We have discussed Alphabet (GOOGL) several times. It is one of the most remarkable companies of the last few decades, which itself has been a golden era for new fast-growing companies. Our original note which was like a eulogy to the company can be found here. Our most recent note on them can be found here.

Last week they announced an all-cash offer to take over Israeli company Wiz.

Reuters reported it as follows

“Alphabet is paying in cash to buy the startup backed by Blackstone, Andreessen Horowitz and Sequoia Capital. It was a hard-fought agreement. Back in the middle of last year, the technology goliath offered $23bn for Wiz, according to the Wall Street Journal, which would already have made it Google’s largest acquisition. Talks collapsed in part over concerns that hostile trustbusters under President Joe Biden would nix any tie-up.

The companies may feel emboldened by new President Donald Trump’s self-professed love of deals. The basic rationale at least makes sense. Google is a distant third place in selling services to crunch data across its fleet of servers, trailing Microsoft and Amazon.com. Yet high-profile hacks have made governments and businesses antsy to better safeguard these processes. Wiz’s secret sauce is that it tries to flag and catch nefarious activity before it happens. By combining, Google can differentiate itself from its rivals in a way customers care about.

This simple story is complicated by the financial reality. Granted, privately held Wiz may be growing faster than competitors, with the company touting that it expects to hit $1 billion in recurring revenue in 2025, according to CNBC, up from $500 million last year.

Yet the original mooted price tag was already expensive; adding an extra $9 billion makes it even more so. The deal values the target’s enterprise at 32 times its sales goal. Peers Datadog, Snowflake and Crowdstrike trade at 9 times, 10 times and 17 times expected recurring revenue, respectively, according to Visible Alpha.

Worse, there is no guarantee that a Trump administration will be friendlier. The Department of Justice continues to pursue Alphabet in court over anticompetitive behaviour. The Federal Communications Commission is eyeing YouTube for allegedly discriminating against faith-based channels.”

What does Wiz do?

Wiz provides cloud-based cybersecurity solutions, powered by AI, that help companies identify and remove critical risks on cloud platforms. It works with multiple cloud providers such as Microsoft and Amazon (which are Google Cloud competitors) and has companies from Morgan Stanley to DocuSign among its customers. With 900 employees across the United States, Europe, Asia and Israel, Wiz previously said it planned to add 400 workers globally in 2024.

Wiz was created in 2020 and reached $1M in Annual Recurring Revenue (ARR). This is a phenomenal rate of growth.

Interest in the cybersecurity industry has surged since the global CrowdStrike outage last year, making enterprises more concerned about protecting their digital infrastructures. This is industry is difficult for a non-technical analyst to understand. We tried to work on this in our notes on CrowdStrike which can be seen here and here. It is tell the difference between the offerings of the various companies in this space and, therefore, hard to say whether any particular firm has a unique or compelling offering. It is a competitive market with many players including Microsoft. Our reading suggests that while Wiz’s offering is similar to others, its runtime security is considered high-quality and more differentiated.

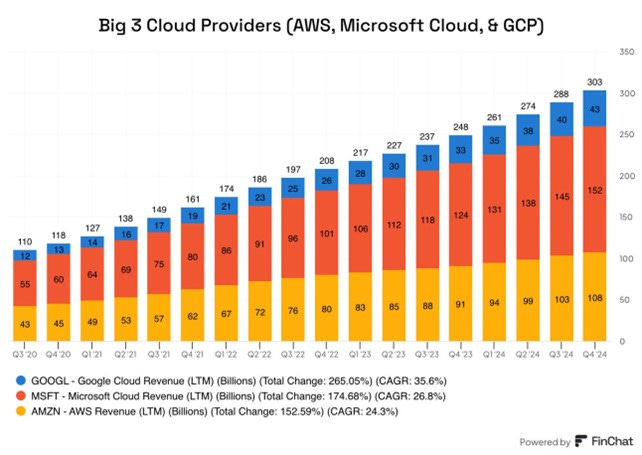

Wiz will be integrated into Google Cloud Platform(GCP), which should help that Division continue its growth, as it continues its well-executed strategy to catch up with Amazon and Microsoft.

In its press release announcing the deal, Google stated “This acquisition represents an investment by Google Cloud to accelerate two large and growing trends in the AI era: improved cloud security and the ability to use multiple clouds.”

Wiz’s financial numbers are not a matter of public record, but it is generating somewhere between $500 million and $1 billion in Annual Recurring Revenue (ARR).

This means Google is buying Wiz at more than 60x sales using the lower point of the range and 40X sales if we use the mid-point of that range. This is a steep multiple.

Alphabet’s last number for cash and short-term investments was $95bn, so the asking price would reduce that by a not insignificant 30%.

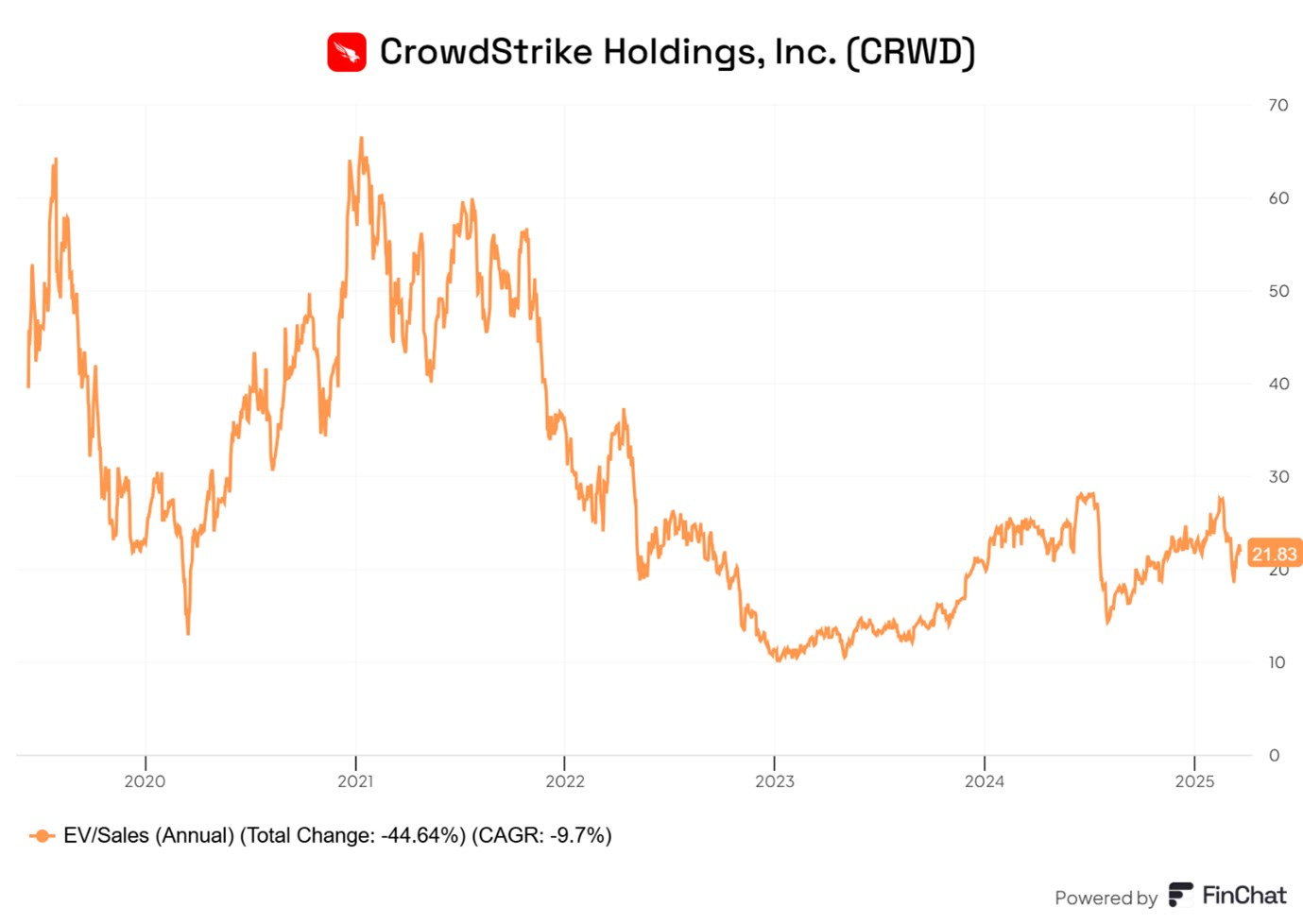

Cloud security is a high-growth business, and each breach or major spate of ransomware demands convinces companies of the need to invest more in cybersecurity. According to analysts, Crowdstrike (CRWD) is due to see 20% revenue growth for the next four years and to become strongly profitable as shown in chart below:

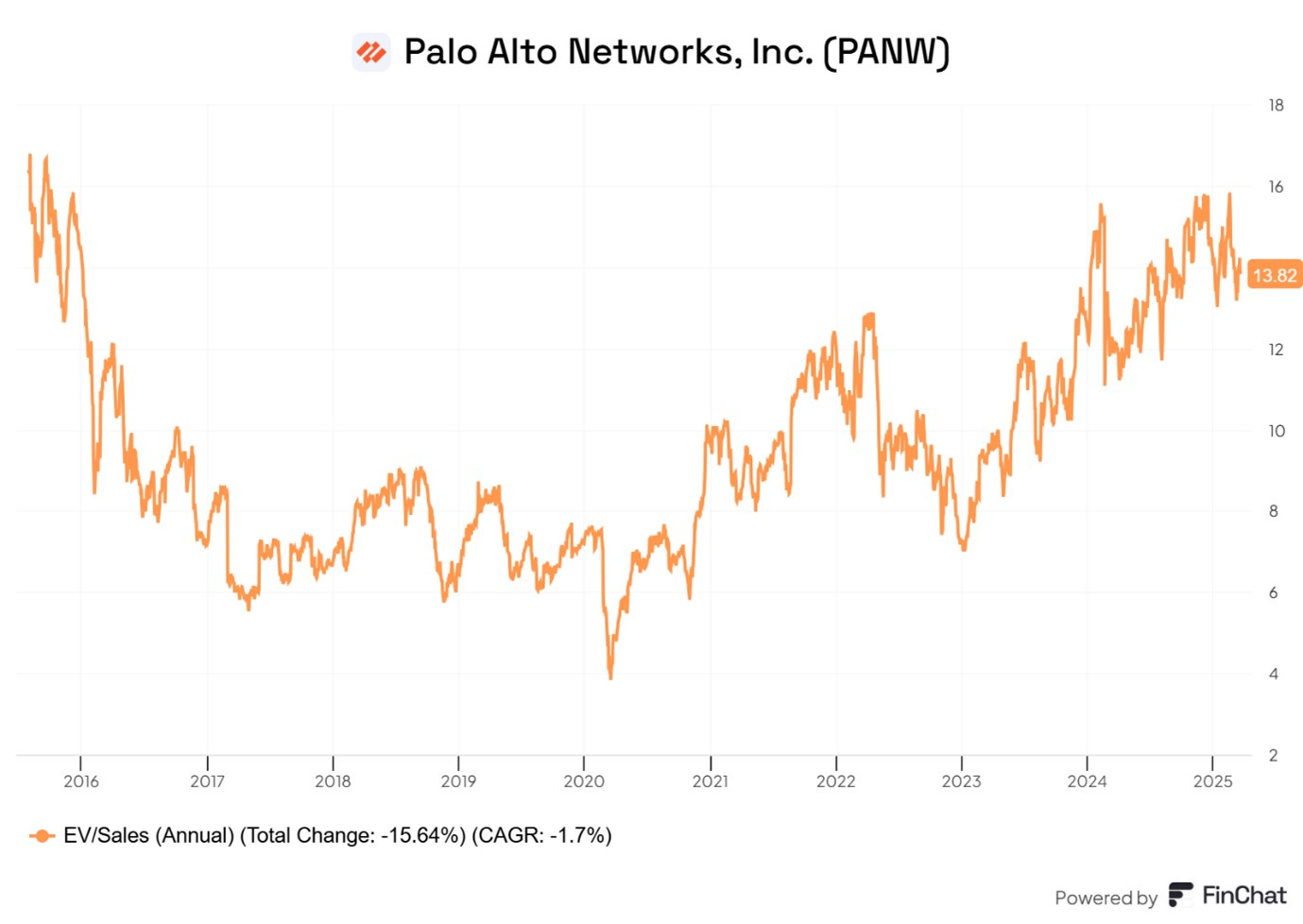

The much larger Palo Alto Networks (PANW) is due to see 14%% revenue growth for the next three years and elevated net profit levels over the next three years, as shown in chart below:

Crowdstrike is on a Price to Sales/ Ratio of 21.8X.

Palo Alto Networks (PANW) is on a Price to Sales/ Ratio of 13.8X.

Both companies are trading at much lower EV/ Sales ratio compared with the multiple that GOOGL is paying for Wiz.

Wiz is smaller than these companies but currently growing at a much faster rate so a higher multiple is justified.

When Wiz is integrated into Alphabet there will be some significant initial cost savings.

It will reduce

significant cloud hosting costs as it will get cloud hosting services at cost from Google Cloud Platform (GCP).

go-to-market and brand-building expenses and back-end maintenance needs and many other costs will be redundant after the integration with GOOGL.

This means margins will increase. However, the main rationale for the deal is not increasing margins, but boosting revenues.

GCP has to show it can leverage its existing corporate relationships at Scale to cross sell Wiz products and Services. GCP has a lot of corporate customer relationships and the main rationale for this whole transactions, is the opportunity to cross sell Wiz product and solutions to GCP customer base. The GCP business is still much smaller than it rivals but has grown much more strongly.

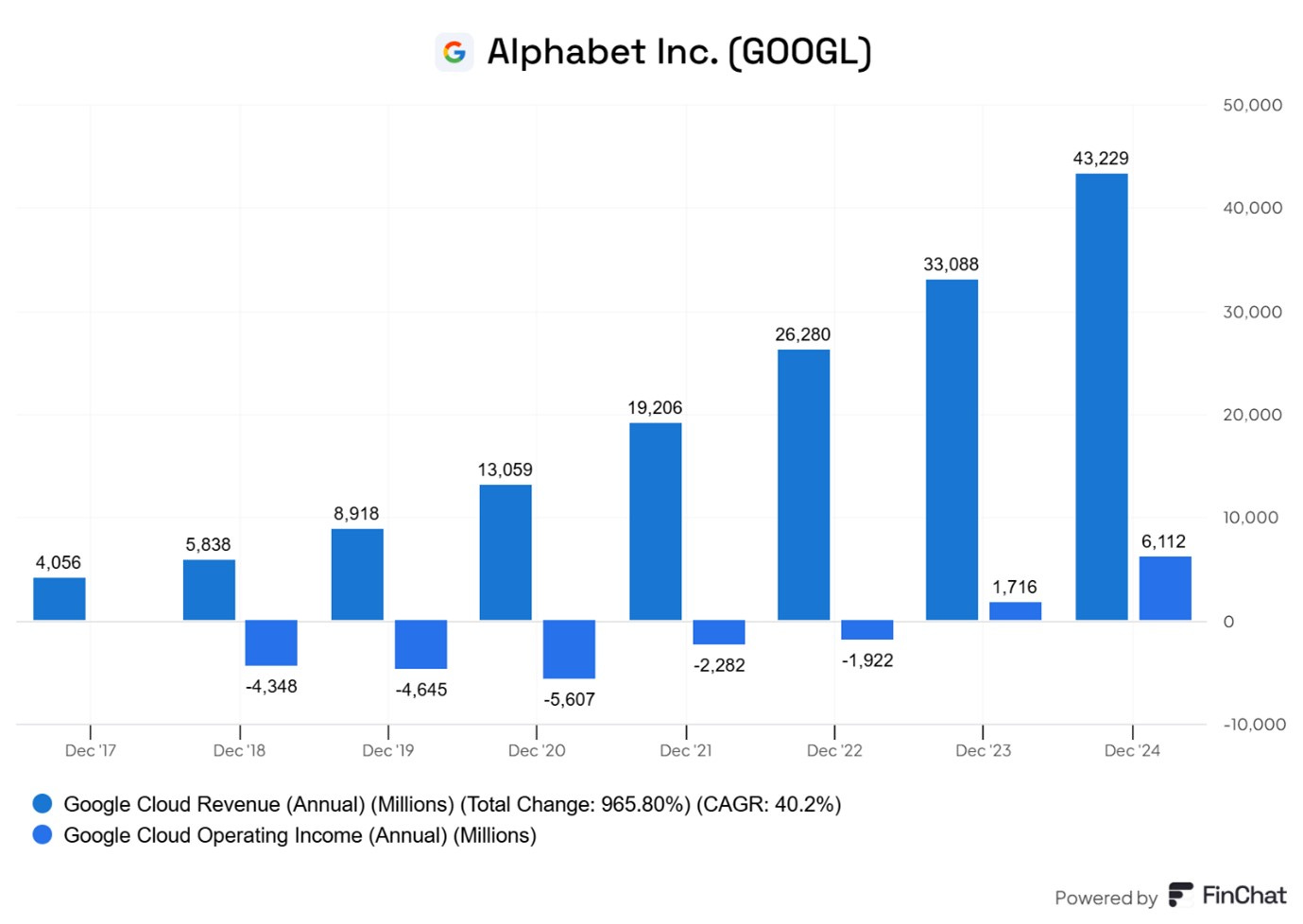

In FY 2024, GCP had operating revenues of $43bn and Operating Income of $6bn. Revenues have 10x in five years.

Google has done some very successful takeovers in the past including Doubleclick ($3.1bn) YouTube ($1.65bn) and Android ($50mn).

However, most of these were done a long time ago. And markets are very unsentimental and care little for history which is “already in the price”. Markets always ask companies “What have you done for me lately?”.

The $30bn proposed cost of Wiz is much more than all the past takeovers combined. The price at 40 + times sales appears to be high. Google is paying a high price for a company in a crowded industry. It is going to struggle to maintain its track record of extracting great value from its acquisitions esp. as it is looking to pay a steep entry fee.

The founders and shareholders of Wiz will have large payday as they created $30bn of value in 5 years. Some of venture the investors in Wiz will also gain. Index Ventures has turned its $245mn investment (First $3.3mn was invested in 2020) into $4.3bn. The investment was made in 2020 and just five years later was part of the biggest venture-backed sale of all time. Wiz was co-founded by Assaf Rappaport, a veteran of the Israeli Army’s elite Cybersecurity Unit, along with three colleagues.

The big question is will this deal benefit GOOGL shareholders? Time will tell.

Our View

In our view, GOOGL most likely suffers from a variant of The Dutch Disease. Its Search business and some of the early acquisitions were so successful, the business could not help gushing free cash flow. This good fortune encouraged laziness, over hiringand excessive remuneration.

There is a lot of anecdotal evidence of the growing of bureaucracy and management growth in the company. Large numbers of people are very well paid but seem to get by doing little. This tendency has probably been exacerbated by the trend towards WFH.

Wiz was only started in 2020. GOOGL has a lot of clever talented people on its books. Why did they not come up with something half as valuable?

Looking the recent financial performance data for GOOGL, there is some indication of a recovery in the last three years. Operating margins and Return on Equity are just back at 2021 level.

Free cashflow has growth by an impressive CAGR of 19% over the last ten years. However, Stock Based Compensation has increased by 17.8% CAGR over the same period. Therefore, non-employee, minority shareholders have had to share the fruits of increased free cashflow with employees. The trend has not favoured the providers of risk capital.

The company has increased capital investment greatly in the last few years in a successful attempt to catch up with Microsoft and Amazon in the Cloud hosting business.

Capital expenditure as increased from $10bn in 2015 (40% of operating cash) to 52bn (42% of operating cash). Capital expenditure is shown as a negative bar in the chart above at it is a cash outflow.

As a result, GOOGL has become a more capital-intensive business. Gross Property, Plant and Equipment (PPE) has increased from $40bn (27% of total assets) in 2015 to $ 254bn (56% of total assets).

The business will have higher depreciation costs over time, and this will tend to reduce reported net profits. GOOGL will have to reduce costs and become more efficient over time if it is to maintain reported net profits. This is going to be a tough cultural change for a workforce used to the easy life.

GOOGL needs a new, profitable growth engine. Time will tell whether Wiz will prove to be that. They will have to boost Wiz’s sales significantly to justify the price they have paid.

Conclusions

Alphabet have a great track record of integrating acquisitions and of generating huge returns from them.

The Wiz acquisition is their largest ever and is made at a high EV/Sales multiple.

It will reduce their cash holdings significantly at a time when its investments, especially in AI, are growing strongly

Alphabet will need to boost Wiz’s revenues strongly and cut costs.

The fact that GOOGL had to buy Wiz (at a steep price) rather than being able to develop the same capacity in house suggest the company is not as entrepreneurial and innovative as it should be.

Perhaps the best thing GOOGL can do is to give the founders and senior managers of Wiz, who have crated $ 30bn of value in five years, much greater and wider responsibly in the vast Google organisation. This means they can inject some dynamism, innovation and entrepreneurialism into the company.

As a recent of recent share price declines, GOOGL shares appear to be trading at an attractive multiple.

Hi Sir,

This is an excellent post, thanks for your effort!

I had a question though based on the following lines:

"The fact that GOOGL had to buy Wiz (at a steep price) rather than being able to develop the same capacity in house suggest the company is not as entrepreneurial and innovative as it should be"

Google is not anywhere near the cybersecurity space. And if they dont want to spend their resources (all of them) on building their own cybersecurity infra, what exactly is the problem? It probably would have costed them more to make their in house cyber security system.

Acquiring a small competitor (valuation maybe justified) does make sense from my statement.

Perhaps they may not declare dividend this year in order to save cash, time will tell.