ExxonMobil (XOM)

Time to add exposure to Oil?

I started writing this note two weeks ago when the oil price was on a clear uptrend but before the Iranian attack on Israel which has led to a spike in energy prices.

A month ago, I read that the valuation of Nvidia was higher than all the companies in the main US Oil and Gas ETF. If true, this suggests that Nvidia is overvalued and/or Oil and Gas Companies are undervalued. Oil prices are on a rising trend as are other major commodities including Gold, Silver and Copper. Rising commodity prices will add to inflationary pressures around the world. This reduces the probability of, and the number of, interest rate cuts the Fed can implement this year.

Our portfolio only has 2% direct exposure to Oil & Gas through a position in Shell. We have some indirect exposure through Berkshire Hathaway which is our third largest holding, as the latter has investments in Occidental Energy and Chevron.

I decided to read the Annual Report (10-K) of an Oil Company for the first time. The company in question is ExxonMobil (XOM). We chose XOM as it is the largest Oil and Gas company in the USA.

This is like a long overdue piece of schoolwork. Many of you probably know more about the industry than I do. You may find much of what follows to be quite elementary.

ExxonMobil's is one of the largest, most integrated businesses of its kind among, with significant representation across the entire fuel value chain including refining, logistics, trading, and marketing.

Their principal business involves exploration for, and production of, crude oil and natural gas, manufacture, trade, transport and sale of crude oil, natural gas, petroleum products, petrochemicals, and a wide variety of specialty products.

Their business also involves the pursuit of lower-emission business opportunities including carbon capture and storage, hydrogen, lower-emission fuels, and lithium.

In October 2023, XOM entered into a merger agreement with Pioneer Natural Resources Company, an independent oil and gas exploration and production company. Pioneer has fields in the Permian basin, mainly in West Texas, USA.

XOM are expanding investments in lower-emission energy and emission-reduction services and technologies.

XOM has a long track record in the development of proprietary technology and holds over eight thousand active patents worldwide at the end of 2023. For technology licensed to third parties, revenues totalled approximately $155 million in 2023.

Over 60% of their global employee workforce of 62k is outside the U.S.

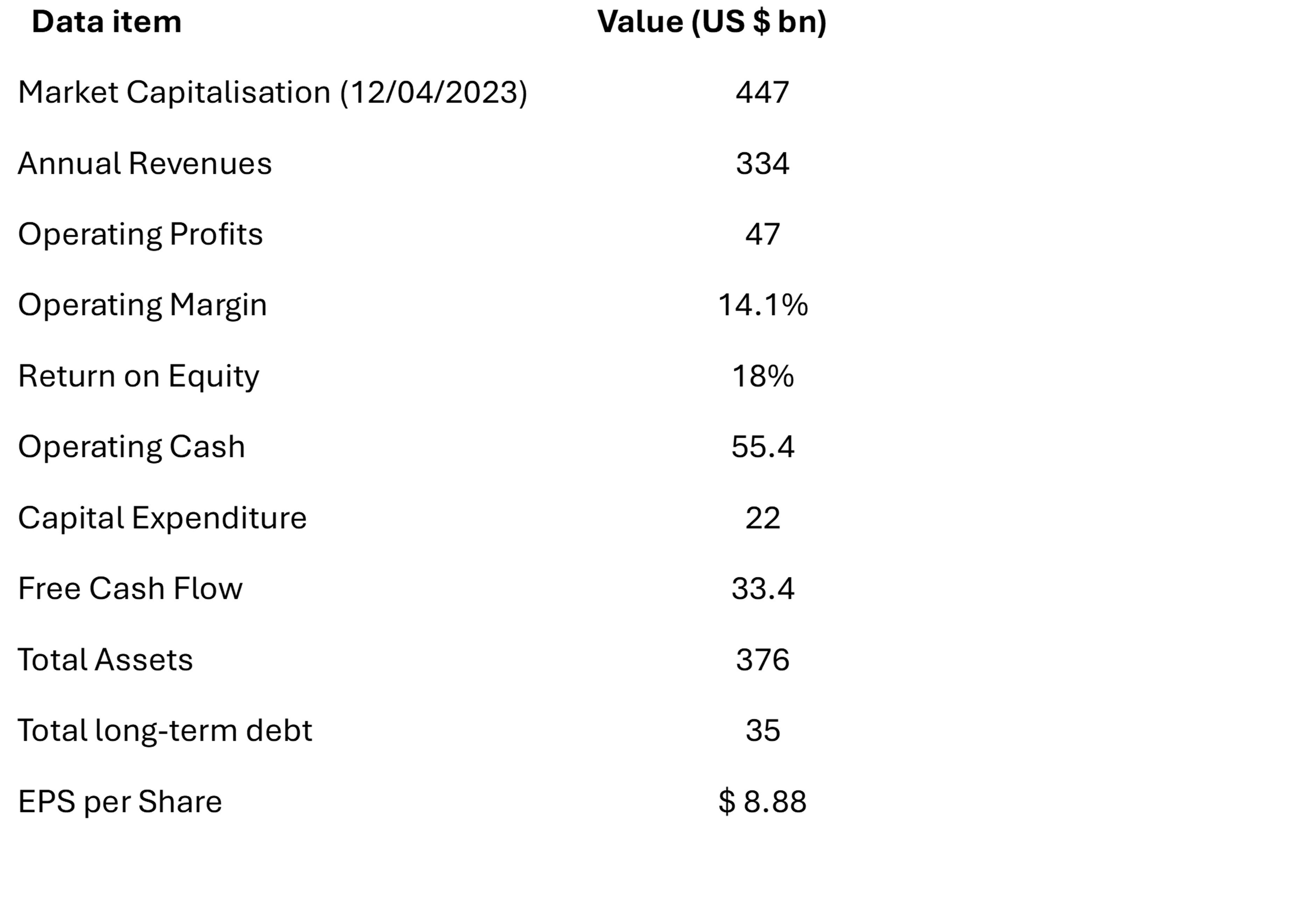

We present below some key financial statistics to get an idea of the scale of the company. These numbers are mostly at the end of 2023.

XOM: Selected key financial statistics at end 2023.

Revenues of $ 338bn and Free Cash Flow of $ 33.4 bn gives an indication of the substantial scale of this company.

Forecasting long-term Oil demand

The XOM Annual Report has a lot of space devoted to a model which forecasts oil demand in 2050. The key points are as follows:

By 2050, the world’s population is projected to be around 9.7bn people, or about 2bn more than in 2021, an increase of 28%.

Even with significant efficiency gains, global energy demand is projected to rise by 15% from 2021 to 2050.

This increase in energy demand is expected to be driven by developing (i.e. non-OECD) countries.

Increasing use of energy-efficient technologies and practices as well as lower-emission products will continue to help significantly reduce energy consumption and CO2 emissions per unit of economic output.

Substantial efficiency gains are likely in all key aspects of the world’s economy through 2050, affecting energy requirements for power generation, transportation, industrial applications, and residential and commercial needs.

Energy for transportation - including cars, trucks, ships, trains, and airplanes - is expected to increase by over 30% from 2021 to 2050.

Transportation energy demand is expected to account for more than 60% of the growth in liquid fuel demand worldwide over this period.

Light-duty vehicle demand for liquid fuels is projected to peak by around 2025, and then decline to levels seen in the early-2000s by 2050, as better fuel economy and growth in electric cars, work to offset growth in the worldwide car fleet of almost 70%.

More energy will be needed to power homes, offices, schools, shopping centres, hospitals, etc. Combined residential and commercial energy demand is projected to rise by around 15% through to 2050. Led by the growing economies of developing nations, average worldwide household electricity use will rise about 75% between 2021 and 2050.

By 2050, global demand for liquid fuels is projected to grow to approximately 110 million oil-equivalent barrels per day, an increase of about 15% from 2021.

The non-OECD share of global liquid fuels demand is expected to increase to nearly 70% by 2050, as liquid fuels demand in the OECD is expected to decline by more than 20 percent.

Natural gas is a lower-emission, versatile, and practical fuel for a wide variety of applications. It is expected to grow the most of any primary energy type from 2021 to 2050, meeting about 40% percent of global energy demand growth. Gas demand is expected to rise nearly 25% from 2021 to 2050, with more than 75% of that increase coming from the Asia Pacific region.

Significant growth in supplies of unconventional gas - the natural gas found in shale and other tight rock formations - will help meet these needs. In total, about 50% of the growth in natural gas supplies is expected to come from unconventional sources.

At the same time, conventionally produced natural gas is likely to remain the cornerstone of global supply, meeting around two-thirds of worldwide demand in 2050. Liquified Natural Gas (LNG) trade will expand significantly, meeting about two thirds of the increase in global demand growth, with much of this supply expected to help meet rising demand in Asia Pacific.

The world’s energy mix is highly diverse and will remain so through 2050. Oil is expected to continue as the largest source of energy with its share remaining close to 30% in 2050. The share of natural gas will grow growing to more than 25% percent by 2050, while that of coal will fall to about half that of natural gas.

The investments to develop and supply resources to meet global demand through 2050 will be significant and would be needed to meet even rapidly declining demand for oil and gas envisioned in aggressive decarbonization scenarios.

Conclusion on long-term demand

Overall demand for Oil and Gas will increase by 15% (esp. in developing countries) in the next 25 years. Oil will remain the most important part of the global energy mix.

Transportation demand will increase by 30%, despite the growth of electrical vehicles. While demand for light vehicle fuel will plateau, demand from, heavy vehicles, aviation, and shipping will grow.

Demand for gas will grow strongly as it is a low emission fuel. In terms of the energy mix in 2050, Oil is expected to account for 30%, Gas for 25% and Coal for 13%.

Huge investment will be required to find and develop new discoveries and rejuvenate existing assets.

The impact of Climate Accords and Emissions Targets

XOM’s policies and actions are heavily influenced by international climate accords. The company must work to reduce its emissions by 2030. Specifically in 2030, relative to 2016 levels, there should be a

•20-30 percent reduction in corporate-wide greenhouse gas intensity.

•70-80 percent reduction in corporate-wide methane intensity.

•40-50 percent reduction in upstream greenhouse gas intensity; and

•60-70 percent reduction in corporate-wide flaring intensity.

These substantial obligations reduce the company’s flexibility and constrain its strategic options.

XOM says they are working “to grow a pipeline of emission-reduction opportunities in carbon capture and storage, hydrogen, and lower-emission fuels, as well as lithium to supply the global battery and electric vehicle markets.”

XOM hopes to transform the emission reduction obligations into a business opportunity. A cost-efficient transportation and storage system has the potential to accelerate carbon capture and storage deployment for both XOM and third-party customers. They will offer lower emissions solutions they have developed for their own use, as a profit-making service to external customers.

Refining Margins

XOM’s earnings are closely tied to industry refining margins. Refining margins are driven by differences in wholesale oil prices and the price of refined petroleum products. They are sometimes known as crack spreads and are expressed in terms of US dollar per barrel.

Refining Margins are determined by demand and supply conditions in both the oil market and the refined products markets, as well as the operational efficiency (measured by conversion rate) of the refiner.

When the wholesale oil (a feedstock to the refinery) price fall, refining margins tend to rise. Margins tend to fall when feedstock prices rise. Suppose you have a refinery with a high conversion rate, operating in an area with strong demand for refined products at a time of falling oil prices. This refinery will tend to have high and rising refining margins.

Management commentary on refining margins

“In 2023, refining margins remained above the pre-COVID 10-year historical range (2010–2019) but started to normalize from their 2022 highs. Continued strong margins were supported by gasoline and distillate demand growth and relatively low inventory levels. “

“Refining margins will remain volatile with changes in global factors including geopolitical developments; demand growth; recession fears; inventory levels; and refining capacity utilizations, additions and rationalizations.”

In addition to refining margins, strong operational performance, product mix optimization, and disciplined cost control are also critical the financial performance.

Integrated companies talk about upstream and downstream. Upstream is the oil discovery and exploration and extraction. On the other hand, downstream refers to refining and distribution. Midstream (in the middle) refers to the transportation of Crude Oil. XOM is involved in the entire length of the Oil and Gas value chain.

XOM notes their upstream capital program continues to prioritize low cost-of-supply opportunities. XOM claims to have a strong pipeline of development projects including continued growth in Guyana and the Permian Basin (West Texas and New Mexico field), and LNG (Liquified Natural Gas) expansion opportunities in Qatar, Mozambique, Papua New Guinea, and the United States. XOM has stated it tries to keep its cost of oil below US$ 35 per barrel and recent discoveries in Guyana have been particularly helpful in keeping average costs at this level.

XOM expects a shift in the geographic mix and in the type of opportunities from which volumes are produced.

“Based on the current investment plans and merger with Pioneer, the proportion of oil-equivalent production from the Americas is generally expected to increase over the next several years.”

50% of production comes from unconventional, deepwater, and LNG resources. This proportion is generally expected to grow.

The company has been strongly focused on cost savings in recent years.

“Organizational changes implemented over the past several years enabled the Corporation to capture $9.7 billion of structural cost savings versus 2019, including $2.3 billion of savings during 2023, through increased operational efficiencies and reduced staffing costs.”

“The company sees additional opportunities in areas such as supply chain efficiency, improved maintenance and turnarounds, modernized data management, and simplified business processes. These savings are key drivers for further improving the earnings power of the Corporation.”

Petrochemicals

XOM is a leading manufacturer and marketer of petrochemicals.

“(XOM) is uniquely positioned with a combination of industry-leading scale, integration, and proprietary technology, which are fundamental to producing affordable products that are more sustainable, use less material, save energy, and reduce waste.”

In 2023, chemical industry margins remained bottom-of-cycle, below the pre-COVID 10-year historical range (2010-2019), as capacity exceeded demand growth. The company optimized production across our global footprint to profitably meet customer demand. Earnings benefited from the North American feed and energy advantage, strong reliability, and higher performance products sales.”

XOM’s Speciality Products division is a combination of business units that manufacture and market a range of performance products including high-quality lubricants, base stocks, waxes, synthetics, elastomers, and resins. It provides performance products that help customers improve efficiency in the transportation and industrial sectors.

Financial Summary

We will review some summary financial numbers for XOM.

Chart 1: XOM Annual Revenues 2014-2023

As the chart above shows, annual revenues can be volatile reflecting changes in Oil and Gas prices. Revenues fell from $ 401bn in 2022 to about $ 338bn in 2023. Conversely 2021 earnings were about $ 277bn. The volatility reflects price changes, as volumes are relatively stable on a year-to-year basis.

In 2023, XOM produced 2.4mn barrels of oil and 7.7bn cubic feet of natural gas daily. This is the equivalent of total production of 3.7mn barrels of oil per day. As a comparison, global demand and supply is about 104mn barrels per day. So XOM is responsible for about 2.5% of global production.

Breakdown of 2023 revenues of ~ $ 338 bn is as follows:

Source: XOM Annual Report

XOM is active in more than 70 countries and non-US revenues are higher than US revenues.

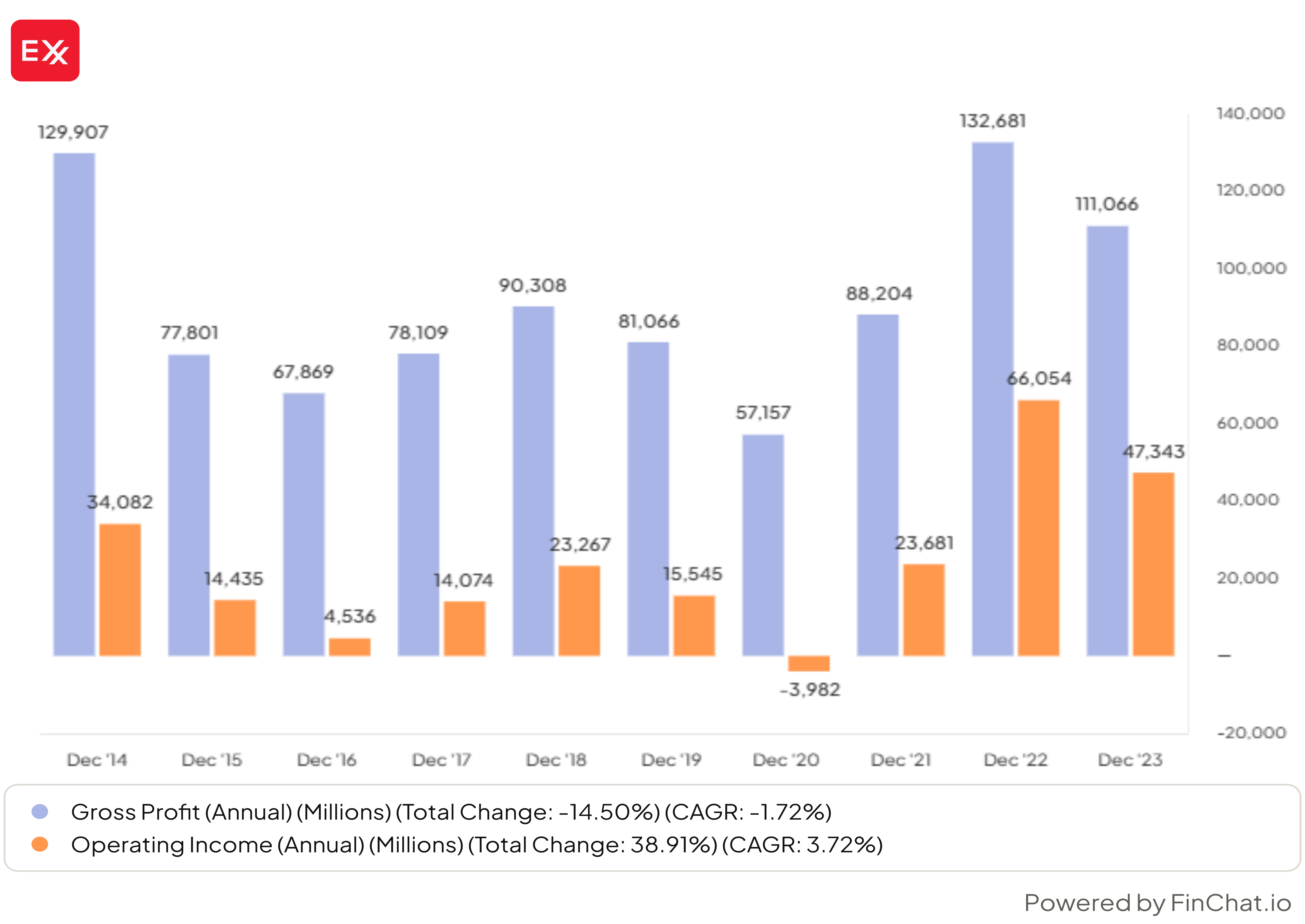

Chart 2: XOM Annual Gross Profit and Operating Income 2014-2023.

Despite the swings in Oil Prices, XOM has been mostly profitable in the last decade with the exception of an operating loss in 2020, during the Covid Pandemic.

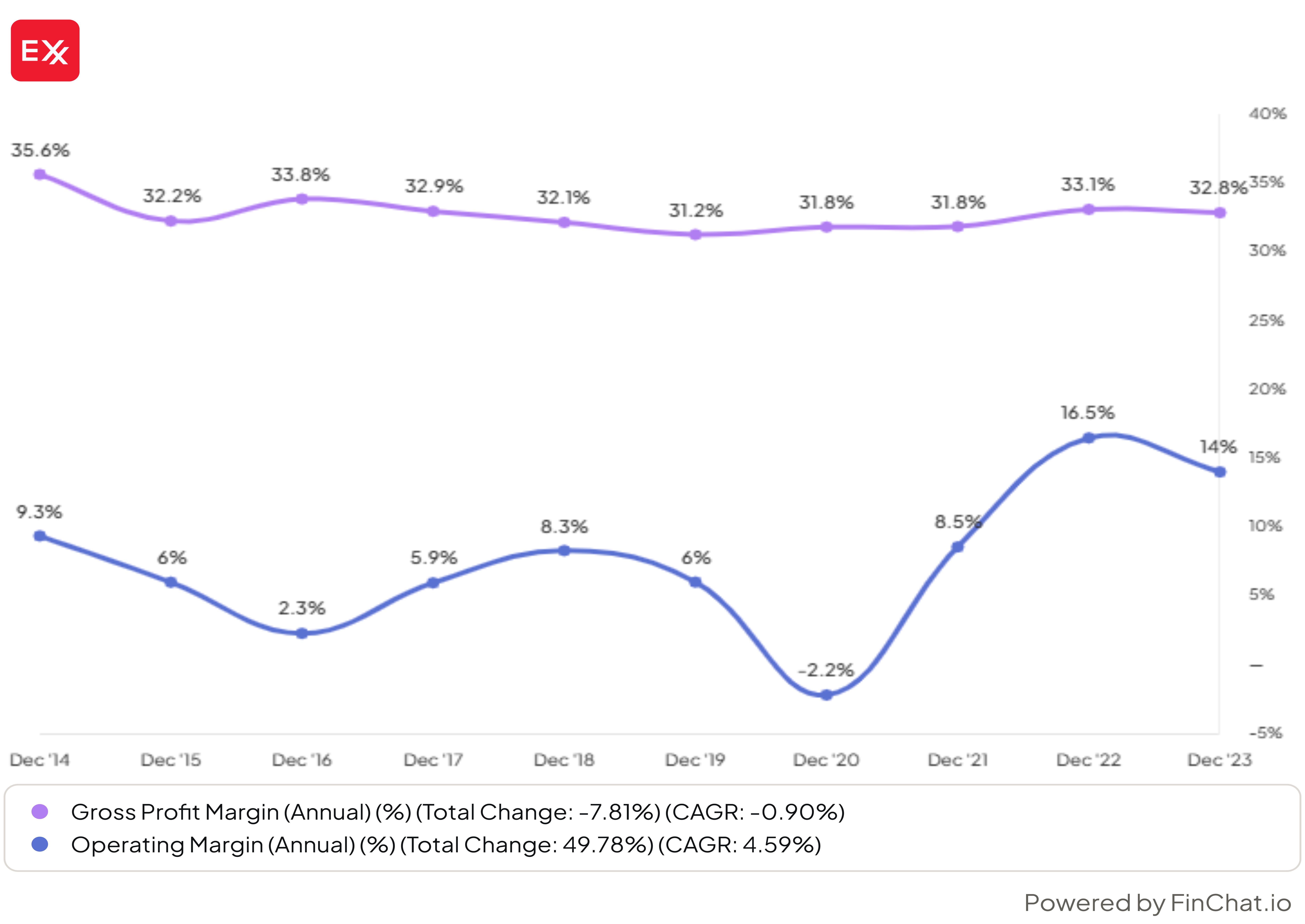

Chart 3: XOM Gross Profit Margins and Operating Margins. 2014-2023

XOM’s Gross Margins are consistently between 32% and 35% suggesting a strong ability to pass on price changes. Operating margins are more volatile as might be expected given high fixed costs and price changes.

Chart 3: XOM Returns on Invested Capital (ROIC) and Return on Equity (ROE) 2014-2023.

The profitability data above shows the variability we would expect given the above. If we ignore the Covid hit in 2020, ROE has been in a range of 4.5% to 29.5% in the last ten years.

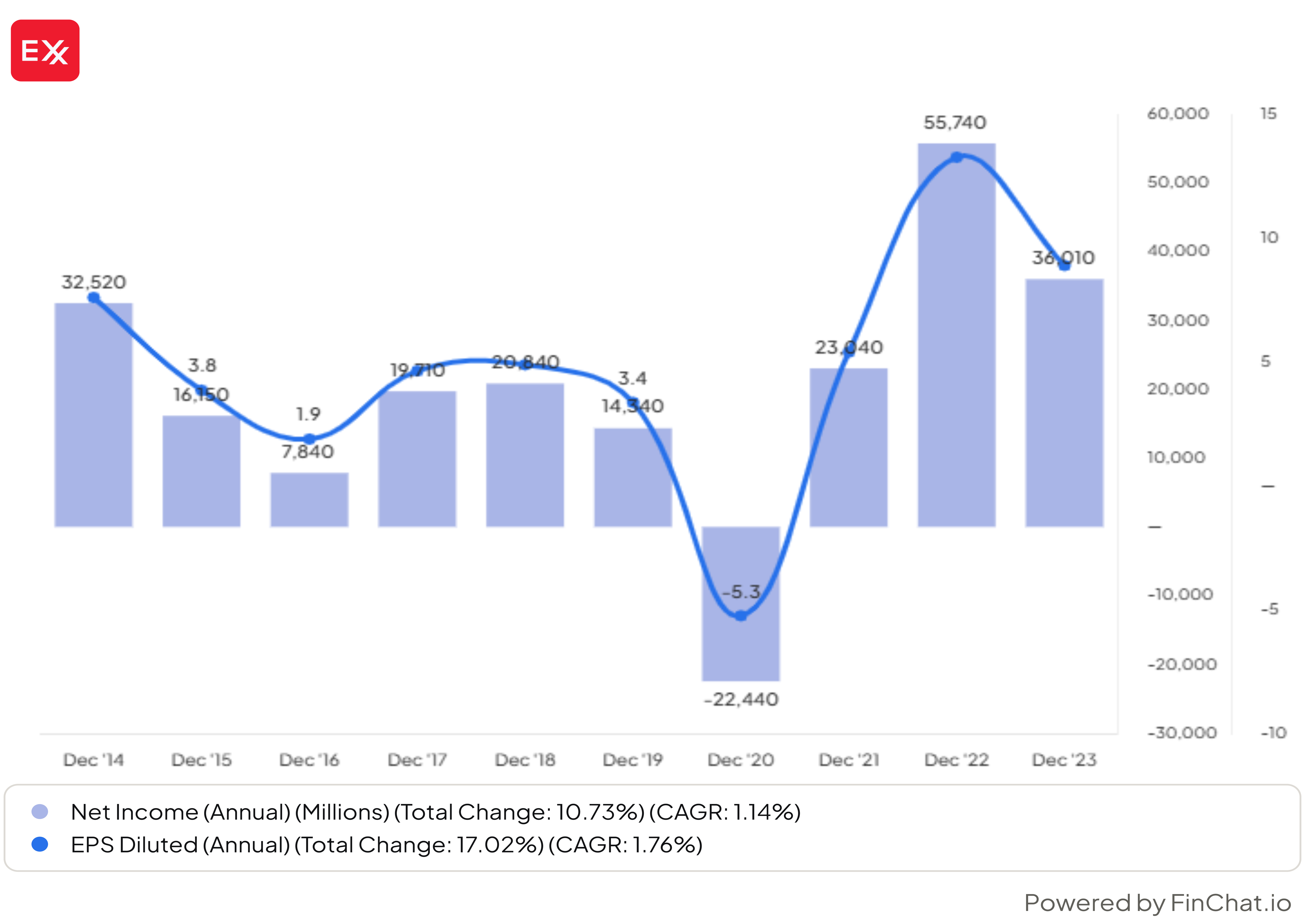

Chart 4: XOM Annual Net Profit and Fully Diluted Earnings Per Share (EPS). 2014-2023.

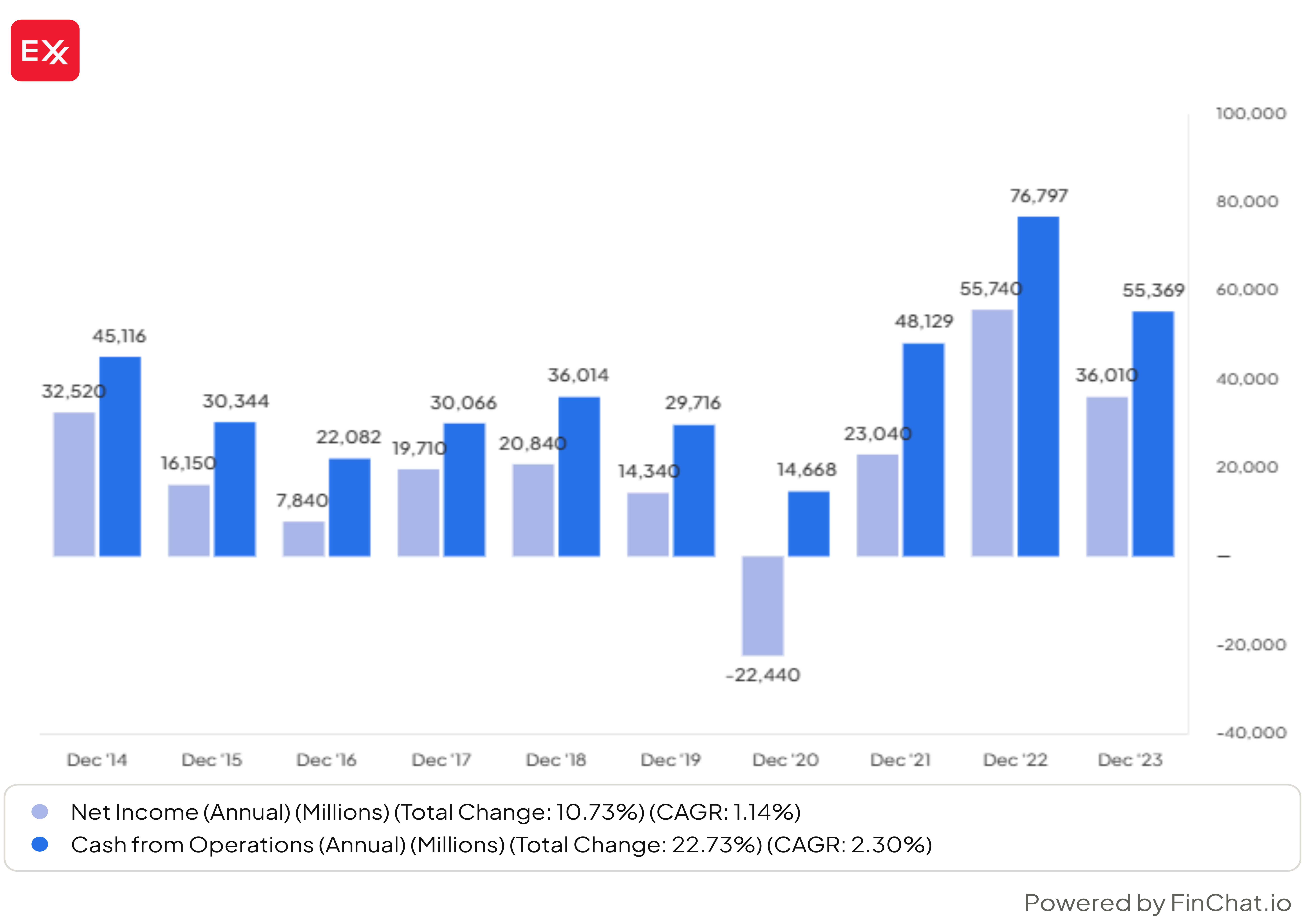

Chart 5: XOM Annual Net Income and Cash from Operations. 2014-2023.

The company has generated positive net cash from its operations every year in the last decade. The company has a significant depreciation charge (given large capital base) and therefore operating cash is much higher than reported net profit.

Chart 6: XOM Operating Cash and Free Cash Flow 2014-2023.

In 2018, XOM announced a plan to double cash flow between 2018 and 2025-2027. Chart 6 suggests that some good progress has been made on this. Free Cash Flow (FCF) has been mostly positive in the last the last ten years but 2020 was again an exception. FCF is much lower than Operating Cash Flow given the high levels of capital expenditure.

Chart 7: XOM Free Cash Flow and Dividends and Stock Repurchases.

The company has consistently paid dividends and in the last two years has bought back a significant number of shares. Share purchases were $15bn and $17bn in 2022 and 2023 respectively. The impact of this can be seen in the number of shares outstanding which has fallen in the last two years, as can be seen in the chart below.

Chart 8: XOM Total weighted average number of shares outstanding 2014-2023

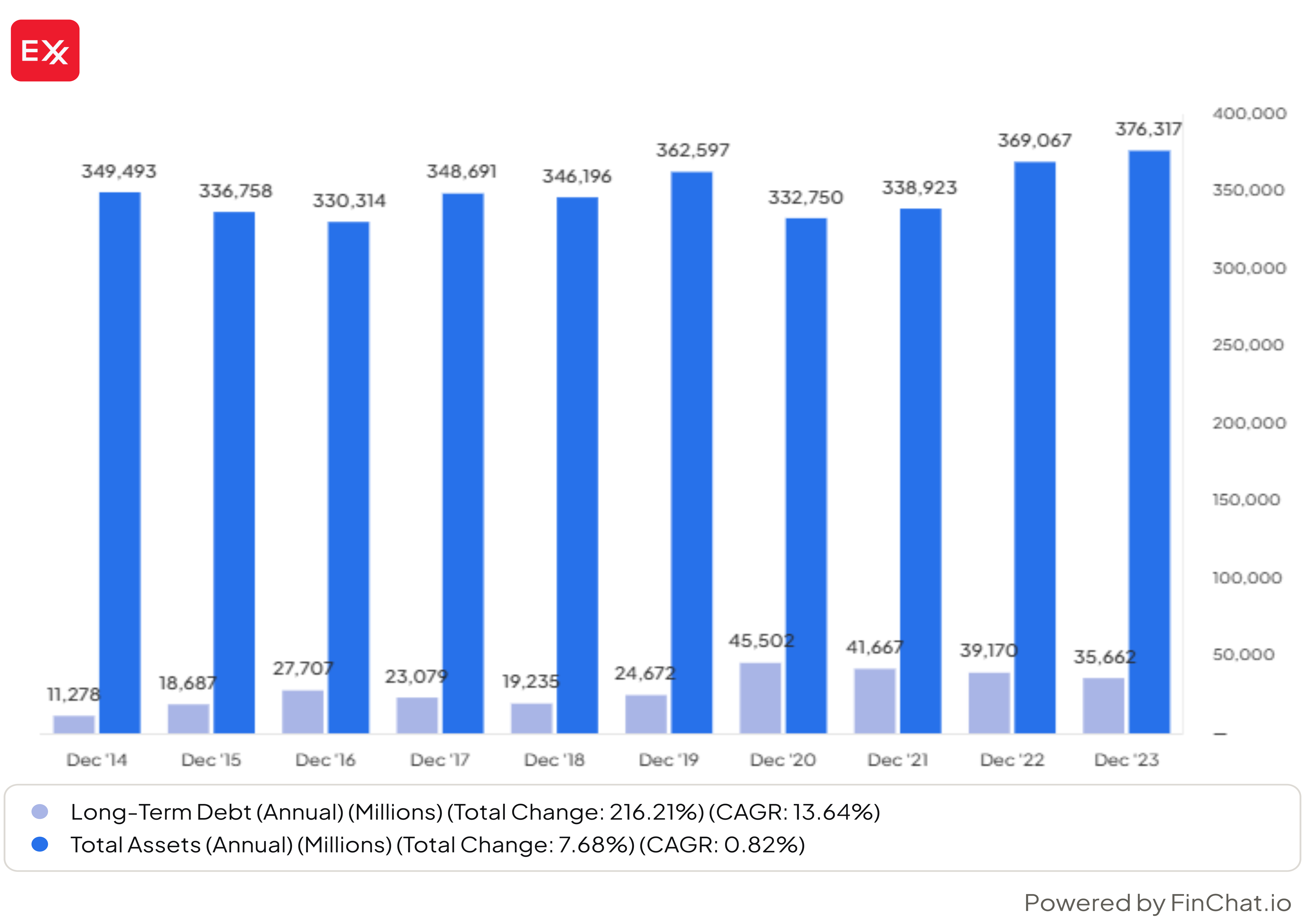

Chart 9: XOM Long-term debt and total assets 2014-2023

Chart 9 shows that long-term debt has been relatively small relative to total assets and suggests that leverage is low. This conclusion is supported by the debt interest coverage as shown in the Chart below.

Chart 10: XOM Interest Coverage Ratio.

Chart 10 above attempts to measure interest coverage of debt. It looks at annual EBITDA minus Capital Expenditure divided by interest expense as a proxy for measuring by how many times available cash flow covers the interest rate expense. Except for the Covid year 2020, when profits and cashflows collapsed, interest coverage has been at least 12.1 times and usually much higher. This indicates XOM is not operating with too much leverage.

Proved Reserves

An important Metric for Oil & Gas companies is Proved Reserves.

The estimation of proved reserves, which is based on the requirement of reasonable certainty, is an ongoing process based on technical evaluation, commercial and market assessments and detailed analysis of well and reservoir information such as flow rates and reservoir pressures.

XOM only records proved reserves for projects which have received significant funding commitments by management toward the development of the reserves. There is reasonable certainty about these numbers, but they can of course be adversely affected by a number of factors.

“Like other companies, XOM has a dedicated Global Reserves and Resources group that provides technical oversight and is separate from the operating organization. Primary responsibilities of this group include oversight of the reserves estimation process for compliance with Securities and Exchange Commission (SEC) rules and regulations, review of annual changes in reserves estimates, and the reporting of XOM’s proved reserves. This group also maintains the official company reserves estimates for ExxonMobil’s proved reserves of crude oil, natural gas liquids, bitumen, synthetic oil, and natural gas.”

The current Global Reserves and Resources Manager has more than 30 years of experience in reservoir engineering and reserves assessment, has a degree in Engineering, and served on the Oil and Gas Reserves Committee of the Society of Petroleum Engineers. The group is staffed with individuals that have an average of more than 15 years of technical experience in the petroleum industry, including expertise in the classification and categorization of reserves under SEC guidelines.

XOM’s Proved Oil and Gas Reserves are 17.7 bn barrels equivalent. As a comparison, Saudi Aramco has proved reserves of 258 bn barrels equivalent. In 2023, XOM annual production was about 3.7mn barrels per day or about 1.35bn barrels per annum. This implies that, based on current production the company has about 13 years of proved reserves. We do not know what the general industry average for this number is. XOM have to devote significant resources to the exploration for new reserves.

“Overall, investments of $14.6 billion were made by the Corporation during 2023 to progress the development of reported proved undeveloped reserves, including $14.3 billion for oil and gas producing activities, … These investments represented 74% of the $19.8 billion in total reported Upstream capital and exploration expenditures.”

There is a long time-lag between recognising proved reserves and starting production.

“Development projects typically take several years from the time of recording proved undeveloped reserves to the start of production and can exceed five years for large and complex projects.”

“80% of Proved undeveloped reserves are in Australia, Kazakhstan, the United Arab Emirates, and the United States.”

“Proved reserves will be produced; however, the timing and amount recovered can be affected by a number of factors including completion of development projects, reservoir performance, regulatory approvals, government policies, consumer preferences, the pace of co-venturer/government funding, changes in the amount and timing of capital investments, and significant changes in crude oil and natural gas price levels.”

Summary

Despite the advance of electric transportation and increases in energy efficiency, Oil demand is likely to grow steadily in the next 25 years and beyond.

The bulk of the growth will come from demand in developing countries.

Despite the growth in low-emission fuels such as gas and renewables, Oil exploration and production will also grow steadily in the medium term.

Companies like XOM will have to invest to get new oil reserves through exploration and acquisitions.

Despite volatility of earnings due to oil price swings, XOM has a relatively good track record of profits, profitability and cash generation.

The company is making good progress in its current plan to boost Free Cash Flow.

A significant and increased part of the increased Free Cash Flow has been used to buy back shares in the last two years.

Valuation

We will look at some basic relative value metrics for XOM.

XOM is currently trading on a Forward P/E ratio of 12.7 times.

The Forward Price to Free Cash Flow (P/FCF) ratio is 14.2 times which implies an FCF yield of 7%.

The current dividend yield is 3.24%. This implies a combined “Cash yield” of over 10% (7% + 3.24%).

These numbers are reasonable given the Company’s operating margin levels and Profitability.

Conclusions

We believe that it is worth investing 1% to 2% of our portfolio in XOM to increase our Oil and Gas exposure. Our positive view is based on:

relatively consistent performance in the last decade despite energy price volatility and the demand shock of the Covid Pandemic

good progress in boosting Cash Flow and increase stock re-purchases in last few years

The low relative valuations of the company and therefore the high cash yield

Our view is not based on any view on Oil prices or refining margins as we have no expertise in forecasting them. Our best guess is that Oil prices will be elevated for some time.

Appendix One

Highlights of the most recent Earnings Conference Call

“2023 was an outstanding year. We delivered $36bn of earnings, strong cash flows, and a 15% return on capital employed. Our strategy, introduced in 2018, coupled with consistently strong execution, is delivering results that lead industry across a range of metrics, including earnings and cash flow growth, total shareholder distributions, and total shareholder returns since 2019, the baseline year of our plans.”

“We more than doubled earnings in 2023 versus 2019, demonstrating the improved earnings power of the company. The growth in profitability reflects significant progress in high-grading our portfolio of assets through advantaged projects, divestment of less strategic operations, and significant cost reductions.”

“We entered the lithium business, where we see an opportunity to supply approximately 1 million electric vehicles per year by 2030 with economically advantaged production that has a much smaller environmental impact than today’s supply.”

“In the carbon capture and storage space, we recently completed the construction of a pilot plant to further develop a unique, proprietary technology, which has the potential to significantly lower the cost of direct air capture.”

“For 2024, we expect to invest $23 billion to $25 billion to grow our portfolio of advantaged, low-cost of supply assets, further shift our product mix towards higher value, higher margin performance products, and reduce emissions, both our own and others.”

“Our plan also continues to structurally reduce costs to achieve $15 billion in structural cost savings through 2027.”

In 2018, XOM announced a plan to double cash flow between 2018 and 2025-2027, a growth of about 15% CAGR.

“We've grown earnings at compounded annual basis by 40%, greater than 40%. We've grown cash flow from operations almost 20%, greater than 15%. ... earnings improvement that is flowing through to cash flow. And so as you think about cash flow, our earnings expectation in the corporate plan in terms of doubling it out to 2027, it's well ahead of doubling it.”

“We see huge potential in terms of linking together all the opportunities to reduce emissions, high concentration emissions along the US Gulf Coast and along that pipeline system. So the team's doing a lot of work around developing the business there, a lot of work with potential customers around how we can help capture their emissions, and a lot of work around the operations and improving and growing the capacity of that pipeline.”

“If you think about what we're trying to do there with respect to addressing the risk of climate change and significantly reducing emissions for third parties, that's a business that doesn't exist today anywhere in the world.”

“Our track record demonstrates that we are not about going after volume or going after marginal investment opportunities. These things have to be unique. The hurdle to get into the capital plan is pretty high, we have a clear understanding of cost of supply. We know where we sit on the cost of supply curve. We know as new projects or opportunities come forward, we look at those in terms of where they sit from a competitive standpoint. They have to have a structural advantage. They have to be robust and resilient to the bottom of cycle conditions.”

On the Petrochemical cycle

“Perhaps 20203 was kind of the bottom of the chemical cycle. “…the bottom of the trough. It was definitely a challenging year, well below, I think, the bottoms of previous cycles. we definitely demonstrated that, that the projects -- the new projects that we've brought on, that have some run time in them, are earnings and cash positive, even in these very challenging conditions. So I think like many others in the chemical industry, we'd like to see us come out of the trough and when we do, our expectation is the capital that we've brought on will obviously be performing even better with better margins. I would say as well with respect to turning points, we have seen some -- we certainly saw in the fourth quarter some slight improvements. There's still a lot of capacity that's come on out there.”

On Carbon Capture

“We're convinced that carbon capture is going to play a really important role in helping society meet its ambitions to get to net zero or to make certainly significant reductions in carbon emissions. …the existing technology was designed for a different purpose. There's a lot of advances in technology since the existing technology was developed. And so there's a question of how can we better capture CO2 by using advances in the existing technology. It's early days like all these technology developments. And so we built a pilot plant and we'll see and test out some of these new capabilities and test the cost effectiveness of capture. I'd say our first step, we're looking to get about a cost reduction of about half. That's still not enough. But if we can see a significant step change in that cost or path to that cost reduction, that gives us hope that we can then continue to advance that and get it back -- get it down to something that is more competitive and then economic to deploy across the world.”

“Our technology companies have got some great ideas, know how to scale things, know how to optimize not only materials but processes and bringing all that together to see if we can't make a step change here is the objective. And it's too early to judge how successful we'll be, but I certainly feel like we've got the capabilities and should be working hard to try to make advances here.”