JP Morgan (JPM)

Q4 2024 Results

Introduction

On the eve of the Inauguration of President Trump, the legendary investor Stanley Druckenmiller was interviewed on US television. He said animal spirits among businessmen were at a maximum level as a very anti-business administration was being replaced by a pro-business one. Senior Management in the large banks, who presented their (very good) results last week, may be excused for being similarly excited.

There are three main reasons for this

2024 was a good year. The economy grew strongly, the Fed cut rates and boosted asset prices. Trading activity increased as stock indices advanced more than 20% for the second successive year.

The prospect of a new administration has boosted business confidence. It is likely to be more permissive on mergers and takeovers and may cut taxes, though difficult fiscal position probably makes this inadvisable.

Banks also believe the Trump administration will be more willing to ease their regulatory burden. They argue current regulations force them to hold too much capital and restricts their ability to lend.

JP Morgan

We have written twice before about JP Morgan. These reports can be found here and here.

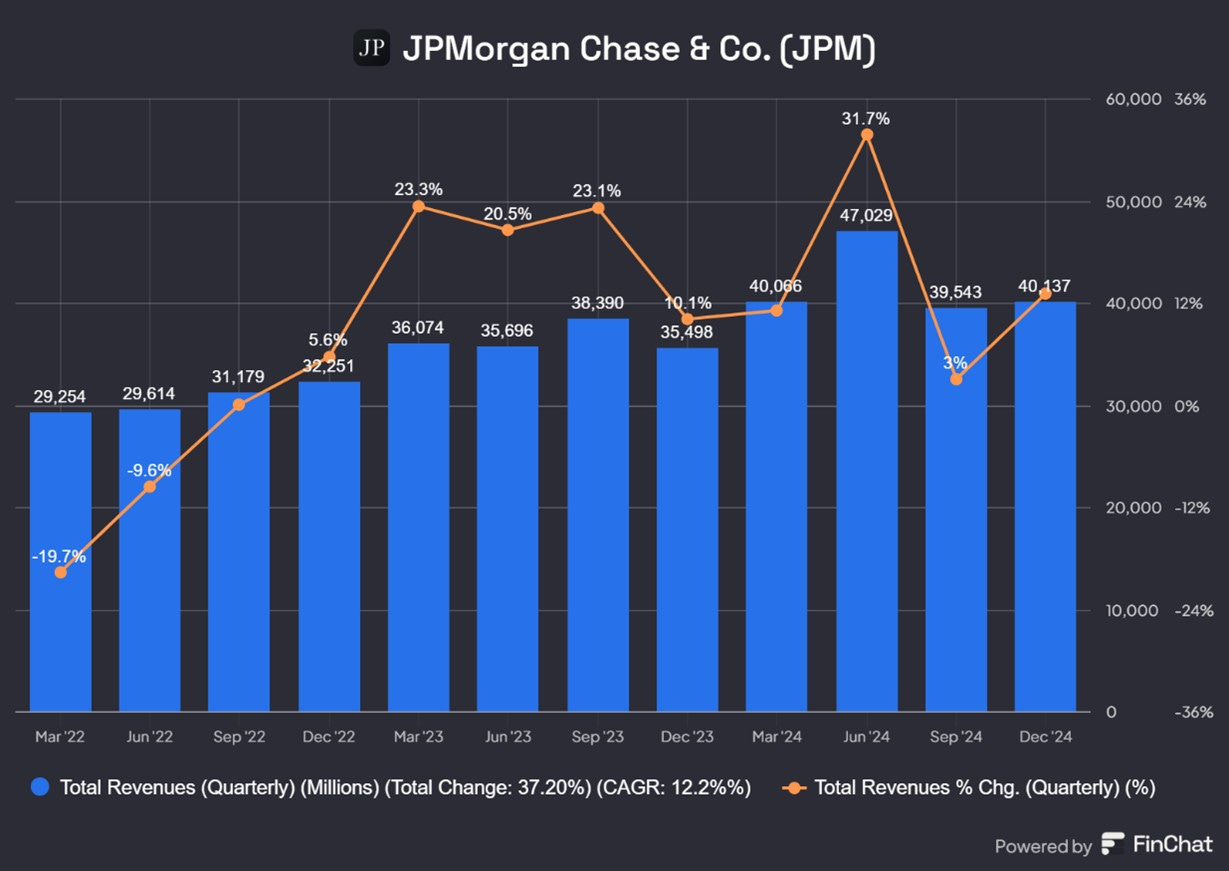

The big banks kick off the US quarterly reporting season and the numbers have been good.

JPMs Q4 Revenue rose 11.5% (y/y) to $40.1bn.

The firm reported net income of $14bn, EPS of $4.81 with an ROTCE of 21%.

Segments

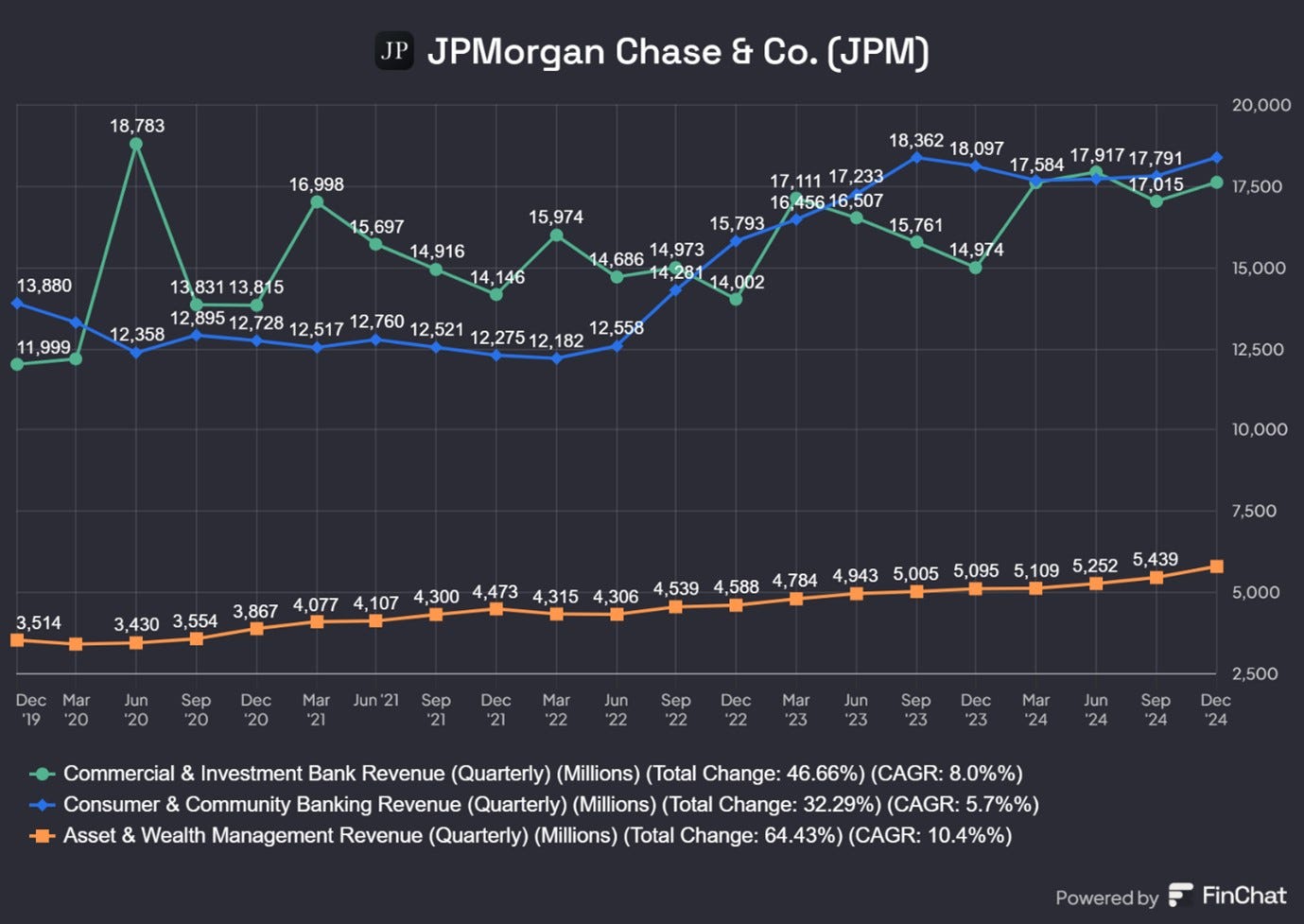

The retail business including housing finance and credit cards was subdued but wholesale banking and market related businesses did well.

Consumer & Community (CCB) only rose 1.4% (y/y).

However, booming markets boosted the Commercial and Investment Bank (CIB) and Asset & Wealth Management (AWM).

CIB revenues rose 14.9% (y/y) and 3.2% (q/q).

AWM revenues rose 11.6% (y/y) and 3.4% (q/q).

CCB

In CCB, Net Interest Income (NII) NII was down $548mn or 2%, driven by the impact of lower rates and the associated deposit margin compression.

CIB

In CIB, JPM saw record revenue in markets, payments, and security services.

CIB reported net income of $6.6 bn on revenue of $17.6 bn.

Investment Banking (IB) fees were up 49% (y/y) JPM was no 1 with wallet share of 9.3% for 2024.

Advisory fees were up 41%, benefiting from large deals and share growth in a number of key sectors.

Underwriting fees were up meaningfully with debt up 56% and equity up 54%, primarily driven by favourable market conditions.

Markets revenue was up $1.2 bn to $7bn (up 21%).

The Markets division saw similar revenue growth in both Fixed-Income and Equity.

Fixed income was up 20% with better performance in credit as well as continued outperformance in currencies and emerging markets.

Equities was up 22% on elevated client activity and derivatives amid increased volatility and higher trading volumes and cash.

AWM reported net income of $1.5bn with pre-tax margin of 35%. Revenue of $5.8bn was up 13% (y/y) driven by growth in management fees on higher average market levels and strong net inflows as well as higher performance fees. Expenses of $3.8 bn were up 11% (y/y) suggesting little operating leverage in AWM.

AUM of $4trn and client assets of $5.9trn were both up 18% (y/y), driven by continued net inflows and higher market levels.

They have a “fortress” balance sheet and ended the quarter with a Core Equity Tier 1 (CET1) ratio of 15.7%, with regulatory capital of $275bn.

Highlights of the earnings conference call.

After the Global Financial Crisis, during which many banks failed, global regulations were tightened and banks were required to hold more capital. Banks have used the last decade and a half of buoyant market conditions to build up their capital base. JPM has much greater capital than the regulatory minimum. They believe they have too much capital.

“It makes sense for us to have a nice store of extra capital in light of the current environment. We would like to not have the excess grow from here. It means more capital return through buybacks, all else being equal in order to arrest the growth of the excess, and that is our current plan.”

JPM have stepped up hiring in recent years and now believe they need to grow with the people they already have.

“we're going to try to run things, with some important exceptions, that I'll highlight in a second, on roughly flat headcount and have that lead to people generating internal efficiencies as they get creative with their teams and reconsider more efficient ways of doing things.”

Regulations have been tightened since the global financial crisis and banks have had to comply and build up regulatory capital, compliance and risk management. However, the industry, including JPM, are now pushing back against the increased regulatory burden.

“All we want is a coherent, rational, holistically assessed regulatory framework that allows banks to do their job supporting the economy that isn't reflexively anti-bank. It doesn't default to the answer to every question being more of everything, more capital, more liquidity. It uses data and it balances the obvious goal that we all share of a safe and sound banking system with actually recognizing that banks play a critical role in supporting growth. The hope is that we got some of that and that also while we're at it, some aspects of the supervisory framework get a little bit less bureaucratic and a little bit less adversarial and a little bit more substantive so that at the margin, management can focus its time on the things that matter the most.”

Despite improved business confidence, they are seeing little increase in the demand for loans

Given the significant improvement in business sentiment and the general optimism out there, you might have expected to see some pickup in loan growth. We are not really seeing that. I don't particularly think that's a negative. I think it's probably explained by a combination of wide-open capital markets. And so many of the larger corporates are accessing the capital markets and healthy balance sheets in small businesses and maybe some residual caution.

“And maybe there are some pockets in some industries where some aspects of the policy uncertainty that we might be facing are making them a little bit more cautious than they otherwise would be about what they're executing in the near term. We'll see what the New Year brings as the current optimism starts getting tested with reality one way or the other and maybe if it materializes with tangible improvements and things one way or the other, you'll actually see that come through C&I loan growth in particular.”

Wealth Management is one area where they scope for growth

“The biggest single one arguably is that in what you might call the affluent section of the wealth management space, we are significantly underpenetrated relative to the number of households that we bank in the country and our capabilities and our brand and what we think we bring to the table. So that's why we're pushing so hard on that front because I think we can get more share there and it completes the franchise very nicely.”

Credit losses have been very low for over a decade and they will rise at some point. One trigger for this could be rising unemployment and higher inflation (if it happens).

“We were coming out of a 10 plus year period of an exceptionally low charge-off rate. And so, at some point, that has to normalize to a slightly more reasonable level, - some things are still not fully normalized and arguably wholesale credit could be one of those. We do run extensive stress test on the sensitivities to the portfolio -- of the portfolio to rate shock. A lot of what we do from an underwriting perspective is designed to protect us from that, frankly. I would just point the biggest driver of credit has been and always will be unemployment, that's both on the consumer side and it bleeds into the corporate side. It bleeds into mortgages, subprime, credit card. Your forecast of unemployment, which you're going to have to make your own, which will determine that over time, and so -- and the second thing that you said vulnerabilities, it's unemployment, but the worst case would be stagflation, higher rates with higher unemployment will drive higher credit losses literally across the board.”

Comment

This was a strong performance by JPM driven by positive economic headwinds and favourable market conditions. The JPM stock rose strongly after the results. JPM stock has risen 55% in the last year.

Bankers are expecting that the good times to continue and the Trump government will boost business.

If taxes are cut and more take overs are allowed, asset prices will tend to rise and M&A bankers and financiers will get busy. Big banks are hiring Republican lobbyists to reach the Trump government on capital requirements and regulations.

Among the industry's goals are

lock in a much weaker version of the "Basel Endgame" capital rule,

reduce a capital surcharge levied on large systemically important global banks, (the so- called G-SIB charge)

re-work a key leverage constraint, and

overhaul the Federal Reserve's annual "stress tests". This is currently the subject of a lawsuit between the industry body and the Fed. See here for details on this.

Under Trump's first term, U.S. banks scored some de-regulatory wins, including a loosening trading rules and simplification of stress tests. However, they did not secure a comprehensive review of big bank capital rules implemented after the global financial crisis.

The beefed-up regulations have worked well. Banks say capital requirements are excessive and poorly calibrated, and some of that cash could better serve the economy by being lent out.

The industry tasted partial victory last year after intense lobbying succeeded in halving the additional capital banks would have to hold under the Basel proposal, and prompted the Fed to review its stress test process. The capital increase was reduced from 19% to 8%.

Buoyed by those wins, and with Trump due to appoint new industry-friendly officials - including a new Federal Reserve regulatory chief nearly 18 months earlier than expected - banks see a unique opportunity to reshape capital rules. This follows the early departure of the Federal Reserve Vice Chair for Supervision Michael Barr. This was to avoid a battle with the Trump administration and paves the way for a more bank-friendly successor to be appointed. More details on this can be found here.

David Solomon, CEO of Goldman Sachs said he expected the change in administration would lead to a new approach to capital rules.

"It feels like we're in an environment where there could be a constructive discussion about improving the transparency, clarity and consistency around this,"

After years of criticism for the financial crisis, large banks feel they now need to move on. They played a key role in stabilizing regional banks such as Silicon Valley Bank in 2023. They feel the tide of regulation needs to be reversed.

The Trump administration is likely to be sympathetic and banks will get a significant boost from a dilution of regulation.

Valuation

At the current price of $261.8 per share JPM is trading on a one -year forward P/E Ratio of 14.3X. This is an earnings yield of 7%. This looks like a reasonable valuation for a company likely to grow revenues, net profits and EPS at 8%, 9% and 11% respectively, for the next few years, and likely to achieve an ROE in the 14% to 18% range.

The dividend yield is 2%, perhaps a little on the low side, but the dividend is likely to rise as it is quite well covered.

The Price to Book Value (P/B) and the Price to Tangible Book Value is 2.3X and 2.87X respectively and they look high. As the chart below shows the P/B Ratio has trended higher and is currently at a ten-year high.

Conclusion

JPM shareholders are likely to benefit from buoyant conditions, a possible Trump boost to the economy, a possible easing of capital requirements and regulatory burdens and increased share buybacks as “excess” capital is returned.

If you want to invest in banks, JPM is probably the best in class, and can safely be a part of your portfolio. However, the bigger question is should you invest in banks at all?

Terry Smith, the highly successful investor at Fundsmith does not invest in banks. He believes they are a black box and it is difficult for an outsider to know what is going on inside. He has cited a number of reasons for staying away from banks. They include the following:

Complex business models that make it difficult to truly understand their assets and liabilities.

High leverage ratios inherent to banking business models, which create significant risks. – Leverage is inherent but valuations reflect this.

Banks are highly cyclical businesses tied closely to economic cycles, making their earnings less predictable. This is true but valuations probably reflect this.

Returns on equity tend to be lower than other sectors he prefers to invest in, particularly consumer staples and technology. This is true but it is definitely reflected in the valuations.

Heavy regulation of the banking sector can impact profitability and business flexibility. This is undoubtedly true.

I would like to add two more reasons to Smith’s list.

Banks have an annoying habit of blowing up and destroying shareholders every one or two decades.

Banks which have large wholesale businesses and Investment Banks are trophy assets like Sports Franchises. In both cases, it is much better to be an employee than a shareholder.

But enough of lists let us look at the data. As Narayana Murthy, the co-founder of Infosys (and the father- in-law of former British Prime Minister Rishi Sunak) said “In God we trust, everybody else must bring data to the table.”

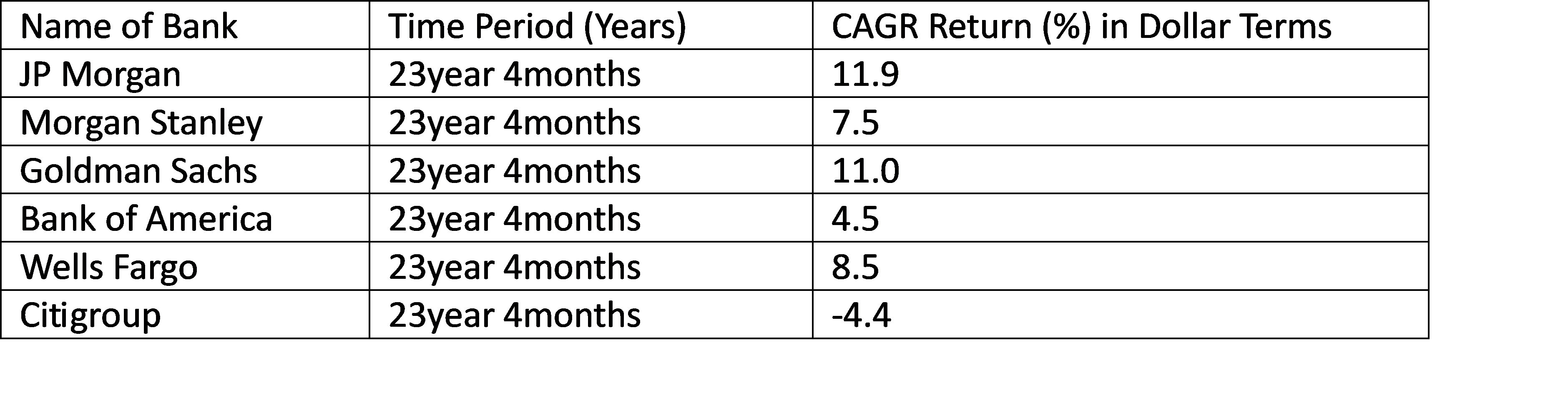

The returns this century have not been great. The global financial crisis did not help.

JP Morgan and GS lead the pack with CAGR returns of 11.9% and 11.0%. Over the same period, the S&P 500 ETF (SPY) and Nasdaq 100 ETF (QQQ) have generated a CAGR return of 9.6% and 13.2%. GS and JPM have given performance that is equal to an equal weight portfolio SPY and QQQ. Good but not spectacular.

Conclusions

As investors “you pays your money and you takes your choice”. Going forward, We will just follow GS and JPM in the banking sector. However, we are not currently invested in either.