Microsoft

Some thoughts in light of the recent quarterly results. I will not cover the results in details as these are covered extensively elsewhere.

Microsoft (MSFT) reports in three segments

These are noted above:

Productivity and Business Processes have the core Office (Word Excel and PowerPoint. Exchange, SharePoint, Microsoft Teams etc) which is now christened Office 365. Also included in this segment are LinkedIn and Dynamics 365.

Intelligent Cloud includes fast growing cloud hosting business Azure as well SQL Servers . Any New AI investments will probably be included in this segment as Github is there .

More Personal Computing is mainly the Consumer facing businesses and includes Surface devices, X-box Gaming and Bing. If the US$ 80bn Activision acquisition is completed, it will be placed in this segment.

In 2018/2019, the financial breakdown between divisions was easy to remember. Total Revenue was US$120bn and each business segment accounted for one third (about US$ 40bn each). The operating margin was 30% and so operating profit was about US$ 36bn. The quarterly run rate for total revenue was US$30bn (~ US$10bn in each segment) and quarterly operating profit run rate was US$ 9bn.

Fast forward to today, the numbers look very different. Total revenue is 30% higher at US$ 53bn per quarter. All three segments have grown but the star has been the Intelligent Cloud which accounts for 40% of revenues, Productivity and Business Processes is still 33% while More Personal Computing is now only about 25%. The Operating Margin is now much higher at 40% and the quarterly operating profit is more than 100% higher at US$ 22.5bn.

The main reason for the growth in operating profits has been the advances in the higher margin Azure cloud hosting business and the large increase in IT spend as companies geared up for WFH. This included the huge growth in Microsoft Teams which benefited revenues in the Productivity and Business Processes segment.

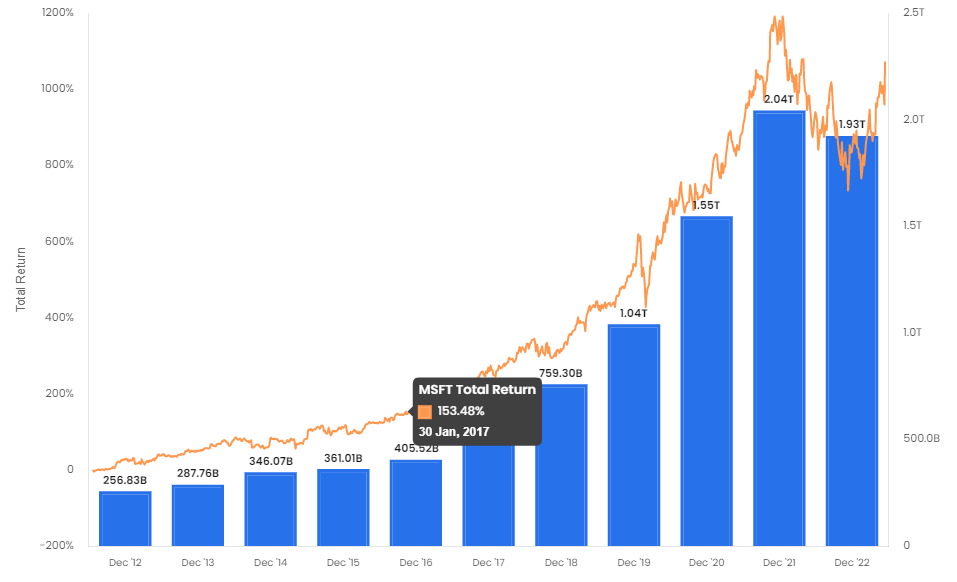

This is the essence of MSFT of the last three years. Strong growth in revenues and margins. The annual EPS has almost doubled from US$ 4.75 in 2019 to US$ 9.21 in 2022 ( see table above) and the market cap has roughly doubled form 1trillion to 2 trillion (see below) .

The most recent quarterly results were a case of more of the same. The consumer facing businesses saw some weakness but otherwise it is a picture of continued strength.

The quarterly growth in revenue was 7.1% (y-o-y) or 10% in constant currency terms. Intelligent Cloud grew 15.7% while Personal compute fell 8.3%

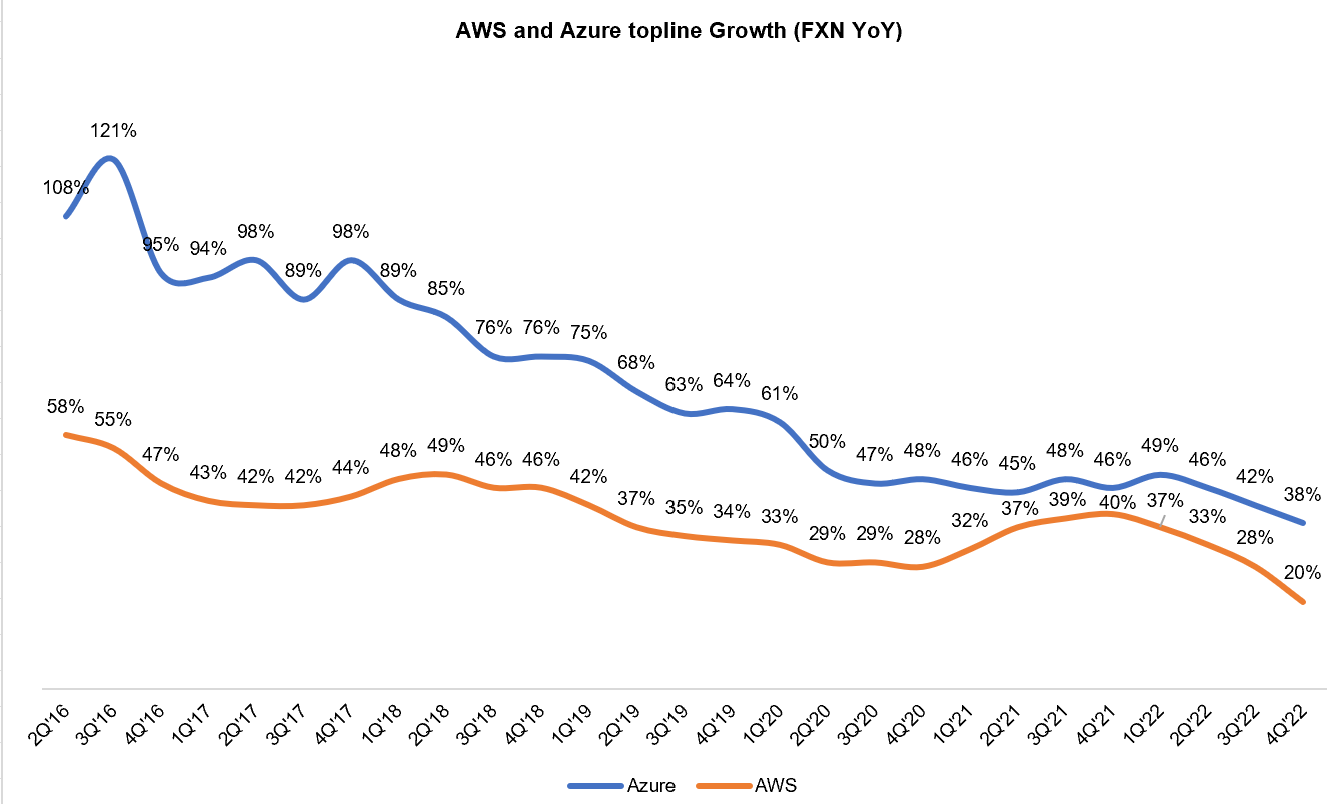

Margins rose further with EBIT margin rose 1.0% (y-o-y) to 42.3%. As noted above, the Azure Cloud business is in the Intelligent Cloud segment and Microsoft does not break out the Azure Revenue within it. They do however outline the revenue growth rate for Azure. In the most recent quarter Azure grew 27% YoY and 31% on a constant currency case. ”

This is less than the previous quarter growth rate of 38% . Growth rate has been trending lower due to the larger base. 31% in the three months to 31 March 2023 is impressive especially as Amazon reported their Cloud business (AWS) grew at 16.3% and has slowed to 11% in April 2023. Azure has consistently grown faster than AWS as Microsoft was catching up with Amazon in the cloud business. There a number of differences between Azure and AWS business profiles which mean that Azure is likely to grow much faster than AWS for the foreseeable future.

We estimate that Azure annual Topline is US$ 45-50bn compared with about with US$ 72bn for AWS. We estimate the Azure operating margins are likely to be 45%-50%. The key point is revenue growth of 31% is impressive for such a large profitable business.

15 years ago, MSFT made most of its money from Windows and Office and Cloud accounted for just 10%. Since then, in a period of strong overall growth, the very profitable Azure cloud business now accounts for an estimated 45% of total revenue. The company has been totally transformed.

The Post Results conference call

Satya Nadella stated following observation in the conference call.

“We continue to focus on three priorities:

First, helping customers use the breadth and depth of the Microsoft Cloud to get the most value out of their digital spend.

Second, investing to lead in the new AI wave across our solution areas, and expanding our TAM.

And, third, driving operating leverage, aligning our cost structure with our revenue growth. - even more emphasis on operational efficiency with a view to further improving operating margin.”

The emphasis going forward will be on the Cloud, AI and Operational Efficiency. These seems to us exactly the right areas to focus on.

The Cloud still has huge growth potential. Andy Jassy, CEO of Amazon in their conference call noted that 90% of company is still sits on servers in their premises and implied that much of this will shift to the Cloud hosting hyperscalers (mostly, Amazon AWS, Microsoft Azure, Google GCP, Alibaba, Oracle and IBM).

AI seems to be the new exciting frontier for everybody. Like Amazon Meta and Google, a lot of the MSFT post-results conference call was about AI. Microsoft seems to be in a strong position in this stage. Nadella made the following comments.

“Azure took share, as customers continue to choose our ubiquitous computing fabric from cloud to edge, especially as every application becomes AI-powered.”

“We have the most powerful AI infrastructure, and it’s being used by our partner OpenAI, as well as NVIDIA, and leading AI startups like Adept and Inflection to train large models.”

“Our Azure OpenAI Service brings together advanced models, including ChatGPT and GPT-4, with the enterprise capabilities of Azure.”

Microsoft invested US1 bn in Open AI in 2019 and Us$ 2bn in 2021. In 2023 , it is investing an additional $10 billion at a valuation close to $29 billion. In exchange, Microsoft is getting the right to 75% of OpenAI’s profits until it earns back $13 billion After that, Microsoft will be entitled to a further 49% of OpenAI’s profits until it earns a profit of $92 billion (7X its original investment). After that the shares will revert to the non-profit Open AI Foundation.

In addition to the likely substantial financial returns, MSFT will benefit from the technical collaborations. It has already incorporated AI products and features into Bing, GitHub and is about to add Copilot AI into its core Office 365 suite of products.

Operational Efficiency; Microsoft has been more focused on profitability, margins and cashflow than its rivals. Amazon has a barely profitable ( Net margins below 2%) retail business, Google has its “Other bets” which seems to absorb cash but with no sign of profits and Meta has its big metaverse bet. Microsoft under Nadella does not seem to have obvious weaknesses.

Other points

“Nadella also mentioned Teams which has reached 280mn users.

Teams is also expanding our TAM. Nearly 60% of our enterprise Teams customers buy Teams Phone, Rooms, or Premium.Teams Phone is the undisputed market leader in cloud calling, helping our customers reduce costs with a three-year ROI of over 140%.

Teams Rooms revenue more than doubled year-over-year. And Teams Premium meets enterprise demand for AI-powered features like intelligent recaps. Now generally available, it’s one of our fastest growing Modern Work products ever, with thousands of paid customers just two months in.”

Conclusions

Microsoft has been our favourite large cap tech stock for the last thee years

It has performed very strongly in the last ten years and the most recent results continue the trend. The company looks set to grow in many established businesses especially the Cloud and is the best placed large tech company to benefit from developments in AI.

The current valuations (Forward P/E ratio of 29 times and Free Cash Flow Yield of 2.5%) do not indicate that the stock is cheap but given the profitable growth opportunities , we may add a little to our position.