Costco Wholesale (COST)

A unique business model and culture.

“Culture eats Strategy for breakfast” - Peter Drucker

We have held Costco stock for three years. Our interest was sparked after reading it was one of the just three or four stocks that accounted for the bulk of the portfolio of the late Charlie Munger. We did not do too much research at the time, which was an error, but it has worked out well. We look at it now in the light of its most recent results.

Introduction

Costco operates membership warehouses in North America, the United Kingdom, Mexico, Japan, Australia, Spain, Taiwan and Korea.

COST operates 861 warehouses with a huge average size of 147, 000 square feet. They operate on a seven-day, 70-hour week.

591 (68%) stores are in the US, 107 in Canada and 163 in the rest of the world. In terms of ownership, 677 of the stores are owned by the company while 184 are leased.

They have a relatively small range of goods ((4,000 stock-keeping unit (SKU) vs ~140,000 at a Walmart) and generally sell items in bulk.

A large part of their profit (70%) is made from their membership income which, by definition, is almost 100% gross margin - this ensures excellent revenue predictability and enables them to cut prices on their core offering to generate more membership income.

History

To understand the history of Costco you have to look at the lives of two men, Sol Price and Jim Sinegal.

Sol Price (1916-2009)

In 1976, Sol Price founded Price Club. It was a revolutionary concept at the time. It was a membership-based warehouse store aimed at government employees that sold products in bulk at low prices. The business model was driven by the idea that while goods would be offered cost, profits would come from annual membership fees.

This helped to build loyalty with customers who became more regular shoppers, and this generated a steady stream of recurring revenue.

The business had a virtuous circle where the discounts attracted more people to become members, and the membership fees enabled the business to offer more discounts. Member retention rates were exceptionally high and, as new members joined, the business grew rapidly.

Sol Price once said. "We're not in business to sell things. We're in business to make our customers happy, to build a relationship with our customers."

Sam Walton of Walmart in his book Made in America that he "borrowed" "as many ideas from Sol Price as from anybody else in the business."

Jim Sinegal

Jim Sinegal worked for Sol Price and, in response to a journalist who said ‘you must have learnt a lot from him’, Sinegal replied “No, that’s inaccurate, I learned everything from Sol Price… He was the smartest businessman I ever met.”

Sinegal and Price co-founded Costco in 1983, building upon the successes of Price Club.

Jim Sinegal in a Costco Warehouse

Costco was not just about offering products at low prices: it was also about delivering the highest quality products at the best price, which took the concept to a new level.

To achieve this, Sinegal developed a stringent set of standards for the products sold at Costco, requiring suppliers to meet strict quality standards.

Costco developed its own brand, known as Kirkland where Costco sought to offer products of equivalent quality to major brands but at a lower price point.

The range of products is quire extensive (though less than Walmart) and includes food, clothing, home appliances and even, cars. The company expanded into the provision of car fuel at discounted prices for members only.

The format has been a great success and Costco has expanded outside the United States.

Some Jim Sinegal quotes.

"We're in the business of creating loyal customers.”

"The key is to set realistic customer expectations, and then not to just meet them, but to exceed them — preferably in unexpected and helpful ways.

“You could raise the price of, say, a bottle of ketchup to $1.03 instead of $1, and no one would know. Raising prices just 3% per product would add 50% to your pretax income. Why not do it? It’s like heroin: You do a little and you want a little bit more. Raising prices is the easy way.”

Introduction to Costco

Traditional retailing is a game of thin margins and high fixed costs.

The shopping day that follows the Thanksgiving Holiday in November in the USA is called Black Friday. This is because every year, retailers do not break into the black until around that day. Up to that point, they are paying fixed costs and making losses. After that, they hope for a good Christmas season, where they will make the bulk of their profits (if any) for that year.

Costco is different, as its membership fee ensures that it is profitable on day one. On 1st January, Costco can accurately predict the total number of members for the coming year and therefore, the resulting total membership income.

The membership income has ~100% gross margin. The most profitable business imaginable, the proverbial free money. The company offers the highest quality goods at low margins to attract more of the profitable membership fees. This creates the valuable fly-wheel that drives Costco’s success.

The company explains their business model thus

“offering our members low prices on a limited selection of nationally-branded and private-label products in a wide range of categories will produce high sales volumes and rapid inventory turnover.”

“When combined with the operating efficiencies achieved by volume purchasing, efficient distribution and reduced handling of merchandise in no-frills, self-service warehouse facilities, these volumes and turnover enable us to operate profitably at significantly lower gross margins (than most other retailers).”

“We often sell inventory before we are required to pay for it, even while taking advantage of early payment discounts.”

“Our depots receive large shipments from suppliers and quickly ship these goods to warehouses. This process creates freight volume and handling efficiencies, lowering costs associated with traditional multiple-step distribution channels.”

“Floor plans are designed for economy and efficiency in the use of selling space, the handling of merchandise, and the control of inventory. Because shoppers are attracted principally by the quality of merchandise and low prices, our warehouses are not elaborate.”

“By strictly controlling the entrances and exits and using a membership format, we believe our inventory losses (shrinkage) are well below those of typical retail operations.”

If you have visited one of their large, cavernous, windowless high-ceilinged warehouses, you can get a good understanding of their business model. We are occasional visitors to their Watford warehouse which is just north of London UK.

Costco Wholesale, Watford, UK.

We will describe the Warehouse. Costco in Watford sells petrol (Gas in North America) in the forecourt at a very competitive price.

At the entrance is large desk where new members can sign up. You walk in through a narrow entrance (where they check membership ) having picked up one of the giant trollies from outside.

The first area is full of large televisions. I bought one two years ago. This is followed by casual clothing which is piled high in rows and there are no assistants or fitting rooms.

There is a freezer room for fruits and vegetables and special sections for meat and fish. There are all kinds of other items including large bulky items in many rows. They are all stacked on pallets to the (very high) roof.

In every category, the choice is much more limited than a rival supermarket but the prices are very attractive. In some categories the only offering is the in-house Kirkland brand.

You cannot buy one bottle of tomato ketchup or can of baked beans. They are sold in cases of 6 or 12. The whole idea is to buy in bulk to reap savings.

One you have filled your trolley, you line up to pay at the cash tills which are spread out sufficiently to allows customers to navigate the wide trolley through.

Costco Warehouse, Watford . UK

Behind the line of tills is a food court which offers cheap fast food including the largest pizza I have seen. There is also a pharmacy, an optician and (I think) a travel agent and a desk where you can talk to somebody about replacing your car tyres.

The Food Court at Costco showing, among other things, a £1.50 Hotdog and Pepsi. The US equivalent has been priced at $ 1.50 since the mid 1980s.

At the till your membership card is checked. Once you have paid, you walk along a narrow corridor where they advertise large bulky items such as windows, doors, garden sheds and outhouses etc.

A few items you saw on your last visit may no longer be there but there are always new items. This makes the shopping experience something of a Treasure Hunt.

At the narrow exit, staff check your shopping against the receipt. They check for theft including the possibility that a cashier may be known to the customer and not scan all items.

A popular UK newspaper, The Sun, compared prices of a few staples at Costco and other supermarkets plus Amazon.co.uk. This is shown below. Costco is the cheapest in 3 out of 4 categories.

The Membership Programme

The most important aspect of Costco’s business model is the membership programme. An active annual membership is required to shop at Costco warehouses. Members can bring up to two non-members as guests, but only the member is allowed to purchase merchandise.

“The membership format is an integral part of our business and has a significant effect on our profitability. This format is designed to reinforce member loyalty and provide continuing fee revenue. The extent to which we achieve growth in our membership base, increase the penetration of our Executive members, and sustain high renewal rates materially influences our profitability.”

COST provides a money-back guarantee for all memberships but does not provide day passes, trial periods, or other promotions. There is a perception of exclusivity. In theory, membership is reserved for business people and professionals but it relies on self-certification. Membership is not hard to obtain but excludes the casual shopper who just wants a few items and perhaps does not own a car.

Charlie Munger was once asked why membership was maintained, if it excluded people, and resulted in lower revenues. He said it was important because it excluded the small casual buyers, and ~100% of potential shoplifters. A customer who is willing to pay $60 or $120 for a membership is unlikely to steal. Costco’s customer base is skewed toward higher income customers who have discretionary income sufficient to buy in bulk. Customers facing financial problems are unlikely to be willing or able to part with $60 for a membership or to have enough income to purchase bulk quantities of goods. Costco’s shrinkage (theft) is 0.11% of sales compared with ~1.3% for other large retailers.

A Costco member is likely to feel driven to justify the membership fee and will be more likely to choose to shop at Costco rather than other retailers. Renewal rates are more than 90% in North America and slightly less in other countries.

Costco exercises restraint when it comes to increasing membership fees. The last increase was in 2017 when the basic membership rose from $55 to $60 in the United States. Dues increased by $5 in 2006 and 2012, so there has been a pattern of a five dollar increase about every five years.

Costco has strict rules in place when it comes to sharing a membership. However, one free household card is available to any other person over the age of eighteen who lives at the same address as the paying member.

Members are allowed to bring up to two guests during visits to a warehouse. When non-members are exposed to Costco, there is a good chance some of them will eventually become paying members. When a free household card holder moves to a new address, e.g.. as a young adult forms a new household, they may well buy a new membership.

The membership is very good value, Given Costco’s lower gross margins relative to competitors means it would take ~$500 worth of shopping to save the cost of the $60 membership fee.

If we take Costco’s FY 2023 net sales of $242 billion and divide by 75mn paying members, we arrive at an average of $3,200 in spending per member. Members clearly enjoying a compelling value proposition in exchange for the membership fee.

In addition, to the membership fee there are a number of key elements to the Costco Model

• Shopping Frequency. Having cheap petrol, cheap food etc encourages customers to visit often. If you have driven to a store to fill your car tank, you might as well do some shopping. The “treasure hunt” atmosphere also encourages frequent visits.

“One of the most exciting things about shopping in our warehouses is you never know the kind of incredible deals you’ll find from one visit to the next! Costco members know the trick to getting the best value on exclusive or one-time-buy merchandise: Visit often! And, because we rotate out and introduce new merchandise all the time, we encourage you to purchase items that interest you sooner rather than later to avoid missing out.”

• Inventory Management. Costco offers a limited number of stock keeping units (SKUs) (4,000 vs ~140,000 at Walmart) compared with other large retailers. This simplifies the process of sourcing, distributing, and managing inventory. Products are offered in bulk quantities which provides efficiencies in terms of packaging, warehouse-level inventory management, and reduces the risk of shoplifting.

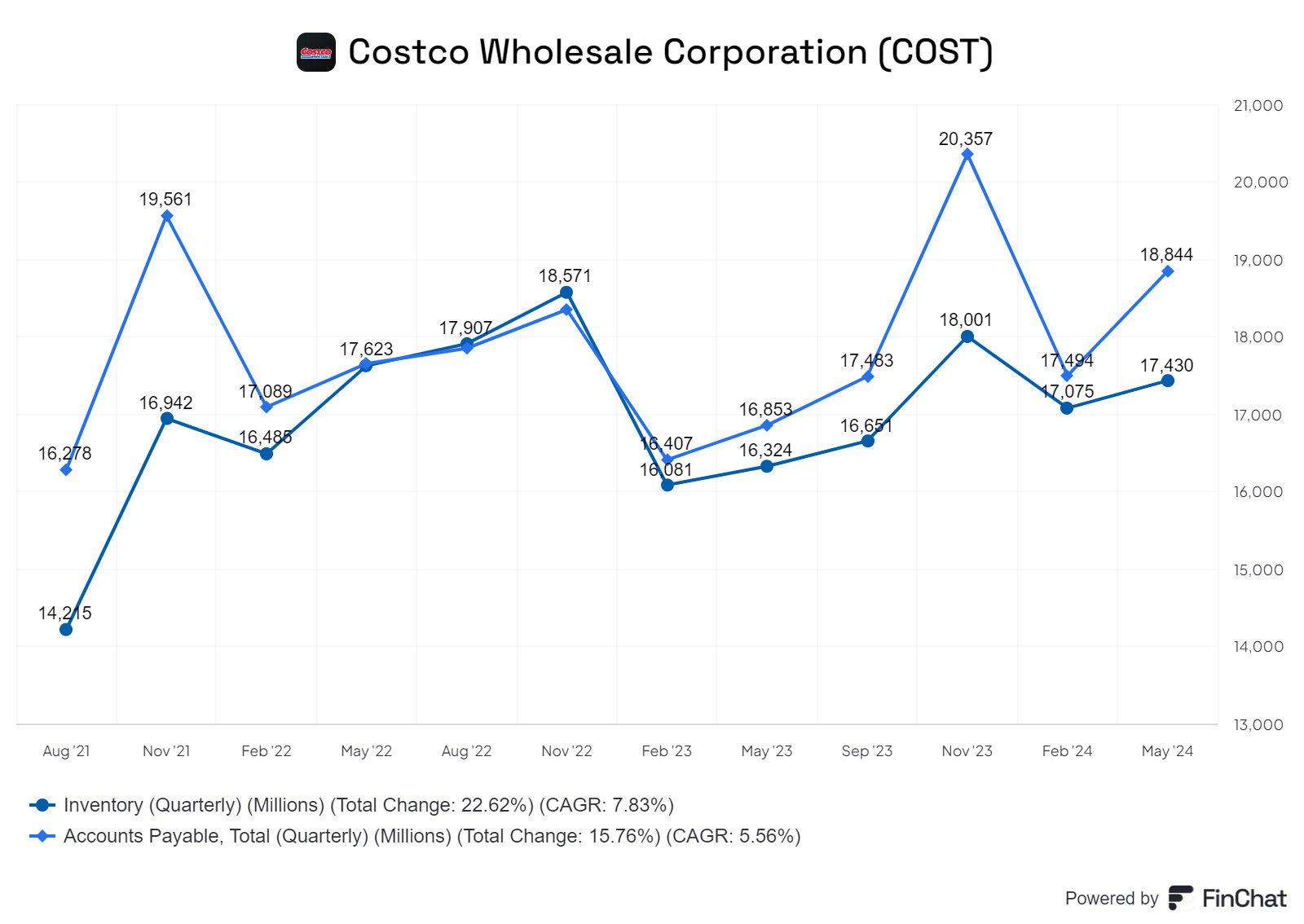

• Scale Economics. The limited selection within each product category makes it possible to acquire large amounts of each SKU increasing Costco’s negotiating leverage with suppliers. This brings down prices, and leads to attractive payment terms. Costco turns its inventory over 12 times per year and suppliers are effectively financing Costco’s inventory with payables typically exceeding the value of inventory. For example at the end of May 2024, payables were $18.8bn vs inventories of $ 17.4bn.

• Low Operating Costs. Warehouses have few amenities and products are displayed on simple fixtures or on pallets. Inventory can be moved directly from trucks to the selling floor. These factors allow Costco to achieve high employee productivity despite paying above-average wages and retaining employees for the long term.

Costco’s rapid inventory turnover means less inventory relative to sales volume. Costco needs less working capital to support the business. Costco’s payment terms with suppliers and rapid inventory turnover combined to ensure it sells merchandise before suppliers must be paid. Costco typically has a payable-to-inventory ratio of slightly over 100 percent. Suppliers rather than shareholders finance a large portion of Costco’s working capital requirements

In the USA, Costco is the second largest bricks-and-mortar retailer behind Wal-Mart. It shifts a huge volume of merchandise through a relatively small number of warehouses. This means a much simpler logistical network. The logistics advantage is increased by the limited number of SKUs that are offered.

How is management able to keep SG&A costs in check given the company’s reputation for offering higher than average wages and benefits to employees?

Sol Price’s believed in paying higher than average wages and generous benefits in exchange for hard work. This is in sharp contrast with many leading retailers that tend to pay low wages and limit benefits. Costco’s management believes that higher labour costs are more than offset by better productivity that is driven by a high level of employee loyalty.

Costco has a long-standing policy of promoting employees from within the company and offering not just a job but a career path. They limit part-time employees to less than 50%. Jim Sinegal has estimated that employee turnover is typically around 5 percent for employees who have been on the job for at least a year. This compares favourably with the 60% typical at some large retailers.

Costco created the Kirkland private label in 1995 at a time when such products were seen as inferior to branded products. The idea was to provide the best value for top quality merchandise that is as good or better than the leading national brand. Customers save at least 15 to 20% relative to the national brand’s price at Costco. Costco opted to use the Kirkland brand across categories. The Kirkland and branded products are usually displayed side-by-side in the warehouse, allowing customers to make quick comparisons.

Costco’s massive scale means it can negotiate advantageous pricing for the Kirkland private label. It is an open secret that the manufacturer of most Kirkland products is also the manufacturer for the equivalent branded product. Many customers view Kirkland Signature itself as a branded product.

The gasoline business represented approximately 13% of total net sales in 2023.

Net sales for e-commerce represented approximately 6% of total net sales in 2023.

Details of Membership Scheme

There are two types of memberships

1. Gold Star Memberships are available to individuals;

2. Business memberships are limited to businesses, including individuals with a business license, retail sales license, or comparable document. Business members may add additional cardholders (affiliates), to which the same annual fee applies.

Affiliates are not available for Gold Star members. All paid memberships include a free household card.

The annual fee for these memberships is $60 in the U.S. and varies in other countries to the local currency equivalent of ~$45 to $60.

Member renewal rate was 92.7% in the U.S. at the end of 2023.

Paid cardholders (except affiliates) are eligible to upgrade to an Executive membership in the U.S., for an additional annual fee of $60. Executive member thus pay a total fee of $120.

Executive members earn a 2% reward on qualified purchases (generally up to a maximum reward of $1,000 per year), redeemable at Costco warehouse.

Executive members totalled 32.3mn and represented 45.4% of paid members. As they have paid more, they feel more motivated to buy more to “get their money’s worth.” Executive members represented 72.8% of worldwide net sales in 2023.

In 2023, The membership status was as follows:

Gold Star 58,800,000

Business 12,200,000

Total Paid Members 71,000,000

Household Cards 56,900,000

Total Cardholders 127,900

At the end of 2023, They employed 316,000 employees worldwide. Their progressive HR policies and higher remuneration results in a higher than average retention rate . In 2023, 90% for employees who had been with the company for at least a year. 65% of the employees are in the US and the US accounts for 72 % of sales.

Nick Sleep Scale Economies Shared (SES)

Nick Sleep, the renowned Fund Manager, was also a fan of Costco. He identified the business model in Costco as what he dubbed Scale Economies Shared (SES). Due to scale and buying power, Costco can extract a higher margin. Rather than pocketing this margin, it shares a large part of it with customers. This drives sales and memberships which add further to the buying power of the business. Sleep believed the Amazon also has SES in its business model.

Some Key Financial Data

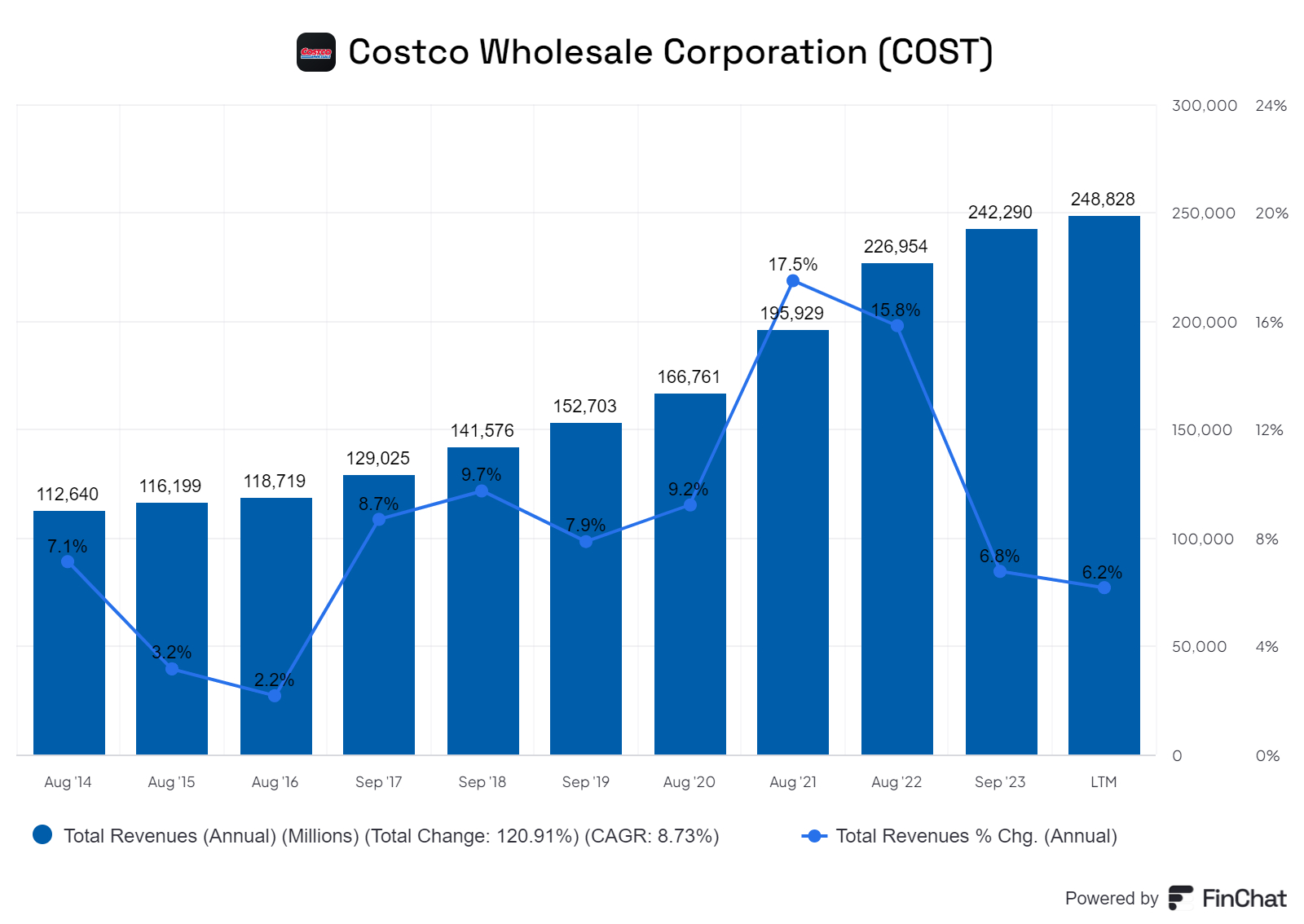

Annual sales run rate is about $242bn. The rate of growth spiked to 17% during the COVID 19 pandemic but has otherwise been in the mid to high single digit percentages in recent years.

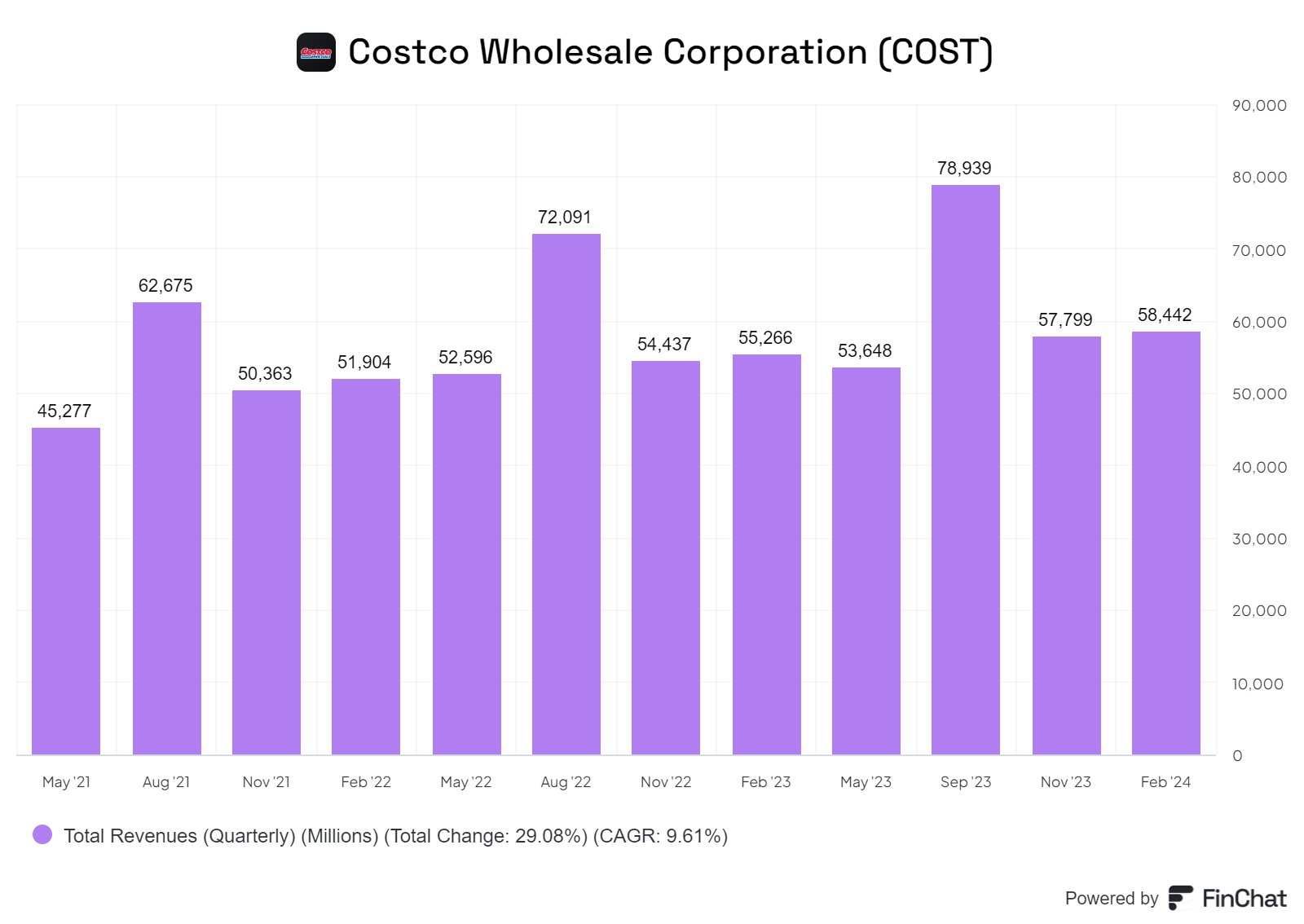

The quarterly numbers show a peak in the quarter ending August or September. The last quarterly revenue was $58bn.

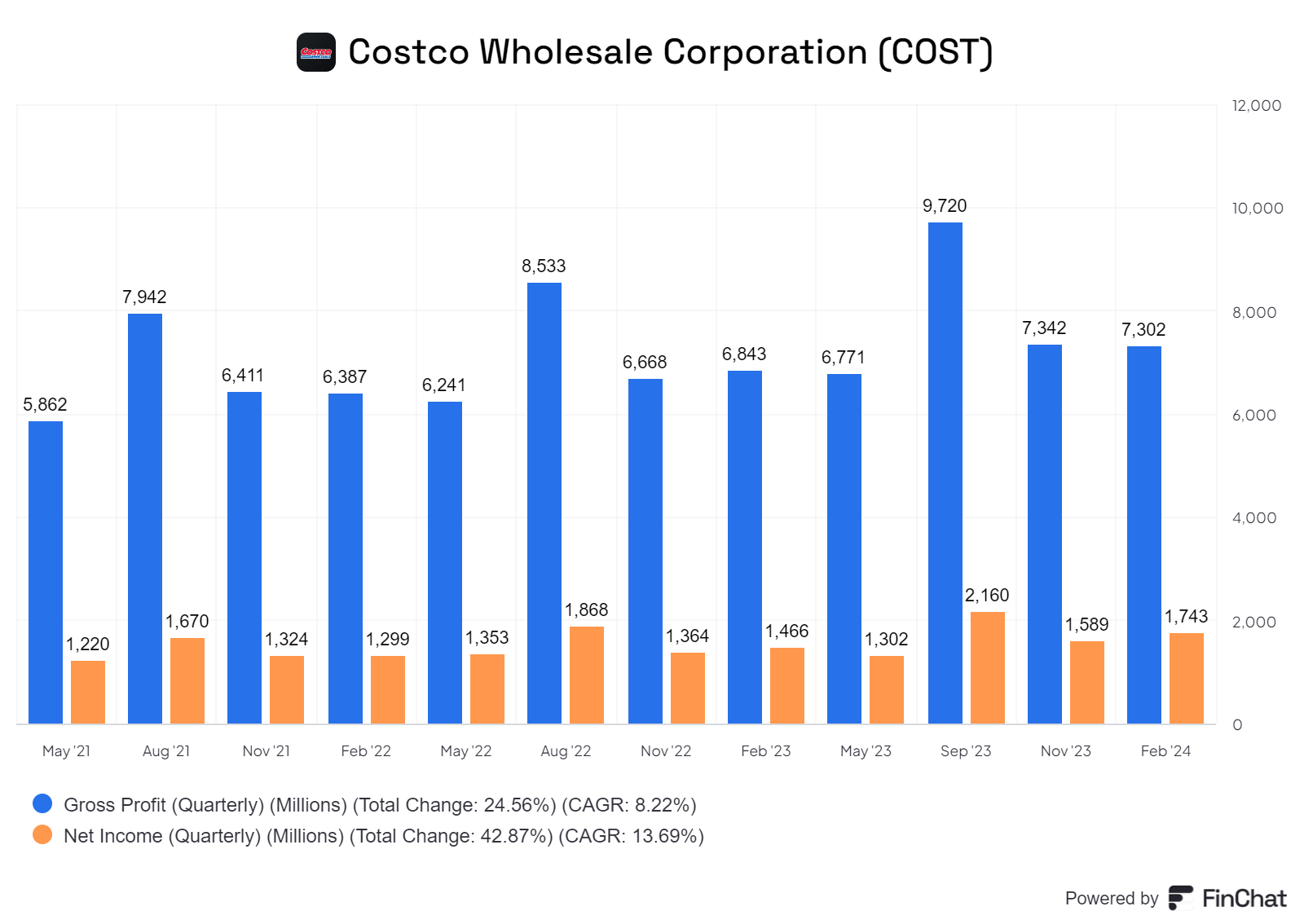

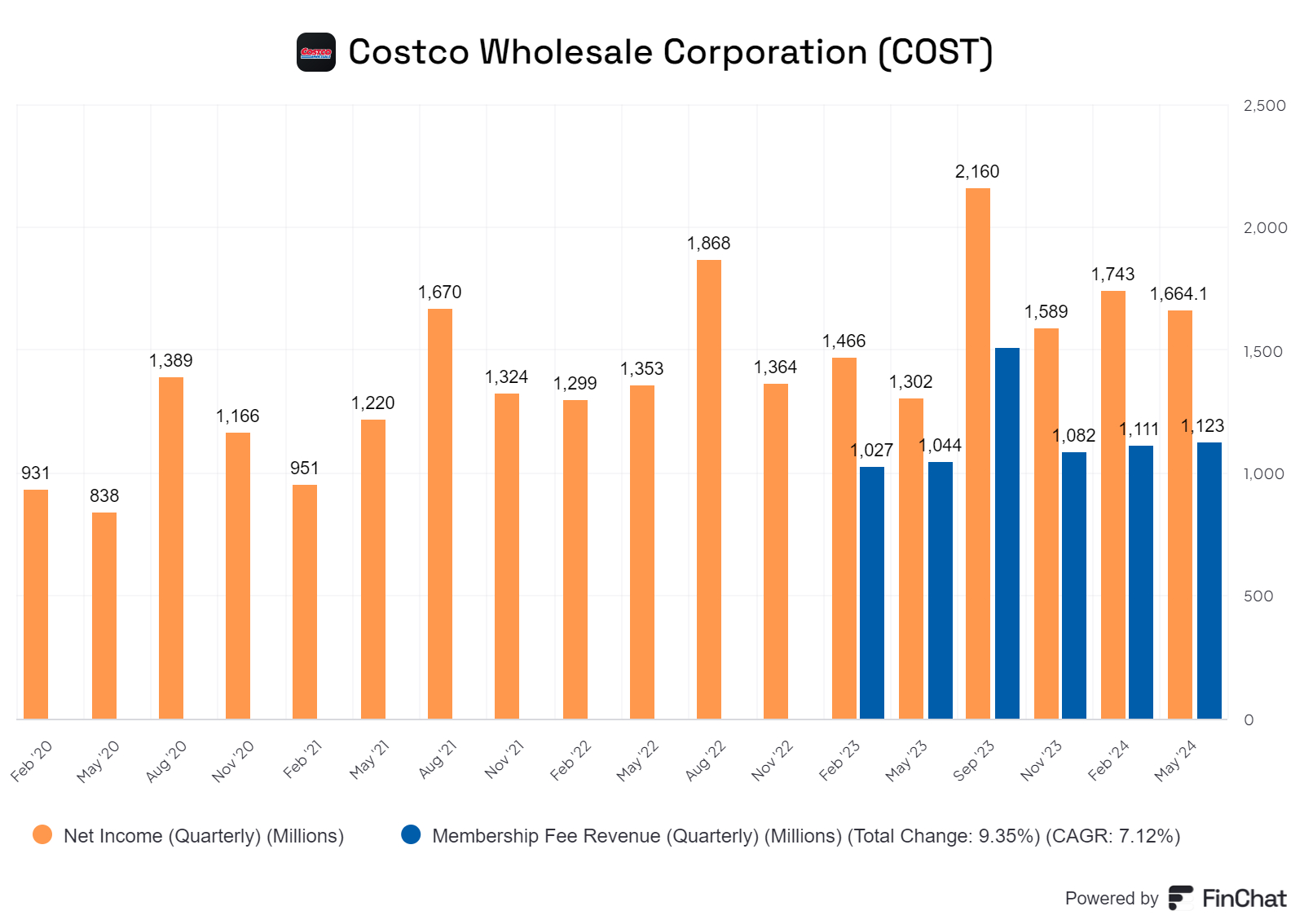

The chart below quarterly Gross Profit and Net Profit. The most recent quarterly data for these $7.3bn and $1.7bn respectively.

The chart above shows quarterly net profit and membership income. Assuming membership income has no cost (likely to close to the truth), the latter is an impressive 67% of the former.

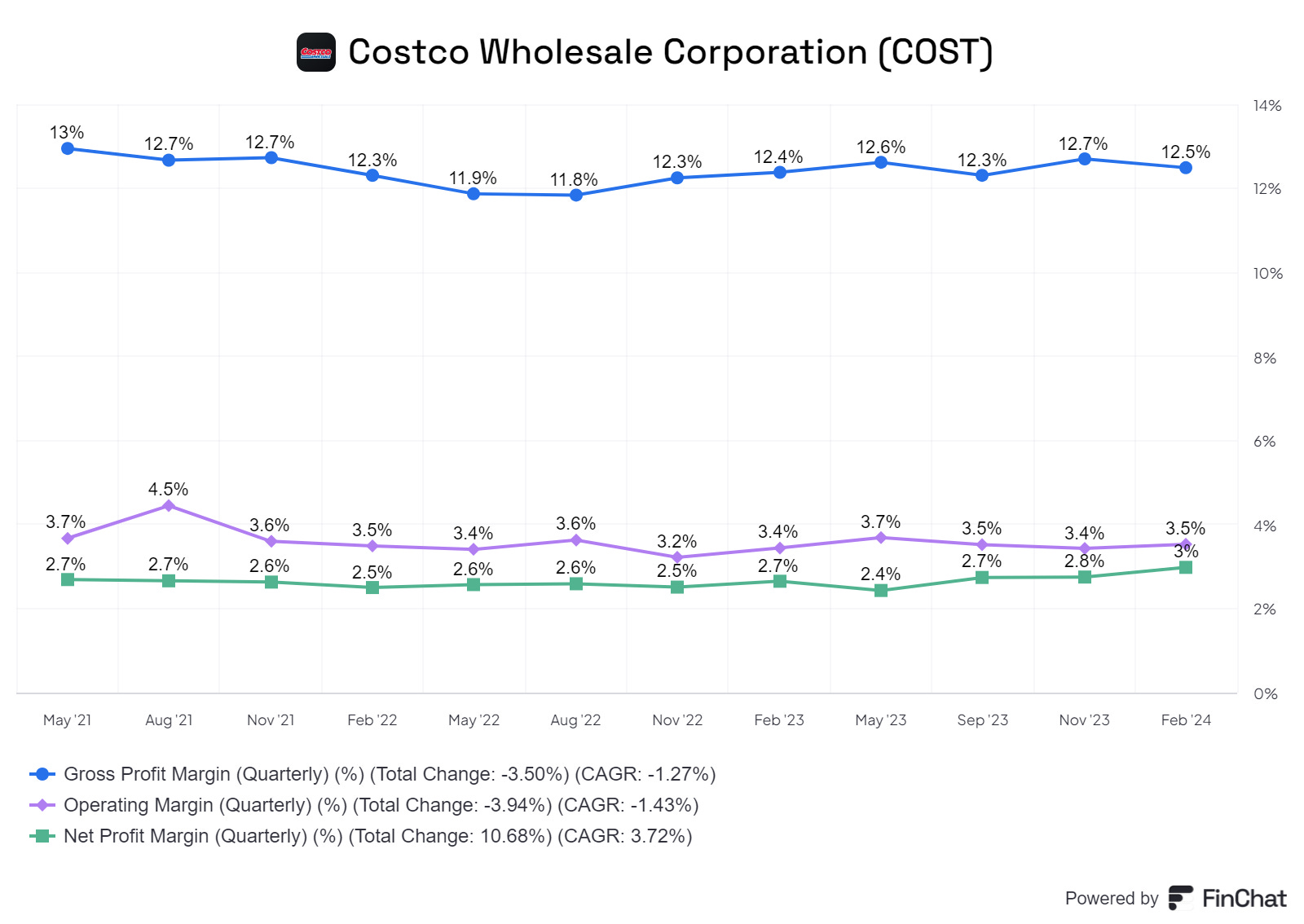

The chart below shows Costco’s margins. The company keeps Gross Margins capped at 12% to 14%. Operating Margins are around 3.5% and Net Margins are around 2.6%.

This means that Selling, General and Admin Expenses (S,G&A) have to be kept to at or below 10% of revenues. This has to be achieved despite paying higher than average wages. They do this by higher employee productivity (due to lower turnover) and almost no advertising.

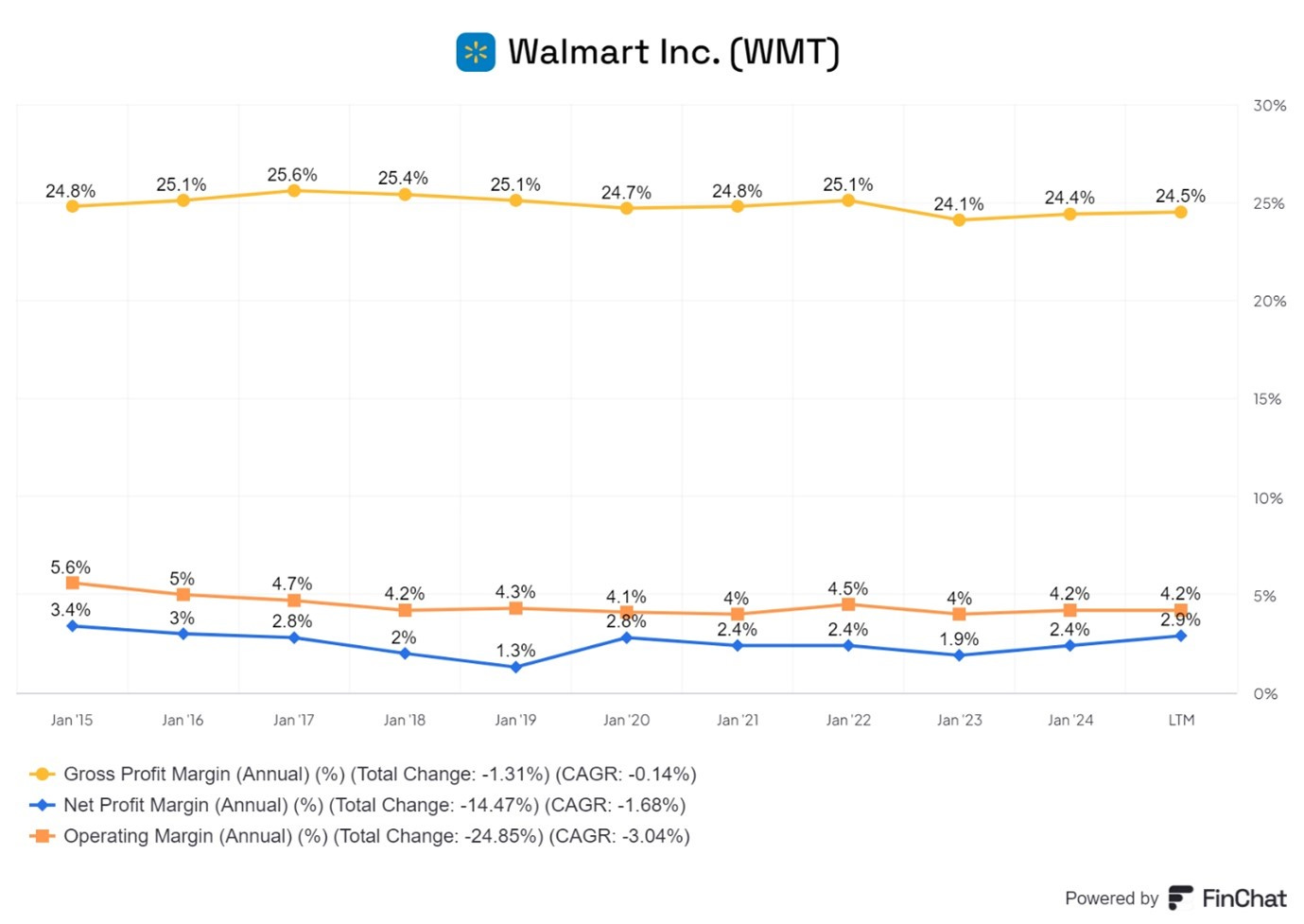

The chart below shows the margins for Walmart (WMT). It should be noted WMT is much bigger than COST with annual sales of ~ $600bn (vs $240bn) WMT have much higher gross margins than Costco (24.4%) but end up with similar Net Income Margin (of 3%).

This shows the much larger WMT has a much less efficient business model with S,G&A costs almost double of COST (19% vs 10%)

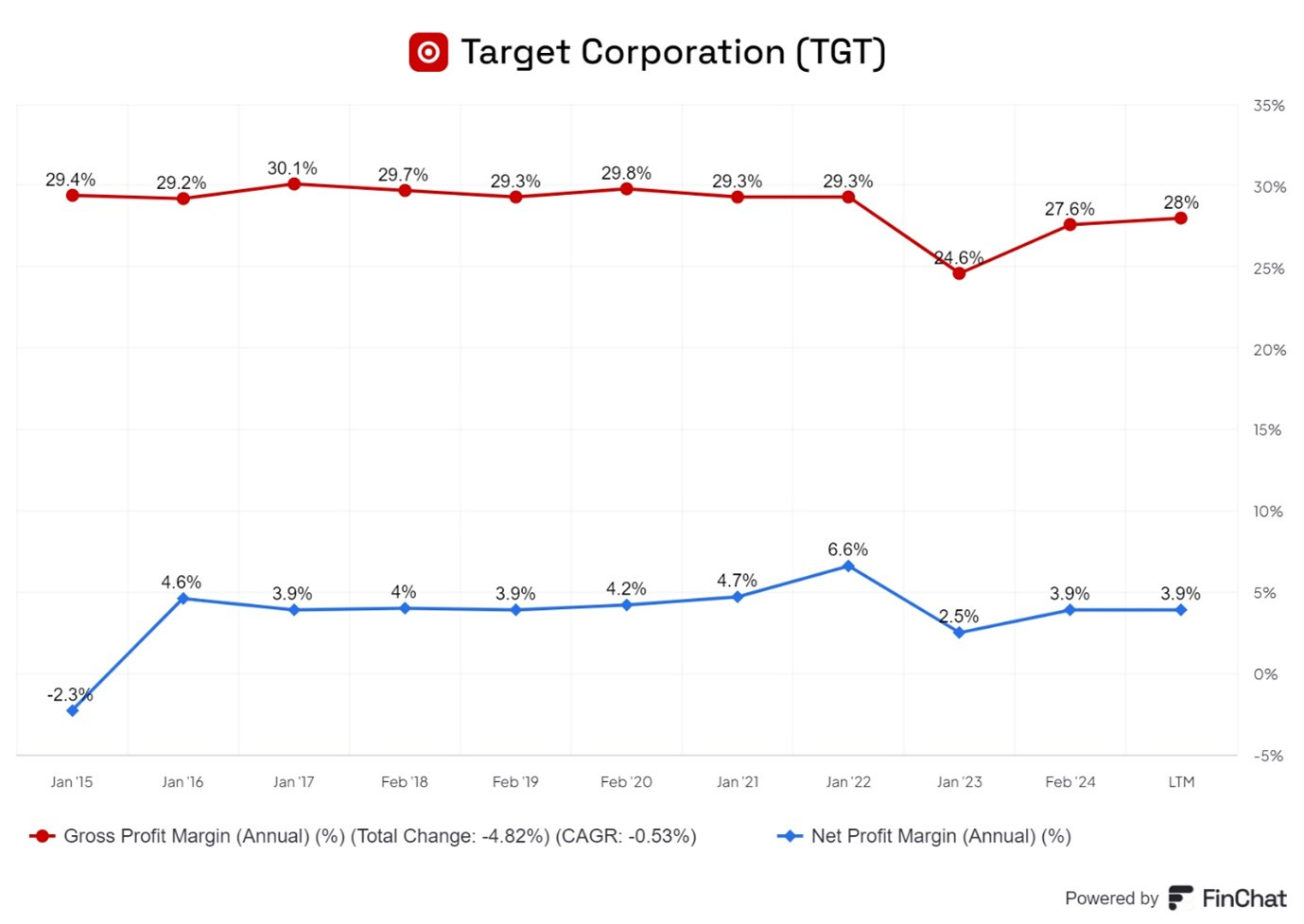

Target (TGT) has a similar margin profile as shown below.

This difference in margins between Costco on the one hand, and Walmart and Target on the other, which reflects the former’s much lower operating cost, has important implications.

For the more limited goods that Costco supplies, it will almost always have lower prices than WMT or TGT assuming similar cost of goods. This means it will win any price war and can use that advantage to grow sales and the all-important memberships. Supermarkets may offer loss leading driven prices on certain limited key products but cannot compete on price across the piece.

Costco’ s strategy is to establish new warehouses and slowly expand the range of goods they offer, provided they keep their operating cost advantage. As Michael Porter noted in “Competitive Advantage” being the lowest cost supplier can be a durable source of competitive advantage.

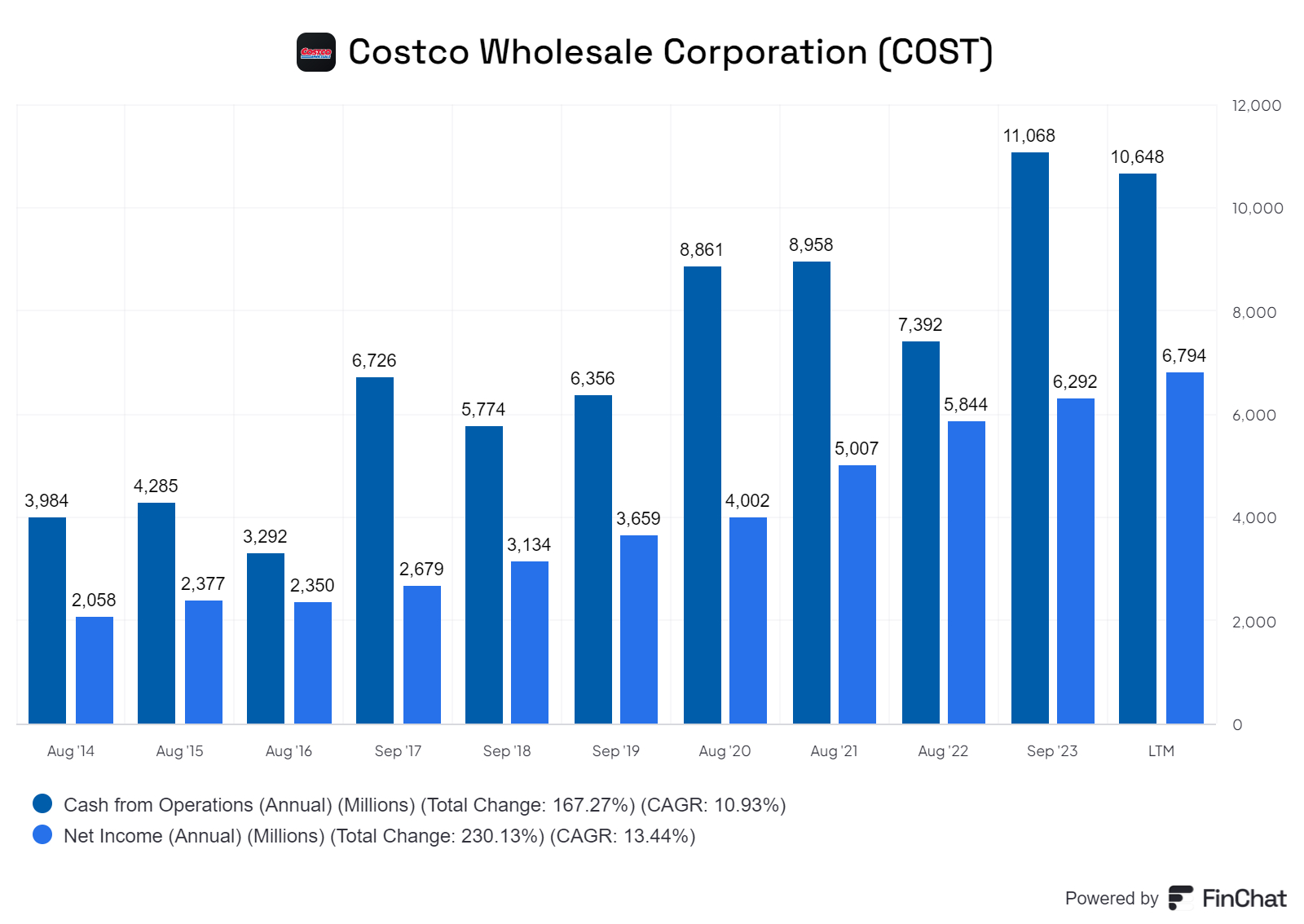

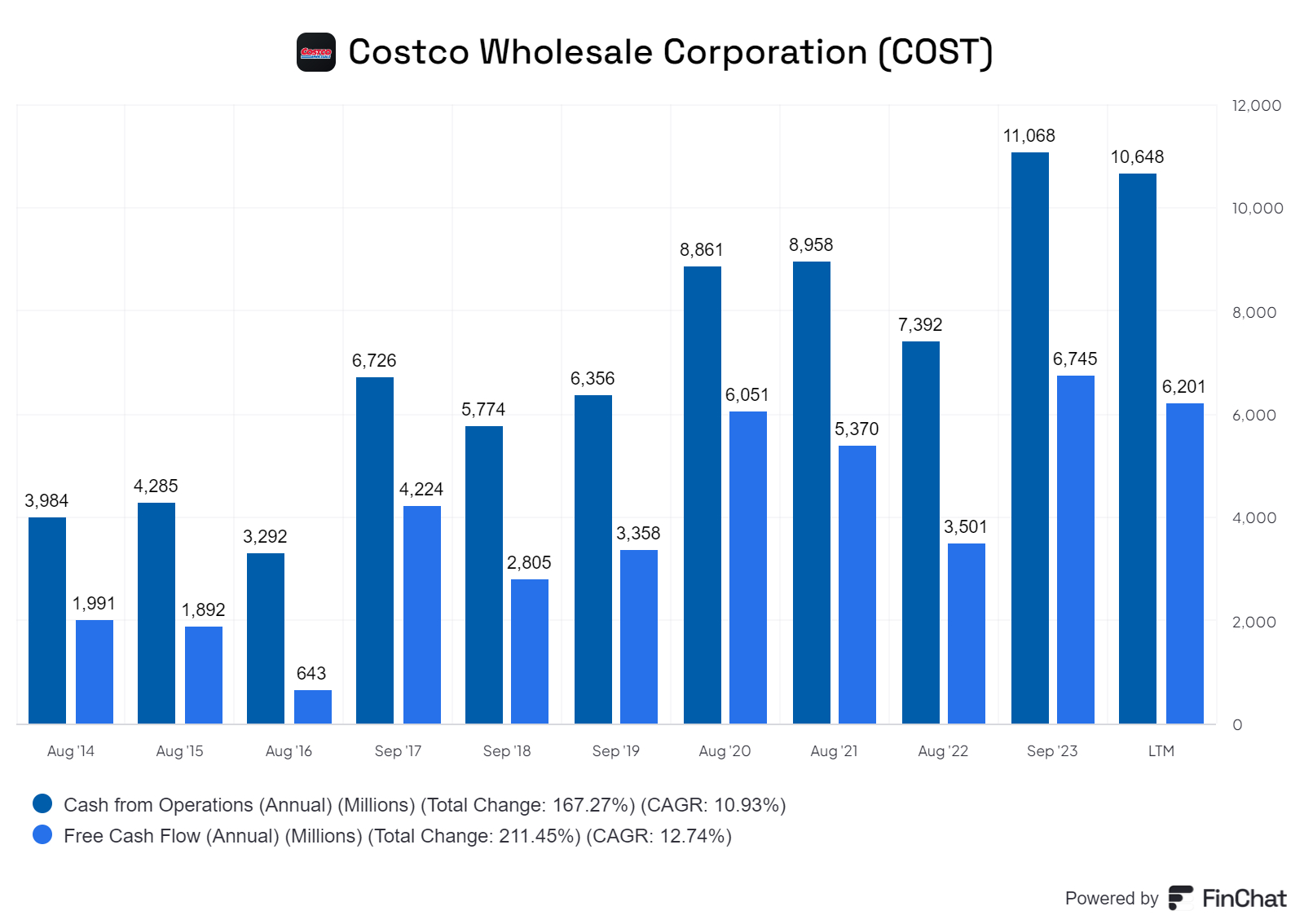

In the last quarter Operating cash was $10.6bn and Free Cash Flow was $ 6.2bn. This shows the strong cash generation profile of the company.

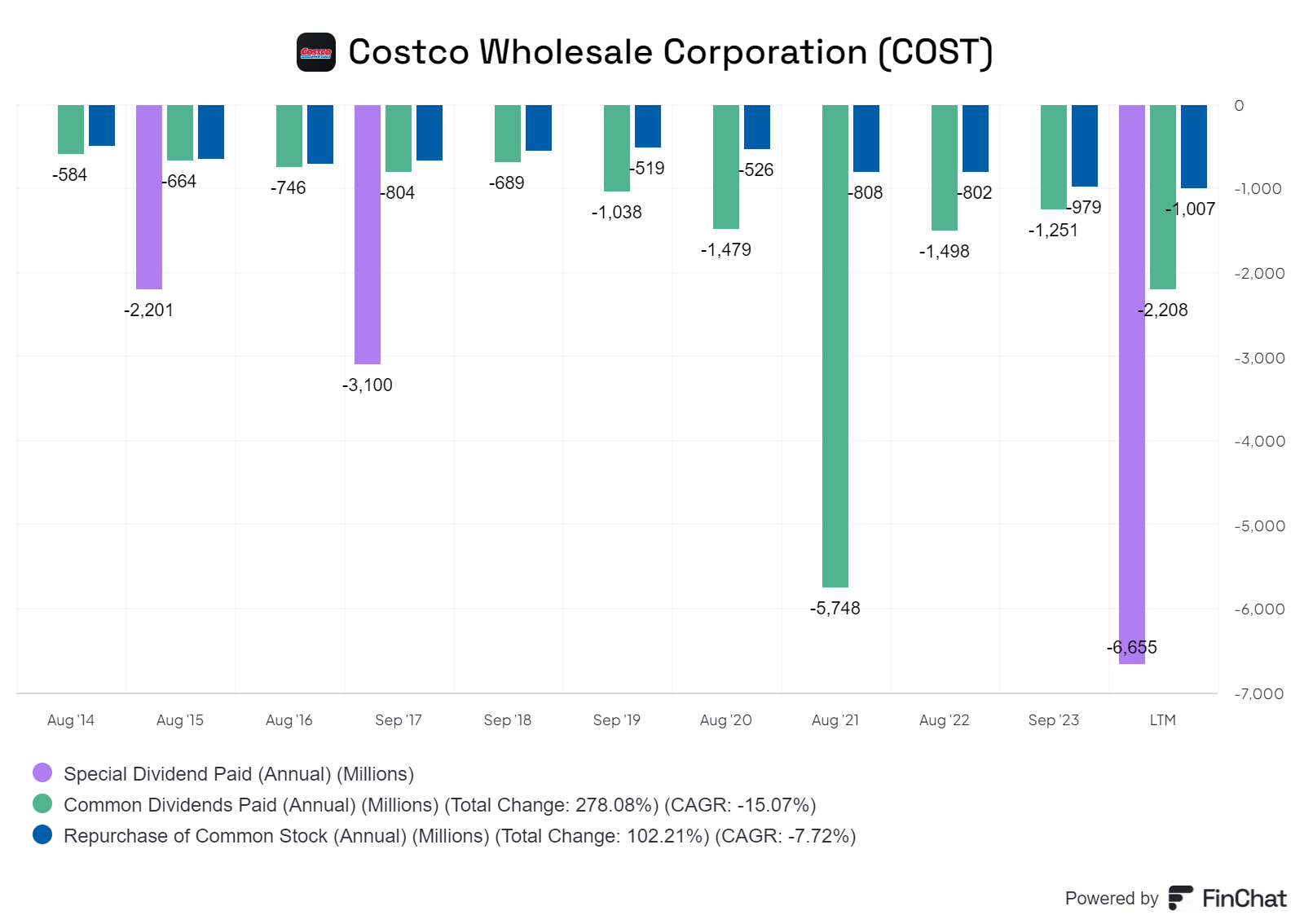

The chart above shows some of the uses of cash. In most years the company pays a common dividend and repurchases some stock. In addition, there are large periodic special dividends (shown in purple). The items in the chart are shown as negative as they represent cash outflows.

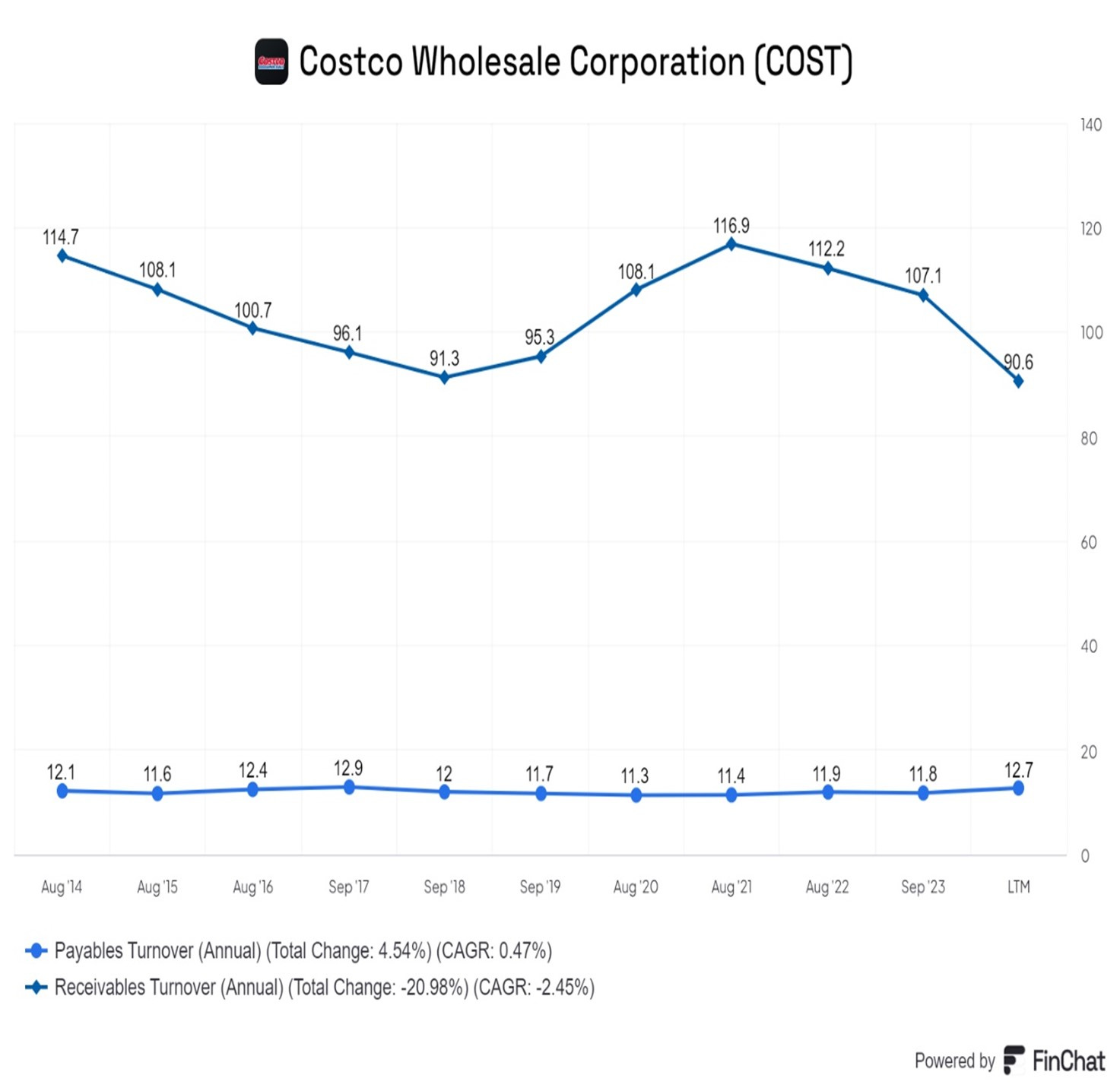

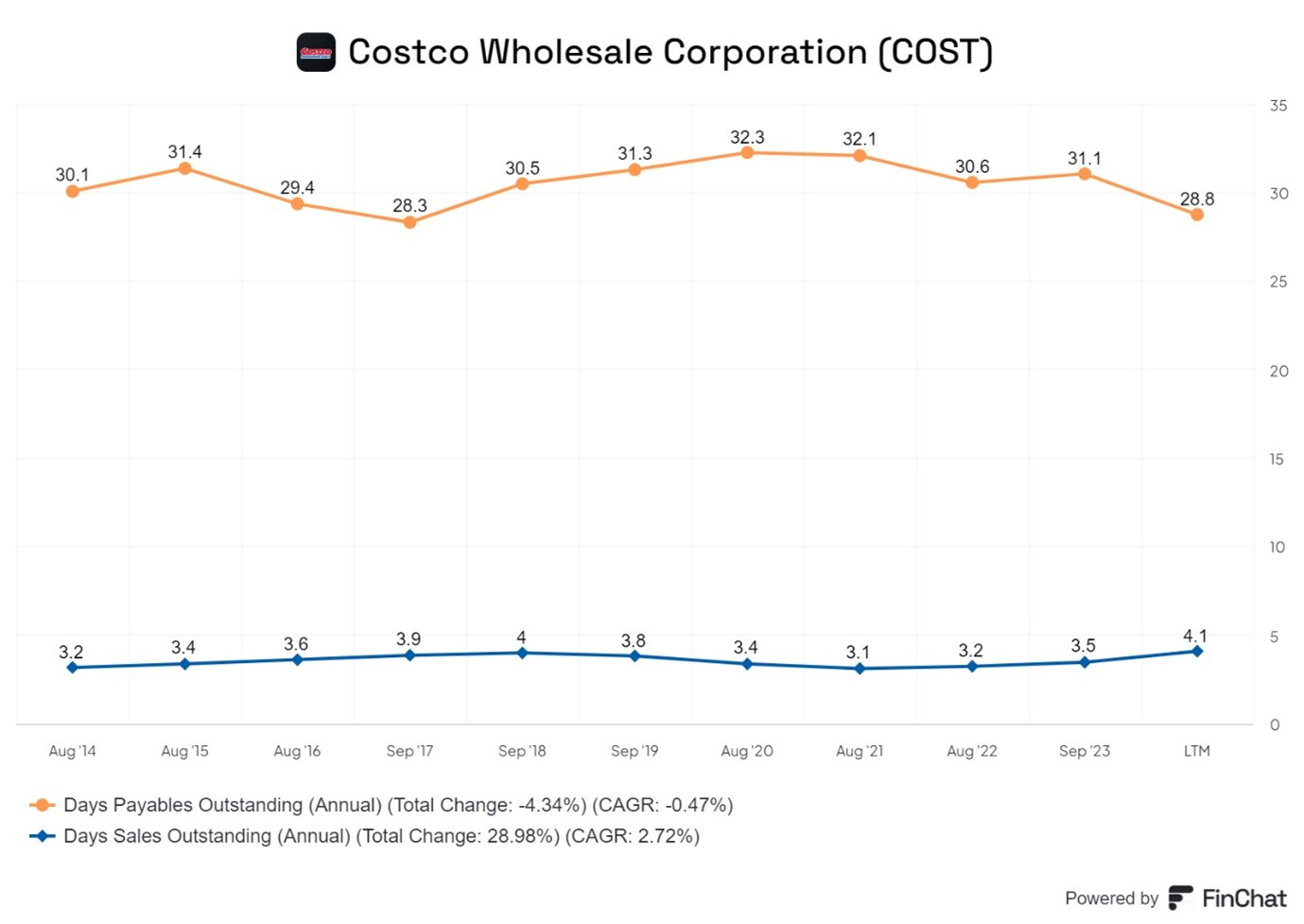

The chart above shows receivable turn over 90 times a year while payables turn over approximately 12 times a year.

This means Costco gets paid on average within 4 days (360/90) but can pay suppliers only after 28 days (360/12.7) on average. This mean the inventory is mainly financed by suppliers and Costco can have low or negative working capital. This illustrated in the chart below which shows that Accounts Payable are usually greater than or equal to inventories.

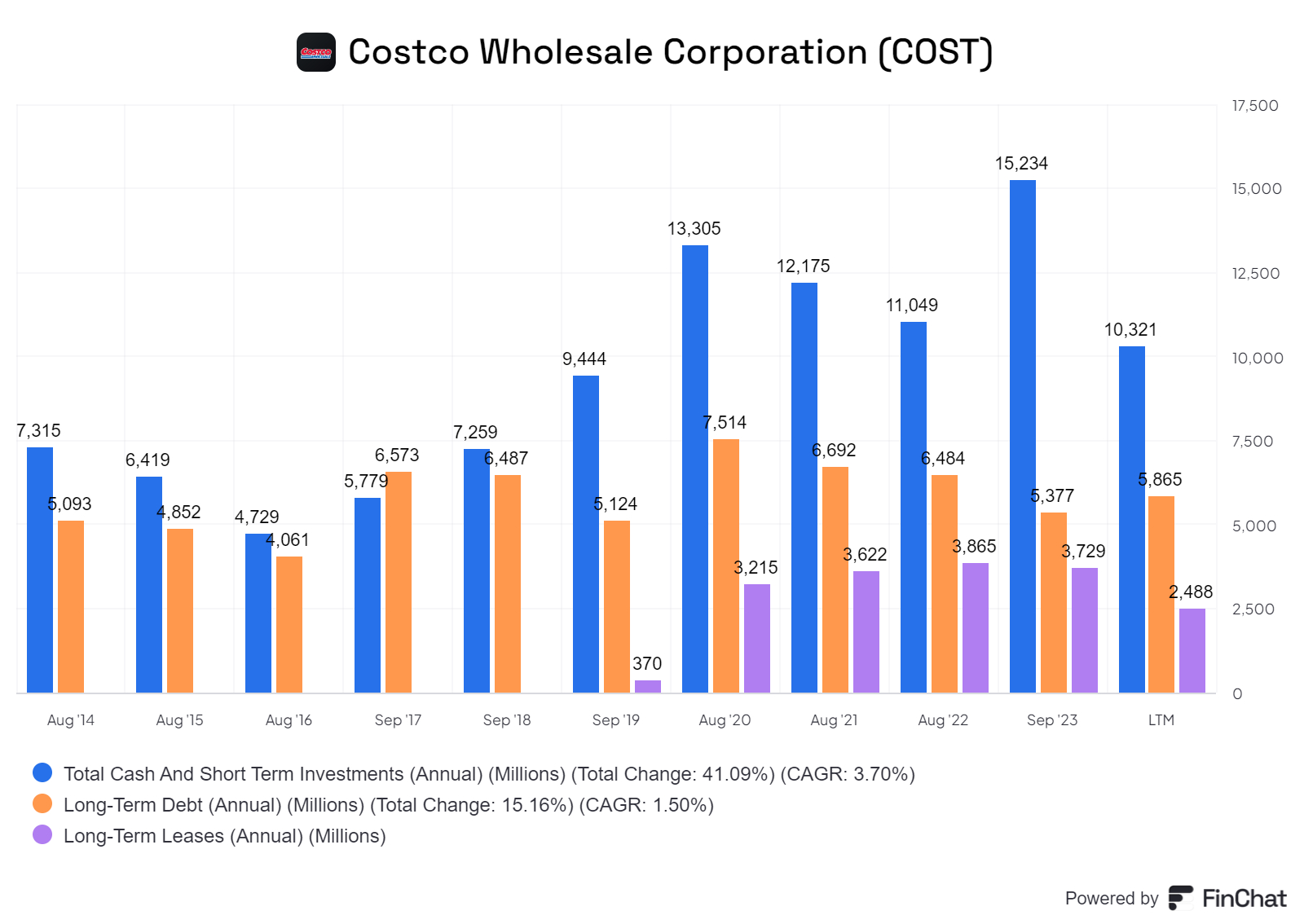

Costco’s balance sheet is strong as indicated by the fact the total cash is more than long-term debt and long-term leases combined (see below).

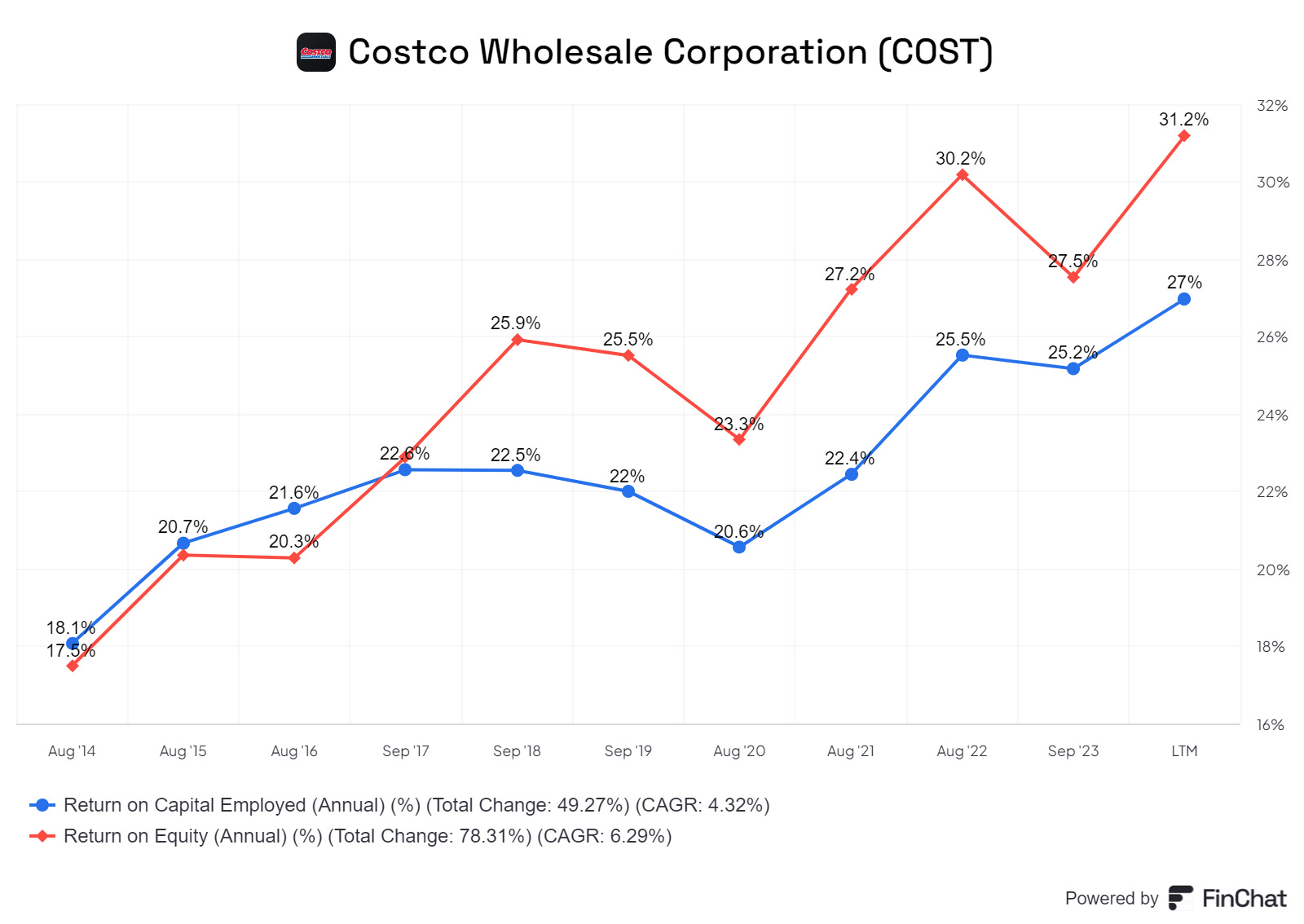

The chart above shows the increase in profitability. Return on Equity (RoE) increased from 17% to 31% in the last ten years. A comparable figure for current RoE for WMT and TGT is 19% and 32% respectively.

Returns from the Costco stock have been higher than average in the last ten years. Over the last 30 years the Costco stock has given a CAGR Return of 15.6%. Over the last 10 years, the CAGR Return has been 21.6% (6X over ten years) .

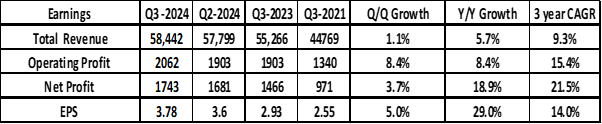

The Q3 2024 Quarterly Results

· Total revenue grew 5.7% 9 (y/y) but net profit grew 18.9%.

· In the last three years, sales grew 9.3% (CAGR) while net profit grew 21.5% (CAGR).

These numbers indicate some degree of operating leverage in the business model.

Margins are very stable. As noted above, the company restricts Gross Margins to the 12% to 14% and needs to keep S,G&A costs down to~10% to end up with 3% Net Income Margin. This was achieved in the most recent quarter.

Highlights from the Earnings Conference Call.

· Traffic or shopping frequency increased 6.1% worldwide and 5.5% in the U.S.

· Average transaction or ticket was up 0.5% worldwide and up 0.7% in the U.S.

· Membership fee income of $1,123 million, an increase of 7.6% year-over-year.

· U.S. and Canada renewal rate were 93%, up one tenth of a percent from Q2 end.

· Worldwide renewal rate came in at 90.5%, the same as Q2 end.

· They ended Q3 with 74.5 million paid household members, up 7.8% versus last year, and 133.9 million card holders.

· There were 34.5 million paid executive memberships- they now represent over 46% of paid members and 73.1% of worldwide sales.

Costco expect to add 29 stores net this year (growth of 3.5%).

“Q3 capex was $1.06bn, and we estimate full year 2024 capital expenditure will be between $4.3bn and $4.5bn.” This compares with $4.3bn in 2023

“Across all core merchandise, inflation was essentially flat in Q3, with fresh foods close to zero and slight inflation in food and sundries being offset by some deflation in non-foods. The deflation in non-foods was led by hardware, sporting goods and furniture, all still benefiting from lower freight costs year-over-year.”

“We're intentionally creating incremental value for our members by delivering lower prices wherever possible. We believe our strategy of delivering value to drive unit volume and member satisfaction is the winning combination for us.”

“Our buying teams are constantly aware of changing costs across all of their SKUs and are ensuring that we are capturing all cost decreases quickly so that we can pass on incremental value through price reductions.”

Although the physical warehouses are the core of Costco they have a growing online presence.

“We continue to make enhancements to the app and website and are excited about the traction that these initiatives are getting with members. Total e-commerce sales growth in the quarter was led by Gold and Silver bullion, gift cards and appliances.”

“Our app downloads were up 32% versus a year ago with about 2.5 million new downloads in the quarter, bringing total downloads to more than 35 million. Site traffic was up 16% and average order value was up 8%.”

They have extended an agreement with Uber eats from just Texas to 17 states plus the whole of Canada . Under this, Uber eats will deliver Costco goods.

“In addition to the increased access to Uber Eats customers, the agreement will allow us to sell Uber gift cards globally and offer discounted Uber One annual membership to Costco members.”

One lever to raise profits is to increase the membership fee. The last increase was in 2017.

“We've historically looked at increasing the membership fee every five years or so. ….we're beyond that time period now in terms of what would be the typical cycle”

“We feel really good about membership renewal rates. We feel really good about the test of are we delivering significantly more value to members than we were or have since we last increased the membership fee.”

Fee increases are an important part of the business model.

“You know fee increases go back to the members in lower prices. I mean that's s one of the key parts that we use that money for is that it allows us to broaden that distance from the competition and bring greater values than improving our operation overall for the member. So that's the primary focus.”

As 70% of their sales are from the US, have they reached saturation there?

“We still see significant runway to continue to opening more warehouses in the U.S. in the future. I think that sort of 25 to 30 new warehouse count is a reasonable proxy for what we think the runway is for the foreseeable future for new warehouses. We still see plenty of runway in the U.S. to continue to open more warehouses, but we also see a lot of growth opportunity, of course, in the international markets as well.”

They are experimenting with buy online and pick n store (bopis) offering.

“We are rolling out an expanded buy online pickup in warehouse that is always going to be limited in scope based on the volume in our warehouses that we have. We can't expand to all categories, but we're expanding as we currently speak in televisions and other electronic items that are there as -- and so yeah, we see that as a real opportunity for us.”

They are looking at using technology and the data they have on their members.

“Technology and data are something that we're sort of building a path towards, I would still say there's significant opportunity for us to grow in that space because of the unique nature of the relationship we have with our members and the ways in which we can deliver value for them and tap into that data and tap into the growth that we're creating both in the warehouse and through digital channels.

“We do have a unique model. We have a relationship with all of our members. Our responsibility is use that data wisely and respectfully. “

The “Treasure Hunt” element which is a key aspect to the Costco customer experience is greatly valued.

“We never want to compromise the treasure hunt of Costco. And that's equally as important as people that go to costco.com, never knew that they needed a 16 foot shed and they see a phenomenal value as they do in the warehouse.” “People come in to spend $100 and walk out with $300. That's because our buyers and our operators do a great job in making the warehouses exciting.”

They believe they are growing faster than the overall market and gaining share

“We're gaining market share. we're drawing customers to what Costco has offer for many years and it's never more relevant than now based on what we're hearing from members and consumers.”

“So we feel good about our ability to continue to outpace the market there and we're seeing a good opportunity within digital in particular to really drive more connection with the member and take some of those big ticket items from the warehouse to online as well.”

Summary

Costco has a unique and differentiated business model.

Retailers do not normally deliberately limit their margins so consistently and keep at a low level.

Retailers do not normally look to pay above average wages and benefits.

However, the model has many strengths, and it demonstrably works. In recent years, profitability has improved greatly .

Costco does not compete across all categories but strictly it limits itself to a few where it can be by far the lowest cost supplier. This means they can win almost any price war as competitors have much higher cost structures.

Costco has a unique culture where it is not a conventional retailer but a buying agent for the customer. For a small fee, Costco sources the best possible merchandise at the lowest possible prices.

The culture demands that management act as a fiduciary for members and drive down prices as far as possible consistent with earning a reasonable return. Growth is made possible not through gross margin expansion but through operating efficiencies and opening new warehouses. The business model builds great customer loyalty.

We believe the company can continue to sustainably increase warehouses at a rate of 3% -4% per annum for many years given

· the free cash flow it generates,

· the management bandwidth it has and

· the growth opportunities it see both in North America and the Rest of the World.

We believe there are two risks to continued progress.

The first is the management may change the culture and business model.

Our research and reading suggests there is little risk of that. Costco’s executive management team appears to be fully on board with the corporate ethos pioneered by Sol Price and Jim Sinegal.

One relevant key factor is the policy of higher remuneration and the tradition of promoting from within. The former ensure employee longevity and the latter means senior and middle management are deeply steeped in the Costco culture.

The second is if a deep recession hits consumers. This is a risk for all retailers, especially those focused on discretionary expenditure. Costco is better placed than most as its customers have higher disposable income and are perhaps, less likely to lose jobs in a recession

In summary, Costco is a quality business which has performed well for three decades.

However, it well known to investors given its strong performance and the unstinting advocacy by Charlie Munger.

This means the stock is not cheap and the valuation is lofty. The risk for an investor entering now, is they may experience a poor return, even if the company performs well, especially if there is some valuation compression.

Valuation

As the chart below produced by Maverick Equity Research shows, Costco trades at a relatively expensive level compared with other companies broadly in the same sector

The analysts’ consensus expectations for EPS in FY2024, FY2025 and FY2026 are at $ 16.1, $ 17.7 and $ 19.4 respectively.

This means at the current price per share of about $ 816 the stock is trading at 46 times FY 2025 earnings and 42 times FY 26 earnings.

This seems a little expensive – three years ago we bought the stock reluctantly at a forward P/E of 40X but fortunately it has given a fine result since then.

The decision making is complicated as we do not know what premium to assign to Costco’s higher quality business model. What is the justified premium for higher predictability of earnings thanks to membership income?

We can do a quick “back of the envelope” valuation calculation.

Let us assume that revenues grow at 8% to 9% per annum for the next five years.

Let us further assume that this leads to EPS growth of 15% for the next five years.

FY 2023 EPS was $14.2 . We can forecast 2028 EPS to be $28.6 ( (1.15)^5) * $14.2)

If we assume in 2027 the forward P/E multiple will be 35, the share price in 2027 will be ~$1000 per share.

This compares with today’s share price of $ 826 - a 21% discount.

A 21% discount implies a CAGR return of 6.5% for the next three years on the Costco Stock. This is clearly too low and indicates that the stock is perhaps a little overvalued currently.

Conclusions

· Costco is a well-established company with a great business model.

· We will continue to hold on to our shares where our position represents 4.5% of our portfolio.

· However, at the current valuation, we are reluctant to add to our holding at the current valuation.

· We would consider adding about 2% to 3% more if the forward earnings multiple goes below~ 32X forecast earnings.

Engaging read. The COST magic is to make everyone buy more than they need due to alluring prices - it must work when other retailers suffer during an economic downturn and it must work when everyone is cash surplus. We bought a membership for A$60 but never ended up buying enough to earn discounts sufficient to recover the membership cost during the year! If I were any wise, I would rather buy the stock than shop there.