We have written one posts about Meta. This dates from 28th April 2023 and can be found here.

Mets has three key properties, Facebook, Instagram and WhatsApp. About 3bn people access one of these apps daily and 4bn users do so at least once a month. This is a huge base given the global population is about 8bn.

The large crowd attracts advertisers. Meta has to increase the frequency and duration of the visits to their properties. It also provides tools and services which helps advertisers target the right people for their messages and thus improve the Return on Investment (ROI) for their advertising dollars.

This has been an incredibly successful business model which generates lots of free cash flow. This excess cash is being used to develop new products and services such as those in the Metaverse and in AI.

The stock has been very volatile. In the last three years, the stock has lost 75% of its value (from 400 to 100) and then gained 400% (from 100 to 400). It is at 487 after the results.

Meta Q4 Results

Fourth-quarter earnings were better than Wall Street expectations.

Meta reported EPS of $5.33 per share versus estimates of $4.91 and

Revenue of $40.1bn versus estimates of $39.0 billion.

The first-quarter guidance was higher than expected.

Meta beat free cash flow (FCF) estimates by 28%.

Meta is increasing its share buyback program by $50 billion and will pay a dividend for the first time.

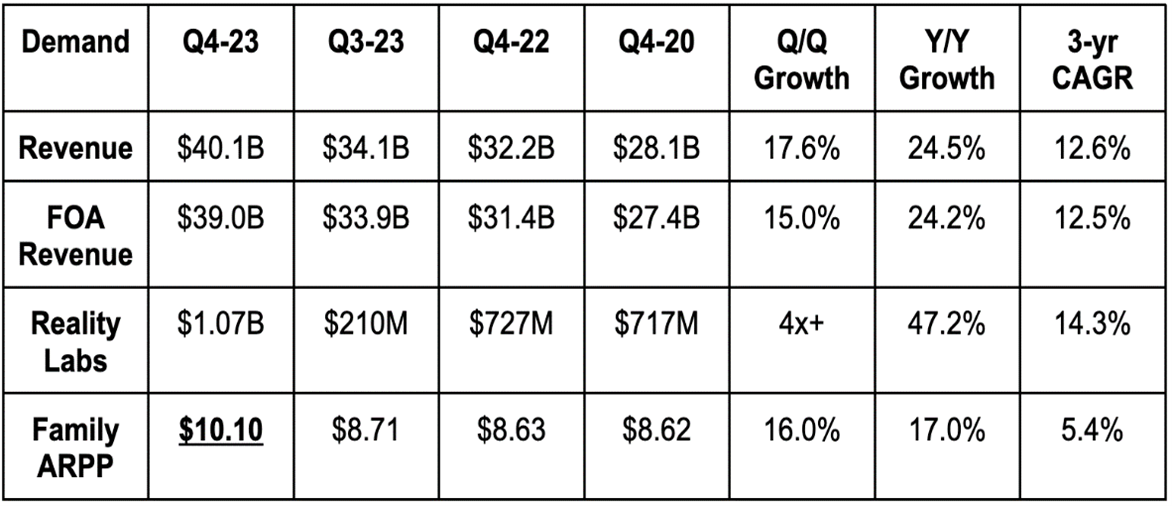

FOA = Family of Apps; ARPP = Average Revenue per Person

FOA= Facebook, Instagram, Messenger, WhatsApp and other services.

Source: The Stockmarket Nerd

Quarterly Revenue was $40bn and grew 24.5% (y/y)

Reality Labs (the Metaverse segment) was $1.1bn.

The ARRP increased 17% to US$ 10.1. This is a global average. Annual ARPU in North America reached ~$220 in 2023 (a staggering figure) but is obviously much lower elsewhere.

DAU = Daily Active User; MAU = Monthly Active User

Source: The Stockmarket Nerd

User engagement continues to increase. Total Daily Average Users (DAU) across the Family of Apps (FOA), is now 3.2 bn and grew by 7.6%

Monthly Average Users (MAU) is almost 4bn (50% of global population!).

Source: The Stockmarket Nerd

As an indicator of increasing engagement, the DAU to MAU ratio is at 80% is at an all-time high. The DAU/MAU ratio has been inching up for the last eight consecutive quarters. DAU/MAU rose QoQ in every single region. This increasing engagement is a global phenomenon.

The numbers of visitors are growing steadily, and they are watching many more advertisements as shown below.

Source: MBI Deep Dives

The number of advertising impressions increased 21% and the average advertisement price increased by 2% after seven quarters of declines.

Source: MBI Deep Dives

Advertising Revenue in Q4 23 was $38bn and is 95% of Total Revenues. Reality Labs (the metaverse business) makes up the rest. Note FOA EBIT Margin is 53.9% (above 50% for the second consecutive quarter) but overall EBIT Margin is much lower at 40.8% due to losses at Reality Labs.

Source: Stratosphere.Io

Operating Margins have recovered strongly in the last year.

Balance Sheet

Balance sheet continues to be very strong.

$65 billion in cash & equivalents

$18.4 billion in debt.

Basic share count fell 2.8% Y/Y.

$80.9 billion left in buyback capacity as it added a new $50 billion buyback programme.

Guidance

Next quarter guidance was a robust 5.5% ahead of expectations. This was a positive surprise for the market.

2024 operating expense (OpEx) guidance was reiterated at $96.5 billion. Capital Expenditure (CapEx) guidance was raised from $32.5 billion to $33.5 billion due to ramping investment in AI infrastructure to support the technology’s boom. Infrastructure investments will continue to grow beyond 2024.

Conference Call Highlights

Highlights

As was the case with Microsoft and Google, AI was the main focus during the call.

Mark Zuckerburg’s talk outlined a 5-part plan to ensure Meta leads in AI for decades to come.

Part 1 is building world class AI infrastructure.

The company has given a huge order for 350,000 Nvidia H100 Chips this month to ensure secured supplies. Zuckerburg noted that Meta is going to “remain on the offensive here” and will “play to win.”

They are betting on what they call “general AI” (multi-modal models that can do everything from reason to plan, to code, to remember”)

“After underspending on Reels, I decided that we should build enough capacity to support both Reels and another Reels-sized AI service that we expected to emerge to avoid that situation again. The decision at the time was controversial, but I’m so glad we made it.” –

Part 2 is its open-source approach to software.

Meta makes its “general infrastructure” available to all developers “while keeping specific product implementations and data proprietary.”

This means it does not give up its competitive edge while letting 3rd party developers build in its ecosystem.

App developers want access to Meta’s unrivalled consumer traffic. They want to build products they know will be bought and utilized. Meta delivers this with Llama (it LLM model) and 4 billion people on its FOA.

Foundational models are likely going to be commoditized in the future. Meta is flooding the market with open-source Llama models knowing that it can monetize elsewhere with subscriptions and a app take rates.

Part 3 is taking the “long approach to development” as it has already begun work on Llama models up to version 7.

They are investing in products which may be rolled out in 2 years and others which may not see the light for 10 years.

Part 4 is utilizing its world-class data set to train algorithm.

The 4bn user space means they have a lot of data that algorithms can be trained on.

Part 5 is supporting a culture of rapid experimentation.

This 5-part process will deliver many products including:

Meta AI (a GenAI assistant just released into beta testing),

Business AI products (for customer support),

Creator AI series to help anyone create a personal AI and more.

Advertising.

Meta is using AI and other techniques to better target advertisements to its 4bn users.

Meta Shops Ads (designed to pull consumers to your stores) crossed a $2 billion revenue run rate. This type of on-site conversion advertising, along with other business messaging products, make Meta even less reliant on 3rd party data access. This was a worry after Apple’s made changes to its data sharing policy changes.

“Shops ads, we talked about the $2 billion annual run rate in Q4 after we just opened availability to all U.S. advertisers in Q2.”

“…eligible Shopify businesses can now onboard to shops on Facebook and Instagram very seamlessly. And we're making it easier for advertisers to turn their existing ads into shops ads. And we'll continue to focus on deepening integrations with partners and leveraging AI to make shops ads even more performant.”

Our approach to optimizing ad levels in our apps has become increasingly sophisticated over the years as we've developed a better understanding of the optimal place, time and person to show an ad, which has enabled us to adopt a more dynamic approach to serving ads. We expect to continue that work going forward, while services with relatively lower levels of monetization like video and messaging will serve as additional growth opportunities.

Metaverse:

Quest 3 headset is off to a “strong start” as it topped the app store rankings list for the holiday season.

Ray Ban will make more smart glasses due to “high demand.”

Reality Labs made $1 Bn revenue for the first time, thanks to Quest 3 and Quest 2 headset sales during Christmas season but the losses have shown no signs of peaking.

In fact, Meta mentioned again for 2024, “for Reality Labs, we expect operating losses to increase meaningfully year-over-year due to our ongoing product development efforts in AR/VR and our investments to further scale our ecosystem.”

WhatsApp is finally gaining users in the United States after many false starts in the past. WhatsApp’s newer “Channels” (one way messaging to large groups of people) product is growing rapidly. It has 500 million MAUs since launching last quarter.

“Business messaging from WhatsApp is becoming a material part of the business. It drove 82% Y/Y growth in FOA’s other revenue segment to reach $334 million.”

WhatsApp Channels could be a significant revenue opportunity in the USA.

Reels

Reels are short films that are “pushed” to the user on Facebook. Reels is now an important growth phase. It enjoys 3.5 billion re-shares per day.

“We're seeing sustained growth in Reels and video overall as daily watch time across all video types grew over 25% year-over-year in Q4 driven by ongoing ranking improvements.”

Key Financial Metrics:

Operating Expenditures fell 8% Y/Y mainly due to lower restructuring charges and headcount reductions.

Headcount fell a significant 22% Y/Y but rose 2% Q/Q as Meta resumes selective hiring.

Valuation

At today higher price of $478 per share, Meta is trading at a forward multiple of 22.4 times. Company is likely to grow at 20% a year for the next few years at a Return on Equity (ROE) of 20% to 24%.

The company had demonstrated a strong ability to get billions of daily users, keep them engaged and target advertisements to them. The company is also investing aggressively in AI investments and its open-source approach seems sensible as it will attract independent developers who will do much of the heavy lifitng.

The Metaverse investment continue are likely to lead to large losses for a few years at least. Apple’s launch of its Apple Vision Pro headset has signalled their interest in this area. Meta seems determined to contest this area with them in what could be David vs Goliath type battle given the larger size of the latter.

A Meta investor has to take act in faith that this will prove to be profitable in the long run. In fact, any investment in Meta is an act of faith in Mark Zuckerberg He started Facebook 20 years ago and is still only 38 years old. He could be running Meta for the next thirty years,

Comments

This was a very strong set of results, and the Stock is trading 21% higher today.

Our previous reports had been cautious. We were worried about the large investments that Meta was making on the Metaverse on what seemed like a personal project.

Our worries were misplaced for two reasons:

First. Meta embarked on a strong cost cutting drive in 2023 in what was called the year of efficiency. This has worked very well as can be seen in the strong recovery in operating margins.

Meta seems to like operating as a leaner company and it looks as if cost cutting has become part of its DNA.

“we're in a place now where the business is performing well. And I think the obvious question would be, okay, well, given that, should we just invest a lot more in things?

And the biggest thing that's holding me back from doing that is that at this point, I feel like I've really come around to thinking that we operate better as a leaner company.

Even beyond 2024, my operating assumption is that we will also try to keep it relatively minimal because I think that -- until we reach a point where we're just really underwater on our ability to execute, I kind of want to keep things lean because I think that's the right thing for us to do culturally.”

Second. Meta has increased revenues impressively than to a growth in users on the FOA, increase in user ad impressions and a recovery in the price of the ads.

Source: Stratosphere.io

Conclusions

We have been wrong in our reading of Meta in the past.

We are rating it as a Buy at current levels due to its strong reach, its ability to monetise their vast user base and as a call option on AI, the Metaverse and Mark Zuckerburg,