Blackstone Inc (BX)

A first note

There have been a number of notable broad trends in the US asset management industry in the last three decades. Three of these are:

1. a great increase in investment in passive, liquid, low-cost investments such as ETFs and this has greatly boosted companies like Blackrock and the unlisted Vanguard.

2. a huge increase of funds into Hedge Funds which typically offer some liquidity (monthly or quarterly). In the last few years, growth in the sector has been in multi-strategy Hedge Funds (“Pod Shops”) at the expense of single strategy funds. The big winners here have been companies like Citadel and Millenium.

3. a tremendous boost of investment into illiquid private investments such as Private Equity, Private Credit, Real Estate, Infrastructure. The big listed winners in this listed space (often confusingly called alternative asset managers) have included Blackstone, KKR and Apollo Global.

These major trends have created huge firms. The relative “losers” have been traditional long-only active managers such as Franklin Templeton, Legg Mason, Fidelity and others.

We want to get a quick understanding of some of the listed players in the Private Equity space and we will begin by looking at Blackstone Group Inc.,

Introduction to Blackstone Group Inc.

Blackstone Group Inc. (BX) is the largest global alternative asset manager. It was founded in 1985 and listed in 2007. Its assets under management (AUM) crossed $1trn ($1,000,000,000,000 (!)) in 2023. It has a market capitalisation of $132bn and net worth of about $7bn. Since the IPO in 2007, it has given a CAGR total return of 15.6% to shareholders.

BX manages money in investment vehicles focused on Private Equity, Non-Investment Grade Credit, Infrastructure, Secondary Private Equity Fund of Funds and Multi-Asset strategies. It also invests in Investment Grade Credit for Insurance company clients.

BX makes money from Management Fees and Performance fees (“Carried Interest”)

Business Segments

The two main business segments in terms of revenue are Real Estate and Private Equity.

Real Estate (39% of Revenue) - The Blackstone Real Estate Partners funds target a range of opportunistic real estate and real estate related investments.

Private Equity (31% of Revenue) - The Private Equity segment includes its corporate private equity business, which consists of its corporate private equity funds, Blackstone Capital Partners funds, its sector-focused corporate private equity funds, including its energy-focused funds (Blackstone Energy Partners funds) and its core private equity fund.

Credit & Insurance (10%) - The Credit segment consists principally of the erstwhile business of GSO Capital Partners LP which is now known as Blackstone Credit.

Hedge Fund Solutions (8% of Revenues) - The Hedge Fund Solutions segment consists of Blackstone Alternative Asset Management.

A detailed look at the business segments

Real Estate

Real Estate is globally integrated business, with investments in the Americas, Europe and Asia.

The main vehicle for direct investment is the Blackstone Real Estate Partners (“BREP”) Funds.

The BREP Funds are geographically diversified and target a broad range of “opportunistic” real estate and real estate-related investments. The Funds include global funds as well as funds focused specifically on Europe or Asia investments.

BREP invests thematically in “high-quality” assets. Past themes have included Logistics, Rental housing, hospitality esp. hotel franchises and Retail. The current themes are Logistics, Rental Housing and Technology (AI Datacentres).

Investment in real estate debt is done through Blackstone Real Estate Debt Strategies (“BREDS”). BREDS provides commercial real estate and mezzanine loans and buys residential mortgage loan pools and liquid real estate-related debt securities.

The BREDS platform includes

A number of high-yield real estate debt funds and Blackstone Mortgage Trust (BXMT) a $3.1bn, NYSE-listed real estate investment trust (“REIT”).

In November 2020, Blackstone Real Estate launched Blackstone BioMed Life Science Real Estate L.P. (“BPP Life Sciences”), a long-term, perpetual capital, core+ return fund that owns BioMed Realty and is focused on life science office investments, primarily across the U.S.

Private Equity.

Blackstone Private Equity is corporate private equity business. In Private Equity, BX pursues transactions across industries in both established and growth-oriented businesses globally. The company claims they target “control-oriented “investments in high-quality companies with durable businesses and seek to offer a lower level of risk and a longer holding period than traditional private equity.”

The main Private Equity platform is Blackstone Capital Partners (“BCP”) family of Funds.

They also have sector-focused private equity funds, including energy-focused funds. The latter are known as Blackstone Energy Partners (“BEP”) funds.

In Asia, they have Blackstone Capital Partners Asia (“BCP Asia”) fund).

In addition, they have something called Core Equity and the relevant Fund business is called Blackstone Core Equity Partners (“BCEP”).

Private Equity also has an opportunistic investment platform that invests globally across asset classes, industries and geographies. This is called Blackstone Tactical Opportunities (“Tactical Opportunities”).

One of their best past deals in Private Equity involved Hilton Hotels.

“Blackstone's acquisition of Hilton was achieved through an all-cash leveraged buyout, or LBO which is an acquisition of another company completed almost entirely through debt. In the case of Hilton, $20.5bn , or 78.4 percent, was financed through debt with the remaining $5.6bn in equity. At the time of the deal, the Wall Street Journal called it “one of the group’s more aggressive forays,” and “at a time when the market is full of talk about tightening conditions for leveraged deals. “The deal, which could have easily gone sideways since it was made just prior to the Great Recession of 2008, bagged Blackstone a hefty sum. The firm netted a $14bn profit when it fully cycled out of it in 2018.”

Source: Wikipedia

They also have

a secondary fund of funds business called Strategic Partners Fund Solutions (“Strategic Partners”),

An infrastructure-focused funds family called, Blackstone Infrastructure Partners (“BIP”),

A life sciences private investment platform, Blackstone Life Sciences (“BXLS”) and

A growth equity investment platform, Blackstone Growth (“BXG”),

A multi-asset investment program for eligible high net-worth investors called Blackstone Total Alternatives Solution (“BTAS”) and

A capital markets services business, Blackstone Capital Markets (“BXCM”).

Some of the business segments are perhaps not self-explanatory, so we will give a little information on some of them.

Tactical Opportunities

Tactical Opportunities invests globally across asset classes, industries and geographies, seeking to identify and execute on attractive, differentiated investment opportunities, leveraging the intellectual capital across their various businesses.

Strategic Partners

Strategic Partners is a total fund solutions provider that acquires interests in high-quality, third-party private funds from original holders/investors seeking liquidity, makes primary investments and co-investments in third party funds with financial sponsors and provides investment advisory services to clients investing making primary and secondary investments in private funds and co-investments.

We have looked at Real Estate and Private Equity. The other smaller business segments are Credit & Insurance and Hedge Fund Solutions.

Credit & Insurance (C&I)

The origins of this business are with a company GSO Capital Partners. GSO was founded in 2005 as a credit hedge fund. It had focused on Leveraged Finance and non-investment grade credit. In 2008, Blackstone acquired GSO for approximately $1bn. In 2020, the GSO name was changed to Blackstone Credit.

BX broadened the product to a much wider range of Private Credit including Investment Grade (IG). BX are not just investors in Credit but also act as originators/arrangers. They approach potential borrowers/issuers, including companies that their Private Equity division might have invested in, and place the private debt with their various credit and real estate funds. This is a different business model. From being an independent investor – just a buyer of debt, they have pivoted to also being an originator and seller as well. This might give rise to internal conflicts of interest which will have to be navigated carefully.

In the Insurance segment of C&I, BX are a third-party investment manager for Insurance companies. They currently have strategic partnerships with four large insurance companies and Separately Managed Accounts (SMAs) with twenty-five. BX consistently differentiate their strategy from that of Apollo Global (APOL). The latter has formed/acquired an insurance company called Athena and therefore operates an insurance company creating fixed liabilities and investing premiums collected in fixed-income assets. BX emphasises they are an independent, fee-earning manager for insurance company clients and state they have no intention of competing with their clients.

Hedge Fund Solutions.

This business is called Blackstone Alternative Asset Management (“BAAM”). BAAM is the world’s largest discretionary allocator to hedge funds. It also has investment platforms that seeds new hedge fund businesses and purchases minority interests in more established general partners and management companies of Hedge Funds. BX is not primarily a Hedge Fund Manager but an investor in Hedge Funds and Hedge Fund Management Companies.

Sources of Revenue

BX generates revenue mainly from fees earned arising from contractual arrangements with funds and institutional investors.

They also make money from the provision of capital markets services.

BX also sometimes invests a small percentage of its own capital in the Funds they manage.

Private equity funds are usually structured as limited partnerships with a general partner (GP) and various limited partners (LPs). Limited Partners are the outside investors in the Fund while the promoters are the investment managers for the Fund.

BX gets the Carried Interest which is the performance or incentive fee in a private equity fund that is paid to the General Partners (GP). The economics of carried interest structure means GPs are entitled to a disproportionate allocation of the Performance fee income otherwise allocable to the limited partners.

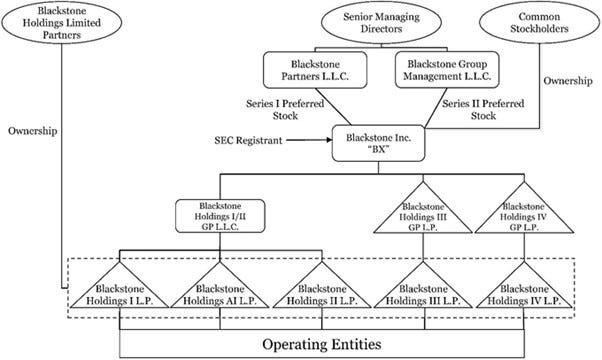

Organizational Structure of BX

The diagram below depicts BX organizational structure. It excludes certain subsidiaries.

The listed entity (BX) is owned by common stockholders (ordinary shares) and by Senior Managing Directors (Preferred Stock) via two entities: Blackstone Partners LLC and Blackstone Group Management LLC.

BX itself owns operating entities via three holding companies which in turn hold five holding companies. These latter lower-level holding companies also have Blackstone Holdings Partners (BHP) as shareholder. BHP is owned by key senior staff of BX. BX is not the 100% owner of its operating entities as BHP is a minority shareholder.

The structure is more complex than it probably needs to be. Complex structures are usually a warning sign for minority investors. There are likely to be a lot of leakages in complex structures before money is distributed to external ordinary shareholders.

A Quick look at Summary Financials

We will take a look at some summary financial numbers to get a quick idea on the scope and scale of BX’s business.

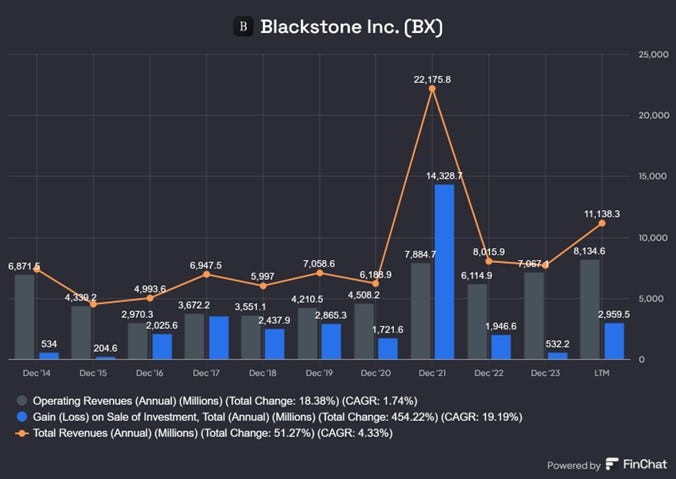

Total Revenues are composed of the fees earned (operating revenues) and realised gains and losses on the sale of investments (if any). The first is relatively stable but the latter can be volatile depending on the timing and magnitude of sales and the gains made.

In FY 2023, Operating Revenues were $7bn while gains were just $523mn. By contrast, in FY 2021 Operating Revenues were $7.8bn but gains were a much larger $14.3bn. BX clearly had some very profitable exits from investments in FY 2021.

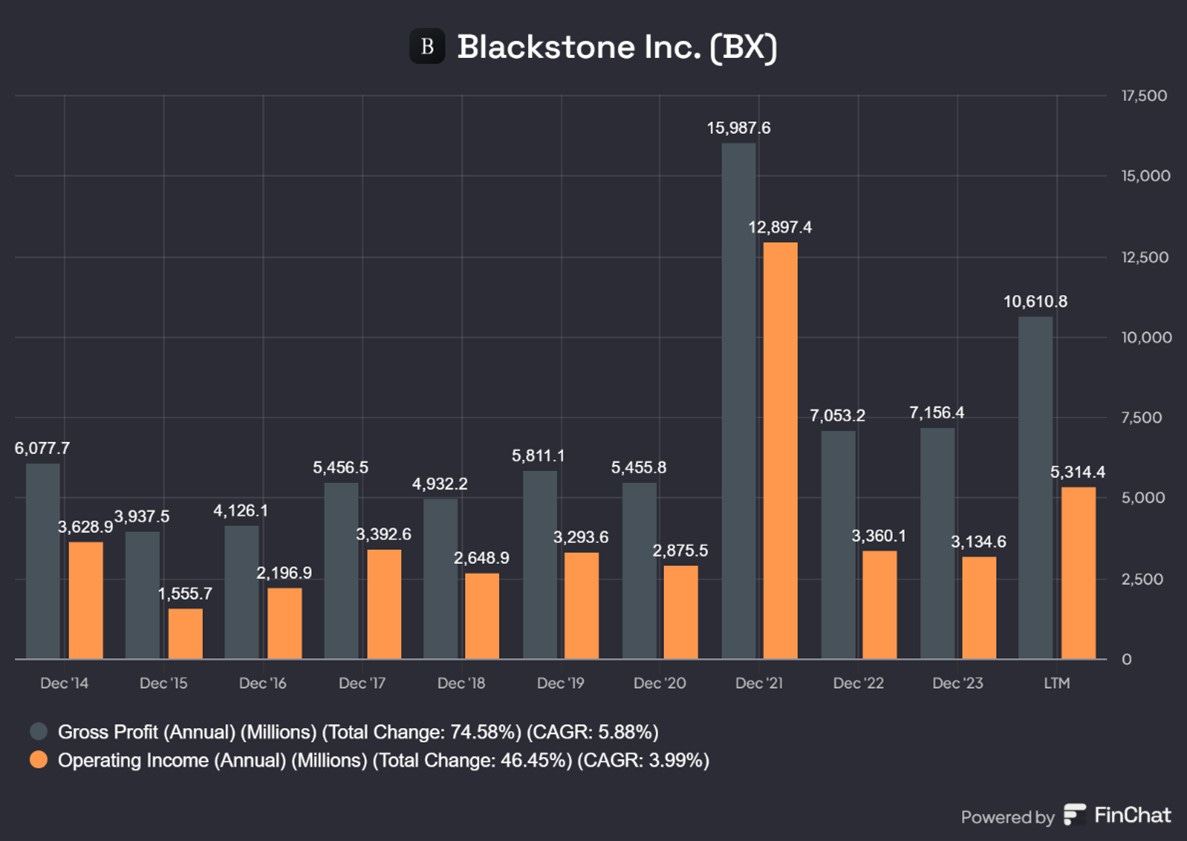

In a fee-earning business, cost of goods sold (COGS) is not relevant and usually quite small. The bulk of Total Revenues translate to Gross Profit. The Gross Margin in FY 2023 was 93.1%

Operating Income is about 50% of Gross Profit. The difference between the two is Sales and General Admin Costs (SGA). These are the operating expenses of the company. These are quite high for a fee earning company as salaries and earnings are the major expense.

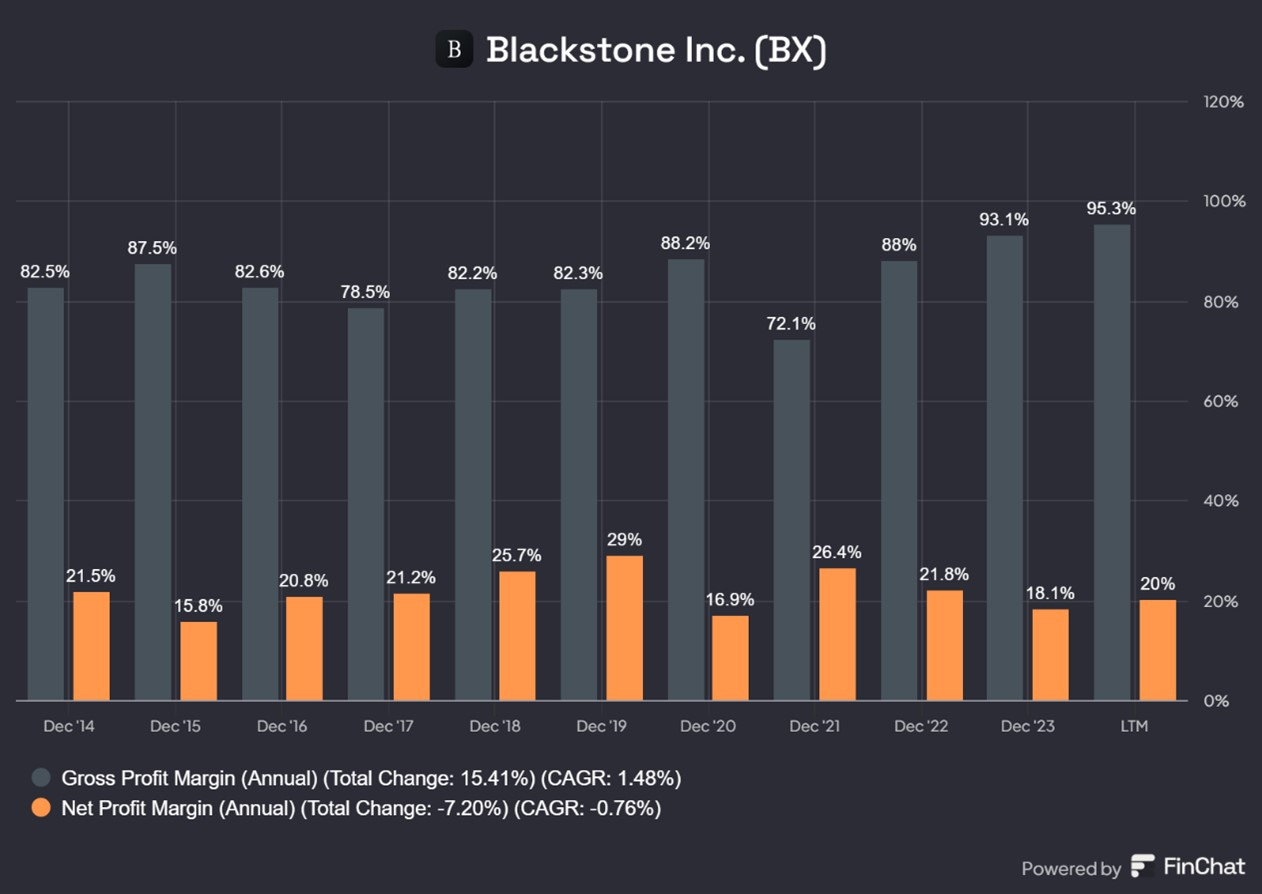

Net profits margins at 20% are much lower than Gross margins of 90% plus. This is not surprising given it is a fee earning, people-driven capital light business with substantial minority equity holdings in its operations.

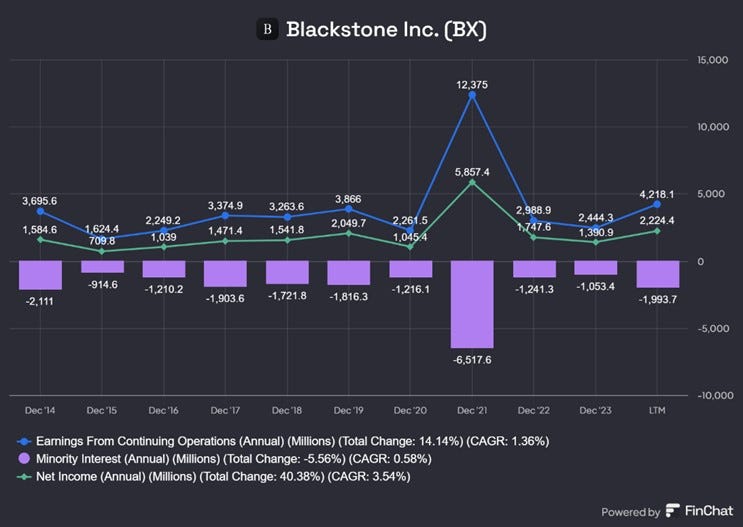

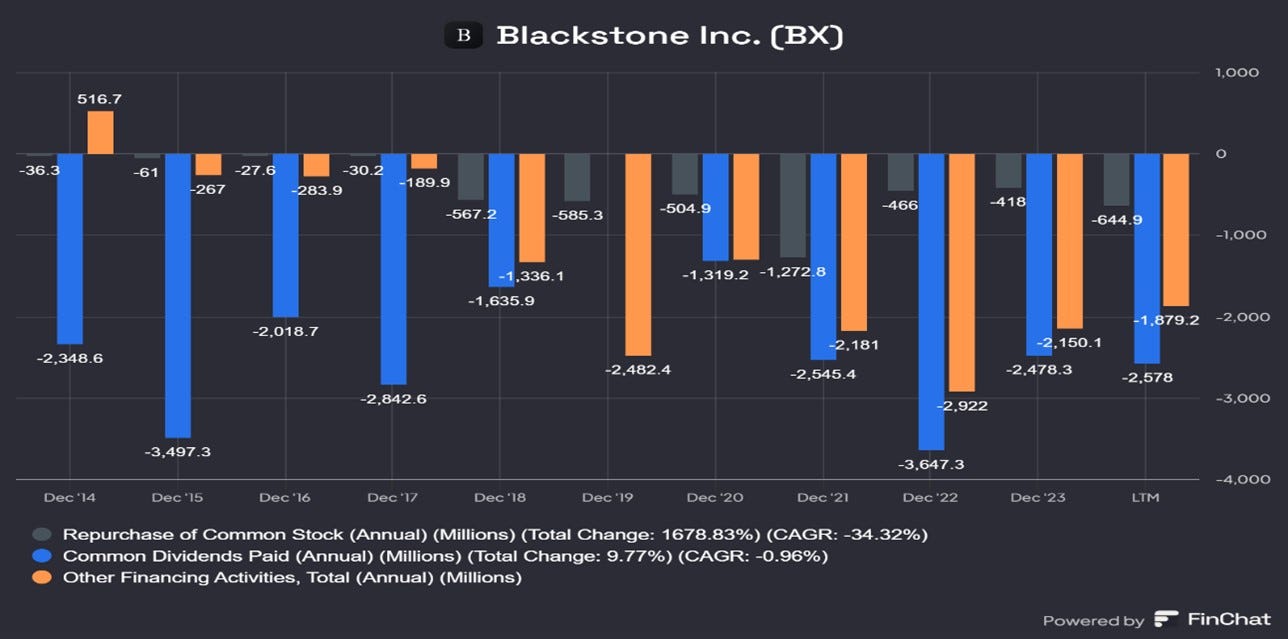

We noted above on the organogram which showed that Blackstone Holding Partners (BHP) has a minority interest in BX’s operating companies. Therefore, a minority interest has to be paid out form operating earnings. The minority interest payout is shown as a purple bar in the chart below. It is shown as negative as it is a cash outflow from BX. Minority interest is a very significant 50% of the Operating Earnings. A vehicle owned (BHP) by the senior partners of BX receives about 50% of BX’s operating earnings. Senior Partners of BX take a very high level of the earnings. BX is a listed company but, in this regard, at least, it has features of a Partnership.

The Chart above shows Annual Net Income and Minority Interest. In FY 2023, Reported Net income was $2.4bn. $1bn was distributed to the minority investors (i.e. BHP). About $ 1.1bn was for non-controlling ordinary shareholders

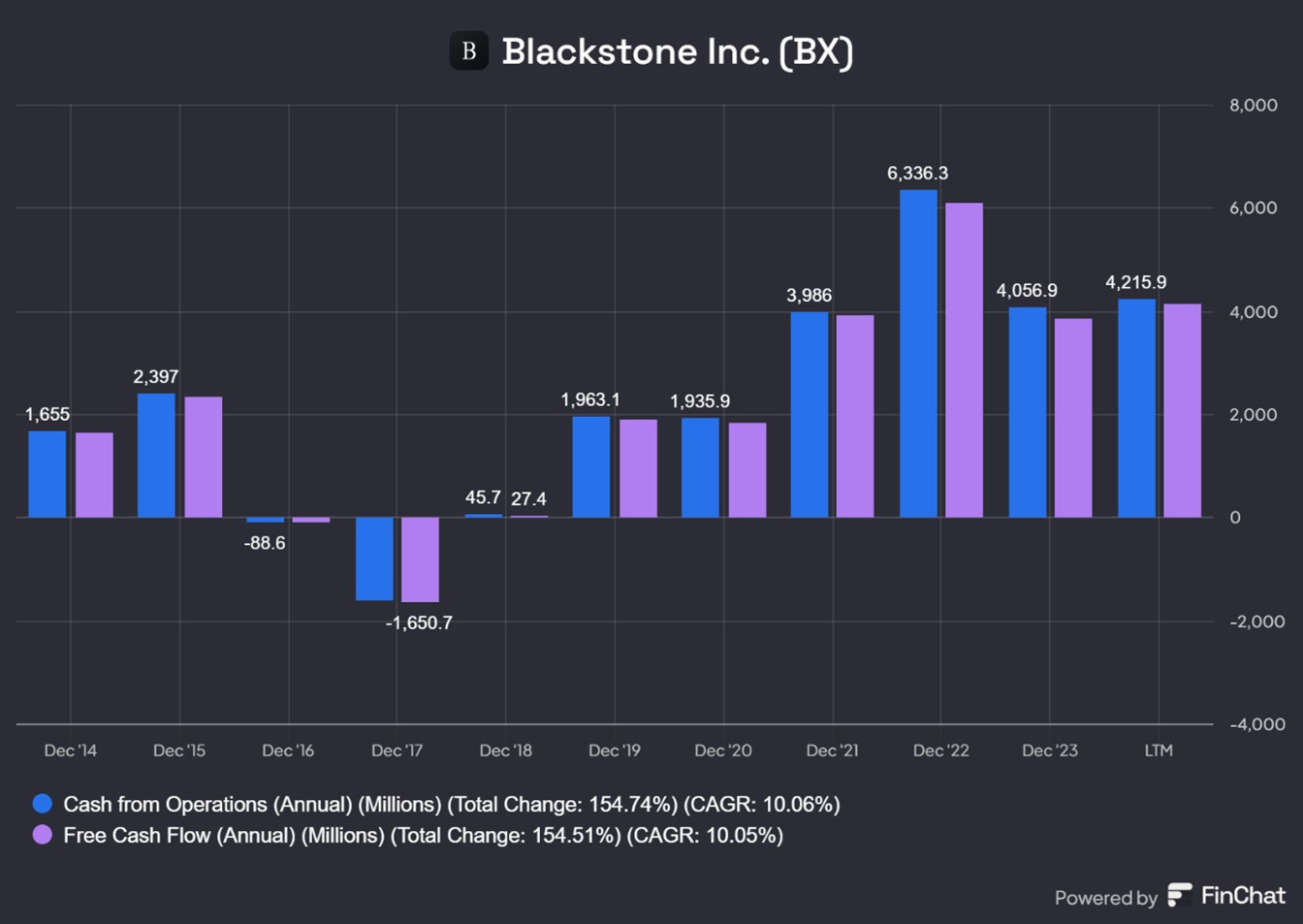

Operating Cash Flow are almost equal to Free Cash Flow as no Capex is required.

The dividend accounts for a high 50% to 60% of Free Cash Flow.

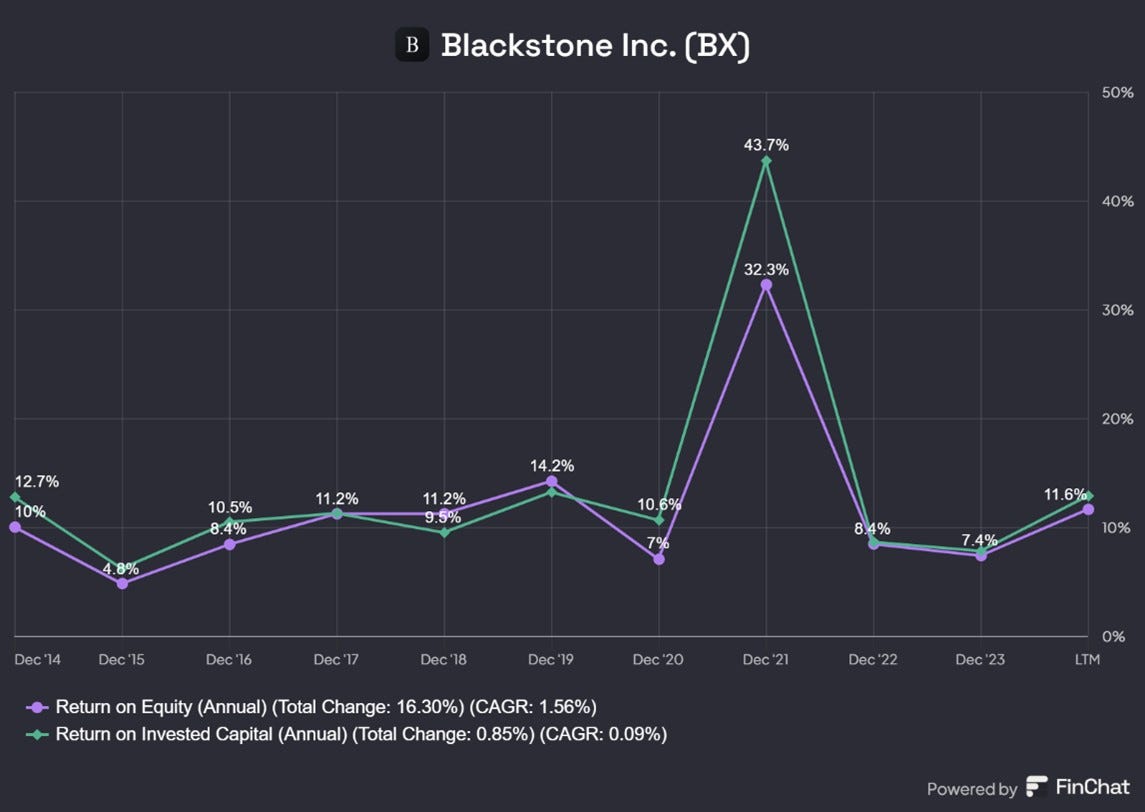

BX’s profitability can be boosted dramatically in years such as 2021 when there are large profitable exits from investments such as in 2021. In more normal years, profitability as measured by Return on Equity is in the range of 8% to 14%.

Blackstone’s Business Drivers

There has been a huge growth in private assets in the four decades since Blackstone was founded. The key driver of this was David Swendsen, who was appointed as the Chief Portfolio Manager of Yale Endowment Fund in 1985 at the age of just 31. Swendsen developed what later became known as the Yale Model or the Endowment Model.

Swendsen described the model in his 2000 book, 'Pioneering Portfolio Management.” The model requires broadly dividing a portfolio into five or six roughly equal parts and investing each in a different asset class.

The emphasis is on broad diversification and an equity orientation, avoiding asset classes with low expected returns such as fixed-income and commodities. The key revolutionary idea was that liquidity is a bad thing, something to be avoided as it comes at a heavy price in the form of lower returns. The Yale Model has relatively heavy exposure to asset classes such as private equity compared with prevailing traditional portfolios.

The Yale endowment carefully selected outside investors rather than manage the money in-house. In the early days, not many investment firms specialised in the asset classes that Swensen was interested in. Yale had to become a venture capitalist of venture capitalists. They invested in the equity of new investment firms, many of which received allocations of capital to manage as well. As of 2019 about 60% of the Yale endowment portfolio is allocated to alternative investments such as hedge funds, venture capital and private equity.

Under Swendsen's guidance, the Yale Endowment saw an average annual return of 11.8% from 1999 to 2009 and this was better than what was achieved by most other university endowments and institutional investors. Investment heads from many other universities including Harvard, Princeton, MIT, Wesleyan and University of Pennsylvania adopted the Yale Model. Many other institutions including Pension Funds and Insurance Companies adopted the model, especially after the publication of Swendsen’s book in 2000.

The success of the Yale Model and its widespread imitation by other institutional investors led to a growth in demand for the services of private asset fund managers. Blackstone and other firms grew strongly in response to this demand.

Blackstone moved into Real Estate for the first time in the early 1990s, after the values collapsed after the Savings and Loans (S&L) crisis. The government had set up a company called the Resolution Trust Corporation (RTC) which bought Real Estate portfolios from the collapsed S&Ls. It then sold them on at distressed prices and Blackstone was a buyer.

After the Global Financial Crisis, US house prices collapsed and there were a lot of foreclosures on Single Family Residential (SFR) mortgages by US banks. Blackstone bought SFR homes at distressed prices. It has become the largest single residential landlord in the world as it has continued to invest in residential real estate in the last 15 years.

By 2010, Real Estate had become a second significant leg in BX’s business after Private Equity

After the Global Financial Crisis in 2009, the US Federal Reserve left interest rates near zero for almost twelve years. Bond yields fell to historically low levels. This encouraged investors to borrow to “reach for yield” and seek higher yielding assets. In fixed income, this meant going down the credit curve and into more illiquid assets. This decade long period led to a huge growth in the market for private credit and this has been a huge growth area for BX.

In summary, Blackstone started as an advisory business in 1985. It then become a large player in Private Equity. They ventured into Real Estate in in 1991 when values collapsed following the S&L crisis. They had expanded into Credit by taking over GSO in 2008. BX became America’s largest landlord of SFR homes and thus probably the largest global player in real estate in the aftermath of the Global Financial Crisis of 2008/09. In the last decade they have become a major intermediary and investor in private credit. They started and developed a dedicated private wealth business in 2011 and introducing the first large-scale perpetual product for that channel in 2017. In 2025, their assets under management crossed over $1trn.

The Recent History of Blackstone

In order to understand today business situation and business mix at Blackstone, we decided to go back starting with the 2018 Investors Day Presentation.

2017/18 must have been a very strong period as they stated the following:

“Blackstone has grown assets under management by $168bn or over 60%. We've expanded our existing businesses into new geographies and new product areas and also added several completely new business lines.”

In ball park numbers, their AUM in a twelve-month period went from about say $105bn to $273bn around 2018.

“In our Private equity funds, since 1987 we've delivered returns to our limited partners of 15% per year, net of all fees. In Real Estate, 16% annually since 1991, net of all fees. These funds have beaten the relevant public market indices by 7% to 9% on average.”

7% to 9% per year difference can compound to huge cumulative difference if it persists for some time.

“That's 700 basis points to 900 basis points on average with an exceptionally low rate of realized losses. In total, across the firm, we've created approximately $200bn of gains since inception for our investors and their beneficiaries. Our performance over 33 years is what sustains us as a firm.”

“Our firm has become the go to alternative manager for investors around the world, and our share of wallet for these rapidly growing pools of capital is by far the largest. Our extensive array of alternative products, combined with the Blackstone brand, creates a huge moat around our franchise. And that's why we've been able to take $400,000 of start-up capital in 1985 and turn it into $439bn of assets we manage today. That's a compound rate of growth, for those who care of 52% a year for 33 years.”

Annual strategic planning process

In 2018, they described their strategic planning process.

“We have an annual strategic planning process, that challenges each of our businesses to create 1 to 3 new product ideas per year. Our ability to aggregate intellectual capital enables us to better evaluate each of these ideas because we want them to be successful. The firm's decision to move forward with the new business idea is based on 3 principles.

1. there has to be a substantial opportunity in the market to create something special for our investors and to generate outsized risk adjusted returns.

2. we have to identify the right leader. We only attack new initiatives with absolutely first-class people, and we do attack them.

3. any new business has to further increase the firm's intellectual capital so that the entire organization is always to become no 1 in this space and move the new business rapidly to profitability on a stand-alone basis. We're also risk averse and approach every day believing that we're only as good as our last investment decision and our latest fund.

“Our IPO (in 2007) and the capital we raised before the financial crisis helped us not only survive but thrive and gave us the opportunity to extend our leadership position in basically every area. At the time of our IPO, we had 4 primary businesses and $88bn of AUM. Corporate Private Equity consisted of 1 actively investing opportunistic fund. Real Estate had 2 opportunistic funds, one focused on North America and the other on Europe. Our credit business was primarily comprised of CLOs and a mezzanine fund, while in hedge funds, we were evolving from co managed products to a greater focus on customized solutions.”

“Fast forward to today (2018) And we've created something unique in virtually every area, adding dozens of new product areas and several altogether new business lines. The firm is 5x larger today than it was at our IPO at a time when most financial institutions were shrinking and more diverse than any of our peers.”

“Just as a reference point, if we grow at a low double-digit rate, which is slower than our growth rate of the past several years, we would reach $1trn of AUM comfortably within the next decade. I think that would be a remarkable achievement for a business that started with $400,000 of capital.”

In fact, with the benefit of hindsight, we can say they achieved an AUM $1trn within 6 years.

Blackstone today

“We now have 75 individual investment strategies, and we are working on many more currently. Our near-term plans include launching several new products in the private wealth channel, the global expansion of our infrastructure platform, further deepening our penetration of the private credit and insurance markets, and expanding our business in Asia.”

We hope to understand the Private Equity sector by researching this piece. Private Equity companies operate by offering two types of Funds. Drawdown Funds and Evergreen Funds. Investors in both types of Funds are committing capital for long periods. One common structure is 7+2 years where money is locked up for seven years and the Fund Manager has an additional two years (if needed) to exit the investments. The long lockdown period is designed to reflect the illiquidity of the underlying investments of the Fund.

Lockdown Funds, which are more common than Evergreen Funds, aim to eventually invest all of the capital in illiquid assets. Evergreen Funds invest mostly in illiquid private assets but have some allocation to liquids as well so they can offer some limited liquidity to investors who wish to exit.

We will focus on Lockdown Funds only as they are the most common vehicle. When a PE firm raises a Fund, investors make a commitment to invest. The actual funds are only advanced or a drawdown called once investment opportunities have been identified and decided on.

In drawdown funds, management fees are typically charged on committed capital during the investment period, switching to being charged on invested capital thereafter (in some strategies, management fees are charged on invested capital throughout the life of the fund). Charging on invested capital means that management fees are only charged on the cost basis and decline over time as investments are harvested.

An established company like BX would have a range of funds in various stages ranging from the marketing phase, deployment phase, fully invested and actively harvesting or divesting.

We can compare the situation of mutual fund manager and a PE firm. The former can collect money at any time by creating units but faces the risk of money leaving at any time due to redemptions. This redemption risk means mutual fund investors have to invest in relatively liquid assets. In fact, their investment rules may forbid investment in illiquid assets. The UK had a number of property mutual funds which invested in property but offered daily redemptions to their investors. In periods of stress, these funds were unable to meet liquidity demand needs and redemption facility had to be suspended. This led to a crisis in the sector. A Mutual Fund is revalued every day by marking to market daily by an external independent administrator. The NAV and the performance are transparent and visible to all,

A PE Fund manager can only market the fund during the launch phase but has no risk of redemptions for about 7 years. They get semi-permanent capital. The PE Fund investment cannot be marked to market as there is no reliable market. Therefore, the NAV is derived by a series of estimates, approximations and guesses. It has to be done periodically say quarterly but it makes no sense to have a daily calculation. The valuation process and the performance derivation is opaque. There are many rules and safeguards around the process but there is an element of the PE Fund marking their own homework.

The assets of PE Funds are semi-permanent but are clearly shorter dated than assets held by Pension Funds and Insurance companies. Blackstone has raised some perpetual capital while rivals Apollo and KKR have gone into the insurance business to increase the duration of the capital they can deploy.

Real Estate

Blackstone moved into Real Estate for the first time in the early 1990s, after the values collapsed after the Savings and Loans (S&L) crisis. They moved into Residential Real Estate after values collapsed in the aftermath of the Global Financial Crisis.

“This demonstrated ability to be in the right place at the right time continues on an accelerated basis today.”

“During the global financial crisis, most competitors were forced out of business or delivered mediocre results. In fact, sometimes losing money for their customers, where Blackstone, for our investors, ultimately doubled their money.”

They do not offer a standard Real Estate investment strategy but concentrate on a small number of themes.

“How did we do it? We owned the right assets in the right sectors with the right capital structures, enabling us to emerge from the crisis as the clear market leader. As a result, institutional limited partners and subsequently, individual investors allocated significant capital to Blackstone real-estate in contrast to most other real estate managers. With that capital, we repositioned our portfolio over time by selling US office buildings and instead bought warehouses, rental housing, and eventually datacentres.”

“These three sectors comprised approximately 75% of our global real-estate equity portfolio today compared to 2% in 2007. This repositioning drove the outperformance and extraordinary growth of our real-estate business over the last decade and a half. Real-estate markets, of course, are cyclical, and over the past 2.5 years, the increase in interest rates and borrowing costs has created a more challenging environment. Even through this period, Blackstone real estate has delivered differentiated performance.”

Their listed Real Estate Investment Trust (BREIT) has greatly outperformed the REIT sector

“BREIT for example, has generated a cumulative return of 10% net in its largest share class since the beginning of 2022 and 10% plus net returns annually since inception 7.5 years ago, more than double the return of the public-REIT market. Nearly 90% of BREIT's portfolio is in warehouse, rental housing, and datacentres, with datacentres alone contributing almost 500 basis points to returns in the last 12 months. The performance BREIT has achieved is the key reason it is 3x larger today than the next five largest non-traded REITs combined.”

They are optimistic that Real Easte prices are due to rise now. One reason for this is the reduction in supply.

“We believe creating the basis for a new cycle of increasing values in real estate. At the same time, new construction for most types of real-estate is declining dramatically, down 40% to 70% year-over-year, depending on the asset class.”

They are strongly focused on meeting the very strong demand for AI Datacentres.

“Today, Blackstone is the largest datacentre provider in the world with holdings across the U.S., Europe, India, and Japan. Last month, we announced another major expansion by agreeing to acquire Air Trunk, the largest datacentre operator in the Asia Pacific region for $16 billion. We were uniquely positioned to execute on this investment, given our expertise in this sector, the scale of our capital, the global integration of our teams, and our connectivity to the world's largest datacentre customers.”

They see a great opportunity to not just provide AI datacentre infrastructure but also the significant power generating infrastructure that AI datacentres need.

“The Blackstone portfolio consists of $70bn of datacentres and over $100bn in prospective pipeline development, including Air Trunk and facilities under construction. We've conceptualized this new business area, built conviction, and in only three years, scaled it to the largest platform in the world. And there is much more we're doing and plan to do in this area, including addressing the sector's growing power needs, which we believe will create enormous additional opportunities for investment over time.”

Another reason for their belief that the real estate cycle is due to turn is that BREIT redemption requests have fallen and it is moving toward net inflows of investor funds.

“Turning to the recovery in commercial real estate. With the cost of capital moving lower (this was stated in mid-2024), we've previously discussed our expectation of a new cycle of increasing values and improving investor sentiment towards the sector. One indication of this shift now underway is the renewed interest in the asset class from limited partners and financial advisors, notably for BREIT. Repurchase requests in September were down over 90% from their peak, and we're seeing encouraging signs in terms of new sales.”

BREIT is clearly moving towards positive net flows based on current trends. The vehicle's largest share class has outperformed the public REIT index by approximately 50% annually since its inception nearly eight years ago. We believe BREIT's standing as the largest vehicle of its kind by far with strong investment performance and exceptional portfolio construction, including nearly 90% concentrated in warehouses, federal housing, and datacentres. It positions the vehicle extremely well in the context of improving flows into private real estate.

“Historically, in multi-year recovery periods following a downturn, private real estate has delivered approximately double the returns of all periods. As the largest owner of commercial real estate, this dynamic should be quite positive for Blackstone and our investors. Overall, our limited partners have benefited significantly from the exceptional balance of the firm and the careful way we've positioned their capital in a volatile world. Looking forward, our business is accelerating, and we are in the early days of penetrating markets of enormous size and potential.”

Credit and Insurance

“Our credit and insurance business is thriving in an environment of higher interest rates and accelerating demand for both investment-grade and non-investment-grade strategies.”

They believe the health of their credit portfolio is very good

“Our performance has been outstanding, with minimal defaults of less than 40 basis points over the last 12 months in our non-investment-grade portfolio. Our scale allows us to focus on larger investments, where competitive dynamics are more favourable, and where the quality of borrowers and sponsors is higher.”

“In our nearly $120bn global direct lending business, our emphasis on senior secured positions with average loan-to-values of 44% provides significant equity cushion subordinate to our loans. We're the sole or lead lender in approximately 80% of our U.S. portfolio, helping us to drive document negotiations and control the dialogue with borrowers if any challenges arise.”

In the Investment Grade (IG) Credit business, they invest in IG Debt mainly for Insurance companies. This IG debt they claim yielded 185bps more than equivalent or equivalently rated publicly announced and traded IG bonds. That is substantial difference. As noted above, they are not just investors but are also originators of such debt which they place with their insurance companies among others.

“In our investment-grade focused credit business, our goal is to deliver higher yields to clients, primarily insurers, by migrating a portion of their liquid portfolios to private credit. We place or originated $24bn of A-rated credits on average in the first half of 2024, up nearly 70% year-over-year, which generated approximately 185 basis points of excess spread versus comparably rated liquid credits. Our insurance AUM grew 21% (y/y) to $211 billion, driven by strong client interest in our asset-light open architecture model.”

Infrastructure

Infrastructure is a relatively newer business. These are, by definition, very long-dated assets. The Blackstone Infrastructure Partners (BIP) fund has raised permanent capital. BX claims that at assets of $100bn, it is one of the largest platforms of its type.

“Moving to infrastructure, our total platform across the firm now exceeds $100 bn, including our perpetual BIP strategy, infrastructure secondaries, and other infrastructure equity and credit investments. We built this platform from the ground up to become one of the largest in the world. BIP specifically reached the $50bn milestone, including July fundraising, up 21% from year end 2023.”

“In the perpetual vehicles, we raised over $6bn in the second quarter, and nearly $13 billion in the first half of the year, already exceeding what we raised from individuals in all of 2023.”

They define Perpetual Capital as below:

“Perpetual Capital refers to the component of assets under management with an indefinite term, Perpetual Capital includes co-investment capital with an investor right to convert into Perpetual Capital. It represents capital we manage that has a longer duration and the ability to generate recurring revenues in a different manner than traditional fund structures.”

The graphic above suggests that nearly 30% of their capital is Perpetual. This is much higher than we were expecting. The bulk of this is Real Estate (may be mainly BREIT) and Private Credit (maybe sourced from Insurance companies). This needs to be looked into further.

Private Wealth

The more nascent business in the mix is Private Wealth. Historically, Blackstone’s client base has been Institutional investors. BX and their competitors have had great success in the last three decades in attracting Institutional capital. To some degree, they must have penetrated the sector to a great degree and so it difficult to grow their institutional money. BX are looking at Private Wealth (Family Offices, High Net Worth Individuals etc) as a potential source of growth.

“Moving to our private wealth business, where our momentum has been accelerating. We raised $7.5 bn in the channel overall in the second quarter.”

They have to tap Private Wealth money using distribution partners such as Private Banks and other financial intermediaries.

“Well, I'd start with this being a huge strategic area of focus to your point. We started, I think, 15 plus years ago doing drawdown funds for very affluent clients with our distribution partners. 8 years ago, we really revolutionized access to alternatives for individual investors by creating modern semi liquids, BREIT, then BCRED, private equity strategies. We're now into infrastructure. We're going to have a multi asset credit product.”

“We now have more than 300 people who focus on distribution. And the most important thing is that we've delivered great results, be it in BREIT or BCRED, the products we have here, because ultimately just like our institutional clients, it's about performance. And we are laser focused on delivering great performance.”

“Our institutional customers are a third or more allocated to privates. Wealthy individuals have similar long duration needs and yet they're probably 1% to 2% allocated. And so this year (2024), obviously, the tone has improved. 1st 9 months of the year, inflows into our individual products were up double year on year.”

“We will continue to be a massive player in the institutional area, but this area can grow a lot and we're operating off of what I think is a tiny base when you have $80bn plus in this area where people have more than $1trn of investable capital, early days in my mind.”

There are reports the industry is lobbying the Trump administration to allow 401k to be able to access Private assets. 401k are tax efficient vehicle which the great American Middle class utilises to save for retirement. The PE industry wants to manage middle class wealth and not just money from institutions and the truly wealthy. It is lobbying hard to access 401K money and the Trump administration is likely to be sympathetic.

Planned Fundraising

“We've launched or expect to launch fundraising in the next few quarters for the new vintages of multiple strategies.

These include the successors to our $5 billion Life Sciences Fund,

$9 billion private credit opportunistic strategy,

$22 billion private equity secondaries fund, and $6 billion private equity Asia fund.

All have strong track records, and we expect the new vintages to be at least as large as, and in most cases, hopefully larger than the current funds.”

A successful company has to show good investment performance and a track record of timely exits and timely returns of capital back to investors. Such a track record combined with new compelling ideas can be used to raise new funds.

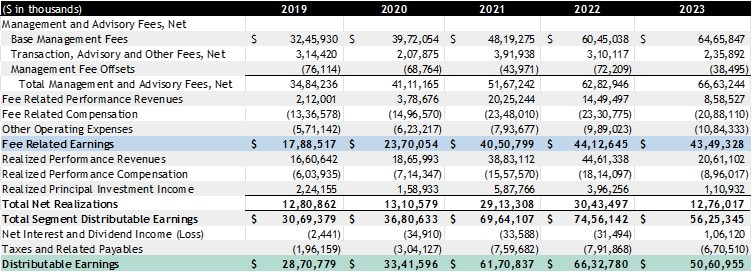

Some detailed data on BX’s business ($oos)

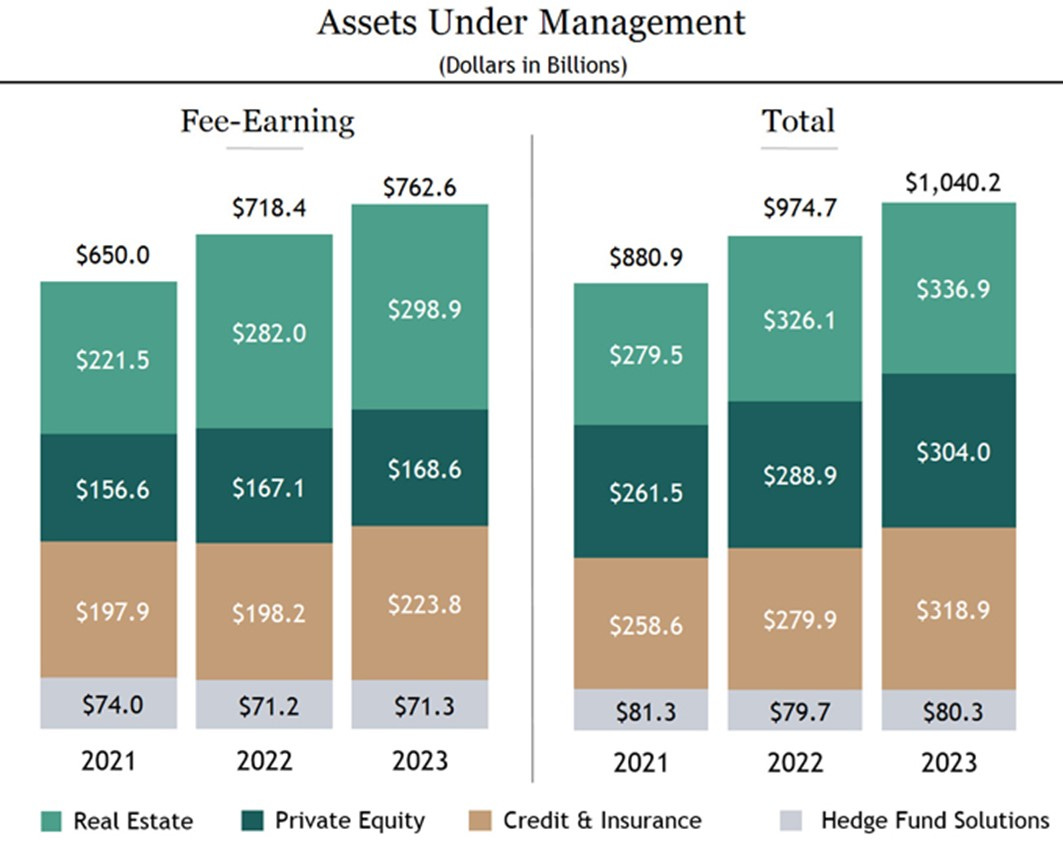

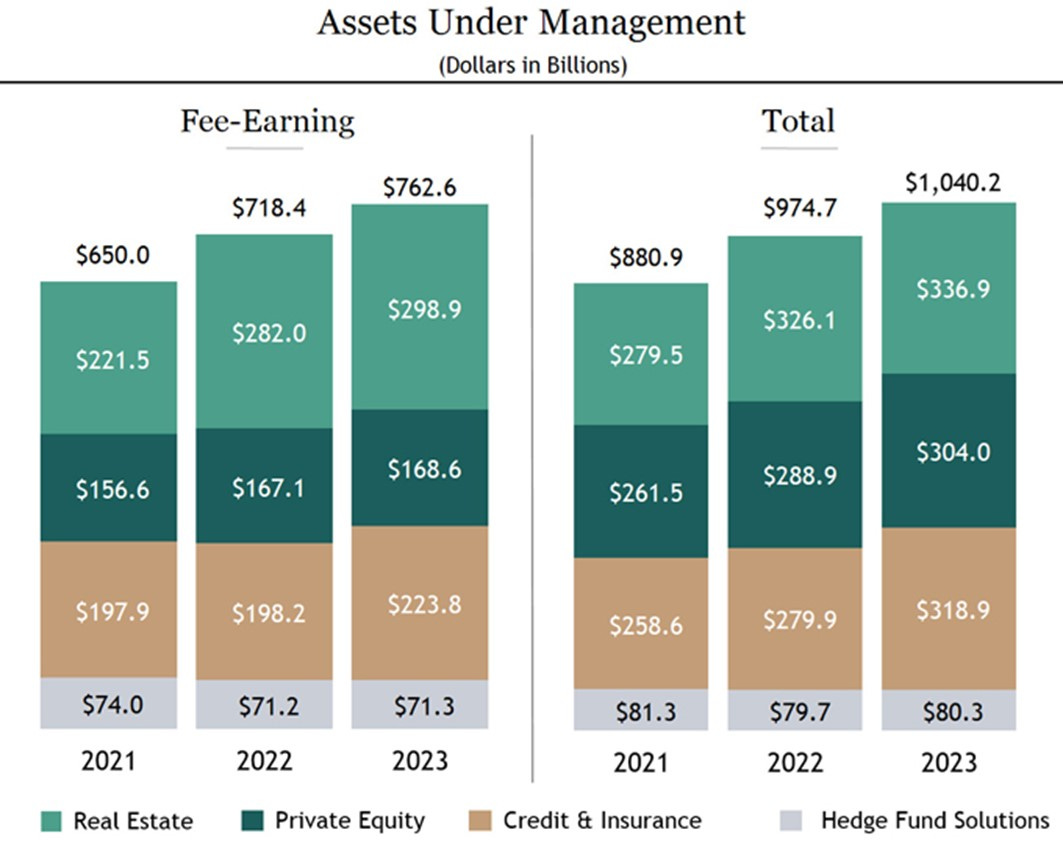

These numbers look strange as Excel (on my Indian laptop) places the comma according to Indian convention (at 100,000 (Lakhs) and 10mn (Crore) and not at 1mn). I have not been able to change it! No worries, we will have to work a bit harder to gain insights. The entry in the top left is 34,84,236 is $3,484,236,000 or $3.4bn. Total Management and Advisory Fees have grown from $3.4bn in 2019 to $ 6.6bn in 2023 (shown as 66,63,244). Total Assets have increased from $ 571bn at end 2019 to $1.04trn at end 2023. Of the latter, $762bn was fee earning at end 2023.

The split of the AUM is shown below:

As noted above, not all of this AUM is fee earning. The weighted average fee earning AUM increased from $375bn in 2019 to $735bn in 2019. In 2023, therefore about 72% of the AUM was fee earning.

We guess the balance 28% was made up of

AUM made up of capital from Blackstone Inc. or Blackstone Holdings on which no fee is payable.

Capital which the manager cannot, or does not yet want, to deploy and the fee is waived or no fee is due.

Total Management and advisory fees rose from $3.48bn in 2019 to $6.66bn in 2023. This fee number as a percentage of weighted-average fee earning AUM is 0.93%. This is consistent with the level of management fees for the various funds disclosed in the company’s filings.

The company also presents something called Distributable Earnings. The derivation of this is shown below

Distributable earnings are the sum of Fee Revenues and Realised performance revenues minus all operating earnings and tax.

Distributable Earnings is used to assess performance and amounts available for dividends to Blackstone stockholders, including Blackstone personnel and others who are limited partners of the Blackstone Holdings Partnerships.

Distributable Earnings have risen from $2.8bn in 2019 (shown as 28,70,779 in table above) to $5.06bn at end 2023.

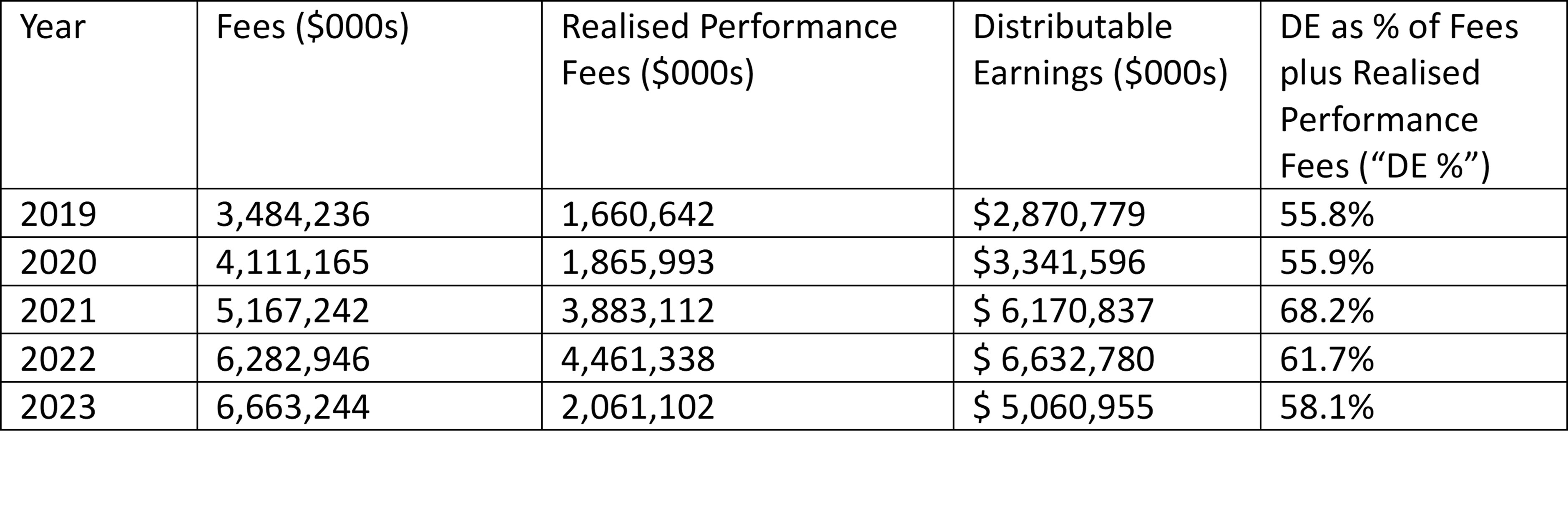

Distributable earnings are between 55% and 68% of Fees plus realised Performance Fees as Shown below:

As shown above, 2021 was a particularly good year of profitable realisations and the DE % was 68%. In more normal years, the DE % is closer to 56% to 58%. The balance 42% -44% is accounted for by operating expenses and taxes.

The company has a policy of distributing up to 85% of their distributable earnings.

“Our intention is to pay to holders of common stock a quarterly dividend representing approximately 85% of Blackstone Inc.’s share of Distributable Earnings, subject to adjustment by amounts determined by our board of directors to be necessary or appropriate to provide for the conduct of our business, to make appropriate investments in our business and funds, to comply with applicable law, any of our debt instruments or other agreements, or to provide for future cash requirements such as tax-related payments, clawback obligations and dividends to stockholders for any ensuing quarter. The dividend amount could also be adjusted upward in any one quarter.”

This distribution policy reflects the fact the company have low need for capital as it is a capital light business.

“Blackstone’s business model derives revenue primarily from third party Assets Under Management. Blackstone is not a capital or balance sheet intensive business and targets operating expense levels such that total management and advisory fees exceed total operating expenses each period. As a result, we require limited capital resources to support the working capital or operating needs of our businesses.”

“As a result, we require limited capital resources to support the working capital or operating needs of our businesses. We draw primarily on the long-term committed or invested capital of investors in our investment vehicles to fund the investment requirements of the Blackstone Funds and use our own realizations and cash flows to invest in growth initiatives, make commitments to our own funds, where our minimum general partner commitments are generally less than 5% of the limited partner commitments of a fund, and pay dividends to stockholders and distributions to holders of Holdings Units.”

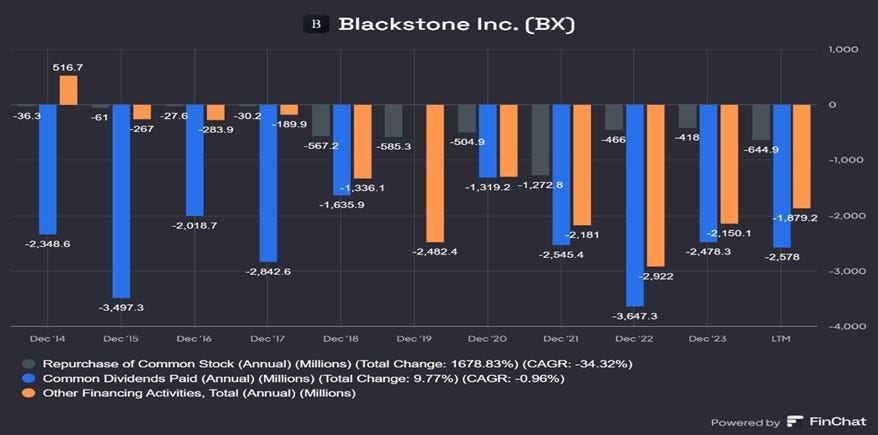

In FY 2023, outflows in the form of common dividends ($2.47bn), stock repurchases ($418mn) and other financing ($2.15bn) were a total of about $5bn which is exactly the Distributable earnings in FY 2023.

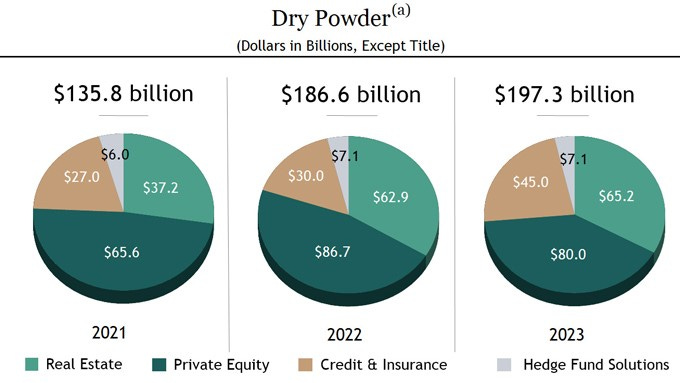

Dry Powder

Private Equity managers have more leeway as to the exact timing of their investments relative to long-only investors. They have more flexibility as to the timing and one measure of this Dry Powder.

“Dry Powder represents the amount of capital available for investment or reinvestment, including general partner and employee capital, and is an indicator of the capital we have available for future investments. It provides insight into the extent to which capital is available for Blackstone to deploy capital into investment opportunities as they arise.”

They had $197bn of Dry Powder at the end of 2023. As noted, some $92bn plus of it was deployed in 2024.

“While the fundraising environment has been challenging, we're seeing more receptivity from LPs today as markets improve. Importantly, when we meet with our clients around the world, what we consistently hear is that they are holding or increasing their allocations to alternatives and to Blackstone.”

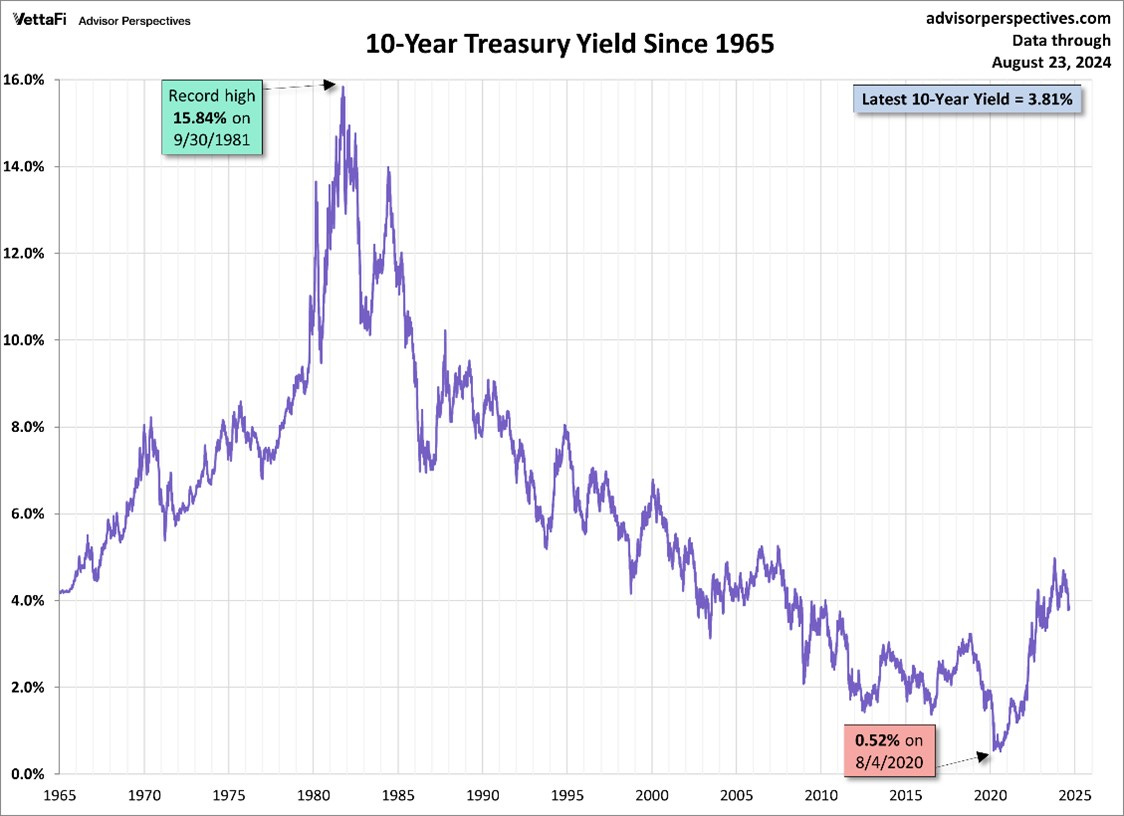

Long-term bond yields, the business cycle and Blackstone.

The chart above shows a 60-year history of the yield of the US 10-year Treasury Bond. It is a long period and covers a lot of economic cycles. Yields peaked in 1983-84 and were on a falling trend for 35 years. While Central Banks control short term rates, bond yields have more influenced by market and economic factors though they are broadly tethered by the level of short-term interest rates. Bond yields have a great influence on the cost of capital for corporates. Bond yields are important for the valuation of almost all risk assets including all corporate securities. Most assets are valued as the Present Value of future cash flows. And bond yields are big factor in the derivation of the discount rate. Broadly speaking, the lower the bond yields, the higher risk asset values are.

Blackstone was founded in 1985 and the chart above shows this was almost perfect timing as they enjoyed almost 35 years of falling bond yields and rising risk asset values process. This is a huge secular tailwind to their business.

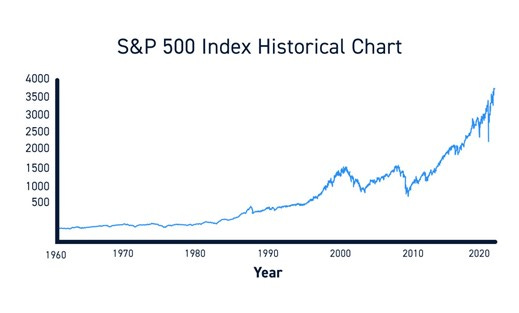

The US stock market has risen strongly since 1985. The rise in the stock indices led huge flows into stocks, the rise of the mutual fund industry and the rise of Initial Public Offerings (IPOs). Private Equity has been a big driver of Blackstone’s business especially in the first 6-7 years when it was their main business. Private Equity is greatly enabled by a booming IPO market as it facilitates profitable exits. The chart below shows high IPO activity in the period 1985 to 2000. It normalised after 2000 but by then Blackstone has built up a strong Real Estate business and went on to build a growing Private Credit business, especially after 2010.

In addition to these external secular trends, Blackstone made well-timed cyclical investment decisions which have also contributed to their success. We have noted two examples of this above.

1. In the early 1990s, they made their first investments in Real Estate after the Savings and Loan collapse led to a huge collapse in property prices. It eventually led to an orchestrated rescue by a government-owned company, the Resolution Trust Corporation (RTC).

2. In 2009, the global financial crisis was mainly driven by the collapse in securities backed by US mortgage-backed securities. In the aftermath, real estate process and in time Blackstone invested heavily in portfolios of single homes being sold by distressed lenders at highly discounted prices. In the process, Blackstone became the largest residential landlord in the United States and probably the world.

After the global financial crisis, the Federal Reserve and other Central Banks cut interest rates to near zero and held them for over a decade. This led to lower near zero bond yields (or negative bond yields in Western Europe). As a result, returns on many other assets fell as investors scrambled for yield. This led to huge growth in Private Credit which has greatly boosted the business of Blackstone and their rivals.

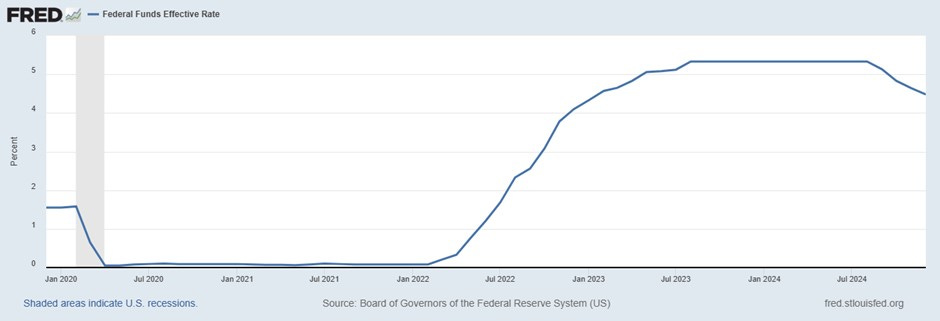

Bringing this story more up to date, bond yields started rising in 2020/21 as the chart above shows. Markets were responding to rising inflation which resulted for the supply side disruption after the Covid Pandemic. The US Federal Reserve responded by rating the Fed Funds Interest Rate as shown in the chart of the Effective Funds Rate below. In 2022, the Fed Funds Rate rose from about 0.25% to 5.25% in twelve months.

This led to much higher bond yields from 2021 to 2023. Blackstone officials have noted that this period was a difficult period for the business and it was period when they probably slowed the deployment of Funds. The Dry Powder increased by 50% from $137bn in 2021 to nearly $ 200bn at the end of 2023.

At the beginning of 2024, Blackstone took the view that bond yields had peaked and were likely to fall and invested heavily in anticipation. They deployed over $92bn in 2024.

That bet looks less sure today at the beginning of 2025. Bond yields have started rising since September on fear that the inflation is rising and the Fed may go slow on easing after two cuts in 2024. The ten-year treasury yield has risen 100bps from 3.7% level to about 4.7% and the market now fears a yield of 5%. If this happens, that will present a question mark against Blackstone’s investment strategy in 2024.

Summary

Since its founding in 1985, Blackstone has been a great success and has made a great deal of money for its employees. It has also made money for shareholders since its IPO 18 years ago. In the last seventeen years, BX has given has given a CAGR Price return of 11.75%. Over the same period, the CAGR total return was 15.63%. The difference is due to the dividends paid.

This compares with a CAGR return of 9.1% for the S&P 500 and a return of 15.7% for the Nasdaq 100 Index. BX has given a return similar to the Nasdaq 100 over the last 17 years.

They have successfully diversified their business from just Private Equity to add Real Estate, Credit including IG Credit, Infrastructure and Private Wealth. In the process their AUM has grown to over 1 trillion dollars.

Their timing was lucky.

They were founded in 1985, a year after what proved to be 25-year broad rally in bonds began. Rising bond prices and falling bond yields resulted in lower and lower cost of capital and this boosted the values of most risky assets and created a mood for risk taking.

In 1985, David Swendsen took over the management of the Yale Model. It’s success and widespread adoption by other university endowments and Pension Funds created a huge growth in demand for the kind of private asset management provided by Blackstone and its competitors.

It is not all luck since many other entities could have benefited form the above scenarios. BX has proved their ability to execute well. In addition, they have shown an ability to act as opportunistic value investors.

In the early 1990s in the aftermath of the S&L crisis real estate prices had collapsed. A government owned rescue company called the Resolution Trust corporation (RTC) was selling portfolios of real estate at “pennies to the dollar”. Blackstone recognised the opportunity and bet big on real estate. They did the same thing in 2011 in the aftermath of the great financial crisis when banks were selling single family homes at distressed prices.

They also took advantage of the decade long period of near zero interest rates and very low bond yields to build a world-leading private credit business.

They have built up business in investing in hedge funds, hedge fund managers, infrastructure and Private Wealth. They are no longer just a Private Equity but have diversified very well into many other segments.

They have also shown and ability to pick winners and use their intelligence to create very different but successful portfolios. For example, they pivoted their real estate portfolio so that 70% of it was accounted for by Logistics, Residential housing and datacentres. Thus, they avoided excessive exposure to area that suffered from chronic oversupply such as “Miami Condos” or areas facing demand shocks such as the Corporate Office sector after work form home became much more common

However, all that is in the past and is already in the price. What of the future?

They already have $1trn of assets and the iron law of large numbers suggest that growing significantly on such a large base will be difficult. The institutional client base has been saturated and there are business and regulatory challenges in tapping Private Wealth and the retirement savings of the middle class.

The macroeconomic scenario in the next four decades will be very different form the period 1985-2025. Paul Volcker at the Federal Reserve had hiked short term interest to as high as 19% in the early 1980s. This caused a steep recession but had the effect of breaking the entrenched inflationary cycle. The recession drove inflation to a low point during Volcker's terms of 2.5 percent in August 1983. The decline in inflation and the breaking of the inflationary expectations cycle allowed for decades of interest rate cuts and lower bond yields.

Today, interest rates are low and inflationary pressures are high and government deficits and debt are much higher. There is no chance or room for a sustained period of interest rate cuts. In fact interest rates are likely to head higher. There is no chance of decade long period of near zero interest rates that we saw in 2010-2021.

In 2022 the Federal Reserve ended this long period by raising the Fed Funds from about 0.25% to 5.25% in twelve months. Blackstone has noted that the 2022/23 period was tough. At the end of 2023, they took the view that the Fed was due to start an easing cycle and deployed huge amounts of capital in 2024 with a view that assets prices were set for a period of sustained appreciation.

“We've been so active deploying capital last 12 plus months is we wanted to invest before that all clear sign because eventually after 3 years of this cost to capital storm, we knew it would pull back at some point and that has happened and that's obviously beneficial, I think for both the economy and markets.”

At the beginning of 2025, this does not look like a good bet. It is likely the fed easing cycle had needed and the next move in interest rates is more likely to be up. There are structural factors pointing to higher inflation and interest rates in the short and medium term.

The world is uncertain and we have no expertise or track record in macroeconomic forecasting. However, we do not believe that macroeconomic conditions will be as favourable as they have been in the past and Blackstone’s investment performance will face short and medium-term headwinds

Valuation

Many years ago, the rule of thumb for valuation of institutional fund managers (who at the time were long-only fund managers) was 3% -4% of AUM. Those companies probably had fees equal to 0.75% to 1.0% of AUM and so the implicit valuation was 3 to 6 times revenues.

These days these companies are under pressure as they are finding it difficult to raise AUM and their fees are under pressure. The PE firm should trade as a high percentage of AUM compared with a conventional long-only Fund Management Company due to the possibility of earning Performance Fees.

At a $119bn market capitalisation, BX trades at about 12% of AUM. With a one-year forward P/E of 28X, a one-year forward Price to Free Cash Flow multiple of 29X and a dividend yield of 3%.

Blackstone is a formidable company with tremendous human capital and a proven ability to execute. They have created life changing wealth for their employees and given outside investors market matching returns in the last 15 years. However, they face significant challenges going forward and current valuations look elevated.

Conclusion

We will continue to study the sector and watch the company. We will not be committing capital to them.

Annexe 1

Blackstone and BlackRock

In 1987, BX formed a partnership with the founders of BlackRock to manage an investment fund focused on fixed-income investments. This partnership later led to the establishment of BlackRock as a separate entity. In 1992, Blackstone had a stake equating to about 36% of BlackRock. Stephen Schwarzman and Larry Fink were considering selling shares to the public. BlackRock was managing $17 billion in assets by the end of the year. At the end of 1994, BlackRock was managing $53 billion.

In 1994, Schwarzman and Fink had an internal dispute over methods of compensation and equity. Fink wanted to share equity with new hires, to lure talent from banks, unlike Schwarzman, who did not want to further lower Blackstone's stake. They agreed to part ways, and Schwarzman sold BlackRock, a decision he later called a "heroic mistake."

Annexe 2

BX Current Investment Themes

The main themes they are currently focused on are

the build-out of digital energy infrastructure needed to support AI,

the renewable energy transition,

the rise of private credit,

the development of the secondaries market or alternatives,

the extraordinary advances in drug development in the life sciences area,

the emergence of India as one of the most important major economies, and

the cyclical recovery in commercial real estate.