We have covered Arista Networks on several occasions in the past. These reports can be found here, here and here. In our view, the first one especially is worth reading if you wish to understand the company

We revisit Arista after the publication of the Q2 results.

These were another set of excellent expectations beating results.

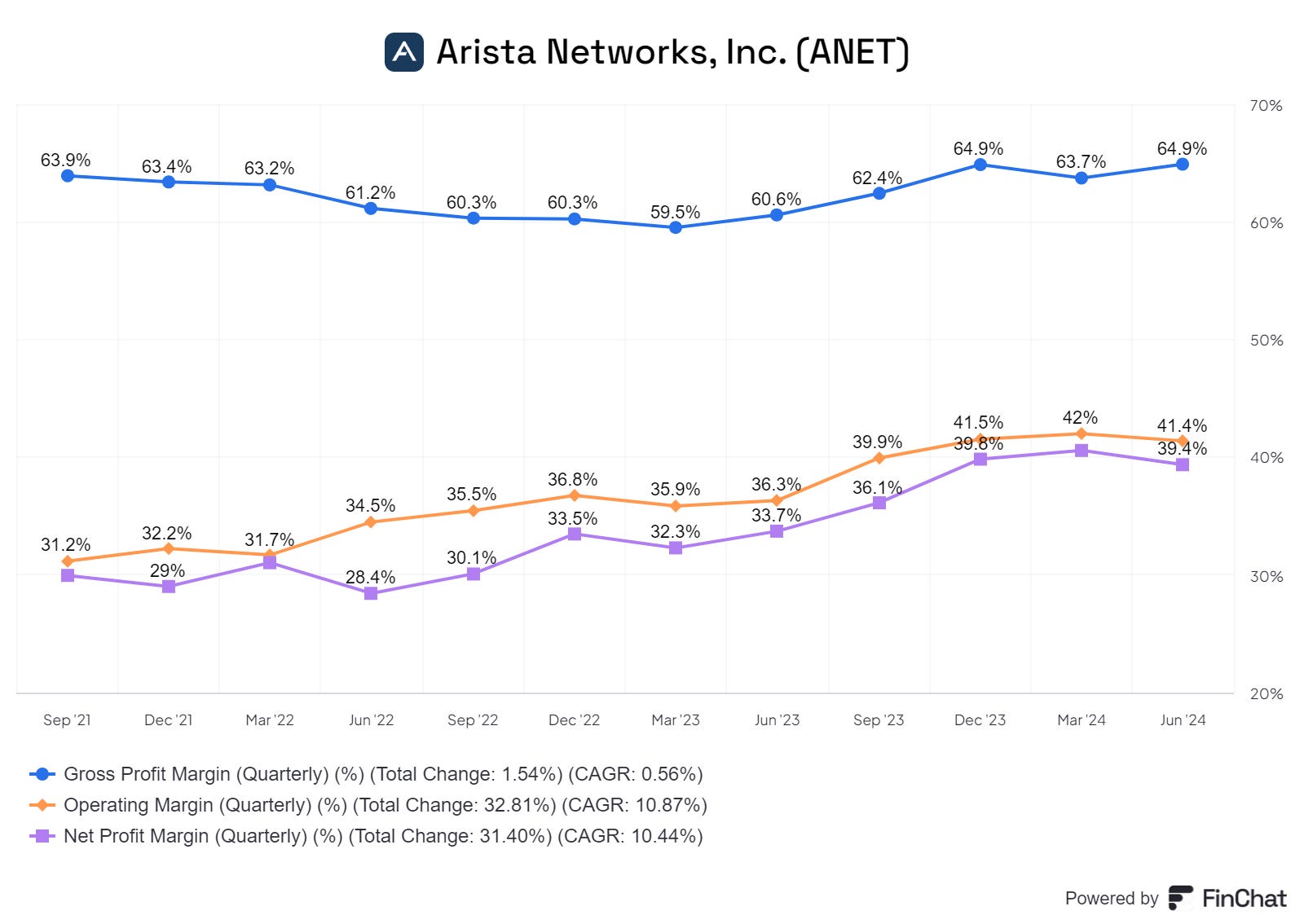

Arista Networks Q2 gross margin 64.9%.

Q2 revenue $1,690mn beating analysts’ consensus estimate of $1,652mn.

Q2 adjusted net income $672.6mn beating analysts’ consensus estimates of $623.6mn.

Q2 net income $665.4mn.

Q2 adjusted gross margin 65.4% above guidance of 64%

Outlook for Q3 revenue of $1,720-1,750mn.

The numbers show consistent growth in revenues both on a q/q and y/y basis. In the last quarter, services grew faster than products albeit from a low base. Services renewals contributed strongly at approximately 17.6% of revenue, up from 16.9% in Q1.

The 15.9% growth in revenues translated to a 30%+ increase in operating profit, net profit and EPS. This shows the business model continues to have significant operating leverage.

Margins have grown well on a (y/y) basis. The year-over-year gross margin improvement was primarily driven by a reduction in inventory-related reserves

International revenues for the quarter came in at $316mn or 18.7% of total revenue, down from 20.1% in the prior quarter.

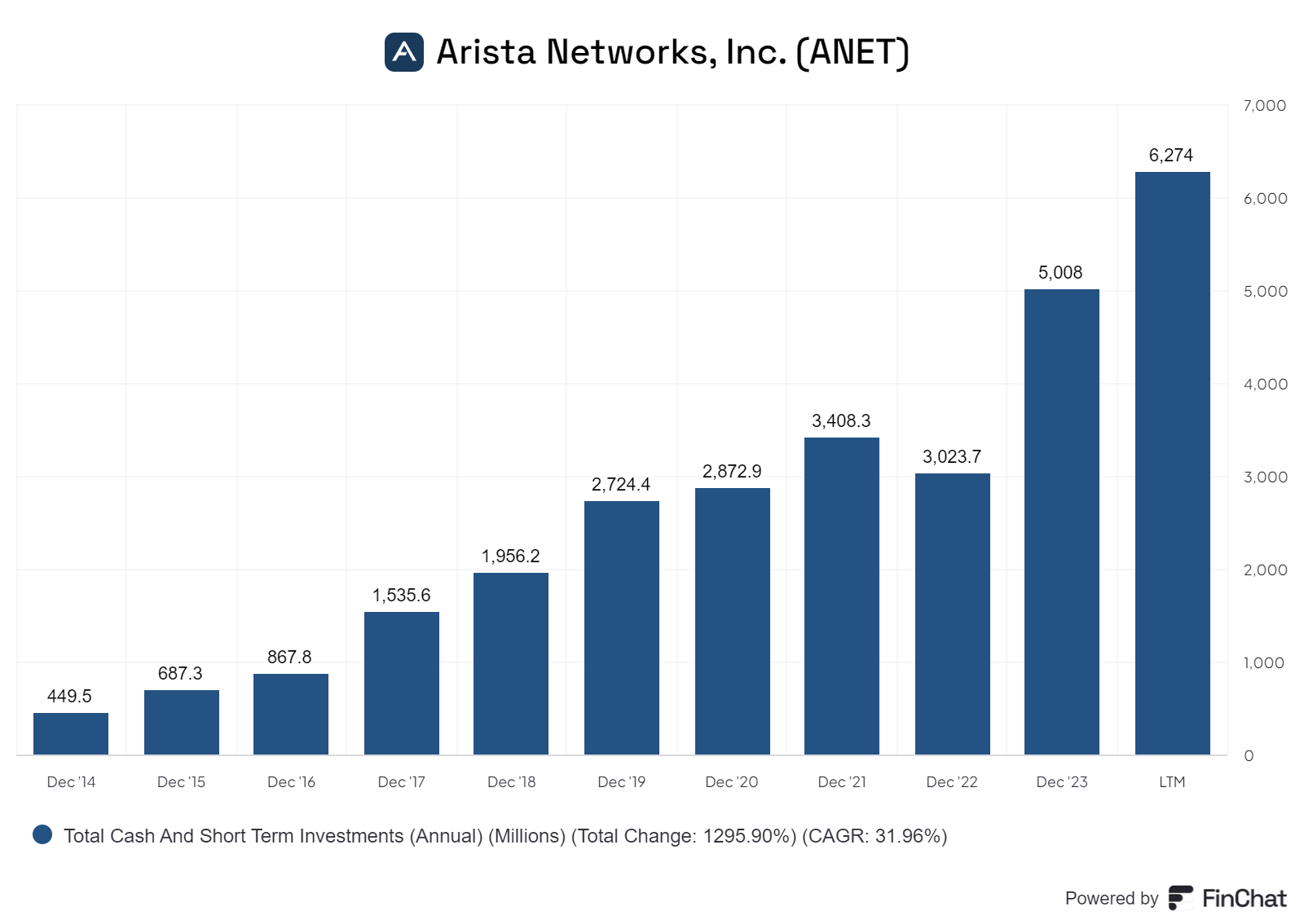

Balance Sheet.

Cash, cash equivalents and investments ended the quarter at $6.3bn- this is a high ~50% of total assets. Arista also has zero debt and therefore a very strong balance sheet.

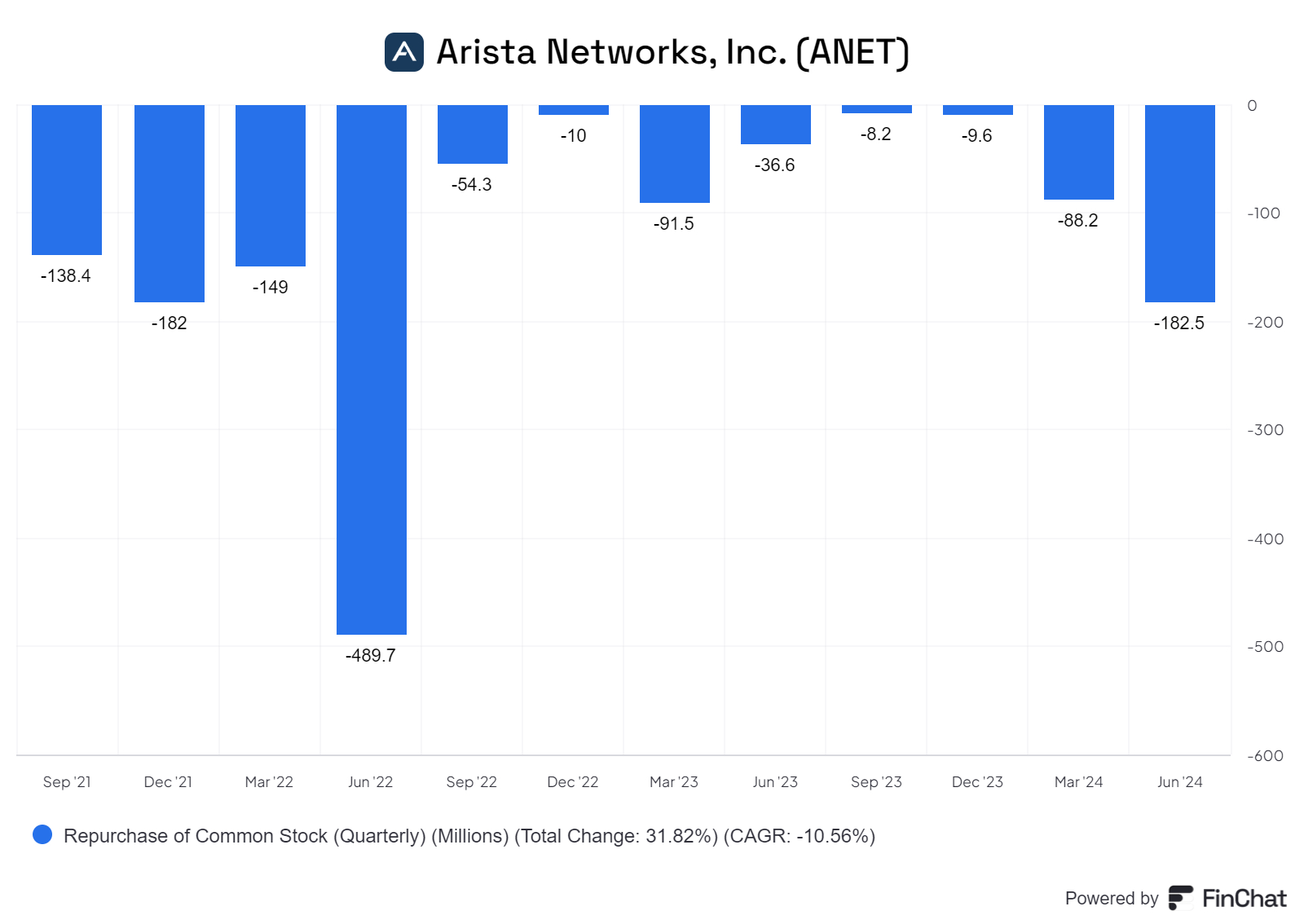

In the quarter, Arista repurchased $182mn of our common stock.

R&D spending came in at $216.7mn or 12.8% of revenue, up from $164.6mn in the last quarter. This primarily reflected increased headcount and higher new product introduction costs in the period. Capital expenditures for the quarter were just $3.2mn.

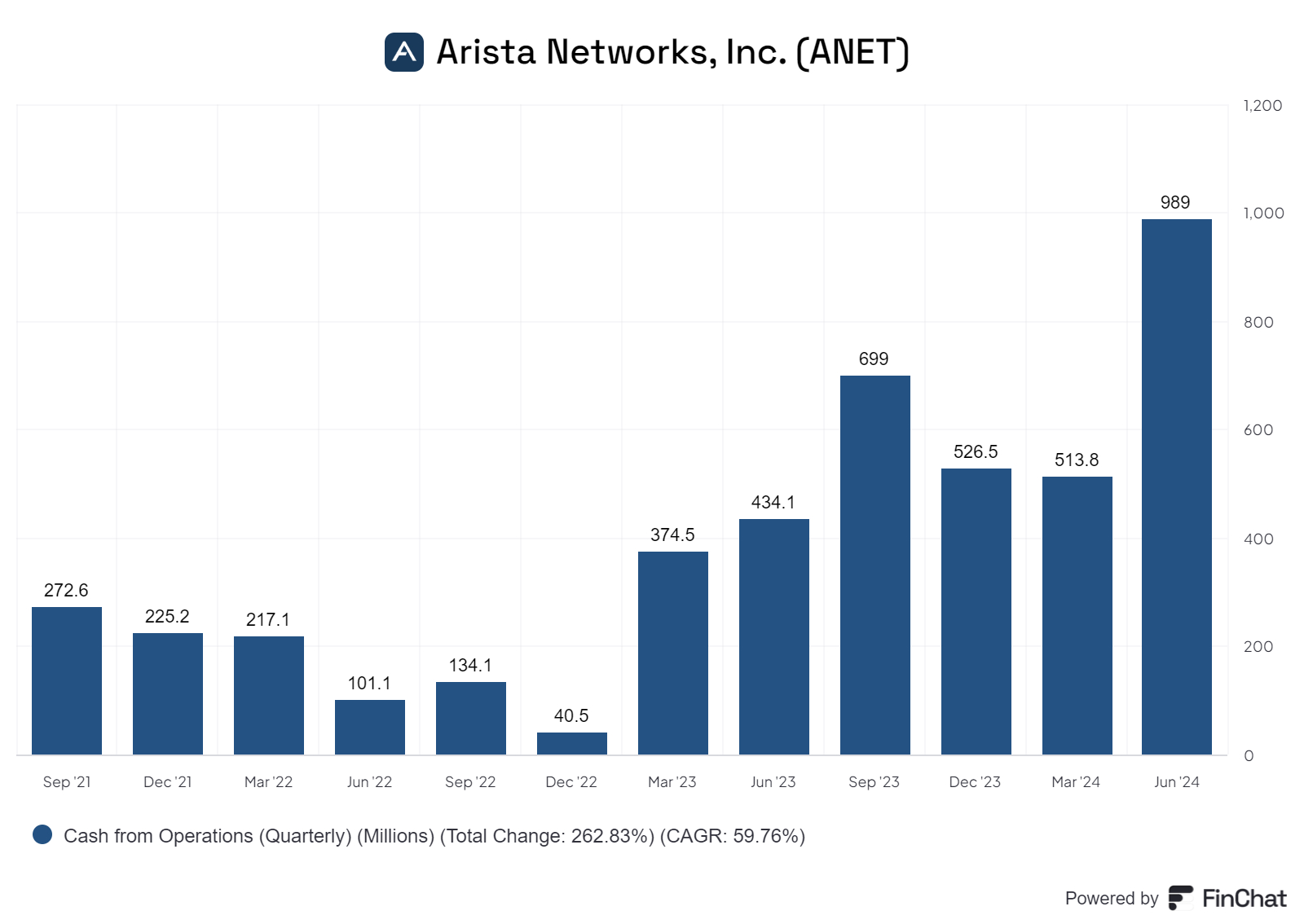

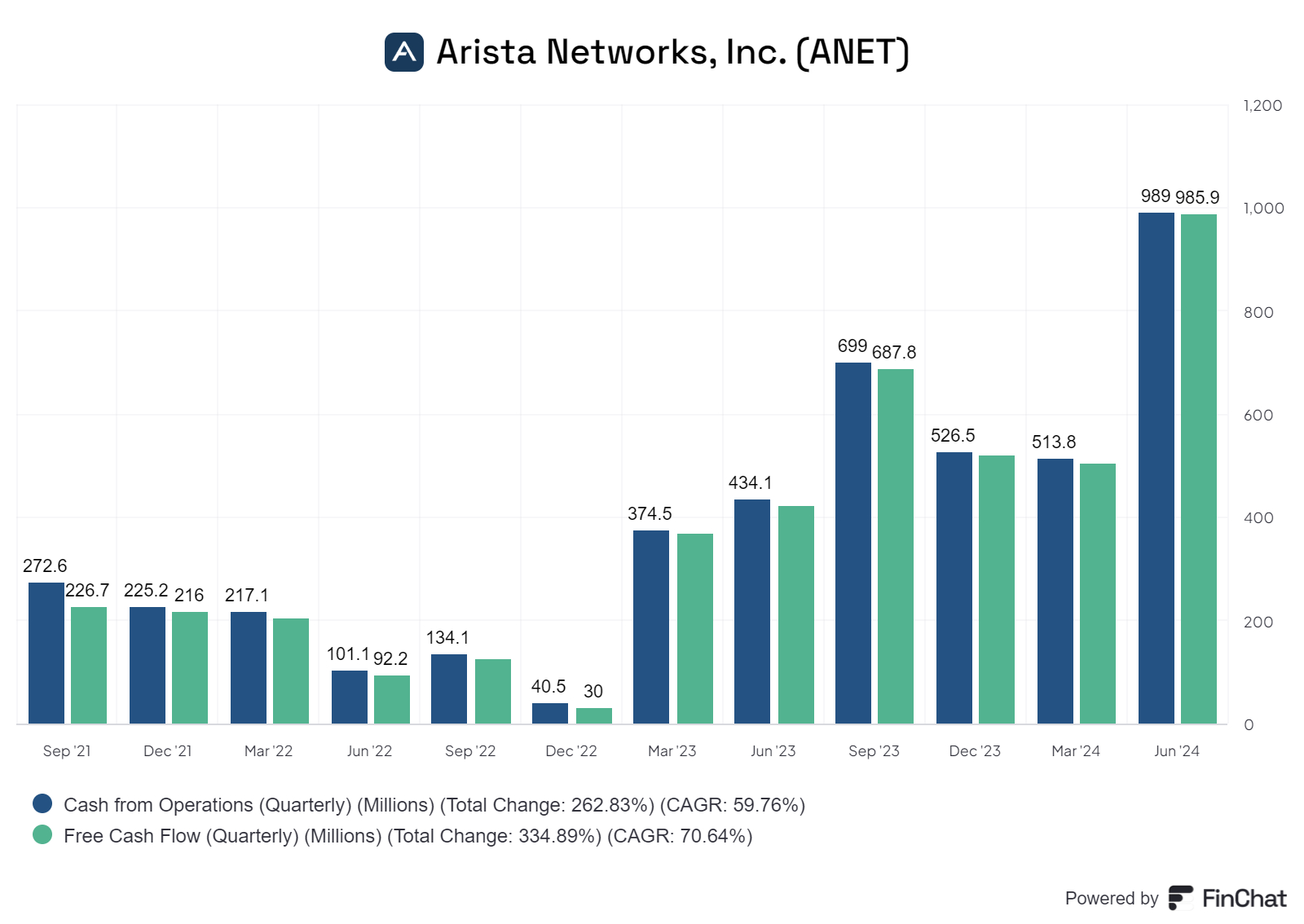

ANET generated $989mn of cash from operations in the period. This was the highest in more than 12 quarters and reflects strong earnings performance with a favourable contribution from working capital.

As Capex is very low, most of the Operating Cash translates to Free Cash Flow.

Arista’s total deferred revenue balance was $2.1bn, up from $1.7bn in Q1. The majority of this services related and directly linked to the timing and term of service contracts which can vary on a quarter-by-quarter basis.

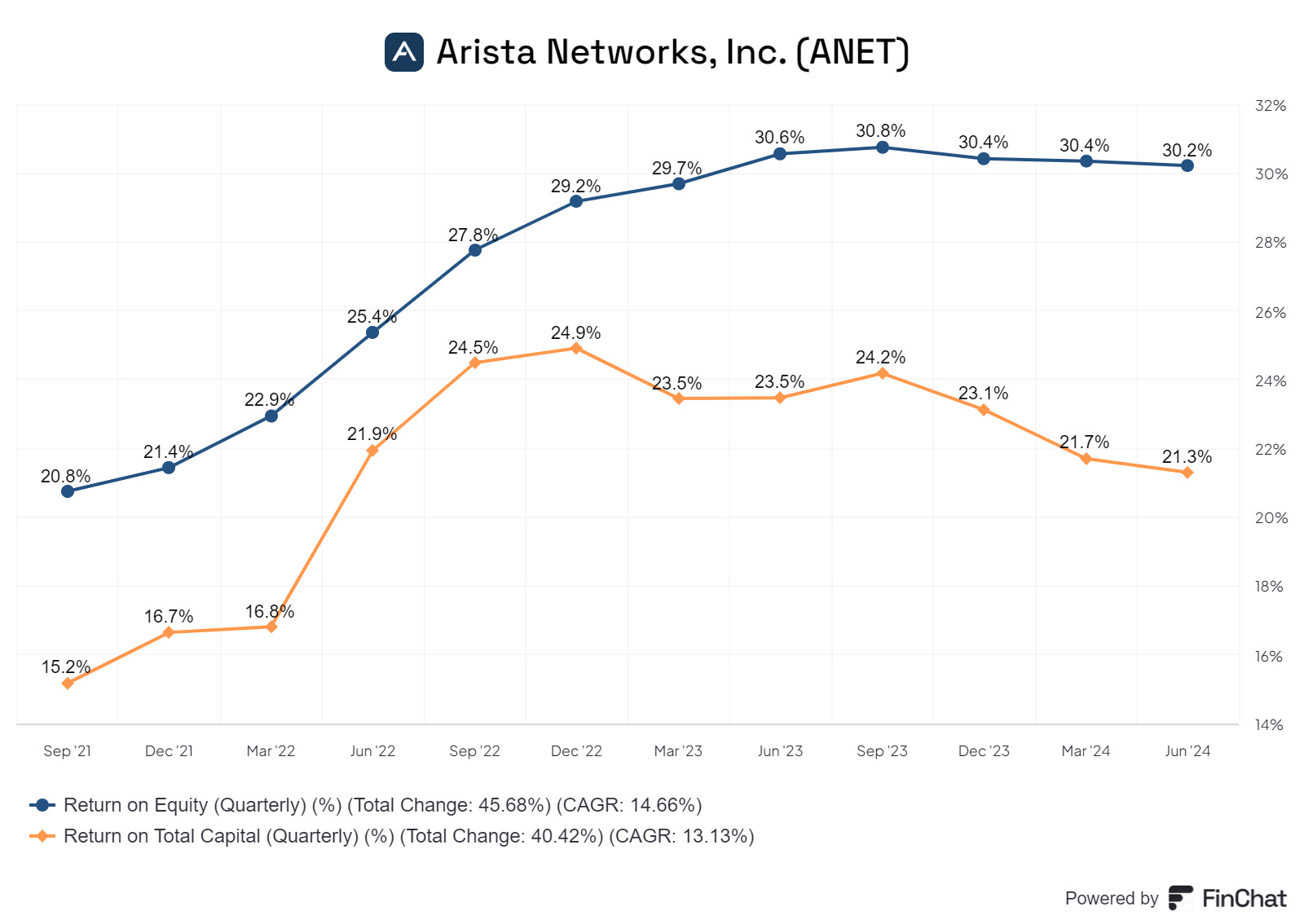

In addition to the strong cash generation, the company is also very profitable. The ROE has been stable in the last year at 30.4%.

They expect 2024 to be a year of new product introductions, new customers and expanded use cases.

Guidance and Forecasts

· Revenues of approximately $1.72bn to $1.75bn,

· Gross margin of approximately 63% to 64% and

· Operating margin at approximately 44%. (cf with 41.4% in the most recent quarter)

The customer base

Arista’s customer base can be described in term of their business verticals. These are

Cloud Hyperscalers

Enterprise

Specialist Cloud Providers

Financials and Service Providers

In 2022, the Cloud hyperscalers accounted for 46% of revenues. Enterprise and Financials together was strong at approximately 32%, while the providers were at approximately 22%. Meta and Microsoft accounted for 25.5% and 16% respectively.

Over 40% of the demand come from two customers Microsoft and Meta. No other customer accounts for more than 10% of demand. Both Microsoft and Meta have significantly stepped up their investments in AI datacentres which should lead to sales for ANET.

In recent quarters, Arista has been working hard to increase sales to enterprises albeit starting from a low base. This involves providing networking software and services at corporate campuses.

In the last three quarters, investments in AI from existing customers has provided a huge boost to Arista and this continues to be feature of the current results as well

Highlights form the recent Earnings conference call.

“A pure-play networking innovator with greater than $70bn total addressable market (TAM) ahead of us, we are pleased with our superior execution this quarter.”

“We are now supporting over 10,000 customers with a cumulative of 100mnn ports deployed worldwide. “

In terms of Networking standards there is strong rivalry between two industry standards protocols, Ethernet and InfiniBand. The latter is the property of Mellanox which was acquired by Nvidia. ANET is promoting Ethernet and is a Steering Member of the Ethernet Consortium. More information on the latter can be found here

“In June 2024, we launched Arista's Etherlink AI platforms that are ultra-Ethernet Consortium compatible, validating the migration from InfiniBand to Ethernet. Let's just say once again, Arista is making Ethernet great.”

“ We're feeling very gratified that the whole world, even InfiniBand players have acknowledged that we are making Ethernet great again.”

They have had four global customer wins and they wanted to highlight these to illustrate their progress. Three of these are detailed below:

1 A large Tier 2 cloud provider which has been heavily investing in GPUs to increase their revenue and penetrate new markets. Their senior leadership wanted to be less reliant on traditional core services and work with Arista on new, reliable and scalable Ethernet fabrics.

2 Customer is a large datacentre customer which has deployed us for almost a decade. The team was able to leverage that success to help them demonstrate our value for the global campus network which spans across hundreds and thousands of square feet globally.

Customer had considerable dissatisfaction with a current vendor which led them to a last-minute request to create a design for their new corporate headquarters. In three months, Arista leveraged the existing datacentre design and adapted this to the campus topology with a digital twin of the design in minimal time.

3 A large automotive manufacturer that due to its size and scale, previously had more than 3 different vendors in the datacentre which created a very high level of complexity both from a technical and also from an operational perspective. The customer's key priority was to achieve a higher level of consistency across their infrastructure which is now being delivered via a single U.S. binary image and CloudVision solution from Arista.

“So far in 2024, it's proving to be better than we expected because of our position in the marketplace and because of our best-of-breed platform for mission-critical networking.”

A lot of ANET’s demand is driven by networking of AI Datacentres. As we have noted before, AI models have two stages of work. Training which is very intensive in terms of the processing power required and the huge amounts of data that needs to be processed and needs the highest level of performance from Networks

“The collective nature of AI training models mandating a lossless highly available network to seamlessly connect every AI accelerator in the cluster to one another for peak job completion times.”

Once the models are trained the inference stage begins where they are connected to a large number of users and face queries and models learn and improve by answering the queries.

“Our AI networks also connect trained models to end users and other multi-tenant systems in the front-end datacentre, such as storage, enabling the AI system to become more than the sum of its parts.”

“We believe datacentres are evolving to holistic AI centres, where the network is the epicentre of AI management for acceleration of applications, compute, storage and the wide area network.

AI centers need a foundational data architecture to deal with the multimodal AI data sets that run on our differentiated EOS network data systems.”

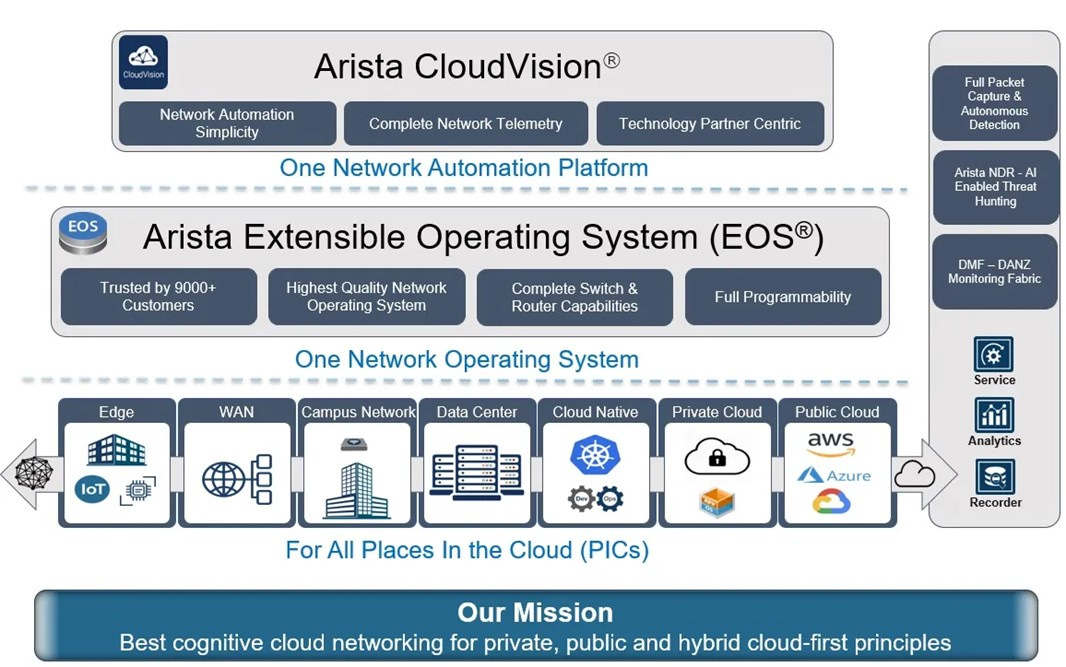

EOS or Extensible Operating System (EOS) is a software developed over five years ( 2004-2009) by Arista Networks for operation of Cloud Networks.

EOS is a scalable network operating system (OS) that offers high availability, streamlines maintenance processes, and enhances network security. EOS is described as containing a multi-process state-sharing architecture provides for fault containment, so that when problems occur in one part of the network, they will not easily spread to other parts. In addition, programmes can in effect heal themselves when bugs or malware cause problems.

They have developed an AI Agent in EOS.

“Arista showcased the technology demonstration of our EOS-based AI agent that can directly connect on the NIC (Network Interface Card) itself or alternatively, inside the host. By connecting into adjacent Arista switches to continuously keep up with the current state, send telemetry or receive configuration updates, we have demonstrated the network working holistically with network interface cards such as NVIDIA BlueField. Well, I think the Arista purpose and vision is clearly driving our customer traction.”

“Our networking platforms are becoming the epicentre of all digital transactions, be they campus centre, datacentre, plan centres or AI centres.”

As companies like Nvdia develop ever more powerful and faster GPUs, they are dependent on the networks’ ability to process information at the required speed.

“As GPUs get faster and faster, obviously, the dependency on the network for higher throughput is clearly related. Our timely introduction of these 800-gig products will be required, especially more for Blackwell.”

NB Blackwell is the next leading edge GPU from Nvidia which is due to be launched later this year.

They are running some trials with four large customers which could be significant, if they are converted into orders down the line.

“All 4 trials are largely in what I call Cloud and AI Titans. A couple of them could be classified as speciality providers as well, depending on how they end up. But those 4 are going very well. They started out as largely trials. They're now moving into pilots this year, most of them.”

Customers are starting AI trials and pilots in large numbers.

“When it comes to mission critical networks, they've recognized the importance of best-of-breed reliability, availability, performance, no loss and the familiarity with the datacentre is naturally leading to pilots and trials on the AI side with us.”

Customers want reliability and resilience in their networks

“They want to make sure that when they wake up in the morning, the network is not down. And so Arista today actually has a brand. It has a value for there. And we've actually been delivering this for the last 10-plus years. the message is echoing successfully in our existing customers who are taking Arista not only in the single use case of datacentre but expanding that across datacentre, campus, routing, WAN.”

Summary

This was yet another good set of results for Arista. It combined consistent growth in revenues, significant operating leverage with an impressive growth in margins. It has been strong generator of cash and has achieved high levels of profitability. It ahs a strong balance sheet ( 50% of BS is cash) and no debt. It is a story of continued progress.

Valuation

The market is well aware of ANET’s strong performance and therefore, it is likely to be reflected in the current share price.

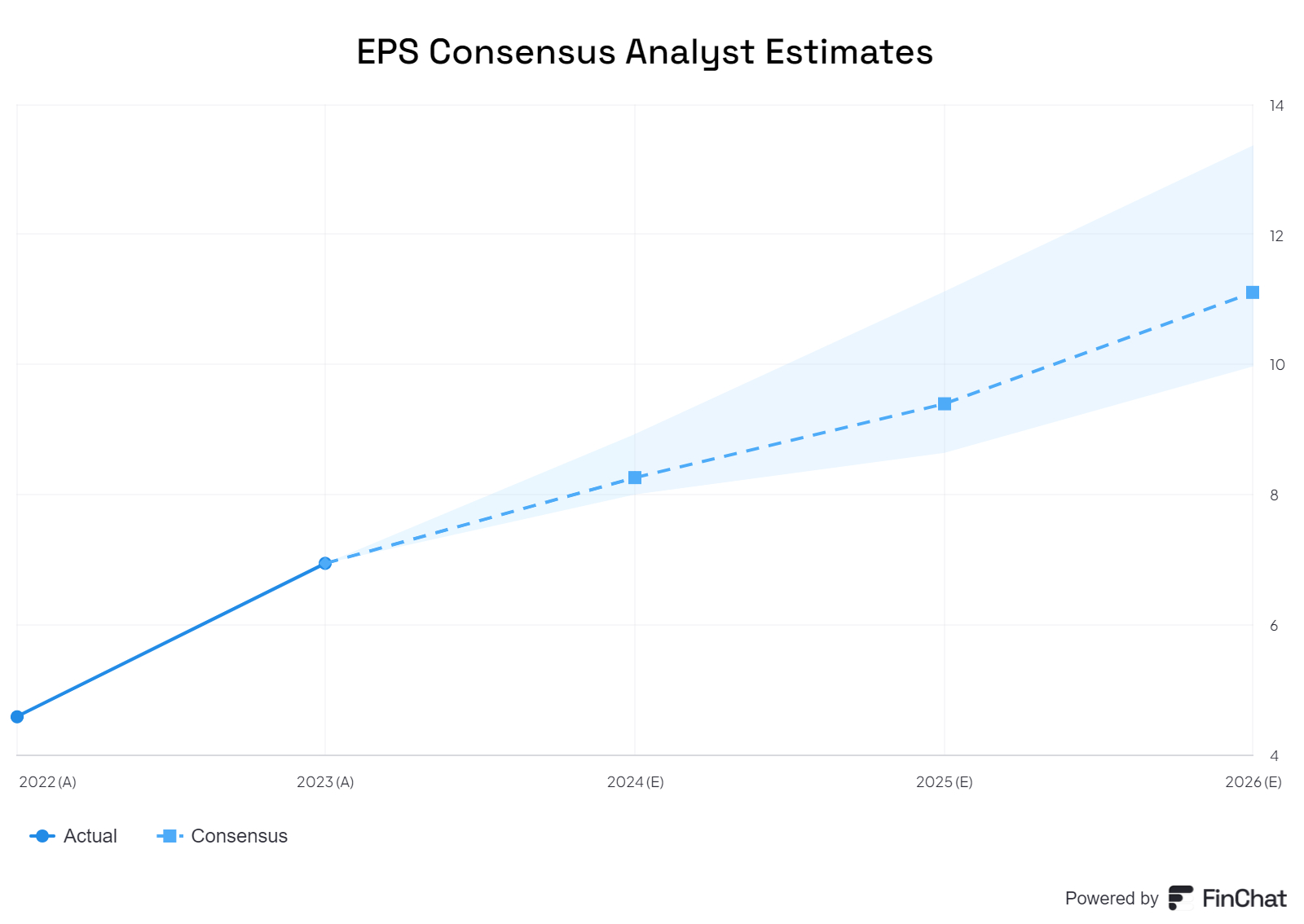

The consensus analysts’ expectations for FY 25 EPS and FY 26 EPS are $ 9.37 and $ 11.18 respectively (See chart above)

At the current share price of $ 314, it is on a two year forward P/E multiple of about 28x.

All the metrics indicate the stock is fully valued and not cheap at this levels . The best we can say it is fairly valued for a company which generates an ROE of ~34% and ROCE of ~27.5%.

Conclusion

We have held Arista Networks for some time, and it currently accounts for 3.5% of our portfolio.

We will continue to hold on to the position but will not add to it.