I attach a write up these two companies. I had completed most of it by 9th March 2023 and had not got round it posting it here. This week Enphase Energy reported Q1 results and noted slowing demand in the USA and the stock fell 25% in the day !! On 9th March, I had concluded that the fair price for the share was USD 200 and I would be looking for a discount and enter at about USD 178 per share. With the fall this week, the share is trading at US$ 164. I should be buying it at this price (!) However, I will need to look at the Q1 results reported this week and the post-results conference call to see if the investment thesis outlined here needs to be reconsidered. However, I will still post the write-up here as completed on 9th March as it is still. I believe, a valid introduction to the two companies.

Introduction

Three years ago, I decided to install some solar panels on my roof in suburban London. The installer advised me to combine some relatively cheap, no-brand Chinese made solar panels with relatively expensive Enphase microinverters and a very expensive battery from LG or Solis. The company behind the Solis product is a listed Chinese company called Ginlong Technologies while Enphase Energy is listed in the USA. As I have no experience of the Chinese stock market, I decided to look at the latter. My research indicated that it was an interesting company and the in the process, I learned a lot about Inverters and the history and nature of the company. However, I concluded that the valuation was too high. This was a big error of commission as the stock has risen from about USD 40 per share at the time to USD 218 currently. If instead of installing a solar system, I had invested in Enphase, the profits on the shares today would be more than the cost of the solar installation!

In this note, we will look at two key companies that seem to be developing a duopoly in a niche market in the Solar energy value chain. Enphase Energy (ENPH) and SolarEdge Technologies (SEDG). The former is focused on Microinverters while the latter is focused Power Optimisers and large inverters.

String Inverters, Microinverters and Power Optimisers

An array of solar panels generates electricity (when the sun shines) in the form of Direct Current (DC). This must be converted to Alternating Current (AC) before it can be used in the home or exported to the Grid.

An inverter is required to invert the current from AC to DC. The inverter is considered the smartest piece of technology on the solar installation, because it facilitates the connection between the solar system and the Grid and manages the electrical current.

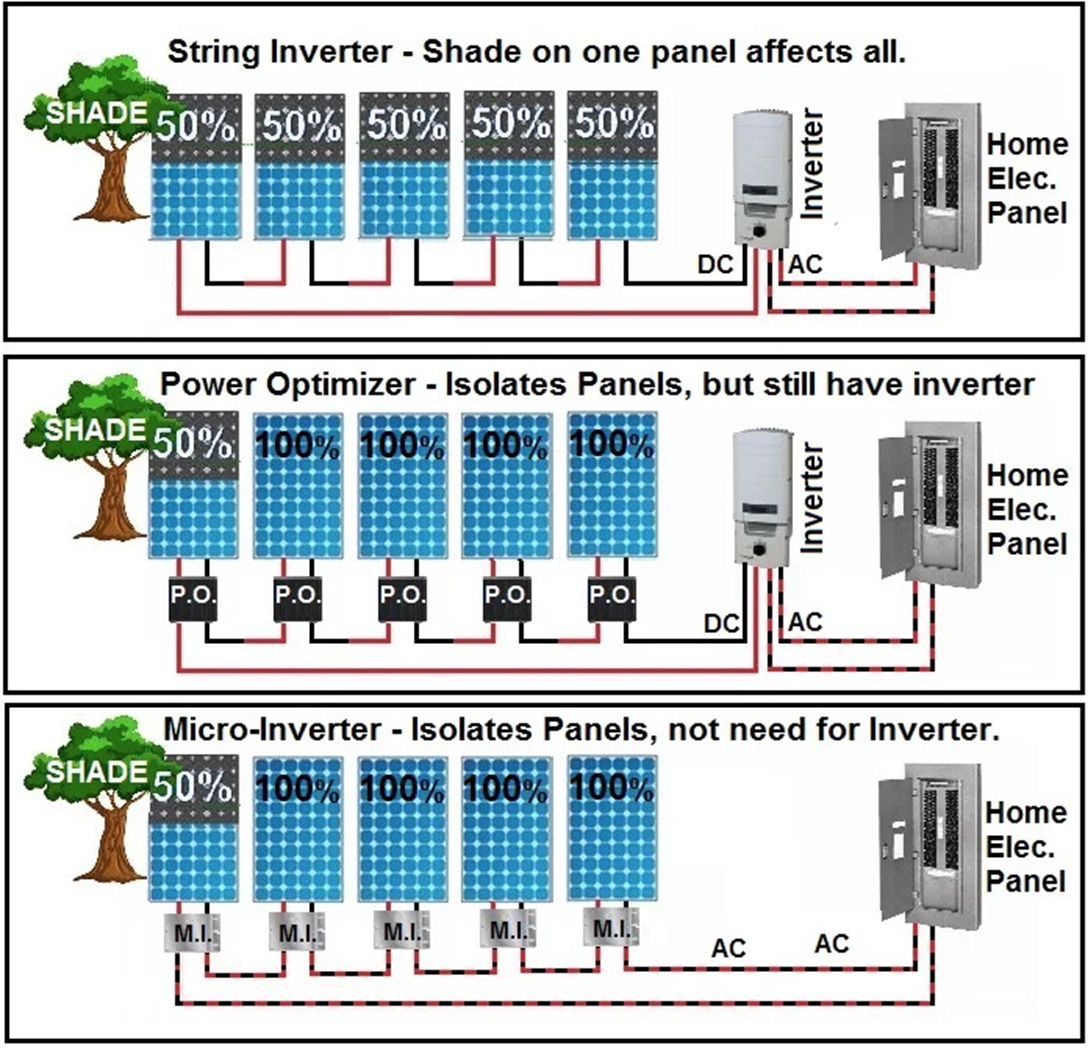

The most basic inverter is known as a string inverter (see the top panel above) which has wires from an array of panels running to it at a single point. The inverter converts the power from DC to AC and then runs it to the home. String inverters are cheap but have issues relating to safety and load management ability. In particular they possess a single point of failure i.e. the entirety of the system is only as efficient as its lowest performing panel - for example if one panel is operating at 50% output due to shading, all panels will be reduced to that level (as shown above). My installers emphasised this to me as one of the nine panels I wanted to install is poorly located in terms of shade and it would drag the output of the whole array down. String inverters make it more difficult to identify a problematic panel (which may not be performing for whatever reason) and require more maintenance.

However, string Inverters are the cheapest option and are commonly used for commercial, industrial, and utility-scale projects where the location is carefully chosen to ensure shade is not an issue. They were also widely used in residential installations in the US until regulations were changed in 2013. Since 2014, the inverter has become advanced :- innovation has been driven by the rapid adoption of renewables as well as legislation.

Solar power system owners aim for high energy production, low cost, high reliability, and low maintenance requirements, as well as reduced fire risks. Residential Solar owners with string inverters are unable to optimize the size or shape of their solar PV installations due to design limitations. As such, they experience performance loss from shading and other obstructions, can face frequent system failures and lack the ability to effectively monitor the performance of their solar PV installation. They face higher fire risk and due to their large size. String inverter installations can affect architectural aesthetics of the house or commercial building.

Enphase Energy (ENPH) has focused on microinverters (see bottom panel in above illustration). A microinverter is fitted to each individual panel rather than bulking multiple panels to one inverter. This is a distributed architecture where the DC is converted AC at each panel and shading on one or more panels does not drag down the output of the system. Microinverters are more expensive than string inverters but ensure output is less affected when part of the system suffer from shading. They are particularly suited to domestic systems where roof design is often affected by shading and other imperfections.

Solaredge Technologies (SEDG) has focused on Power Optimisers (See middle panel of the illustration above). SEDG developed a DC optimized inverter solution that changed the way power is harvested and managed in photovoltaic systems. It maximizes power generation at the individual panel but retains a String Inverter. This is suitable for a broad range of solar market segments, from residential solar installations to commercial and small utility‑scale solar installations.

We will look at recent developments in global renewables (including Solar) before looking at the companies in more detail.

Developments in the Global solar Industry.

Global electricity consumption is expected to double by 2035 and more than triple by 2050 relative to 2020. Urbanisation is expected to increase from 55% to 80% and this will be a major driver of the increase. Renewables are set to be the dominant electricity source. Solar’s share of installed capacity is expected to increase from 11% currently to 32% by 2050 according to Bloomberg NEF. This massive growth in electricity demand will require huge expansion in energy infrastructure. The growth will be characterised by the decentralization and digitalization of energy networks.

There are several trends favouring solar.

The cost of solar energy equipment has fallen dramatically in the last ten years,

Solar energy is suitable for a large part of the earth.

Global restrictions on carbon emissions driven by the need to combat climate change favour solar.

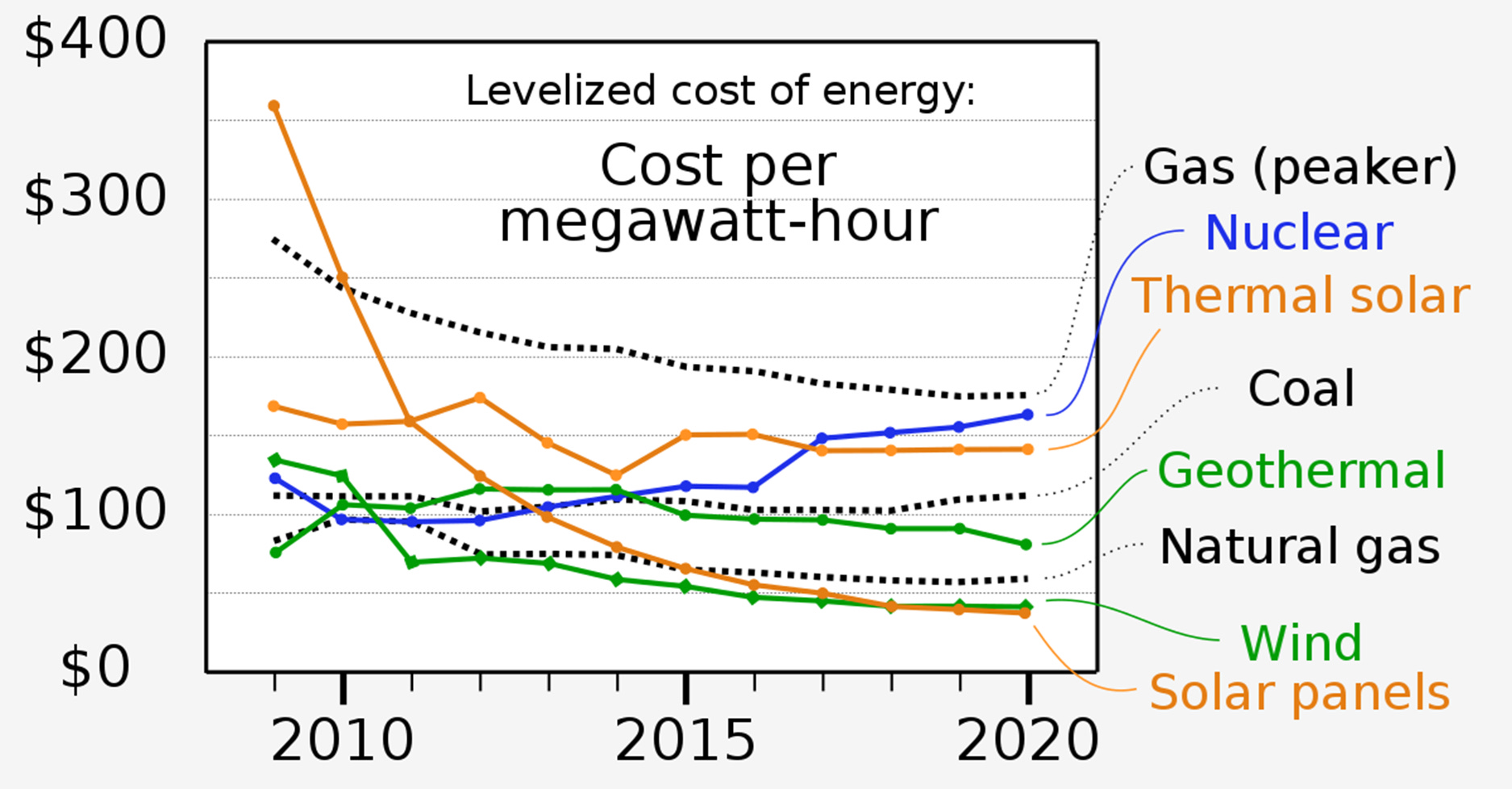

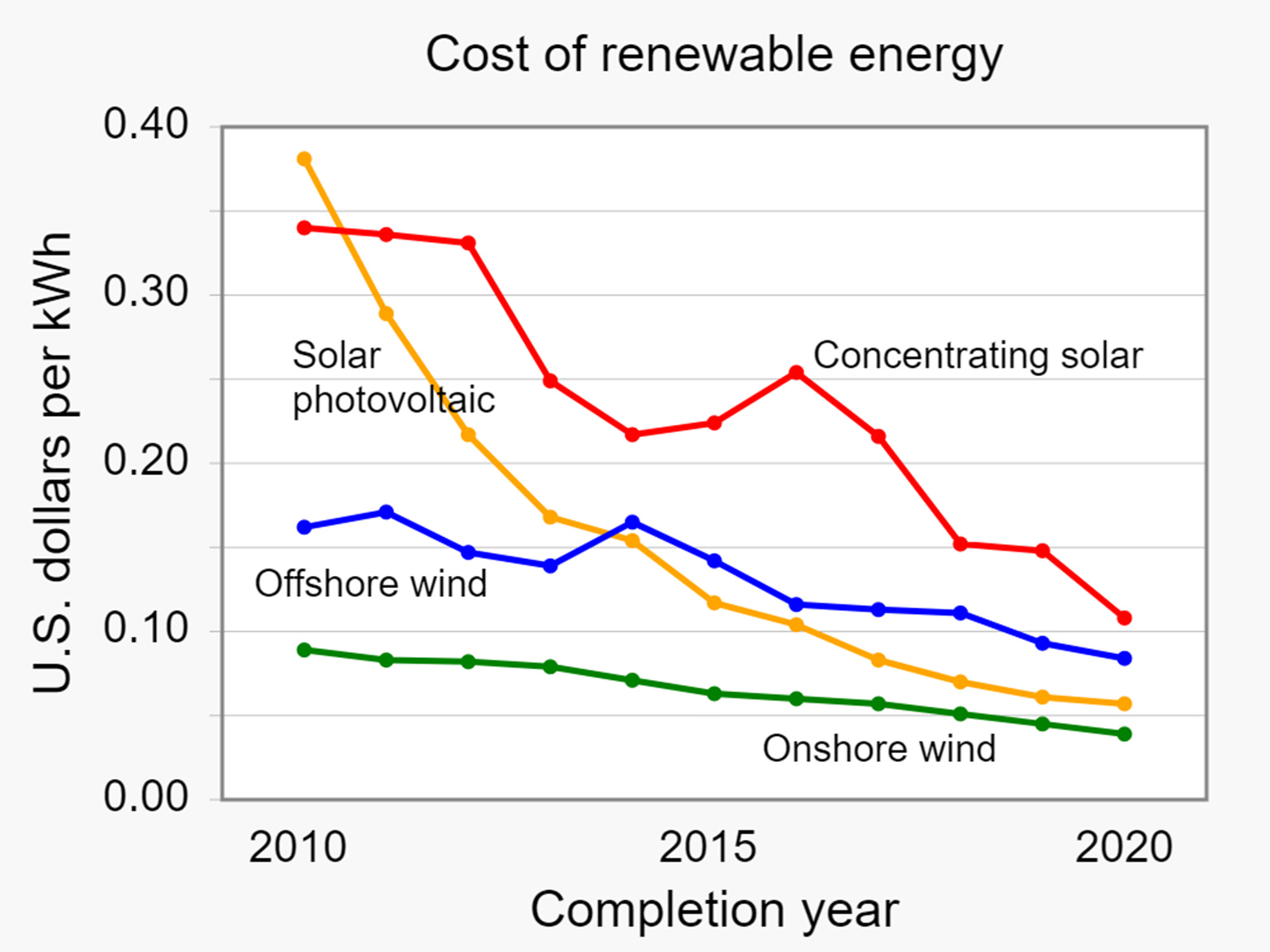

Levelized cost of electricity (LCOE) calculates the cost (initial investment, O&M, cost of fuel, cost of capital) of generating electricity and is the price at which the generated electricity should be sold for the system to break even. LCOE is often used to compare different energy- producing technologies.

As the charts below show, LCOE has fallen by 70% for renewables including solar over the last 10 years and is now the lowest cost source of new-build utility-scale power in countries that comprise 90% of global electricity generation. Only onshore wind is cheaper than Solar power and the difference is small. The projections for costs are dramatic. For example, a Indo-US study found the cost of solar power in India is likely to fall to Indian Rupee 1.9 per unit - about 2 pence or 3 cents per kw/h. As a comparison in 2023 in the UK in the middle of an energy crisis, I pay 31 pence per kw/h.

Improvements in solar design and efficiencies in production of Photovoltaic cells have underpinned sharp cost declines for the last two decades. Developers and installers have also gained valuable operating experience through the years while financing costs have declined as financiers and lenders have become more comfortable with the technologies and risks. In the last year, the gap between fossil fuels and renewables has continued to widen, with the driver being the rising prices of gas and coal due to the invasion of Ukraine.

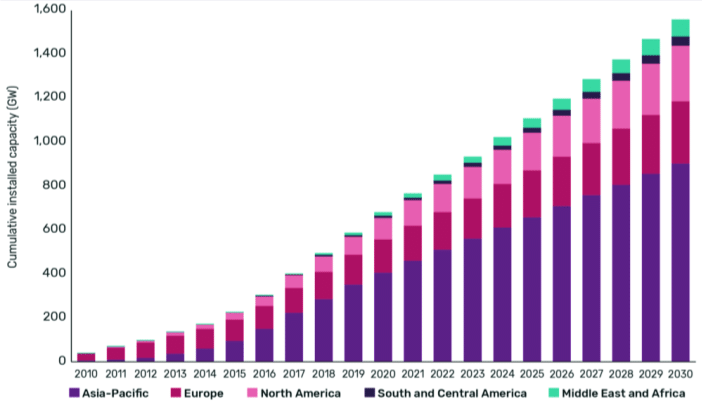

Global Solar Installed capacity

Source: ResearchGate.

Solar capacity has grown strongly in the last decade and this is expected to continue through to 2030 with most of the growth coming in the Asia- Pacific. ReseachGate expect total cumulative solar installed solar capacity to rise to 1600 GW. This compares with current total global capacity of 800 GW (CAGR of 9%). The ResearchGate forecast is underpinned by the stated plans of various countries or regions

In the US, annual solar capacity additions have grown rapidly in the last decade and doubled in the past two years (35% CAGR). Momentum has accelerated with declining costs, regulatory support, and increased public support for clean energy initiatives, and bringing total solar capacity installed to ~115 GW by the end of 2020. Solar has accounted for 50% of new US electricity-generating capacity additions since 2018. The 33% CAGR in solar installations over the last decade is attributable to strong federal policies and tax credits, rapidly declining costs, and increased demand from a more energy-conscious population.

There will be a huge growth in Solar investments in the next decade. This will lead to greater demand for Inverters and Power Optimisers. The chart above is from 2020 and suggested the inverter market could double in the five years to 2025 with the bulk of the growth coming from Asia Pacific

Renewable energy has low marginal costs and is relatively unlimited by physical constraints. The main problem with renewable is intermittency – what is the power source when the wind does not blow, and the sun does not shine? There must be enough baseload capacity in the form of traditional sources such as Coal, Gas and Nuclear and greater investment in battery and storage capacity.

Enphase Energy, Inc (ENPH)

Key facts

Founded In 2006, with 2,834 employees as of Sept. 30, 2022

Headquartered in Fremont, California with offices globally.

Customers are installers, homeowners, and module partners.

More than 1,200 installers in the Enphase Installer Network (EIN) as of Sept 2022

More than 52mnmicroinverters shipped, representing approx. 17 GW capacity.

There are more than 2.7 million systems in more than 145 countries.

Key Data (as of (9 March 2023)

Company Description

Enphase Energy is a global energy technology company that designs, develops, manufactures, and sells home energy solutions that manage energy generation, energy storage, and control and communications on one intelligent platform. It currently offers solutions targeting the residential and commercial markets in the US, Canada, Mexico, Europe, Australia, New Zealand, India, Brazil, South Africa, and certain other Central American and Asian markets. Enphase Energy has shipped more than 25 million microinverters, and approximately 2.1 million Enphase residential and commercial systems have been deployed in more than 130 countries. The company generates most of its revenue in the US (80%).

The Enphase offering is a Microinverter based system.

The basic system consists of four components:

Enphase microinverters,

AC Battery,

an Envoy gateway and

Enlighten cloud-based software.

Enphase IQ7+ Microinverter is the recent iteration of their core product. The company’s microinverters have a ASIC chip. As noted above one of these is attached to each Solar Panel.

The generated electricity is monitored by the Envoy™ Communications Gateway with IQ Combiner which is combined with Enphase Enlighten, a cloud-based energy management platform ( below) . These provide users with the ability to monitor the output of the solar installation in great detail An App on my phone allows me to look at data on all the electricity generated since the system when the system went live. It also has a cool feature which shows how any trees the system has saved since inception.

Enphase IQ7+ Microinverter

Enphase IQ Envoy Unit

Enphase IQ 10 Battery

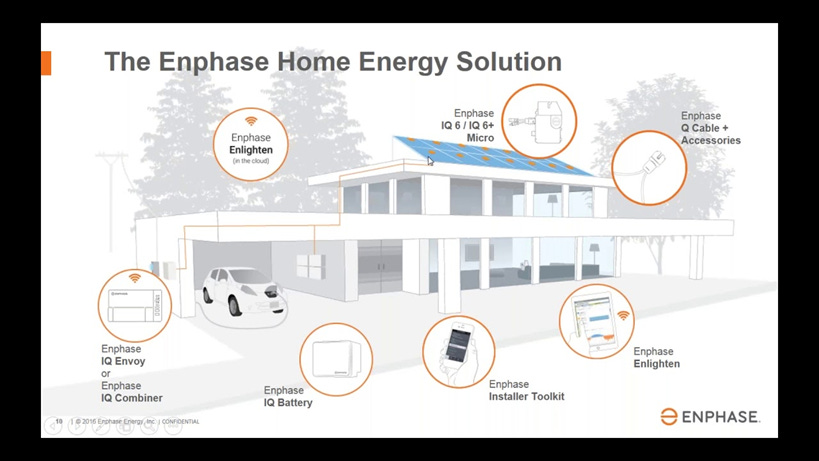

These units are part of the broader Enphase Energy Management System (EMS) called the Enphase Home Energy Solution which is shown below:

Enphase uses a single technology platform for seamless management of the whole installation and operation of solar system. It includes:

The Installer Toolkit™ - This is a software package for installers which allows them to design, plan and manage the proposed installation to the end-user. It plays an important role in explaining the proposed installation to buyers and in enabling the rapid installation of the agreed system

Envoy™ Communications Gateway with IQ Combiner+plus Enphase Enlighten, a cloud-based energy management platform.

Enphase AC Battery™. - battery for storing generated power.

Chargers for charging Electric Vehicles (EVs).

The EMS allows for remote firmware and software updates, enabling cost-effective remote maintenance and ongoing utility compliance. System owners monitor their solar generation, energy storage and consumption from any web-enabled device. The company has 350 patents relating to their products and software. The company designs products and software but manufacturing is outsourced to five contract manufacturers with whom the company has long standing relationships.

In line with the industry, the company has pivoted from being a provider of solar-linked products to a supplier of holistic Energy Management Systems. This means a much greater emphasis on battery which are a very high-cost, high revenue item.

Enphase Energy targets the residential and commercial markets. The company sell directly to large installers, OEMs and strategic partners.

OEM’s integrate the company's microinverters with their solar panels. and resell to both distributors and installers.

Enphase also targets installers directly. In 2021, one customer accounted for about 35% of total net revenues. This is thought to be ADT Corp. Other large customers are Commonwealth of Australia, Caisse de depot (France),Baywa and Centrolsolar in Germany, Green Mountain Power (Vermont) Solar Integrated Roofing (SIRC), SunRun (RUN) (second largest installers of residential solar energy systems in the US), Maxeon Solar Technologies (MAXN) in Singapore and so on.

The company has a Capex lite model as it is not involved in manufacturing. It outsources the manufacturing of its products to 4-5 contract manufacturers with whom it has long-standing relationships. The manufacturers include Flextronics International Ltd., and Phoenix Contact GmbH & Co in Germany. Manufacturing locations include China, India, the Far East, Romania and Mexico- low cost manufacturing locations close to particular large markets. ENPH currently has capacity to produce over 6 million microinverters on a quarterly basis - 2.25 million microinverters in Mexico, 1.5 million in India, and the remainder in China. Current plans are to expand this to 10mn. For battery manufacture, ENPH has two sources for their battery cell packs.

The company also claims their business model is Operational expenditure lite. 55% of the headcount is based in lower cost India and only 33%in USA (with 5% in Australasia and 4% in Europe).

Strategy;

Key elements of Enphase stated strategy include:

Achieve best-in-class customer experience.

The company's value proposition is to deliver products that are productive, reliable, smart, simple, and safe, and superior customer service, to enable homeowners' storage and energy independence. On the service front, its installer, distributor, and module partners are the company's first line of association with its ultimate customer, the homeowner and business user. Enphase's goals are to partner better with these service providers so that it can indirectly provide exceptional high-quality service to the end-customer.

Grow market share worldwide.

Enphase intends to capitalize on its market leadership in the microinverter category and its momentum with installers and owners to expand the company's market share position in its core markets. Enphase also intends to increase its market share in Europe, Asia Pacific, and Latin America regions. In the medium term, the company intends to expand into new markets, including emerging markets, with new and existing products and local go-to-market capabilities.

Expand the company's product offerings.

Enphase will seek to invest in research and development to develop all components of its EMS. This reflects the commitment to providing customers and partners with best-in-class power electronics, storage solutions, communications, and load control all managed by a cloud-based energy management system. This means the company will offer a holistic energy management solution and capture revenue of up to US$10,000 per home (assuming 10kWh battery system at ~$800/kWh) versus US$2,000 for a solar centric solution without battery storage. There is significant scope to increase revenue per customer in residential solar.

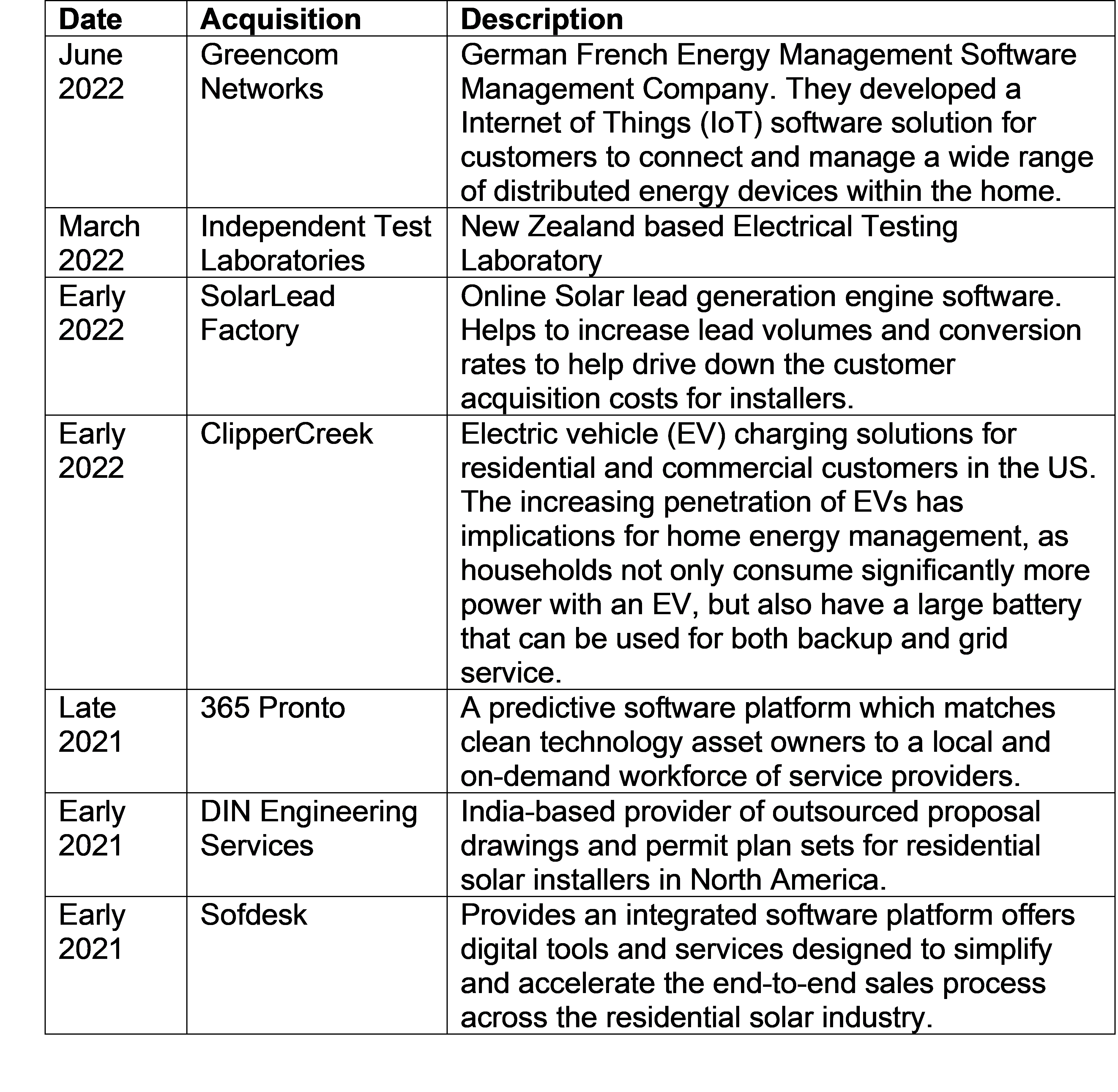

The company has built up the components of its EMS either through in-house R&D (especially the core microinverter products) or through acquisitions (mainly software and EV charging solutions). Some of the key acquisitions in the last three are shown below :

Enphase Summary Financial Statements

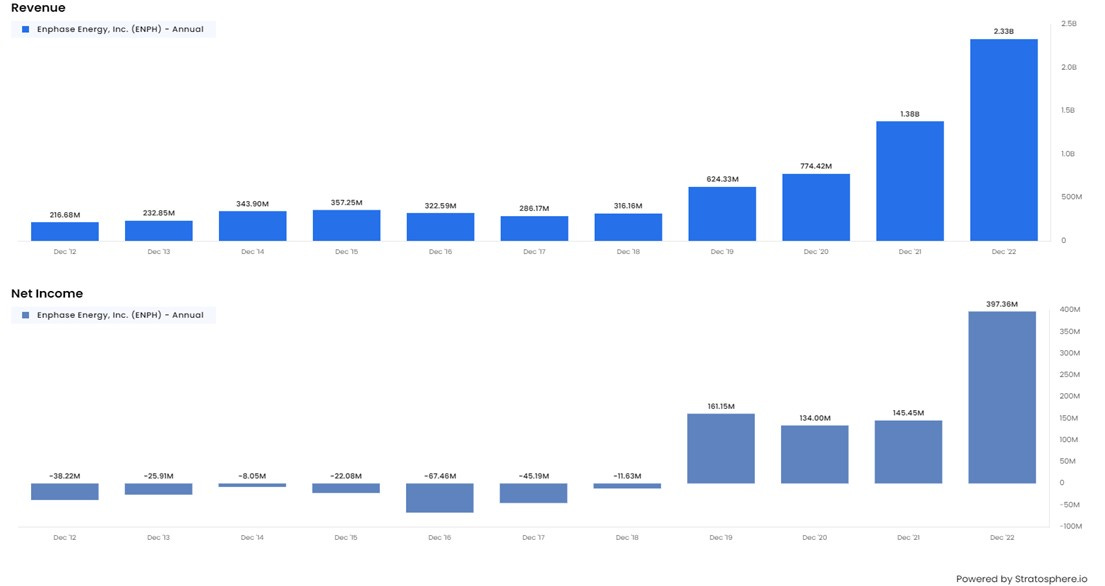

Summary Income Statement

All units in US$ million unless stated otherwise

Enphase revenues have increased tenfold from US$ 232mn in 2013 to US$ 2.3bn in 2022. Over the same period, Net income has risen from US$ -25.9mn to US$ 397mn. The company has been profitable at the net level since FY 2019

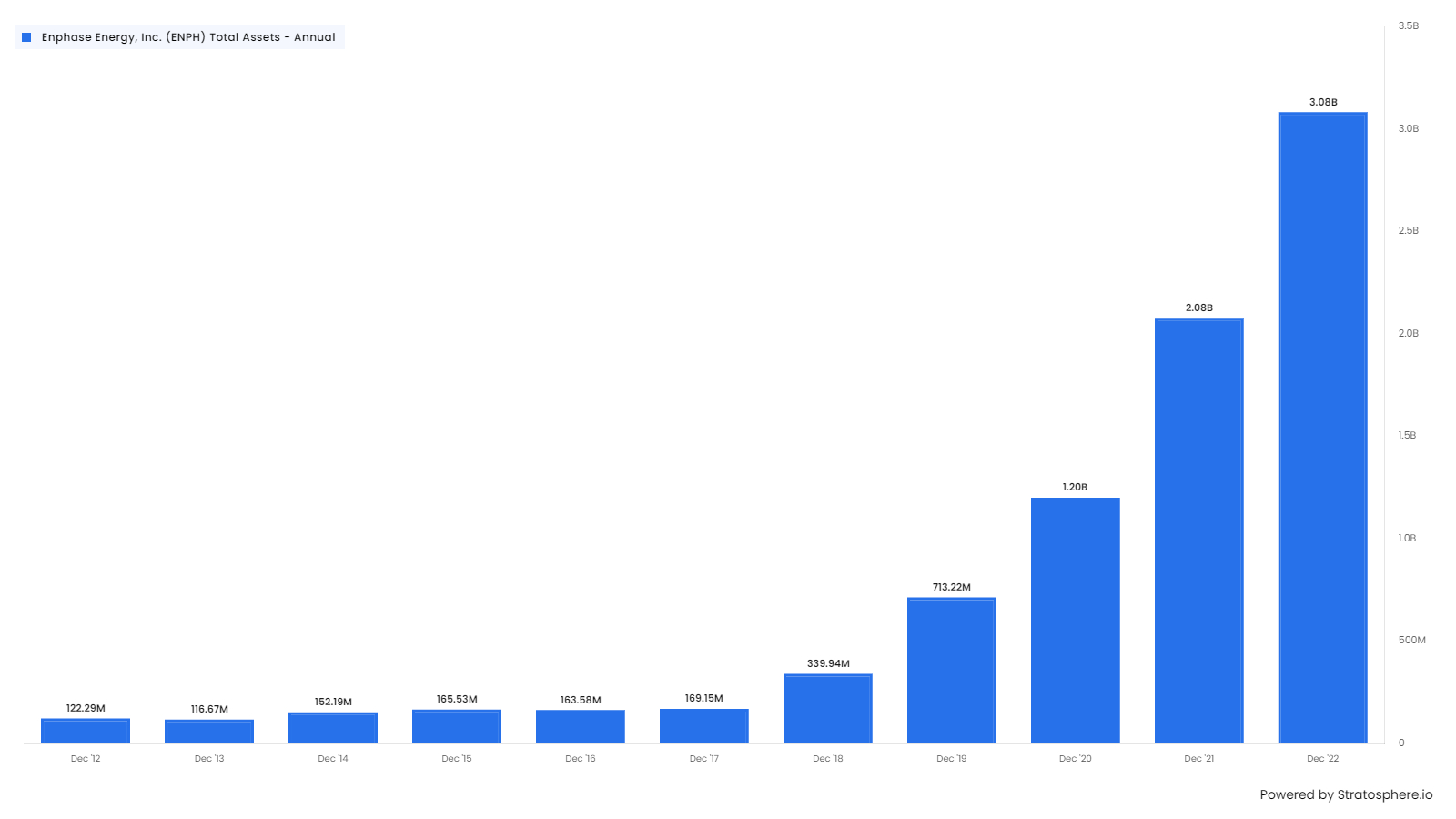

Summary Balance Sheet

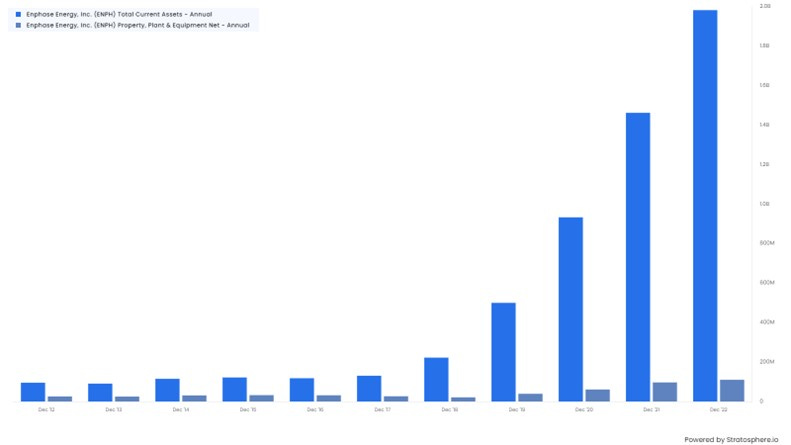

Enphase total assets have grown from just US$115mn in 2013 to 2,264mn in 2022.

In 2022, Property Plant and Equipment was only 132mn or less than 5% of total assets which reflects the capital lite nature of their business model.

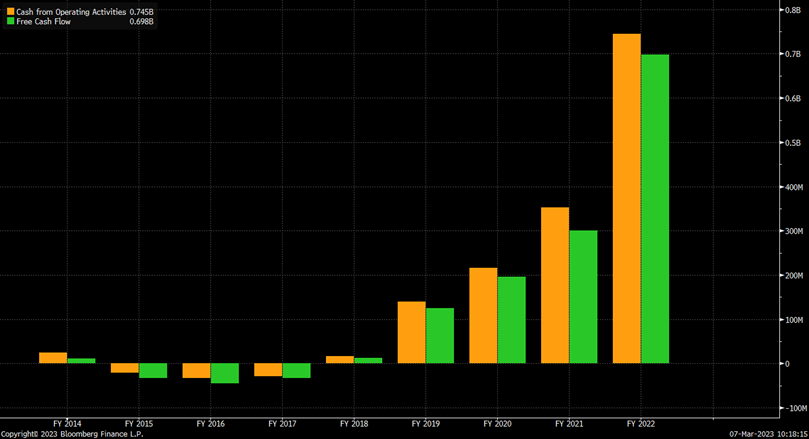

Cash flow from operations increased from just US$ 24mn in 2014 to US$ 744mn in 2022. This is shown below.

Enphase Energy: Cash Flow from Operations and Free Cash Flow 2014 to 2022

Source Bloomberg

As the above chart shows, most of the Operating Cash Flow is converted to Free Cash Flow due to the relatively low Capex required. This reflects the Capex-light business model.

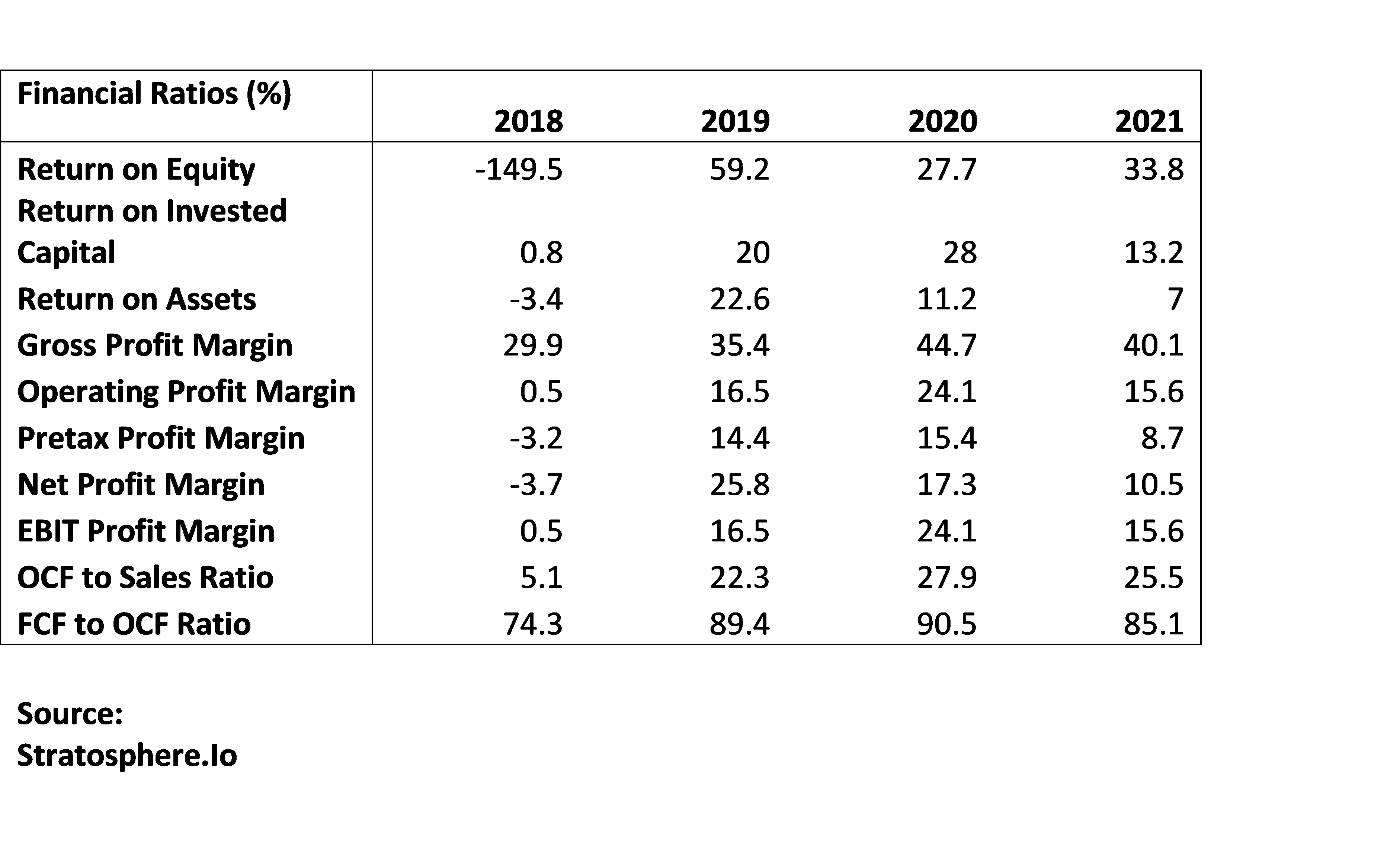

Some Financial Ratios (%)

In 2021, Enphase Energy had a Return on Equity of 33.8%, Gross Margins of 40.1%, Operating Margins of 15.6%. 25.5% of revenue was converted to operating cash flow and 85% of Operating Cash Flow (OCF) was converted Free Cash Flow (FCF).

R&D and innovation

The company’s core strength is R&D. Over 30% of the employees of the company work in R&D, product design and engineering. The company has used R&D to launch new, improved products and cut costs significantly in response to competition and deflation in the industry.

Enphase has launched the 8th iteration of their microinverter, the IQ8 which allows homeowners to make and use their own power even during a power outage even if they do not have a Battery. Its predecessor IQ7A greatly increased the power of the Solar Panels that it could be combined with. For emerging markets. Enphase have developed an off-grid solar and storage AC inverter, switches, and battery in one box. This portable device is aimed at Indian farmers and can be used to power solar water pumps in fields where there no electrical connection. Over 300 million people in Asia are living in energy poverty. Current solutions with DC systems are inefficient. The company estimates that this product represents a USD 4bn global market in developing economies.

Enphase has recently demonstrated a bidirectional EV charger technology combining vehicle to home, vehicle to grid and green charging functionality which can be changed depending on relative prices and consumer requirements.

Two factors which are likely to affect the short to medium-term prospects will be discussed in a little more detail.

1. Inflation Reduction Act (IRA)

2. New Feed-in-Tariff in California

Inflation Reduction Act (IRA)

The Inflation Reduction Act (IRA) which was passed in August 2022 directs US$ 400 billion in federal funding to clean energy, with the goal of substantially lowering the nation’s carbon emissions by the end of this decade. Funds will be delivered through a mix of tax incentives, grants, and loan guarantees. Clean electricity and transmission command the biggest slice, followed by clean transportation, including electric-vehicle (EV) incentives. It includes an extension of the investment tax credit (“ITC”) as well as a new advanced manufacturing production tax credit (“AMPTC”), to incentivize clean energy component sourcing and production, including to produce solar related components, battery cells and battery packs.

The ITC was extended by the IRA until 2032 and allows a qualifying homeowner to deduct 30% of the cost of installing residential solar systems from their U.S. federal income taxes.

The IRA provides for an AMPTC on microinverters of 11 cents per AC watt basis until 2030 at least. The IRA will boost Enphase business in two ways. The 30% ITC will increase the demand for residential solar power systems. It also applies to batteries and will encourage homeowners to retrofit batteries into existing residential solar systems. The AMPTC gives a benefit of 11 cents per watt which amounts to about US$ 35 for a 320 AC Watt Inverter. Enphase believes the net benefit for manufacturing inverters in the USA compared with Mexico will be US$ 20 to 30 per unit. They are currently looking into the possibility of beginning contract manufacturing in the US.

California

California has been an important Solar due to the size and wealth of the state, the abundance of sunshine and the magnitude of state incentives. About 1.5 million California homes and businesses have solar systems with a capacity of more than 12,000 megawatts of renewable power, or the equivalent of 12 nuclear reactors. According to Bloomberg NEF, the Golden State accounts for about one-third of all US residential capacity installed Top states for the residential market are CA, FL and TX and they account for about 50% of installed capacity.

In addition to Federal incentives such as IRA noted above, California has certain additional State incentives for solar. The Self Generation Incentive Programme (SGIP) provides 15% to 20% financial rebate for using battery storage. The state allows a property tax exclusion for qualifying new solar installations. In addition three large utility companies in California, Pacific Gas & Electric (PG&E) or Southern California Edison (SCE) and San Diego Gas & Electric (SDG&E) give homeowners credits for the extra electricity generated by their solar panels. This is called Net Energy Metering (NEM). These programmes date back two decades. Enphase have indicated that California accounts for 20% of their revenue.

In December 2022, the California’s Public Utilities Commission (“CPUC”) approved and voted for a new net metering policy, called Net Energy Metering 3.0 (“NEM 3.0”), which will be in effect starting April 15, 2023. NEM 3.0 is expected to reduce the average export rate in California to US$0.05/kWh to US$0.08/kWh compared to current average of $0.25/kWh to $0.35/kWh. This is a substantial reduction. It increases the payback period for a solar installation and could reduce demand for solar PV systems, including future microinverter sales. However the NEM 3.0 makes using the solar generated electricity more attractive than exporting it to the Grid. This should result in more demand for batteries both for new projects and for retrofit. Batteries are expensive and represent a substantial up-front cash outflow for the homeowner but the 30% tax credit and the improved payback period for the battery should support demand for batteries. The changes to NEM 3.0 were made with the specific aim of encouraging more battery installation.

Enphase Energy Inc : SWOT Analysis

Strengths

Solar Power is likely to grow strongly over the next few years due to much lower cost compared to alternatives, the global abundance of sunshine and the pressing challenges of climate change.

Enphase is a leading player in an important niche with a strong position in the US market and a growing position in the rest of the world.

The company has a long history of product innovation which should continue to be a feature and will help them to gain market share.

The company is trying to change from a solar provider to a holistic energy management solutions provider which implies a grater emphasis on storage and batteries which are much higher value items compared with Inverters or Solar Panels.

The company has foothold outside the Untied States and should benefit from the fact growth in the next decade is likely to be higher outside the US.

The company has a Capex lite and an Opex lite business model. This is due to the outsourcing all manufacturing to contract manufacturers and the offshoring of some R&D and operations to India.

Weaknesses

The company is several players in the market for microinverters, batteries, and energy management systems. Enphase may not have any significant competitive advantage over the competition.

Opportunities

The global growth in solar power will lead to a greater demand for Energy Management systems in the residential, commercial and small-scale Utility space and Enphase is well placed to take advantage of this demand.

Electric Vehicle Owners are more likely to install residential solar systems. The popularity of electric vehicles will boost solar demand.

New products such as the solar water pumps for farms could be another growth vector

Threats

Competition is likely to intensify as the strong demand prospects for the industry could attract many new entrants. Enphase’s strengths in R&D, Innovation and Product Engineering might not prove to be as strong a competitive advantage as ii has in the past.

The changes to NEM 3.0 in California could have a significant negative effect on the demand for residential solar there which many only be partially offset by higher demand for batteries.

Much of the future growth in demand will be in the Asia-Pacific region especially in China. Enphase may be at a disadvantage relative to local firms such as Huawei and less able to compete with them.

Many buyers finance solar systems investment by borrowing. Higher interest rates as the Fed has tightened monetary policy significantly may lead to lower demand.

Valuation

We believe the foregoing has shown that Enphase Energy is an interesting company. It is a worthy candidate for inclusion in watchlists of long-term investors. Interested readers should do more research on the company.

We have decided to do a very quick and dirty DCF valuation of the company. This requires a number of assumptions about a number of metrics including future revenue growth and operating cash flow margin etc. There is some debate about the utility of valuation models. A large number of assumptions have to be made and the final result is very sensitive to the exact parameters chosen It is very much case of garbage in – garbage out (GIGO). Given this large health warning, we prepared a basic Levered DCF calculation of the value of the shares of Enphase Energy.

The output of the model is a fair value of US$ 200 for shares compared with the current market price of US$ 215. Given the shortcomings of the approach noted above, one should think about a range rather than a point valuation. It might be useful to think of this as US$ 178 and US$ 210. I would be looking for an entry price at some significant discount to US$ 178 per share and do further research in the meantime.

Solaredge Technologies (SEDG)

Key facts

Founded In 2005 in Israel and listed on the Nasdaq in 2015.

Produces and sells DC Inverters, Power Optimisers, Batteries, and products for solar systems.

Headquartered in Israel with offices globally with 4360 employees.

Customers are installers, homeowners, and module partners.

More than 94 Mn power optimisers shipped, representing approx.16 GW generating capacity in more than 133 countries.

Has sold systems in more than 133 countries.

Key Data (as of 9 March 2023)

Company Description

SolarEdge was founded in 2005 in Israel and listed in Nasdaq on 2015. The company tackles the same market as Enphase Energy but has focused on a slightly different approach.

Traditional Solar Systems with String inverters do not work to their capacity if one or more of the panels are overlooked by an obstruction and suffer shading. The Enphase solution was to develop Microinverters which were attached to each panel. The SEDG approach shown below involves power optimisers attached to each sola panel and a DC optimised inverter replacing the string inverter. The two diagrams below show a stylised version of both approaches.

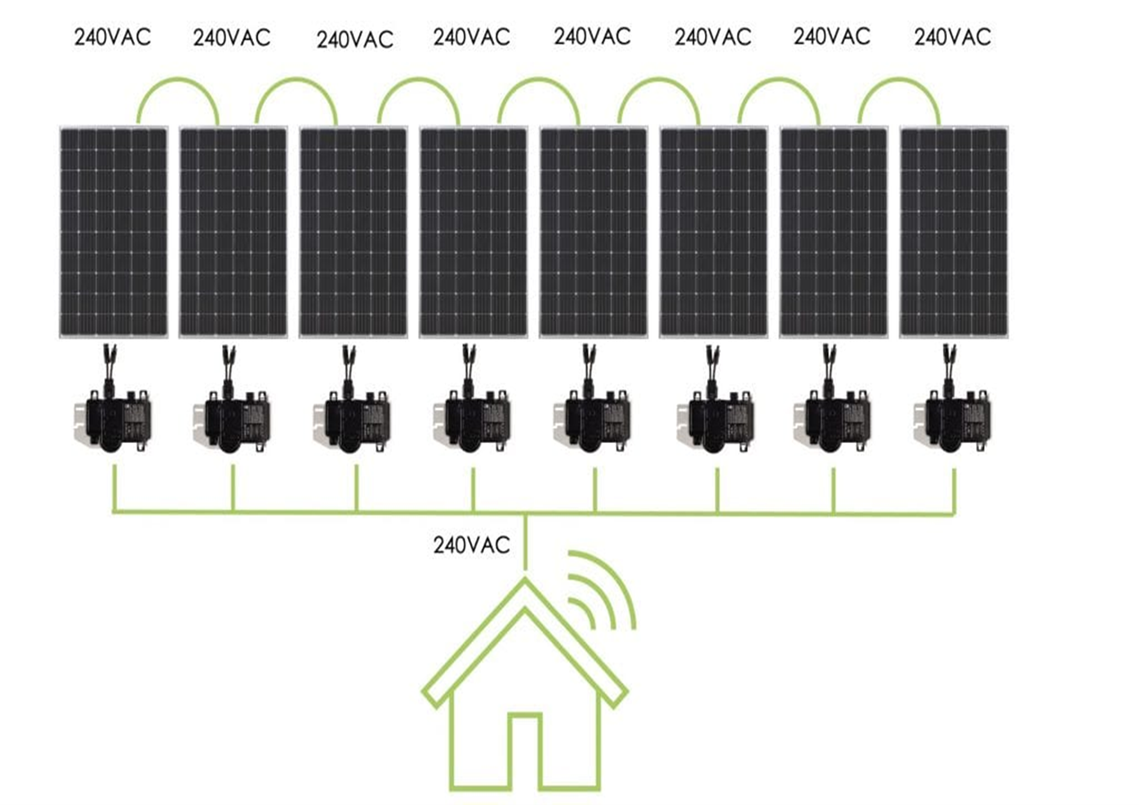

Stylised view of Enphase of approach in a 8 panel residential solar installation. Power optimisers are attached to each Panel and 240 volts of AC is delivered to the house

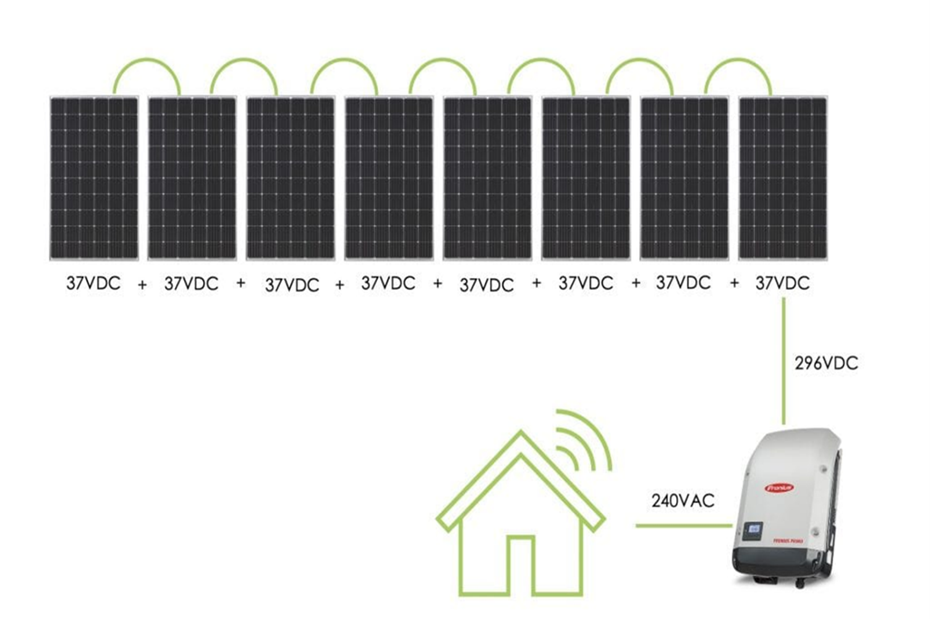

Stylised view of SolarEdge approach in a 8-panel residential solar installation. Power optimisers are attached to each Panel and each panel delivers 37 Volts of DC per panel (total of 296 Volts of DC) to the SolarEdge String Inverter. The latter ensures that 240 volts of AC is delivered to the house. The final result is the same. I searched online for articles where specialists comparing the products of the two companies.

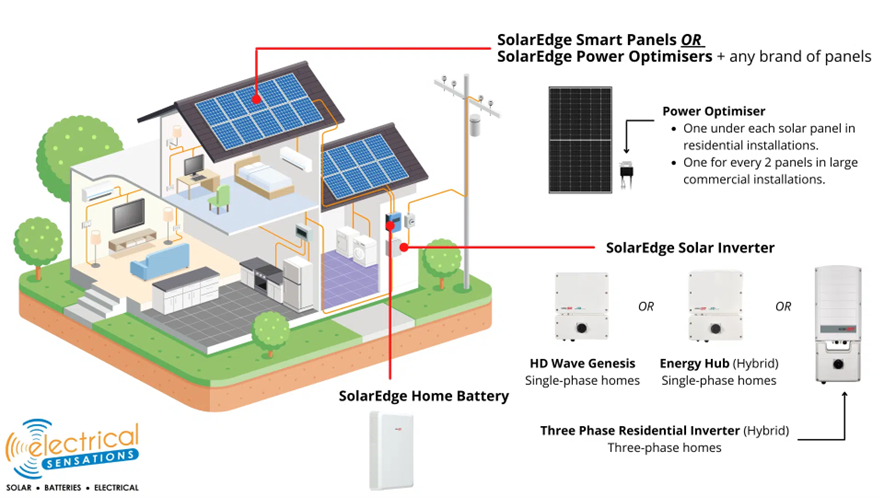

This is a good example for the UK. https://nrgcleanpower.com/learning-center/solaredge-vs-enphase/ . In general, they conclude there is not much to choose from Solaredge products have a slight the edge on reliability while Enphase products are slightly better for scaling up systems. Like Enphase, SolarEdge is moving from a solar provider to a holistic energy management system provider. A diagram of thelatter is shown below:

SolarEdge 5kw Single Phase HD Wave on grid solar Inverter

Screenshot of mySolarEdge - a mobile app for system owners

SolarEdge also has offices and lab facilities in California, Nevada, Germany, Netherlands, Italy, France, Australia, UK, Japan, Turkey, India, Bulgaria, Belgium, Taiwan, Korea, Vietnam and China as well as an R&D and call-center in Bulgaria.

SolarEdge primarily sells its products indirectly to thousands of solar installers through large distributors and electrical equipment wholesalers and directly to large solar installers and engineering, procurement, and construction firms (EPCs). Two customers Consolidated Electrical Distributors Inc. (CED) and Sunrun Inc. (RUN) represent around 30% of the company's revenues.

Consolidated Electrical Distributors, Inc. (CED) Is a unlisted US wholesalers of electrical systems and equipment. It sells to residential, commercial, industrial facilities, and factories. Solar products represent a small part of its total revenue. Sunrun is large solar installer in the US which is active in 20 states with an installed capacity of 4,600 MW.

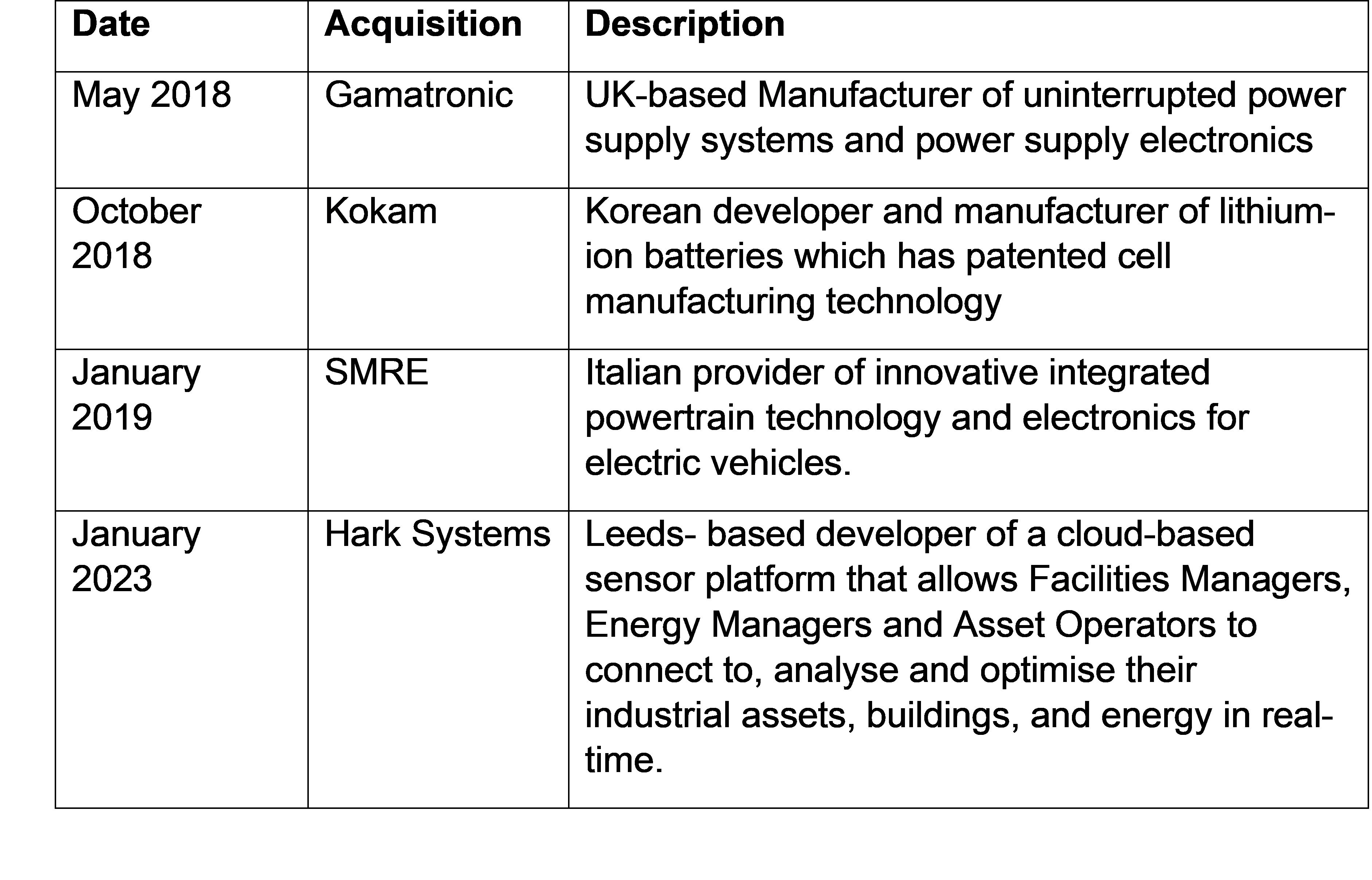

Like Enphase, SEDG has completed some (small) acquisitions in recent years which address growth in areas of smart energy technology and power optimization. Some these are listed below:

SolarEdge had 348 issued patents, world-wide and 266 patent applications pending for examination. Most patents relate to DC power optimization and DC to AC conversion for alternative energy power systems, power system monitoring and control, and management systems. Patents are scheduled to expire between 2020 and 2036. In addition, Kokam in Korea has many patents relating to lithium-ion batteries and power storage.

SolarEdge Financial Statements

Source: Stratosphere.IO

All units in US$ million unless stated otherwise

SolarEdge Technologies revenues have grown from just US$ 79mn in 2013 to US$ 3110mn in 2022. The company has been profitable at the net level since 2015.

All units in US$ million unless stated otherwise

SolarEdge balance sheet has increased from US$ 49mn in 2013 to around US$ 4265mn in 2022 - a decade of very strong growth.

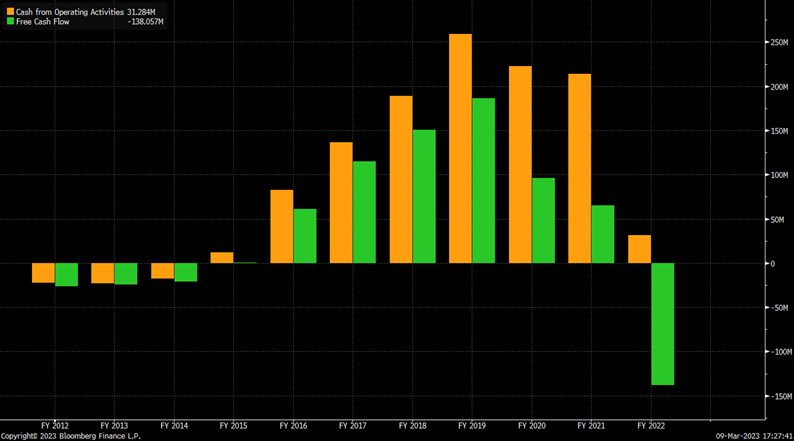

Summary Cash Flow Statement

The company has been free cash flow positive since 2015 and this has grown strongly until 2021. The reason for the decline in 2022 need to be investigated further.

The table above shows margins and profitability of SolarEdge have declined in recent years and the reasons for this needs to be investigated further.

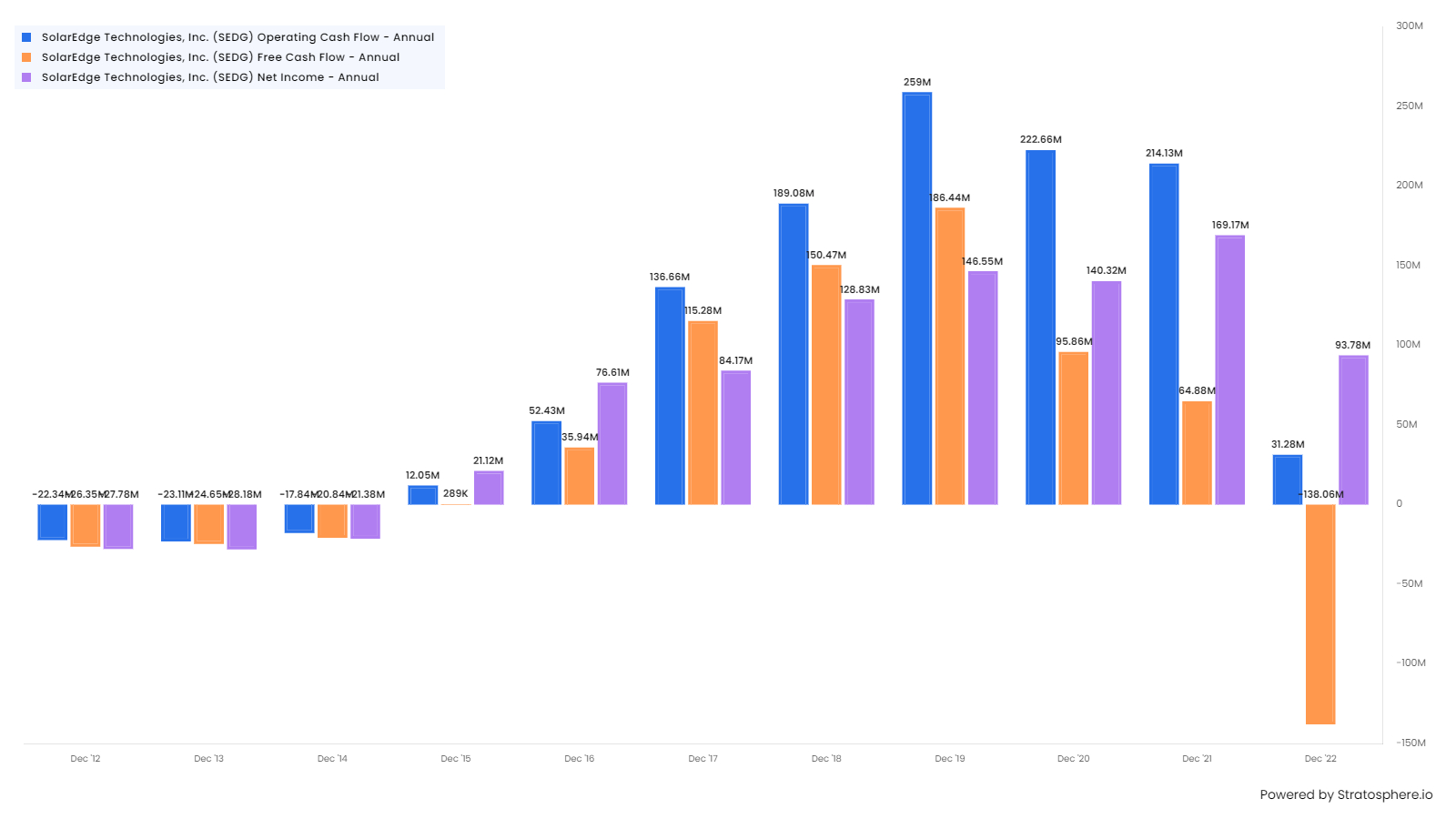

SolarEdge Technologies: Cash Flow from Operations and Free Cash Flow 2014 to 2022

The Chart above shows the Cash Flow from Operations and Free Cash Flow between 2012 and 2022. They both increased steadily between 2016 and 2019 but have declined since.

The reasons for this have to be investigated further.

Levered DCF Calculation for SolarEdge Technologies

As noted above, DCF Models should come with a big bag of salt and results should be treated with caution. This particularly applied to our effort which is very much a quick and dirty calculation.

Nevertheless, the model suggest that the fair value of the shares of SolarEdge are about US$ 281 per share compared with the current value of US$ 371 a share.

Although both stocks are currently overvalued, the difference appears to be much greater in the chase of SolarEdge Technologies

Differences between Enphase Energy and SolarEdge technologies.

Although there are a lot of similarities between the companies, there are some important differences. We can think about these by looking at some numbers for the two companies for 2021 as the SolarEdge numbers for 2022 were quite poor .

Enphase had lower sales in 2021 but had higher margins and is more profitable (higher ROE). Enphase is unsurprisingly more highly valued (higher price to sales and price to earnings ratios). There are several factors which may in a large part explain these differences.

Enphase Energy gets more of its revenue from the US market than SolarEdge Technologies. SolarEdge Technologies gets a higher percentage of its revenues from the United States. Safety rules are much higher in the US, making it harder for Chinese and European companies to compete. European markets are more competitive than the US and have lower profitability. As Enphase increases it sales in Europe, its average profitability is likely to decline as well.

Enphase has a lot of workers in low-cost India and this may in part explain why it has better margins.

Enphase Energy does not engage in Manufacturing and relies 100% on Contract Manufacturers. SolarEdge has a more hybrid approach and has announced it will invest more in manufacturing over the next few years especially in Kokam, its battery manufacturing subsidiary.

Plant, Property and Equipment (PPE) account for just 7.7% of Enphase’s balance sheet. The equivalent for Enphase is 20%

Conclusions

The Solar Industry is likely to grow strongly in the next two decades.

Enphase Energy and SolarEdge Technologies are both likely to grow strongly in the next few years

I believe the true value of a company is closely related to the Present Value of the future cashflows that the company can generate over its lifetime.

In this regard, Enphase Energy’s capital light model gives it a key advantage. SolarEdge will have to invest more and this will tend to depress its free cashflows.

We will continue to follow both companies closely.

Further Work

We will look more closely at Enphase Energy and build up a more detailed valuation model. In particular the Q1 Results for Enphase need to be looked at carefully.

We need to look at other potential investments in the Solar value chain such as installers (Sunrun Inc, Sunnova Energy) and specialist companies such as Array Technologies which makes solar Tracking equipment .