Copart Inc. (CPRT)

We wrote a quite detailed piece on Copart on 23 August 2023, and this can be found here. The note contains a detailed explanation of the company’s history and business model and in our biased view, it is worth reading if you do not know the company.

We also did a follow up piece on 19th September 2023 after the release of quarterly results which can be found here.

We revisit the company now after it released the most recent quarterly results last week.

The company is the leading player in the disposal of written-off cars in the USA which accounts for 80% of its revenue.

Copart operates a robust online salvage vehicle auction platform, connecting sellers with over 750,000 potential buyers globally.

The company facilitates more than 3.5 million vehicle transactions annually. The majority of Copart's vehicles come from auto insurance companies. Copart's services extend beyond auctions, offering transportation, storage, title transfer, and salvage value estimation, primarily on a consignment basis.

It has a dominant share in the US market. In recent years, it has expanded outside the US and is active in several countries. The overseas markets are growing faster but are much less profitable than the US business.

A summary of the quarterly results is shown in the tables below:

Revenue and Net Income Growth

Q2 revenue was $ 1020mn and grew 6.6% y/y but was flat q/q.

Net Profit was $ 325.6mn and grew 10.9% y/y but fell 2.1% q/q.

EPS was 0.33 cents 10% higher both q/q and y/y.

Revenue growth of 6.6% led to EPS growth of 10%; the business model continues to have operating leverage.

The chart and table above show that revenue growth has slowed compared with recent years.

Margins generally maintained their high levels. There is no sign of any pressures on margins despite the slower rate of growth of sales.

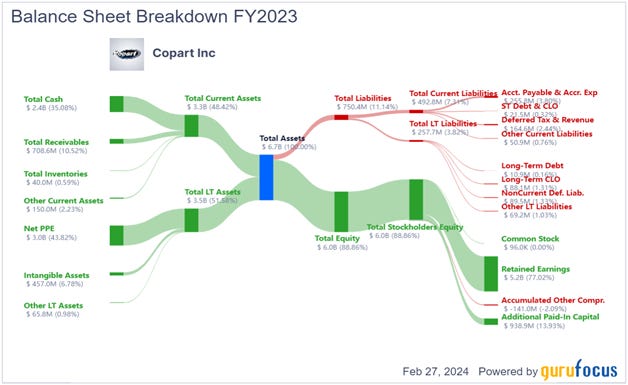

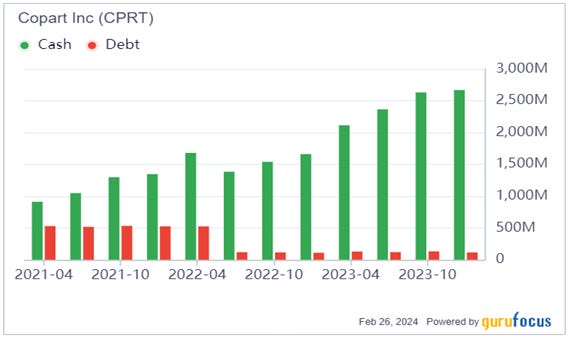

Balance Sheet

The company has always run with a very strong balance sheet. Evidence of this can be seen in the two charts below:

Current assets are 48% of total assets. Of this, cash accounted for 35%, or $ 2.4bn, at the end of FY 2023. Long term (non-equity) liabilities were just US$ 257mn of which long-term debt was just $10mn.

The stock rose 63 % in 2023 but has been flat in the last three months. This was perhaps in anticipation of the slow quarter they just reported. This subdued performance in the last quarter is understandable given market sentiment was dominated by AI and technology and the S&P 500 performance was driven by the Magnificent 7 stocks.

Highlights of the earnings conference call.

The supply of written off cars is drive by used car prices and repair costs.

If used car prices fall and/or repair costs rise, there will tend to be a rise in the supply of written off cars that are put up for auction for Copart and its competitors.

“New and used vehicle prices have decreased somewhat steeply in the past few quarters while repair costs continue to increase. Those factors have driven a strong and continued recovery in total loss frequency (tlf)”

Tlf is the percentage of cars involved in accidents which are written off.

· We noted a 7% year-over-year decline in the Manheim Used Vehicle Value Index.

· At the same time accident severity as measured in cost of repair increased 1.7%.

· According to CCC, total loss frequency for the fourth calendar quarter of 2023 was 20.9% across all loss categories.

A fall in used car prices will tend to increase the supply of written-off cars which come to auction. However, this increased supply tends to put downward pressures on the selling prices that can be achieved at auction. Copart’s revenue model is broadly a percentage of the auction average selling prices (asp).

However, Copart reported that their auction selling prices did not fall as much as used car prices.

“Despite the decrease of 7% in the Manheim Used Vehicle Value Index, our U.S. insurance selling prices by comparison have remained flat year-over-year, a reflection of our auction liquidity and buyer activity.”

“As always, we continue to believe that long-run trends continue to make repairing vehicles less economically attractive to insurance carriers and totalling vehicles more economically attractive to them at the same time.”

The slower growth in revenue largely reflects the fact previous two years were affected by devastating hurricanes, particularly Hurricane Ian (Category 5 in 2022) and Hurricane Ida (Category 4 in 2021). 2023 was a relatively calm hurricane season.

“Our nominal U.S. insurance volumes increased just 0.3% year-over-year, so largely again due to the effect of the sell-through of units from Hurricane Ian a year ago.”

“While we responded to multiple smaller weather events this year, they did not in the aggregate approach the magnitude of Hurricane Ian. Normalized for Ian's impact, we estimate our U.S. insurance volume to increase 9.2% for the period, a reflection again of total loss trends and market share growth.”

The company is the largest player in the US insurance segment. It is the dominant player in an oligopoly with IAA and therefore there is little scope for winning market share in the USA. The company has in recent years diversified in three principal ways.

Boosting non-insurance sources for cars. From car dealers, banks and hire fleets. This business division is called Blue Car.

The company has acquired two companies operating auction marketplace in goods such as farm machinery and heavy equipment (Purple Wave Auctions) and high-performance motorbikes, all-terrain vehicles and snowmobiles (National Powersport Auctions (NPA)).

The company has expanded abroad and is investing. It is still early days.

The overseas expansion to new countries has been slow and steady:

Canada in 2003

UK in 2007, 2008

UAE, Brazil, Germany, Spain in 2013

Bahrain, Oman in 2015

Ireland, India in 2016

Finland in 2018

The conference call had updates on the three diversification aspects:

Non-insurance US business

“First, we continue to grow our Blue Car business which serves our bank and finance fleet and rental partners. In the second fiscal quarter of 2024… we observed year-over-year growth of north of 30%.”

“All told our U.S. non-insurance automotive volume, excluding low value and wholesale units increased north of 30% year-over-year.”

Non-insurance US business is growing much faster than average, but it is at a low base and remains relatively small compared with the core US insurance business.

Overseas business.

“We saw unit growth of over 21% with fee units increasing 22% and purchased units increasing by over 19%. Our international business ended the quarter with inventory levels over 16% ahead of prior year. So much higher growth internationally.”

“Our U.S. Service revenue grew by over 7% and international service revenue grew by nearly 26% for the quarter.”

“In the U.S., our gross profit margin increased to 50.2% and our international gross profit margin increased to 24.9.”

The company continues to invest in the business for the long term.

“In addition, we invested about $123mn (in Q2) in capital expenditures, with nearly all of this amount attributable to our real estate and physical infrastructure to support capacity expansion, which contributes to our ability to serve our customers while simultaneously reducing our transportation costs and corresponding fuel consumption”.

“Our top priority is to invest to grow our core business. To achieve this, over the last 12 months, we have deployed over $540 million into our real estate portfolio, fleet, and technology to provide best-in-class products and services to our customers.”

“We are growing our capabilities. So, the bringing on of new senior talent and the expansion of our offering in the whole car universe and frankly, our sophistication in the insurance world as well. Those all require new capabilities, and we are delighted to invest in them. So that reflects some of the G&A growth over time.”

“I would say everything else we're focused on is really to drive incremental operating leverage in the future.”

For the reasons we outlined in original note, Copart has a great long-term performer due to its significant strengths. We highlighted two of these in our original note: Network Effects and Economic Moat.

We reproduce the points on these below:

Network Effects

This auction house has a very powerful network effect which has helped Copart and IAA grow stronger. Sellers like to participate in auctions because the buyers are there. On the other hand, buyers go to the market because the sellers are there. In most markets such as stock exchanges the same logic applies. Most countries only have one or two stock exchanges. Attempts to introduce a third stock exchange almost always fail. Liquidity begets liquidity.

This self-reinforcing dynamic develops over years, but it is cumulative as existing players capture an increasing share of the market over time. It would be very difficult for a newcomer to break into the Salvage market due to the Economic Moat the existing players have created.

Our growth is the result of our commitment to customer service and our auction liquidity. With each additional vehicle we earn the right to sell, we increase the attractiveness of our auction platform to the world's automotive buyers, drawing still more buyers to our auctions to the benefit of all of our sellers, new and old.

Economic Moat

Salvage yards are large, unsightly, dirty, industrial units that nobody wants in their neighbourhood. It can take a long time (and a lot of money) to build a new yard. In smaller cities that can’t support more than one yard, or larger cities that don’t want another one, it can lead to a local monopoly.

In our note, we wondered whether Copart was an unregulated monopoly. Such an institution can earn above average profits over a long period but might attract regulatory attention.

Willis Johnson, Copart’s founder, described the company as “a sewer system”. Insurance companies need to write policies for cars and looking to minimise losses after each accident. Auto manufacturers need insurance companies to insure their vehicles. There just needs to be someone to get rid of the waste.

“We’re a utility. Nothing can get rid of us – nothing. Two of the biggest businesses in the world are car manufacturers and insurance companies,” I went on. ” If insurance companies don’t write insurance policies on cars, then they’re out of business. If manufacturers don’t make cars, then they’re out of business. They’re always going to make cars and they’re always going to insure them. We’re the guys in between.

As long as we’ve got the land in the right place to put the cars on, we can’t fail. We are like the septic tanks of the sewer system. You can’t have the system without us.”

From Junk to Gold – the biography of Willis Johnson

Summary

These were a good set of results.

Revenue growth was slower in 2023 as the previous year’s volumes were boosted by a severe hurricane season.

Net Profit growth and EPS growth was faster than revenue growth.

Profit Margins are stable.

Valuation and Conclusion

The stock now trades at a multiple of 32X two-year forward earnings. Given prospective high single digit growth in revenue and low double dight growth in net profit and ROE of about 22%, the stock does seem to be fully valued.

US core insurance growth may not grow but the non-insurance and overseas businesses hold out the promise of much higher growth in the future.

Currently, the company is in an investment phase in these new business segments and the new businesses are still too small, but they should contribute meaningful growth in the long run.

We will continue to hold the stock.