Broadcom Inc (AVGO)

Q2 2025 Results.

We wrote about Broadcom (AVGO)on June 17th 2024. That report can be found here. In our biased view, it should be read as it is a good introduction to the company! We wrote a subsequent report which can be found here. We decided to check in on the company again in the light of their Q2 2025 Results.

Introduction

In the first report referenced above, we made the following observations at the beginning of the note.

Nvidia (NVDA) is making a lot of money selling GPUs, associated networking technologies and software to the fast-growing number of new GenAI-driven datacentres. Who else benefits from this megatrend?

AMD has been mentioned frequently in the press. They will make progress as GPU demand grows and exceeds supply, but their market share is currently very low. The server manufacturers like Super Micro, Dell and Hewlett Packard Enterprises have all seen some momentum in their share prices. However, Dell has seen some reversal since the most recent earnings call.

One company that has perhaps been less mentioned is Broadcom Inc (AVGO). It is the second largest AI chip company in the world in terms of revenue, behind NVIDIA, with many billions of dollars of AI accelerator sales. They also sell a wide range of networking products and services which will be in strong demand as AI datacentres proliferate. These accelerators are sometimes called XPUs.

We wanted to consider whether AVGO was likely to benefit from the massive AI-driven investment in datacentres. Broadcom is sometimes perceived as roll-up operator driven by cost cutting and financial engineering like a private equity operator. The net result of all this acquisition activity is a large, diversified company with a market cap of ~$.2trn and ~23 divisions. It is difficult for securities analysts to research the company. The company describes itself thus:

“We offer thousands of products that are used in other end-products such as enterprise and datacentre networking, home connectivity, set-top boxes, broadband access, telecommunication equipment, smartphones and base stations, datacentre servers and storage systems, factory automation, power generation and alternative energy systems, and electronic displays.”

“We differentiate ourselves through our high-performance design and integration capabilities and focus on developing products for target markets where we believe we can earn attractive margins.”

“Many of the largest companies in the world, including most of the Fortune 500 and many government agencies, rely on our enterprise and mainframe software to help manage and secure their on-premises and hybrid cloud environments.”

Broadcom is an amalgamation of a portfolio of 16(!) semiconductor franchises and two main software franchises that have come together to form the company that exists today.

Broadcom is a global technology leader that designs, develops and supplies a broad range of semiconductor and infrastructure software solutions.

Broadcom products can be found in many parts of various types of common networks as shown with their red circle symbol in the chart above.

One of the key products seeing huge demand in the GenAI boom are GPU Accelerators which are also known as XPUs.

The generally accepted definition of an accelerator is “A purpose-built design that accompanies a processor for accelerating a specific function or workload (also sometimes called “co-processors”)”.

Since General Processors (GPUs) are designed to handle a wide range of workloads, processor architectures are rarely the most optimal for specific functions or workloads.”

A GPU accelerator is “hardware that is optimized for doing the computations for three-dimensional computer graphics.”

Broadcom does not compete with Nvidia as it does not design or supply GPUs. Instead, it supplies GPU accelerators which help GPUs work better for specialised tasks. Large companies such as Google and Amazon are designing their own chips (Custom Silicon) and are a major source of demand for accelerators for Broadcom,

Broadcom’s rising accelerator sales are to some significant degree currently driven by Google’s aggressive ramp up of its custom developed Tensor Processing Units (TPU)

Google’s website describes TPU as follows:

“TPUs are Google's custom-developed application-specific integrated circuits (ASICs) used to accelerate machine learning workloads. Cloud TPU is a web service that makes TPUs available as scalable computing resources on Google Cloud.”

“TPUs train your models more efficiently using hardware designed for performing large matrix operations often found in machine learning algorithms. TPUs have on-chip high-bandwidth memory (HBM) letting you use larger models and batch sizes. TPUs can be connected in groups called Pods that scale up your workloads with little to no code changes.”

Google has been investing heavily for the last five years in the Google Cloud Platform (GCP). The pace has increased significantly after the recent Microsoft + Open AI alliance that is challenging Google’s world leadership in AI.

A large part of the new workloads that will move to the Cloud in the next few years will be GenAI driven. The large Hyperscalers or Cloud Service Providers (CSPs) plus Meta Platforms are investing heavily in datacentres. Those datacentres need GPUs (Nvidia, AMD, Intel) and Accelerators (Broadcom, Marvell) as well networking (Nvidia, Broadcom, Arista, Cisco) and Software (Nvidia, AMD).

Q2 2025 Results

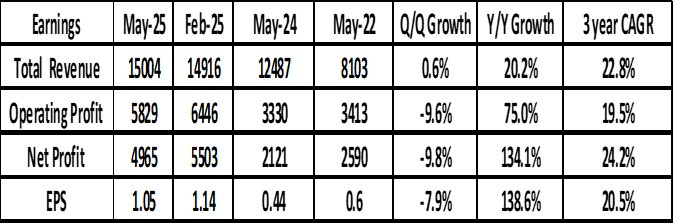

Q2 Revenues grew 20% to $15bn. This growth was all organic as Q2 last year was the first full quarter with VMware numbers included. Revenue was driven by continued strength in AI semiconductors and the momentum in VMWare.

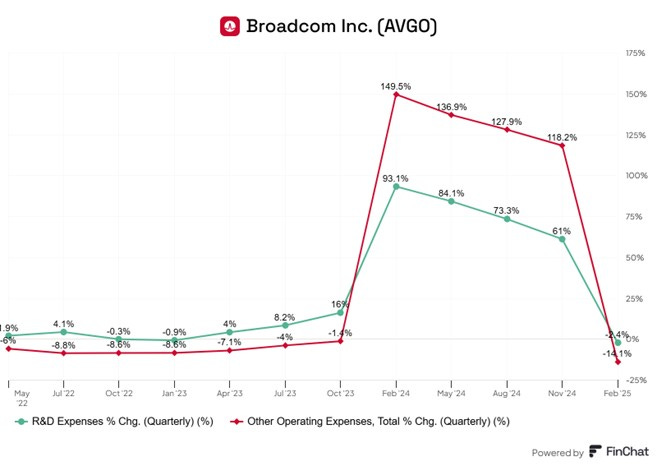

Operating Profits and Net Profits grew much faster at 75% and 134% (y/y) respectively. May 2024 profits were much lower due to much higher R&D and other operating costs due to the inclusion of VMWare. The rise can be seen in the chart below.

The company seems to have done a good job in reducing these costs in the last year. Given this improvement, Q2 2025 numbers showed very high growth.

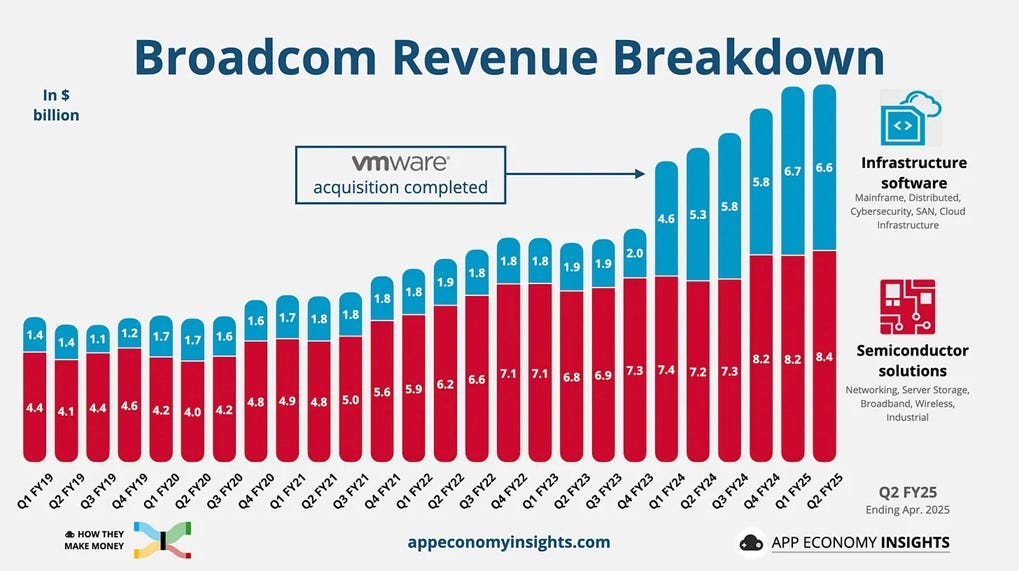

The main segments are Semiconductor solutions (SS) and Infrastructure Software (IS).

Q2 SS revenue was $8.4bn with growth of 17% (y/y)

This was driven by growth in AI semiconductor revenue of 46% (y/y), which AVGO claims is nine consecutive quarters of strong growth.

Within AI, Networking grew particularly strongly and accounted for 40% of AI Revenue, above the long-term average of 30%.

Non-AI SS revenue of $4bn and down 5% (y/y).

IS grew 24.8% (y/y) to $6.5bn. This was driven by strong demand for VMWare products.

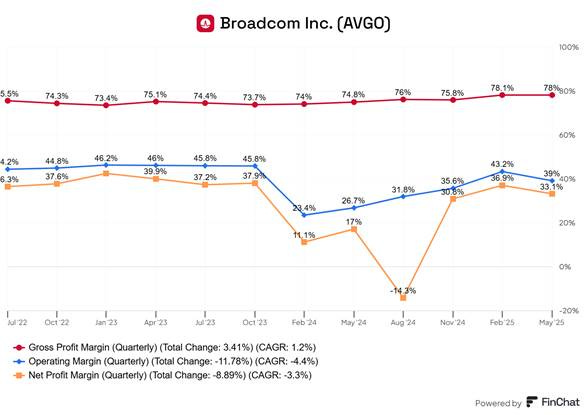

Company level margins were much higher compared to a year ago. Firm Gross Margin was 79.4% and Operating Margin was 38.8%. This reflects the significant cost cutting noted above.

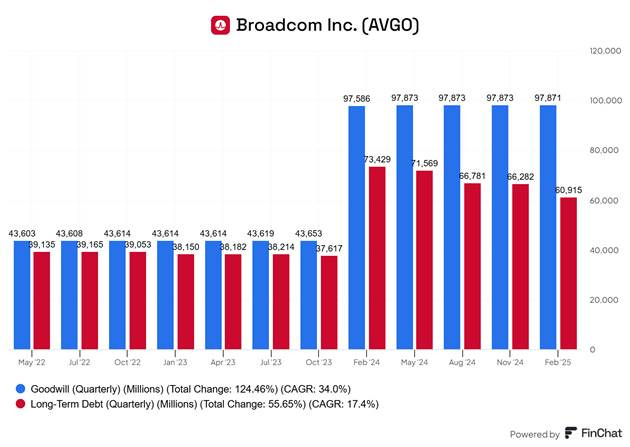

Broadcom acquired VMware for $67bn in February 2024, and this was still impacting in the consolidated numbers for the first time in the quarter ending November 2024 (Q4).

The VMware numbers are included in Infrastructure software segment. Their inclusion had the effect of increasing Infrastructure Software Revenues and reduced operating margins.

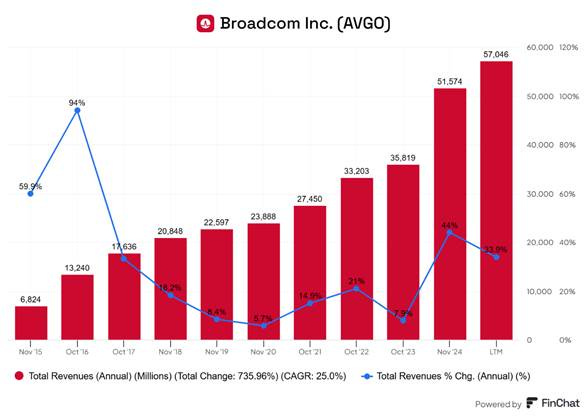

The chart below shows the step change in both Total Revenues and Infrastructure Software Revenues after VMWare.

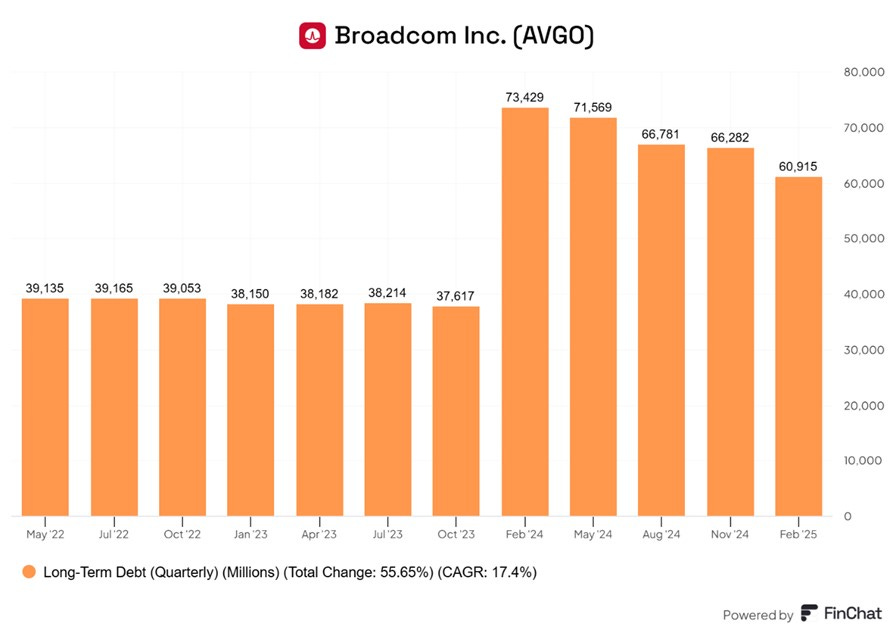

There was also a decline in operating margins after the VMWare acquisition. The $67bn purchase was part funded by debt and led to an increase in Long-term debt and Goodwill.

Debt has declined suggesting the company retains the capacity to de-leverage quickly after an acquisition as they have done historically.

This continues the Broadcom playbook where they reduced debt progressively after acquisitions such LSI, the reverse takeover of Broadcom, Brocade Communications, Computer Associates and Symantec. Their usual long- term target is to bring long-term debt down to about 2X of Ebitda. The chart below shows they tend to approach that level before a new acquisition is considered.

Quick Financial Summary in Charts

Q2 revenue growth has slowed down as the VMWare acquisition is not in the picture anymore. However, it still grew at an impressive 20%.

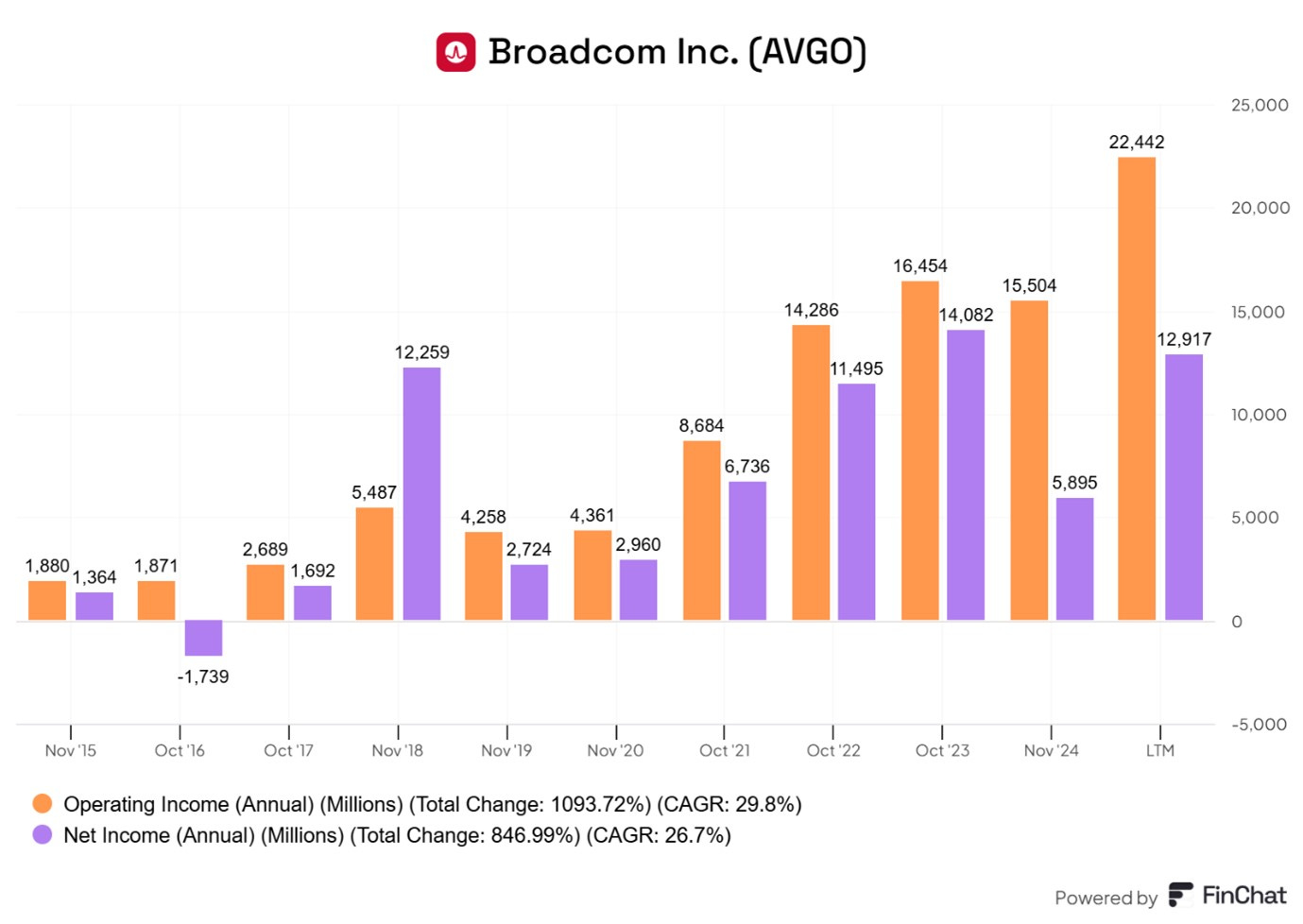

Over a longer period of a decade, Total revenue has grown at a CAGR of 25%. Over the same period, Operating Profit and Net Profit have grown 29.8% and 26.7%, respectively.

Margins have been stable except for the post-VMWare acquisition decline and a hit to Net Margins in August 2024.

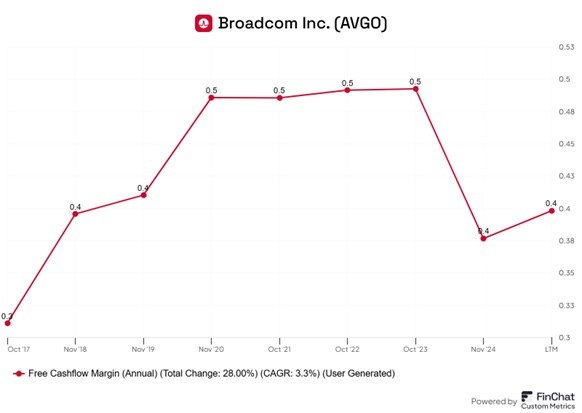

n the last decade, Cash Flow has grown, not surprising fact as Broadcom has acquired a few large companies. For example, Free Cash Flow growth has been 30.8% CAGR over the last decade.

Free Cash Flow in the quarter was $6.4bn and represented 43% of revenue. This metric is Free Cash Flow Margin and is shown in the chart below. Cash flow strength bodes well for their ability to reduce long-term debt from the current $60bn.

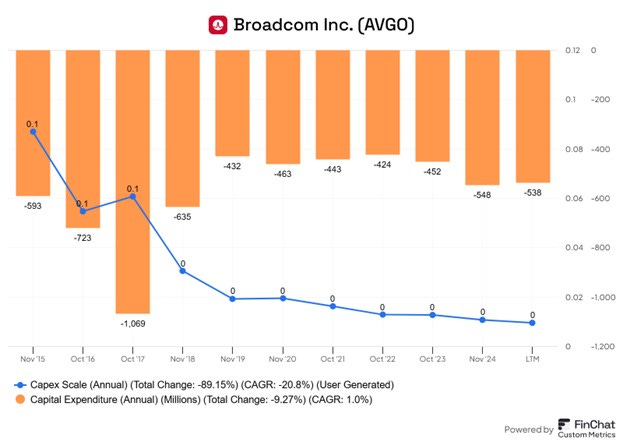

The company has a capital-light model[1] and fixed capital investment is negligible. For example, it was $548mn in FY 2024 which is 1.0% of revenues.

Capex is shown as a negative bar in the above chart as it is a cash outflow. Capex Scale which we define as Capex to Revenues is shown a the blue line above and s currently about 1.2%.

The chart above shows the profitability of the company as measured by ROIC and ROE. Profitability declines after an acquisition, but rises as the company cuts costs and deleverages.

Over the last15 years, the company has given a CAGR total return of 40%.

In the last 3 years, the company has given a CAGR total return of 67%.

Q3 Outlook as forecast by management

Q3 total revenue is forecast to be $15.8bn up 21% (y/y).

Q3 Semiconductor Solutions revenue of is forecast to be $9.1bn up 25% (y/y). Within this AI semiconductor revenue of $5.1bn up 60% (y/y).

In Q3 infrastructure software revenue to forecast to be approximately $6.7bn up 16% (y/y)

Margins are expected to decline by about 1.3%, primarily reflecting a higher mix of XPUs in AI revenue. Networking which is higher margin business will not grow as fast.

In summary, management expects current trends to continue in Q3.

Highlights of the Conference Call

AVGO believe they have the right portfolio to meet demand generated by the huge capex by the handful of large tech player investing a scale in AI Datacentres.

Our networking portfolio of Tomahawk switches, Jericho routers and NICs (Network Interface card) is what's driving our success within AI clusters in hyperscalers.

Broadcom are very excited about the launch of their latest Tomahawk Switch

Momentum continues with our breakthrough Tomahawk six switch just announced this week. This represents the next generation 102.4 terabits per second switch capacity. It enables clusters of more than hundred thousand AI accelerators to be deployed in just two tiers instead of three. This flattening of the AI cluster is huge because it enables much better performance in training next generation frontier models through a lower latency, higher bandwidth, and lower power.

They are not selling it yet but sending out to existing customers to deploy as proof of concept.

Now we're not shipping, big orders or any orders other than basic proof of concepts out to customers, but there is tremendous demand for this new 102 terabit per second Tomahawk switches.

Their main AI business is selling Accelerators or XPUs to three large AI datacentres players. These are not names but are likely to be Amazon, Google and perhaps Microsoft.

Turning to XPUs or custom accelerators. excellent progress on the multiyear journey of enabling our three customers and four prospects to deploy Customer AI accelerators.

We eventually expect at least three customers to each deploy 1mn AI accelerated clusters by 2027, largely for training their frontier models. And we forecast and continue to do so a significant percentage of these deployments to be custom XPUs.

What we have quite a bit of visibility increasingly is increased deployment of XPUs next year, much more than we originally thought.

In the recent Nvidia earnings call, Jensen Huang the CEO said LLM Inference-driven demand from the large players was very strong. Broadcom management confirmed this.

They are doubling down on inference in order to monetize their platforms. And reflecting this, we may actually see an acceleration of XPU demand into the back half of this year to meet urgent demand for inference on top of the demand we have indicated from training.

Broadcom is a technology conglomerate built inorganically. They have many product and software offerings. Currently, other than AI and Networking, demand is sluggish.

Non-AI Semiconductor revenue is close to the bottom, has been relatively slow to recover, but there are bright spots. In Q2, Broadband, Enterprise Networking and Server Storage revenues were up sequentially. However Industrial was down and Wireless was also down due to seasonality.

The VMWare acquisition has boosted Enterprise Networking.

The momentum from strong VCF[2] sales over the past eighteen months since the acquisition of VMware has created annual recurring revenue or otherwise known as ARR growth of double digits in our core infrastructure software.

This growth reflects our success in converting our enterprise customers from perpetual vSphere to the full VCF software stack subscription. Customers are increasingly turning to VCF to create a modernized private cloud on prem, which will enable them to repatriate workloads from public clouds while being able to run modern container-based applications and AI applications.

Of our 10,000 largest customers, over 87% have now adopted VCF.

In the previous earnings call, they had outlined the reasons for the good progress in selling VCF.

And as of today, in collaboration with NVIDIA, we have 39 enterprise customers for the VMware Private AI Foundation. Customer demand has been driven by our open ecosystem, superior load balancing, and automation capabilities, which allow them to intelligently pool and run workloads across both GPU and CPU infrastructure, leading to very reduced costs.

They were asked for a more detail on the reasons for the strong Networking demand. They noted the difference between Scale Up and Scale Out. The latter is the building of new datacentres; the former is where they add more equipment in, and increase the density of, existing datacentres.

AI networking goes pretty hand in hand with deployment of AI accelerated clusters. They're deployed a lot in scale out where Ethernet, of course, is the choice of protocol, but it's also increasingly moving into the space of what we all call scale up within those data centres, where you have much higher, more than we originally thought consumption or density of switches than you have in the scale out scenario. It's in fact, the increased density in scale up is five to 10 times more than in scale out.

Broadcom are also working with four other large technology companies, but they have not become customers yet. There is long journey (perhaps a year long) between initial deploying and configuration and the flow of large orders.

Even as we have three hyperscale customers, we are shipping XPUs in volume today. There are now four more who are deeply engaged with us to create their own accelerators. These four are not included in our estimated SAM[3] of $60bn to $90bn in 2027.

As custom accelerators get used and get developed on a on a road map with any particular hyperscaler, that's a learning curve, a learning curve on how they could optimize the way the algorithms on their large language models gets written and tied to silicon. And that ability to do so is a huge value added in creating, algorithms that can drive their LLMs to higher and higher performance, much more than, basically a segregation approach between hardware and the software. you literally combine end to end hardware and software as they take that as they take that journey. They don't learn that in one year.

It will take time, but they are optimistic it will lead to large XPU orders from these additional four customers.

Do it a few cycles, get better and better at it, and therein lies the fundamental value in creating your own hardware versus using a third-party merchant silicon: you are able to optimize your software to the hardware and eventually achieve way higher performance than you otherwise could. we also limit ourselves in selecting partners to people who really need that large volume.

Tariffs and export controls to China.

They were asked about the impact of tariffs and export controls. They have a capital light models and all their manufacturing is outsourced to China and the Far East.

Nobody can give anybody comfort in this environment, Joe. You know that. Rules are changing quite dramatically as trade bilateral trade agreements continue to be negotiated in a very, very dynamic environment. So I'll be honest, I don't know. I know as little as probably you probably know more than I do maybe, in which case then I know very little about this whole thing about how whether there's any export control, how the export control will take place.

Research and Development

They do not do much Capex. However, they do spend large sums on R&D. these are expensed in the P&L immediately[4] and accounts for about 17% of revenues.

Summary

Broadcom is seeing strong demand in XPUs and In Networking products offered by VMWare.

Broadcom is in a sweet spot in AI-demand. Current growth is driven by three large customers. It will grow further when they have 7 such customers. This is likely in the next six months.

They have successfully integrated the Feb 20204 VMWare acquisition taking out a lot of costs.

Profits have recovered strongly and Cashflows have been strong.

Profitability has recovered and the improving trend should continue.

The stock has given very strong investor returns in the last 15 years.

Valuation

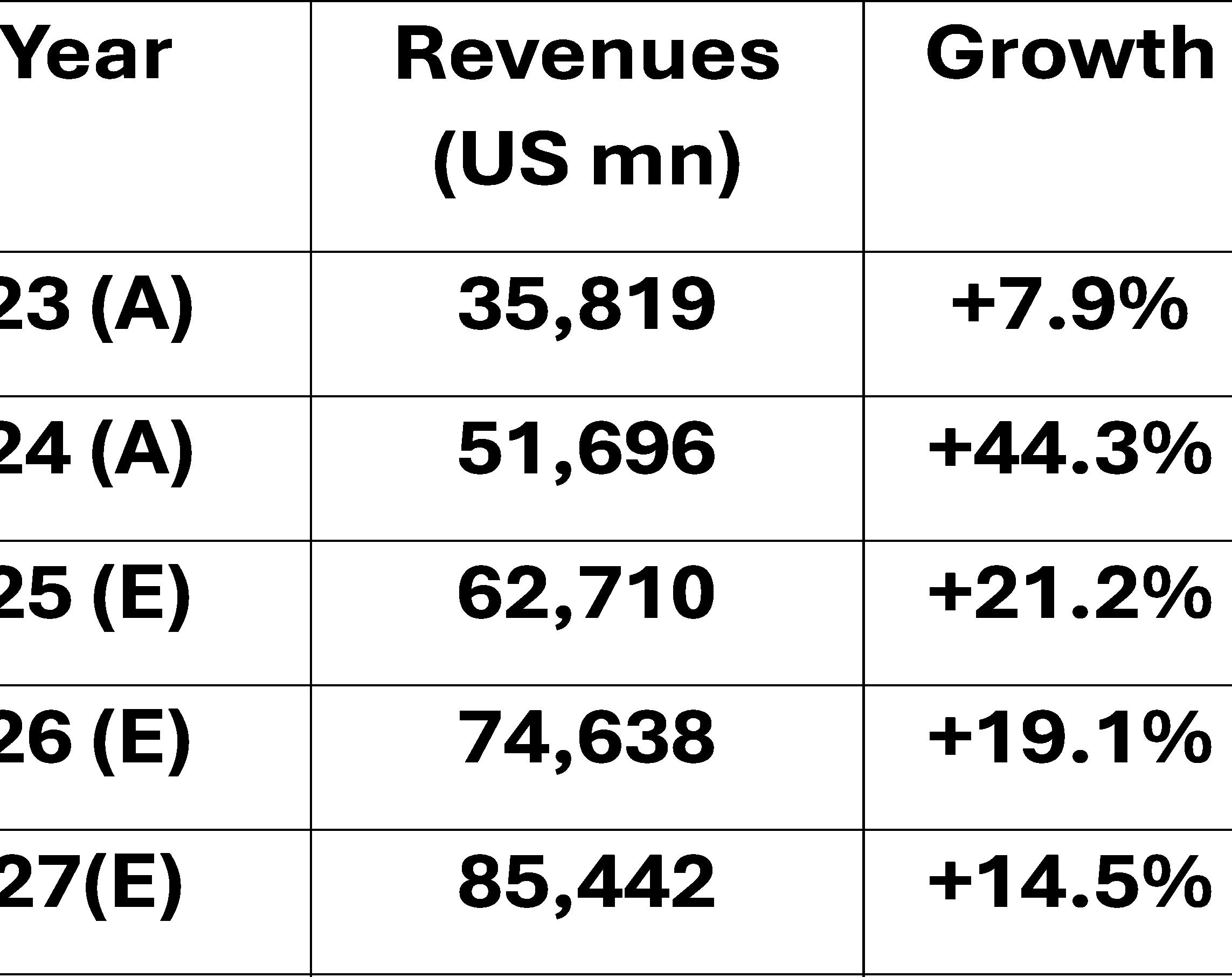

The consensus analysts’ forecasts for revenues are as follows:

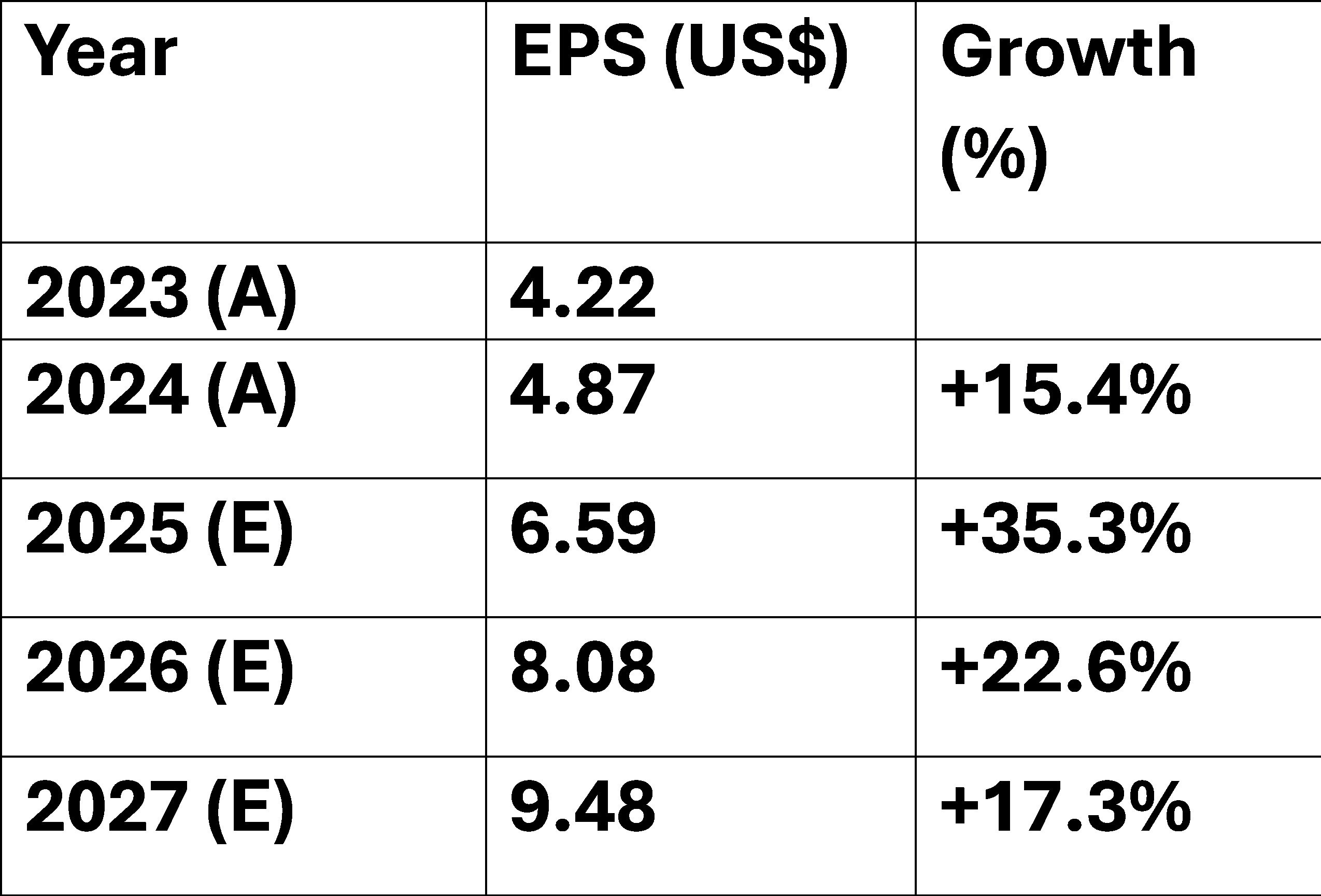

The analysts’ consensus estimates for EPS are as follows:

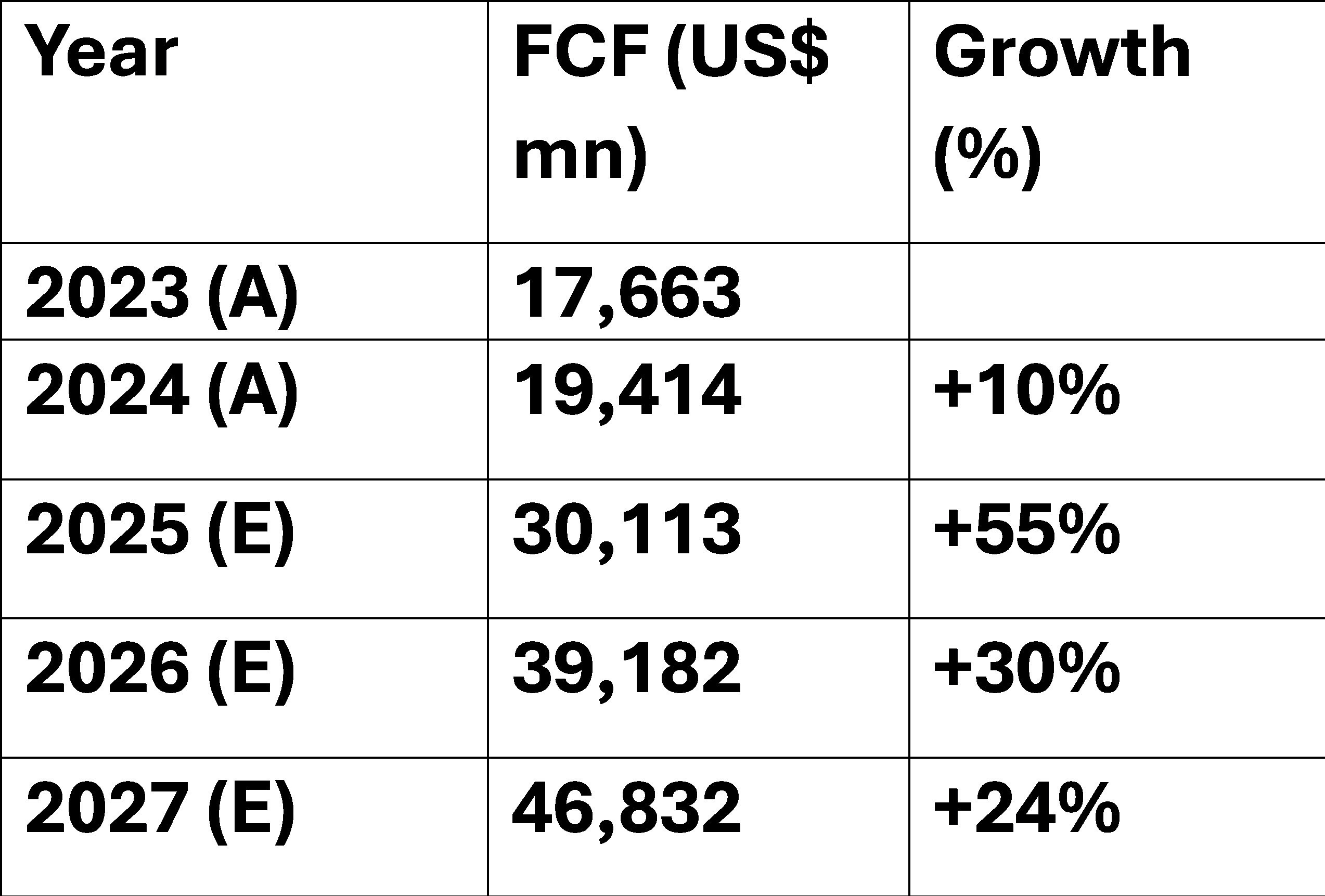

The analysts’ consensus forecasts for Free Cash Flow (FCF) are as follows:

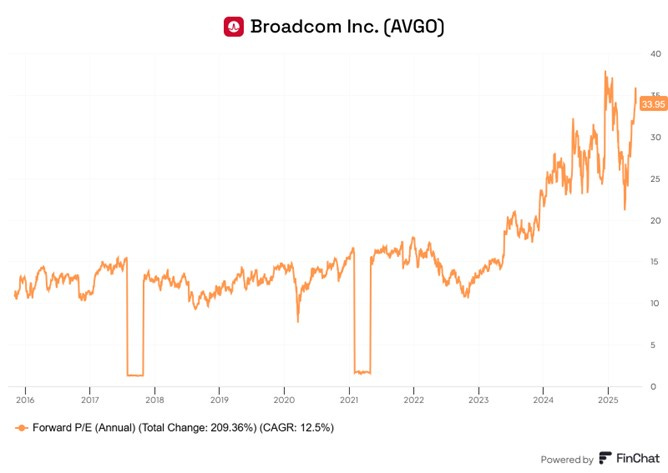

At the current price of 246.9, AVGO is trading at a two-year forward P/E Ratio of 30X.

At the current market cap of $1,160bn, AVGO is trading at a two- year forward Price to Free Cash Flow Ratio of 29.6X.

These numbers imply a two-year forward Earnings yield of about 3.3% and a Free Cash Flow Yield of 3.4%.

These suggest the stock is somewhat over valued given the fundamentals noted above.

The forward P/E and P/FCF charts above suggest the stock is much more valued than it has been in the recent past.

We conducted a Discounted Cash Flow (DCF) Calculation to double check on this.

We use the prior revenue assumptions noted above.

We made the following additional assumptions.

We assumed FY 29 revenue growth at 12%. This is assuming a further slowdown in the terminal year.

We assume EBIT margin will fall to 55% in FY 2028.

The risk-free rate is currently of 4.41% and the Market Risk premium of 4.3%

The Stock Beta is a high 1.1. The Weighted Average Cost of Capital (WACC) for Nvidia is 9.7%.

Finally, we assume that in FY 2029, the terminal exit multiple for EV/FCF is 33X. The current EV/FCF ratio is about 52X.

With these assumptions, we calculated a theoretical Broadcom stock value of $208 per share – the current share prices of $246.9 is at a 15.5% premium.

If the terminal exit multiple for EV/FCF is increased to an aggressive 38X, we get a theoretical fair value equal to the current share price.

Conclusion

The calculations above indicate the stock is overvalued at the current share price. Our best guess is that the stock should earn a minimum average return of 8.5%-9.5 % CAGR over the next five years. This it too low.

We currently have 1.5% position in Broadcom. We will not add to it bit will keep an eye on the stock. We would look to buy if it fell back to the $175 to $185 range.

Annexe 1: The Tomahawk6 Switch Series

In June 2025, Broadcom announced they were

shipping the Tomahawk® 6 switch series, delivering the world’s first 102.4 Terabits/sec of switching capacity in a single chip – double the bandwidth of any Ethernet switch currently available on the market.

With unprecedented scale, energy efficiency, and AI-optimized features, Tomahawk 6 is built to power the next generation of scale-up and scale-out AI networks, delivering unmatched flexibility with support for 100G/200G SerDes and co-packaged optics (CPO).

It offers the industry’s most comprehensive set of AI routing features and interconnect options, designed to meet the demands of AI clusters with more than one million XPUs.

“It marks a turning point in AI infrastructure design, combining the highest bandwidth, power efficiency, and adaptive routing features for scale-up and scale-out networks into one platform. Demand from customers and partners has been unprecedented. Tomahawk 6 is poised to make a rapid and dramatic impact on the deployment of large AI clusters.”

“AI clusters are scaling from tens to thousands of accelerators, turning the network into a critical bottleneck while expected to deliver unprecedented bandwidth and latency,” said Kunjan Sobhani, lead semiconductor analyst, Bloomberg Intelligence.

“By breaking the 100Tbps barrier and unifying scale-up and scale-out Ethernet, Broadcom’s Tomahawk 6 gives hyperscalers an open, standards-based fabric—free of proprietary lock-in—and a clear, flexible path to the next wave of AI infrastructure.”

For more information please see:

[1] Net Property and Plant is just 2% of total assets.

[2] VMware Cloud Foundation - private cloud software platform that allows organizations to build, manage, and extend their private cloud infrastructures across various environments, including on-premises, public clouds, and edge datacentres. It's designed to simplify and automate the deployment and management of cloud infrastructure, offering consistent operations and management across different locations.

[3] Serviceable Aggregate market

[4] Which is conservative from an accounting point of view