Meta Platforms (Meta)

Q2 2025 Results

We first wrote about Meta on 5th May 2023. This note can be found here.

More recent notes on the company can be found here and here.

Yahoo Finance had the following summary of the results.

“Meta posted stronger-than-expected results for the second quarter, buoyed by growing ad revenue even as its expenses increased.

The company earned $18.34bn, or $7.14 per share, in the April-June period. That's up 36% from $13.47bn, or $5.16 per share, in the same period a year earlier.

Revenue jumped 22% to $47.5bn from $39.0bn.

Q2 2025 Results

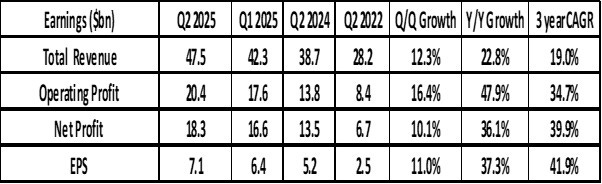

Q2 revenues were $47.5bn and up 22.8% (y/y) and the EPS was 7.1 (+37.3% (y/y)

Q2 total expenses were $27.1bn, an increase of 12% (y/y).

Operating revenue and net profit grew at 47.9% and 36.1% (y/y) respectively.

The business model shows continuing excellent operating leverage.

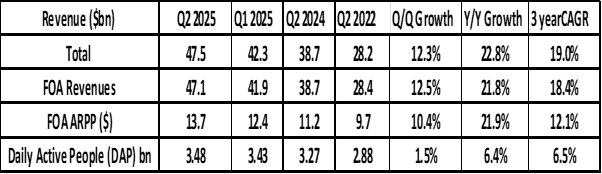

The number of daily active users of the Family of Apps (FOA) rose 6.4%% to 3.48bn or 6.8bn eyeballs: an impressive percentage of the global human population!

Family of Apps (FOA) segment.

FOA consists of

Facebook

Instagram

WhatsApp

Messenger (Facebook Messenger)

Threads (launched as a competitor to Twitter in 2023)

Q2 total FOA revenue was $47.1bn up 22% (y/y).

Q2 FOA expenses were $22.2bn (+14% (y/y)).

Average Revenue Per Person (ARPP) rose to $13.7 per quarter. This implies an annual ARRP run rate of $52. Therefore, Meta’s annual revenue run-rate is about $ 180bn (3.48bn X $52).

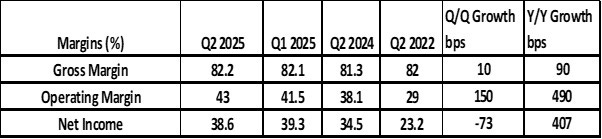

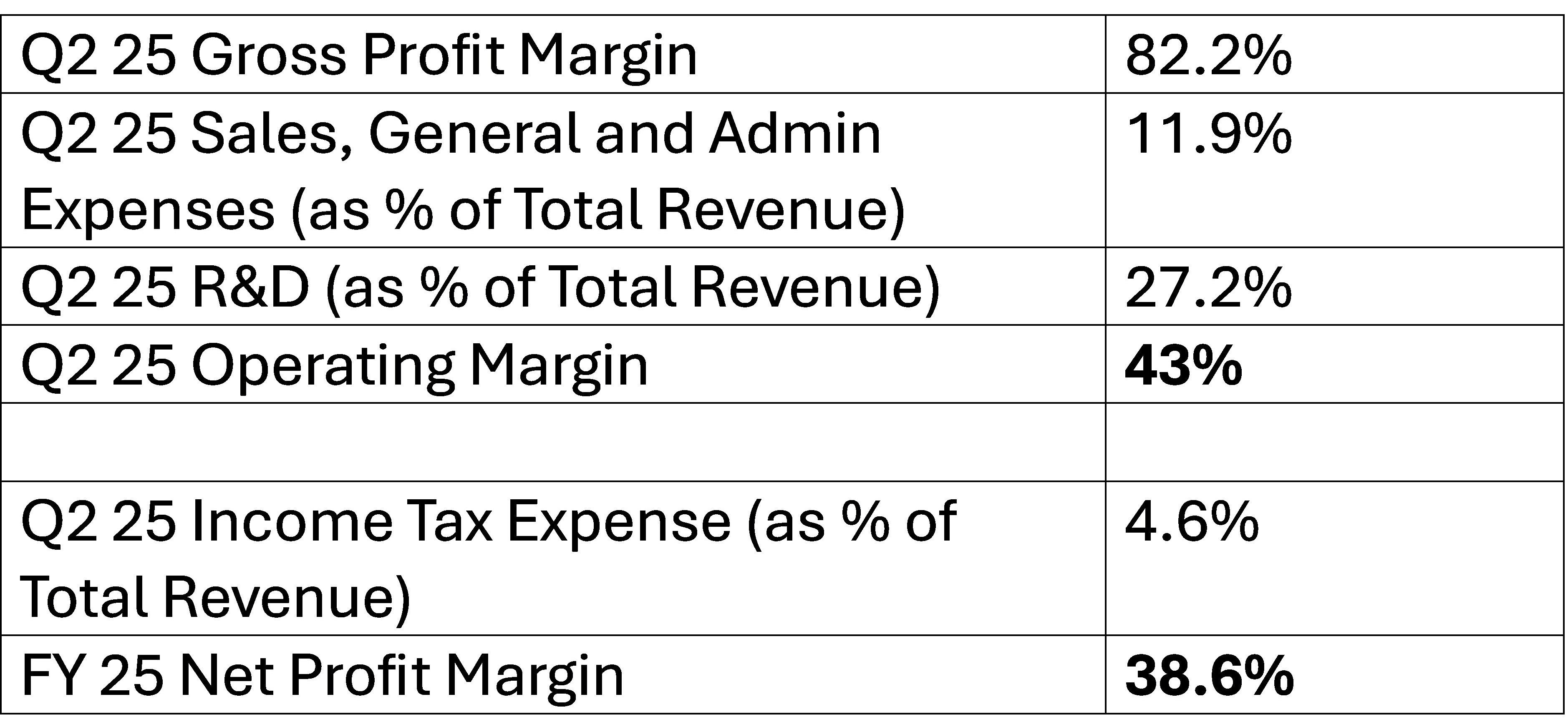

Both operating and net profit margins rose in Q1 on a (y/y) basis.

A detailed analysis of the margins is shown below:

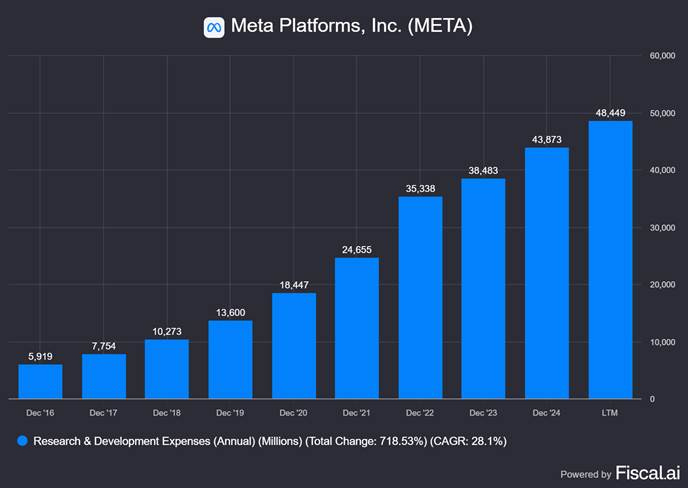

R&D is a major operating expense. R&D increased 23% to $12.9bn in the quarter, mostly due to higher employee compensation and infrastructure costs as the company boosted investment.

Annual R&D expenses have increased at a CAGR of 28% in the last 8 years or 7.2x. They have risen from ~$6bn in 2016 to ~$43.8bn in 2024.

Outlook

We expect third quarter 2025 total revenue to be in the range of $47.5-50.5 bn.

At the lower end of this range, this implies a growth rate of 17%. At the higher end, it will be 23.6%.

We expect full year 2025 total expenses to be in the range of $114-118 billion reflecting a growth rate of 20-24% year-over-year.

This expense growth is very high and in line with the rate of revenue growth. They explained the reasons for this.

There are a few factors we expect will provide meaningful upward pressure on our 2026 total expense growth rate.

The key factors will be depreciation and higher compensation. The former reflects the recently elevated capital expenditure.

The largest single driver of growth will be infrastructure costs, driven by a sharp acceleration in depreciation expense growth and higher operating costs as we continue to scale up our infrastructure fleet.

Depreciation is an expense in the Profit and Loss line. Higher depreciation will tend to put downward pressure on reported profits.

The second factor will be higher employee compensation. This is not surprising as Meta has been on an aggressive hiring spree.

Aside from infrastructure, we expect the second largest driver of growth to be employee compensation as we add technical talent in priority areas and recognize a full year of compensation expenses for employees hired throughout 2025.

We expect these factors will result in a 2026 (y/y) expense growth rate that is above the 2025 expense growth rate.

We currently expect 2025 capital expenditures, including principal payments on finance leases, to be in the range of $66-72bn.

While the infrastructure planning process remains highly dynamic, we currently expect another year of similarly significant capital expenditures dollar growth in 2026 as we continue aggressively pursuing opportunities to bring additional capacity online to meet the needs of our artificial intelligence efforts and business operations.

Analysts expect Meta capital expenditure to rise to $93bn in FY 2026 and $99.8bn in FY 2027. These are huge figures. Annual capital expenditure has grown at a CAGR of 30.8% rapidly in recent years.

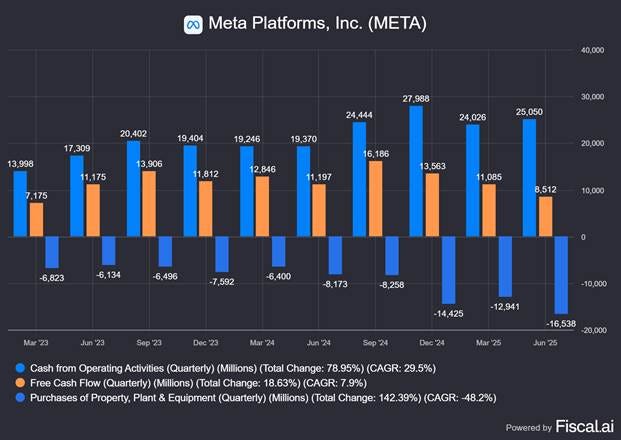

Q2 Operating cash flow was $25.0bn

Q2 Free cash flow was $8.5bn.

Free cash flow is operating cash flow minus capital expenditure. As capital expenditure growth is faster than operating cash flow growth, Free cash flow growth is slowing.

In the chart below we can see

Cash from operations increased at a CAGR of 29.5%

Capital Investment (Defined here as purchase of property, plant and equipment) rose at a 48.2%

As a result, free cash increased by much less: 7.9% CAGR.

If Capital investment continues to grow faster than operating cash. Free cash flow could fall and even potentially go negative. Analysts expect capital investment to rise rapidly as we saw in the chart above.

With slower free cash flow growth, the company will be more constrained in the amount of cash that it can return to shareholders.

Our Analysis

This is our analysis of Meta in the light of the Quarterly numbers and the earnings conference call.

Meta Platforms has been one of the most remarkable companies of the last three decades. It has built up an audience of about 50% of the global human population and has developed a very successful business model for selling advertisements targeted at the massive audience.

Unlike other large tech firms, Meta is still led by its charismatic founder. Bill Gates may have moved on and Larry Page and Sergey Brin are no longer involved in day- to-day management at Alphabet but Mark Zuckerberg is still very much running the show at Meta, and he is likely to do for two or three more decades. The dual share structure at Meta gives Zuckerberg a degree of control that Satya Nadella at Microsoft can never achieve.

Zuckerberg can make much bolder bets than a typical CEO can.

A few years ago, Zuckerberg made a big bet on Virtual Reality (VR) and the VR domain which he called the Metaverse. To signal his commitment to it, he changed the name of the company from Facebook Inc. to Meta Platforms.

A new Metaverse division was set up within Meta called Reality Labs and billions of dollars were invested in the Metaverse. Markets took fright at the prospect of money being squandered and the Meta share price took a dive in 2022.

The rest of the business continued to do very well, and the shares recovered strongly. However, Reality Labs continues to make very large losses.

Meta has made an even bigger bet on AI. The large tech companies have invested hundreds of billions of dollars in giant datacentres, power utilities to run. Their combined investment is likely to total a staggering US$400bn next year.

In terms of the nature of the investment, Meta’s approach is different from the others in one respect. Google, Amazon, Microsoft and Oracle are making investment in AI primarily because they want to lease it to their clients in the cloud hosting business.

Meta’s approach is different. They do not have a cloud hosting business. Their investments in AI are driven by the aim of using AI to improve their core business further and to develop new products and services which will create new revenue streams. As an AI bet Meta seems like a higher risk/ higher reward play than the other large tech players.

In the last few weeks, Meta has increased the stakes in the AI race by betting on what they call Superintelligence. They have announced higher investments and engaged in a talent war to hire the very best AI researchers from companies such as OpenAI, Thinking Machines, Anthropic, Google, Apple and others. They have bought out start-up companies so the founders can work for Meta.

The investment case for Meta (if any) boils down to a belief that this huge bet on SuperIntelligence will pay off for both Mark Zuckerberg and Meta.

SuperIntelligence

In recent weeks, Meta founder and CEO Mark Zuckerberg has been using the term “SuperIntelligence” and has been recruiting heavily to help Meta achieve it.

Our business continues to perform very well, which enables us to invest heavily in our AI efforts. Over the last few months, we've begun to see glimpses of our AI systems improving themselves. And the improvement is slow for now, but undeniable and developing superintelligence, which we define as AI that surpasses human intelligence in every way, we think, is now in sight.

The problem is superintelligence is quite vague, and it is not clear how it differs from artificial general intelligence (AGI) with which we have all become familiar in the last few months.

Meta and Mark Zuckerberg (the two are interchangeable) believe that SuperIntelligence is achievable and Meta will be at the forefront in developing it.

Meta's vision is to bring personal superintelligence to everyone, so that people can direct it towards what they value in their own lives.

And we believe that this has the potential to begin an exciting new era of individual empowerment. A lot has been written about all the economic and scientific advances that superintelligence can bring, and I'm extremely optimistic about this. But I think that if history is a guide, then an even more important role will be how superintelligence empowers people to be more creative, develop culture and communities, connect with each other and lead more fulfilling lives.

It is a bit hard to believe this stuff about individual empowerment as Meta’s business model required people perpetually stuck on their social media and chat internet properties consuming advertisements.

To build this future, we've established Meta Superintelligence Labs, which includes our foundations, product and FAIR teams as well as a new lab that is focused on developing the next generation of our models.

We're making good progress towards Llama 4.1 and 4.2, and in parallel, we are also working on our next generation of models that will push the frontier in the next year or so.

As has been widely reported, they have been in a hiring spree for elite AI talent and offering eye-popping remuneration.

We are building an elite, talent-dense team Alexandr Wang is leading the overall team, Nat Friedman is leading our AI Products and Applied Research, and Shengjia Zhao is Chief Scientist for the new effort. They are all incredibly talented leaders, and I'm excited to work closely with them and the world-class group of AI researchers and infrastructure and data engineers that we're assembling.

One of the reasons researchers have for joining Meta is unparalleled computing resources. One planned datacentre cluster (Prometheus) is said to be the size of Manhattan.

The people who are joining us are going to have access to unparalleled compute as we build out several multi-gigawatt clusters. Our Prometheus cluster is coming online next year, and we think it's going to be the world's first gigawatt-plus cluster.

We're also building out Hyperion, which will be able to scale up to 5 gigawatts over several years, and we have multiple more titan clusters in development as well.

They believe SuperIntelligence will help this in their own business.

We are making all these investments because we have conviction that Superintelligence is going to improve every aspect of what we do.

From a business perspective, there are five basic opportunities that we are pursuing,

improved advertising,

more engaging experiences,

business messaging,

Meta AI and

AI devices.

They discussed each of these in detail in the earnings call.

Revenue drivers

Meta makes almost of its money from advertising. Advertising revenue is a product of number of ad impressions multiplied by average price per ad.

In Q2 2025

Ad impressions – Ad impressions delivered across our Family of Apps increased by 11% (y/y).

Average price per ad – Average price per ad increased by 9% (y/y).

Impression growth accelerated across all regions due primarily to engagement tailwinds on both Facebook and Instagram and to a lesser extent, ad load optimizations on Facebook.

The average price per ad increased 9%, benefiting from increased advertiser demand, largely driven by improved ad performance.

Their revenue strategy is simple:

Maximise the number of people visiting their FOA sites.

Maximise the amount of time spent on the sites.

Target personalised advertising and maximise the probability of monetisation.

There are two primary factors that drive our revenue performance,

Our ability to deliver engaging experiences for our community and

Our effectiveness at monetising that engagement over time.

Engaging experiences

Engagement is rising.

In both Facebook and Instagram, video time was up 20% (y/y).

What is the reason for this? Meta tweak and develop their ranking systems to better identify the most relevant content to show.

They are using AI LLMs in in Threads recommendation systems. This is driving a meaningful share of the ranking related time spent gains on Threads.

We're now exploring how to extend the use of LLMs and recommendation systems to our other apps.

Monetising Engagement

Now to the second driver of our revenue performance, increasing monetization efficiency.

There is a science to determining the amount of ads that can be “pushed”. Too much of the wrong sort of ad will only irritate the web browser. Too few and the monetisation revenues will be too low.

The first part of this work is optimizing the level of ads within organic engagement. We continue to optimize ad supply across each surface to better deliver ads at the time and place they are most relevant to people.

In Q2, we also began introducing ads within Feed on Threads and the Updates tab of WhatsApp, which is a separate space away from people's chats.

It is early days for adverts in both Threads and WhatsApp.

While ad supply remains low and Threads is not expected to be a meaningful contributor to overall impression growth in the near term, we are optimistic about the longer-term opportunity with Threads as the community and engagement grow and monetization scales.

On WhatsApp, we are rolling out ads in status and channels, along with channel subscriptions in the Updates tab to help businesses reach the more than 1.5 billion daily actives who visit that part of the app. We expect the introduction of ads and status will be gradual over the course of this year and next, with low levels of expected ad supply initially.

We also expect WhatsApp ads and status to earn a lower average price than Facebook or Instagram ads for the foreseeable future, due in part towards WhatsApp skew toward lower monetizing markets, and more limited information that can be used for targeting.

The second part of increasing monetization efficiency is improving marketing performance.

They are improving marketing performance by improving ad systems, advancing ads products, and evolving ads platform to drive results that are optimized for each business' objectives.

This is important - they are using AI to meaningfully improve the performance of their business.

These improvements have driven nearly 4% higher conversions on Facebook Mobile Feed and Reels.

Meta AI.

The main interaction that users will have with AI is through Meta AI. This has appeared on WhatsApp and is highly visible on Facebook.

The primary way we're using Llama in our apps today is to power Meta AI which is now available in over 200 countries and territories. WhatsApp continues to be the largest driver of queries as people message Meta AI directly for tasks such as information gathering, homework assistance and generating images.

We're seeing Meta AI become an increasingly valuable complement to our content discovery engines. Meta AI usage on Facebook is expanding as people use it to ask about posts they see in Feed and find content across our platform in Search.

Another way Meta AI will help with content discovery is through the automatic translation and dubbing of foreign language content into the audience's local language.

Thanks to ranking and recommendation systems as well as AI they are able to generate engaging experiences which attracts more users to their sites.

Capital Allocation.

Our primary focus remains investing capital back into the business with infrastructure and talent being our top priorities.

Expenses are going to grow in 2026 due to infrastructure investment and compensation increases.

They key factors in the new strategy at Meta are Talent and Infrastructure.

We really believe that this is a time for us to really make investments in the future of AI as I think it will open up both new opportunities for us in addition to strengthen our core business.

Talent

Meta is trying to hire the most talented AI researchers and is willing to pay large sums of money. As we noted in our recent article which can be seen here, the effort is being led by Mark Zuckerberg personally.

Our approach to adding head count continues to be targeted at the company's highest priority areas.

We expect talent additions across all of our priority areas will continue to drive overall head count growth through this year and 2026.

While head count growth in our other functions remains constrained, within AI, we've had a particular emphasis on recruiting leading talent within the industry, as we build out Meta Superintelligence Labs to accelerate our AI model development and product initiatives.

Meta believes the task required small teams of the most talented people.

I've just gotten a little bit more convinced around the ability for small talent-dense teams to be the optimal configuration for driving frontier research.

This is different to the approach in the rest of their business.

And it's a bit of a different setup than we have on our other world- class machine learning system. So if you look at like what we do in Instagram or Facebook or our ad system, we can very productively have many hundreds or thousands of people basically working on improving those systems, and we have very well-developed systems for kind of individuals to run tests and be able to test a bunch of different things. You don't need every researcher there to have the whole system in their head.

But I think for this -- for the leading research on superintelligence, you really want the smallest group that can hold the whole thing in their head, which drives, I think, some of the physics around the team size and how -- and the dynamics around how that works.

Infrastructure.

Investment in infrastructure is being increased form already high levels.

This means having large network of giant datacentres to increase computational capacity, often referred to as compute.

We expect having sufficient compute capacity will be central to realizing many of the largest opportunities in front of us over the coming years.

The investment will help them to improve the performance in their core business…

We continue to see very compelling returns from our AI capacity investments in our core ads and organic engagement initiatives and expect to continue investing significantly there in 2026.

…as well as build up the infrastructure needed for future innovation.

We also expect that developing leading AI infrastructure will be a core advantage in developing the best AI models and product experiences.

we do take very seriously that this is a just massive amount of capital to convert into many gigawatts of compute which we think is going to help us produce leading research and quality products and in running the business, I do look for opportunities to basically convert capital into quality of products that we can deliver for people.

As they have increased investment they have consistently underestimated the scale of demand.

So far, we've observed the more kind of aggressive assumptions, or the fastest assumptions have been the ones that have most accurately predicted what would happen.

The work that we're seeing with teams internally being able to adapt Llama 4 to build autonomous AI agents that can help improve the Facebook algorithm to increase quality and engagement are like -- I mean, that's like a fairly profound thing if you think about it. I mean it's happening in low volume right now.

The trajectory on this stuff is very optimistic.

That informs a lot of the decisions from everything from the importance and value of having the absolute best and most elite talent-dense team at the company to making sure that we have a leading compute fleet so that the people here can do -- obviously, the researchers here have more compute per person to be able to lead their research and then roll it out to billions of people across our products,

our company is the best in the world at is basically when we take a technology, we're good at driving that through all of our apps and our ad systems and all that stuff, it's not just going to kind of sit on the vine. There's no other company, I think that is as good as us at kind of taking something and kind of getting it in front of billions of people.

Massive bet

They rightly describe their huge bet on people and infrastructure as a massive bet.

But this is certainly a massive bet that we're kind of -- we're focused on, and we want to make sure that what we build accrues to building the best products that we can deliver to the billions of people who use our services.

Co-financing

The scale of the funding is so large they may not be able to fund it all by themselves. There are models for working with financial investors such as Brookfield, KKR and Blackstone.

We certainly expect that we will finance some large share of that ourselves, but we're also exploring ways to work with financial partners to co-develop datacentres.

we generally believe that there will be models here that will attract significant external financing to support large-scale data center projects that are developed using our ability to build world-class infrastructure while providing us with flexibility should our infrastructure requirements change over time.

ROI of Capex

The Meta management were asked about the current or likely ROI on all this huge investment?

They divided the answer into two aspects.

1. On the core AI side, we continue to see strong ROI. Our ability to measure that is quite good, and we feel sort of very good about the rigorous measurement and returns that we see there.

2. On the GenAI side, we are clearly much, much earlier on the return curve and we don't expect that the GenAI work is going to be a meaningful driver of revenue this year or next year.

we see a lot of attractive investment opportunities that we believe are going to set us up to deliver compelling profit growth in the coming years for all of our investors.

Glasses

Meta’s Reality Labs has developed smart glasses which Meta is selling working with Luxottica Group. These are branded Rayban Meta Smart Glasses. They combine the basic functionality of a pair of glasses (or sunglasses) with many of the media and AI features you'd get from a smartphone. The glasses feature a built-in camera and Bluetooth earphones. One can capture photos and videos, listen to music, and interact with a digital assistant without ever having to pull out the phone. Meta seem to be pleased with the product.

This product category is clearly doing quite well. It is stylish eyewear, so people like wearing them just as glasses.

They believe in the long-term glasses ( not the smartphone or the computer) will be the key way through which Users will interact with AI.

Glasses are basically going to be the ideal form factor for AI because you can let an AI see what you see throughout the day, hear what you hear, talk to you.

Once you get a display in there, that’s also going to unlock a lot of value where you can just interact with an AI system throughout the day in this multimodal way.

It can see the content around you, it can generate a UI for you, show you information and be helpful.

They believe Smart Glasses will become a necessity.

In the future, if you don't have glasses that have AI or some way to interact with AI, I think you're kind of similarly, probably be at a pretty significant cognitive disadvantage compared to other people and who you're working with, or competing against.

This is kind of what we've been maxing out with Reality Labs over the last 5 to 10 years is basically doing the research on all of these different things.

they are going to be the ideal way to blend the physical and digital worlds together.

Summary

Meta continued its strong performance in Q2 2025.

The stock has proved to be a very successful investment over the last few years generating a CAGR of 25% over the last 13 years.

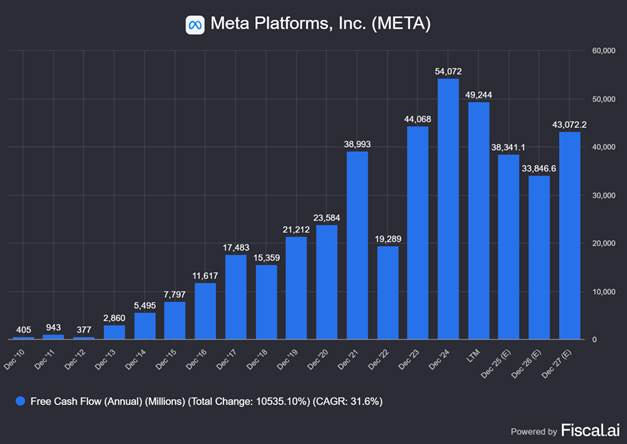

Along with other large companies, it is making a big bet on AI. Meta’s capital Expenditure less than $5bn in 2016 is expected to be 93bn in FY 2026 and $100bn in FY 2027.

In the short term the financial impact of this is relatively clear.

Free Cash flow will fall and therefore there will be less cash for share buybacks and dividends. The chart below shows Free Cash flow which peaked at $54bn in 2024 will fall to $33bn in FY 2026

In addition, the greatly increased level of capital expenditure will lead to much higher level of future depreciation and amortisation, and this will tend to reduce reported profits.

In the longer run, however if these investments generate returns, they will lead to much higher profits and cash flows.

For the investors, the essential question is can Mark Zuckerberg and Meta win against other large tech companies and AI startups and generate high returns on these massive capital investments.

The investment case for Meta depends largely on how one answers that question.

Valuation and Conclusion.

At the current share price of $763 per share, the stock is trading at a two-year forward P/E ratio of 25.9X, which is fair value for a company with a ROCE of 30% and a likely earnings growth of 8% to 10% in the next o three years.

We think there is a good prospect of a minimum return of 9%-10% per annum over the next few years.

We currently have a 2.8% holding in Meta. We will increase this to 3.5% of our portfolio. This is essentially an act of faith that the company can efficiently deploy $230bn of investment in the next two and a half years.

Thank you.