Meta

Comments in the light of most recent quarterly results

I make some comments on Meta (formerly Facebook) in the light of its most recent quarterly results. I will not comment on all aspects of the Quarterly Report as these have been covered extensively elsewhere.

The graphic above shows the evolution of Meta.

2004 - Facebook launched

2006 - Newsfeed launched - FB mobile launched

2012 - Acquired Instagram and IPO

2014 - Acquired WhatsApp

2014 - acquired Oculus VR

Their Family of Apps (FOA) (Facebook, Messenger, Instagram, and WhatsApp) delivered a huge audience - some 3bn engage daily and 3.9bn do so at least monthly. Given that China is a no-go and the world population is 7bn, this is an impressive number. They had to keep that maximise the audience engagement and gather as much user information as possible, in order to boost the quality of targeted advertising which increased the ROI of the ad spend A huge audience was delivered, and advertisers were happy to pay up and the company prospered mightily

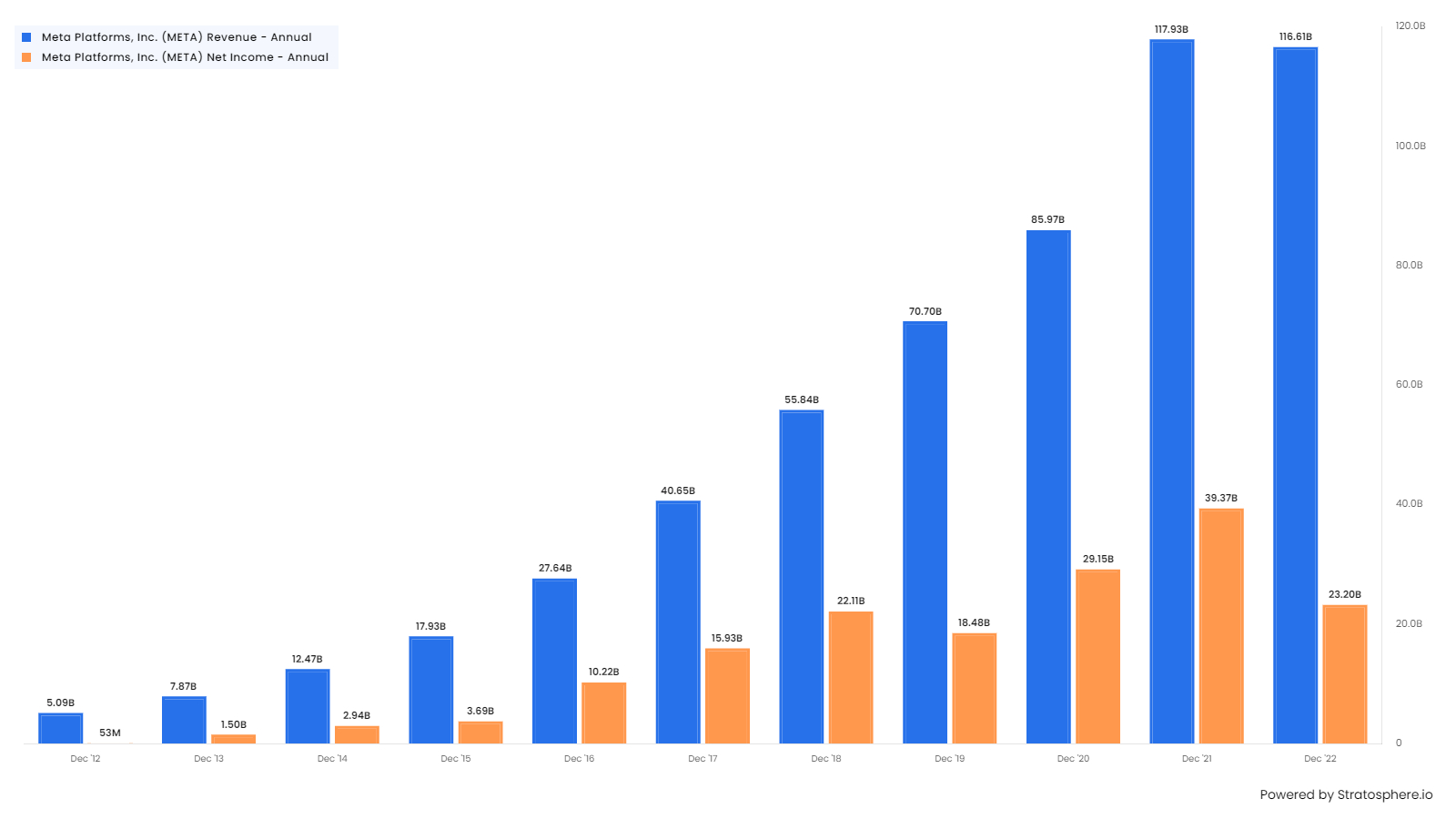

Total revenue grew from US$ 5.1bn in 2012 to 116bn in 2022

Net profit grew from US$ 53mn in 2012 to 19bn in 2022

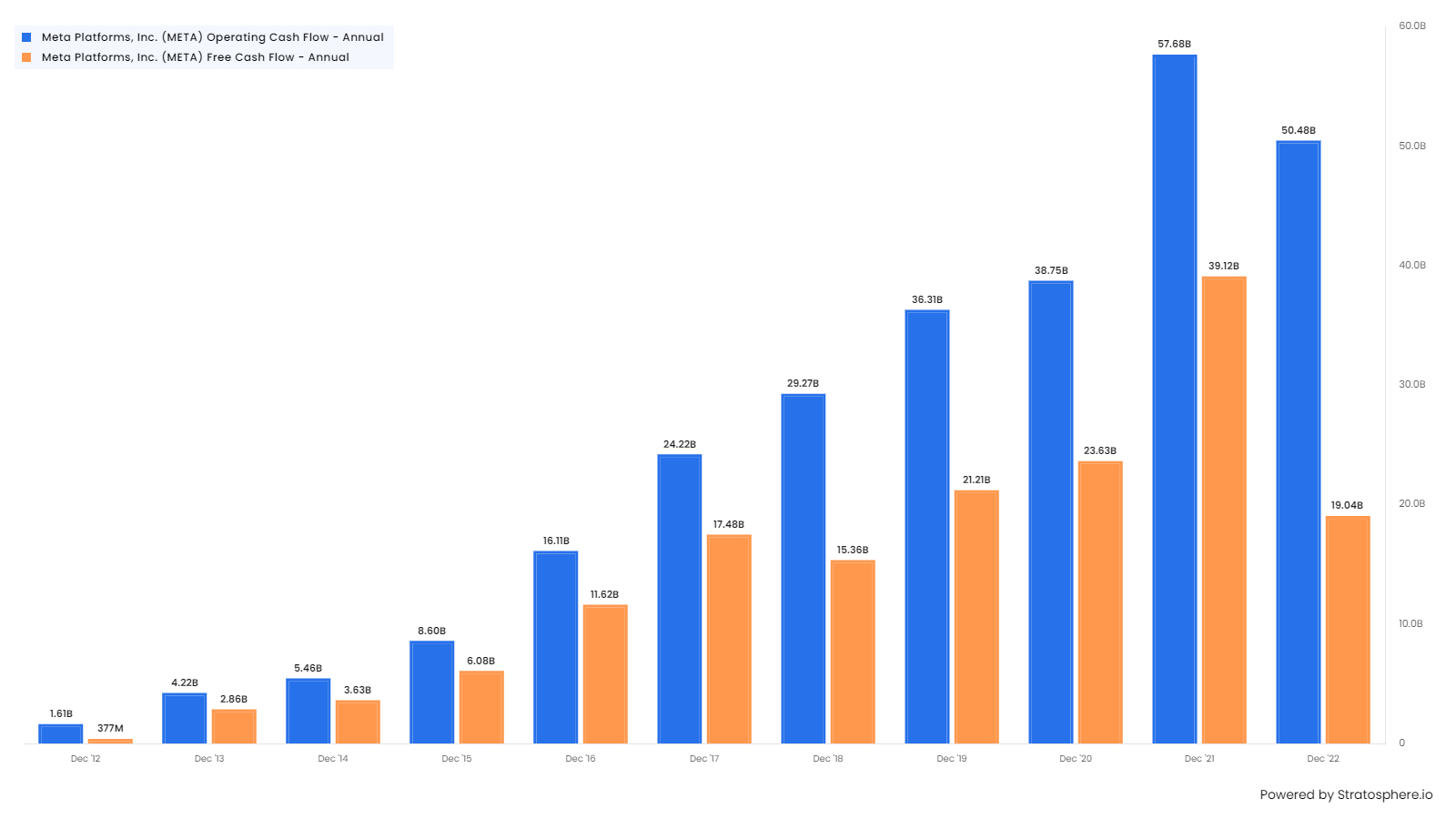

Operating Cash Flow grew from US$ 1.6bn in 2012 to 50.4bn in 2022

Free Cash Flow grew from US$ 377mn to US$ 19.1bn in 2022

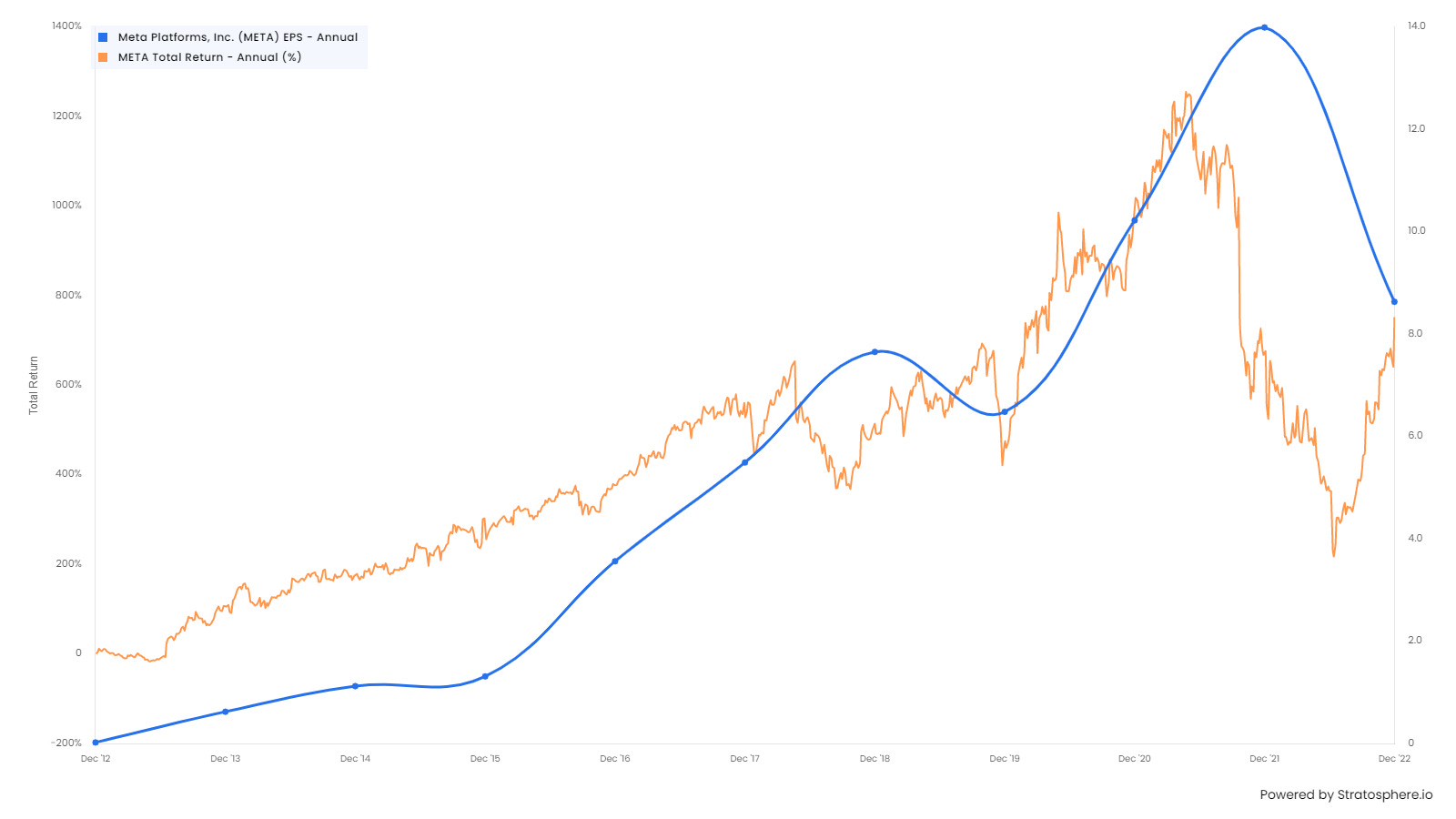

Earnings per share grew from US$ 0.02 in 2012 to US$ 9.15 in in 2022.

The return for the IPO investor reached 1200% in early 2021 before the correction in the last two years.

The company and the stock price has been a huge success in its first decade as a public company

However, in mid 2022 some serious questions began to emerge. There were three main questions>

The first question related to Apple and IDFA.

Apple decided in 2020/2021 to make IDFA an opt-in feature in its operating system upgrade to iOS-14. IDFA stands Identifier for Advertisers) crates a unique identifier assigned to each Apple device that allows advertisers to track user behavior across multiple and target ads. These IDs were freely available and third parties were harvesting them and selling them to marketers raising privacy concerns. Only 10% of Apple device users were thought likely to Opt-in to IDFA. This was a big blow to the effectiveness of targeted advertising and Meta was expected to be the worst hit of the large Social Media companies. In early 2022, the company estimated that the revenue impact would be US$ 10bn or 8% of total revenue.

The second problem was Tiktok

Although Meta user numbers were high, Tiktok was growing much faster especially among younger people as its algorithms worked hard to provide short films based on user history and boosted engagement significantly. If users were spending more time on Tiktok, the advertising dollars were likely to flow from Meta FOA to Tiktok.

The third problem was the Metaverse

The Metaverse can be defined as a virtual world where people can interact with each other in a more immersive and realistic way than is currently possible on phones or computers. Mark Zuckerberg was prepared to make a big bet on the Metaverse and changed the name of the company from Facebook to Meta. Investors worries that huge expenditures would be made on a “personal project” that might not generate significant returns in the short to medium term if at all. This added to a more general concern that employee and compensation growth was out of control

These worries were not without foundation.

The threat from IDFA removal from Apple was real. As the chart above shows , revenues peaked in 2021 at US$ 117.3bn and fell to US$ 116.61bn in 2022.

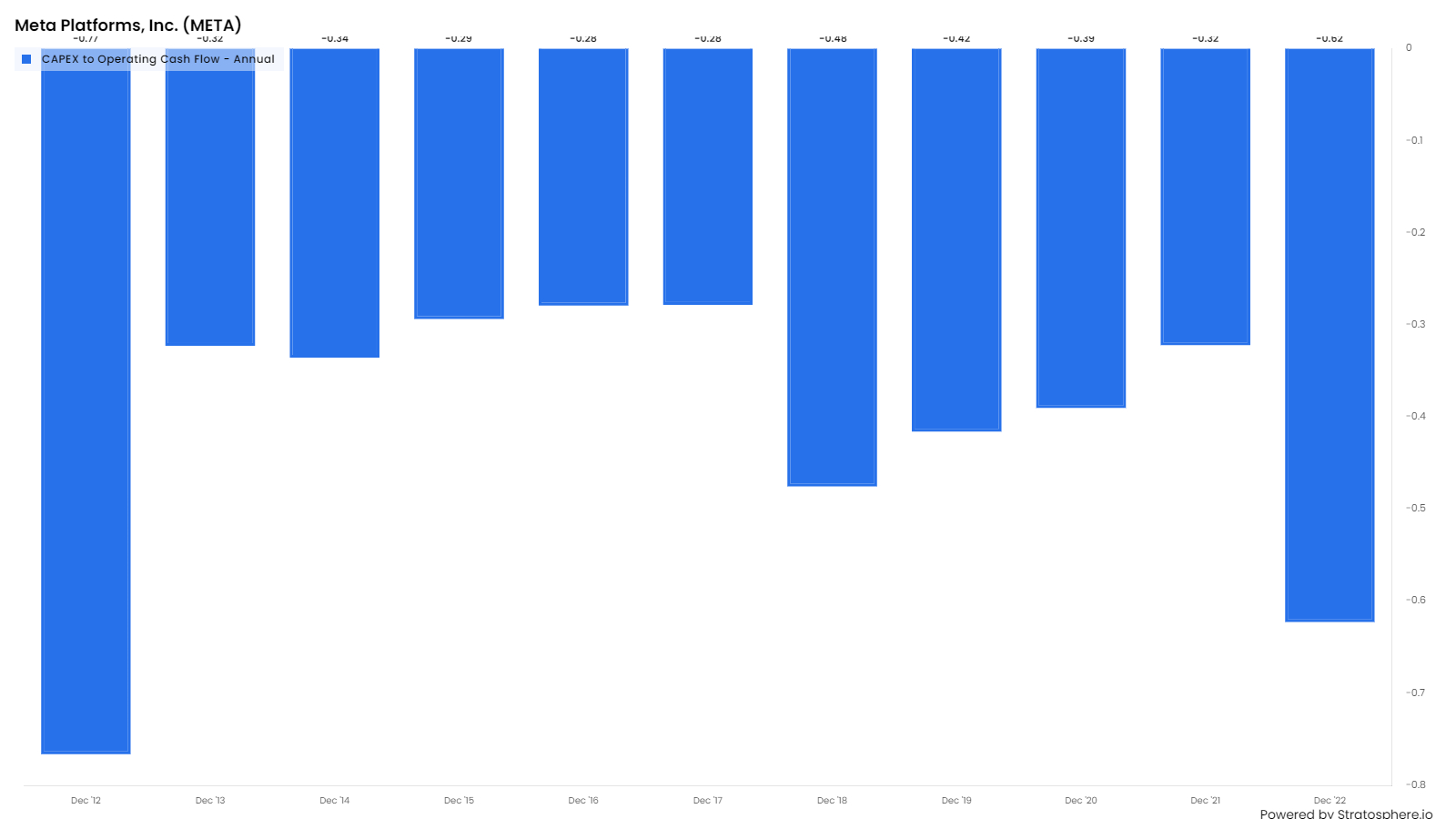

R&D expenses increased greatly due primarily to Metaverse investments. The chart below shows that R&D expenses at US$ 35bn in 2022 double the figure of 2020. 62% of the Operating Cashflow was devoted to Capex ( see bar chart below). the highest level since 2012. As the chart above shows, Free Cash Flow fell to US$ 19bn in 2022 compared with US$ 39bn in 2021.

The Chart below shows Capex as a percentage of operating cashflow rose to 62% in 2022 ( Shown as a negative as capex is an outflow).

These worries and fears had an impact with the share price falling from US$ 360 in August 2021 to US$ 91 in November 2022. End-December 2022 market was 323bn compared with US$ 947bn a year earlier. The share price has doubled so far in 2023.

The earnings numbers released this week and the conference provided some positive indications on the three concerns

1 . Q123 ad revenues grew 4.1% (y-o-y) and ARPU only fell 1.7%.

Total monthly average users(MAU) grew 4.7% suggesting the impact of the removal of IDFA has not been as bad as feared. There were few references to IDFA in the conference call.

Tiktok

Meta responded to the threat of Tiktok by introducing Reels to the Facebook menu of Newsfeed and Stories. In the conference call they noted the following:

2 billion reels are shared per day up 100% from 2 quarters ago.

The company is “gaining share in short form video.”

Reels and AI investments have led to a 24% rise in time spent on Instagram since inception.

Reels monetization efficiency is up 30% QoQ on Instagram and 40% QoQ on Facebook.

They did note that as Reels are longer than Stories, it more difficult to monetize on a per second rate as users would be irritated if there were as frequent advert interruptions on Reels as there are on stories.

This suggest that Meta has quickly scaled up Reels and are meeting the challenge of Tiktok though the latter remains a formidable challenger

Metaverse and Capex.

There was very little mention of the Metaverse but a lot of mention of AI which is the current buzzword. At one point, Mark Zuckerburg said something to the effect that Metaverse investments were AI investments.

“We've been focusing on both AI and the Metaverse for years now, and we will continue to focus on both. The 2 areas are also related. Breakthrough in computer vision was what enabled us to ship the first stand-alone VR device. Mixed reality is built on a stack of AI technologies for understanding the physical world and blending it with digital objects. “

The company has tackled general cost escalation and have announced three restructurings , two of which have already occurred. They took a US$1bn charge with respect to this and expect to take US$3-5bn for the full year. This not trivial but is manageable and is non-recurring and will hopefully bring employee growth and costs much more in control.

The Metaverse continues to be an area of investment even though the emphasis is now on labelling it AI. Meta indicated that capital expenditure in 2023 will be at similar level to 2022 (@US$32bn). In 2022, this level of Capex meant that Operating Cashflow of 50bn was reduced to a Free Cashflow of just US$ 19bn. We like to see companies that look to grow Free Cashflow over time and worry that Meta is moving in the opposite direction. The substantial investments in Metaverse could prove to be money down the drain.

Other points

Some investors have been looking for the plan to monetise the 2.4bn Whattsapp user base.

The call gave some updates on this. They noted click-to-message ads ( mainly on Whatsapp) continue to grow and bring incremental demand onto our platform. This format is mostly used by smaller advertisers today in Southeast Asia and Latin America, and one of the exciting opportunities ahead is to expand adoption to larger advertisers in more markets by investing in increased automation and reporting to help businesses more easily manage messages and measure results at scale. This is encouraging

The graphic above shows FOA operating profit was US$ 11.2bn but an operating loss of US$4bn in Reality Labs (the Metaverse business) reduced overall operating profit to US$ 7.2 bn. Reality Labs is expected to make losses on this scale for a few years.

Conclusions

The quarterly was a good set of numbers for Meta.

The company has overcome the headwinds of IDFA and Tiktok and has very belatedly brought some control over costs and increased the emphasis on operational efficiency.

We look for companies that generate a lots of Free Cash flow and allocate that capital well. META is suspect on both these grounds.

Capital expenditure is set to remain high and this will serve to depress Free Cash Flow.

Meta allocation of the Free Cash Flow is generated is suspect. The company spent billions buying back shares when the market cap was much higher and then sought to conserve cash when the share prices and the market cap collapsed in 2022. Stock-based compensation remains elevated.

The share prices has risen100% this year and at a forward PE of 20 times and a Free Cash flow Yield of 3% no longer look cheap.