We wrote about Broadcom (AVGO)on June 17th 2024. That report can be found here. In our biased view, it should be read as it is a good introduction to the company. We wrote a subsequent report three months ago which can be found here.

We invested a nominal 1% of the portfolio in the stock at the time and shares have risen about 30% since then. We had been hoping to add to our stake, if the stock fell lower, but did not get the opportunity to do so.

We decided to check in on the company in the light of their Q4 and FY 2024 Results.

Introduction

In the Report referenced above, we made the following observations at the beginning

Nvidia (NVDA) is making a lot of money selling GPUs, associated networking technologies and software to the fast-growing number of new GenAI-driven datacentres. Who else benefits from this megatrend?

AMD has been mentioned frequently in the press. They will definitely make progress as GPU demand grows and exceeds supply but their market share is currently very low.

The server manufacturers like Super Micro, Dell and Hewlett Packard Enterprises have all seen some momentum in their share prices. However, Dell has seen some reversal since the most recent earnings call. We hope to cover the server makers later in a separate note.

One company that has perhaps been less mentioned is Broadcom Inc (AVGO). It is the second largest AI chip company in the world in terms of revenue, behind NVIDIA, with many bn of dollars of AI accelerator sales. They also sell a wide range of networking products and services which will be in strong demand as AI datacentres proliferate.

We wanted to consider whether AVGO was likely to benefit from the massive AI-driven investment in datacentres.

Broadcom is sometimes perceived as roll-up operator driven by cost cutting and financial engineering like a private equity operator. The net result of all this acquisition activity is a large diversified company with a market cap of ~$1trn and ~23 divisions. It is difficult for securities analysts to research the company. The company describes itself thus:

“We offer thousands of products that are used in other end-products such as enterprise and datacentre networking, home connectivity, set-top boxes, broadband access, telecommunication equipment, smartphones and base stations, datacentre servers and storage systems, factory automation, power generation and alternative energy systems, and electronic displays.”

“We differentiate ourselves through our high-performance design and integration capabilities and focus on developing products for target markets where we believe we can earn attractive margins.”

“Many of the largest companies in the world, including most of the Fortune 500 and many government agencies, rely on our enterprise and mainframe software to help manage and secure their on-premise and hybrid cloud environments.”

Broadcom is an amalgamation of a portfolio of 16(!) semiconductor franchises and two main software franchises that have come together to form the company that exists today.

Broadcom is a global technology leader that designs, develops and supplies a broad range of semiconductor and infrastructure software solutions.

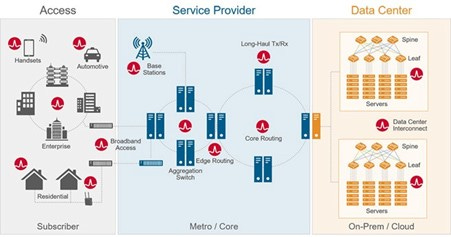

Broadcom products can be found in many parts of various types of common networks as shown with their red circle symbol in the chart above.

In semiconductors, they develop semiconductor devices with a focus on complex digital and mixed signal complementary metal oxide semiconductor (CMOS) based devices and analogue III-V based products.

One of the key products seeing huge demand in the GenAI boom are GPU Accelerators. The generally accepted definition of an accelerator is “A purpose-built design that accompanies a processor for accelerating a specific function or workload (also sometimes called “co-processors”)”. Since General Processors (GPUs) are designed to handle a wide range of workloads, processor architectures are rarely the most optimal for specific functions or workloads.”

A GPU accelerator is “hardware that is optimized for doing the computations for three-dimensional computer graphics.”

Broadcom does not compete with Nvidia as it does not design and supply GPUs. Instead, it supplies GPU accelerators which help GPUs work better for specialised tasks. Large companies such as Google and Amazon are designing their own chips (Custom Silicon) and are a major source of demand for accelerators for Broadcom,

Broadcom’s rising accelerator sales are to some significant degree currently driven by Google’s aggressive ramp up of its custom developed Tensor Processing Units (TPU)

Google’s website describes TPU as follows:

“TPUs are Google's custom-developed application-specific integrated circuits (ASICs) used to accelerate machine learning workloads. Cloud TPU is a web service that makes TPUs available as scalable computing resources on Google Cloud.”

“TPUs train your models more efficiently using hardware designed for performing large matrix operations often found in machine learning algorithms. TPUs have on-chip high-bandwidth memory (HBM) letting you use larger models and batch sizes. TPUs can be connected in groups called Pods that scale up your workloads with little to no code changes.”

Google has been investing heavily for the last five years in the Google Cloud Platform (GCP). The pace has increased significantly after the recent Microsoft + Open AI alliance that is challenging Google’s world leadership in AI.

A large part of the new workloads that will move to the Cloud in the next few years will be GenAI driven. The large Hyperscalers or Cloud Service Providers (CSPs) plus Meta Platforms are investing heavily in datacentres. Those datacentres need GPUs (Nvidia, AMD, Intel) and Accelerators (Broadcom, Marvell) as well networking (Nvidia, Broadcom, Arista, Cisco) and Software (Nvidia, AMD, Intel).

Q4 Results

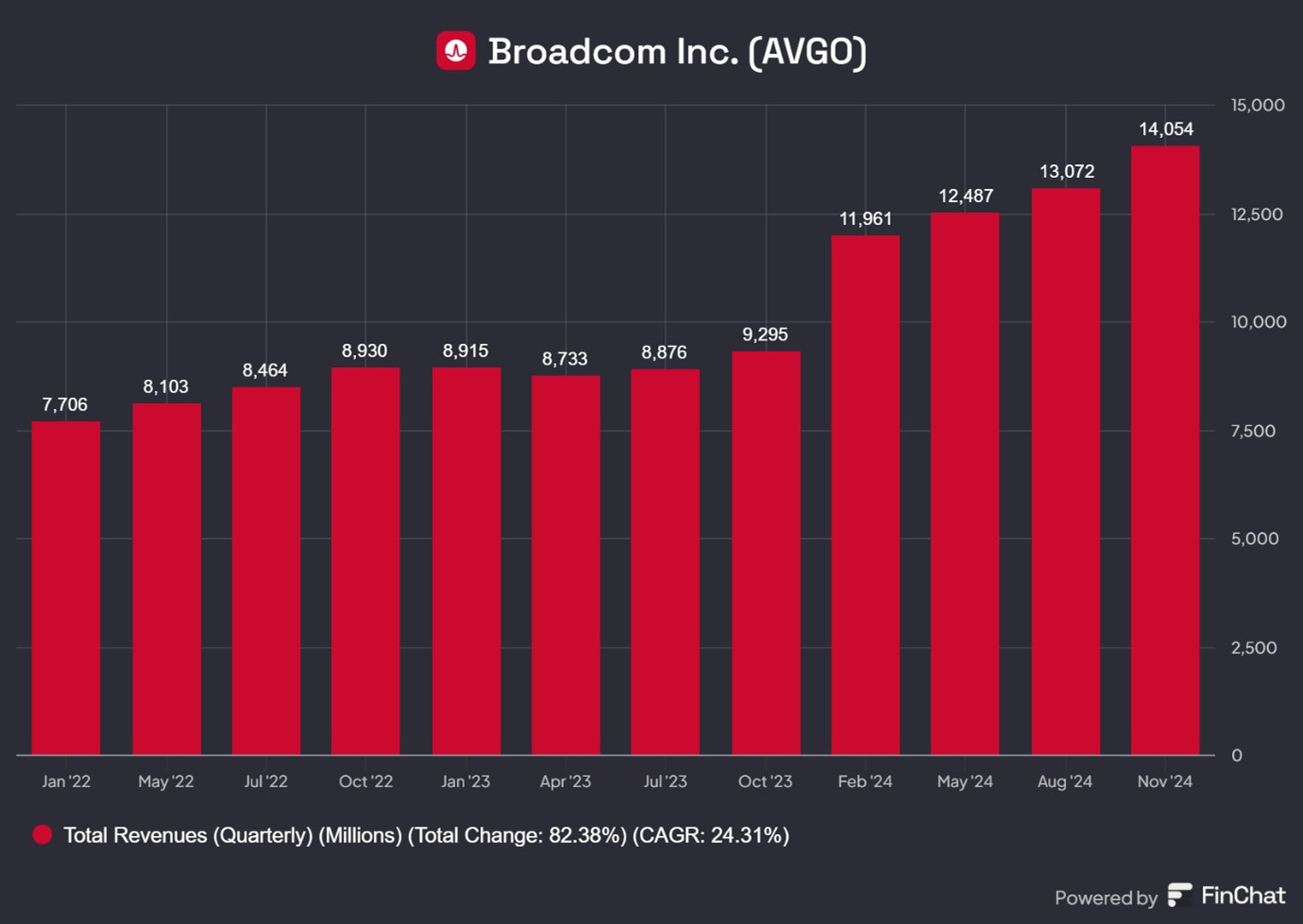

AVGO posted fourth-quarter revenue growth of 58% to $14.05bn slightly below, analysts' estimates of $14.09bn

AVGO forecasts first-quarter revenue of about $14.6bn in line with analysts' estimates.

Semiconductor revenue of $8.2bn grew 12% (y/y) and 13% sequentially.

The company highlighted that AI Revenues were very strong. Q4 AI revenue grew a strong 150% (y/y) to $3.7bn.

Networking Q4 revenue of $4.5 billion grew 45%(y/y). AI networking revenue, which represented 76% of networking, grew 158% (y/y).

AI demand was driven by a doubling of their AI XPU (AI Accelerators) shipments to their three hyperscale customers and 4X growth in AI connectivity revenue driven by their Tomahawk and Jericho shipments globally.

Detailed Financial Performance

The 58% growth in revenue to $14.1bn for Q$4 reflected the fact that numbers from VMware are included.

The chart above shows the step change in the Feb 24 quarter, when VMware numbers were first included. From the next quarter onwards, the comparisons will include the VMware numbers and the rate of change will be normalised.

Excluding the contribution from VMware and - Q4 revenue increased 11% (y/y).

Revenue for the Semiconductor Solutions segment was $8.2bn (12.3% growth (y/y)) and represented 59% of total revenue in the quarter.

Within Semiconductor Solutions, AI demand grew very fast. Q4 AI revenue grew a strong 150% (y/y) to $3.7bn. Non-AI Semiconductor Solutions revenue declined by 23% (y/y) to $4.5bn, but still a 10% recovery from the bottom of six months ago.

Revenue for infrastructure software was $5.8bn, up 196% (y/y). This was primarily due to the inclusion of VMware and it now represents 41% of revenue. This compares with about 26% before the acquisition of VMware.

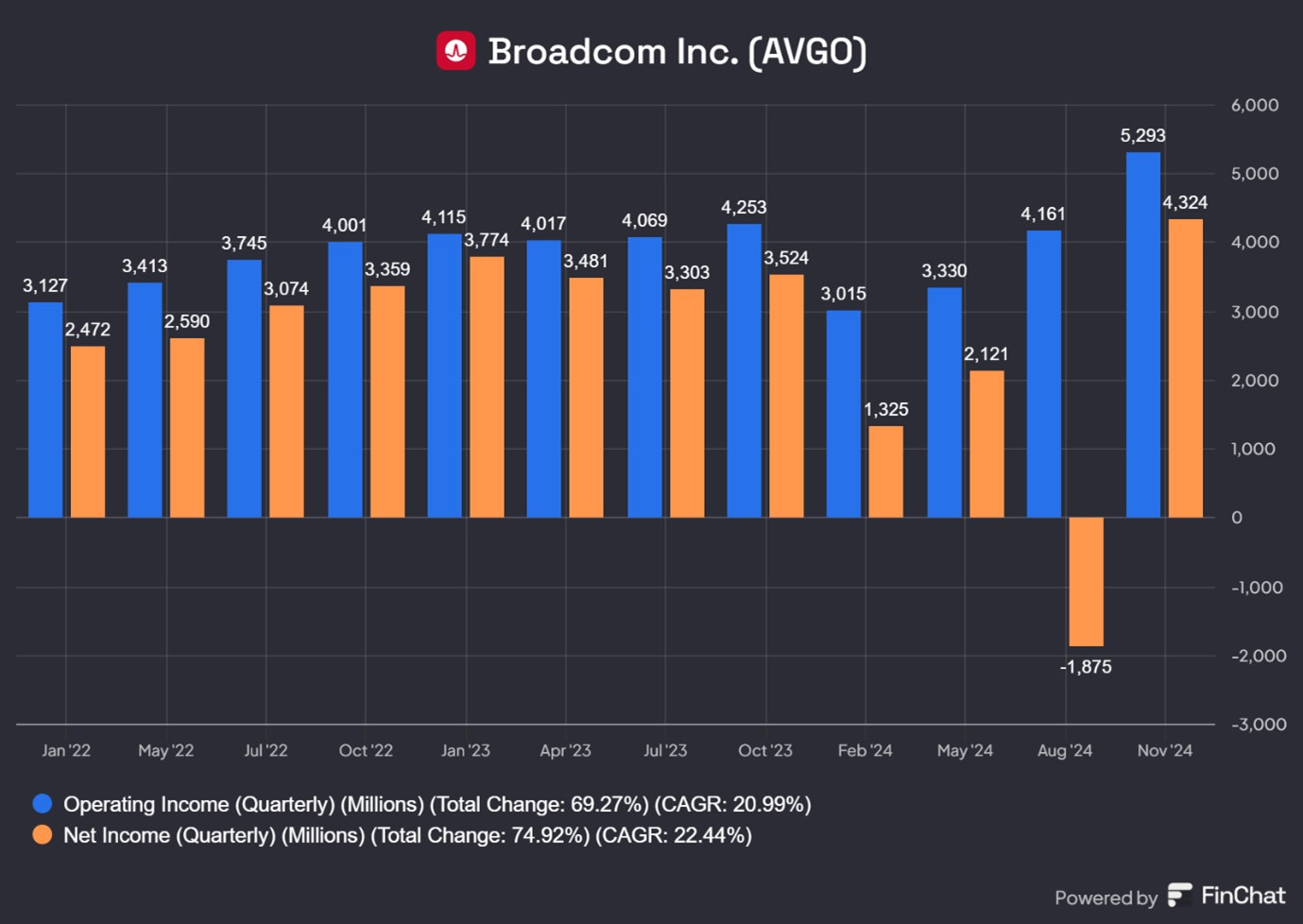

Overall Gross Margin was 75.9% while Operating Profit Margin was 37.7%. The latter was down 810bps (y/y) due to costs arising from the integration of VMware.

Operating Profits and Net Income were the highest ever in Q4 as shown above.

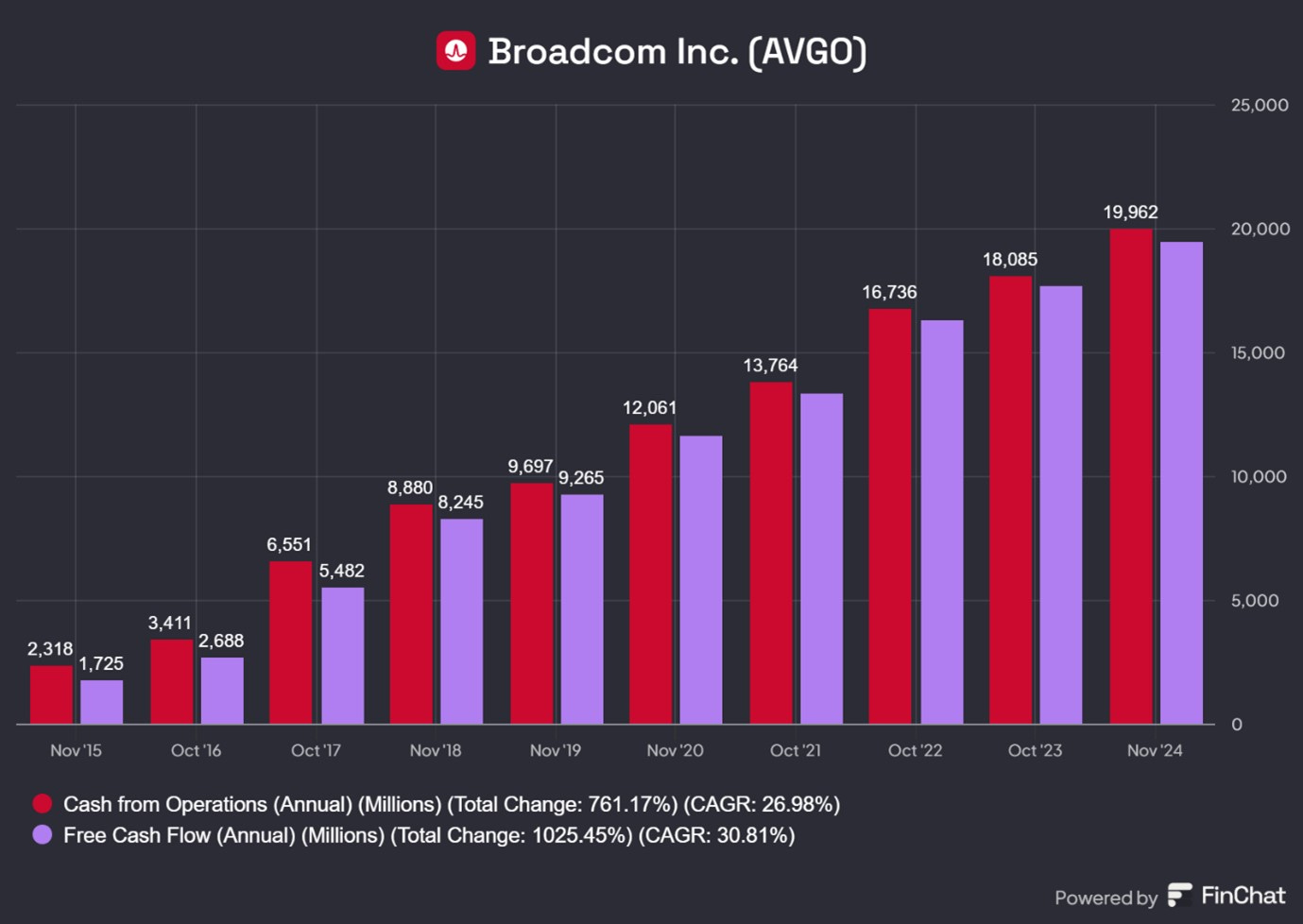

Annual Operating Cash Flow (OCF) and Free Cash Flow (FCF) show steady long -term growth.

Chart above shows quarterly OCF and FCF. The former is now at a run rate of $5.5bn per quarter. The relatively small difference between OCF and FCF is due to the very low capital expenditure in AVGO’s capital-light model, as manufacturing is outsourced to third parties.

“Excluding cash used for restructuring and integration of $506mn, free cash flows of $6 bn were up 22% (y/y) and represented 43% of revenue.”

In summary, revenues are growing strongly, even if we ignore the impact of VMware inclusion in the numbers. The company is profitable and generating annual free cash flow of about $ 20bn per annum.

Highlights from the conference call

“This has been a transformative year for Broadcom.

Our fiscal year 2024 consolidated revenue grew 44% (y/y) to a record $51.6bn.

Now, excluding VMware, our revenue grew over 9% organically.

FY 2024 operating profit, excluding transition costs grew 42%(y/y).

We returned a record $22bn in cash to our shareholders, up 45% (y/y) through dividends, buyback and eliminations.”

The company noted there are two reasons behind this performance.

The $67bn acquisition of VMware

The strength of AI demand

VMware

The integration of VMware is complete so there should not be any integration costs going forward.

First, we closed the acquisition of VMware in the early weeks of fiscal 2024 and have focused VMware on its technology leadership in data center virtualization. The integration of VMware is largely complete.”

“(VMware) Revenue is on a growth trajectory and operating margin reached 70% exiting 2024. We are well on the path to delivering incremental adjusted EBITDA at a level that significantly exceeds the $8.5bn we communicated when we announced the deal. We are planning to achieve this much earlier than our initial target of three years.”

“In VMware, we booked $21mn total CPU costs in a quarter versus $19mn a quarter ago. Of these, about 70% represented VMware Cloud Foundation or VCF, the full software stack virtualizing the entire data center. And this translated into Annualized Booking Value (ABV) \ of $2.7bn for VMware in Q4 up from $2.5 bn in Q3. Since closing the acquisition just over a year ago, we've signed up over 4,500 of our largest 10,000 customers for VCF.”

AI

“Our AI revenue, which came from strength in custom AI accelerators or XPUs and networking, grew 220% from $3.8bn in fiscal 2023 to $12.2bn in FY 2024 and represented 41% of our semiconductor revenue.”

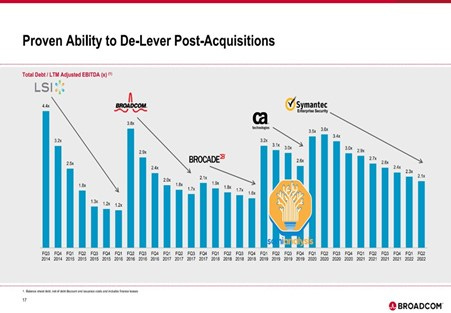

Post acquisition Debt

AVGO post-acquisition strategy is to cut costs in the company that has been acquired and successfully deleverage in the two to three years following the acquisition.

The chart above shows their effective de-leveraging after past acquisitions.

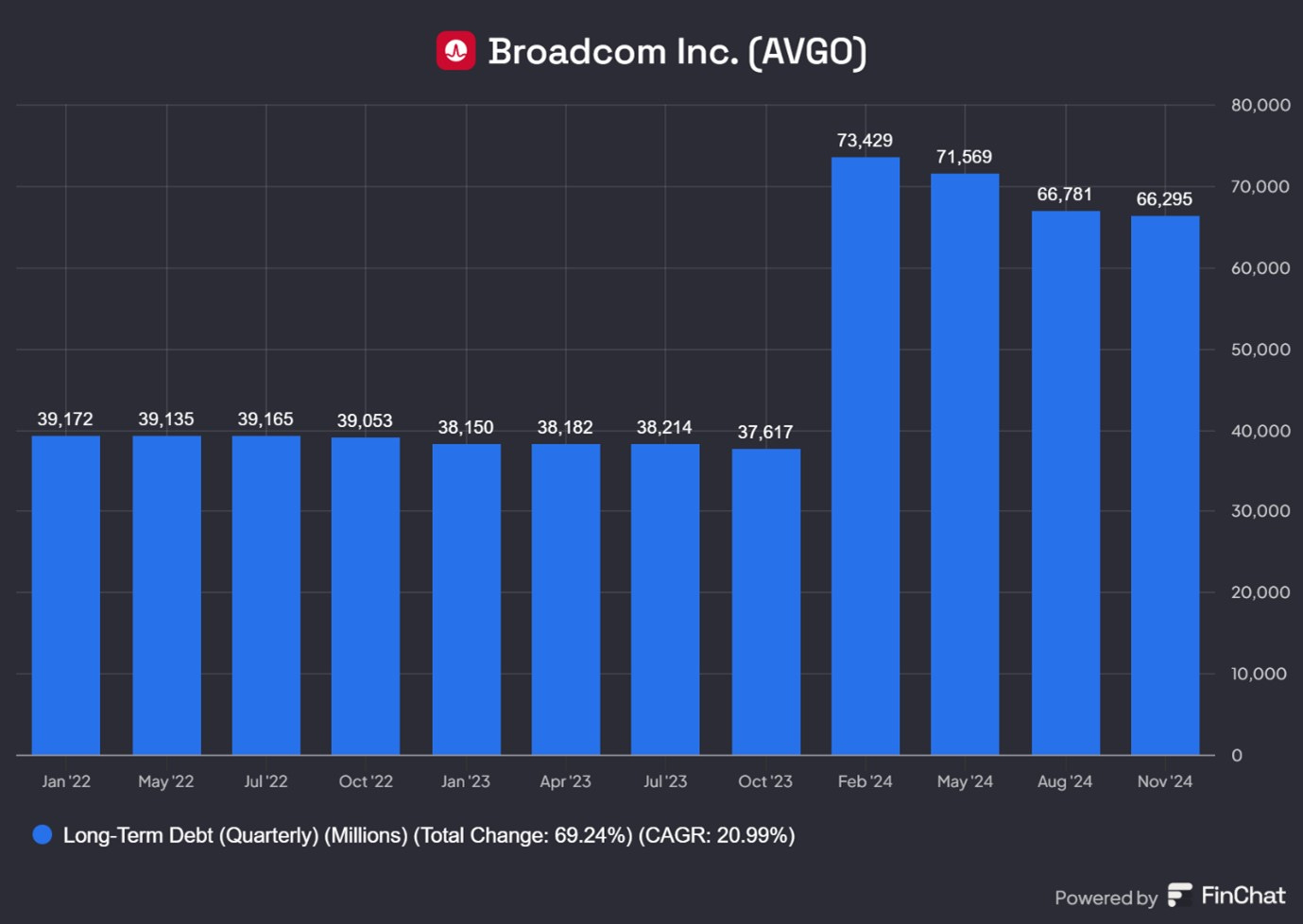

Long-term debt doubled to $73bn at the beginning of 2024, due to the acquisition of VMware but has already started to decline.

AVGO has started to cut costs in VMware.

“We continued to drive down spending in VMware. We brought spending down to $1.2bn in Q4, down from $1.3bn in Q3. VMware spending was averaging over $2.4bn per quarter prior to the acquisition with operating margin less than 30%.

AVGO has been reducing the debt as can be seen on the chart above.

“We ended the fourth quarter with $9.3bn of cash and $69.8bn of gross principal debt. During the quarter, we replaced $5bn of floating rate debt with new senior notes. We use cash on hand to pay a mix of senior notes, which came due in Q4 and additional floating rate debt, reducing debt by $2.5 bn.”

“Following these actions, the weighted average coupon rate and years to maturity of our $56 bn in fixed rate debt is 3.7% and 7.6 years, respectively. The weighted average coupon rate and years to maturity of our $14bn in floating rate debt is 5.9% and 3.2 years, respectively. We expect to repay approximately $495 mn of fixed rate senior notes coming due in Q1.”

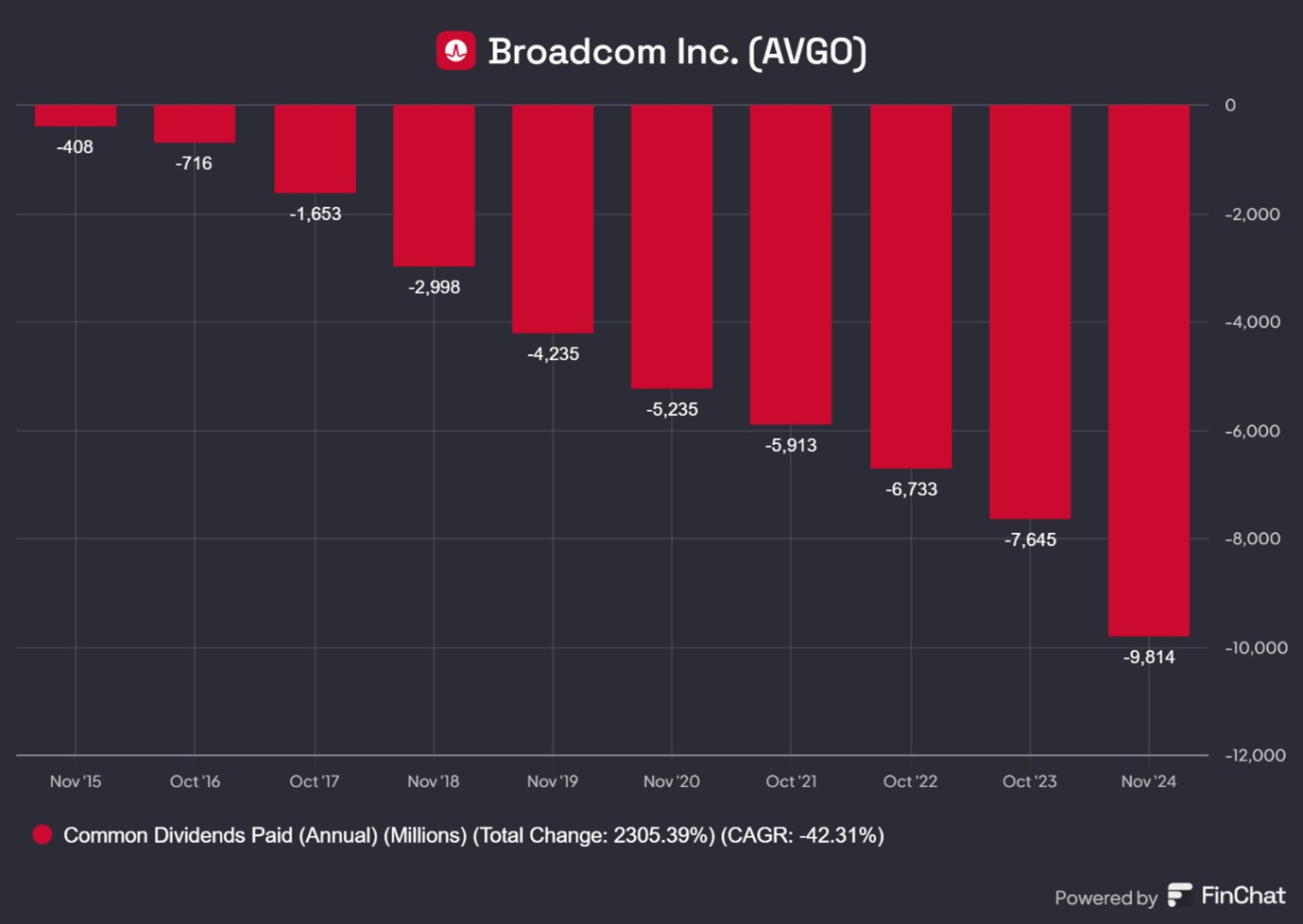

The Chart above shows the annual dividend payment which has grown to $10bn per annum. The bars in the chart above are shown as negative, as the dividend is a cash outflow for the company.

The Company’s annual Free Cash Flow (FCF) run rate is $20bn. If $10bn is used for dividends, debt can be reduced by up to $10bn per annum. Therefore, it would fall by 30% in two years.

Q1 Outlook

“In Q1, we expect the momentum in AI connectivity to be as strong as more Hyperscalers deploy Jericho3-AI in their fabrics. Our next generation XPUs are in 3 nanometres and will be the first of its kind to market in that process node. We are on track for volume shipment at our hyperscale customers in the second half of fiscal 2025.”

Contrast between AI and non-AI Semiconductor business

“On the broad portfolio of non-AI semiconductors with its multiple end-markets, we saw a cyclical bottom in fiscal 2024 at $17.8bn. We expect a recovery from this level at the industry's historical growth rate of mid-single digits.

“In sharp contrast, we see our opportunity over the next three years in AI as massive. Specific hyperscalers have begun their respective journeys to develop their own custom AI accelerators or XPUs, as well as network these XPUs with open and scalable Ethernet connectivity. For each of them, this represents a multi-year, not a quarter-to-quarter journey.”

Huge Forthcoming AI Demand

“We currently have three hyper-scale customers who have developed their own multi-generational AI XPU roadmap to be deployed at varying rates over the next three years. In 2027, we believe each of them plans to deploy 1 million XPU clusters across a single fabric.”

“We expect this to represent an AI revenue Serviceable Addressable Market, or SAM, for XPUs and network in the range of $60bn to $90bn in fiscal 2027 alone.”

Broadcom can only hope to capture some fraction of this but even that could represent a significant revenue boost.

“We are very well positioned to achieve a leading market share in this opportunity and expect this will drive a strong ramp from our 2024 AI revenue base of $12.2bn. We have been selected by two additional hyperscalers and are in advanced development for their own next generation AI XPUs.We have line of sight to develop these prospects into revenue generating customers before 2027 and could therefore expand the SAM significantly.”

“We are working very hard with them ( the two additional Hyperscalers) to get it production stage. We're pretty deeply engaged with tape-out chips. And -- but they've got to get their software ready, they got to get it tested and they got to get going on it. So now I'm not sure – but definitely over the next three years.”

Capital Allocation

As noted above the Free Cash Flow in FY 2024 was $20bn. AVGO returned $ 22bn to share holders in that period.

“For FY 2024, we spent $22.2bn, consisting of $9.8bn in the form of cash dividends and $12.4bn in share repurchases and eliminations.”

“We are announcing an increase in our quarterly common stock cash dividend in Q1 fiscal 2025 to $0.59 per share on a split-adjusted basis, an increase of 11% from the prior quarter. This implies that our fiscal 2025 annual common stock dividend to be a record $2.36 per share on a split-adjusted basis, an increase of 12% (y/y). This represents the 14th consecutive increase in annual dividends, since we initiated dividends in fiscal 2011.”

Going forward, the company will maintain and grow the dividend but will also use part of the remaining cash to reduce debt.

“We do intend to use part of that 50% free cash flow that's not used for dividends to go de-lever ourselves, given the size of the debt we are taking on -- or we have taken on since we acquired VMware.”

Serviceable Addressable Market, (SAM)

The company is forecasting a SAM of $60bn to $90bn revenue range by FY 2027 for AI.

This is an estimate based on the likely investment plans of their three large Hyperscaler customers.

“First, on the total dollars, by the way, is the revenue opportunity for us is what I call Serviceable Addressable Market, as we all term SAM., and is Serviceable Addressable Market for three of our hyperscale customers. That's it. It's a very narrow Serviceable Addressable Market we're talking about.”

The SAM will grow from the current level of $ 20bn.

“Where we are saying what is the baseline on the $60bn to $90bn in three years' time, where we are specifying down to these three customers of ours. And I would estimate this 2024 for that to be about less than $20bn - $15bn to $20bn at this point, in 2024.”

AVGO will only get a fraction of that SAM. They believe AI connectivity will be 15% to 20% of the SAM.

Technology and deep embedded relationships with key large clients

“We have, by far, one of the best technology -- combination technology out there to do XPUs and to connect those XPUs. The silicon technology that enables it, we have it here in Broadcom by the boatloads, which is why we are very well positioned with these three customers of ours.”

“This has been going on now for a while in terms of deep engagement with engineering teams from the other side -- each of the other side, we are very-well positioned, well underway to creating a multiyear road map for -- to enable these few customers of ours to get to when their ambition leads them to be in.”

Summary

The reported quarterly performance was boosted by the inclusion of the very large ($67bn) VMware acquisition which concluded about a years ago.

· It was a good performance even if we ignore the effects of VMware with organic revenues growing about 11% (y/y).

· AI Revenue is growing strongly and AVGO expect it to grow 65% (y/y)

· They expect the Serviceable Addressable Market (SAM) in 2027 from just their three large Hyperscaler clients will be $60bn-$90bn. They expect to target about 15%-20% of that.

· This large SAM estimate caught the attention of market participants and the stock rose 38% in the two days after the results were announced.

· The company is a large diversified technology company which has grown inorganically over many years.

Valuation

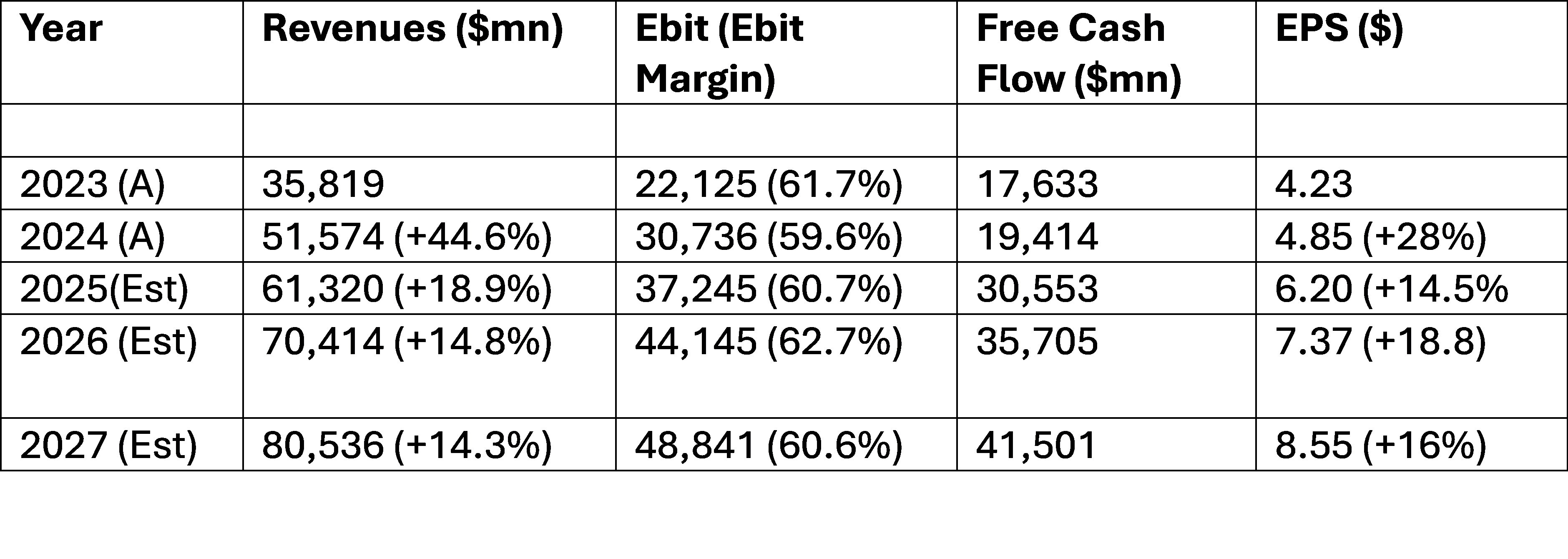

The consensus analysts’ forecasts for Revenues, EBIT, EBIT Margin, Free Cash Flow and EPS are as follows:

The analysts’ consensus estimates show steady double digit percentage revenue growth in FY 2026 and FY 27.

Operating margins are expected to be maintained at 60%.

This will lead to higher profitability and double-digit percentage EPS growth in the next three years.

Free Cash Flow will more than double to over $ 40bn in 2027.

At the current price of $223, AVGO stock is trading at a two-year forward P/E Ratio of 30X. The three-year forward P/E Ratio is 26X.

At a current market capitalization of $1trn, the two- year forward Price to Free Cash Flow ratio is 28.6X.

These numbers imply a two-year forward Earnings Yield of about 3.3% and a two-year Free Cash Flow Yield of 3.4.%.

The stock appears to be overvalued but this is not surprising as it has advanced 116% year to date. We conducted a Discounted Cash Flow (DCF) Calculation which suggested the stock is overvalued by about 20%

As we have noted before, the problem with all such valuation models is they are highly dependent on the inputs. If one makes small changes in the assumptions, there can be a wide range in the outputs. Therefore, all valuation estimates must be taken with a lot of salt.

It is however difficult to avoid the conclusion that the company is overvalued currently.

Conclusions

The company is a large diversified technology company which has grown inorganically over many years.

It is well set to grow revenues and earnings by double digit percentages over the next few years thank to the boom in AI-driven infrastructure investment.

However, at current levels, the stock, like much of the rest of the market, looks expensive.

We will have a position of 1.2% of the portfolio in the stock. We will not add to it but we will continue to hold