Arista Networks ( ANET)

Software-driven Networking (SDN)

There was an extraordinary boom in stock prices at the end of the last century. Investors were gripped by excitement about the mass adoption of the Internet. The boom peaked in March 2000 and a huge bubble gave way to a prolonged bear market.

During this boom, Cisco briefly become the most valuable company in the world and its stock price peaked on 7th April 2000.

According to a recent article in the Financial Times:

“From the beginning of 1999 to March 2000 the shares rose 236 per cent to a market capitalisation of $555bn, or $80.06 per share, backed by a crazed enthusiasm for the technological shifts bought about by the internet. The thesis was solid: as a provider of networking equipment for both telecom players and other businesses, Cisco was the shovel-seller in a dot com gold rush. What could go wrong?”

“The problem was the share price. It was, simply, too high. At the March 2000 peak, Cisco’s price-to-earnings ratio stood at 201 times, its enterprise value to sales at 31 times and its price-to-free cash flow at 176 times. By anyone’s standards, the valuation was too high. And, suddenly, everyone realised. Over the next two years, Cisco’s share price collapsed 80 per cent, a total market capitalisation loss of $431bn, as the dot com bubble deflated and telecom capital expenditure fell with it. Twenty-odd years, Cisco’s shares are at $46.25, still 42 per cent below their dot-com peak.”

Cisco continued to grow revenues and income steadily but the last two decades have been a lost period for the shares.

Arista Networks (ANET) was formed in 2004 by a group of that included ex-Cisco employees. The current CEO, Jayshree Ullal, joined from Cisco in 2008. It was listed in 2014 and was a direct competitor of Cisco, Alcatel Lucent and Juniper Networks which were giant companies at the time.

Arista was founded by Andy Bechtolsheim, Ken Duda, and David Cheriton.

Andy Bechtolsheim is a legendary figures in Silicon Valley. He is a co-founder of Sun Microsystems.

David Cheriton is a Canadian computer scientist, businessman, philanthropist, and venture capitalist. He is a computer science professor at Stanford University where he founded and leads the Distributed Systems Group.

David Cheriton co-founded Granite Systems with Andy Bechtolsheim. The company developed Gigabit Ethernet products and was acquired by Cisco Systems in 1996.

Sergey Brin and Larry Page, the founders of Google, were Cheriton’s PhD students at Stanford. Cheriton and Bechtolsheim were the first investors in Google and committed their capital before it was even incorporated.

Ken Duda was the first employee of Granite Systems and was also a student of Cheriton at Stanford.

Andy Bechtolsheim is currently the Chief Development Officer while Ken Duda is the Chief Technology Officer at Arista Networks.

Andy Bechtolsheim owns 15% of Arista, a stake currently worth ~US$ 7bn.

Jayshree Ullal is the CEO of Arista Networks. She worked for Cisco systems for 15 years before joining Arista in 2008 as CEO and President. She has a 3.3% stake in Arista which is currently worth US$ 1.3 bn.

In a 2018 interview, Bechtolsheim said he was inspired to start Arista after a lunch with Sergey Brin of Google where the latter described that Google’s then ~100,000 servers could not be networked efficiently using existing technologies. Google was considering developing their own networking solutions.

In 2012, Arista Networks had a tiny market share of 3.5% while Cisco was the dominant player at 78.5%. Today the equivalent figures are about 25% and 36% respectively. Arista has grown strongly and gained significant market share over the last decade.

How have they done it?

CEO Jayashree Ullal gave an interview in 2012 when the company was still private which is worth listening to and can be found here or click below. The interviewer expresses some scepticism as to whether the established giants of the day, Cisco, Alcatel, Lucent and Juniper Networks would allow a gap big enough for Arista to thrive (it is at about 2 minutes 30 seconds).

In response, Ullal says they have a deep focus on the Cloud and their approach emphasises software. She notes they spent five years (2004-2009) developing a software for Cloud networks.

That software is called Extensible Operating System (EOS).

At the time, networks were growing in importance with the growth of the internet, the acceleration in e-commerce and the advent of the Cloud. Amazon was showing the potential of both e-commerce and the Cloud.

Client-to-cloud networking represented a fundamental shift from traditional legacy network architectures. As organizations of all sizes have moved workloads to the Cloud, spending on cloud and next-generation data centers has increased rapidly, while traditional legacy IT spending has grown more slowly.

Most consumer applications today are delivered as cloud services. Cloud-hosting was powered by the likes of Amazon, Microsoft, Google IBM and Oracle. They pioneered the development of large-scale cloud datacentres in order to meet ever-growing user demand. Netflix, for example, could not have operated and scaled the way it did without Amazon Web Services (AWS).

Enterprise applications are rapidly moving to the Cloud as cloud services are easier and more cost effective to deploy, scale and operate than traditional applications. Enterprises and service providers around the world are adopting cloud computing technologies in order to achieve better performance, operational efficiencies and cost reductions.

The new large scale networks needed to allow real-time communications at scale. Networks have to be Resilient and have great efficiency and low Latency.

Resilience refers to the ability of a network to continue operating in the event of a failure. This can be caused by a variety of factors, such as hardware failures, software errors, or natural disasters.

Latency is the time it takes for a data packet to travel from one point to another. It is measured in milliseconds (ms). It depends on factors such as the distance between the sender and receiver, the type of network infrastructure, and the amount of traffic on the network.

Low latency is critical for applications that require real-time communication, such as online gaming, video conferencing, and financial trading. High latency can cause these applications to lag or become unresponsive.

Some of the earliest customers for Arista were financial trading firms who wanted to upgrade their networks to support High-Frequency Trading (HFT) which was was growing strongly at the time. A key early Arista client in this space was Lehman Brothers. Unfortunately, they went out of business in 2008. However, financial institutions were the most important group of customers for Arista until the Cloud hyperscaler demand picked up strongly around 2014.

Networks should have no downtime (they should not go down even for a few seconds - think of high-frequency trading, stock exchanges or Netflix and how disruptive an outage would be) and have no discernible lags.

EOS was specifically designed to tackle these and other issues. EOS is a scalable network operating system (OS) that offers high availability, streamlines maintenance processes, and enhances network security. EOS is described as containing a multi-process state-sharing architecture provides for fault containment, so that when problems occur in one part of the network, they will not easily spread to other parts. In addition, programmes can in effect heal themselves when bugs or malware cause problems.

According to Arista, EOS offers a unique opportunity improve the functionality and evolution of next-generation datacentres. EOS has the following five key capabilities and benefits.

In-Service Software Upgrade (ISSU) reduces maintenance time by allowing updates to take place without interrupting the system.

Software Fault Containment (SFC) prevents problems from spreading beyond the modules in which they first occur.

Stateful Fault Repair (SFR) watches over the health of all system processes and resolves problems without disruption, often without users noticing.

Security Exploit Containment (SEC) detects vulnerabilities and confines them to the modules in which they originate.

Scalable Management Interface (SMI) facilitates automated system maintenance and updates.

The EOS is built on the Linux kernel, and offers open access to Linux tools and network services. It is not a closed garden. It can be programmed using standard scripting languages, such as Python and Ruby. This allows users to customize EOS for their specific needs.

EOS is designed to be easy to use, with a simple and intuitive command-line interface. This makes it easy for network administrators to manage and troubleshoot.

EOS has proved to be a significant competitive differentiator, delivering ease, speed and agility of application and service provisioning. As the foregoing makes clear, Arista is primarily a software rather than a hardware company. In the 2018 interview, Andy Bechtolsheim noted that 90% of their R&D resources are devoted to software not hardware.

What does Arista do?

Arista Networks is a supplier of cloud networking solutions that use software innovations to address the needs of Internet companies, cloud service providers, enterprises, and datacentres.

It offers

EOS Software

a set of network applications

Ethernet switching and routing platforms.

Arista designs revolutionary products in California. These are built by contract manufacturers in Asia and delivered by Arista to customers worldwide through distribution partners, systems integrators and resellers with a strong dedication to partner and customer success.

Switching and Routing

Let us start with a basic question. What is Switching and Routing?

A Google search resulted in the following:

“While a network switch can connect multiple devices and networks to expand the LAN, a router will allow you to share a single IP address among multiple network devices. In simpler terms, the Ethernet switch creates networks and the router allows for connections between networks.”

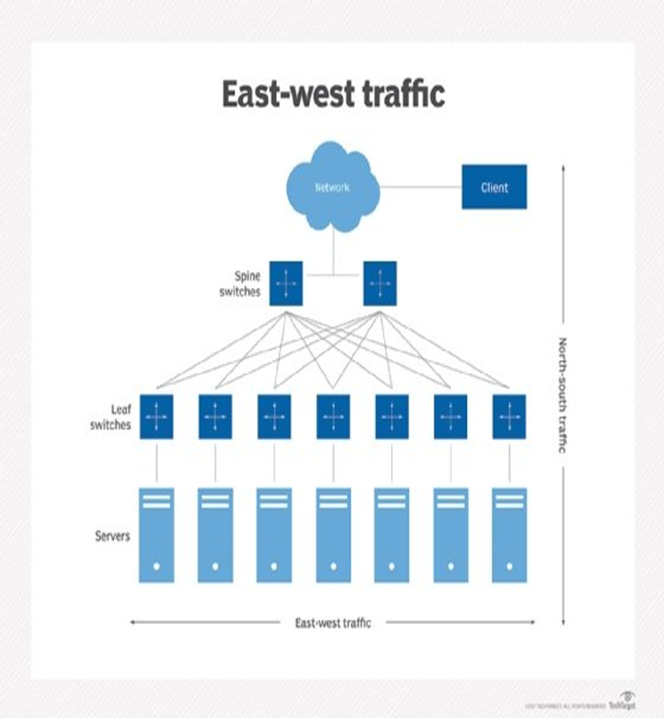

The diagram below shows a simplified, stylised picture of a Network. It shows that switches create networks and router enable networks to talk to each other.

Switches and Routers

The Switches and Routers range in speeds from 10-800 gigabits per second.

Arista Switches and Routers

Arista has outperformed Cisco in terms of market share for several reasons, including:

Cloud computing. Arista Networks has focused on developing products and solutions for cloud computing environments. This has given the company a significant advantage over Cisco, which was been slower to adapt to the cloud.

Open architecture. Arista Networks uses an open architecture for its products, which makes them more flexible and easier to integrate with other systems. This has been a major selling point as customers are looking for ways to simplify their networking infrastructure.

Software-driven networking. Arista Networks is a software-driven networking company (SDN), which means that its products are designed to be managed and configured through software (principally EOS). SDN has made Arista Networks' products easier to use and manage.

Performance and scalability. Arista Networks' products are known for their high performance and scalability. This has made them a popular choice for large-scale Cloud deployments.

Arista Networks' products are more cost-effective than Cisco's. Arista Networks uses merchant silicon, which is less expensive than Cisco's proprietary silicon. This has allowed Arista Networks to offer its products at a lower price point, which has been a major factor in its success. This is discussed further below.

Arista Networks has a strong partner ecosystem. The partners provide support and services for Arista Networks' products, which has made it easier for customers to adopt Arista Networks' products. This is discussed further below.

One metric for tracking Arista’s growth is the number of ports. In 2008, Arista had 1500 ports and this had reached 1mn in 2018. Today that has grown to 75mn. This means their products are connected to over 75 million physical ports on customer networks. A port is a physical or logical endpoint on a network device that allows data to be transmitted and received. In Arista Networks' case, the ports are typically on their switches, which are used to connect computers and other devices together on a network.

The number of ports served is not a static number. It is constantly changes as new customers adopt Arista Networks' products and as existing customers add more ports to their networks.

80% of Arista’s revenues come from North America so there should be considerable scope for growing non-US Revenues.

This market can also be sliced in terms of business verticals. These are

Cloud Hyperscalers

Enterprise

Specialist Cloud Providers

Financials and

Service Providers

In 2022, the Cloud hyperscalers accounted for 46% of revenues. Enterprise and financials together was strong at approximately 32%, while the providers were at approximately 22%. Meta and Microsoft were at 25.5% and 16% contribution respectively.

The Cloud exists physically in large Datacentres.

Definition: A datacentre is a physical facility based on a network of computing and storage resources that enable the delivery of shared applications and data. The key components of a datacentre design include routers, switches, firewalls, storage systems, servers, and application-delivery controllers.

This YouTube video visits he world’s largest Datacentre complex at Tahoe in California which is a campus of Datacentres covering 17.4mn square foot.The largest single unit is 1.2mn square foot which cost $3bn. It gives some idea of what datacentres are all about.

Microsoft and Meta combined represent 40% Arista’s total revenue. Both are currently making huge investments which has been positive for Arista Networks. Historically, large purchases by a relatively limited number of end customers have accounted for a significant portion of their revenues. Customer concentration means they have some leverage over the supplier. Arista admits that with respect to large customers they “typically provide pricing discounts to large end customers, which may result in lower margins for the period in which such sales occur.”

One key reason for Arista’s overall success is they recognised early on that cloud networks and legacy networks are fundamentally different. In particular, the former requires much more bandwidth.

In a traditional datacentre, specific applications are installed on a small number of servers and most network traffic is server-to-client, or “north-south” traffic, which results in perhaps a few terabits/second of aggregate network bandwidth. A terabit is a measurement for 1 trillion bits or pieces of binary data.

In the cloud, most network traffic is server-to-server, or “east-west” traffic. The aggregate network bandwidth in the cloud can exceed 1 petabit/second, orders of magnitude higher than that of typical legacy datacentre networks. A petabit a unit of information equal to 1000 terabits.

In cloud computing, applications are distributed across thousands of servers. These servers are interconnected by high-speed networking switches to form a pool of resources that allows applications to be rapidly deployed and cost-effectively updated. Cloud computing enables ubiquitous and on-demand network access to these applications from internet-connected devices including personal computers, tablets, Internet of Things (IoT) devices, and smartphones. Cloud networks are larger and more complex than traditional networks.

The much larger scale of cloud networks requires much higher network availability since network outages in the cloud are costly to customers.

Traditional network switches have evolved, and the features and capabilities of their operating system have expanded over many years without addressing the structural deficiencies of their underlying software architectures, making it difficult to achieve high network switch reliability.

Some networking vendors have built products that use proprietary protocols to address the scaling needs of next-generation datacentres. However, proprietary protocols are generally not favoured by internet companies or cloud service providers as they create vendor lock-in. The risk for the customer is they get stuck in a permanent relationship with a provider of proprietary software and hardware.

Legacy enterprise networks are generally not programmable and, as a result, are extremely difficult to integrate with third-party applications for network management, automation, orchestration and network services.

This lack of integration forces customers to continue to rely on time-consuming, error-prone manual processes that may be cost-prohibitive.

The programmability of EOS has allowed Arista to expand their software applications to address the ever-increasing demands of cloud networking, including

workflow automation,

network visibility,

analytics and

network detection and response, and

has further allowed them to integrate rapidly with a wide range of third-party applications for

virtualization, management, automation, orchestration and network services

Today’s networks do not just have fixed desktop computers as the endpoint. Mobile devices such as tablets and phones as well as connected, intelligent machines (Internet of Things (IoT) ) outside the premises have to be incorporated as well. The complexity is many times higher relative to legacy networks.

Network administrators have sought to address the resulting increased network complexities and bottlenecks through the adoption of a myriad of platforms, operating systems, proprietary features and network management tools. The operational costs of managing these complexities have become prohibitive.

In recent years, there has been huge growth in infrastructure spending on the Cloud. Cloud inter-datacentre traffic is growing at 50% plus per annum and has been a strong tailwind for Arista’s business.

Network architectures

We need to talk about Network architectures because Arista and the security analysts covering Arista talk a lot about it. Traditional networks have three layers. Modern networks take out a layer and have only two switching layers – called a spine and a leaf.

The spine-leaf architecture was first pioneered by Cisco Systems in the early 2000s. Cisco called this "Fabric Architecture" and it was quickly adopted by other companies including Arista.

Traditionally, data center networks were based on a three-tier model:

1. Access switches connect to servers

2. Aggregation or distribution switches provide redundant connections to access switches

3. Core switches provide fast transport between aggregation switches, typically connected in a redundant pair for high availability

A spine-leaf architecture collapses one of these tiers, as depicted in these diagrams above.

The leaf layer consists of access switches that aggregate traffic from servers and connect directly into the spine or network core.

Spine-leaf architectures have become very popular

As noted above, East-west traffic moves laterally, from server to server. East-west traffic requires low-latency and optimized traffic flows especially for time-sensitive or data-intensive applications. A spine-leaf architecture aids this by ensuring traffic is always the same number of hops from its next destination, so latency is lower and predictable.

Capacity is also better in spine-leaf architecture. EOS software enables enterprises to provide networking resources in minutes with no manual intervention through Zero Touch Provisioning (ZTP)

Definition: ZTP is a method of setting up devices that automatically configures the device using a switch feature. ZTP helps IT teams quickly deploy network devices in a large-scale environment, eliminating most of the manual labour involved with adding them to a network.

CloudVision.

Arista has developed a software product called CloudVision which is a network-wide approach for workload orchestration and automation. It delivers a turnkey solution to enterprises looking to modernize to their datacentres to spine-leaf architecture for cloud networking.

Companies and organisations can move to cloud-class automation without needing significant internal development thanks to CloudVision.

Arista believes that the CloudVision networking platform offers architectural and system advantages that provide their customers with cost-effective and highly available cloud networking solutions.

CloudVision is part of Arista’s larger move to targeting companies’ and institutions’ networking needs, which is a diversification away from the Cloud Titans. They call this the “Cognitive Campus Workspace” illustrating the jargon all too prevalent in the sector.

The Arista data-driven cloud networking platform enables datacentre networks to scale to hundreds of thousands of physical servers and millions of virtual machines with the least number of switching tiers. They achieve this by leveraging standard protocols, non-blocking switch architectures and EOS to meet the scale requirements of cloud computing, including AI workloads.

Best of Breed Merchant Silicon

A datacentre network switch require a particular type of chip called an ASIC which stands for Application-Specific Integrated Circuit.

Definition: ASIC is a kind of integrated circuit that is specially built for a specific application or purpose.

There are two ways for the Networking company to procure the ASIC: Custom Silicon and Merchant Silicon.

Custom Silicon are chips that are custom designed and usually built by the company selling the switches in which they are used. This is broadly Cisco’s approach .

Merchant Silicon is a term used to describe chips are designed and made by an entity other than the company selling the switches in which they are used. Merchant Silicon was pioneered by Arista Networks. They source chips from outside vendors for their switches, particularly from Broadcom.

Arista’s claims the use of best-of-breed merchant silicon that enables open standards-based networking with rapid time-to-market. Most other networking companies have since moved to Merchant Silicon. Even Cisco has made a partial shift.

Let us look at the historical financial performance of the company before considering its business prospects and the nature of the case for investing in the in the stock.

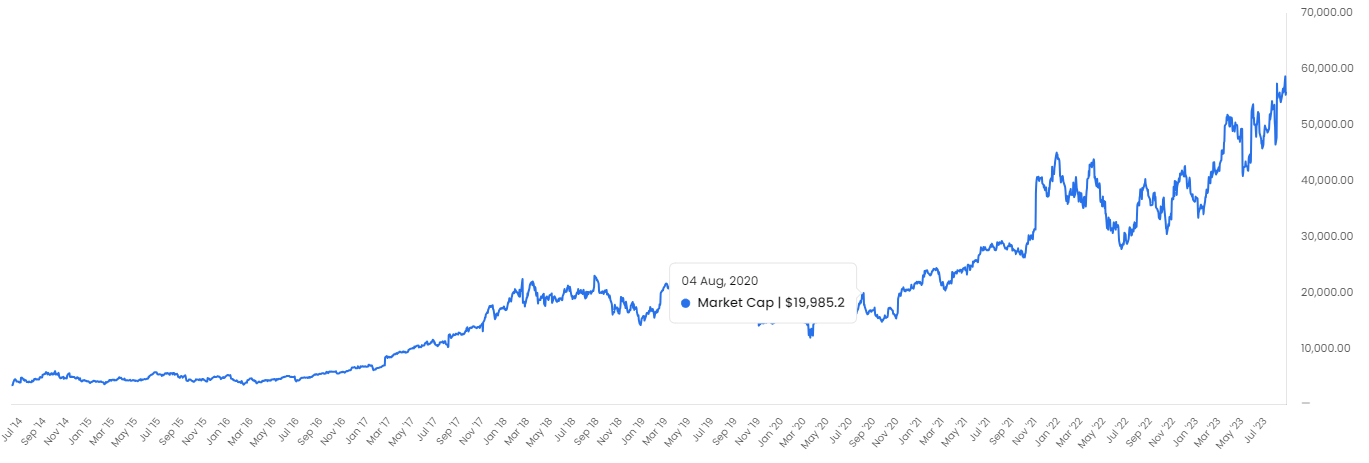

Chart 1 - Arista Networks Stock Price since the IPO

Source : Stratosphere.Io

Since the IPO in Jun 2014, Arista Networks has given a CAGR return of 31.9%. This compares with a CAGR of 27% for Copart Inc and 23% for HEICO over the same period. These are two companies on our watchlist that we have written about recently.

Chart 2 - Arista Networks Market Capitalisation since the IPO.

Source : Stratosphere.Io

Since the IPO in Jun 2014, Arista Networks’ market capitalisation has risen by a CAGR of 34.7%. This is more than the shareholder return due to the issuance of shares during the period.

Chart 3 - Cisco Systems and Arista Networks stock price performance since the Arista Networks IPO.

Source : Stratosphere.Io

Since 2014, Arista Networks share has risen 12.3X. Over the same period Cisco has risen just 2X.

Chart 4 - Arista Networks Total Revenue and Total Revenue Growth.

Source : Stratosphere.Io

ANET Revenues have risen 12 times between 2013 and 2022 to $ 4.4bn. There was negative growth in 2020 due to the global pandemic but it has recovered strongly since then.

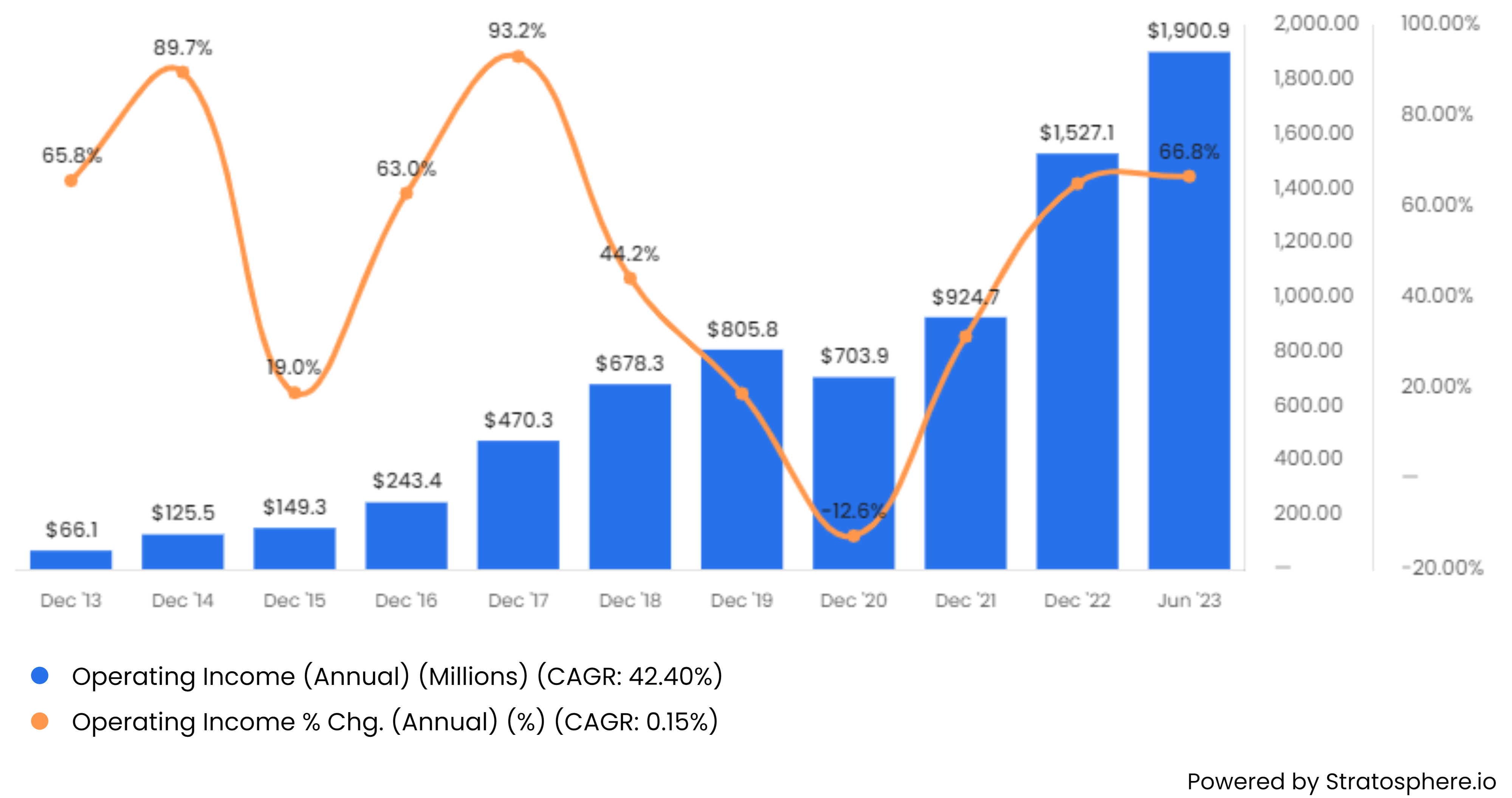

Chart 5 - Arista Networks Operating Income and Operating Income Growth.

Operating Income has risen 28 times since the IPO at a CAGR of 42.4%. This is an impressively high rate of growth sustained over a decade.

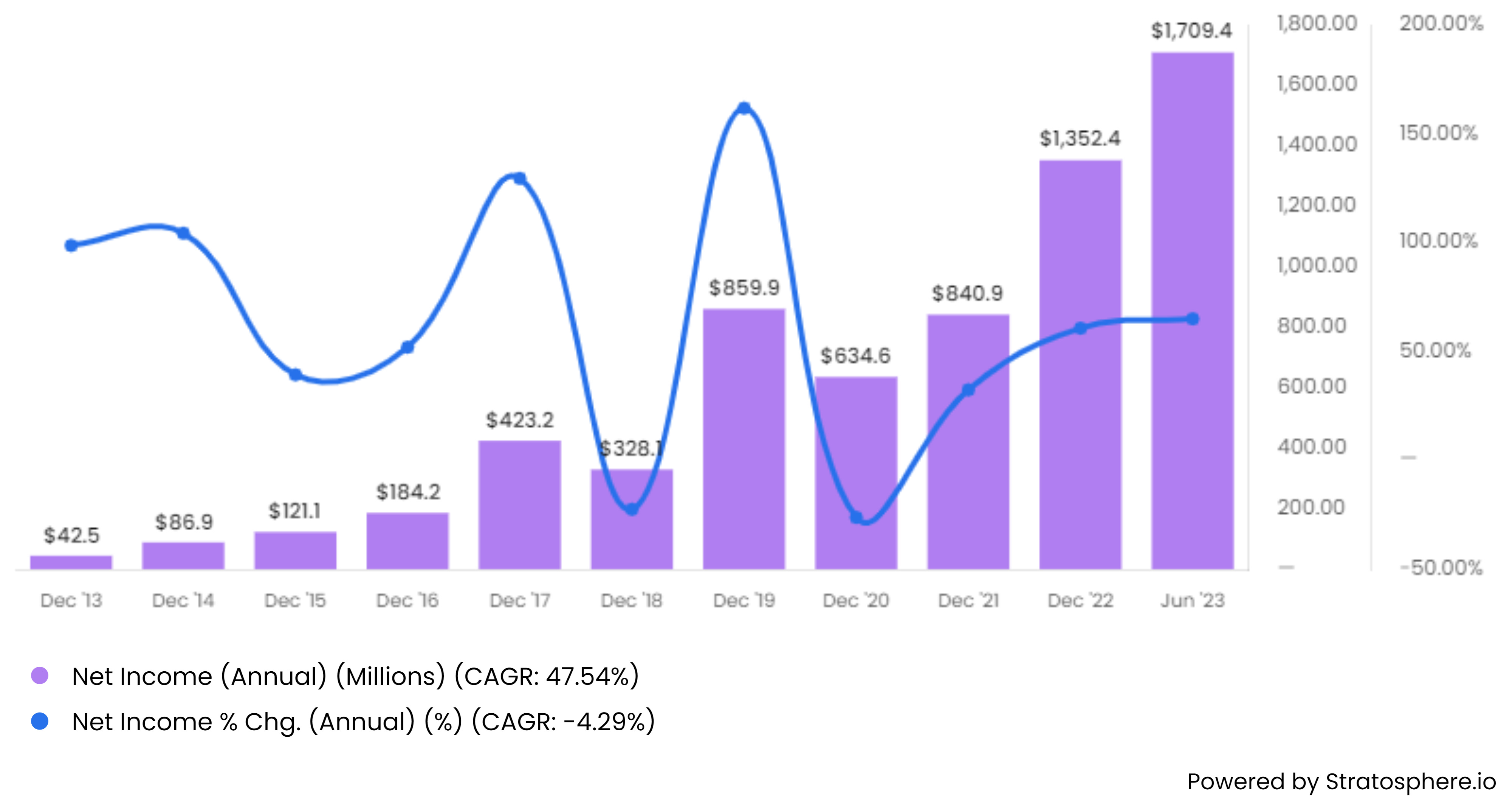

Chart 6 - Arista Networks Net Income and Net income Growth

Net Income has grown 21 times between 2013 and 2023 or a CAGR of 47.54% .

Chart 7 - Arista Networks Earnings Per Share (EPS) and EPs growth.

Source : Stratosphere.Io

EPS growth CAGR has been 42.7% compared with Net Income CAGR of 47.5% which suggests a 500bps p.a. dilution per year, perhaps due to stock-based compensation. Note the 60% growth in EPS in 2022.

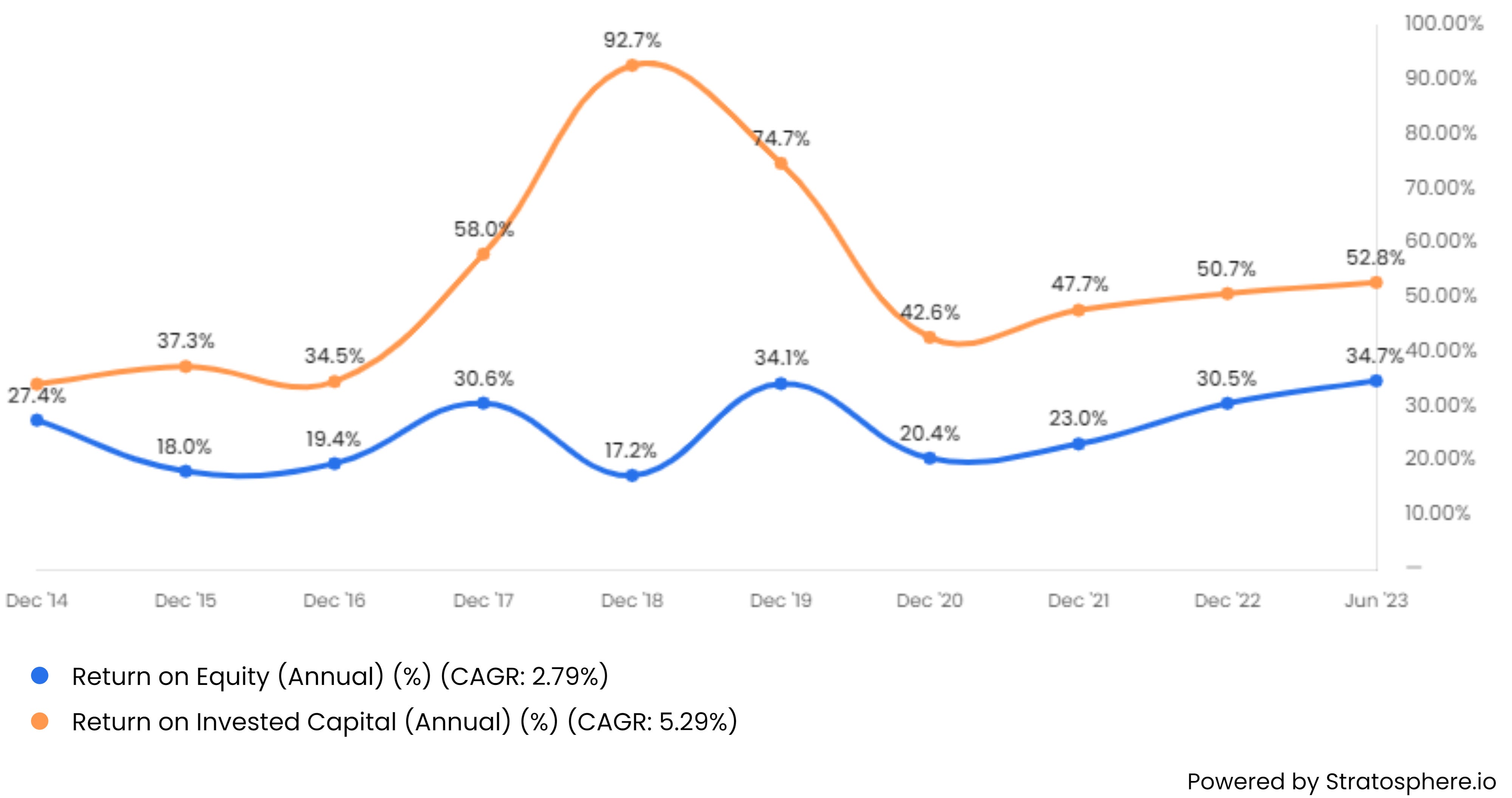

Chart 8 - Arista Networks Gross, Operating, Net Profit Margins and ROE/ROIC

Source : Stratosphere.Io

Gross Margins are at 60% while Operating Margins have doubled to 36%

Return on Equity (ROE) has been ~30% to 35%.

Chart 9 - Arista Networks Cash from Operations and Free Cash Flow.

Source : Stratosphere.Io

Cash from Operations and Free Cash Flow have increased steadily.

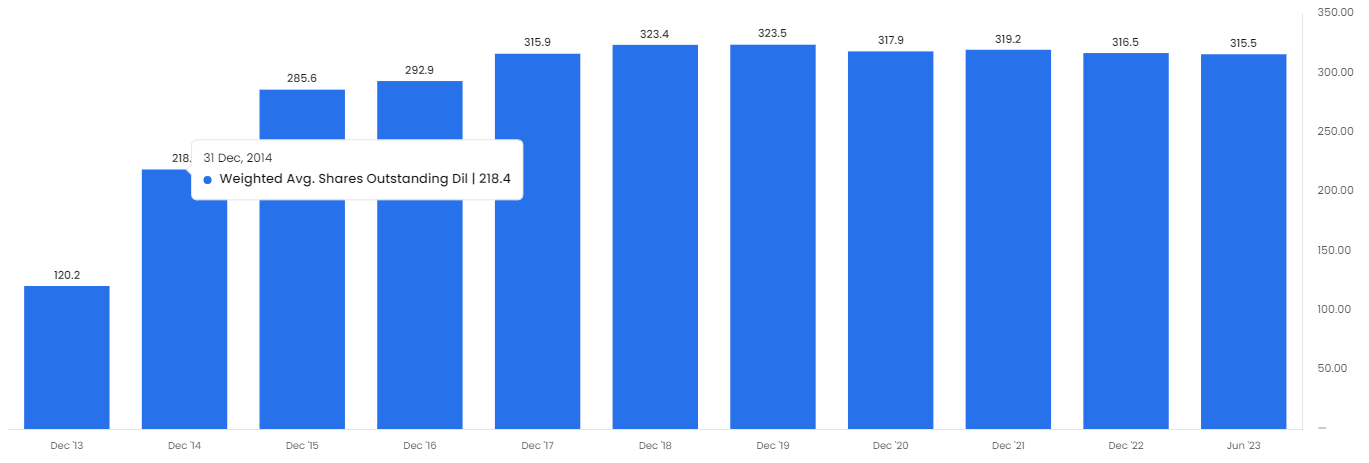

Chart 10 - Arista Networks Weighted Average Shares outstanding (million)

Source : Stratosphere.Io

It is disappointing that the total number of shares outstanding has not declined over the last six years.

Chart 11 - Stock-based Compensation (SBC) in absolute terms (US$ millions) and SBC as a percentage of revenue.

Source : Stratosphere.Io

Stock-based Compensation has risen sharply and currently accounts for ~5% -6% of Revenues. Given ~30% net income margin, SBC amounts to ~ 15% of net profits. It looks on the high side. Most technology companies have high SBC and investors who do not like it have little choice except to refuse to invest in the sector.

Chart 12 - Arista Networks - US$ value of stock purchased by company (US$ Millions)

Source : Stratosphere.Io

The numbers are shown as negative as stock buybacks involve an outflow of cash. A significant amount of shareholders cash is spent to buy back shares but the number of shares outstanding do not fall due to new shares issued under Stock-based Compensation (SBC) or to pay of acquisitions.

“During the year ended December 31, 2021, cash used in financing activities was $360.9 million, consisting primarily of payments for repurchases of our common stock of $411.6 million and taxes paid of $16.5 million upon vesting of restricted stock units, offset partially by proceeds from the issuance of common stock under employee equity incentive plans of $67.2 million.”

Chart 13 - Arista Networks - Current Assets and Current Liabilities (US$ Millions).

Source : Stratosphere.Io

Current assets are much greater than current liabilities. In addition, the company has no long-term debt, so the balance sheet is very strong.

Chart 14 - Arista Networks - Total Value of Inventory and Day inventory outstanding.

Source : Stratosphere.Io

Inventories increased sharply in 2022. We need to investigate the reason for this (see below).

Chart 15 - Arista Networks - Total Assets and Total asset growth.

Source : Stratosphere.Io

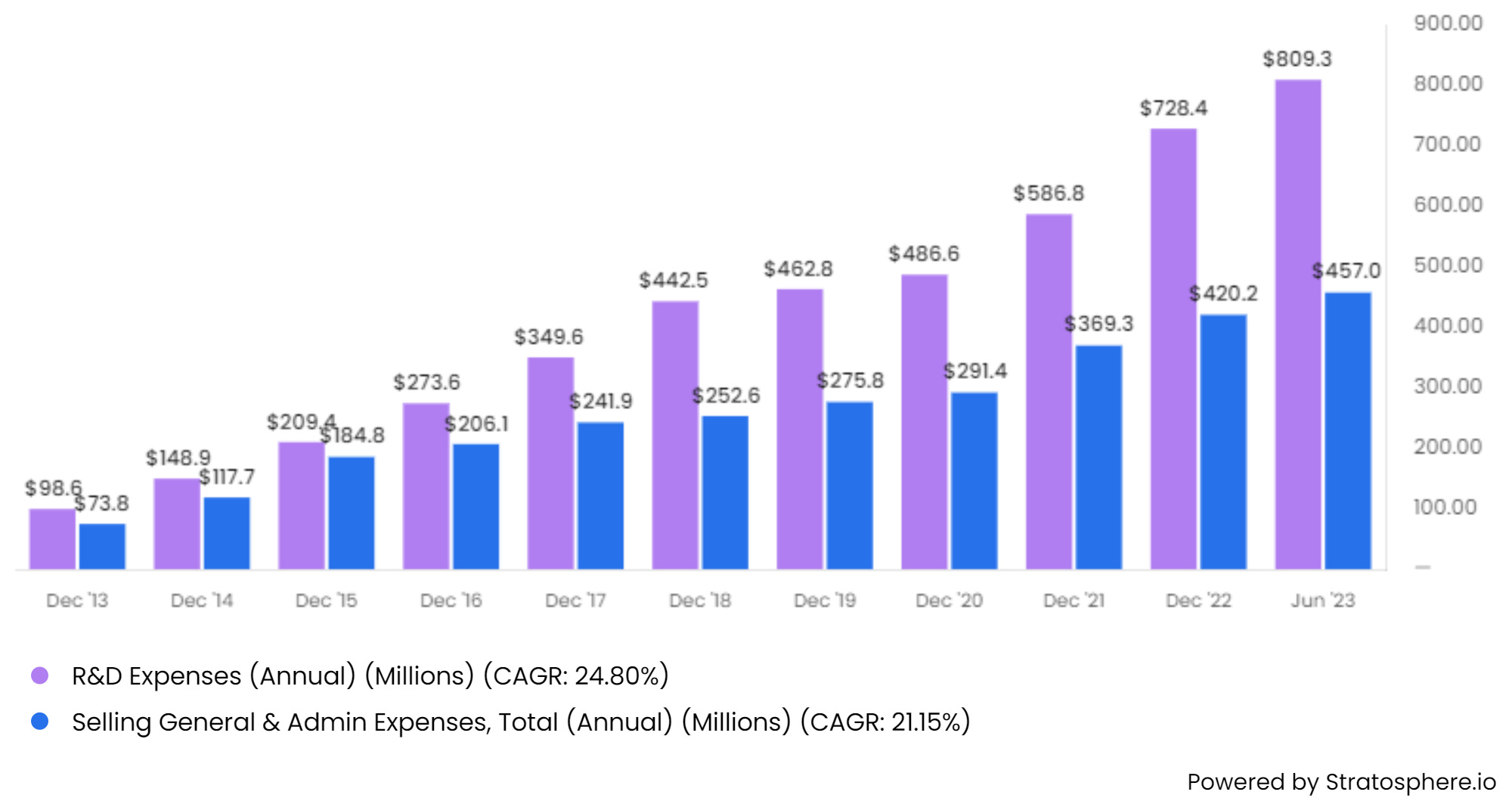

Chart 16 - R&D Expenses and Total Selling General and Admin expenses.

Source : Stratosphere.Io

Operating expenses grown by ~ 23% CAGR much less then CAGR in Revenue (32.7%) and Gross Profit (31.3%) suggesting some significant operating leverage.

Strategic Acquisitions

Arista has a strategy of organic and inorganic growth. They have made a number of small acquisitions to acquire critical technologies in key areas relating to their existing business. Details of their recent acquisitions are given below:

Mojo Networks (August 2018). Mojo Networks was a provider of wireless LAN (Local Area Network) solutions for the enterprise market. Mojo Networks is the inventor of Cognitive WiFi and Arista extended these same cognitive principles to the wireless network. The acquisition gave Arista a foothold in the wireless networking market and expanded its portfolio of products and services.

Metamako (September 2018). Metamako was a provider of low-latency networking solutions. The acquisition gave Arista a technology that could be used to improve the performance of its switches in high-performance computing and financial trading environments.

Big Switch Networks (February 2020). Big Switch Networks was a provider of software-defined networking (SDN) solutions. Their capabilities have been integrated with the Arista switching portfolio to power the DANZ Monitoring Fabric (DMF), a leading network monitoring solution. The acquisition gave Arista a leading position in the SDN market and expanded its portfolio of software-based networking products and services.

Awake Security (September 2020). Awake was a provider of network detection and response (NDR) solutions. They believe the combination of DMF and Awake Security capabilities delivers the next generation of operationally efficient network security and visibility.

Pluribus Networks (August 2022). Pluribus Networks was a provider of unified cloud networking solutions. The acquisition gave Arista a technology that could be used to simplify and automate the management of cloud networks.

These acquisitions have helped Arista to expand its product portfolio, strengthen its market position, and improve its offerings in key areas such as wireless networking, low-latency networking, SDN, security, and cloud networking.

These acquisitions have been in related areas and are believed to have been relatively small. The table below shows the cash paid out for acquisitions. The blue bars are shown as negative as they represent a cash outflow. To the extent that Arista Shares have also been used to pay for acquisitions, these numbers will tend to underestimate the cost of the acquisition.

Arista continues to invest in R&D to improve its hardware, software and services offerings. We noted the growth in R&D spending (above) and much of that is accounted for by the cost of employing software engineers.

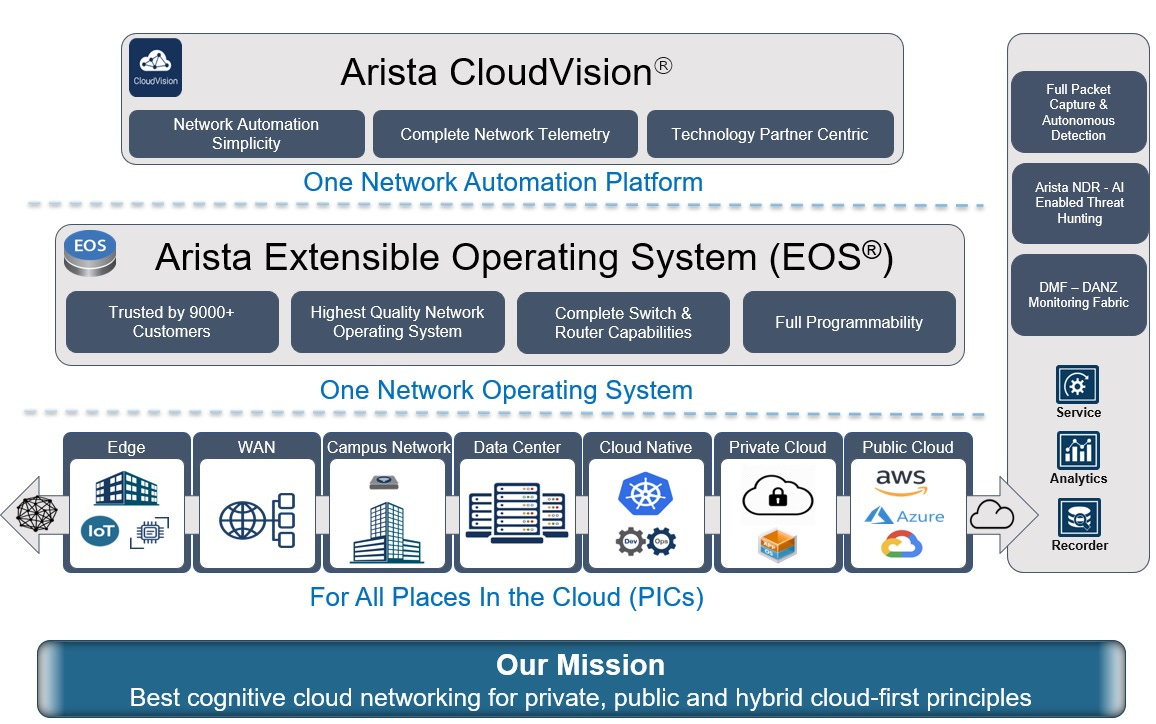

EOS

Arista has said that EOS is a “highly complex and sophisticated operating system" with "millions of lines of code". It has been developed over 15 years and represents a major asset for the company. We discussed it in detail above.

As can be seen in the diagram above, EOS is at the very centre of the Arista offering.

CloudVision is a Network Automation Platform that sits above EOS and gives users to easily view, monitors and control the entire network using full telemetry.

At the lowest level are the various aspects of the individual organisation’s connected network starting with the edge on the left (IoT devices, mobile phones and tablets) to the wireless network(WAN) and all the way to the Public Cloud on the right. A very large company many have all of these elements, a small company many just have the edge and a WAN.

Definition: Telemetry is the automatic measurement and wireless transmission of data from remote sources. Sensors at the edge measure and record and send data to CloudVision which provides users with an aggregate view.

Arista started targeting non-Cloud business such as companies, institutions and governments in a big way three years ago. These entities are under great pressure to move workload to the Cloud and they need to upgrade their networks so they are compatible with and able to integrate with the Cloud.

Arista’s strategy is to use the solutions they have developed in the Cloud to disrupt the wasteful, oversubscribed legacy three-tier architecture in companies, government and academia. They claim their approach reduces operational costs by incorporating a network that is a seamless end-to-end solution rather than silos of different places in the network.

Their solution is marketed as CloudEOS

CloudEOS is a multi-cloud and cloud-native networking solution enabling a secure and reliable networking experience with consistent segmentation, telemetry, provisioning and troubleshooting for the entire enterprise.

Many companies want to put some of their workloads on the Cloud but wish to retain some mission-critical workloads on in-house infrastructure and network. Some large companies do not wish to become dependent on just one cloud hyperscaler and may distribute the work to more than one of them. It might give, say IAAS workloads to Amazon AWS but AI workloads might go to Microsoft Azure or Google Cloud Platform (GCP). Therefore, such Clients need multi-cloud or hybrid networks which may combine Cloud, Campus, WAN and LAN.

CloudEOS can be deployed across the enterprise edge, WAN, campus workspace, data center and multiple public and private clouds.

CloudEOS provides multi-cloud connectivity across the entire enterprise cloud environment with high-performance.

With CloudEOS and CloudVision, customers can integrate their cloud network deployments with the elasticity and automation of the public cloud, private cloud and cloud native platforms.

Manufacturing

Arista designs the Switches, Routers and other related equipment in Southern California but subcontracts the manufacturing of all products to contract manufacturers in Asia. The main manufacturing partners are Jabil Circuit, Sanmina Corporation, Flex Ltd. and Foxconn Hon Hai. They also work for other large US companies such as Apple and many others.

Arista runs four direct fulfillment facilities worldwide to hold finished goods inventory, perform product inspections and transformations before shipping software to customers and partners.

Contract manufacturing partners procure the majority of the components needed to build products and assemble products according to Arista’s design specifications. This allows Arista to leverage the purchasing power of the manufacturers.

Arista retains complete control over the bill of materials, test procedures and quality assurance programs

Strategic partners

Arista works closely worth a number of partners and collaborators. These include companies like Microsoft, VMware, Red Hat (IBM), Equinix, Palo Alto Networks, ServiceNow, Slack, Splunk, Zscaler, and Zoom. The partners provide key technology capability or access to potential customers.

Competitors

Cisco and Juniper networks are big competitors. Others include Extreme Networks, Dell/EMC , Hewlett Packard Enterprise and Nvidia (in networking).

Overview of current trends

2022 was a very strong year for Arista Networks. Revenue and Net Profits grew 48% and 60% respectively. The numbers would have been even better had Arista not faced significant supply chain issues which led to poor availability of products.

The growth was driven by much greater demand from the Cloud Titans, especially Microsoft and Meta Platforms (formerly Facebook). The share of revenue accounted for by Cloud Titans rose from 30% to 46%.

This reflects the huge metaverse investments made by Meta and the ongoing Azure investments by Microsoft. Meta capex in 2022 was a record $ 30bn while MSFT was a record $ 23bn.

2 key things follow from this.

2023 will be a difficult comparator especially in the last three quarters of that year. At this stage the company is guiding to 30% revenue growth in 2023 overall which is better than the 25% forecast at the November 2022 Analyst day.

The exposure to Cloud hyperscalers is quite high and Arista needs to diversify away from them by boosting other demand especially from Enterprise

Enterprise

In the last decade, Arista has grown mainly on the back of datacentre demand due to the fast growth of Cloud Networks. Arista only started looking at the Enterprise market seriously in the last three years. An important enabler was the 2018 takeover of Mojo Networks, noted above, which gave them expertise in wireless networks and LAN which would be of interest to even the smallest company.

In earnings conference calls one or two years ago, Arista used to say their penetration of the enterprise market was so small, that it was not meaningful to talk about market share. In the last two calls they have been talking about stronger momentum in the enterprise business.

“Considering this is only our third full year of shipping versus incumbents who have been in the market for 15 to 30 years, we are very proud of our execution. Our vision for a cognitive campus with network-as-a-service and edge-as-a-service based on NetDL is resonating extremely well and being embraced by our campus customers.”

“Our (enterprise) customers are really looking for consolidation of their data centers in terms of better automation, better telemetry, better consolidation of their operational advantages in the data center.”

“Our enterprise customers are really looking for an alternative to what they have got. There is a lot of fatigue in the system. And what’s driving my optimism, where there is backlog from prior demand or present demand, is they are really hungry, and Arista presents that alternative.”

Enterprise demand has driven demand for CloudVision. “We are proud to note that CloudVision exceeded 2,000 cumulative customers, up from 1,500 the prior year and is really a compelling data-driven platform delivering network agility, continuous integration and operational excellence.”

“In the non-cloud category, we have registered solid number of million-dollar customers as a direct result of our momentum in the enterprise and campus throughout the year.”

The strategy in Enterprise initially is to go to the existing 9000+ customers they have been working with in the Cloud to see if there is scope to work with them in their Premises/ Campus networks. In the second stage, they will develop a strategy for targeting SMEs.

“Well, in the near-term, our go-to-market has very much been to target our 9,000 cumulative customers. But we are building a mid-market strategy. We are going to work closely with channel partners. Those things take time. So, I would say our initial go-to-market is our enterprise customers. And over time, we will have a more mid-market strategy.”

They believe that as a result of a focus on companies, the total addressable market (TAM) will be US$ 50bn in 2027 compared with an estimated TAM of US$ 30bn three years ago. This compares with a current, annual, revenue run rate of about $ 5bn.

“We are uniquely qualified to bring modern software principles to build that world-class data center and data-driven networking. We maintain our campus momentum and are aiming for $750 million in revenue by 2025.”

We believe the forecast for $ 750mn of campus revenue by 2025 looks conservative and will be increased at the Analysts Day in November 2023

Inventories

In 2022 they experienced constraints, with some lingering component shortages, extended lead times, and elevated component and supply chain costs. They have worked with manufacturers to ramp up production. Inventories have risen in H1 2023 as new purchase commitments have been honoured as supply constraints have eased.

“we have worked diligently to drive improvements in these areas, including funding additional working capital and incremental purchase commitments, these delays have negatively impacted our ability to supply products to our customers on a timely basis. Our demand planning horizon remains extended with high levels of purchase commitments and increased investments in working capital to address delays in component sourcing and the risk of future supply chain disruptions..”

Inventories are likely to rise this year and fall next year. However, over the longer- term, the inventory to sales ratio will be higher it was in the past. We believe the experience of not being able to meet customer demand in 2022 was a profound experience for the company which they do not wish repeat. Therefore, they are happy to carry higher inventories relative to sales, than was the case before.

The push into enterprise is working. Sales are growing and the diversity of customers is increasing.

“We have really diversified our business globally in the enterprise. We're not just in the high end financials. We're in just about every major vertical, healthcare, transportation, public sector, education, banks and insurance companies.”

Capital Allocation

Arista’s stated approach to Capital Allocation is as follows:

Maintain a healthy Balance Sheet. As we have noted above, the company does not have any long-term debt. Current assets are much greater than current liabilities.

Invest to strengthen operations and/or the position of existing business if a reasonable return can be earned.

M&A (strategic opportunities)- the company has made a series of acquisitions in related areas to acquire technologies and capabilities to enhance their offerings as noted above .

Share repurchases to offset dilution and return cash to shareholders (if the price is below a reasonable range estimate of intrinsic value) - share purchases have only been done to offset the (high) stock-based compensation. The number of shares outstanding have not fallen significantly.

Dividends as business matures- The company has not paid dividends. This is correct as they generate 30% returns on the capital they retain and re-invest.

Generative AI

The stock market and the technology sector are currently transfixed by the potential of Generative AI. AI is not an immediate opportunity for ANET but it could become an important driver of their business in the medium to long-term.

The Cloud hyperscalers are currently major customers as they have been building up their datacentre network. In the last six months, they have started changed their investing plans a little and started buying GPUs (mostly from Nvidia) in a big way in order to ensure that they can handle AI workloads. We discussed the impetus behind this in a note on Nvidia which can be found here.

Once the Cloud hyperscalers have established these new embellished GPU-heavy data centres, they will optimise them and connect them together to get the best performance from them.

“But the real test of why you buy these expensive GPUs in 2025, when you want to have not just 4,000 to 8,000, but 30,000, 50,000, maybe even 100,000, and this is why 2025 is so critical. And taking -- testing and taking out all the kinks out of the GPUs and networks is important because your network is so -- a good network is so pivotal to getting the most out of your GPUs… If you have idling cycles on those GPUs, you wasted thousands, if not millions, of dollars. And so, I think these next two years are crucial to getting the most out of these expensive GPUs and that's where the network really comes in.”

The initial and perhaps correct short-term solution will be will be to use InfiniBand (IB) technology for Networking. A large part of the benefit of this will to Mellanox, now fully owned by Nvidia.

However, Arista is strongly committed to developing Ethernet-based solutions .

“For the extremely large clusters (of GPUs) with large language training models, especially with the advent of ChatGPT-3 and ChatGPT-4, you're not talking about not just billion parameters, but an aggregate of trillion parameters. And this is where Ethernet will shine. But today, the only technology that is available to customers is InfiniBand.”

“So, obviously, InfiniBand with 10, 15 years of familiarity in an HPC environment is often being bundled with the GPUs. But the right long-term technology is Ethernet, which is why I'm so proud of what the Ultra Ethernet Consortium and a number of vendors are doing to make that happen. So near-term, there's going to be a lot of InfiniBand, and Arista will be watching that outside in. But longer term, Arista will be participating in an Ethernet AI network.”

“Arista is a founding member of the Ultra Ethernet Consortium that is on a mission to build open, multi-vendor AI networking at scale based on proven Ethernet and IP.”

“Arista's cloud customers are resonating with our AI and switching strategy for platforms. Presently, we are in the midst of trials leading to production deployments this year in 2023.”

Arista like everybody else is having to think very hard about the implications of AI for their existing business as well as potential future business.

“AI traffic and performance demands are different as it comprises of a small number of synchronized high bandwidth flows, making them prone to collisions that slow down the job completion time of AI cluster. As they connect thousands of GPUs, generating billions of parameters for petascale cloud clusters, Arista's EOS capabilities must also scale along with our AI spine and leaf platforms to achieve that consistent performance and throughput.”

Arista has been upgrading EOS to better handle AI workloads but this work will take time come through

“Arista has been developing EOS features such as intelligent load balancing and advanced analyzers to report and rebalance flows that can achieve predictable performance. Customers can now pick and choose programmable packet header field for better entropy and efficient load balancing of their AI workloads. Network visibility is also important in the training phase for large datasets to improve the accuracy of large language models. Arista's new AI Analyzer monitors and reports traffic counters at microsecond-level windows to detect and address microbursts.”

“We expect larger clusters and production deployments in 2025 and beyond. In the decade ahead, AI networking will become an extension of cloud networking to form a cohesive and seamless front-end ….”

“We see AI as a very, very important use case and workload for all our cloud titan customers. Clearly, it’s in the first innings. We’re just beginning. So very much like cloud networking 10 years ago, we see AI as an additional use case. It is a very, very small portion of our use cases so far. So a lot of upside ahead.”

AI is a big opportunity in the long term but perhaps only starting in 2025. The high speed 800 gigabit switch and router platforms will see particularly strong AI-driven demand.

Summary

Arista has done very well over the last decade by developing a software-driven approach to cloud networking.

The company has executed strongly and gained significant market share to become the second largest player.

Cloud hyperscale demand was very strong in 2022 and will inevitably grow at a slower rate in the coming years.

However, Arista is likely to make progress in boosting revenues from enterprise clients where its solutions, combining CloudEOS and CloudVision will be well received, in a sector that has been ill-served by vendors in the past.

In future years, the company is also likely to benefit in a meaningful way from the growth of demand due to Generative AI.

Conclusions

Arista Networks seems well placed to grow revenues by ~17% to ~25% for many years.

It is also likely to grow profits by ~20% to ~25% for many years.

This is likely to be achieved with profit margins of ~30% to ~35% and a Return of Equity Percentage of a similar amount.

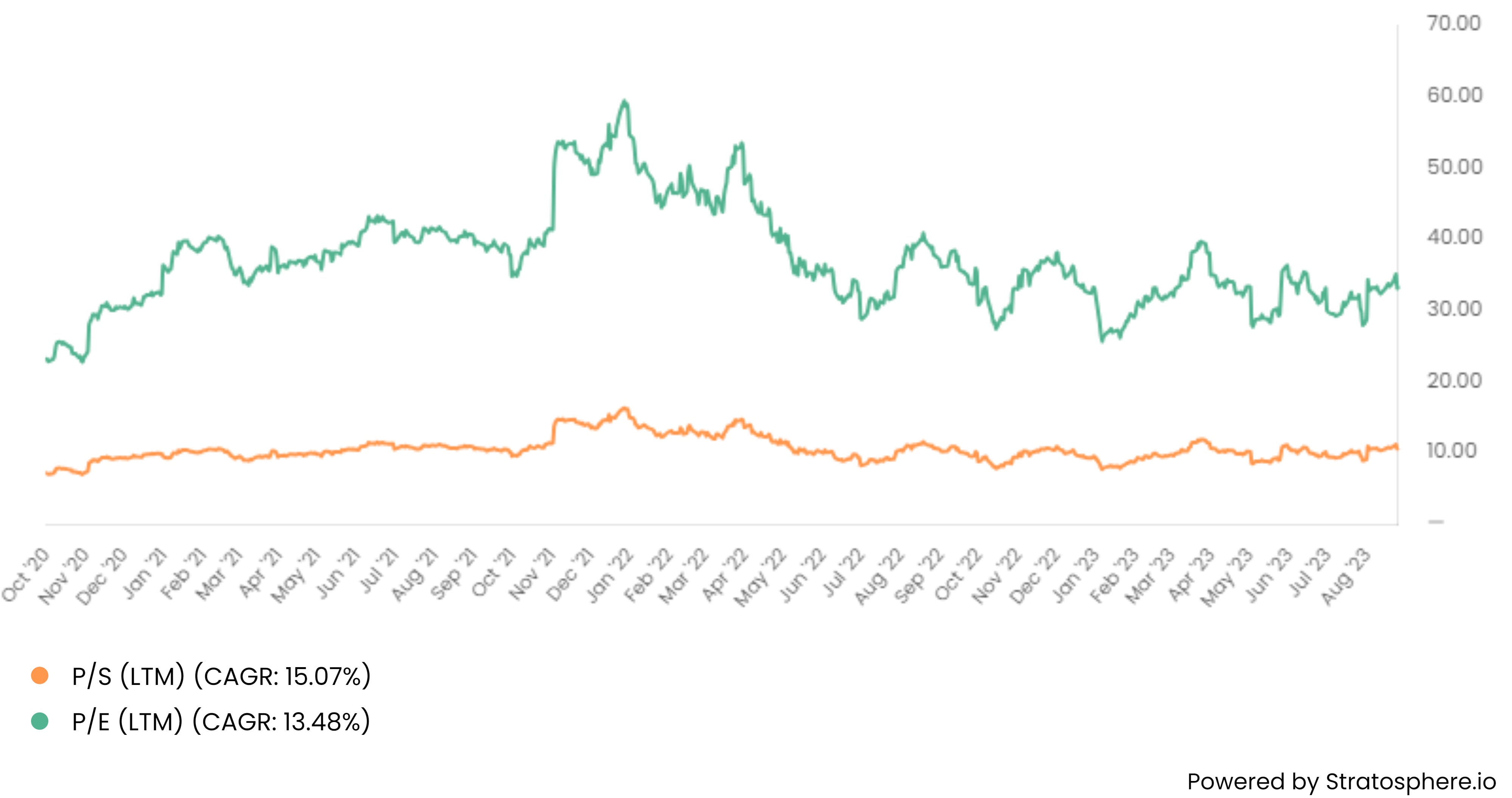

Given all this, a Forward Price/Earnings ratio of 36 times and Price to Sales Ratio of 10 times (see chart below) is not too expensive .

We don’t view the stock as a bargain at the current level but there is a strong chance that the company will grow strongly . It will therefore grow “into its multiples” and prove to be good long-term investment.

We will add to our current position in the company and continue to monitor it closely.