Arista Networks (ANET)

Q1 2024 Results

Arista Networks (ANET)

We have written a few times on Arista Networks (ANET) which can be found here, here and here.

We believe that the original report was one of our better efforts, both in terms of quality (it is worth re-reading), but also because the investment we made in ANET, after the report was published, is up 100%. The stock accounts for 6% of our portfolio and is up 72% from the average acquisition price.

We take a brief look at it in the light of its most recent quarterly results.

There are two key things to remember.

Microsoft and Meta still account for about 40% of the revenues of ANET.

Both companies have announced they are increasing their already high level of investments in computer networks in datacentres. This is driven by GenAI opportunities.

There should be good scope for ANET to continue their 10-year long run of high revenues growth which has seen shareholders get a total return of 36.3% CAGR.

The Quarterly Results

ANET reported healthy Q1 results with solid top and bottom-line growth year over year, driven by robust demand trends.

Both the bottom and the top lines beat the analysts’ consensus expectation

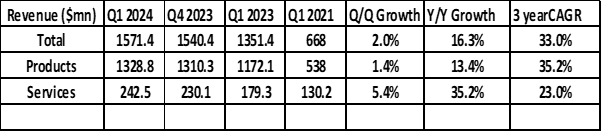

ANET reported Q1 2024 Revenues of $1.57 billion, an increase of 16.3% (q/q) from the first quarter of 2023.

Total Annual Revenues have risen 10X in the last ten years.

Net income of $638mn or $ 2 per diluted share, compared with net income of $437mn or $1.4 per diluted share in the first quarter of 2023, a growth of 46%.

On a three-year basis, revenues grew 33% CAGR while Net Profit and EPS grew 52% and 49% CAGR.

For Q1 2024, the growth of 16.3% was the slowest in three years though operating leverage has improved strongly. The 16% top line growth led to 43% growth in earnings per share indicating the high degree of operating leverage in the business model.

The slowdown reflects a “large number effect” where very high growth numbers of recent years makes for difficult comparisons.

Net quarterly sales from Product totalled $ 1.33bn, 13.4% higher previous than the same quarter last year. Service revenues increased 35.2% to $ 243mn.

ANET gross margin of 63.7% in the fourth quarter of 2023 and 59.5% in the first quarter of 2023. The effect of slower sales growth was greatly offset by an increase in margins (y/y).

The quarterly cash form operations was $ 513mn while free cash flow was an impressive $504mn. As a result, the company added to its already large cash reserves.

The net cash on the balance sheet was $ 5.4bn ( company has no long-term debt), an amount which gives rise to interest income of ~$ 177mn.

Company completed stock repurchases of $2 billion under previous stock repurchase programs. In May 2024, Arista’s Board authorized an additional program to repurchase up to $1.2 billion. However, such stock buying only partially offsets the generous stock awards to the employees and therefore the number of shares outstanding has risen slightly in recent years (see chart below). This is disappointing. One would hope, the average numbers of shares outstanding would be falling for such a comny, due to more shareholder friendly capital allocation policy.

Guidance

The company guidance for the current quarter is for

revenues of approximately $1.62 billion to $1.65 billion (4.7% growth (q/q) at the midpoint)

Gross margin of approximately 64% and

Operating margin at approximately 44%.

New Developments.

The press release form the company highlighted two recent developments.

Arista announced CloudVisionⓇ Universal Network ObservabilityTM (CV UNOTM), a network observability software, which merges network infrastructure performance and data from compute and server systems-of-record, to deliver keen insights into application and workload performance.

The second announcement concerned AI. ANET announced AIEtherlink platforms which deliver high performance, low latency, fully scheduled, lossless for AI networks.

Highlights from the earnings conference call

Company noted they are pleased with the momentum across all our 3 sectors.

· Cloud and AI Titans (40%-45% of market).

· Enterprise and Financial (35% to 40% of market).

· Service Providers (Telcos) and Tier 2 cloud players (20% to 25%).

“Customer activity is high as Arista continues to impress our customers and prospects with our undeniable focus on quality and innovation.”

They announced a new offering which they call Network as a Service (NAAS).

NAAS is an ANET initiative strategy, taking beyond providing network hardware and software, by providing customers with tools to provide services.

Customers sign up, choose a service level and Arista handles the rest including equipment procurement, deployment, implementing networks and monitoring etc.

“In an era characterized by stringent cybersecurity, observability is an essential perimeter and imperative. We cannot secure what we cannot see. We launched CloudVision and UNO in February 2024 based on the EOS Network Data Link Foundation”.

“The (strong) year-over-year margin accretion was driven by 3 key factors

· Supply chain productivity gains

· a stronger mix of Enterprise business and

· a favourable revenue mix between product, services and software.”

“Activity in Q1 alone, and I believe it will continue in the first half, has been much beyond what we expected. And this is true across all 3 sectors, Cloud and AI Titans, Providers and Enterprise.”

Summary

Arista continues to make the progress that we have seen in the last few years.

It is a much larger company than it was just 3-4 years ago and therefore growth going forward is likely to be at a slower pace than seen in the last few years.

However, margins increased strong in the last years.

Company continues to be very profitable with a Return on Equity (ROE) of around 30%.

Valuation

At the current share price of $ 309 per share, the company is trading at a forward P/E ratio of 37.4 X and a current Price to Free Cash Flow ratio of 45.5X. These imply and earnings yield of 2.6% and 2.2%.

These multiples do look a little expensive for a company with the ability to generate ROE of about 30%. However, give the likely demand growth and the strong operating leverage in the business model currently, the degree is of overvaluation is probably not too high.

Conclusion

We have a 6% holding in ANET in our portfolio and will continue to hold on.