low latency hardware acceleration while still giving users the ability to rapidly reconfigure workloads.

Telco Accelerator Cards are geared at 5G-specific applications. These accelerator cards help to convert standard servers into virtual baseband units, abiding by the performance requirements of the O-RAN 5G deployments, allowing for the radio network to become more agile and scalable all while reducing the total costs of the overall deployment.

Software

AMD’s software, particularly in the data center segment, will be crucial for the future trajectory of the company, and should be something investors should focus on for the foreseeable future.

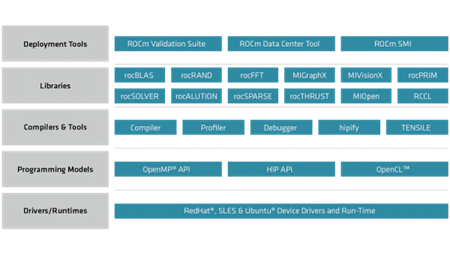

AMD ROCm, is an open software platform that allows for researchers to tap into the AMD Instinct accelerators in order to drive their scientific discoveries.

With this platform, individuals get access to open compute languages, a series of compiler libraries and tools that are designed to increase the rate at which code can be developed. A full overview of the capabilities contained within can be seen outlined below:

AMD Infinity Hub contains a collection of advanced GPU software containers and deployment guides for HPC and AI/ML applications, of which enable individuals to speed up deployment times and efficiencies. Infinity Hub is HPC and AI-specific, making it easier for workloads to be deployed on both GPUs and accelerators.

AMD PRO edition is the company’s all-encompassing name for its driver software. Individuals can leverage drivers that help improve rendering speeds, video encoding, and overall performance across a series of intensive professional applications.

AI-workload

Demand for GPUs is said to be driven by the strong growth in AI-driven workloads. There are reported to be huge shortages of GPUs and Nvidia is charging ~5x markups versus manufacturing costs. The industry is desperate for an alternative.

One possibility is Google TPU which has impressive performance in AI Workloads. they are unlikely to be market leader.

Google TPUs will only ever be available from one firm in one cloud which is Google Cloud Platform (GCP). GCP is unlikely to sell them to AWS, Azure or other competitors.

Google does not disclose chips well after they are but large buyers need it documented before launch with early access systems available before ramp.

Google has not been forthcoming with technical documentation

This strict gatekeeping of Google's biggest technological advancements in AI infrastructure will keep them on the backfoot vs. Nvidia based cloud offerings, structurally, unless Google changes their business model.

AMD’s best hope for this market is currently AMD MI300

AMD has delivered CPUs and GPUs for HPC It delivered HPC GPU silicon in 2021 for the world's first ExaFLop supercomputer, Frontier. While the MI250X powering Frontier worked well enough, it failed to garner any leverage amongst the big spenders of cloud and hyperscalers.

The next one is MI300 GPU which AMD and others hope could challenge Nvidia for GPUs in HPC. MI300 will be the industry's first Data Center chip that combines a CPU, GPU, and memory into a single integrated design, delivering 8x more performance and 5x better efficiency for HPC and AI workloads compared to our MI250 accelerator currently powering the world's fastest supercomputer. MI300 is on track to launch in the second half of 2023.

Bloomberg reported that Microsoft is working with the chipmaker on artificial intelligence processors. Microsoft is providing financial support to bolster AMD's AI efforts. Microsoft is working with AMD on a homegrown Microsoft processor for AI workloads, code-named Athena, the Bloomberg report said.