Meta Platforms (META)

Q1 2024 Results

We have written a few times on Meta Platforms Inc (META) which can be found here, here and here. We are revisiting Meta in the light of its most recent Q1 2024 results.

Introduction

The key fact about Meta is that virtually all of its revenues come from advertising.

Their goal is to maximise the number of people who visit their platforms (Facebook, Threads, Instagram and WhatsApp a.k.a the Family of Apps (FOA) and maximise the amount of time they spend on these platforms.

Meta needs to maximise the number of ad impressions aimed at these users and convert the impressions in revenue. Lastly the revenue must be maximised. This is a function among other things of how well targeted the adverts are. The quality of the targeting depends on the amount of data, Meta has on its users.

Meta no longer breaks down users for each app but for the whole FOA the number of Daily Active Users (DAU) is 3.24bn and annual revenue per user is about $ 44. Monthly Active Users (MAU) data will no longer be released but it was at 4bn at end 2023. This gives the approximate annual revenue run rate of $ 160-176bn 4bn x $44). given Meta is not allowed to operate in China, an MAU of 4bn is an impressive number.

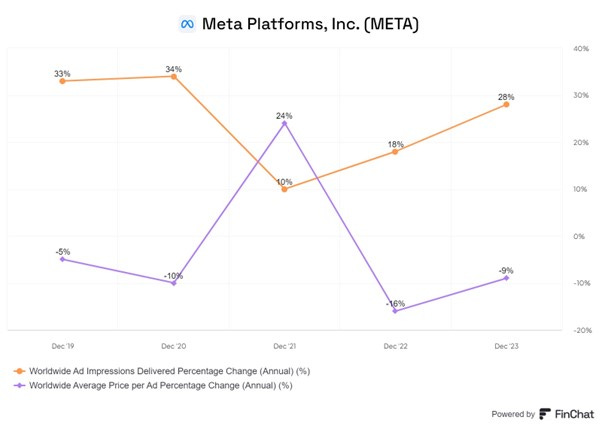

The number of ad impression grew at 28 % last year but the revenue per impression fell 9% so net advertisement revenue growth of ~16%

In the most recent quarter, ad impression grew by 20% but crucially revenue per ad impression grew by 6% which pints to revenue growth of ~27.2%. One of the key questions will be whether they can continue to increase the revenue per ad impression.

Detailed Q1 Numbers

DAU was at 3.24bn (+7.3%) and average quarterly revenue per user was $ 11.2 (+18.3%)

Total Revenue was $ 36.5bn (+27.6%)

Meta beat revenue estimates by 1.0% & beat its revenue guidance by 2.0%.

Meta beat daily active user (DAU) estimates by 5.0%.

Ad revenue growth in Asia Pacific and Rest of the World grew at 41% and 30%, respectively. Europe and North America grew 24% and 19%, respectively. Asia Pacific was driven by a Chinese company in e- commerce (Temu(?)) and in online gaming.

Over a 3-year period, revenues grew 11.7% CAGR while EPS grew 12.6% CAGR which indicates limited operating leverage in the last three years. However in the current quarter, cost rose much less than revenue and there was huge operating leverage. This suggests the “lean corporation” they pushed for in 2023 is being maintained and delivering results. This is a significant positive for the stock.

Margins

Margins have grown impressively. EBIT margins were at 37.9% some 12 percentage points higher than the same level in the previous quarter.

Gross Margins and Operating Margins are stable at about 81% and 39% respectively

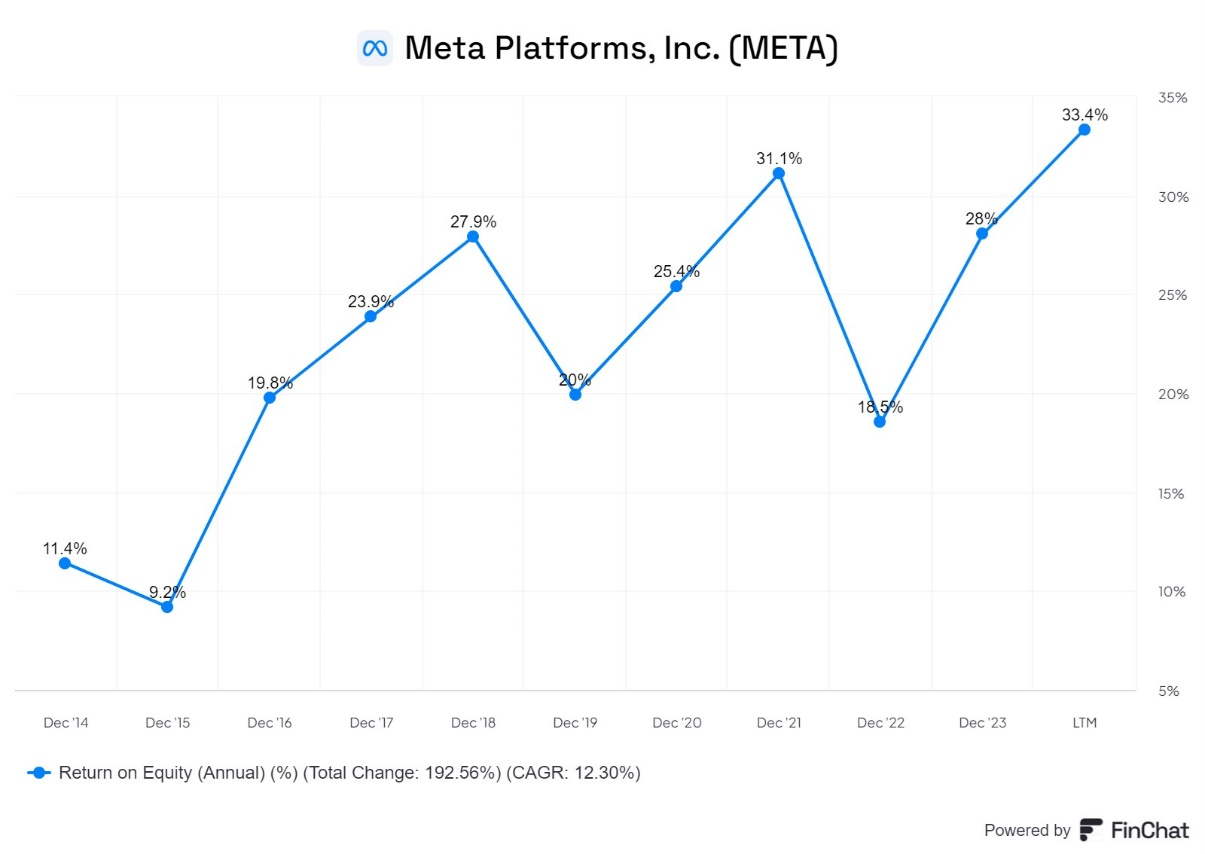

Profitability has risen impressively with the ROE hitting a ten-year high at 33.4%

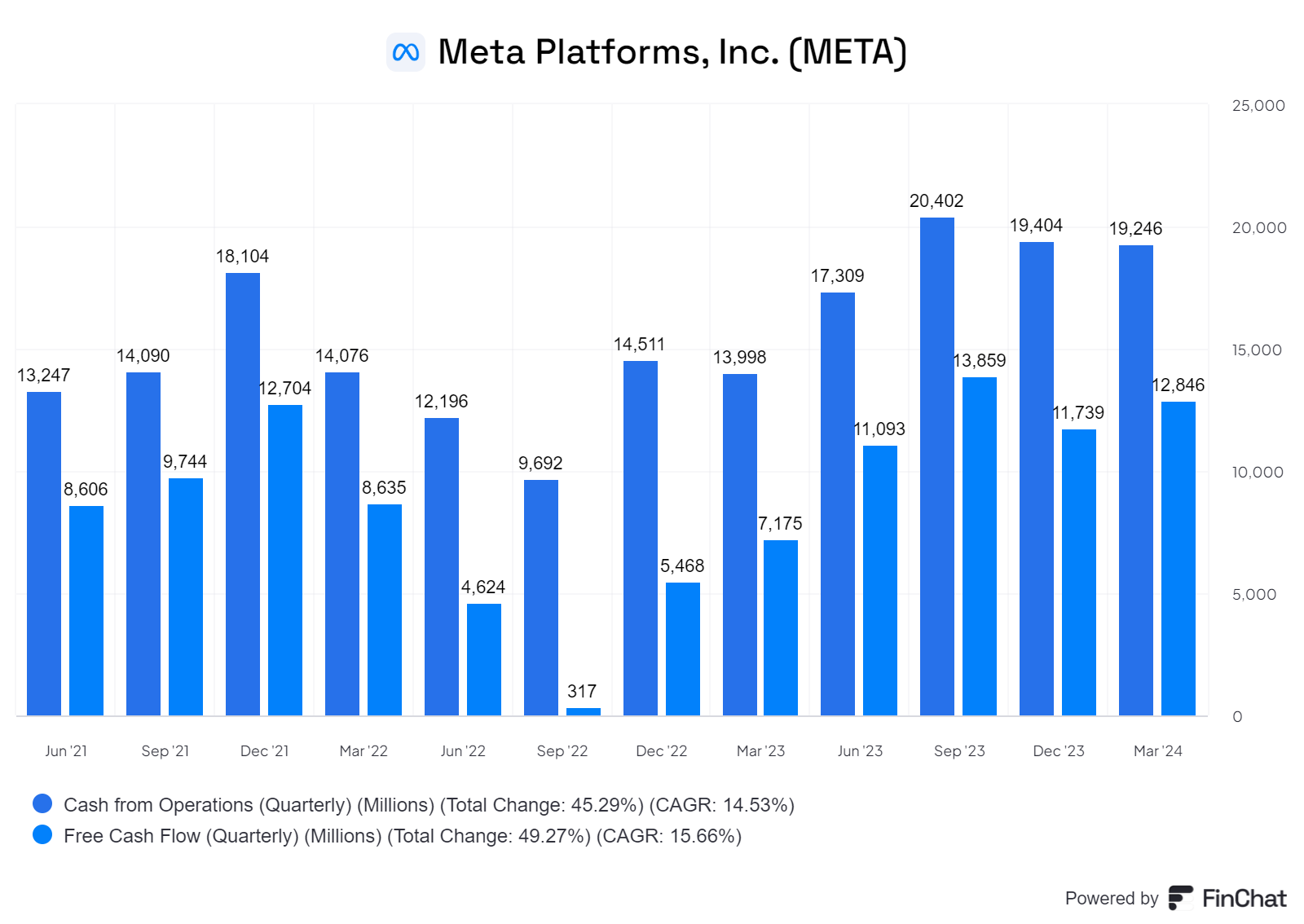

The annual run rate for Cash From Operations is an impressive $ 76bn. Free Cash Flow (FCF) in 2023 was $ 43bn. The business has tremendous power to generate cash.

In the most recent quarter, the company generated $ 19bn of cash from operations and $ 13bn in FCF. This represents an FCF margin at an impressive 36%. This is likely to decline in the next tow years or so as capex will grow and free cash flow will fall.

Strong Balance Sheet

$58 billion in cash & equivalents.

$18.4 billion in total debt. As the chart below shows, long term debt has only grown in the last three years. Therefore, it was about -$ 40bn in net debt.

Share count fell by 1.7% Y/Y.

Highlights from the earnings conference call

A lot of the talk was about AI investments, the company is planning and the benefits they hope to see in terms of revenue performance.

“We estimate that more than 3.2 billion people use at least one of our apps each day and we are seeing healthy growth in the US. And I want to call out WhatsApp specifically where the number of daily actives and message sends in the US keeps gaining momentum.”

AI

“We are building a number of different AI services.

· from Meta AI, our AI assistant that you can ask any question across our apps and glasses,

· to creator AIs that help creators engage their communities and that fans can interact with,

· to business AIs that we think every business eventually on our platform will use to help customers buy things and get customer support,

· to internal coding and development AIs,

· to hardware like glasses for people to interact with AIs and a lot more.

Meta’s large language model (LLM) family is called Llama. Meta, as a deliberate, policy, has made Llama available to all as open source code. This allows software developers to develop and improve it further for the benefit of everybody.

Meta AI is the cor product that users will see. It is Meta’s version of Copilot.

“Last week, we had the major release of our new version of Meta AI that is now powered by our latest model, Llama 3 and our goal with Meta AI is to build the world's leading AI service, both in quality and usage.”

They explain their product development playbook.

“We release an early version of a product to a limited audience to gather feedback and start improving it. And then once we think it's ready, then we make it available to more people.”

“That early release of Meta AI was last fall and with this release, we are now moving to that next growth phase of our playbook.

“Meta AI with Llama 3 is now the most intelligent AI assistant that you can freely use and now that we have the superior quality product, we are making it easier for lots of people to use it within WhatsApp, Messenger, Instagram and Facebook.”

Meta AI has not yet been released in the United Kingdom so we have not had a chance to use it.

What can Meta AI do?

“In addition to answering more complex queries,

Meta AI now creates animations from still images and now generates high quality images so fast that it can create and update them as you are typing.”

Llama is the core intelligence that powers Meta AI. The first two versions were trained in 8bn and 70bn parameters.

“The 8 billion and 70 billion parameter models that we released are best-in-class for their scale. The 400 plus billion parameter model (Llama 3) that we're still training seems on track to be industry leading on several benchmarks and I expect the models are just going to improve further from open-source contributions.”

This progress shows:

“We have the talent, data and ability to scale infrastructure to build the world's leading AI models and services.”

“This leads me to believe that we should invest significantly more over the coming years to build even more advanced models and the largest scale AI services in the world.”

One thought if Meta puts out a 400bn parameter model, what does this mean for the business mode of a company like OpenAI?

Mark Zuckerberg recently give an interview to Dwarkesh Podcast where he explained his passion to continually build new things. It is well worth listening to and can be found here.

Huge capex is coming for Meta.

“Full year 2024 capital expenditures will be in the range of $35 billion to $40 billion, increased from our prior range of $30 billion to $37 billion as we continue to accelerate our infrastructure investments to support our AI roadmap.”

Capex of $ 40bn can easily be funded by operating cash flow which is running at an annual rate of $ 70bn to $ 75bn.

The problem is, when Meta has increased capex in the past, the share price has fallen. For example, in 2022, the share price fell sharply from ~$ 330 per share to $ 90 per share as markets took fright at the huge investment Meta was making in the Metaverse.

“we've historically seen a lot of volatility in our stock during this phase of our product playbook where we're investing in scaling a new product but aren't yet monetizing it.”

“I expect to see a multi-year investment cycle before we fully scaled Meta AI, business AIs and more into the profitable services I expect as well.”

“Historically, investing to build these new scaled experiences in our apps has been a very good long-term investment for us and for investors who have stuck with us.”

“But building the leading AI will also be a larger undertaking than the other experiences we've added to our apps, and this is likely going to take several years.”

“There are several ways to build a massive business here, including scaling business messaging, introducing ads or paid content into AI interactions and enabling people to pay to use bigger AI models and access more compute.”

“AI is already helping us improve app engagement, which naturally leads to seeing more ads and improving ads directly to deliver more value.”

AI has been embedded in their apps for a while. Facebook has algorithms which offers up posts based on the users’ prior activity.

“About 30% of the posts on Facebook feed are delivered by our AI recommendation system. That's up 2x over the last couple of years and for the first time ever, more than 50% of the content that people see on Instagram is now AI recommended.”

“AI has also been a huge part of how we create value for advertisers by showing people more relevant ads. And if you look at our two end-to-end AI powered tools, Advantage+ shopping and Advantage+ app campaigns, revenue flowing through those has more than doubled since last year.”

The huge investments in the Metaverse in 2022 consisted to a large degree of GPUs from Nvidia. The latter has reported a 80% market share in GPUs used for generative AI. Like other large tech companies such as Google and Amazon, Meta is developing its own Silicon Chips, in part to reduce their dependence on Nvidia

“We'll also keep making progress on building more of our own silicon. Our Meta training and inference accelerator chip has successfully enabled us to run some of our recommendations related workloads on this less expensive stack. We plan to expand this to more of our workloads as well”.

With the focus on AI what has happened to the Metaverse?

“Our other long-term focus is the Metaverse. It has been interesting to see how these two themes have come together. This is clearest when you look at glasses. I used to think that AR glasses wouldn't really be a mainstream product until we had full holographic displays.”

“there's also a meaningful market for fashionable AI glasses without a display. Glasses are the ideal device for an AI assistant because you can let them see what you see and hear what you hear, so they have full context on what is going on around you as they help you with whatever you're trying to do. Our launch this week of Meta AI with vision on the glasses is a good example where you can now ask questions about things that you are looking at.”

The huge metaverse investments (reported under Reality Labs) are helping AI and the core advertising business.

“an increasing amount of our Reality Labs work is going towards serving our AI efforts. We currently report on our financials as a Family of Apps and Reality Labs as two completely separate businesses, but strategically I think of them as fundamentally the same business with the vision of Reality Labs to build the next generation of computing platforms in large parts that way we can build the best apps and experiences on top of them.”

So far Metaverse has delivered glasses. These glasses are the initial Meta Quest glasses and the Ray-ban Meta glasses.

“The Ray-Ban Meta glasses that we built with EssilorLuxottica continue to do well and are sold out in many styles and colours.”

They will make the Quest OS open source as that people who want to develop other types of AI glasses based on it can do so.

As the ecosystem grows, I think there will be sufficient diversity in how people use mixed reality that there will be demand for more designs than we'll be able to build, for example,

a work focused headset, slightly less designed for motion, but may want to be lighter by connecting to your laptop,

· a fitness focused headset may be lighter with sweat wicking materials.

· An entertainment focused headset may prioritize the highest resolution displays over everything else.

· A gaming focused headset may prioritize peripherals and haptics or a device that comes with Xbox controllers and a game pass.

“opening our operating system will help the overall mixed reality ecosystem grow even faster. “

In addition to AI and the Metaverse, we are seeing good improvements across our apps.

Progress in the family of apps

“Strong WhatsApp growth in the US and AI powered recommendations in our feeds and reels already, Video also continues to be a bright spot”

“On Instagram, reels and video continue to drive engagement with reels alone now making up 50% of the time that's spent within the app.”

“Threads is growing well too. They are now more than 150 million monthly actives, and it continues to generally be on the trajectory that I hope to see.”

Ad Revenue

Advertising Revenue is driven by Engagement and monetisation.

There are two primary factors that drive our revenue performance, our ability to deliver engaging experiences for our community and our effectiveness at monetizing that engagement over time.

Engagement

we remain pleased with engagement trends and have strong momentum across our product priorities.

Company will use AI to improve engagement.

These (AI) integrations will complement our social discovery strategy as our recommendation systems help people to discover and explore their interests while Meta AI enables them to dive deeper on topics they're interested in.

Monetisation

There are two stages to monetisation .

“The first is optimizing the level of ads within organic engagement. Here we continue to advance our understanding of users' preferences for viewing ads to more effectively optimize the right time, place and person to show an ad to. For example, we are getting better at adjusting the placement and number of ads in real time based on our perception of a user's interest in ad content and to minimize disruption from ads as well as innovating on new and creative ad formats.”

The second part of improving monetization is enhancing marketing performance.

“Here, we are making ongoing ads modelling improvements that are delivering better performance for advertisers.”

“We're leveraging AI is to provide increased automation for advertisers. Through our Advantage+ portfolio, advertisers can automate one step of the campaign setup process, such as selecting which ad creative to show or automate their campaign completely using our end-to-end automation tools, Advantage+ shopping and Advantage+ app ads.”

“Accelerating our AI efforts will help ensure we can provide the best version of our services as we transition to the next computing platform.”

“We expect to pursue these opportunities while maintaining a focus on operating discipline and we believe our strong financial position will allow us to support these investments while also returning capital to shareholders through share repurchases and dividends.”

Zuckerberg hinted that the period between investment and meaningful monetisation could be two years.

“I'm focused on for this year and probably a lot of next year is growing that product and the other AI products and the engagement around them. And I think we should all have quite a bit of confidence that if those are on a good track to scale then they're going to end up being very large businesses.”

The algorithm that Meta has long used to issue recommendations depending on history of user action is a kind of AI model

“Historically each of our recommendation products, including reels, in-feed recommendations, et cetera, has had their own AI model. Recently, we've been developing a new model architecture with the aim for it to power multiple recommendations products.

With this new model they “saw meaningful performance gains 8% to 10% increases in watch time as a result of deploying this.”

“There's a lot of work that we're investing in, in the underlying model architecture for both organic engagement and ads that we expect is going to continue to deliver increasing ads performance over time.”

Use of AI in business messaging

“We have been testing the ability for businesses to set up AIs for business messaging that represent them in chats with customers starting by supporting shopping use cases such as responding to people asking for more information on a product or its availability.”

“We are hearing good feedback with businesses saying that the AIs have saved them significant time while customer - consumers noted more timely response times.”

“With the latest models (Llama3) , we're not just building good AI models that are going to be capable of building some new good social and commerce products. I think we are in a place where we've shown that we can build leading models and be the leading AI company in the world and that opens up a lot of additional opportunities beyond just ones that are the most obvious ones for us.”

“We expect to see good opportunities to continue growing engagement across our products driven by the investments we made in AI based content recommendations, our ongoing video work and we also expect that we will continue to drive ads performance gains and continue to make our ads sort of more effective and deliver increasing value to advertisers.”

They categorized our AI investments into two buckets.

One is a sort of core AI work and the other is strategic bets

“So with our core AI work, we continue to have a very ROI driven approach to investment and we're still seeing strong returns as improvements to both engagement and ad performance have translated into revenue gains.”

“Strategic bets is where we are much earlier, we believe we must create significant value for our business in a number of areas, including opportunities to build businesses that do not exist on us today. We will need to invest ahead of that opportunity to develop more advanced models and to grow the usage of our products before they drive meaningful revenue.”

Advantage +.

They are adding AI to products such as Advantage + which are targeted at advertisers planning campaigns.

“Using Advantage+ audience targeting saw on average, a 28% decrease in cost per click or per objective compared to using our regular targeting. On the end-to-end automation products like Advantage+ shopping and Advantage+ app campaigns, we're also seeing very strong growth. The combined revenue flowing through those two has more than doubled since last year and we think there's still significant runway to broaden adoption. So we're trying to enable more conversion types for Advantage+ shopping.”

“So we're being very disciplined with allocation of new resources. This is a muscle that we really built over 2023 that we believe is important for us to keep carrying forward and I think you'll see us continue to emphasize that especially with the Family of Apps business being at the scale that it is.”

“The 100-plus million businesses on our platform. We basically want to make it very easy for all of these folks to set up an AI to engage with their community for a business that's going to be to be able to do sales and commerce and customer support. because the cost of engaging with people in messaging is still very high, but AI should bring that down just dramatically for businesses and creators and I think that, that has the potential, that's probably the -- beyond just increasing engagement and increasing the quality of the ads.”

“The main goal is getting many hundreds of millions or billions of people to use Meta AI as a core part of what they do. That is the kind of next goal building something that is super valuable. We think this has the potential to be at a very large scale and that's sort of the next step on the journey.”

Conclusions

Facebook has huge reach and tremendous ability to generate revenues, profits and free cash flow. The company is performing strongly with the most recent quarter demonstrating an increase in revenues per ad and impressive operating leverage.

Two years ago, in 2022/23, Meta went on a huge investment seep in building up what Mark Zuckerberg calls the Metaverse.

The market took fright and sold the shares down as they feared a lot of money being thrown down a personal vanity project. In 2022, the share price lost two thirds of its value.

In 2023, the company responded by cutting cost and creating what Zuckerberg calls the “lean company”.

The company is going to be increasing investments in Generative AI as well as the Metaverse which may not see significant monetisation for two years or more.

These investment of about $35bn to $$ 40bn can easily be funded from operating cash flow which is as at an annual run rate of $ 74bn.

We think the market will give the Company the benefit of the doubt to a greater degree than they did in 2022. They will treat Meta in the same way they treat Amazon. They will look beyond the heavy investment to the higher returns un the way that they have always looked at Amazon

Valuation

At the current share price of $ 472 per share, the company is trading at a forward P/E ratio of 22.1X and a current Price to Free Cash Flow ratio of 24X. These imply and earnings yield of 4.5% and 4.1%.

These do not look too expensive for a company with such strong earnings power and the ability to generate ROE of about 30%.

Conclusion

We will add Meta as add 1% allocation to increase it to a 3% share in our portfolio.