Copart Inc (CPRT)

Why did Warren Buffett never invest in Copart?

I recently wrote a note on one of my favourite long term investments, Copart Inc. (CPRT). It can be found here.

Copart is the car salvage business and grew from a single location yard company in 1982 to a business to controlling over 55% of the US market. This remarkable growth was achieved by a policy of controlled but focused organic and inorganic growth.

Copart has a number of strengths.

The company has built up a strong ever-widening economic moat through the strategic ownership of land needed for scrapyards to store the salvaged cars.

It has national contracts with large insurance companies who account for the bulk of the supply of salvaged cars.

The founder was the CEO for decades and remains on the Board as Chairman. He established a strong business and shareholder friendly culture. He was succeeded as CEO by his son in law who started in the business at the age of 19. Both men have substantial stakes in the business (worth over US$ 1bn each today) and so have “skin in the game.”

The company has been profitable, free cash flow positive and has earned a high return on capital for decades.

The company has generally followed a clear, rational capital allocation policy. It has expanded through inorganic and organic means. It has issued shares when prospective returns were attractive and bought back shares when they were trading at attractive levels. More recently, it has used its cash to redeem or buy back its debt and build up a fortress balance sheet.

The company performs an essential service; cars at the end of their lives have to be disposed off. It is like a utility but it is not regulated. Now, that should spark our interest for an unregulated utility should a very promising place to look for investment. It is like Warren Buffett’s theoretical investor who owns the toll bridge which is the only way to get out of town.

The more I looked at Copart, the more I came to feel that it is an deal Buffett Investment. As I far as I know, Buffett never invested in it. It is not a big deal - errors of omission are inevitable in investing and are much less harmful than errors of commission.

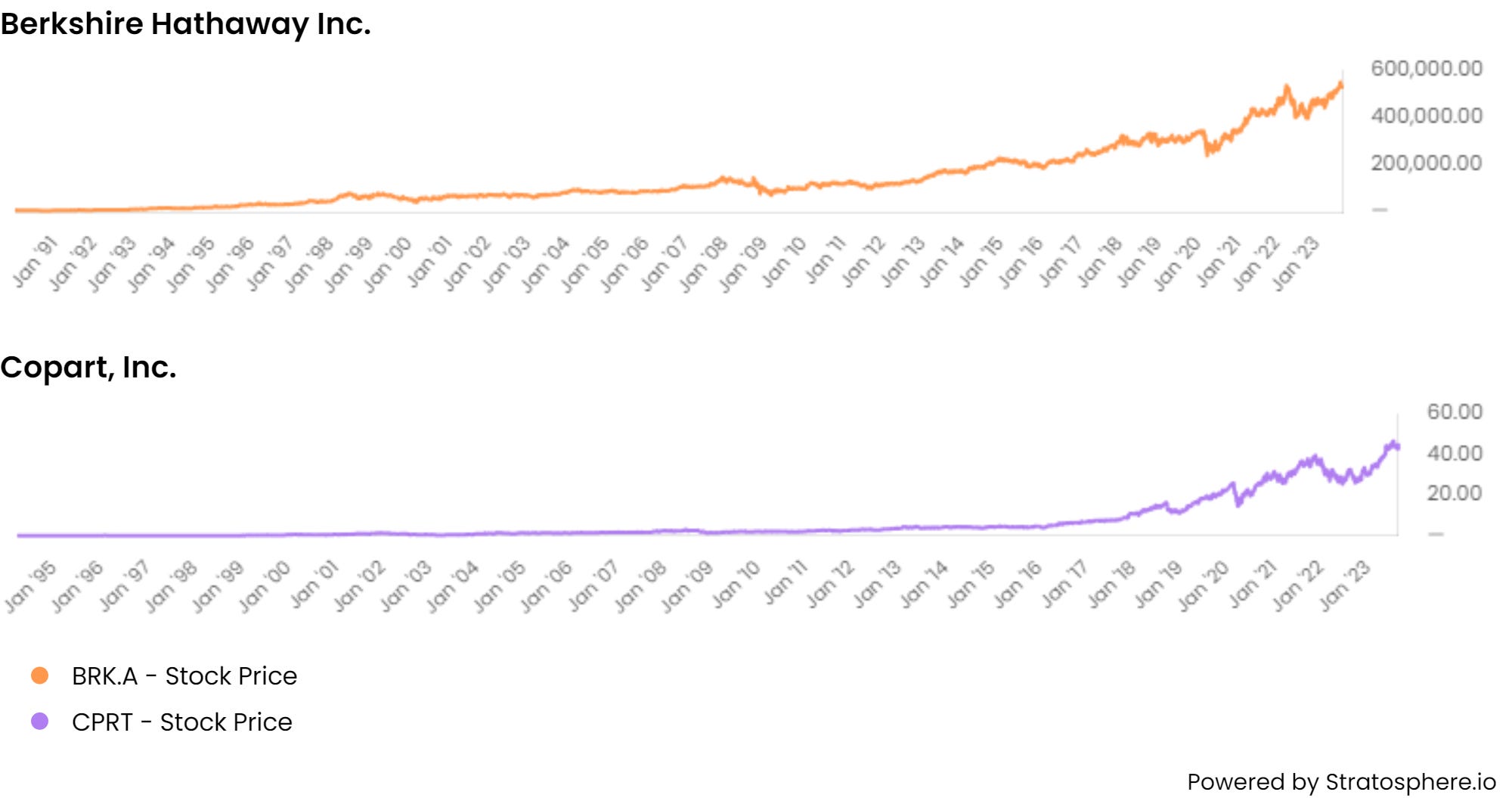

Financially it would have been a very wise move for him. As the Charts below indicate, Copart has significantly out-performed Berkshire Hathaway.

Source: Stratosphere.Io

In the last thirty years, Copart has given a CAGR return of 21.1% (a 286X return) compared with a CAGR of 12.5% (a 32X return) for Berkshire Hathaway. This, of course, is completely with the benefit of hindsight.

Copart would definitely have been within Buffett’s Circle of Competence.

Perhaps Buffett was worried about the high level of capital expenditure which reduced free cash flow. He was probably looking for See’s candies type investments that would generate huge amounts of cash.

See’s Candies delivered over $2 billion in pretax income to Berkshire Hathaway since 1972. This works out to an average of about $66 million per year, not bad for a company bought for US$ 25mn in 1972. See’s sent a lot of cash to Omaha over the years. This was used by Buffett to buy new companies in their entirety and/or positions in marketable securities.

Starting in 2006, Berkshire Hathaway invested heavily in capital-intensive sectors such Railroads and Electric Utilities. At that time, Copart would also have been a very worthy candidate for investment.

One possible reason is the fact that GEICO, the nation’s second or third largest auto insurer was, and remains, a major customer of Copart. A major investment by Buffet in Copart might have been interpreted as a result of information gained as a result of normal commercial relations and that would perhaps have made Buffett wary. He never invested in Microsoft as Bill Gates is a friend and was a member of the Berkshire Board. He would not want to risk being perceived to be investing due to information that is not in the public domain. However, both investments could easily have been made as discrete arms-length transactions.

Perhaps for Warren Buffett, Copart was just one that got away.