Apple Inc (AAPL)

Quarterly Results

We first wrote about apple on May 17, 2023, and that article can be found here.

We are belatedly catching up with the recent results of various companies. We will look at Apple in detail again after the release of their most recent quarterly numbers

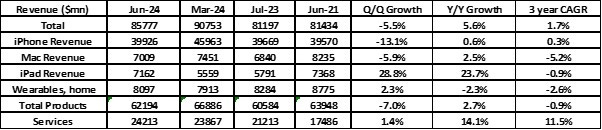

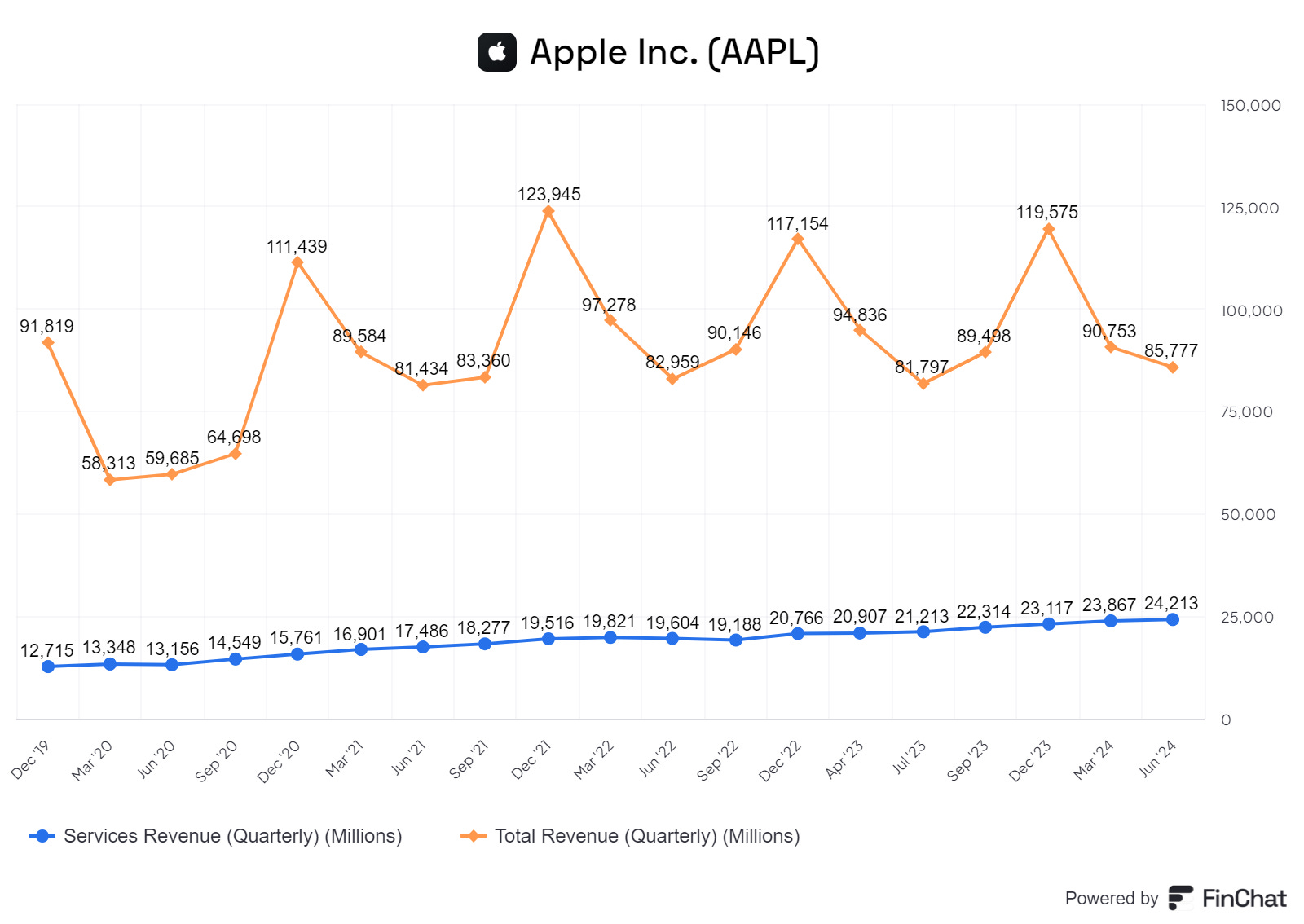

The key feature of the results was lacklustre growth in the key iPhone segment and in other segments. The two exceptions were iPad and Services.

iPad revenues grew 28.8% (q/q) thanks to the launch of two new models in the quarter.

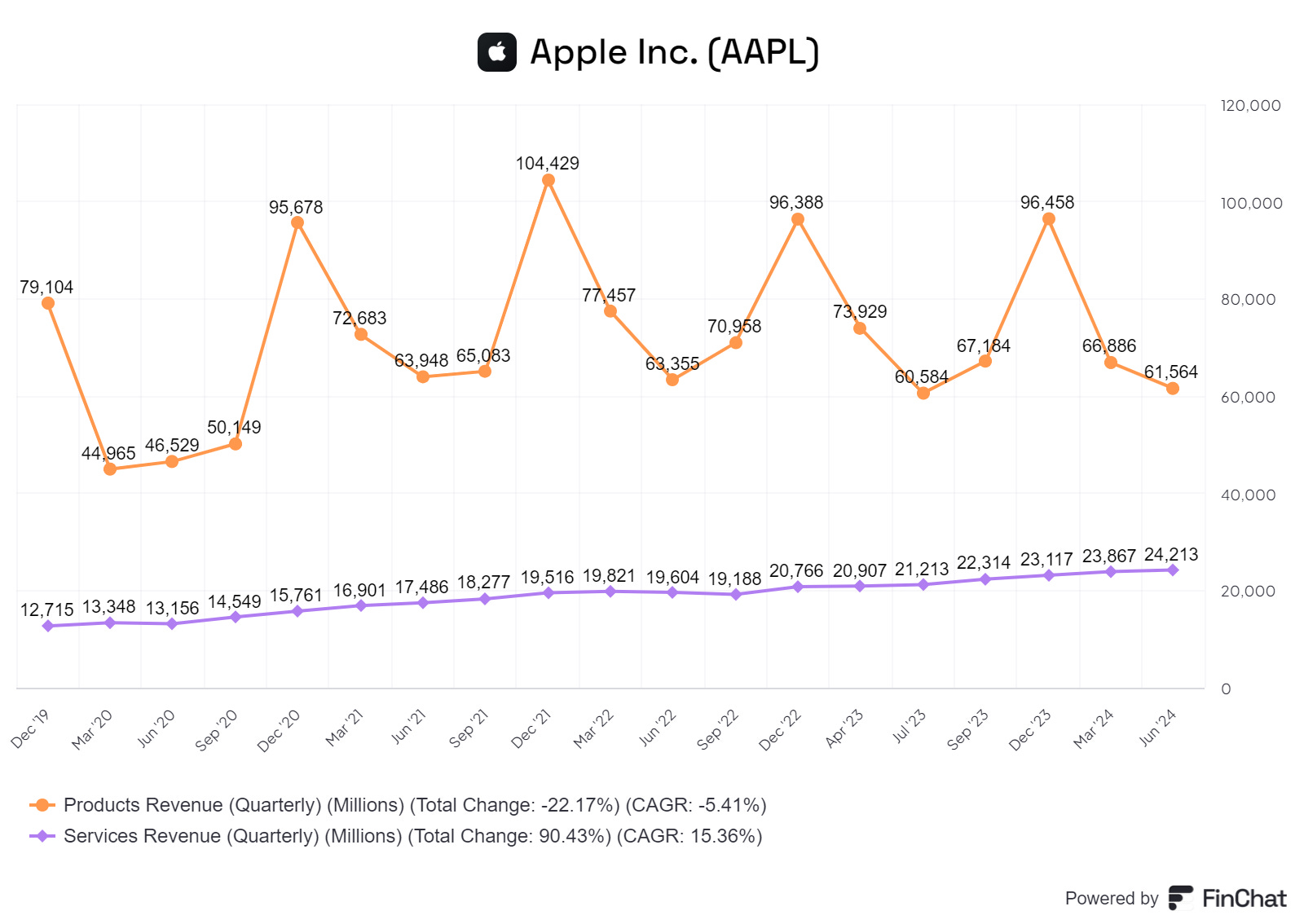

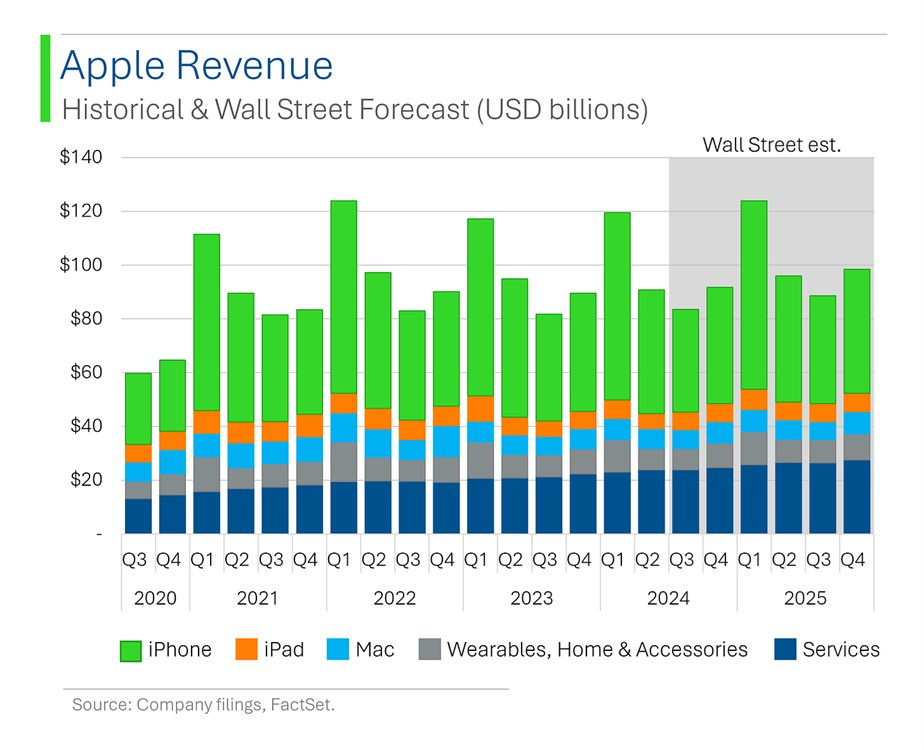

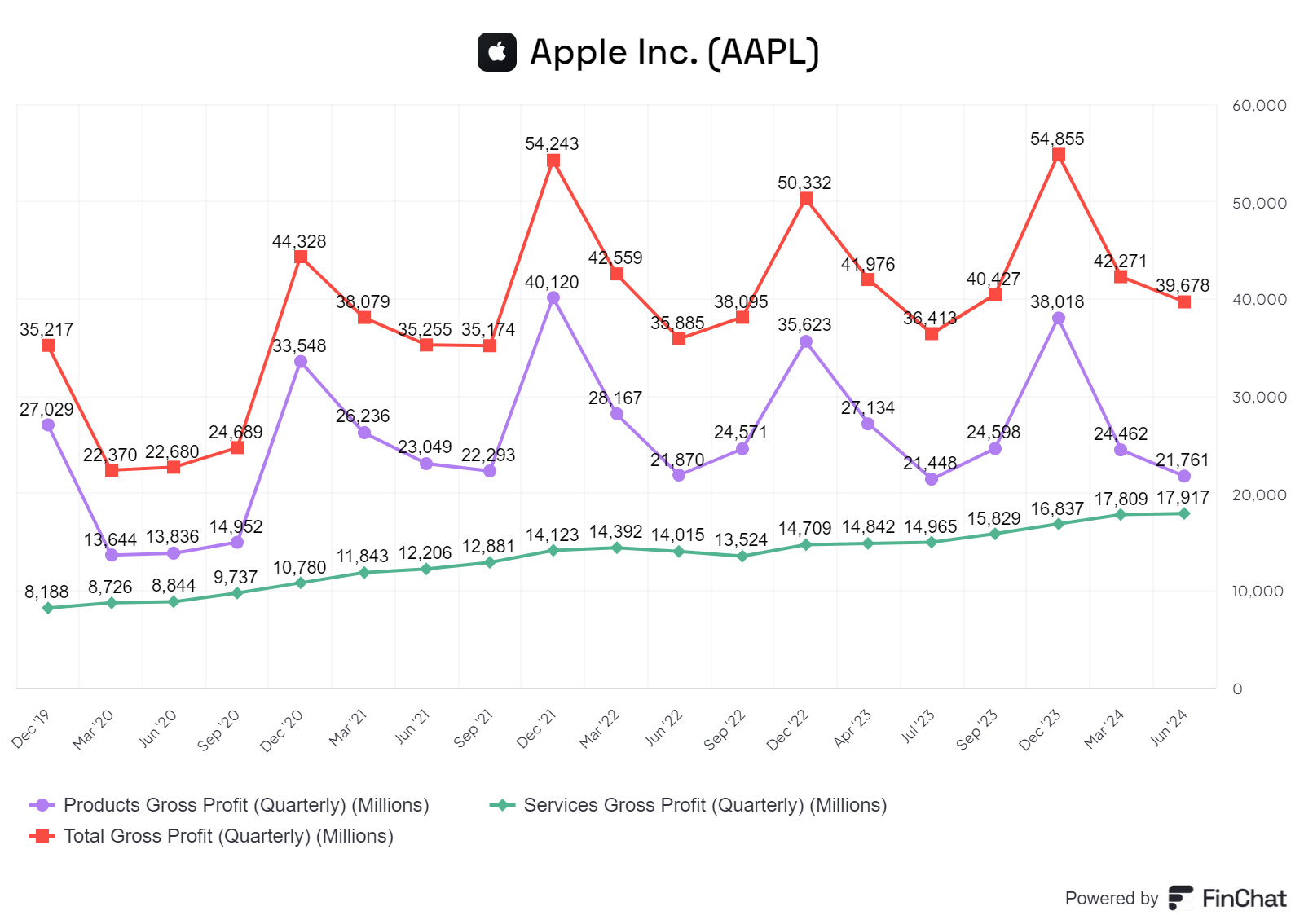

Services has been growing strongly for a few years and now accounts for ~30% of total revenues, up from 22% two years ago. The chart above shows that Services revenues have doubled in the last five years while Product revenues have been broadly flat.

Total Revenue grew 5.6% (y/y), Net Profits grew by 7.9% (y/y) while EPS faltered. The latter is despite a reduction in the share count due to stock repurchases. It probably reflects the dilutive effects of stock-based compensation.

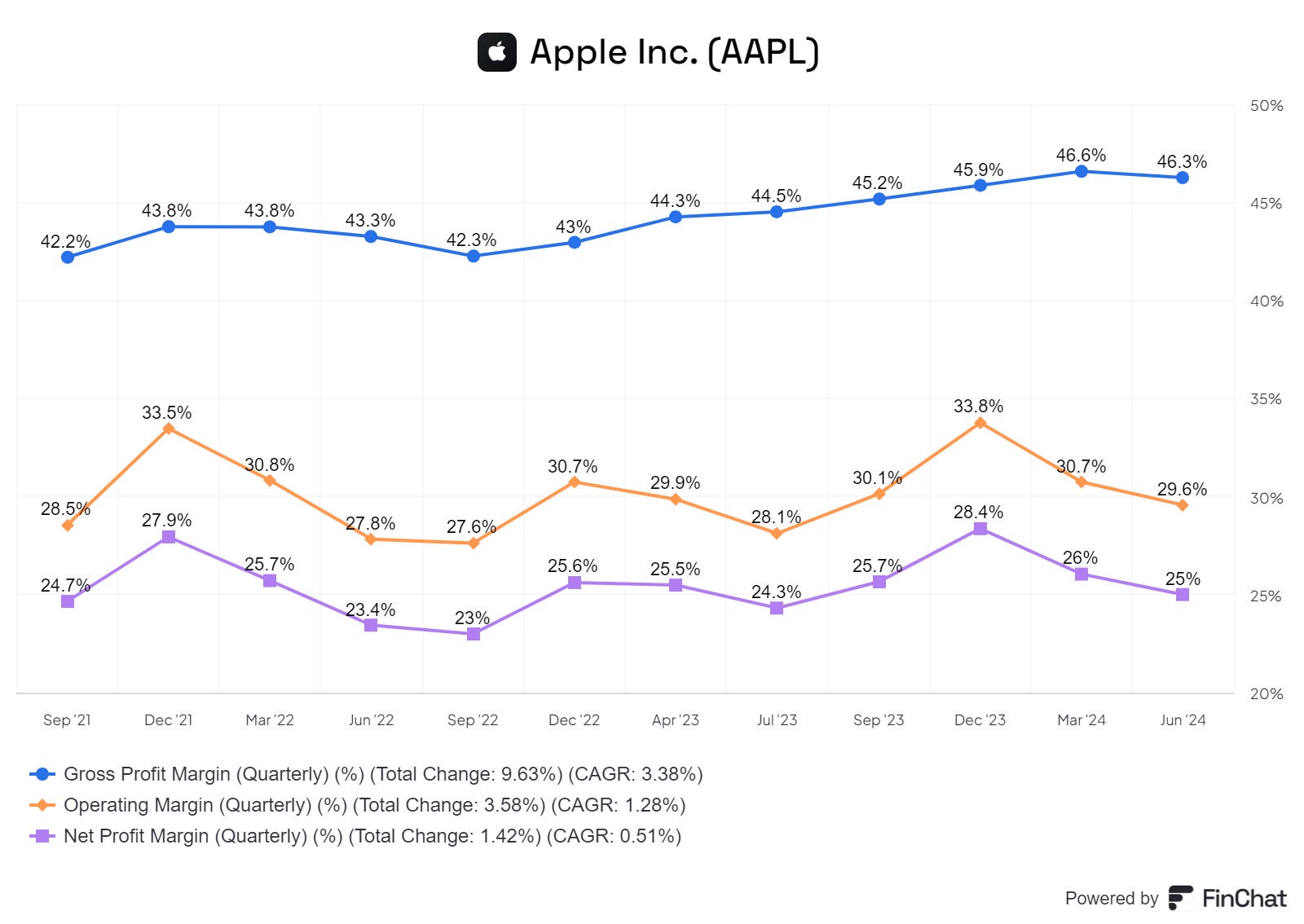

Margins have been stable. This raises the question why they have not risen more, if higher-margin services account for a higher percentage of revenues.

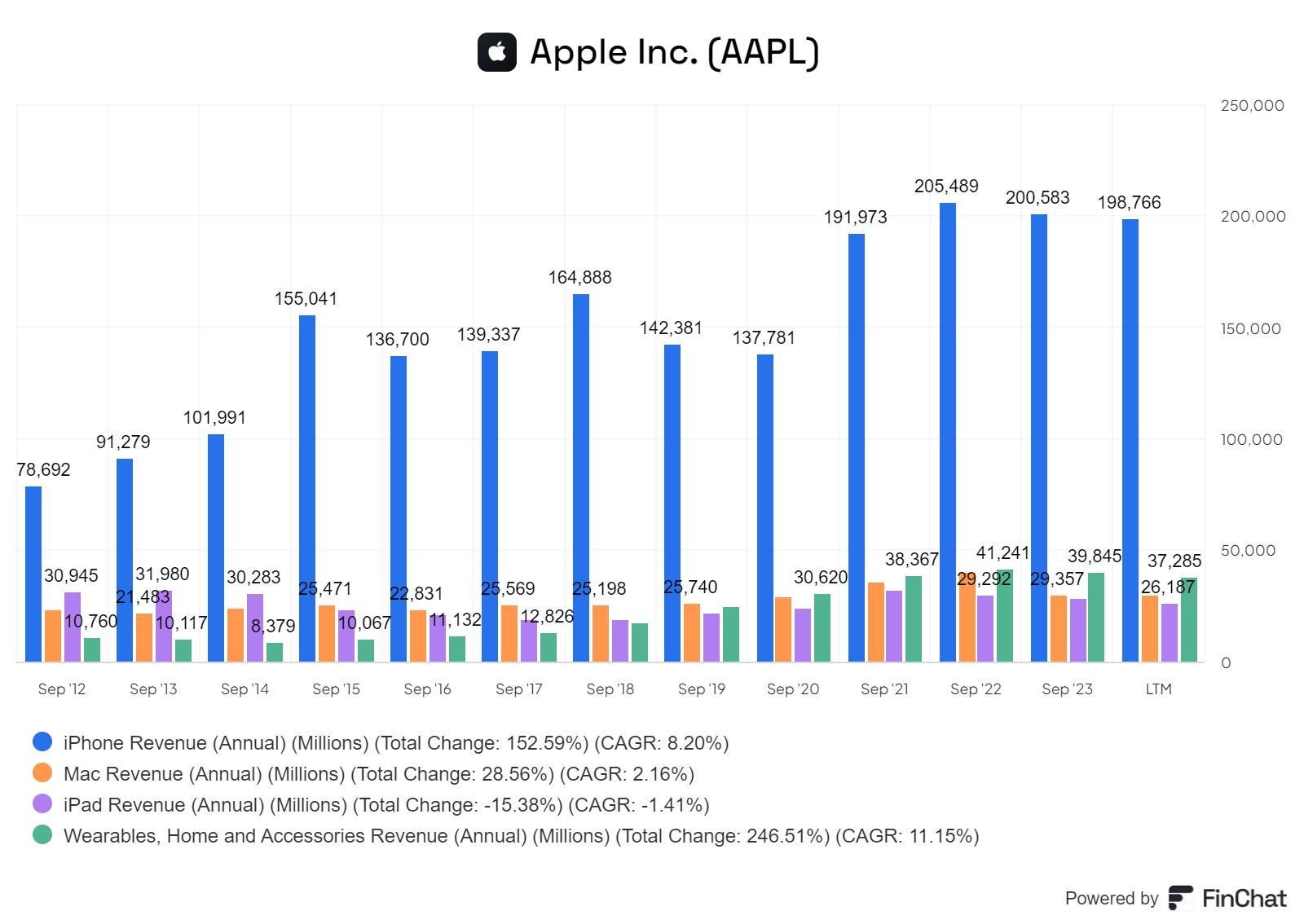

The iPhone segment dwarfs the other product businesses, iPad, Mac and WHA (Wearables and Home Accessories) which are of a similar size. As the Chart below shows, services have been growing faster.

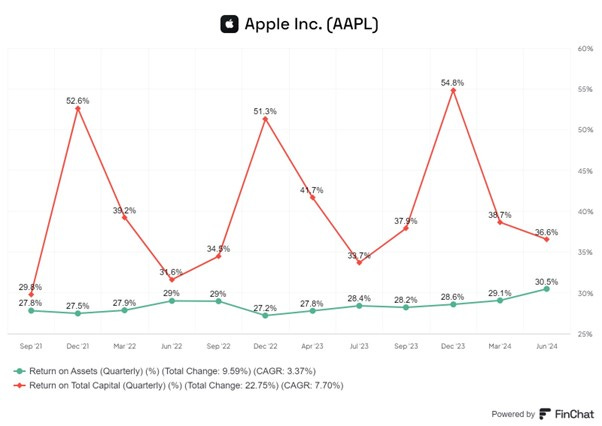

The company remains solidly profitable with a current ROTC of 36.6%.

The overall pictures seems to be of faltering revenue growth, flat margins and poor operating leverage.

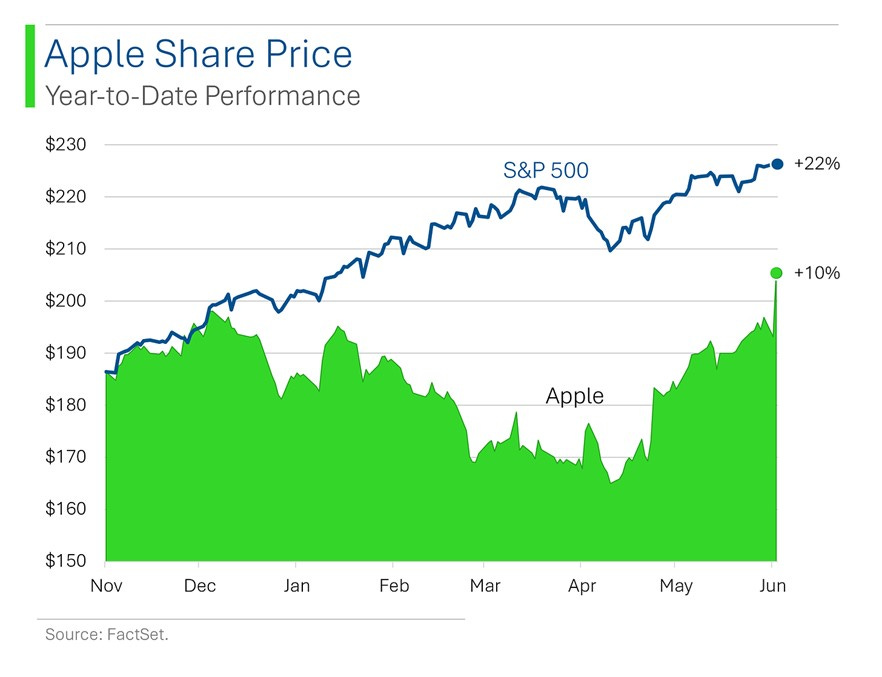

The Apple share price has underperformed the index up to H1 2024.

Revenue Forecasts

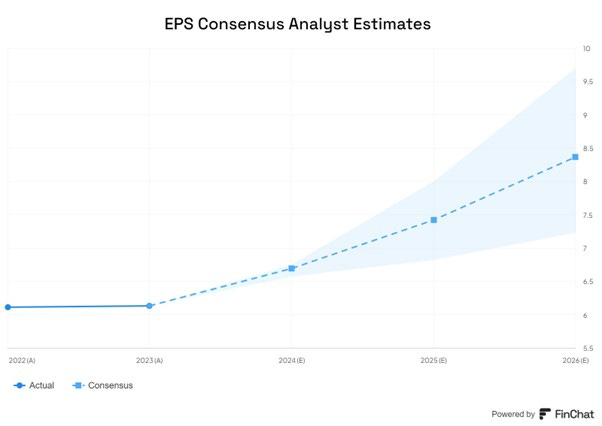

The analysts revenue forecasts shown above) do not suggest significant growth in the next four quarters except in Services.

Highlights of Conference Call

Summary Numbers

“Today, Apple is reporting a new June quarter revenue record of $85.8bn, up 5% from a year ago and better than we had expected. EPS grew double digits to $1.40 and achieved a record for the June quarter.

This was achieved despite a “230 basis points of negative foreign exchange impact.”

“And we set an all-time revenue record in services which grew 14%.”

“Company gross margin was 46.3% near the high end of our guidance range and down 30bps (q/q) driven by a different mix within products . It was partially offset by a favourable mix shift towards services and cost savings.”

“Products gross margin was 35.3%, down 130bps q/q…”

“Services gross margin was 74% down 60 basis points from last quarter.”

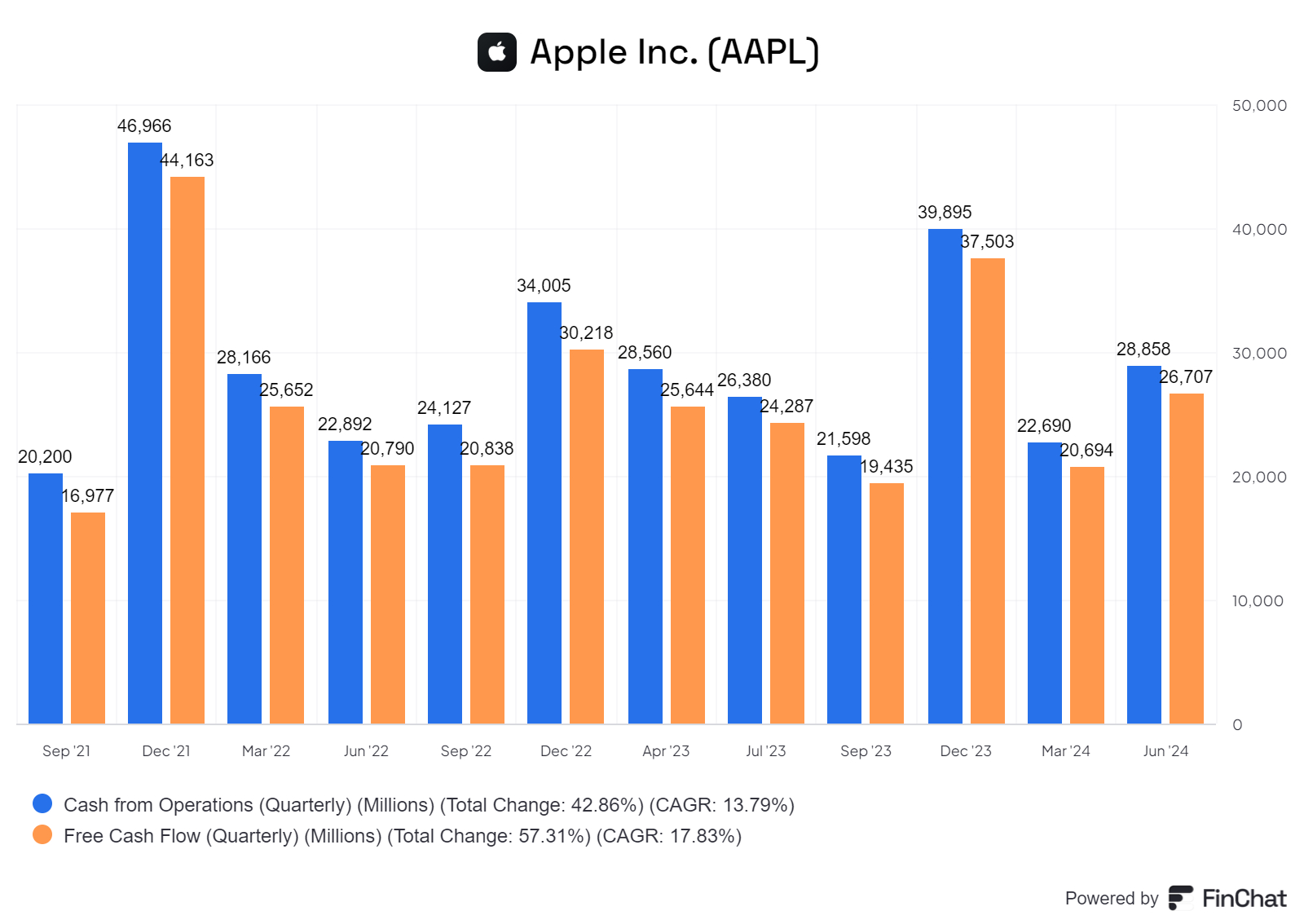

Apple, with its capital light business model and best in class products, continues to be huge generator of operating and free cash flow.

“And operating cash flow was very strong at $28.9 billion, also a June quarter record.”

Apple Intelligence and AI

Apple Intelligence is the catch-all name for Apple’s the AI capabilities, including ChatGPT4 integration coming with its imminent iOS 18 software upgrade.

“At our Worldwide Developers Conference, we were thrilled to unveil game-changing updates across our platforms, including Apple Intelligence.”

“Apple Intelligence builds on years of innovation and investment in AI and Machine Learning. It will transform how users interact with technology, from writing tools to help you express yourself, to image playground, which gives you the ability to create fun images and communicate in new ways, to powerful tools for summarizing and prioritizing notifications.”

“Apple Intelligence is built on a foundation of privacy, both through on-device processing that does not collect users' data and through private cloud compute, a groundbreaking new approach to using the cloud, while protecting users' information powered by Apple silicon.”

“We are also integrating ChatGPT into experiences within iPhone, Mac, and iPad, enabling users to draw on a broad base of world knowledge. We are very excited about Apple Intelligence, and we remain incredibly optimistic about the extraordinary possibilities of AI and its ability to enrich customers' lives.”

“We started the rollout of Apple Intelligence this week with developers, so some of the features are out there as of Monday. this will enable developers to take their apps to the next level. And so, we are taking the first step in getting the beta out there, and we can't wait to see what kind of amazing things they do with it.”

“We started with some features of Apple Intelligence, not the complete suite. There are other features like languages beyond US English that will happen over the course of the year, and there are other features that will happen over the course of the year. And ChatGPT is integrated by the end of the calendar year. it’s a staggered launch”

They are taking a dual approach to AI. They are both developing it in-house but also looking to invest in external entities.

They have announced Apple Intelligence, but they also announced partnerships with OpenAI. They have since taken a stake in Open AI, announced 29 August.

iPhone

The iPhone 15 Pro and iPhone 15 Pro Max will be the first iPhones to support Apple Intelligence. iOS 18 and iOS 18.1 (the latter will support Apple Intelligence) will be launched in the next 1or 2 months.

Here’s when the company released the previous iOS official versions:

iOS 17: September 18, 2023, in the following week after the iPhone event

iOS 16: September 12, 2022, in the following week after the iPhone event

iOS 15: September 20, 2021, in the following week after the iPhone event

Unsurprisingly, the release date of iOS 18 will be the week after the iPhone event. Apple is likely to launch its new iPhone 16 lineup in stores on Friday, September 20.

They hope that this launch, combined with Apple Intelligence in iOS18.1, will boost revenues as users upgrade frm old phones.

The iPhone 15 was releasedo on September 22, 2023, and I the current flagship range.

“Customers continue to praise the iPhone 15 lineup for its incredible battery life, exceptional cameras, and unmatched power and performance. And we are excited to bring incredible new features to the iPhone with iOS 18, making it more personal, capable, and intelligent than ever before.”

“Apple Intelligence utilizes the power of our most advanced iPhones, the iPhone 15 Pro and Pro Max, offering a transformative set of capabilities.”

If you look at the same number of weeks of the 15 from launch and compare that to the 14, the 15 is doing better than the 14.

iPad

iPad revenues were boosted by the launch of two iPad air models during the quarter. It is attracting new customers as well as replacement demand.

“During the quarter, we had an incredible launch where we unveiled the all-new 11and 13-inch iPad Air, the perfect device for education, entertainment, and so much more. And With the new iPad Pro, we pushed the boundaries of power-efficient performance with the remarkable M4 chip, the engine behind this incredibly thin device.”

“And we're very excited that iPad Pro and iPad Air models powered by the M series of Apple silicon will be able to utilize the powerful capabilities of Apple Intelligence.”

“The iPad install base has continued to grow and is an all-time high, as half of the customers who purchased iPads during the quarter were new to the product.”

Services

Services has been the one area of growth.

“…in services, we set an all-time revenue record of $24.2 billion with paid subscriptions climbing to an all-time high.”

“We achieve revenue records in the majority of the services categories with all-time revenue records in advertising, cloud, and payment services.”

“We continue to have great momentum in services, as the growth of our installed base of active devices, sets a strong foundation for the future expansion of our ecosystem.”

“And we see increased customer engagement with our services offerings. Both transacting accounts and paid accounts reach a new all-time high with paid accounts growing double digits year-over-year. Also, paid subscriptions showed strong double-digit growth.”

We have well over 1 billion paid subscriptions across the services on our platform, more than double the number that we had only four years ago.

“And we are constantly focused on improving the breadth and quality of our services. From critically acclaimed new content on Apple TV+ to new games on Apple Arcade and the many latest features we previewed during WWDC for iCloud, Apple Pay, Apple Cash, Apple Music, and more.”

Data Privacy and Data Security

“We are determined to keep our users in control of their own data. And we are just as dedicated to ensuring the security of our users' data. That's why we work to minimize the amount of data we collect and work to maximize how much is processed directly on people's devices, a foundational principle that is at the core of all we build, including Apple Intelligence.”

Outlook

“As we move ahead into the September quarter, I'd like to review our outlook…

We expect

· gross margin to be between 45.5% and 46.5%.

· OpEx to be between $14.2 billion and $14.4 billion.

· our tax rate to be around 16.5%. “

China sales

China continues to be tough markets but perhaps the worst is over.

“..we decreased by 6.5% year-over-year for the whole of Greater China. And if you look at it on a constant currency basis, we declined by less than 3%. So over 50% of the decline year-over-year is currency related. That is an improvement from the first half of the fiscal year.”

“If you look at iPhone in particular for Greater China, the installed base set a record.”

“The competitive environment there is the most competitive in the world.”

“In Mainland China, the majority of customers buying or buying for the first time, buying that product for the first time and the watch, the vast, vast majority of people are buying a product for the first time. And during the quarter, I should say also that iPad returned to growth in Greater China, as it did around the world.

DMA in EU

In June, the European Commission informed Apple of its preliminary view that its App Store rules are in breach of the Digital Markets Act (DMA), as they prevent app developers from freely steering consumers to alternative channels for offers and content.

DMA stands for Digital Markets Act, a European Union (EU) regulation that aims to make the digital economy more competitive and fairer. The DMA applies to large tech companies, which are designated as "gatekeepers"

“We have introduced some changes to the way we run the App Store in Europe already in March. And we are seeing a good level of adoption from developers on those changes. We are on an ongoing basis, discussing with the European Commission how to ensure full compliance with the DMA. It is obviously early stage, but in general, our results for the Services business and for the App Store have been pretty good until now. Percentage of revenue that we generate from the European Union on the App Store is about 7% of the total.”

Summary

As we noted in our original note, Apple is remarkable company with an unmatched ability to produce best of breed and most profitable consumer products.

It has given shareholders a 20.8% CAGR return over the last 30 years.

It has compounded its way to a current market capitalisation of $ 3.4trn- the largest company in the world.

In addition, the capital light model means the company is very capital efficient and a huge generator operating and free cash flow. In the most recent quarter, the free cash flow margin was 31.7% compared with 25% two years ago and 29% in the same quarter last year.

The iPhone is a remarkable product and a highly profitable one. However, it is a premium priced product, and it is difficult for it to gain a meaningful market share in fast growing emerging markets. The latter are characterised by value conscious customers and many cheaper (mainly Chinese) smartphone brands.

Apple has found it difficult to move the needle on its vast product revenues: these have been essentially flat in the last three years.

Services revenues are different story. Apple has taken advantage of the huge installed base of devices and new service offerings to grow revenues aggressively.

Services have grown from ~22% of revenues five years ago to ~30% now. As Services have much higher gross margins than products (~75% vs ~36%), the growth in their relative will, over the long-term, boost average margins and the profitability of Apple.

Valuation

The Apple Stock is current trading at a Forward Price to Earnings Ratio and Price to Free Cash Flow (FCF) Ratio of ~ 30X. This implies an Earnings Yield and FCF Yield of 3.3%. These numbers do not suggest the stock is at a bargain.

For the next two years the analysts are forecasting 10% growth in EPS.

Given this (modest) EPS growth and current profitability (ROIC =35.2% and ROTC= 36.6%), the multiples look more reasonable.

Conclusions

Apple is the largest company in the world and currently has an annual revenue run rate of ~$420bn.

Given its size, it is difficult for the company to grow revenues much faster than a high single digit percentage growth rate.

There may be some boosts to the growth rate when new phones are launched but consistent revenue growth above 7%-9% will be difficult to achieve.

The faster growth of more profitable services will help net profit and EPS to grow at a CAGR of ~12% to 14% over the short to medium term.

Given this scenario, and considering current levels of profitability and trading multiples, our best guess is that the stock is currently slightly overvalued.

Warren Buffett’s Berkshire Hathaway recently halved its stake in Apple, but still has a 2.63% stake worth $ 92bn.

The sale was perhaps driven by prudent risk management and a negative view of the overall market.

However, it was also probably a reflection of the value of the stock. At an FCF yield of 3.3%, it is much lower than the 6%-10% FCF yield level that Berkshire would have done most of its purchases.

We have a small legacy position equal to 1.4% of our portfolio. We will hold on to that but will not commit any more capital to Apple Inc.