Costco Wholesale (COST)

Q3 2025 Results

We wrote our first note on Costco Wholesale in June 2024. It was a comprehensive “Initiating Coverage” type note and can be found here. Our most recent two reports can be found here and here.

We look again at the company in the light of the Q3 numbers released on 28th May 2025.

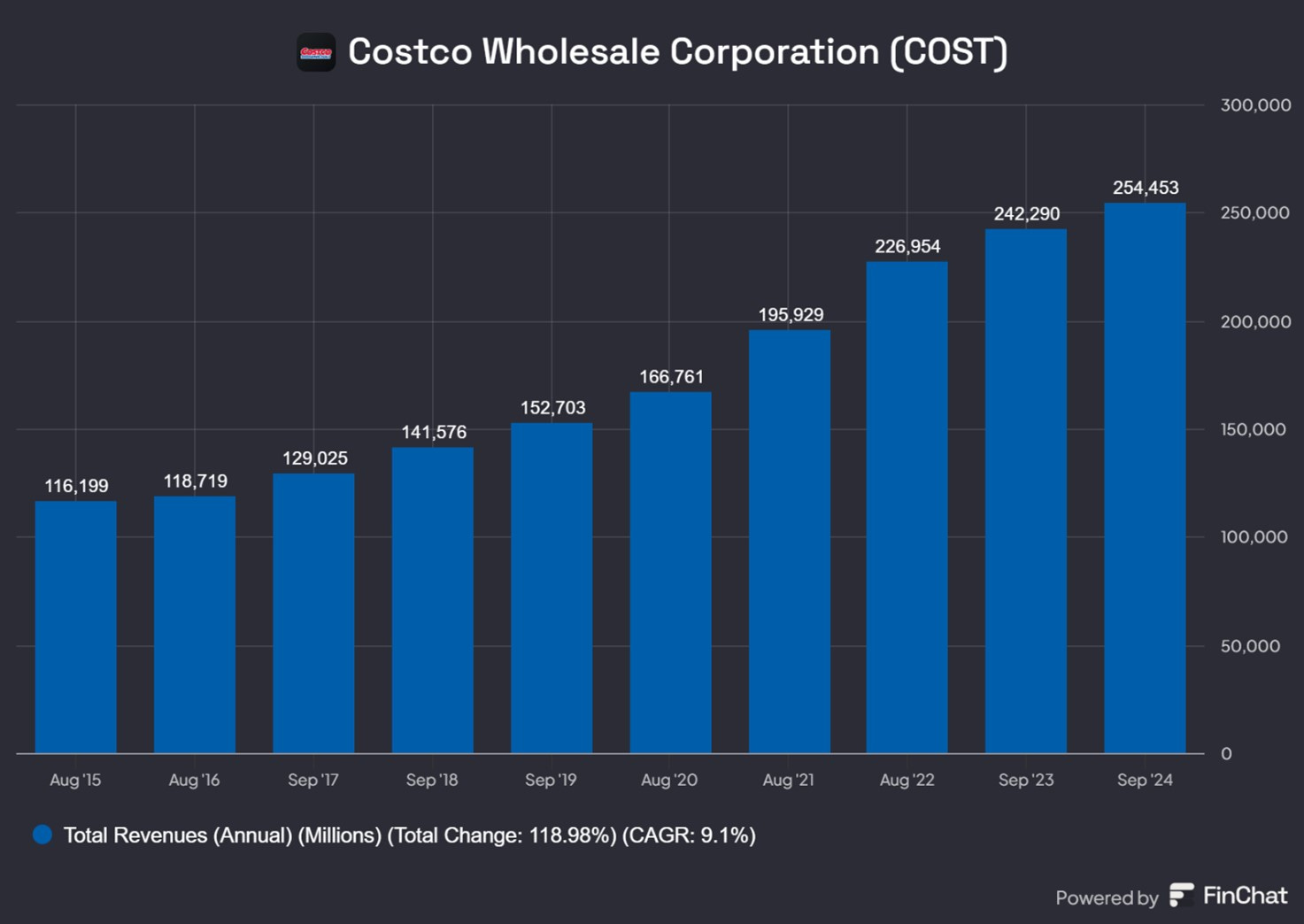

In the last decade sales have grown at a CAGR of 9%. This can be decomposed into same store sales and comparable sales.

The total number of stores have grown at a CAGR of about 2.64%.

Total comparable sales growth has been a CAGR of 6.13%.

The decomposition is thus: (1.0264) * (1.0613) = 1.0893

Costco is like a very large well-oiled predictable oil tanker. It is the second largest retailer behind Walmart but has a very different business model.

Walmart wants everybody as a customer. Costco is a membership club.

Costco has far fewer SKUs and uses the higher volume per item to push aggressively for discounts for suppliers.

Costco has lower Gross margins (13% vs 25%) but much lower operating margins.

Costco deliberately keeps Gross Margins capped a 12% to 13%. Any cost savings which would increase this are passed to customers in the form of lower prices so margins remain at, or below, 13%.

Operating Margins are usually capped at 9%

This means Net Margins are always between 3%-4%.

We can call this the 12/9/3 model where the three numbers are Gross Margins, SGA Percentage and Operating Margins.

For Walmart, the equivalent numbers are 24/20/4 (as shown below).

The reasons for the very different cost structures were discussed in our initial June 2024 report. Interested readers should look at that for the details. The quarterly results were very much in line with this long-standing model.

Sales increased 8.0% for the quarter to $63.2bn.

Net income for the quarter was $1.90 billion ($4.28 per diluted share), up 13.2.%.

Membership Income was $1.24bn or 65% of Net Profit.

Comparable sales increased 5.7% for the quarter.

E-commerce sales increased 14.8% for the quarter and 16.4% for the first 36 weeks.

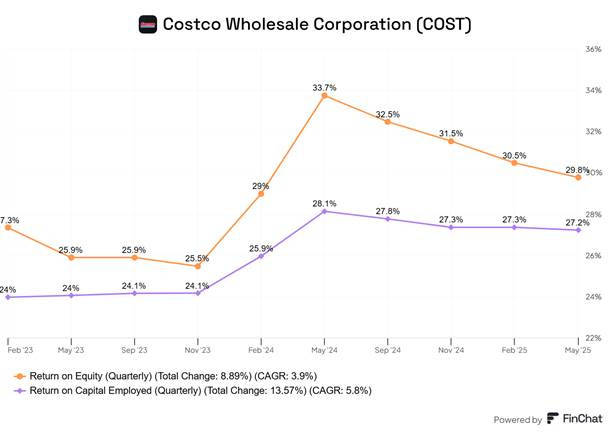

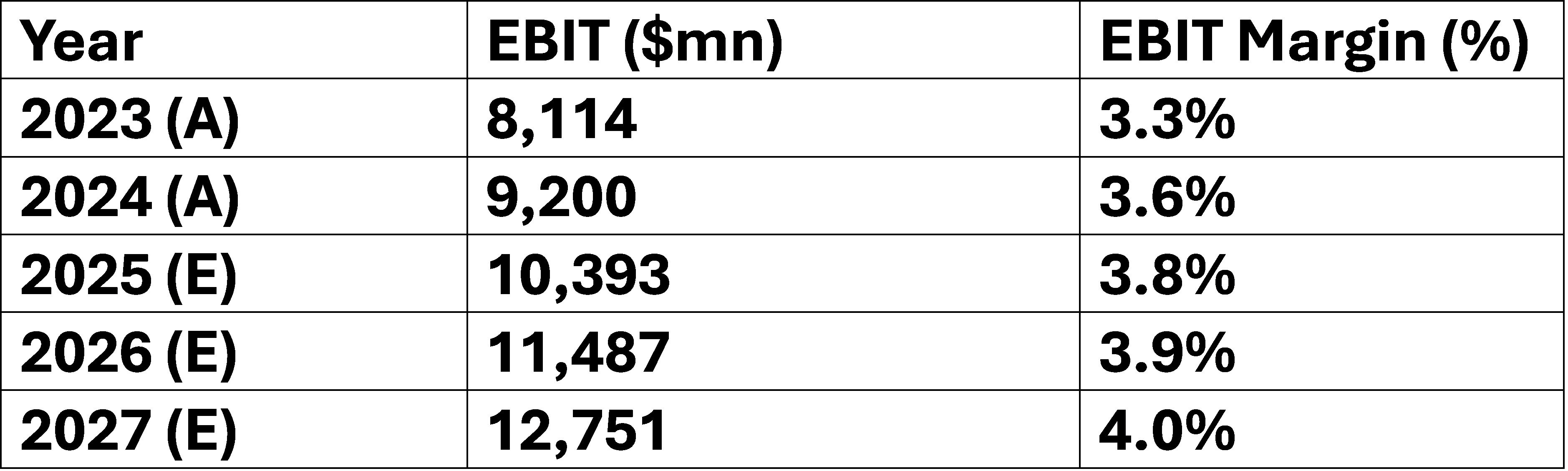

Gross margins of 13% and EBIT Margins of 4% are consistent with the 13/9/4 model. The remarkable thing is keeping margins low has not affected profits and profitability. Over four decades, passing on the savings to customers, has boosted sales growth, profitability and profits.

Profitability as measured by ROE and ROCE is in the range 27% to 29%. In the last 23 years, Costco has given stock investors a CAGR return of 17.5%, well above the likely cost of capital.

Highlights from the Q3 2025 Earnings Conference Call

They continue to open new stores at a steady pace.

We plan to open another 10 warehouses during the fourth fiscal quarter, which will include our 2nd warehouse in Sweden, our 20th warehouse in Korea and our 110th warehouse in Canada.

For this fiscal year, we expect to open 27 new warehouses, including three relocations for a total of 24 net new buildings. This is an increase of 2.65% - in line with the historical average noted above.

They used an expansion on the opening hours of the gas stations to boost sales.

The combination of expanded gas station hours, new gas station openings and lower prices at the pump have led us to having two of our all-time highest gallon weeks in the U. S. during the last month.

Tariffs

The proposed tariff on imports proposed and implemented by the US government will clearly be a big challenge to all retailers. Walmart had already announced on May 14th that the high level of tariffs means they will have to raise prices.

Costco is trying hard not to raise prices, as their whole business model is based on offering lower prices to build volumes. They will try to mitigate the impact of tariffs. For example, making greater efforts to source products from the countries or regions where the items are sold. They use their financial strength to buy forward items, ahead of the imposition or the re-imposition of high reciprocal tariffs. However, this is likely to lead to higher inventory and higher costs.

We continue to move more product sourcing into the countries or regions where the items are sold. And this is helping us to lower costs and mitigate some of the potential impacts of tariffs. We're remaining agile as the situation with tariffs evolves, while also supporting the commitments we've made with our long-term suppliers.

As an example of this, during the third quarter, we re-routed many goods sourced from countries with large tariff exposure to our non-U. S. Markets.

In the U. S, we pulled forward some items that we had planned for the summer and sourced additional locally produced goods to reduce tariff impacts and ensure that we were in stock.

Our buyers were very proactive, and they pulled a lot forward, a lot of our summer goods, most of our patio program, our sporting goods program got in early this year, got it in ahead of the tariff impacts.

In the U. S, we are sourcing more American-made goods where available, including items such as mattresses, pillows and plastic resin goods. New KS (Kirkland Signature) offerings are another way we are delivering more value to members. These items typically offer members 15% to 20% value compared to the national brand alternative with equal or better quality.

A notable example in the quarter was our Kirkland Signature Ultra Clean laundry products. These SKUs are now sourced in Asia for our APAC warehouses, allowing us to significantly lower transportation costs and reduce member prices in the region by approximately 40%.

Actions such as these are allowing us to continue to provide great values for our members, while also delivering value to our shareholders.

As we look ahead to the remainder of the fiscal year, while the impacts of tariffs and the outlook for the economy in general remain unknown, we are confident in the ability of our operators and merchants to rise to the challenges and continue to offer great service and find consistent values for our members.

However, despite these efforts in some cases there are price increases due to the tariffs.

In non-foods, we saw low single-digit inflation return for the first time in several quarters. This was driven primarily by imported items.

As a reminder, about a third of our sales in the U. S. are imported and about two thirds of those sales are in non-foods.

Items imported from China represent about 8% of total U. S. Sales. The inflation experienced in non-foods was the primary driver of the $130m LIFO[1] charge for the quarter.

Any change in the level of inflation in the fourth quarter could increase or decrease the size of that charge. As we navigate an evolving environment with tariffs, we are working closely with our suppliers to find ways to mitigate the impact on cost, including moving production and sourcing to other countries where it makes sense to do so.

At Costco, we remain committed to providing quality items at the lowest possible prices and raising prices is always seen as a last resort.

The evolving landscape with tariffs is adding complexity and challenges for how we operate our business, but we believe our expertise in buying and limited SKU count model give us greater agility to navigate the environment and ultimately increase our member values compared to the market.

They have partnered with BNPL firm, Affirm

Affirm is finance company that allows people to buy now but pay later (BNPL).

A recent example in e commerce is the launch of buy now pay later offering through our partnership with Affirm. This new program allows our members greater access to the Costco values on big ticket items such as appliances, furniture, consumer electronics and much more at exclusive rates for the Costco members. While still early days, we've been pleased with the initial sales results.

Resilience of Business

Costco claims they have historically done well during periods of uncertainty due, in part, to their own-label brand, Kirkland Signature (KS).

In times of the consumer uncertainty, our Kirkland Signature brand is uniquely positioned to provide our members with great quality and great values. And during the third quarter, sales of Kirkland Signature (KS) items again outpaced our overall sales growth with our KS sales penetration up approximately 50 basis points year over year.

Membership Fee

The membership fee is a key part of the business model. Only members can shop at Costco. The membership fee is an almost 100% margin revenue item. The company has to grow memberships, especially the more expensive Executive Membership. The latter has 2% cashback up to a high limit and encourages high volume of shopping.

In addition, Costco need to ensure that Membership renewals are high and above 90% in line with historical trends. They are keen to emphasise the high value represented by the membership fee, but they do raise the fee every five or six years. In 2024, they raised the Membership Fee for the first time in seven years.

We reported membership fee income of $1.24bn, an increase of $117m or 10.4% (y/y). Membership fee income growth was 11.4%: the recent membership fee increase represented approximately 4.6% of fee income in the quarter. In terms of renewal rates at Q3 end, our U.S. and Canada renewal rate was 92.7% and the worldwide rate came in at 90.2%.

As cohorts of new members from digital acquisition campaigns and warehouse openings in Asia move in and out of the calculation, there will continue to be some volatility in this number quarter to quarter. The decreases in the renewal rates in Q3 versus Q2 were primarily attributable to sign-ups from a Groupon promotion in the fall of 2023 entering the renewal rate calculation for the first time this quarter. Higher penetration of online sign ups entering the renewal rate calculation also contributes to the lower renewal rate.

We ended Q3 with 79.6mn paid household members, up 6.8% versus last year and 142.8mn cardholders, up 6.6% (y/y).

At Q3 end, we had 37.6mn paid executive memberships, up 9% versus last year. Executive members represented 47.3% of paid members and 73.1% of worldwide sales.

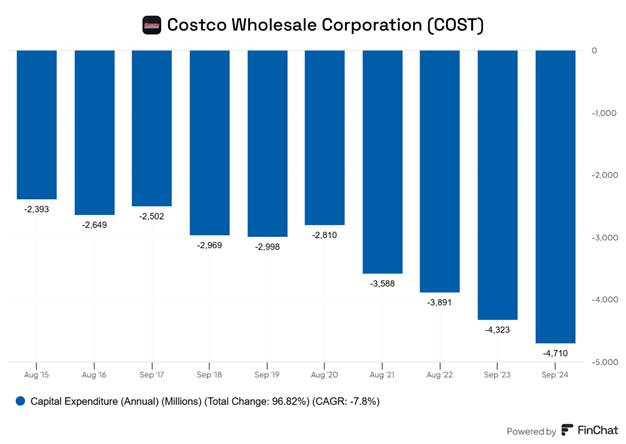

Capital expenditure in Q3 was approximately $1.13bn and we estimate CapEx for the full year will be a little over $5bn.

As the Chart below shows this will be an increase on the previous year.

Capex is shown as a negative bar in the chart above as it a cash outflow. In the last decade, capex has grown at a CAGR of 7.8% which is a little below or in line with total revenues. This indicates that Costco is not getting more capital intensive. This is confirmed by the data for Capital Intensity shown below:

The impact of tariffs has been offset by declines in the prices of a few key commodities.

we're dealing with the moving tariff scenes as things continue to change each day. We have been very fortunate with some of the key commodities coming down and then our buyers are immediately the first ones down in those goods. So we take every advantage of every opportunity that we can lower prices. And we've seen our competitive landscape improve slightly at the latter part of the quarter, which is very good for us.

But we're going to continue to invest in price. It's what we do. It's how we grow our business. And we're going to continue to try and mitigate as much of this impact on tariffs as we can for our members.

we're watching pricing daily and if not hourly on every key commodity. And you have commodities like butter and eggs come down, there's quite a halo effect to many different items.

They watch the declines in prices and where appropriate push suppliers to reduce prices.

our buyers are on top of that talking to all the suppliers that would benefit from those reductions in cost and trying to really move that those products into lower cost as soon as we can. It's about lowering the prices as soon as we can.

One of the issues they are considering is as membership grows in a particular location, the club gets so busy and it's difficult to find parking.It becomes more difficult to navigate through the store, and it takes a little longer to get in and out. This reduces the quality of the membership experience. The management was asked what they are doing about this. They are aware of the issue of these high-volume stores (defined as those with sales of more than $400mn; there are 40 such locations) and are tackling it by opening new nearby stores, increasing opening hours and using technology.

it is a strategic priority for all of us in the company right now is that continue to how we improve the member experience in our high-volume warehouses.

As we speak about the fourth quarter openings, about 80% of those warehouses we're opening are going to cannibalize high volume locations for us. That's going to take some relief off. So we strategically look at new markets for openings, but with the real importance on strategically cannibalizing those warehouses where we can make that improvement of member experience in there as well. The recent expansion of gasoline hours was a great indicator that the throughput for our members improved nicely, and we saw that immediately in gallon increases.

And on the technology front, we've realized with some of these pilots as we are working through these different systems to speed up the front-end experience and get that moving flowing quickly. The backside of that is it turns over parking spaces quicker. And when you turn over parking spaces quicker, it makes the whole experience better.

So we are very mindful of the high-volume warehouses we have and we're strategically working on many different fronts to how do we continue to grow the volume in those existing buildings and continue to infill and look for new markets in The U. S.

where we have over $400,000,000 of sales, which is I think what 40 or so warehouses where we're in that sort of category. So they're the highest priority there. I think as we do that, there's still tremendous growth in the less mature warehouses and we see year over year continued growth.

So I think that gives us a lot of confidence that while we make those enhancements that Ron mentioned, we still have significant opportunity with the vast majority of our warehouses to continue to grow and to for them to look into mature like our higher sales warehouses today.

digital really enhances the speed of checkout. And so we are really working hard on the digital membership card usage as well. We've also engaged in some Scan and Go done by Costco kind of tests that we're doing out there that have been extremely successful of moving people through the lines and expediting the transactions. We've seen some very, very early results have been very positive and great adoption from our members seeing that as well.

They are also investing in their distribution network.

it's certainly interesting being relatively new to the company to see how efficiently we operate our depot network. we generally are not really holding inventory in any of the depots. We're moving products straight through.

when we look at our most productive warehouses and highest volume areas, we see incremental leverage that's created in our overall financial model. … continuing to invest capital in places where it makes sense to optimize the network for depots,

We have built out the Costco logistics network and invested in especially on the West side of the country, I would say when we acquired Innivel, there was a strong presence in the East, less presence in the West. And so we built out that network.

Strategic Buying

Because of our limited SKU count and the expertise of our buyers and that long term commitment to our suppliers that we have, we believe there's opportunity for us to continue to widen our value versus the market as we adapt to the changing environment.

a benefit of being a limited SKU count model is we can look at rotating into different items and finding different assortment that makes more sense for the member.

Summary

Costco is like a very large well-oiled predictable oil tanker. It is the second largest US retailer behind Walmart but has a very different business model.

For a long time, their business has grown and proceeded with very predictable and stable rates of growth.

Same store sales grow at 5%-7% per annum

Store growth is about 2.5%% to 3% per annum

Gross Margins and Operating Margins are 13% and 4 % respectively.

Operating Profit growth of about 11% CAGR

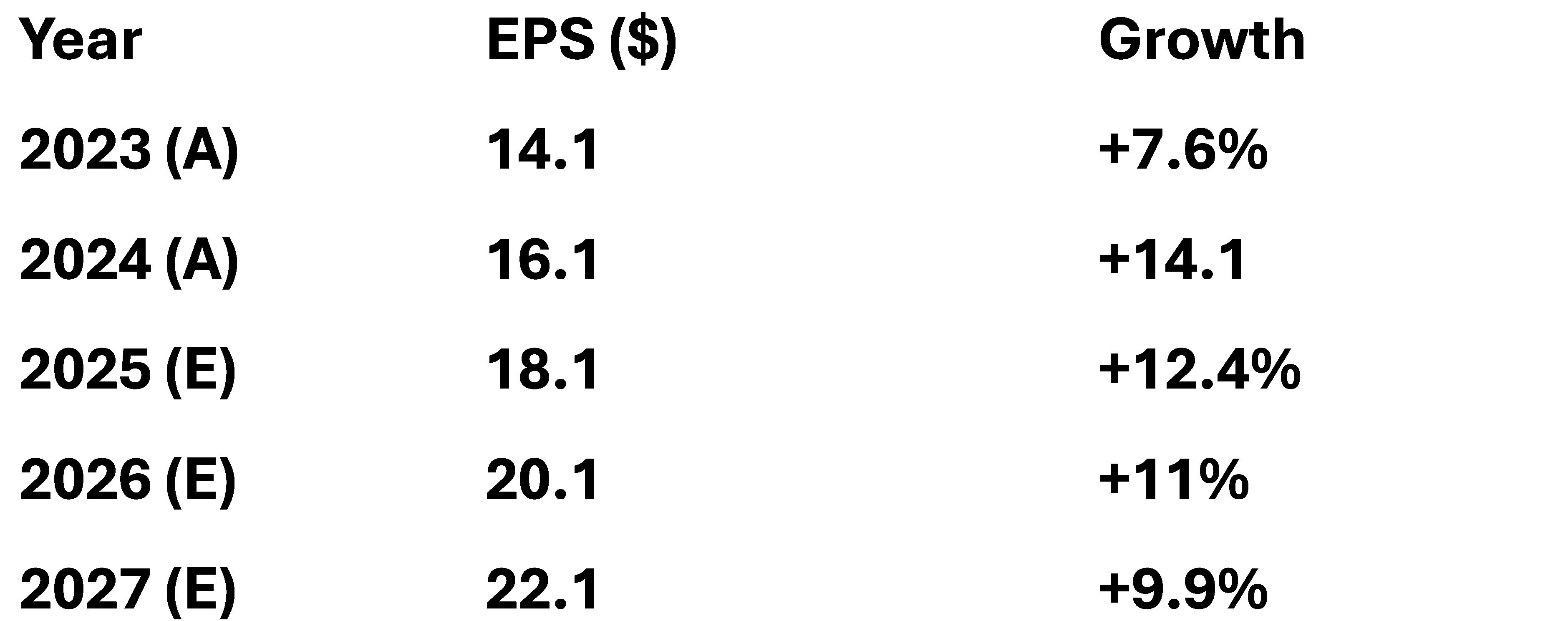

Net Profit and EPS growth of about 11 to 13% CAGR.

Operating cash flow at about 11% to 12% CAGR.

Free Cash Flow growth at 12% -14% CAGR

Profitability ratios have improved steadily

It is a remarkably consistent and steady performance and a tribute to the differentiated and resilient business model and strong management. Generalised tariffs imposed by the US are a big challenge.

Walmart, Target and Dollar General have all indicated they will have to respond to tariffs by raising prices. Costco have said they will try to do everything to avoid raising prices. Time will tell whether they will be able to do this.

Valuation

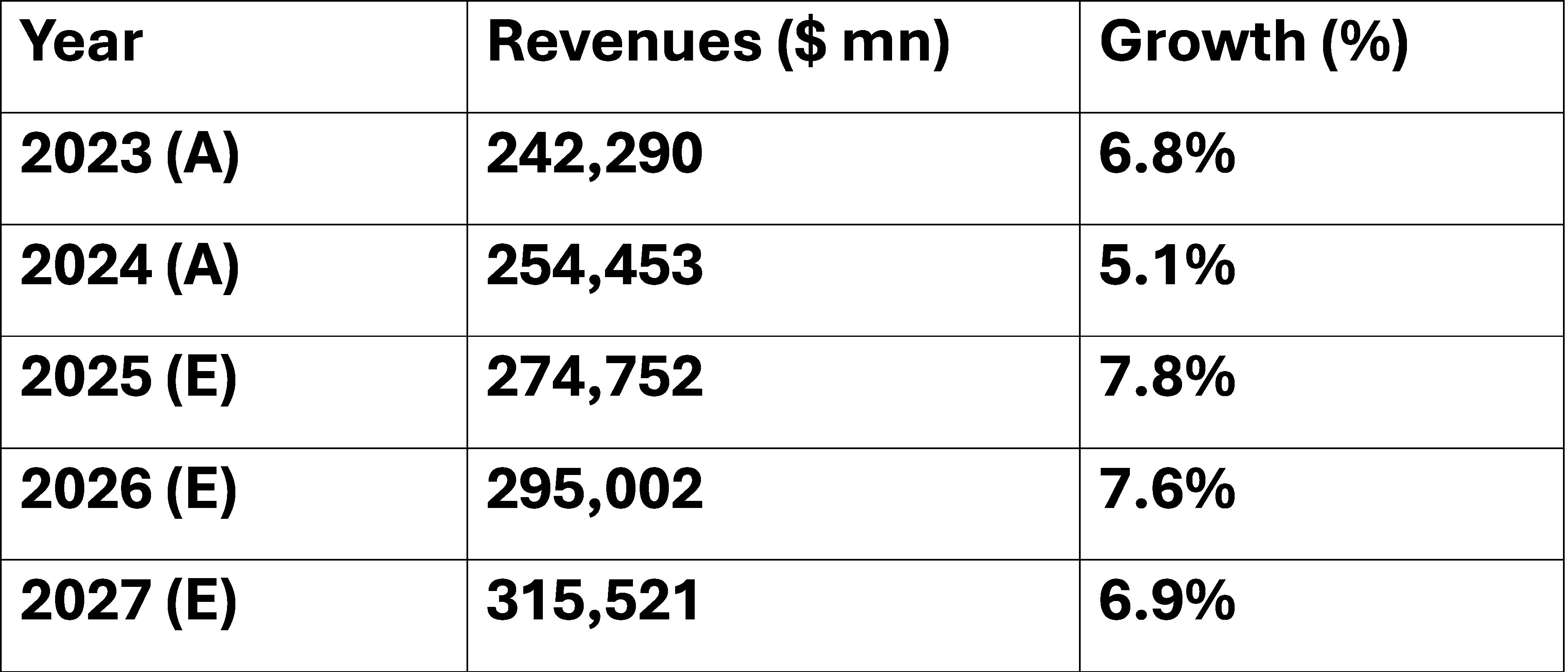

The consensus analysts’ forecasts for revenues are as follows:

The consensus analysts’ forecasts for EBIT and EBIT margins are as follows:

The consensus analysts’ forecasts for EPS are as follows:

The consensus analysts’ forecasts for Free Cash Flow (FCF) are as follows:

Currently Costco’s share price is $1056 per share and the market capitalisation of $486bn. This means it is currently on a two-year forward Price/Earnings Ratio of 52.8X and Price/Free Cash Flow Ratio of 54X.

This implies a two-year forward earnings yield and Free Cash Flow Yield of about 1.9%

On the face of it, these numbers suggests that Costco stock is expensively priced in relation to fundamentals of the company noted above.

As a quick view, the fundamentals indicate the 2 year forward P/E Ratio should be in the range around 33X to 38X.

Cleary the market will give Costco a premium for quality, consistency and predictability. It is hard to say what the premium should be. However, at the current forward P/E multiple of 52.8, our best judgement is that the implied premium is too high.

Conclusion

Costco is a remarkable company with an effective long -term oriented business model and a great management culture.

It has performed well over the years. Over the last 23 years, shareholders have achieved a CAGR return of 17.5% which is well in excess of the estimated cost of capital.

However, the stock is currently trading at a very high valuation. For a buyer at the current level, there is a risk of sub-par returns for the foreseeable future.

Our best forecast is the investor will get a total return of 4% to 6% CAGR over the next 5-8 years. This is too low.

We have a legacy 1% position in the company. We will continue to hold this, but we will not add to the position.

[1] LIFO = Last in First Out method for accounting of inventories. Leads to higher COGS and lower margins due to inflation.