Infosys Inc. (INFY)

A short write-up

This the third short write up. The first two were on Ulta Beauty (ULTA) and AutoZone (AZO). These short reports are not complete and they should be seen as the starting point for further work, evaluation and consideration.

Infosys Inc. (INFY)

Infosys is an-Indian company in the Information Technology Enabled Services (ITES) space. It is also listed on the NYSE in the form of American Depositary Receipts (ADRs).

We have written tangentially about the company twice in the past but have not done a detailed write up. These reports can be found here and here.

As the Indian Economy opened up to the outside world in the 1990s, IT was the first sector to demonstrate global competitiveness.

The two largest ITES companies in India are TCS and Infosys. The third and fourth ranking companies are HCL Technologies and Wipro. The latter also has an ADR listed in the USA which trades under the ticket WIT.

These companies were engaged in global labour arbitrage. India has a huge supply of software workers, and the companies grew by employing software engineers to provide IT services for global clients in the B2B space. They maintained legacy mainframe systems, wrote software code, helped companies transform and monitor IT systems. They got a significant boost due to Y2K issues in the late 1990s when companies had to overhaul IT systems to deal with the Millennium Bug. The large banks who have been among the larger spenders on IT in the last three decades have been important customers for the Indian ITES companies.

For decades, the ITES have earned 70% of their revenues from US companies and institutions, with the balance coming from the rest of the world. Indian customers account for a negligible share.

The ITES companies grew very strongly in the last three decades. They had high sales growth, and high margins and generated huge free cash flows. They gave excellent returns for shareholders over the decades. In the last 30 years they have given CAR return of 30% in INR terms and ~27% in US$ terms.

They have become major recruiters of students in STEM subjects in India and have had to pay well as they battled high levels of attrition. The ITES sector employs 4mn young professionals and has created huge wealth through high salaries and share price appreciation.

The success of these companies was widely applauded. They were seen a symbol of the new capitalist India and India’s first globally competitive industry. There were, however, some criticisms.

One line of argument is they just provided software workers and only interacted with the IT people in the client’s hierarchy. The higher value technology consulting work was still done by the likes of Accenture, Booze Allen and Bain who had deep business relationships with the CEOs and Senior Management.

Another criticism was they only provided services and never developed software which is much more scalable.

Their success encouraged large global companies such as Accenture (ACN), IBM, Cognizant (CTSH) and many others to establish large operations in India. IBM and ACN employ about 300,000 people each in India. CTSH has 200,000.

Indian ITES companies are currently facing significant revenue headwinds. Their customers face difficult conditions and are unwilling to commit to large discretionary expenditures. There is a fear that the rise of AI will reduce demand for their services. The companies will have to adapt and change in response to the growth of AI.

Introduction to Infosys

Infosys HQ in Bengaluru, India

INFY has recognised the vast change in the technology landscape and have changed their self-description. They describe INFY as “a global leader in next generation digital services and consulting. They claim they enable clients in more than 56 countries to navigate their digital transformation powered by AI and cloud.”

INFY was established in 1981 from a capital of $ 250 and has grown to market capitalisation of $ 93bn.

It has 317k employees and has over 1882 clients. 299,814 were professionals involved in service delivery to clients, including trainees. In the 2024 Annual Report, they noted that 250,000 + employees are AI aware.

Infosys Training Centre in Mysuru, India houses the largest corporate university in the world

INFY has 265 offices and 56 companies. It earns 60% of its revenues in North America and 27% from Europe and only 2.5% from India.

85% of free cash flow for FY 2020 to FY 2024 has been returned to shareholders in line with their Capital Allocation Policy. The Company expects to progressively increase its annual dividend per share (excluding special dividend if any)

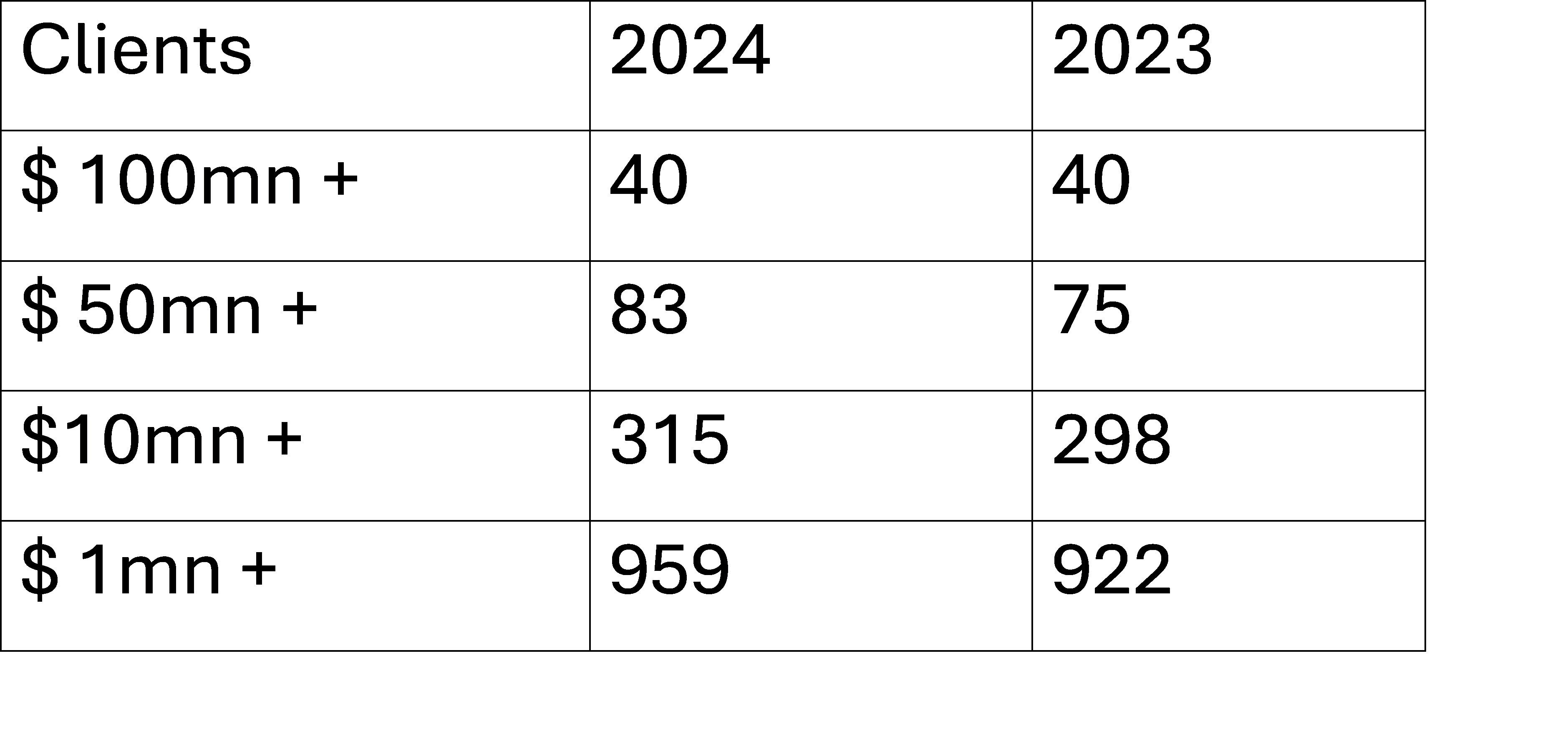

As of 31 March 2024, they had 83 clients whose revenue contribution to Infosys is in excess of $50mn.

“The client segmentation, based on the last 12 months’ revenue for the current and previous years, on a consolidated basis, is as follows:”

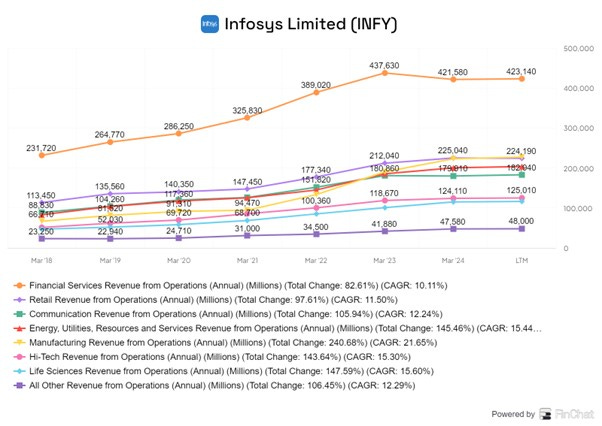

The largest customer base segment is Financial Services. Many of the world’s largest commercial and investment banks are Infosys’ clients. As the chart below suggests, revenues have been flatlining in the last six quarters as clients have responded to the highly uncertain and inflationary times by curbing discretionary spending, including the large IT projects that Infosys specialises in.

Two key features of the INFY’s business. The business model is highly cash generative as there is little or no need for capital expenditure. Infosys has had little or no debt. Cash has always greatly exceeded long-term debt.

The business has little operating leverage. Total revenues grow only if more staff are added so revenues tend to grow in line with costs.

Historically, the business challenge has been to recruit and train enough IT engineers and reduce the amount of time they are benched and hence not working. Another key challenge is to retain trained employees.

Their aim is to increase the number of clients paying the largest fees. In FY 24, “they added 385 new clients, including a substantial number of large global corporations. Our total client base at the end of the year stood at 1,882.”

In his concluding remarks in the most recent Annual Report, the Chairman noted the following.

Above all, the gen AI revolution presents an unrivalled opportunity. The flux of change as the whole technological landscape is being reset will create many large openings. Packaged solutions will be reimagined, and we will see a resurgence of custom-built solutions that must be enabled with new types of AI building blocks. The puck is clearly and quickly moving to a place where the balance of advantage will be with Infosys.

Summary Financial Numbers

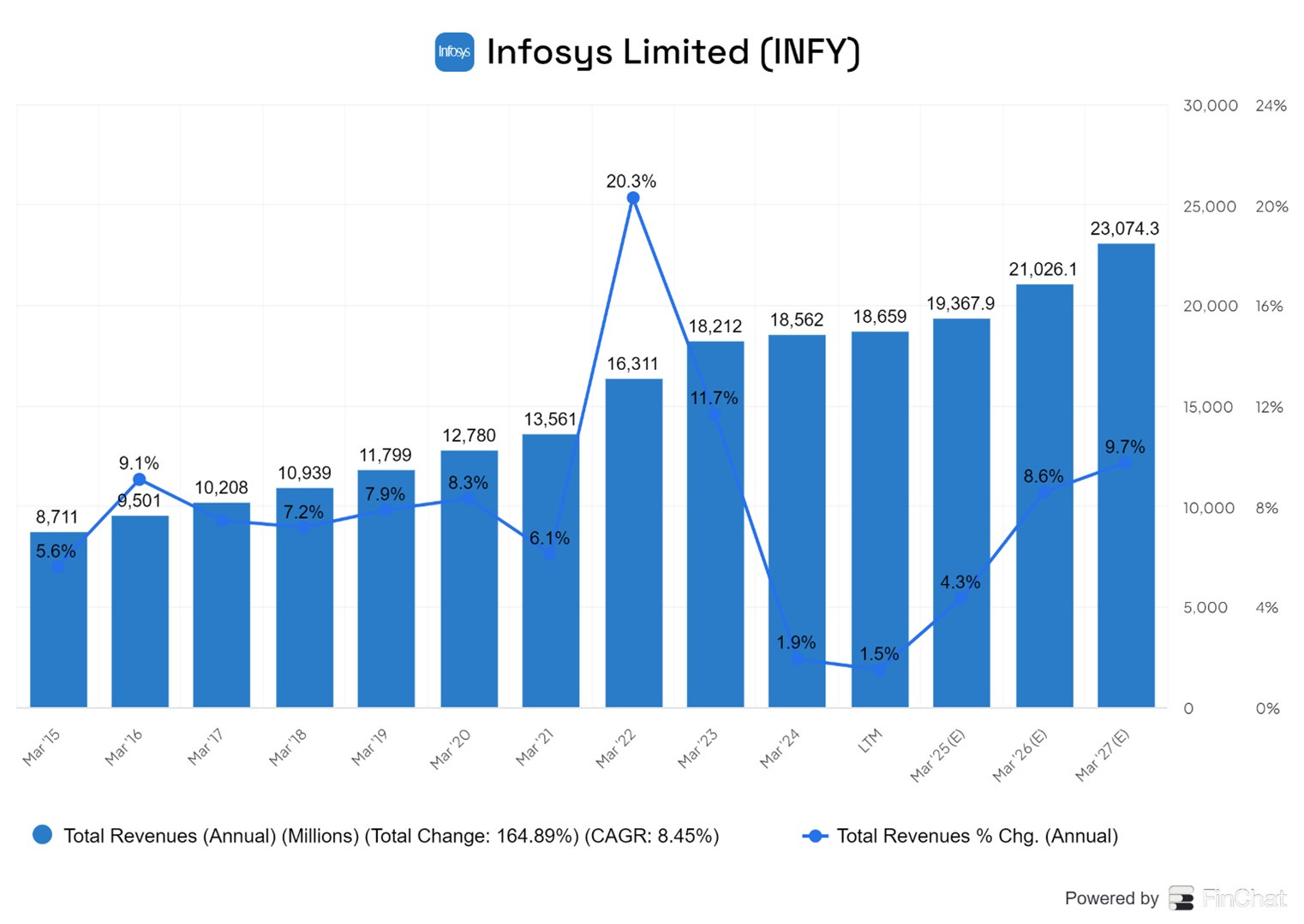

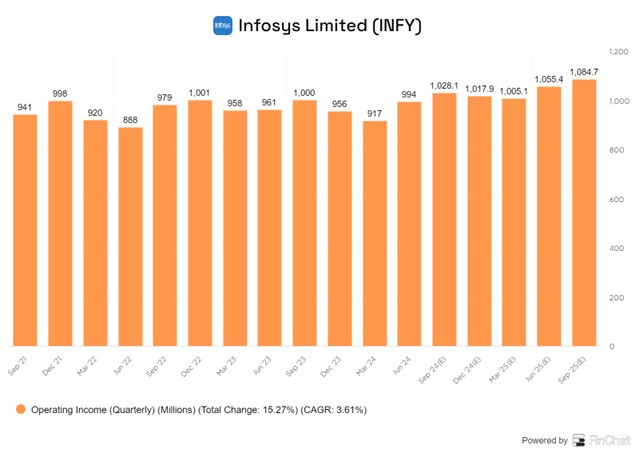

Revenue and Operating Profit growth

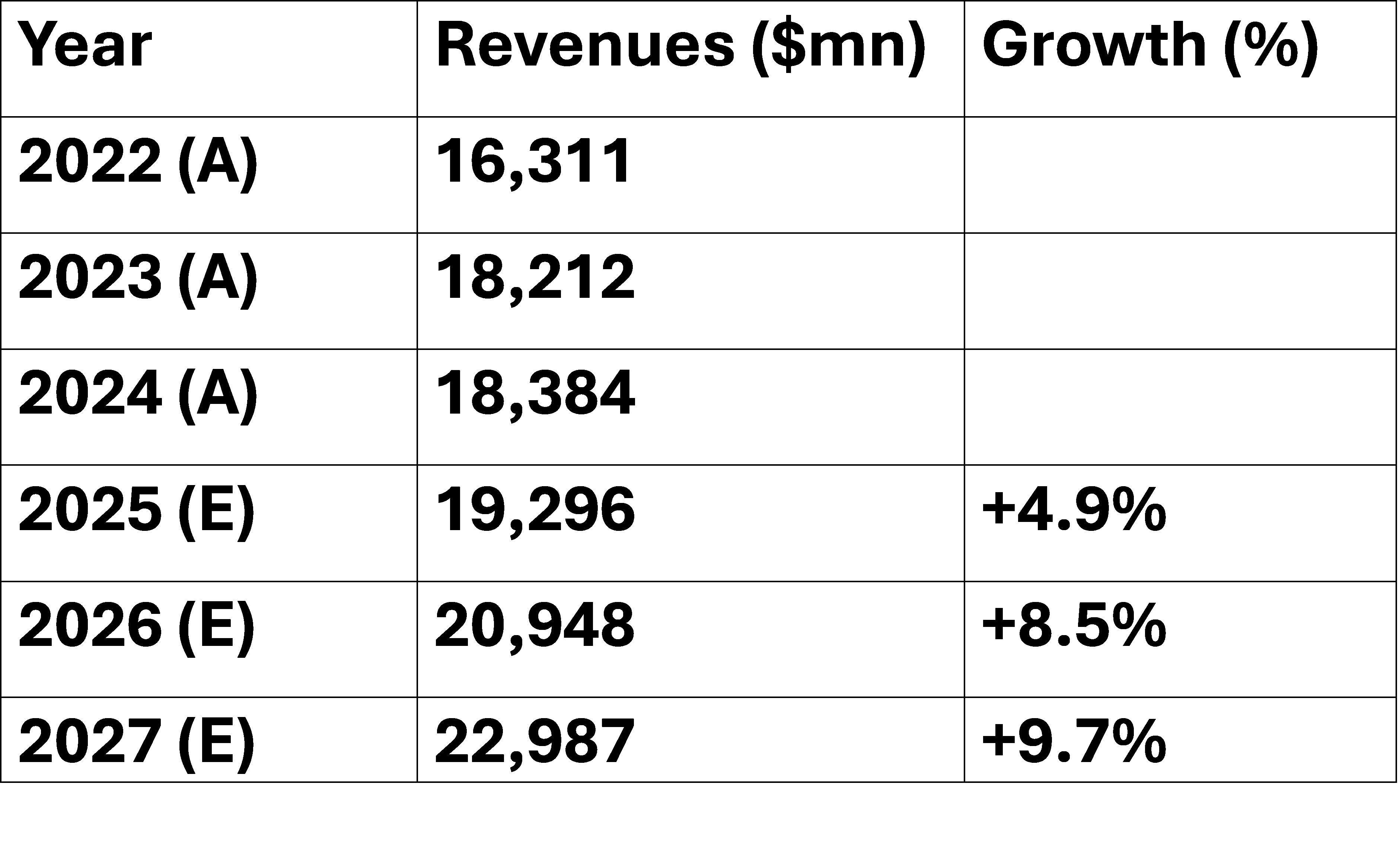

The chart below shows annual revenue and percentage revenue growth. FY 2024 Revenue was US$ 18.56bn. Revenue growth has slowed significantly in recent years.

Sales have been flat in the last two to three years as clients have put a brake on discretionary spending.

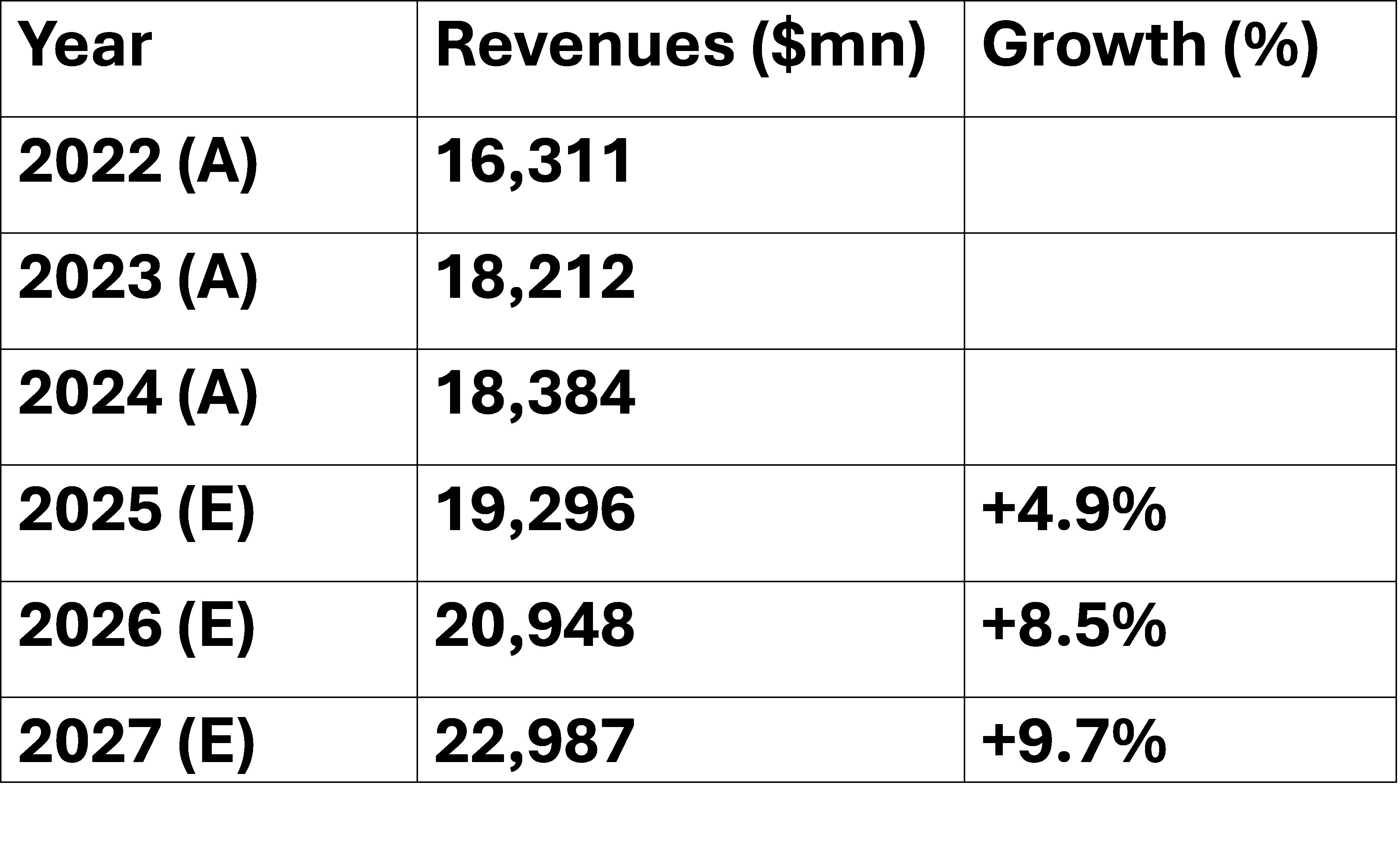

The consensus analysts’ forecasts are for a pick-up in revenue in the next three years.

In the current year, total revenues are expected to grow at 4.3% to $ 19.37bn.

In FY 26, total revenues are expected to grow at 8.6% to $ 21.0bn.

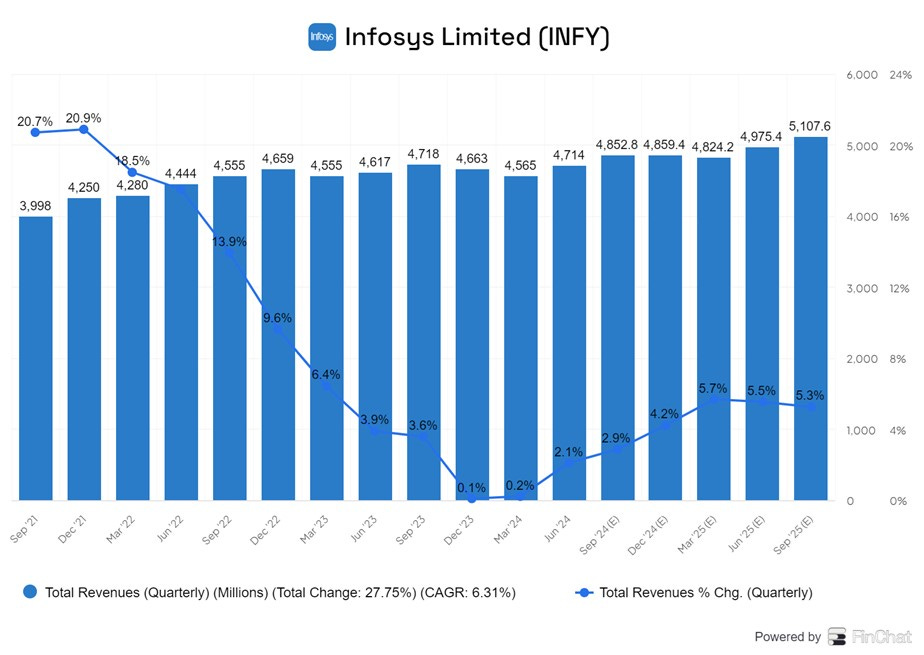

The quarterly revenue run rate is about $4.8bn and is expected to rise to $5.1bn in about twelve months.

Quarterly Operating Income run rate is about $1bn and is expected to rise to $1.1bn in 12 months.

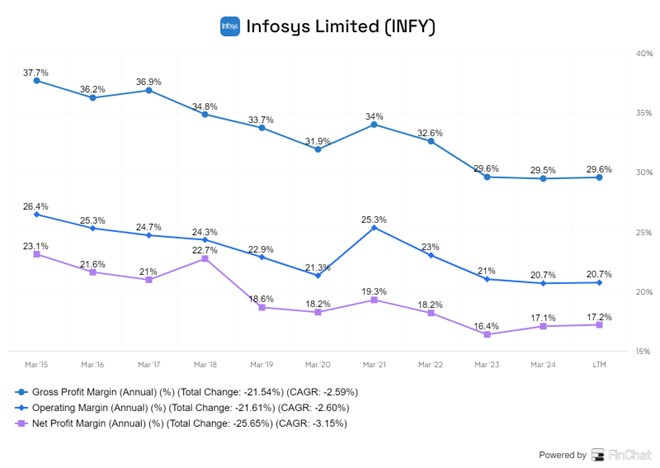

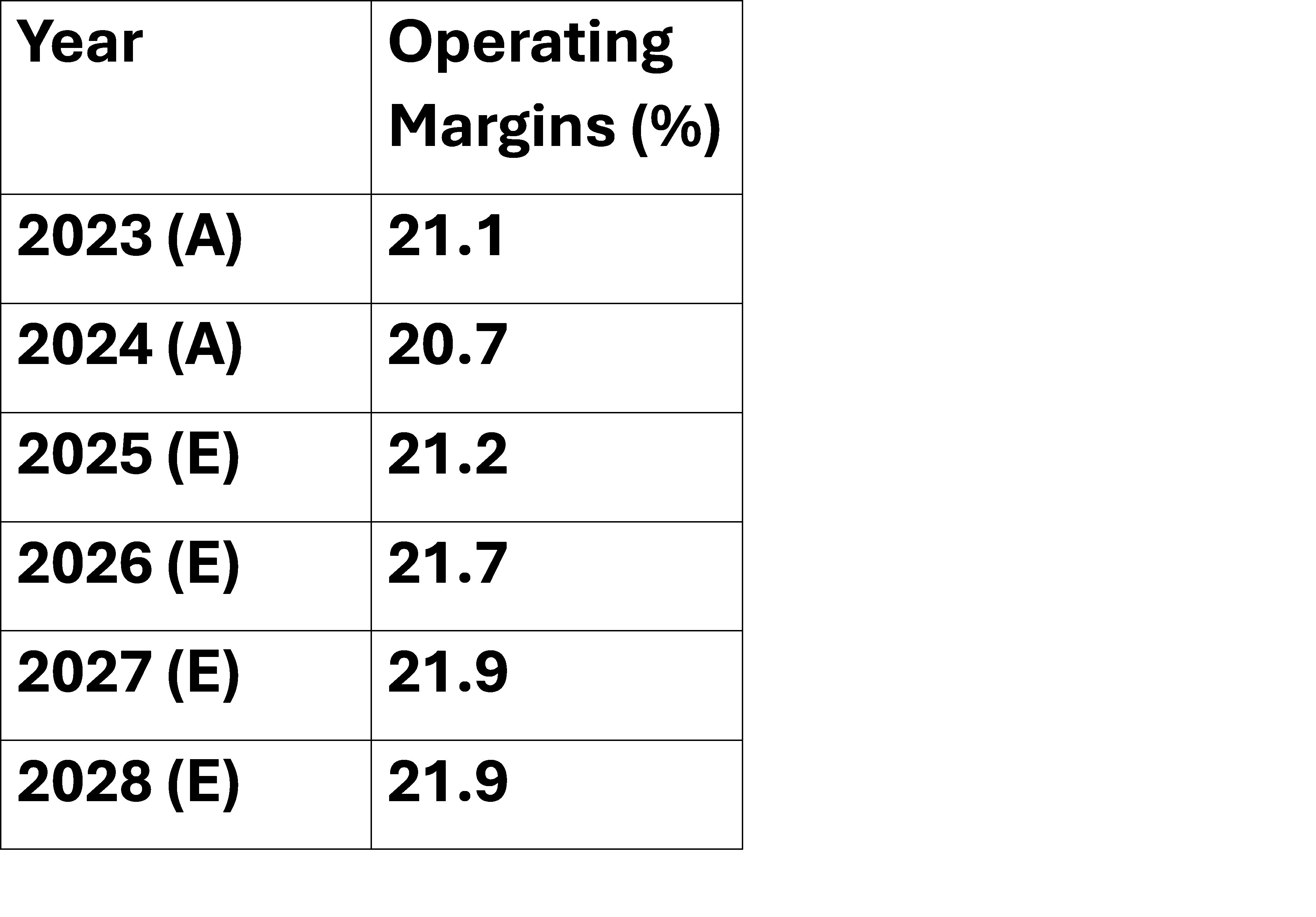

Margin Trends

Margins are high but have been on a gently declining trend in the last ten years. Gross Margins are at 30% while operating margins and Net Income Margins are at 21% and 17% respectively.

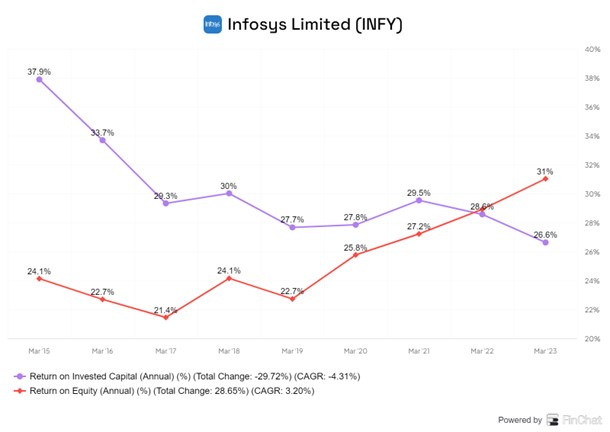

Profitability is high with an ROE of about 31%

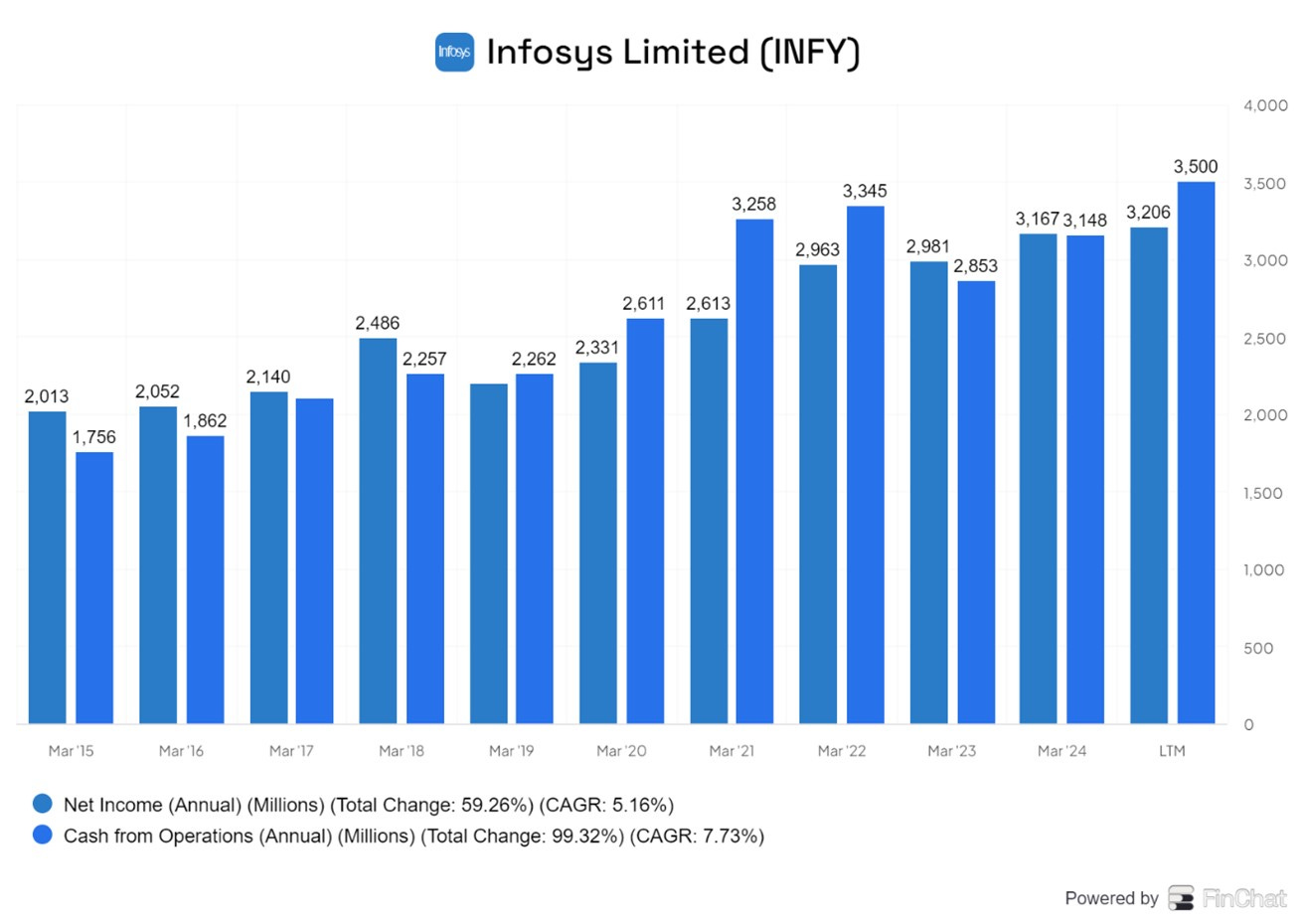

Net Income and Operating Cash Flow

Net Income and Operating Cash have grown in line with no major discrepancy between the two. This indicates that INFY has great capacity to convert Net Profit into Operating Cash.

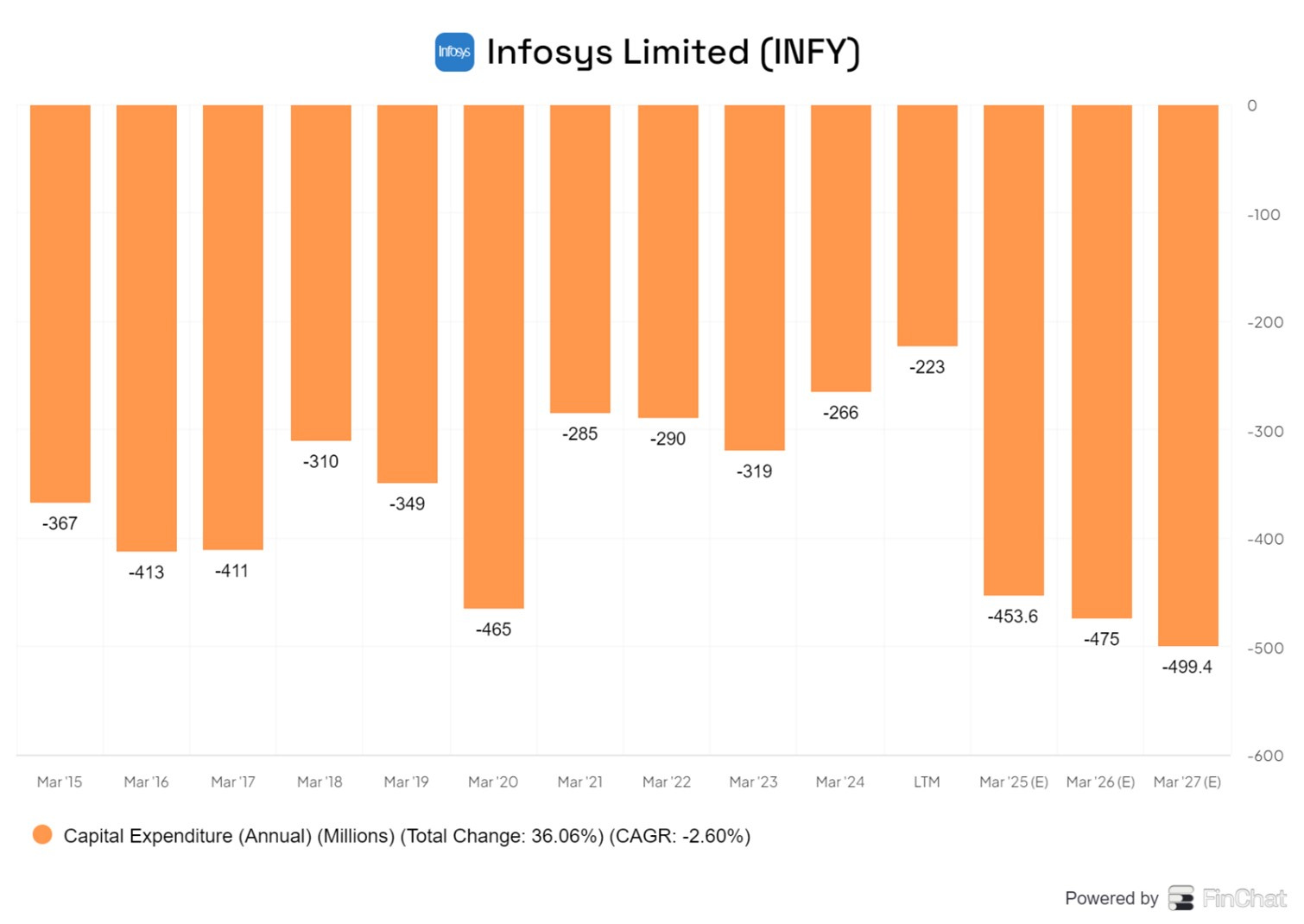

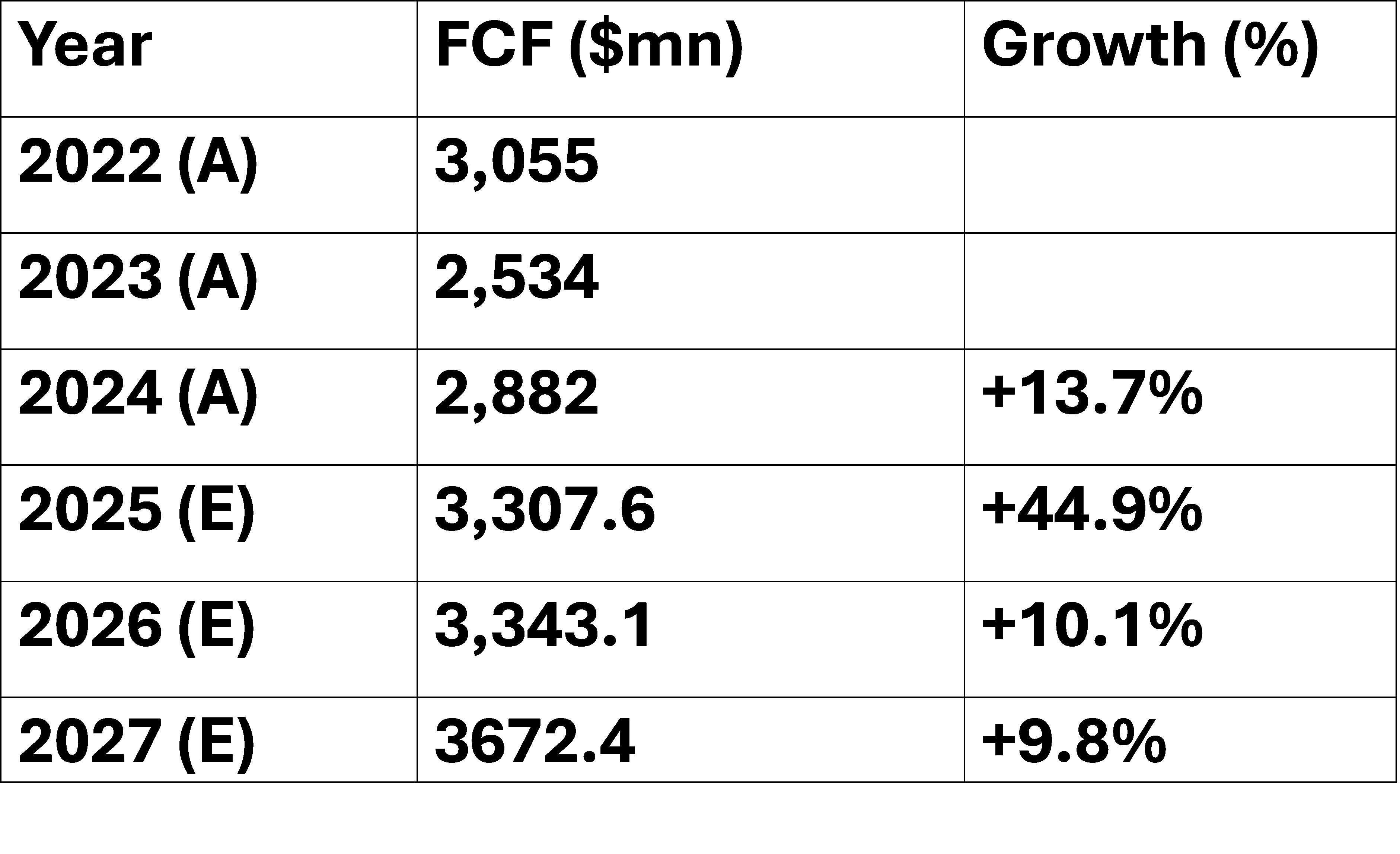

Free Cash Flow trends

Cash from Operations (CFO) and Free Cash Flow (FCF) have both grown. There is little difference between CFO and FCF reflecting the low capex needs of the business. Capex run rate is about $300mn per year. This is forecast to increase to about $ 500mn per year in the next three years (see below).

Capex is shown as a negative in the above chart as its a cash outflow.

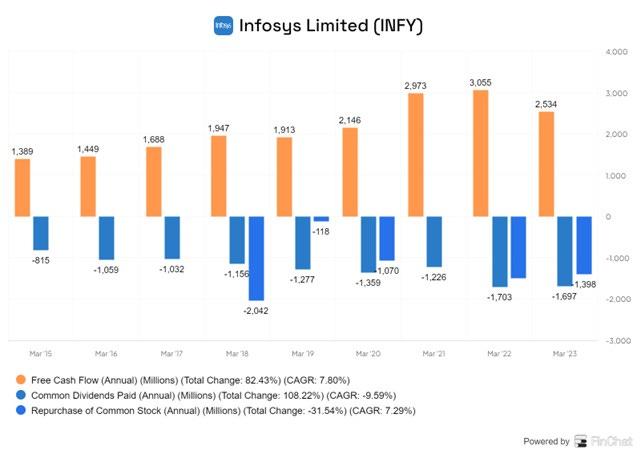

Capital Allocation Policy

Due to low capex outflow, the bulk of free cashflow can be retained by the company or returned to investors. Infosys has a policy of returning approximately 85% of FCF cumulatively over a five-year period through a combination of dividends and/or share buybacks. The company expects to progressively increase its annual dividend per share (excluding special dividend if any). Dividends and Stick purchases are shown as negative as they represent a cash outflow.

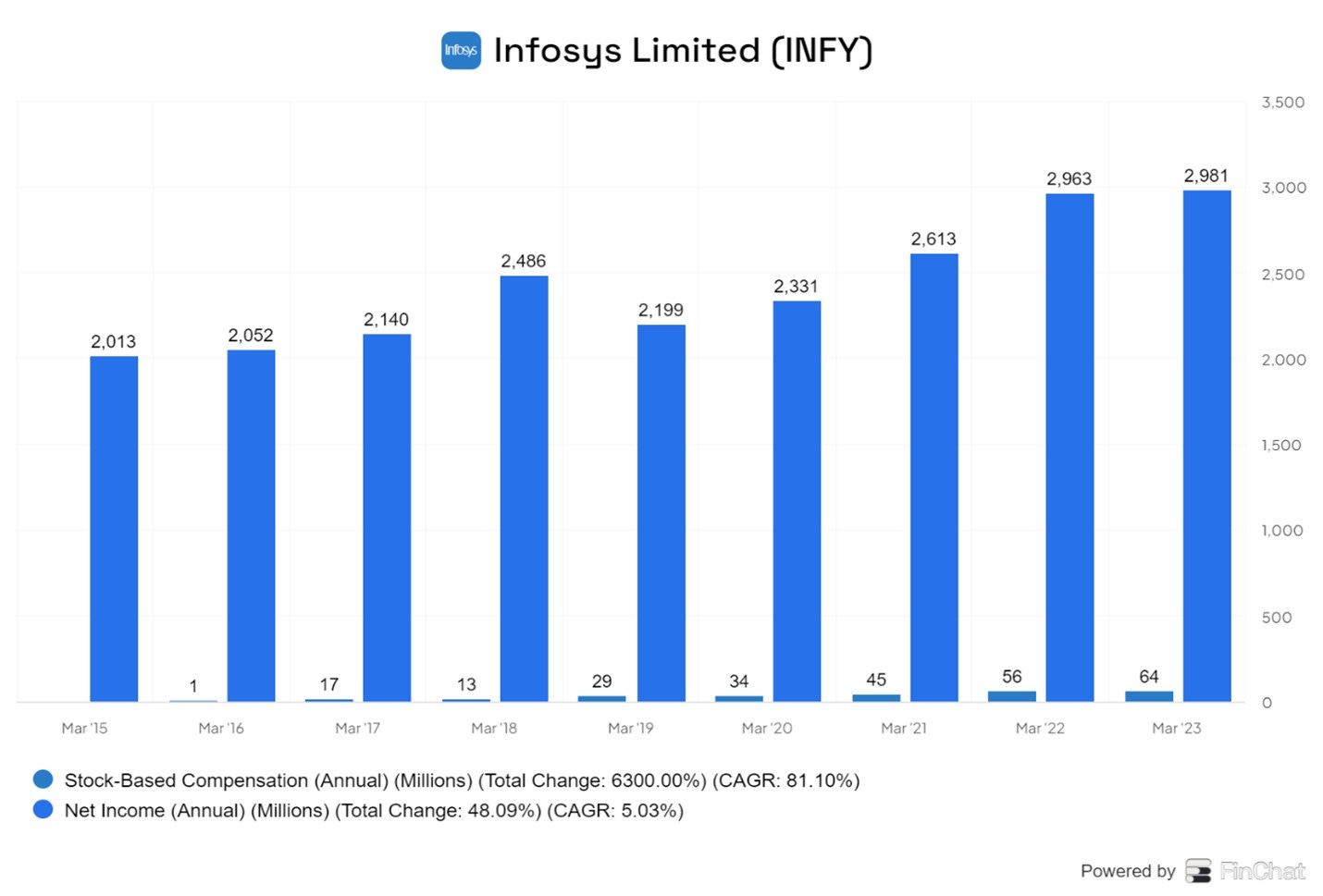

Stock-based compensation (SBC) is relatively low as a percentage of net income. In FY 22 for example, SBC was just $56mn compared with Net Profit of $2.9bn.

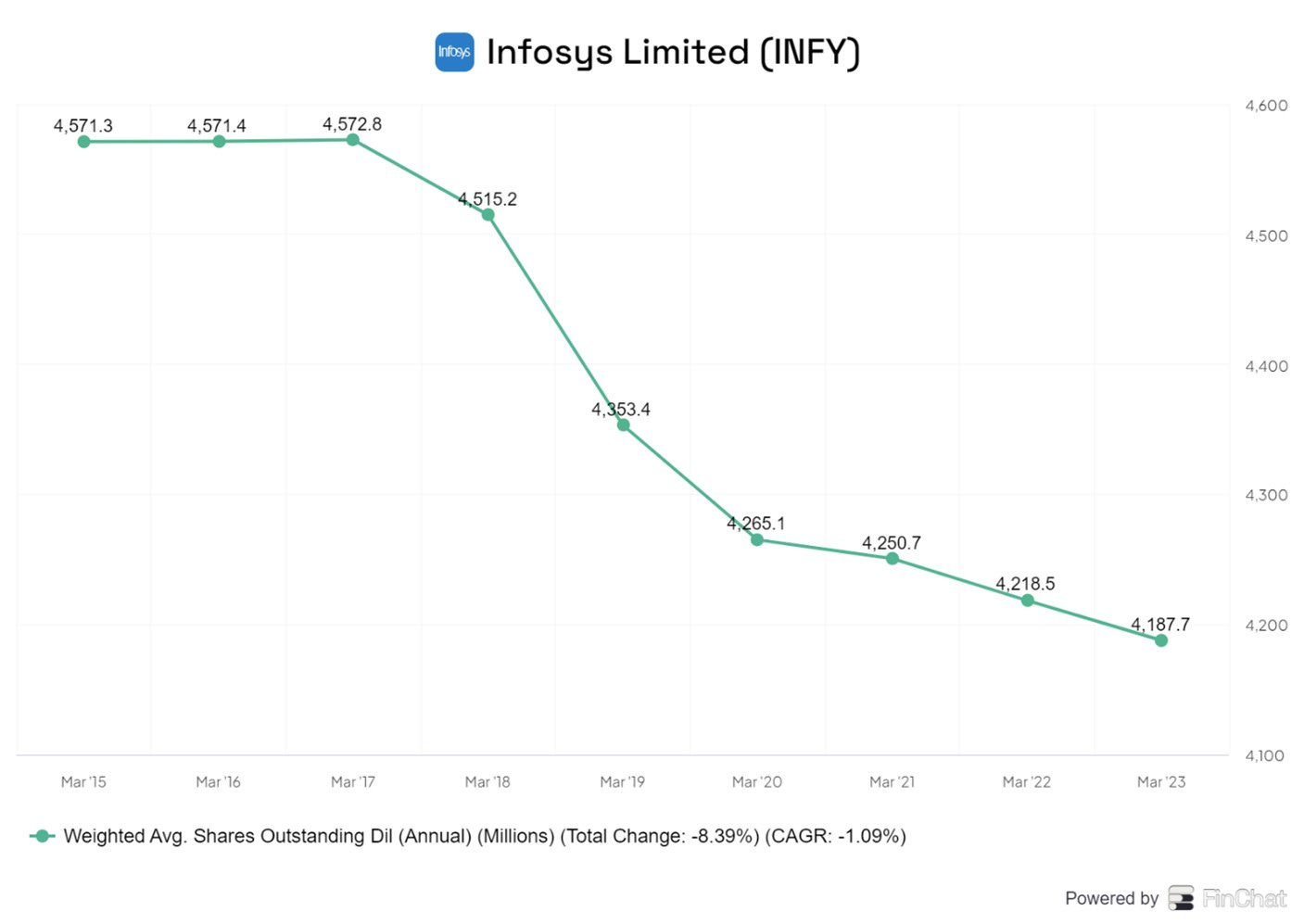

The average number of shares outstanding has fallen steadily in the last ten years at a rate of about 1% per annum.

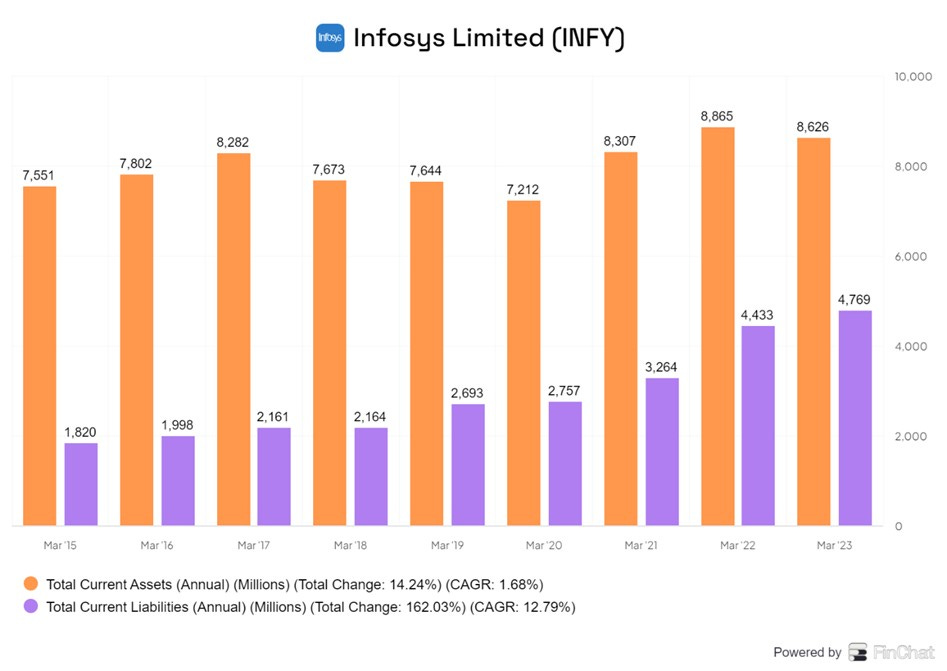

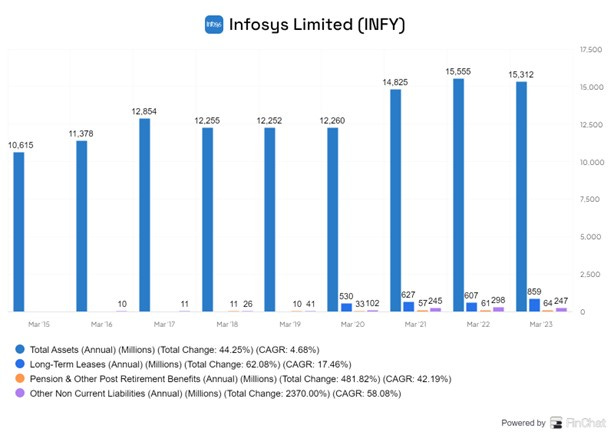

Balance Sheet Strength.

Total current assets are much more than current liabilities.

The company has no long- term debt and other, non-equity non-current liabilities, such as leases, are negligible (see below) compared with Total Assets.

SWOT Analysis

We present a quick SWOT analysis for INFY

Strengths

Infosys is long established ITES company which has given very good shareholder returns for over three decades.

It has built up large scale and capacity to serve large customers and execute large contracts.

Infosys is an export powerhouse. Less than 3% of its revenues are sourced in India but most of its costs are in Indian Rupees. This means its earnings benefit from the long-term trend of rupee weakness.

Low capex needs and a very strong balance sheet with net cash and no long-term debt.

INFY has Strong FCF, and the company has a consistent policy of returning 85% of FCF to shareholders.

Stock-based compensation is very low.

Weakness

Large size (300k+ employees) means it is difficult to grow fast going forward.

Margins are declining gradually, and this may gradually put downward pressure on profitability.

Business has little operating leverage. Revenues can only be really in the medium to long-term by hiring more people. Therefore, costs tend to rise in line with revenue.

Although Infosys has a few software products such as Finacle (for commercial banks), the bulk of its revenues comes from services which are less profitable than software.

Opportunities

Companies and organisations worldwide need to re-engineer their operations in response to the AI revolution. This could generate huge demand for services of companies like Infosys if they can retrain their most of their staff in the requisite skills and deploy them.

Threats

The AI and Machine Learning revolution might reduce the demand for services currently offered by Infosys as smart capable machines can do some of the work.

Higher unemployment amongst IT professionals in US and EMEA may put pressures on local remuneration.

On the other hand, the strong growth of the Indian economy may increase wage pressures and force Infosys and other to pay higher wages.

These two factors many combine to reduce the labour cost arbitrage exploited by Infosys.

Infosys has many formidable competitors such as IBM, Accenture, Cognizant, Cap Gemini, EPAM as well as India-based rivals such as TCS, HCL and Wipro. There are also numerous smaller competitors who are specialists in a small number of niches or technologies.

Valuation

The consensus analysts’ forecasts for revenues are as follows:

The consensus analysts’ forecasts for EPS are as follows:

The consensus analysts’ forecasts for Free Cash Flow (FCF) are as follows:

The market is expecting tepid growth in the current year and subsequent faster growth for Revenues and EPS. Free Cash Flow fell in 2023 and it is set to rise above the 2022 level in the current year and then rise at a double digit percentage rate per annum to FY 27.

At the current price of $22.57, the Infosys ADR stock is trading at a two-year forward P/E Ratio of 26X.

At the current market cap of $93.2bn, the stock is trading at a two year forward Price to Free Cash Flow Ratio of 27X.

These numbers imply a two-year forward earnings and Free Cash Flow yield of about 3.8%. These rise to 4% to 4.2% on a three year forward basis. These are reasonable yields given current interest rates but should ideally be a little higher.

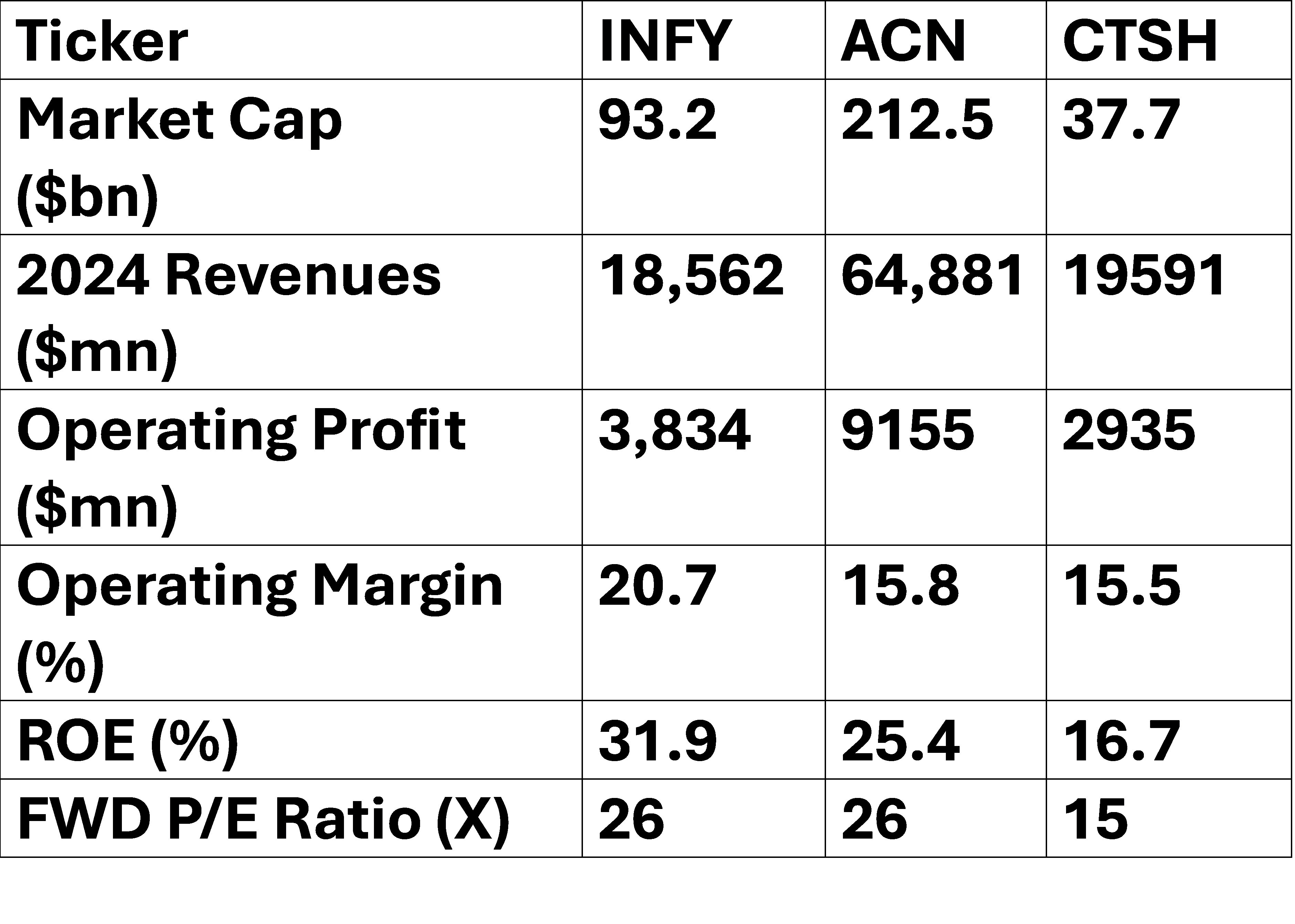

Relative Valuation - We compare some valuation metrics for Infosys, Accenture (ACN) and Cognizant (CTSH) below:

CTSH is on a forward PE of 15X compared with 26x for INFY but its ROE is only 16.7% compared 32 % for INFY. That broadly seems fair: twice the multiple for twice the profitability.

Both INFY and ACN are on a similar multiple. ACN is a much larger company than INFY. However, INFY has higher margins and higher profitability.

This quick analysis indicates that INFY is valued at a broadly similar relative to its peers. On balance, it can be said to be attractively valued relative to ACN.

We conducted a Discounted Cash Flow (DCF) Calculation.

We used the prior revenue assumptions which are reproduced below.

We made the following additional assumptions. On Operating Margins, we assume the following:

We also assume a risk-free rate of 3.5% and a Market Risk premium of 8.3%. The ADR Beta is 0.6. These numbers imply a Weighted Average Cost of Capital (WACC) of 8.5%. Finally, we assume that in FY 2028, the terminal exit multiple for EV/FCF is 26X.

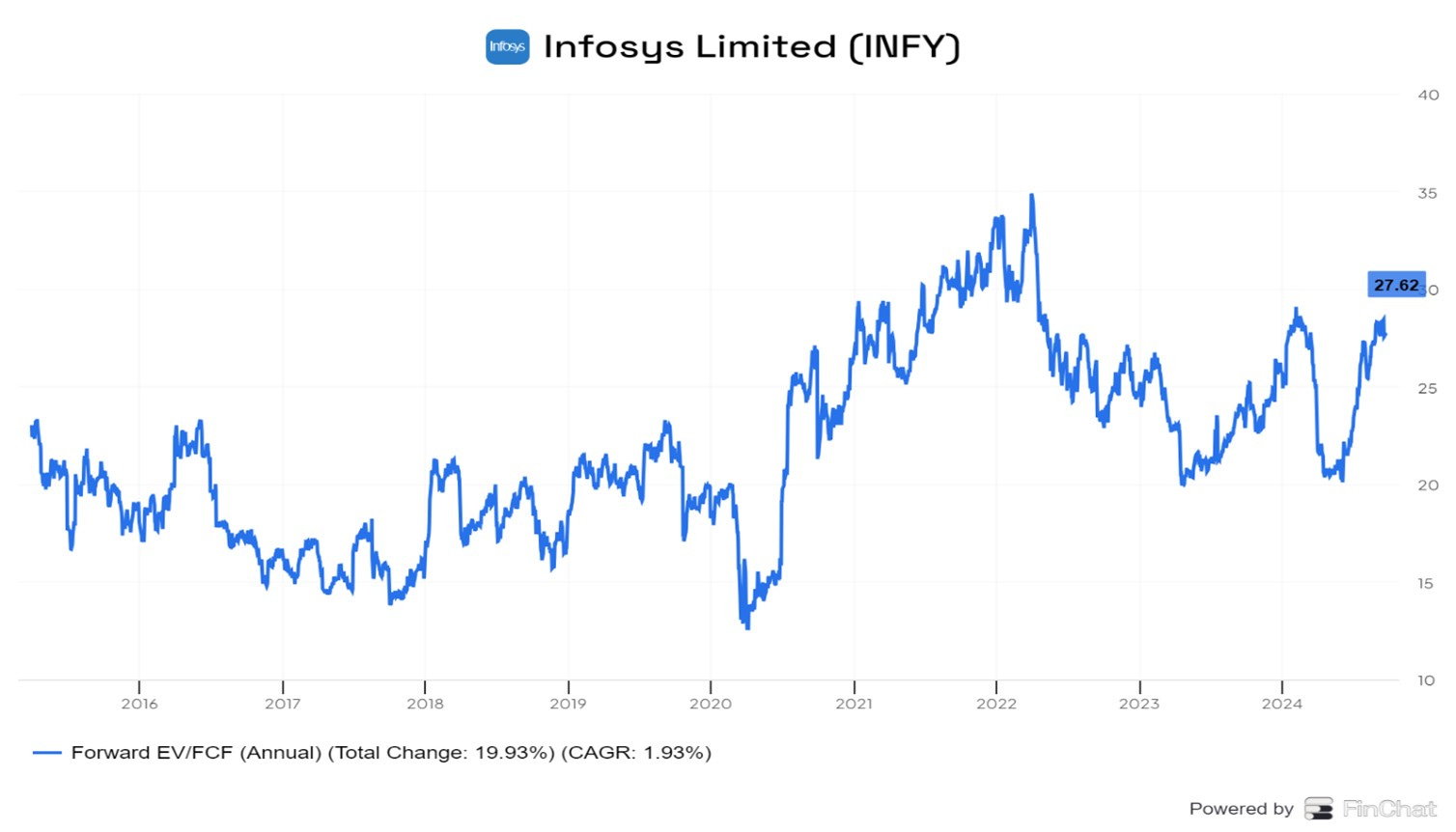

With these assumptions, we calculated a theoretical INFY ADR value of $18.3 – a 19% discount to the current value of the ADR of $ 22.7.

If the terminal exit multiple for EV/FCF is increased to an aggressive 34X, we get a theoretical value of $ 21.8 for ADR. The chart below shows the historic EV/FCF for Infosys and suggests the conservative assumption for the EV/FCF multiple is in the range of 20X - 24X.

Conclusions

We believe Infosys is great solid company. If it was a soccer team, we would say it has a very solid defence (scale, balance sheet, client relationships) but the attack will struggle to score a lot of goals due to some weakness (low growth, competition and current valuation).

We will not allocate Capital to INFY at this stage, but we will follow it and reconsider if the share price goes below $17.50 for the ADR.

I linked to your post my weekly Monday emerging markets links roundup: https://emergingmarketskeptic.substack.com/p/emerging-markets-week-september-30-2024

For better or for worse, I have owned INFY for about 20 years...