Arista Networks (ANET)

Q1 2025 Results

We first covered the ANET stock in September 2023 and established a position soon afterwards. The original note can be found here. It is worth reading to get a good technical overview of the company. We have written a number of notes on the company since then. Some of these can be found here, here and here.

The stock appreciated and gave a 100% gain. In the last report, we noted we sold the stock in late January 2025 as we believed both the market and the stock were expensive.

The decline in stocks after the US tariffs on 2nd April, saw the stock fall below $90 per share. We believed the stock was at reasonable value again and we re-established a 3% position.

We revisit the company in the light of the Q1 2025 Results.

Q1 2025 Results

This was a steady set of results that beat company guidance and analysts’ forecasts.

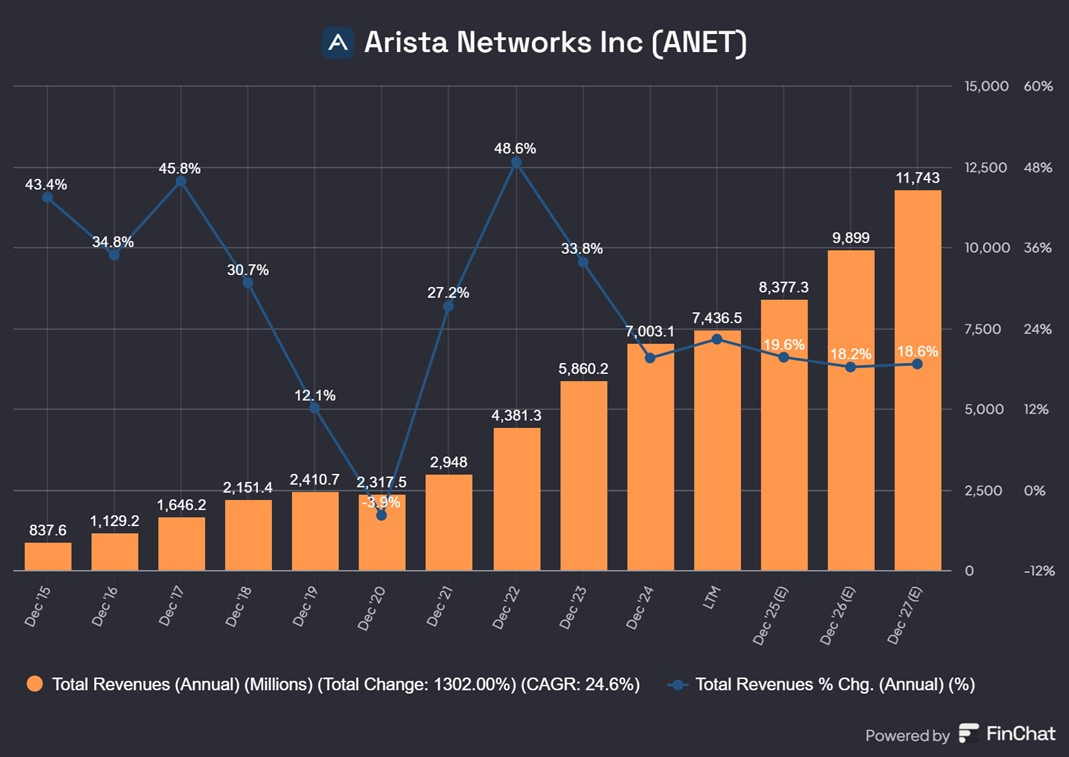

Total revenues in Q1 were $2.0bn, up 27.6% (y/y). This was their first $2 billion quarter, doubling just 11 quarters after their first $ 1billion quarter.

Operating Profit and Net Profit also grew in the 27%-30% range (y/y) in Q1 2025.

Both Products and Services grew about 27%

Software and Services contributed approximately 17.1% of revenue. Products accounted for 80%.

Margins are relatively stable. Operating margins have risen in recent years. As revenues have risen, the company has experienced significant economies of scale. Revenues have risen much faster than operating expenses.

Between 2015 and 2024, total revenues grew at a CAGR of 26.6%. Operating margins have increased an impressive 2.5x from 17.8% to 42.3%

APAC and US grew strongly while EMEA growth was more subdued.

International contribution for the quarter registered at 20% with the Americas super strong at 80%.

We are executing very well, and we aim for $10 billion revenue and beyond sooner than we previously expected.

As the chart below shows, the analysts’ consensus estimates suggest that $10bn annual revenue run rate will be hit in 2026/2027.

Revenue growth has slowed recently but remains around 18% to 20% (y/y).

The company has seen a steady increase in both Operating Income (CAGR 34.9%) and Net Income (CAGR 35.1%) in the last decade. Consensus Analysts’ forecasts project continued growth for the next two years.

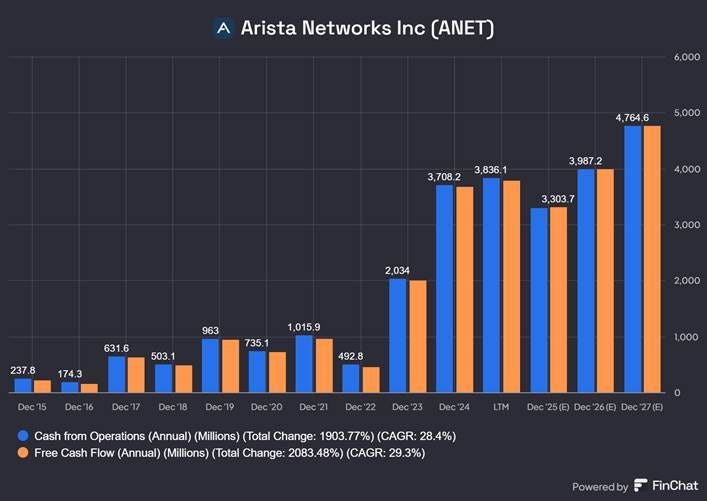

The company has seen increased Cash Flow growth in the last two years. As capital investment is low (manufacturing is outsourced), there is little difference between Operating Cash and Free Cash Flow (see chart above).

We generated approximately $641.7 million of cash from operations in the period, reflecting a growth of 24.9% compared to Q1.

The company has not been a significant buyer of its own stock until 2025 where to date they have repurchased $1.2bn worth.

If we compare the blue and orange bars in the chart above, Stock repurchases (orange bars) have mostly been at a level where they have offset new stock issued as Stock-Based Compensation (blue bars). However the much higher level of buybacks in 2025 ($1.215bn to date) should result in a meaningful reduction in total shares outstanding.

During the quarter, we repurchased $787.1 million of our common stock, our largest repurchase quarterly or annually in Arista's history. In Q1 2025, the share price fell from a peak of $129 on Jan 24th to about $80 at the end of the quarter.

In April, we repurchased an additional $100 million for a total of $887.1 million at an average price of $88.97 per share.

The stock price is now $95. The purchases at $88.97 will look smart, if the share price either stays at this level or rises. The chart below shows share price of ANET and analysts average target price,

To date, we have repurchased 13.3 million shares at an average price of $87.55 with (only) $34 million remaining in the existing $1.2 billion Board authorization. In May 2025, our Board of Directors authorized a new $1.5 billion stock repurchase program, which commences after we have completed repurchases under our existing $1.2 billion authorization. The actual timing and amount of future repurchases will be dependent on market and business conditions, stock price and other factors.

It will be interesting to see how many shares they buy in the current quarter given the share price has recovered.

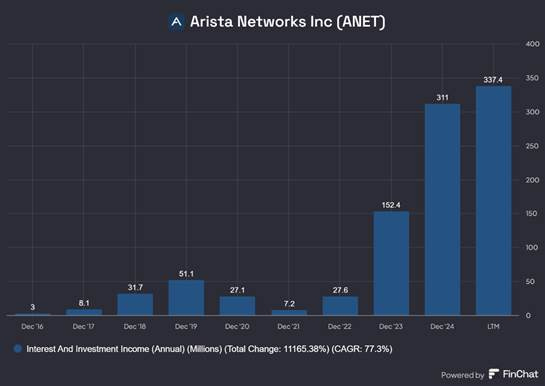

The company has no long-term debt. Cash and short-term investments have increased at 30% CAGR over the last decade and now stand at $8bn. Given current trends, the cash pile might easily grow by $3bn every year. We have listened to many conference calls but have not heard the management talk about, or be questioned on, their asset allocation strategy. What are they going to do with the cash pile?

They do not pay a dividend and currently the cash is invested in Treasury Bills. In FY 24, interest income was $ 300mn.

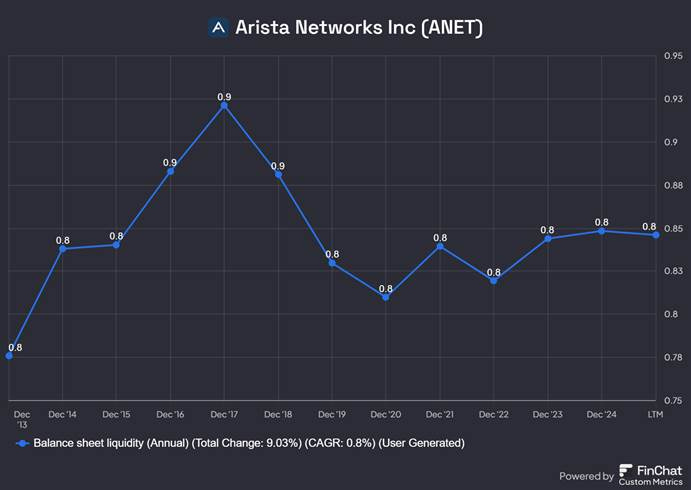

The Balance Sheet is liquid: current assets are 85% of total assets.

The chart above shows balance sheet liquidity (defined as Current Assets divided by Total Assets) has been 80% plus for ten years.

The profitability of the company is very high.

ROIC is 52%. (ROIC = Net Operating Profit after tax/ Invested Capital).

ROE and ROCE are both around 32%

The Total Return that has been achieved in last two decades by investors in Arista Networks is shown below:

35.5% (CAGR) over last 10 years (since listing)

48.7% (CAGR) over the last 5 years.

17.5% (CAGR) in the last 1 year.

Business Profile

“Arista Networks is a provider of data-driven, client-to-cloud networking for large artificial intelligence (AI), data center, campus and routing environments

Its platform is its Extensible Operating System (EOS), a modernized publish-subscribe state-sharing networking operating system which can be said to be unique and a source of competitive advantage.”

The offering can be classified as follows:

Core (Data Center, Cloud and AI Networking)

Cognitive Adjacencies (Campus and Routing),

Cognitive Network (Software and Services).

They help companies “wire up” their networks either on-premises or on the cloud.

More information can be found in our first report on ANET which can be found here.

The company has grown quickly as cloud hosting players, including Amazon, Microsoft and Google, have expanded rapidly.

In the last two years, ANET has benefited greatly from huge investments in Datacentres by large cap tech companies.

Microsoft and Meta account for more than 40% of Arista Networks’ Revenues. Arista work with four large-cap tech companies in total. The large exposure to two of them can be seen as a risk.

However, it should be noted that these companies have been growing fast and have increased their capital expenditures greatly in recent years.

Arista Networks has a capital-light model. Manufacturing is outsourced to contractors in China, Vietnam and the Far East. This means ANET is especially vulnerable to the tariff policies of the US administration.

We can measure how “capital-light” a company is by looking at Capital Intensity (defined as Net Plant and Equipment dividend by Total Assets) and Capital Scale (defined as Capital Expenditure to Revenue).

The chart below shows both metrics have been both quite low and have declined rapidly. This supports our view that ANET has a truly capital-light model.

Highlights from the Earnings Conference Call

Clearly, Arista's redefining the future of data-driven networking, working intimately with our top customers have been matched on in the evolution of data centres, campus centres, branch centres and AI centres.

Our cloud and AI momentum continues as we remain confident of our $750 million front-end AI goal in 2025.

We are progressing well in all four customers[1] and continue to add smaller ones as well.

In addition to the large tech company datacentres, Arista also helps companies in many industries put together Campus and Branch Networks. The configuration of networks is being transformed by the advent of AI.

In today's AI wave, customers can no longer tolerate LAN (Local Area Network) and WAN (Wide Area Network) silos. The concept of what comprises a user or a device or a site fundamentally changes the building of a branch or campus in 2025. Agentic AI[2] makes us question the very definition of what we might even consider a user, future campus and branch centres could be centralized or distributed, or they could be dispersed across laptops, smartphones, a house, an airplane or any other location on the move. Data and applications can be located anywhere and add more dimensions, whether it's a data center or a public cloud or campus.

They believe their “Cognitive Portfolio” with advanced spine (this was discussed in detail in our first report on the company which can be found here.) gives them an advantage in the emerging scenario

Arista's cognitive campus portfolio features our advanced spine with power-over-ethernet wired lease capabilities, along with a wide range of cost-effective wireless 6 or 7 indoor and outdoor access points for the newer IoT[3] and agentic applications.

Inventories

Inventories increased a little from $1.8bn to nearly $2bn.

Inventory turns were 1.4 flat to last quarter. Inventory increased to approximately $2 billion in the quarter, up from $1.8 billion in the prior period, reflecting an increase in finished goods.

The increase can be explained by buying to avoid expected high tariffs.

This is an intentional action regarding both tariffs and in the support of ramping new products. Our purchase commitments at the end of the quarter were $3.5 billion, up from $3.1 billion at the end of Q4. This was driven by a continued investment in chips, as well as an increase in buffers due to the tariff uncertainty.

From a cash flow perspective, we will continue to optimize our working capital investments with some expected variability in inventory due to the timing of receipts on purchase commitments

Inventories have risen but it is not too high if we look at the Inventory /sales ratio. (See Chart above).

Capital Expenditure

As noted above, Capital Expenditure is relatively small both in absolute terms and relative to operating cash flow.

Capital Expenditures for the quarter were $32mn. In October, we began our initial construction work to build expanded facilities in Santa Clara, and we expect to incur approximately $100mn in CapEx during fiscal year '25 for this project.

Outlook

We have seen good momentum at the beginning of fiscal year '25.

There are opportunities across all three customer sectors, inclusive of Gen AI, data centre, cloud and campus enterprises.

The second half holds significant ambiguity related to the tariff scenarios. Given these unknowns, our guidance for FY '25 currently remains unchanged despite the strong results and guidance we are reporting today.

Energized by the current momentum, we continue to focus on operational discipline and innovation, ensuring we deliver strong outcomes for customers and shareholders.

Tariffs

The tariffs announcement on 2nd April (“Liberation Day”) hit Arista as most of their products are manufactured and imported from China and the Far East.

As the news came about, we literally find ourselves in the middle of an ocean trying to figure out which country to go to because the tariffs, as you know, the reciprocal tariffs are much higher in some of the Asia countries.

The 90-day stay of execution to July 9th was a relief to Arista. The rapid and sudden changes on Tariffs create uncertainty and caused problems for corporate planning.

So we are grateful for the measured approach that we do not have to deal mostly with any of these tariffs until July 9.

We are absorbing whatever tariffs we do have to deal with from China and other things. We have taken into consideration for the year and some we will absorb and some we may potentially have to pass to our customers. But we don’t know what we don’t know. So, we can just go at this one quarter at a time.

They think the impact on Gross Margins will be 1% to 1.5% as tariff may settle eventually at 10% to 20%.

On the tariff side, in regard to gross margin, if you were to take those commentaries, that puts the range of gross tariff impact to be 1 to 1.5 points at the top layer with no mitigation.

There may be a point where we have to have the price increases, but we’re looking to mitigate through absorption and tariffs and supply chain fungibility.

They are being conservative on the full year guidance on account of the tariffs though current demand trends are very healthy.

(If) there were no tariffs we'd be even more optimistic about the second half. So we're being careful, measured because we don't know what the tariffs we do

Implications of Microsoft comments

In their earnings conference call, the Microsoft CEO, noted growth in non-AI workload migrations to the Cloud grew faster than AI workloads. ANET management were asked whether they had seen a similar trend.

Two years ago, I was very nervous because the entire cloud titans pivoted to AI and slowed down their cloud. Now we see a more balanced spend and while we can't measure how much of this cloud and how much of it is AI, if they're kind of cobbled together, we are seeing less of a pivot, more of a surgical focus on AI, and then a continued upgrade of the cloud networks as well. So compared to '23, I would say the environment is much more balanced between AI and cloud.

Summary

This was another solid set of results for ANET. It achieved 28%-30% growth in Sales, Operating Profit and Net Profit.

The company has been a consistent generator of Operating and Free Cash Flows.

The company does not have any debt and has over $8bn of Cash and Short-Term Investments.

Shareholders may wonder as to their capital allocation strategy as the large cash pile is likely to continue to grow. The company does not pay a dividend

In 2025, ANET have bought back nearly $1bn of stock after the price fell below $90 a share.

This is positive indicating management is willing to buy back shares when the price falls significantly. It suggests, they may follow rational capital allocation.

ANET is a play on the growth of enterprise technology networking in datacentres, Campuses and Branches.

Unlike the large tech players its model does not require huge capital investment and therefore offers a capital-light business model leveraged to the growth of AI and the Cloud.

The main source of concern is the Tariffs. Their products are manufactured by third parties located in China and the Far East. The tariffs on imports of these products into the US (Americas accounts for 80% of Revenues – the bulk of this will be the US) will be a negative.

The company believes it can pass on the price increases due to tariffs. They believe the hit to their gross margins will be only 1 to 1.5 percentage points. Time will tell.

Valuation

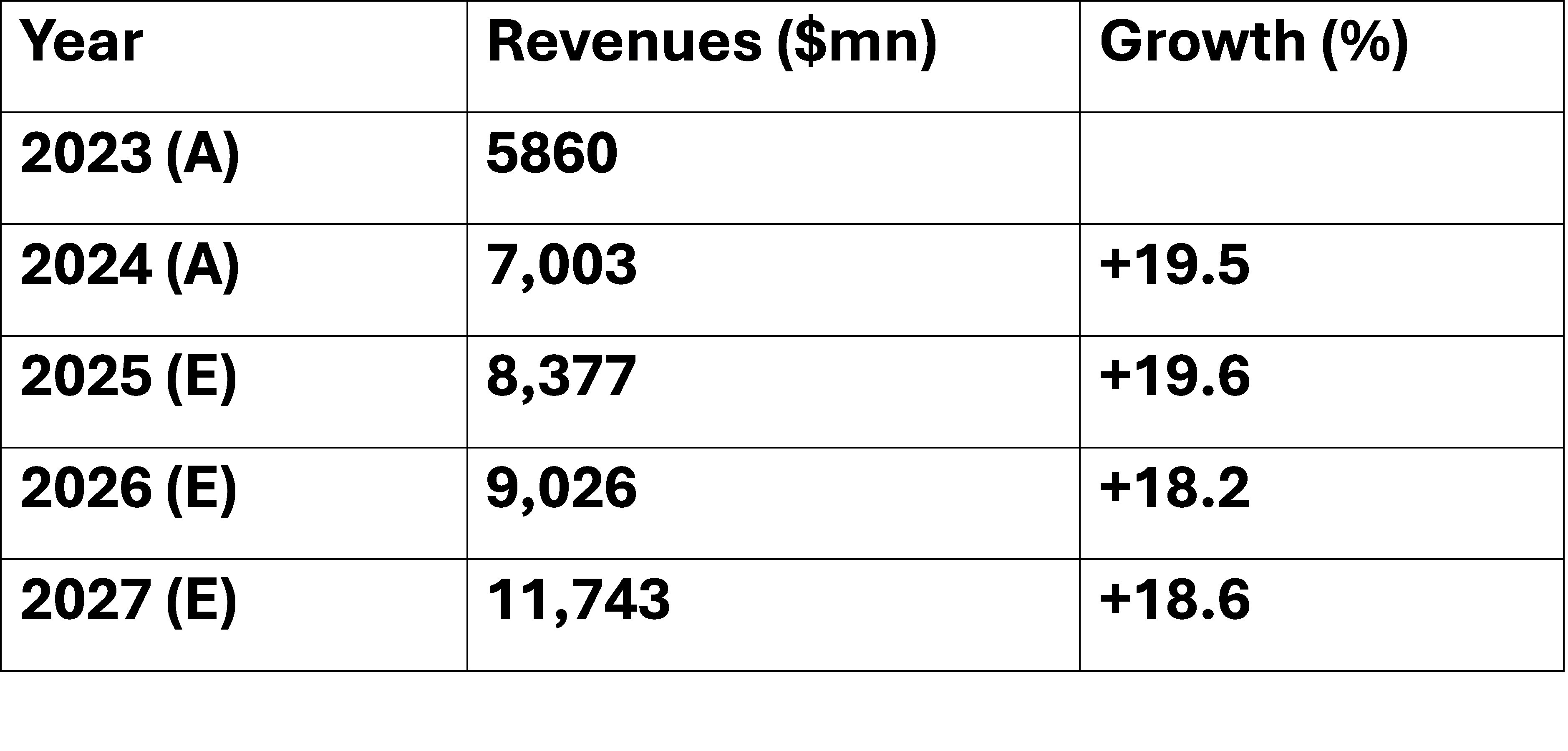

The consensus analysts’ forecasts for Total Revenues are as follows:

The analysts expect total revenues to grow at about 18% to 19% per annum over the next three years.

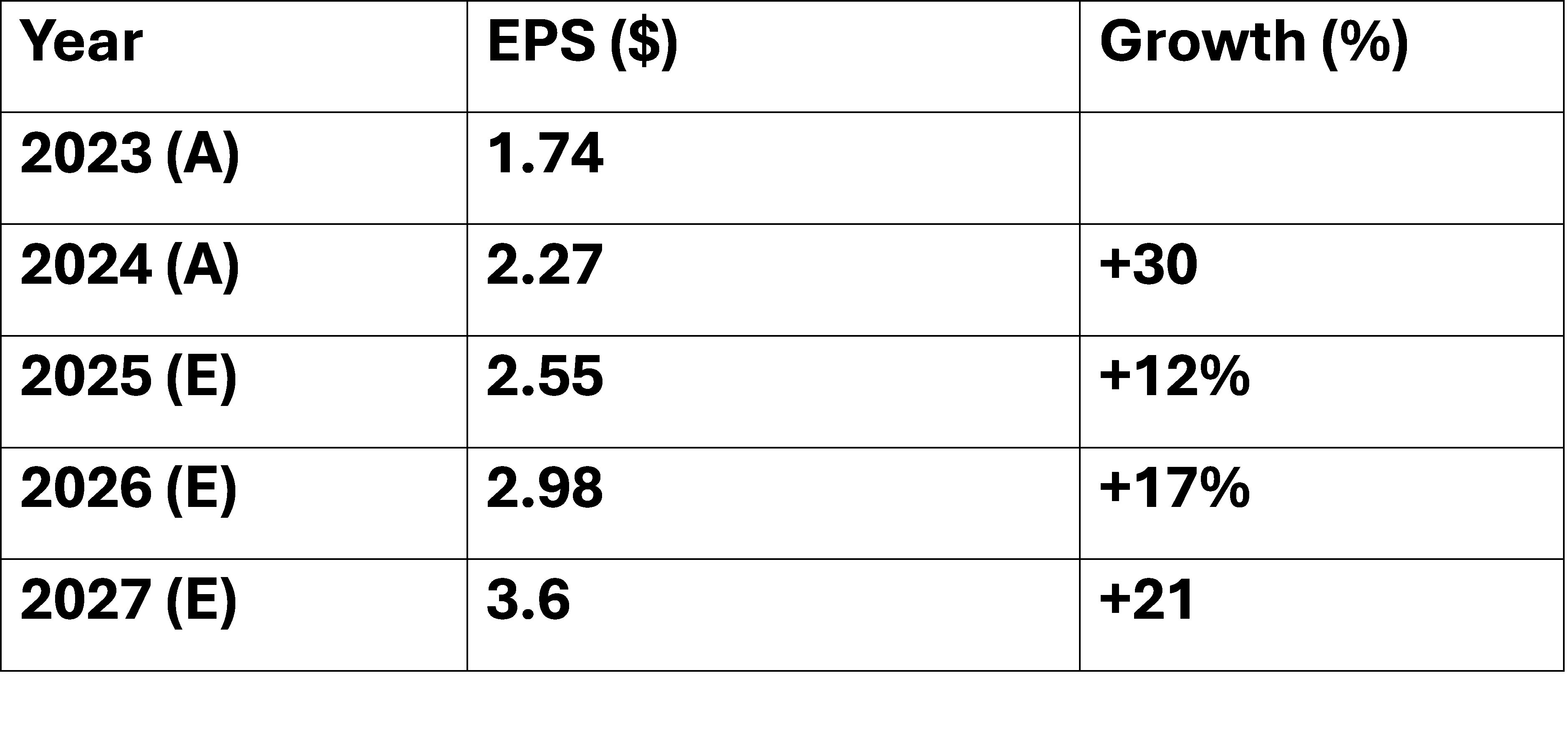

The consensus analysts’ forecasts for EPS are as follows:

The consensus analysts’ forecasts for Free Cash Flow (FCF) are as follows:

The shares currently are at $96.4 per share and ANET’s market capitalisation is $121.1bn. This means it is currently on a two-year forward Price /Earnings Ratio of 32.3X and Price to Free Cash Flow Ratio of 30.4X.

This suggests that ANET stock is fairly valued given the fundamentals of the company covered above.

We conducted a Discounted Cash Flow (DCF) Calculation to double check this view. Using analysts’ consensus figures and some additional assumptions, we sought to value the stock.

The risk-free rate is currently of 4.2% and the Market Risk premium of 5.0%. The Stock Beta is 1.4. The Weighted Average Cost of Capital (WACC) is 11.4%.

We use the analysts’ consensus’ numbers noted above.

In addition, we assume revenue growth in 2028 and 2029 will be 18%.

We assume net margins in 2028 and 2029 will be 39%.

Finally, we assumed that at end-2029, the terminal exit P/E multiple is 35X.

With these assumptions, we calculated a theoretical ANET stock value of $102 – the current price of $96.4 is at a 6.4% discount to this.

If we reduce the terminal exit P/E multiple to 32, we get a theoretical value equal to the current stock price

Conclusion

We sold the stock in January 2025 as noted in our last report. At the time we judged an attractive entry point to be closer to $77.

We re-entered the stock during Q1 at an average price of 84 and currently have a 3.4% holding. We believe ANET is a good quality investment opportunity and we will continue to maintain our position.

[1] These are the four large tech customers including Meta and Microsoft.

[2] Agentic AI where AI is embodies in millions of agents such as Chat Bots. Essentially, it's AI with the ability to think, reason, and adapt to changing circumstances without constant human guidance.

[3] IoT is Internet of Things. This refers to the collective network of connected devices and the technology that facilitates communication between devices and the cloud, as well as between the devices themselves.

Really appreciate the thorough breakdown of ANET's capital-light model and how it's both a strength and vulnerability. The fact that they're generating such strong cash flows ($641M in Q1) without needing massive capex is impressive, but the tariff exposure is a real wild card here. Their decision to buy back nearly $1B in stock at $88-89 after the April selloff shows management is thinking like owners, which is refreshing. The 1-1.5% gross margin impact from tariffs seems managable given their 42% operating margins, but the uncertainty around reciprocal tariffs makes forecasting tricky. Interesting that they're seeing more balanced cloud vs AI spend now compared to 2023—that diversification should help stabilize revenue streams.

Thanks for this really in-depth review. Have a great rest of your day.