Broadcom (AVGO)

Large acquisitive technology conglomerate.

Broadcom Inc. (AVGO)

Introduction

Nvidia (NVDA) is making a lot of money selling GPUs, associated networking technologies and software to the fast-growing number of new GenAI-driven datacentres. Who else benefits from this megatrend?

AMD has been mentioned frequently in the press. They will definitely make progress as GPU demand grows and exceeds supply but their market share is currently very low.

The server manufacturers like Super Micro, Dell and Hewlett Packard Enterprises have all seen some momentum in their share prices. However, Dell has seen some reversal since the most recent earnings call. We hope to cover the server makers later in a separate note.

One company that has perhaps been less mentioned is Broadcom Inc (AVGO). It is the second largest AI chip company in the world in terms of revenue, behind NVIDIA, with many billions of dollars of AI accelerator sales. They also sell a wide range of networking products and services which will be in strong demand as AI datacentres proliferate.

Introduction to Broadcom

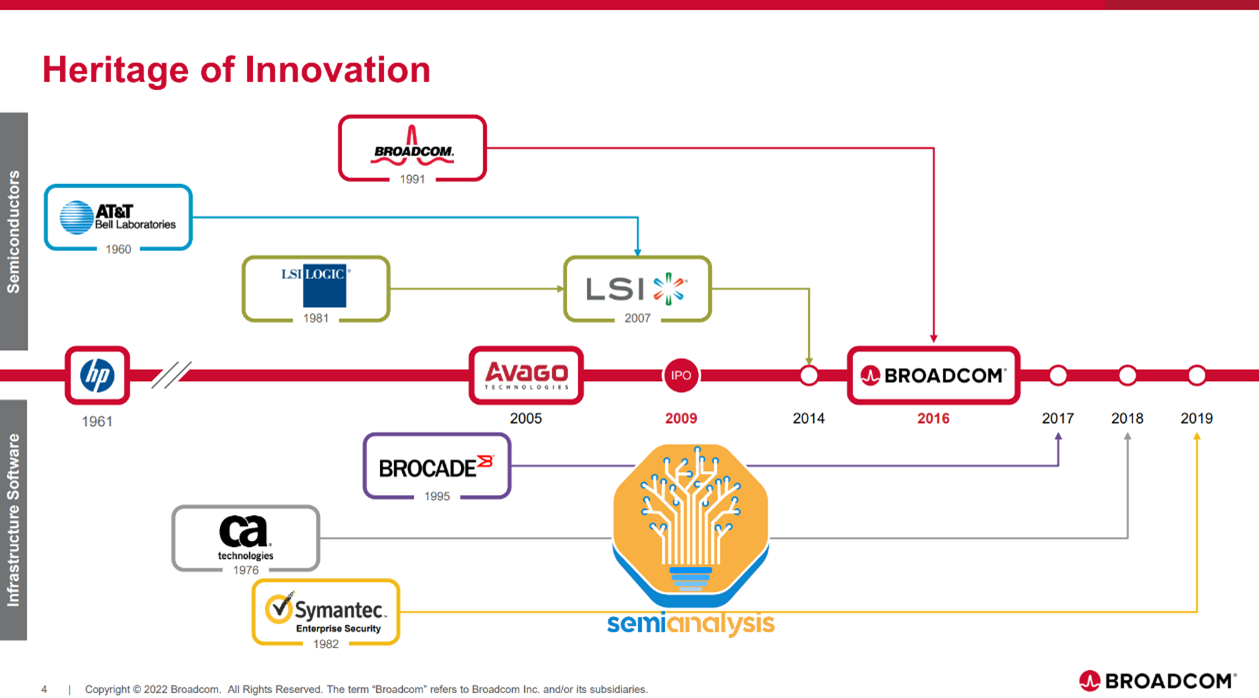

Broadcom is unusual in the big-tech space. Long-time CEO Hock E. Tan has built it up aggressively with many acquisitions such as Computer Associates, Symantec, LSI Logic, Emulex, Avago Technologies (a reverse takeover), Brocade Communications and, most recently, VMWare.

Broadcom is sometimes perceived as roll-up operator driven by cost cutting and financial engineering like a private equity operator. The net result of all this acquisition activity is a large diversified company with a market cap of ~$800bn and ~23 divisions. It is difficult for securities analysts to research the company. The company describes itself thus:

“We offer thousands of products that are used in other end-products such as enterprise and datacentre networking, home connectivity, set-top boxes, broadband access, telecommunication equipment, smartphones and base stations, datacentre servers and storage systems, factory automation, power generation and alternative energy systems, and electronic displays.”

“We differentiate ourselves through our high-performance design and integration capabilities and focus on developing products for target markets where we believe we can earn attractive margins.”

“Many of the largest companies in the world, including most of the Fortune 500 and many government agencies, rely on our enterprise and mainframe software to help manage and secure their on-premise and hybrid cloud environments.”

Broadcom is an amalgamation of a portfolio of 16(!) semiconductor franchises and two main software franchises that have come together to form the company that exists today.

The story starts with HP’s semiconductor division. Inside HP was its test and instrumentation segment, which itself contained an internal chip division, focused on RF components such as filters as well as passive components such as resistors and capacitors. The key product class was RF filters, devices that allows antennae to tune into a specific frequency band while filtering out the unwanted radio signals on other bands.

In 1999, HP decided to spin out businesses that were not considered core. Agilent was spun out in 1999 and it contained HP’s test and measurement business. The semiconductor division within Agilent was further spun out in 2005 to a KKR and Silver Lake-led private equity consortium. In 2005, the company was rebranded as Avago.

Hock E Tan. President and CEO, Broadcom

Hock Tan became Avago's CEO in 2006. In 2008 when he purchased Infineon’s Bulk Acoustic Wave (BAW) business for $30M. This brought the Film Bulk Acoustic Resonator (FBAR) Filter product into the fold – a deal that arguably ranks as one of the most profitable M&A transactions of all time.

The explosion of mobile data consumption after the introduction of the Apple I-Phone required a greater number of frequencies and much wider frequency bands. The list of bands supported by the iPhone 14 Pro would fill up a third of a page. In the 1990s and early 2000s before the smartphone era, three of four frequencies were sufficient.

The FBAR filter became an indispensable part of modern smartphones, earning an estimated $3bn to $4bn per annum for over two decades . This was from a company acquired for $ 30mn.

Hock E Tan has used Avago cash flow to acquire companies and become an aggressive consolidator in the semiconductor and networking industry. Since taking charge of Broadcom in 2015, he has acquired several companies, cut costs, gained pricing power, and ensured Broadcom has a commanding presence in the global chip market.

The original Broadcom had been founded in 1991 but Hock merged it with Avago Technologies in 2016 and renamed the combined entity Broadcom.

After 2016, they started acquiring Software companies starting with Brocade in 2016 and ending with VMWare last year.

In 2017, Tan tried to buy Qualcomm with a price tag of $ 117bn (!) which would have made it the largest ever takeover. US President Donald Trump ordered Broadcom to back away from the deal, citing national security concerns.

In 2023, Broadcom acquired VMware in a cash-and-stock deal worth $61B. It is the third-largest tech acquisition in history behind MSFT’s acquisition of Activision Blizzard and Dell's $67B deal with EMC in 2016.

VMware is credited for pioneering the virtualization software that lets a single computer operate like many small ones. Large corporations use VMware's services to manage public and private cloud networks and datacentres.

In 2016, VMWare partnered with Amazon for its cloud computing business. It has similar partnerships with Microsoft as well as Google's Alphabet. In 2016, the company was spun-off from Dell for the latter to repay its debt.

Broadcom closed its VMware acquisition last year, so VMware's financials are consolidated with the conglomerate from fiscal 2024 (which began in November 2023).

Broadcom have not acquired a semiconductor company since 2016 so all the semiconductor growth has been organic driven by #$ 15bn worth of investments.

The Broadcom acquisition strategy

The strategy is simple – Broadcom acquires companies that sell market leading products with sticky customers, recurring revenue, and high margins but have excessive operating expenses and are generating below potential profit and cash flow.

Broadcom cuts costs deeply, removing layers of middle management, cutting sales and marketing functions down to those needed to directly support individual products, and almost eliminates general and administrative costs in favour of utilizing Broadcom’s existing corporate platform resources.

R&D is a different story. Broadcom does eliminate science projects with unclear near-term return on investment as well as common research and development functions not directly driving revenues, but it leaves product teams intact. As we will see below, R&D is a major expense for the company and tends to grow with sales and therefore with scale.

Product teams can now obtain approvals for plans directly from senior management and can execute them with greater speed.. By loading overhead costs onto the product groups’ P&L and holding managers accountable for the group’s results, Broadcom has further driven a culture of efficiency. In many cases, this has led to post acquisition market share gains.

This practice is well suited to semiconductor products, where the customer set is well defined, and where revenue growth is mainly driven by content growth and spec upgrades rather than rapid growth in the customer base.

In the wireless chips business for example, where most of Broadcom’s sales are to Apple, there is little need for a traditional sales organization, with orders for parts and volume taken by staffers and pricing negotiated at the upper management level.

The result is a very lean organization with much higher margins and cash flow generation that is focused on core products and franchises and carrying out the R+D necessary to drive future cash generation, and advances in those products and fields. M+A brings in new products and pivots the company in new directions.

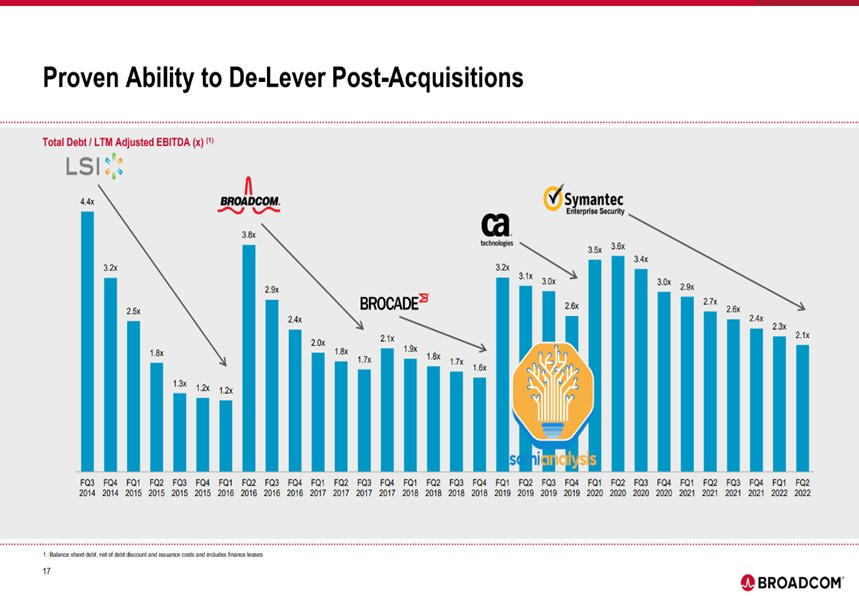

Broadcom does load up debt when they acquire companies but they have demonstrated a track record of growing free cash flow. The free cash flow is used to deleverage quickly post-acquisition while continuing to pay dividends and do share buybacks.

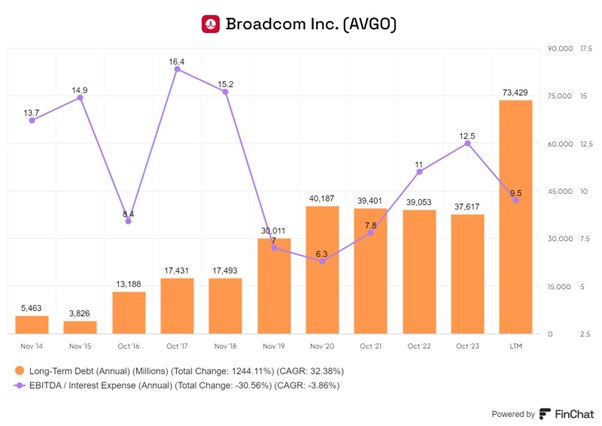

The Chart above shows Broadcom’s Total Debt/ Ebitda profile and indicates post- acquisition peaks followed by steady de-leveraging.

Company Description

Broadcom is a global technology leader that designs, develops and supplies a broad range of semiconductor and infrastructure software solutions.

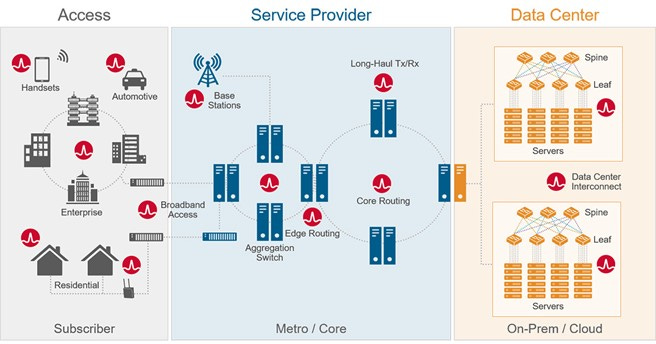

Broadcom products can be found in many parts of various types of common networks as shown with their red circle symbol in the chart above.

In semiconductors, they develop semiconductor devices with a focus on complex digital and mixed signal complementary metal oxide semiconductor (CMOS) based devices and analogue III-V based products.

One of the key products seeing huge demand in the GenAI boom are GPU Accelerators. The generally accepted definition of an accelerator is “A purpose-built design that accompanies a processor for accelerating a specific function or workload (also sometimes called “co-processors”) ”. Since General Processors (GPUs) are designed to handle a wide range of workloads, processor architectures are rarely the most optimal for specific functions or workloads.”

A GPU accelerator is “hardware that is optimized for doing the computations for three-dimensional computer graphics. ”

Broadcom does not compete with Nvidia as it does not design and supply GPUs. Instead, it supplies GPU accelerators which help GPUs work better for specialised tasks.

Broadcom’s business in networking and connectivity, does compete with Nvidia’s switches and its SpectrumX networking product.

Broadcom’s rising accelerator sales are to some significant degree currently driven by Google’s aggressive ramp up of its custom developed Tensor Processing Units (TPU)

Google’s website describes TPU as follows:

“TPUs are Google's custom-developed application-specific integrated circuits (ASICs) used to accelerate machine learning workloads. Cloud TPU is a web service that makes TPUs available as scalable computing resources on Google Cloud.”

“TPUs train your models more efficiently using hardware designed for performing large matrix operations often found in machine learning algorithms. TPUs have on-chip high-bandwidth memory (HBM) letting you use larger models and batch sizes. TPUs can be connected in groups called Pods that scale up your workloads with little to no code changes.”

Google has been investing heavily for the last five years in the Google Cloud Platform (GCP). The pace has increased significantly after the recent Microsoft + OpenAI alliance that is challenging Google’s world leadership in AI.

A large part of the new workloads that will move to the Cloud in the next few years will be GenAI driven. The large Cloud Service Providers (CSPs) plus Meta Platforms are investing heavily in datacentres. Those datacentres need GPUs (Nvidia, AMD, Intel) and Accelerators (Broadcom, Marvell) as well networking (Nvidia, Arista, Cisco) and Software (Nvidia, AMD, Intel).

Their Infrastructure Software (IS) solutions enable customers to plan, develop, automate, manage and secure applications across mainframe, distributed, mobile and cloud computing platforms.

Their portfolio of infrastructure and security software is designed to modernize, optimize, and secure the most complex hybrid environments, enabling scalability, agility, automation, insights, resiliency and security.

They also offer mission critical fibre channel storage area networking (“FC SAN”) products and related software .

Broadcom maintain design, product and software development engineering resources at locations in the U.S., Asia, Europe and Israel. This provides them with engineering expertise worldwide.

They have an extensive portfolio of U.S. and other patents, and other intellectual property (“IP”) to integrate multiple technologies and create system-on-chip (“SoC”) component and software solutions that target growth opportunities. The company claims to have over 23,000 registered patents.

Their products and software deliver high-performance and provide mission-critical functionality. Many customer relationships have been in place for many years and are often the result of years of collaborative product development. This has enabled AVGO to build our extensive IP portfolio and develop critical expertise regarding our customers’ requirements, including substantial system-level knowledge.

The two reporting segments are as follows:

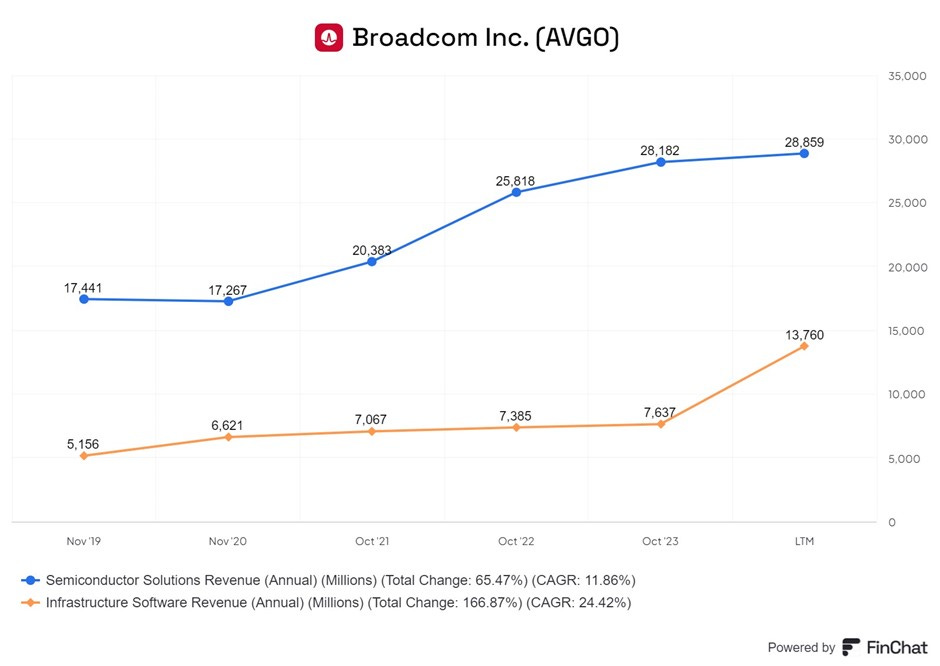

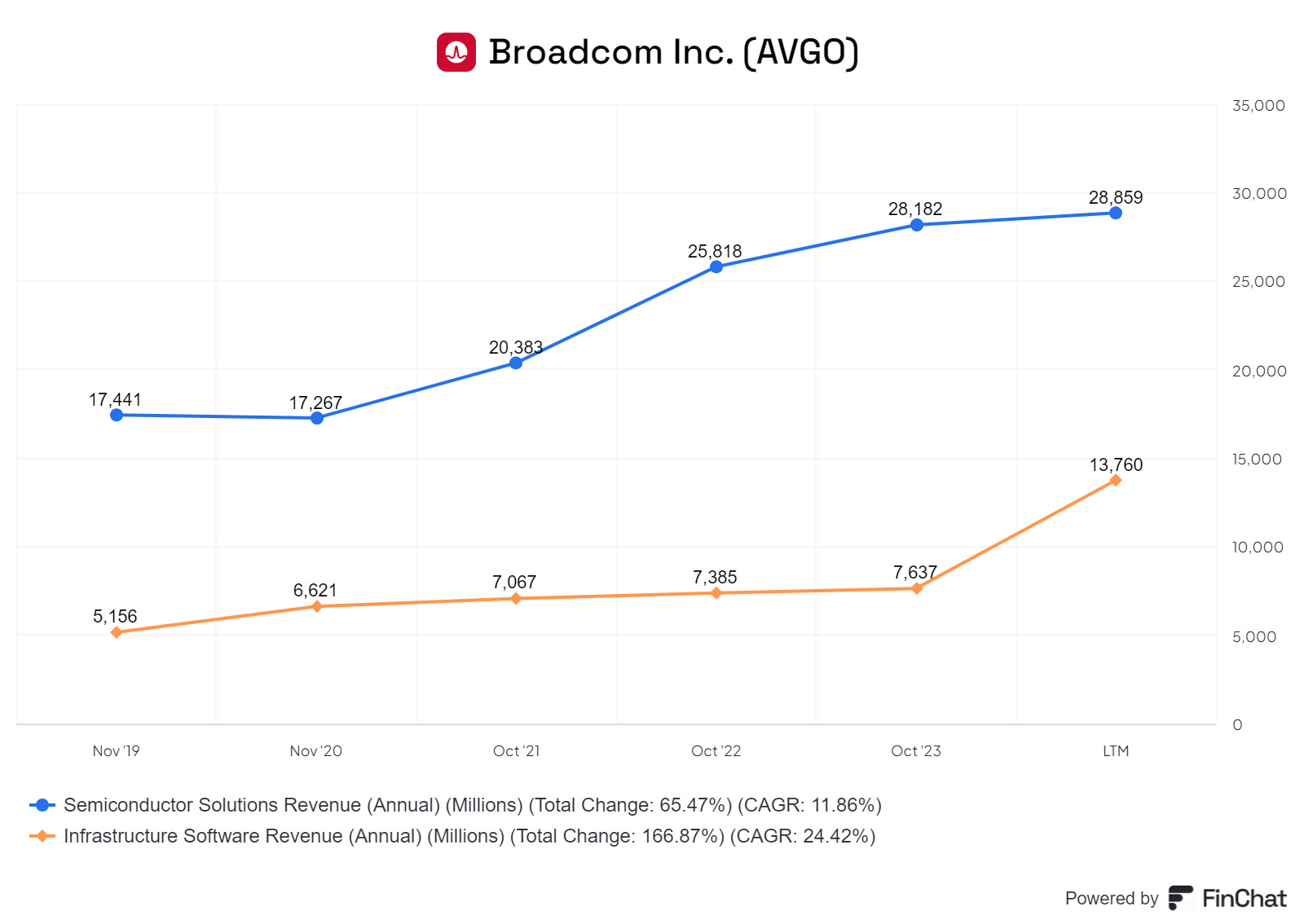

Semiconductor Solutions (SS) ~76% of revenues and Infrastructure Software (IS) ~ 23

% of revenues as shown in the chart below.

Semiconductor Solutions (SS)

Broadcom provides semiconductor solutions for managing the movement of data in datacentre, telecom, enterprise, and embedded networking applications. Its mainframe software solutions include solutions for the IBM Z mainframe platform, which runs business applications.

They have a history of innovation in the semiconductors and offer 1000s of products used in end-products such as enterprise and datacentre, networking, home connectivity, set-top boxes, broadband access, telecommunication equipment, smartphones and base stations, datacentre servers and storage systems, factory automation, power generation and alternative energy systems, and electronic displays.

We can look at a breakdown of businesses within in Semiconductor Solutions.

Networking - Offers high performance connectivity to Enterprises, Service Providers Such as Telcos and Hyperscale Datacentres such as those being set by large CSPs such as Amazon, Microsoft Google and Oracle etc. The latter is currently a source of very fast-growing demand. AVGO provides Switching, Routing, optical Interconnect and Ethernet network interface cards (NIC). For a discussion on these please see our note on Arista Networks (ANET) which can be found here.

Broadcom Brocade Router

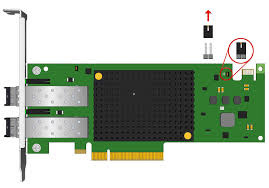

Server/Storage Connectivity products which are supplied to both Cloud and On-Premises infrastructure. Broadcom supplies Network storage products such Fibre channel Host bus Adapters (see below) and Raid (redundant array of independent disks) adaptors.

Photograph above shows Emulex Broadcom Fibre channel Host bus Adapter

Broadband: End to end Solutions These products are bought by Service Providers such as Telcos or go into customer’s premises or into connected devices such as Modems, Wi-Fi Routers, Gateways and Cable Modem Systems.

Wireless: Chips and other components which are required for connected devices such as Phones. Tablets, Laptops, Smartwatches. Customers are companies such as Google, Apple or the contract manufacturers who make their devices.

Industrial: Networking products, sensors etc needed for factory automation, renewable energy products such as batteries and chargers and in smart vehicles.

You can find more information on the company presentation at the link here.

https://investors.broadcom.com/static-files/602c2fd3-89a0-436f-b638-4890f20feda7

Distributors and original equipment manufacturers (“OEMs”), or their contract manufacturers, typically account for most semiconductor sales.

Many of the customers and their contract manufacturers require time critical delivery of our products to multiple locations around the world. Broadcom have 35% of their employees in Asia including sales offices in various countries, a primary warehouse in Malaysia, and dedicated regional customer support call centres. This network means they are well-positioned to support customers throughout the design, technology transfer and manufacturing stages across all geographies.

Given the size of the SS business, there is little doubt that Broadcom is a top 3 fabless semiconductor company behind Nvidia and AMD. However, there a lot more to Broadcom than semiconductors.

Infrastructure Software (IS)

Its infrastructure software segment includes its mainframe and enterprise software solutions and fibre channel storage area networking (SAN) business.

IS solutions enable customers to plan, develop, automate, manage and secure applications across mainframe, distributed, mobile and cloud platforms. The IS portfolio is designed to modernize, optimize, and secure the most complex hybrid environments, enabling scalability, agility, automation, insights, resiliency and security.

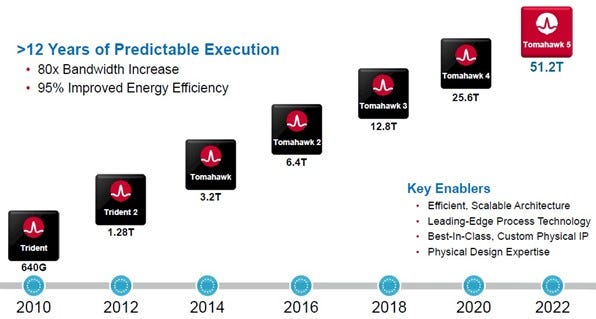

One product example is datacentre switches which determine how fast data travels from one point to another. Their Tomahawk 5 is the latest iteration (see below) of an industry-leading product that is accelerating AI workloads. Networking and equipping the infrastructure of the new AI Datacentres is a major source of demand currently.

A decade of development led to the current Tomahawk 5 datacentre switch.

IS customers are large enterprises that have computing environments from multiple vendors. Broadcom believe their enterprise-wide license model will continue to offer customers reduced complexity, more flexibility and an easier renewal process that will help drive revenue growth.

Customer concentration is quite high.

Aggregate sales to the top five end-customers account for 35% of revenues. Apple Inc. accounted for approximately 20% of Broadcom’s net revenue in FY 2023.

Broadcom outsource the manufacturing of their products to contract manufacturers and companies such as TSMC. They are a top five customer of the latter.

Exposure to Apple

Broadcom has a long and complicated relationship with Apple. It is not a typical Apple low-end, economically powerless, supplier as it provides critical and technologically complex components. CEO Hock Tan is said to personally negotiate supply and pricing agreements with Apple.

Broadcom has benefited from the growth in Apple iPhones as it makes a combined component that handles both Wi-Fi and Bluetooth functions on Apple devices. It also supplies radio-frequency (RF) chips and chips that handle wireless charging.

Apple has a longer term strategy of replacing chips from 3rd parties to its in-house designs. It has replaced Intel as a supplier of chips in laptops and desktop computers with its in-house designed M1 and M2 Chips.

We noted this in our May 17 2023 report on Apple which can be read here. An extract is given below:

“In June 2020, Apple announced it would move away from Intel processors, and Apple would start using their in-house designed processor. In December 2020, MacBook Air, MacBook Pro, and the Mac Mini became the first Mac devices powered by an Apple-designed processor, called the Apple M1. Currently, they use Apple’s M2 Pro and M2 Max. This is the latest stage of Apple’s quest to own and develop everything that goes into its products from the bottom up. It’s also reportedly working on its own modem, a chip that combines Wi-Fi and Bluetooth modem capabilities, and its own display technology.

Developing their own chip has reduced Apple’s reliance on companies like Intel, Qualcomm, Broadcom, and Samsung. It also inspired other companies like Tesla, Amazon, and Meta Platforms to design their own chips in-house.”

Apple has reportedly been working on a product that combines cellular modem, Wi-Fi and Bluetooth capabilities into a single component. This would be a threat to Qualcomm and Broadcom.

However, Apple appears to be making slow progress in developing the components it needs to reduce its dependence on Broadcom and Qualcomm, though it has made some progress in this direction.

There is little doubt that Apple’s relationship with Broadcom is not an easy one. Hock Tan has a reputation for tough negotiations and forced some customers to commit to noncancelable orders during the pandemic-fuelled supply crunch. These issues are ongoing but the high exposure to Apple remains a notable risk for Broadcom.

Google demand

Google has been ramping up chip investments this year as it plays catch-up with Microsoft (MSFT) for the domination of the market for generative AI applications such as ChatGPT.

Google has reportedly had a standoff with Broadcom over the price of the TPU chips. It is reported that Google has also been working to replace Broadcom with Marvell Technology (MRVL) as the supplier of chips that link their Datacentre servers together.

Despite all these concerns, Broadcom looks like it is the second-biggest winner from the generative AI boom after Nvidia.

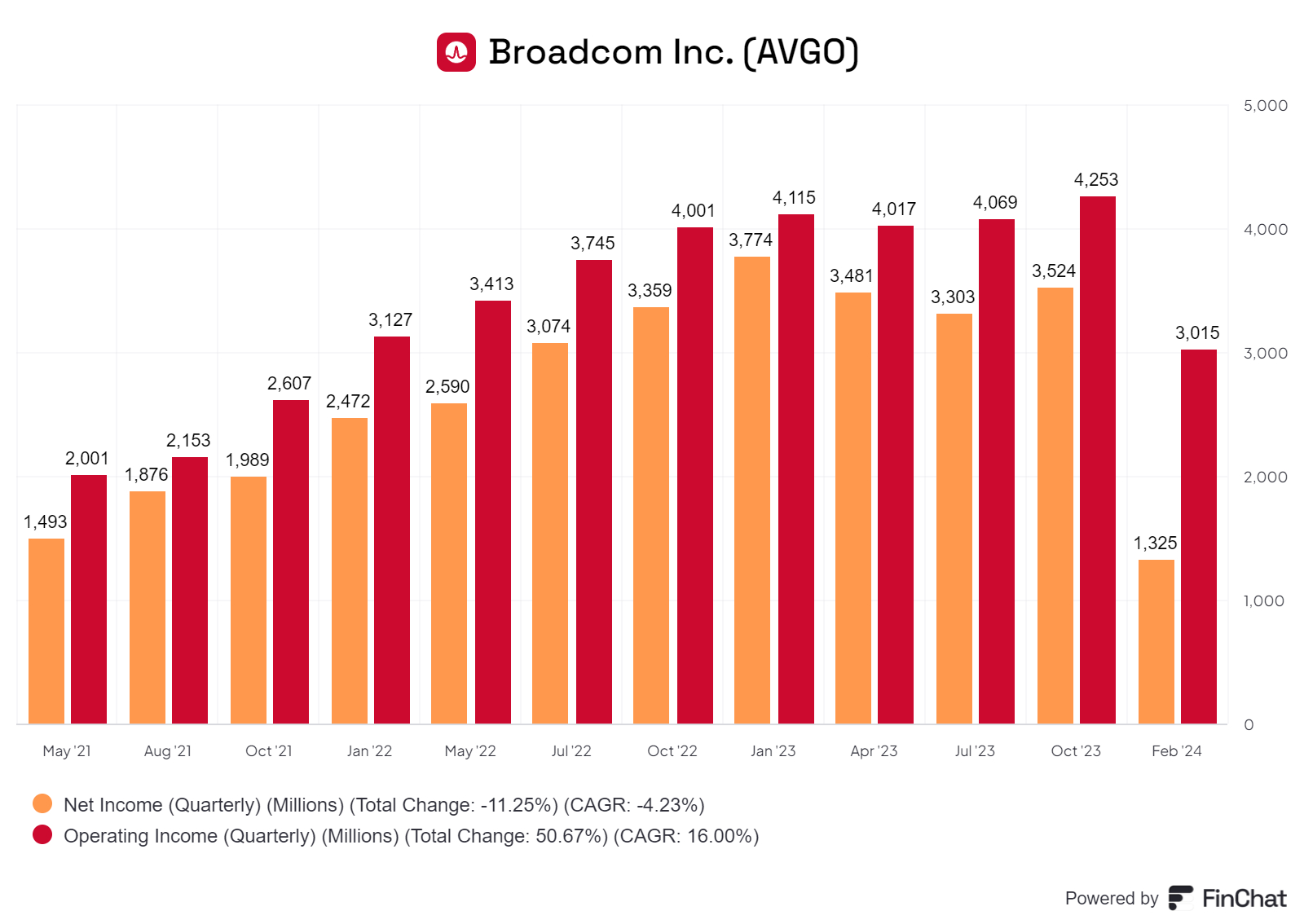

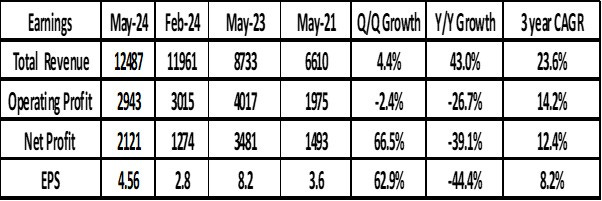

Financial Snapshot

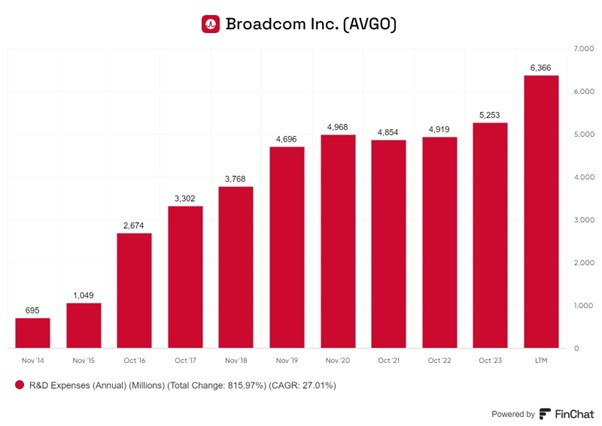

As you can see R&D is a key expense for the company and has reached a run rate of over $ 6.3bn per annum. It is a significant expense which moves in line with the revenues of the company.

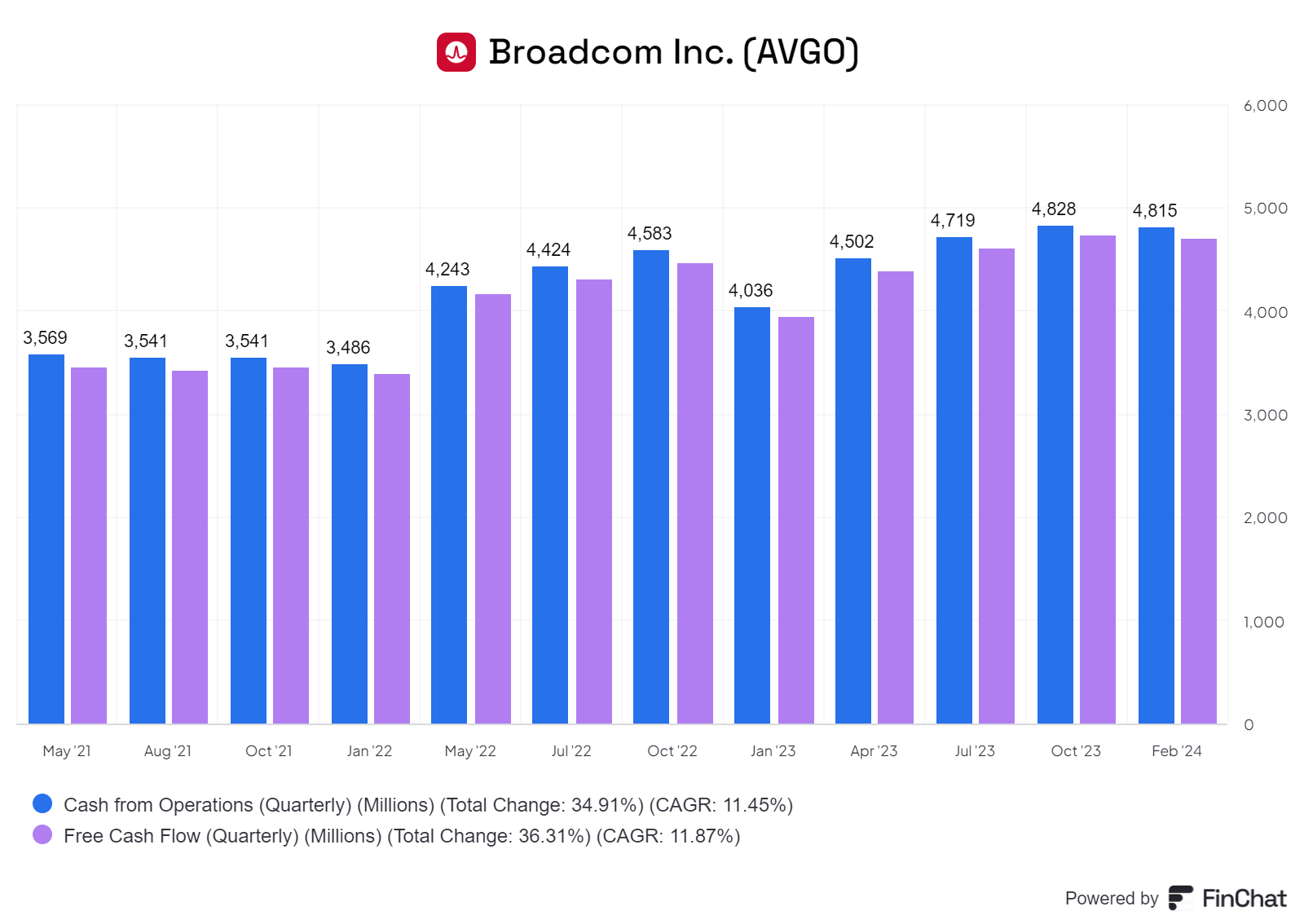

The difference between Operating Cash Flow and Free Cash Flow (see chart above) is quite small and suggests that capex for Broadcom is quite low. This, in large part, reflects the fact the most manufacturing is outsourced.

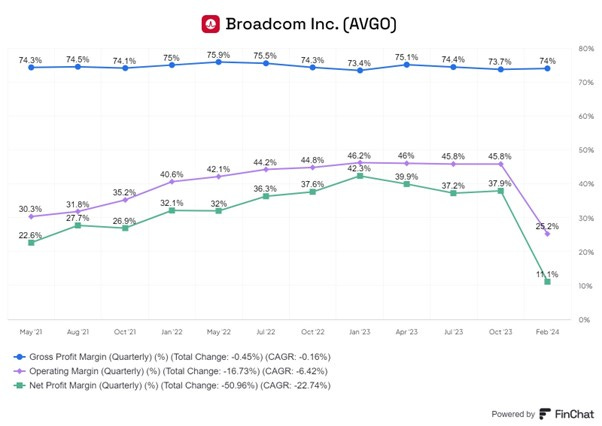

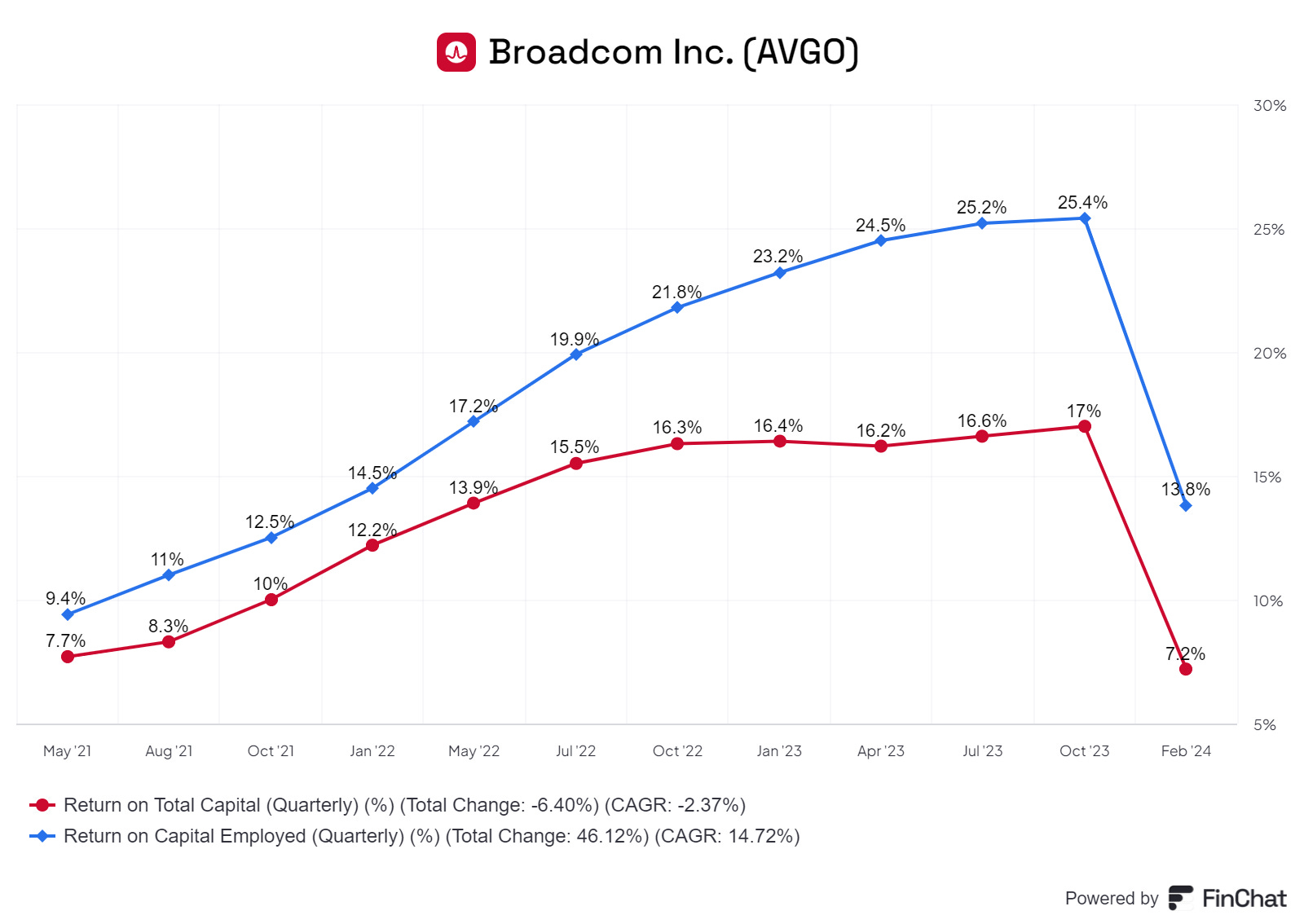

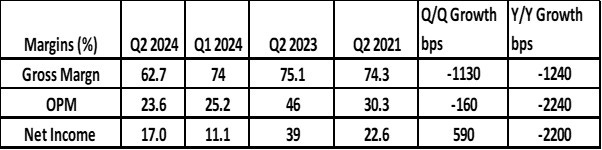

The various margin and return metrics (see charts above) have fallen in the last quarter due to the integration of the VMWare acquisition. It reflects restructuring expenses and the fact that the completion of the takeover triggered certain stock-based compensation. Management have stated the VMWare integration has gone well and they are confident about raising VMWare margins up to the Broadcom average by 2025.

The long-term debt has almost doubled because of the new debt issued to fund the VMWare acquisition. The debt interest cover measured as EBITDA/Interest Cover (Purple line above) has also fallen a little. As discussed above, Broadcom has a track record of reducing debt two or three years after a take-over.

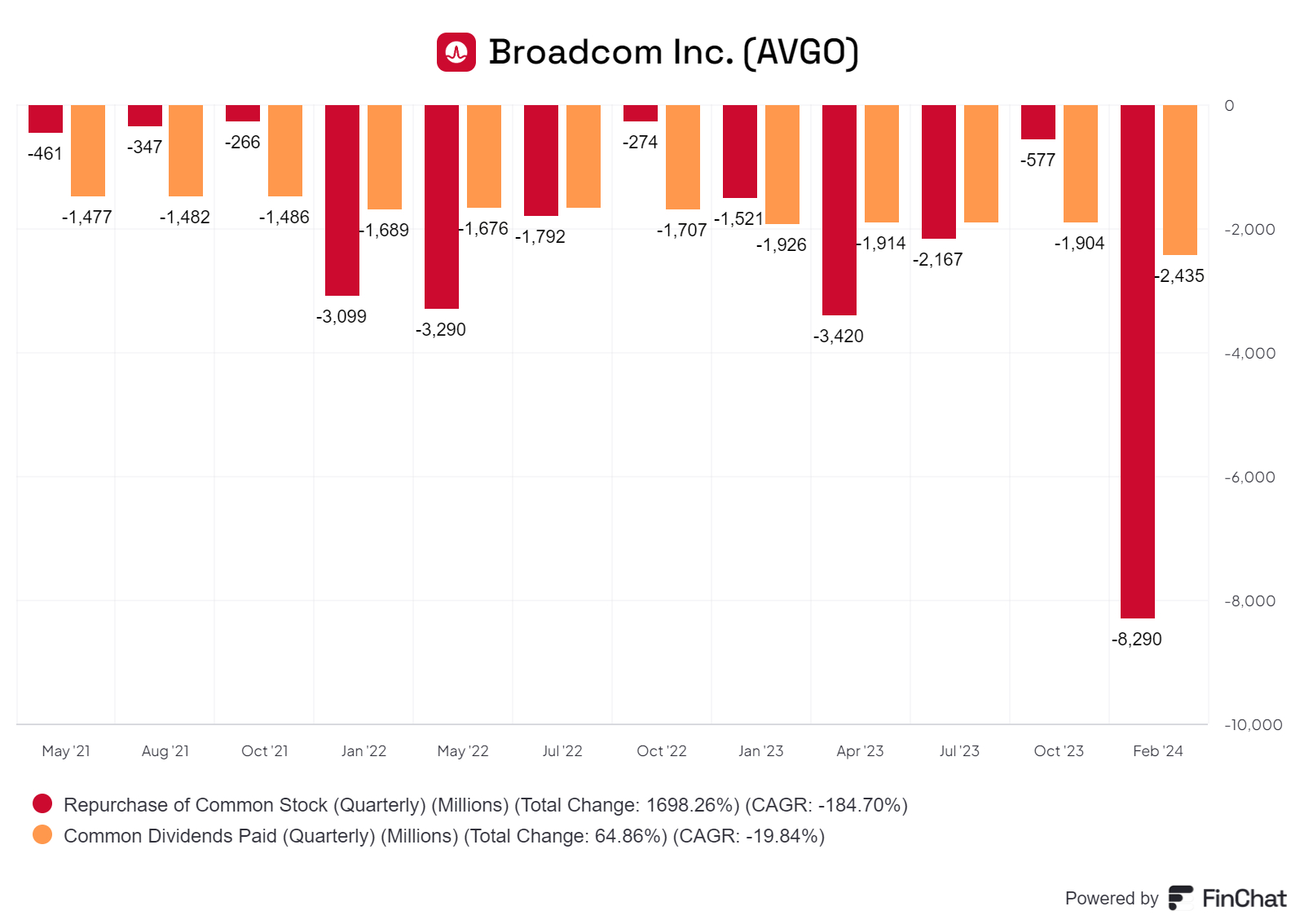

The chart above shows some of the uses of cash made by Broadcom. The company pays a steadily increasing dividend. It also regularly repurchases stock though the size of the buyback varies greatly. Stock buybacks may be subdued for the next few years as the company uses available cash to reduce leverage. The data is shown as a negative as they involve cash outflows.

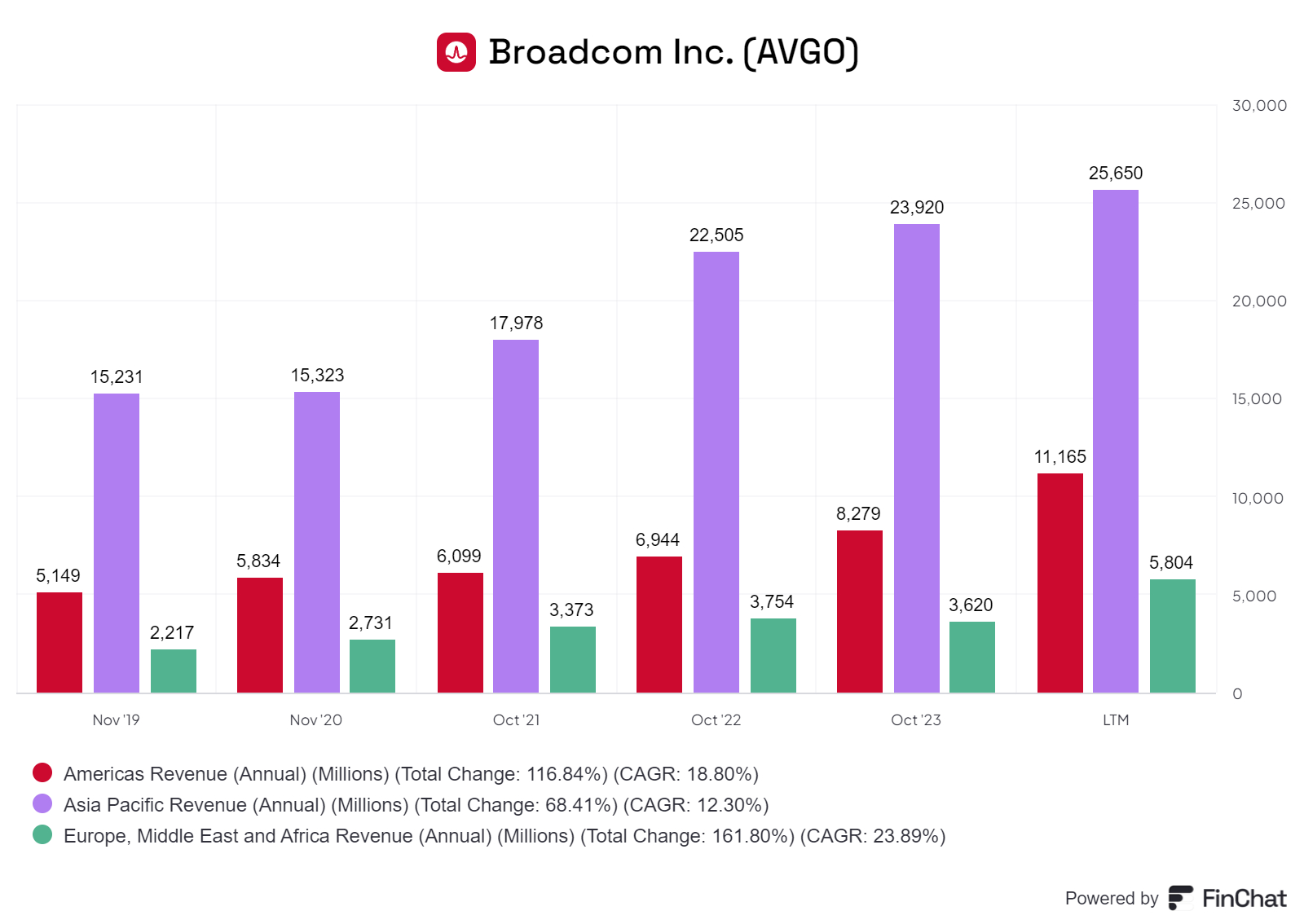

The chart above shows the geographical breakdown of demand. Asia Pacific (APAC) dominates as many of the contract manufacturers and original equipment manufacturers are based there.

The chart above shows revenues are dominated by product revenues. However, subscription revenues has picked up in the last quarter after the inclusion of VMWare revenues.

Quarterly Results

Broadcom posted Q2 earnings last Wednesday that beat analysts’ estimates.

The stock rose about 10% in extended trading after the results were released.

Earnings per share: $10.96 adjusted vs. $10.84 expected by analysts

Revenue: $12.49 billion vs. $12.03 billion expected by analysts

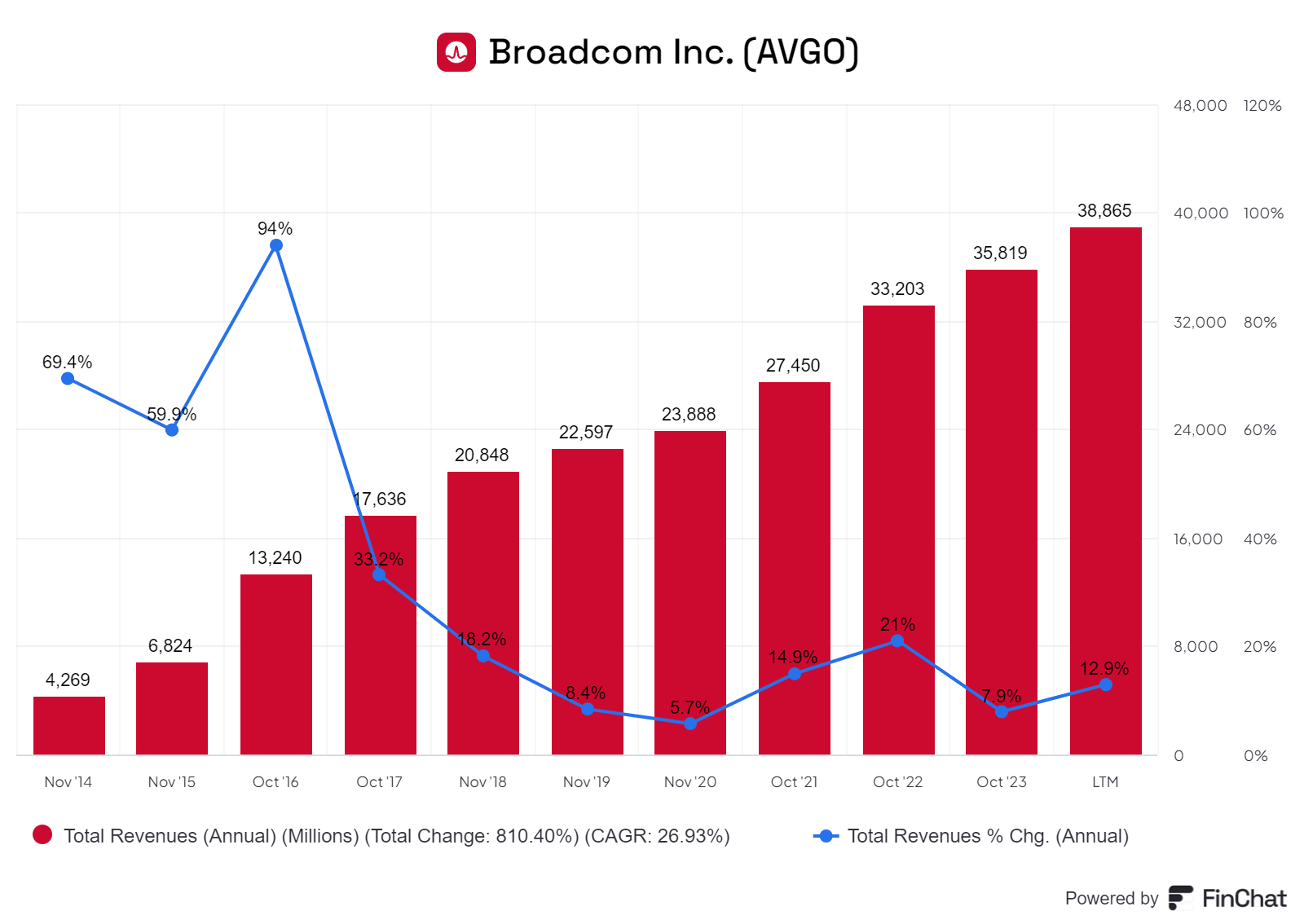

Q2 revenue was $12.5bn, up 43% YoY as revenues included a full quarter of contribution from recently-acquired VMware. If VMware is excluded, revenue was up 12% YoY.

This12% growth was largely driven by AI revenue, which rose 280% (YoY) to $3.1bn (or 24% of total sales)

Infrastructure software (IS) revenue of $5.3bn was up 175% (YoY). This was greatly boosted by a $2.7bn revenue contribution from VMware.

Broadcom reported $2.1bn in net profit. Net profit fell 39% (YoY) due to restructuring costs.

The inclusion of VMWare increased total revenues but reduced profits (due to restructuring costs and stock-based compensation triggered by the takeover) and thus lowered margins and profitability.

Highlights of earnings conference call

We listened to the management earnings call after the results. The highlights are given below:

Integration of VMWare

“The integration of VMware is going very well. We have modernized the product SKUs from over 8,000 disparate SKUs to four core product offerings and simplified the go-to-market flow, eliminating a huge amount of channel conflicts.”

“We are making good progress in transitioning all VMware products to a subscription licensing model”

“VMware revenue in Q1 was $2.1bn, grew to $2.7bn in Q2, and will accelerate towards a $4bn per quarter run rate. We therefore expect operating margins for VMware to begin to converge up towards that of classic Broadcom software by fiscal 2025.”

They have been pleasantly surprised by the scale of VMWare’s reach.

“VMware taught me a few things. They have 300,000 customers, 300,000. That's pretty amazing. And we look at it. And I start to learn the value of a very strong bunch of partners they have, which are a network of distributors and something like 15,000 VARs, value-added resales supported with these distributors. So we have doubled down and invested in this resale network in a big way for VMware.”

Semiconductor Services

The big story is AI demand is driving revenues.

“Networking Revenue of $3.8bn grew 44% year-on-year, representing 53% of semiconductor revenue. This was driven by strong demand from hyperscalers for both AI networking and custom accelerators.”

“As AI datacentre clusters continue to deploy, our revenue mix has been shifting towards an increasing proportion of networking. We doubled the number of switches we sold year-on-year, particularly the PAM-5 and Jericho3, which we deployed successfully in close collaboration with partners like Arista Networks, Dell, Juniper, and Supermicro.”

“We're leading the rapid transition of optical interconnects in AI datacentres to 800 gigabit bandwidth, which is driving accelerated growth for our DSPs, optical lasers, and PIN diodes.”

“Next year, we expect all mega-scale GPU deployments to be on Ethernet. We expect the strength in AI to continue, and we now expect networking revenue to grow 40% year-on-year compared to our prior guidance of over 35% growth.”

In contrast to networking and GPU accelerators, the Wireless, Broadband and Industrial segments were all subdued.

“Q2 wireless revenue of $1.6bn grew 2% (YoY), was seasonally down 19% (QoQ). And in fiscal '24, we reiterate our previous guidance for wireless revenue to be essentially flat year-on-year.”

“Q2 server storage connectivity revenue was $824 million, down 27% year-on-year. We believe though, Q2 was the bottom in server storage.”

“Moving on to broadband. Q2 revenue declined 39% year-on-year to $730 million and represented 10% of semiconductor revenue. Broadband remains weak on the continued pause in telco and service provider spending”

Finally, Q2 industrial rev –sales of $234 million declined 10% year-on-year.

Broadcom’s forecast are bullish reflecting optimism on earning driven by AI activity.

“For FY 2024 we expect revenue from AI to be much stronger at over $11 billion.”

“Talking of AI accelerators, you may know our hyperscale customers are accelerating their investments to scale up the performance of these clusters,”

“And to that end, we have just been awarded the next-generation custom AI accelerators for these hyperscale customers of ours.”

“We launched Tomahawk 5 in 2023. by late 2025, we should be coming out with Tomahawk 6, which is the 100 terabit switch”

“AI has been tremendous because it ties in with the need for a very large bandwidth in the networking, in the fabric for AI clusters and in AI datacentres”.

“7 out of the top 8 CSP hyperscalers use our portfolio. whether you have an architecture that's based on an endpoint and you want to actually build your platform that way or you want that switching to happen in the fabric itself, that's why we have the full end-to-end portfolio.”

Summary

Broadcom is a technology company that has grown through a series of large acquisitions.

The company has a strategy of acquiring companies in its existing area, or in adjacent competencies, and cutting costs and delayering management. However, they tend not to slash R&D expenditures.

It used to be a semiconductor and networking product company but in recent years all the acquisitions have been in software.

Leverage taken to part fund acquisitions has usually been reduced quickly after the acquisitions.

Broadcom has an effective asset light model since virtually all manufacturing is subcontracted out.

Broadcom has a vast range of products in Semiconductor services and Infrastructure solutions.

Many of the products are key components in advanced technical products.

The company is well placed to meet the demand from the boom in investment in datacentres generated by the demand for AI Workloads on the Cloud. Non-AI demand such a wireless has been subdued.

Broadcom is seeing rising demand for AI Accelerators and for its Networking products, services and software.

Broadcom is a B2B player with no consumer brand. It faces large market players such as Apple and Google who have huge market power as well as distributors who have little but are valued re-sellers.

There are some tensions with buyers such as Apple and Google. Given the latter’s scale and market power as well as prevalence of competition means there will always some friction between Broadcom and them about the exact share of the margin generated by Broadcom. The fight is well balanced as Broadcom is a supplier of critical, complex products but the customers have significant market power.

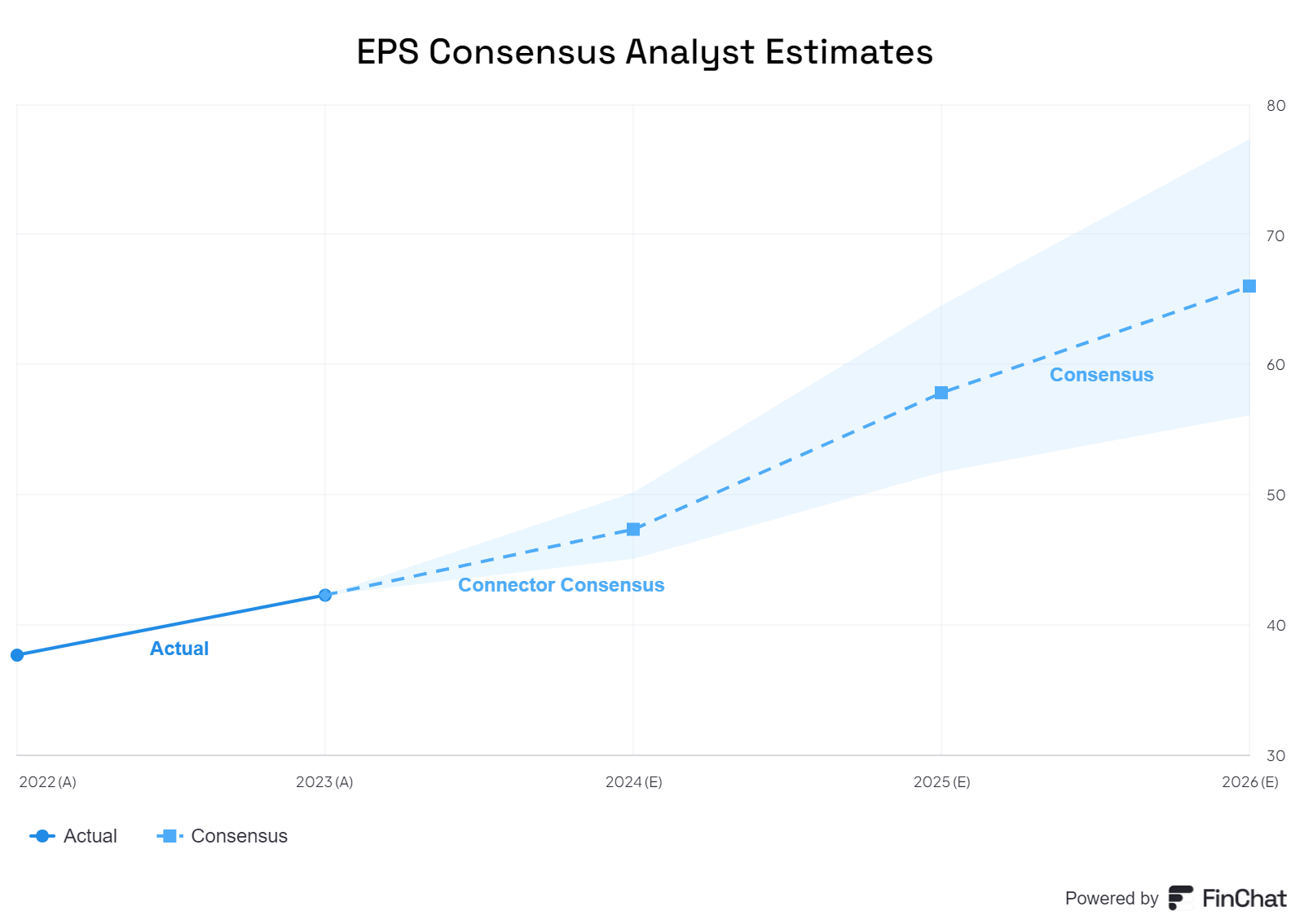

Valuation

The analysts’ consensus expectations for EPS in FY2024, FY2025 and FY2026 are at $ 47.3 $ 57.8 and $ 66 respectively. These are shown below.

We can do a quick “back of the envelope” valuation calculation.

Let us assume that the analysts’ estimates which indicate an EPS of $66 in FY 2026 prove to be accurate.

Let us further assume that this leads to EPS growth of 22% in years 4 and 5 for the next five years. We can forecast 2028 EPS to be $ 95 ((1.2)^2) * $66)

If we assume in 2027 the forward P/E multiple will be 24, the share price in 2027 will be ~$2280 per share. This compares with today’s share price of $ 1735 - a 33% discount.

A 31 % discount implies a CAGR return of 10.04 % per annum for the next three years on Broadcom Stock.

This seems a fair but not particularly attractive given the growth and profit opportunities available to the company.

We supplemented this “back of the envelope” evaluation with a Discounted Cash flow (DCF) calculation for which we made several assumptions. These include the following:

Revenue will grow at 1% in the years 2025-28. Operating margins will be 45% for the next five years.

The weighted average cost of capital (WACC) is 9.1%.

The terminal EV/FCF multiple long-term growth rate is 36 times (compared with 48 times currently)

With these and other assumptions, we estimate the fair present value of Broadcom’s stock to be about $ 1930 which is 11.3% discount to the current price of $ 1735 a stock.

As usual, we must state the caveat that these numbers are highly sensitive to the inputs. A small change in the inputs can lead to a very wide range of outputs.

For what is worth this DCF suggests the stock is a little undervalued at current levels

Conclusions

Broadcom is large company with a sweet spot in AI demand. However, it is hard to argue that the stock is cheap.

We will initiate a 1.0% allocation to the portfolio and look to increase it to 2-3% if stocks falls to a significant discount ( and makes the valuation more compelling) or if the next set of results seem to justify an additional purchase.

Great and detailed article! Small question I tried to do the valuation calculation: is it 20% instead of 22% and is the 10% cagr not 6,2% on 2028? Just to understand