Microsoft (MSFT)

Q4 2025 Results

We have reported on Microsoft on a number occasions and you can find those reports here, here and here. It has done very well for us and is our second largest position (behind Nvidia).

The company recently reported its Q4 2025 results.

We will comment briefly on these and note some highlights from the earnings conference call.

The Yahoo Finance summary of the results included the following:

Microsoft (MSFT) reported its fiscal fourth quarter earnings beating analysts' expectations on the top and bottom lines on the strength of its cloud revenue.

For the quarter, Microsoft saw adjusted EPS of $3.65 on revenue of $76.4bn. Wall Street was anticipating adj. EPS of $3.37 and revenue of $73.89bn, according to Bloomberg analyst consensus estimates.

"Cloud and AI is the driving force of business transformation across every industry and sector," Microsoft CEO Satya Nadella said in a statement.

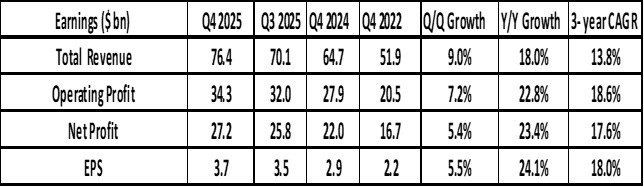

Q4 2025 Results

Total revenues grew by 18% (y/y) to $76.4bn.

Operating expenses were $18.1bn and up just 6%. Operating costs grew less than revenue.

Operating profit grew by 22.8% (y/y)

Net profit and EPS grew by 23.4% & 21.7% respectively (y/y).

This suggests continuing good level of operating leverage in the business.

These are strong expectations-beating numbers.

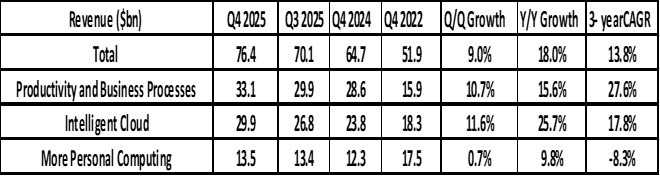

Microsoft’s Reporting Segments.

The three reporting segments are given below:

Six years ago, the three business segments were roughly of equal size in terms of revenue. The “More Personal Computing” segment has been boosted by the $68bn acquisition of gaming company, Activision Blizzard.

In the last five years, enterprise demand, particularly for cloud services, has been very strong while consumer demand has been weak.

Today, “Productivity and Business Processes” and “Intelligent Cloud” both have more than double the revenue of “More Personal Computing.”

In Q4 2025, Intelligent Cloud was again the fastest growing while More Personal Computing was again the laggard.

Intelligent cloud grew by 25.7% (y/y) to $29.9bn

Productivity and Business Processes grew by 15.6% (y/y) to 33.1bn.

More Personal Computing was again the slowest grower. Its revenues increased by 9.8% (y/y) to $13.5bn.

Within Intelligent Cloud, Azure and other Cloud services grew by a pleasing 39% (y/y). Yet again, this was a surprising and very impressive rate of growth. The equivalent but smaller business at Google called Google Cloud Platform (GCP), grew 31% over the same period.

Commercial remaining performance obligation (RPO) increased to $368bn up an impressive 37%. RPO is an attempt to measure the remaining value of all contracted business.

Roughly 35% (of the RPO) will be recognized in revenue in the next twelve months, up 21% (y/y). The remaining portion recognized beyond the next twelve months increased 49%. And this quarter the annuity mix was again 98%. This means most of their business is on a recurring basis rather than one-off transactions. This suggests a high quality of revenues.

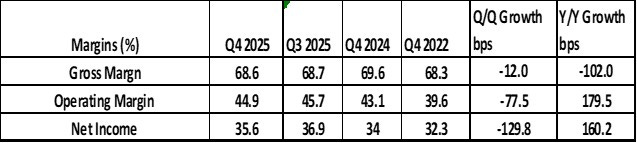

There was a decrease in margins on a q/q level but an increase on a y/y basis ,at least at the Operating and Net Profit level.

This was an impressive set of numbers, and it was largely about the Cloud. Each cloud segment showed above average revenue growth.

Microsoft 365 Commercial cloud revenue growth was 18%.

Microsoft 365 Consumer cloud revenue growth was 20%.

Intelligent Cloud revenue growth was 26%. Within that, Azure and other cloud services was up an impressive 39%

It is not all cloud. Dynamics 365 revenue grew 23% (y/y). This was probably driven by Cloud and AI demand.

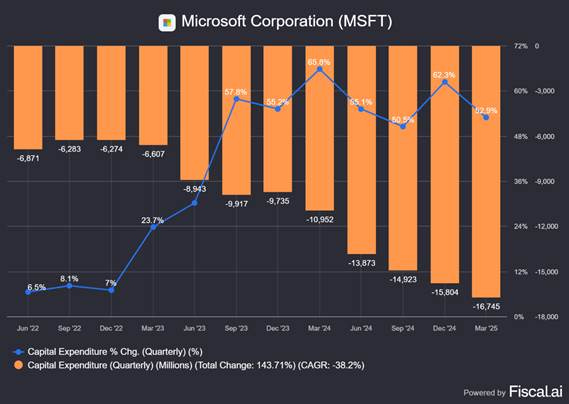

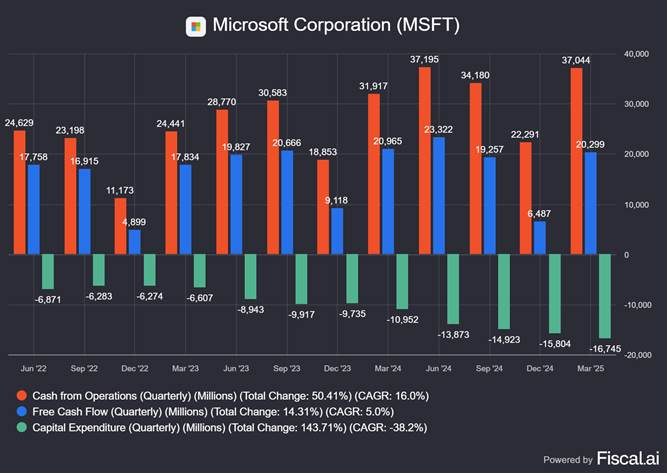

Capital expenditures were $24.2bn compared with $13.8bn in the same quarter last year (+ 73% (y/y)) and $16.7bn in the previous quarter. (see chart below)

As with other large tech firms, capital expenditure is accelerating from already very high levels. The chart below shows MSFT’s quarterly capital expenditure. It has grown at a CAGR of 38%. It is shown as a negative bar as it is a cash outflow.

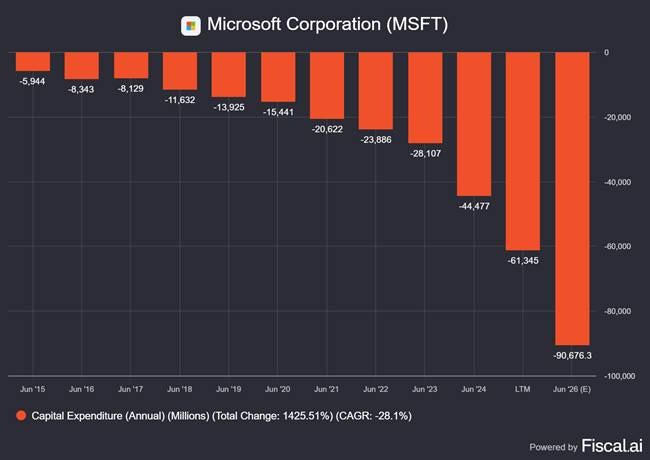

The chart below shows MSFT’s annual capital expenditure. It has grown at a CAGR of 28% in the last nine years and is expected to be $90bn (!) in FY 26. Again, it is shown as a negative bar as it is a cash outflow.

MSFT described the breakdown of this capital expenditure.

More than half our spend was on long-lived assets that will support monetization over the next fifteen years and beyond. The remaining spend was primarily for servers both CPUs and GPUs and driven by strong demand signals.

Cash flow from operations in Q2 was $42.6bn (up 15% (y/y)) driven by strong cloud billings and collections partially offset by higher supplier payments. This was $37.2bn in the same quarter last year and $37bn in the previous quarter.

Free cash flow was $25.6bn. This was only up 10% (y/y). The same quarter last year had free cash flow of $23.2bn.

Free cash flow is operating cash flow minus capital expenditure. As capital expenditure growth has been faster than operating cash flow growth, free cash flow growth is slowing.

Outlook.

The management’s outlook for the next fiscal year is positive.

We expect to deliver another year of double-digit revenue and operating income growth in FY 2026.

We will continue to invest against the expansive opportunity ahead across both capital expenditures and operating expenses….

We expect operating margins to be relatively unchanged year over year.

Segment Outlook

1. Productivity and Business processes, we expect revenues of $ 32.2bn to $32.5bn. Growth of 14% to 15%.

2. For Intelligent Cloud, we expect revenue of $30.1bn to $30.4bn. Growth of 25% to 26%

3. In More Personal Computing, we expect revenue to be 12.4bn to $12.9bn a decline in in the mid to high single digits.

Historical Performance

Microsoft Stock has performed very well in the past especially in the last five years. The total return achieved in last two decades is indicated below:

15.2% (CAGR) over last 24 years.

21.3% (CAGR) over the last 5 years (2.6X).

Highlights of the earnings conference call

“Cloud and AI is the driving force of business transformation across every industry and sector," said Satya Nadella, chairman and chief executive officer of Microsoft.

“We’re innovating across the tech stack to help customers adapt and grow in this new era, and this year, Azure surpassed $75 billion in revenue, up 34%, driven by growth across all workloads.”

This was clearly a strong, second successive quarter where they saw strong growth in many areas, driven by AI and cloud growth.

Azure surpassed $75bn in annual revenue, up 34% driven by growth across all workloads.

We have over 400 datacentres across 70 regions more than any other cloud provider.

We stood up more than two gigawatts of new capacity over the past twelve months alone and we continue to scale our capacity faster than any other competitor.

They are seeing efficiency gains in their AI operations.

Through software optimizations alone, we are delivering 90% more tokens for the same GPU compared to a year ago.

Companies and especially countries are concerned about the integrity and security of their data when workload are moved to the Cloud.

Beyond the AI fleet, we continue to build our commercial cloud to address customers' unique data residency and sovereignty requirements. We introduced this quarter, Microsoft Sovereign Cloud, the industry's most comprehensive solution spanning both public and private cloud deployments.

The trend to move workloads from on-premises infrastructure to the cloud has been in place for a few years. However, it shows little sign of slowing.

We saw accelerating growth from migrations again this quarter. Nestle, for example, migrated more than 10,000 plus servers, 1.2 petabytes of data to Azure with near zero business disruption. That makes it one of the largest and most successful migrations in business history.

When customers want to use AI on their cloud workloads, they increasingly want to use multiple AI models to meet their specific performance, cost and use requirements. Microsoft enables this through the Azure AI Foundry suite of applications .

With Foundry, they can provision inferencing throughput ones and apply it across more models than any other hyperscaler, including models from OpenAI, DeepSeek, Meta, xAI's Grok and very soon Black Forest Labs and Mistral AI.

Azure AI Foundry helps customers to design, customize and manage AI applications and AI agents at scale. The data indicates a very strong take up.

New Foundry agent service, is now being used by 14,000 customers to build agents that automate complex tasks.

The number of tokens served by Foundry APIs, we processed over 500trn, up over 7x.

Standard AI applications

Applications are becoming embedded in our daily work and life. Our family of Copilot apps has surpassed 100mn monthly active users.

Microsoft 365 Copilot is becoming the new way to organize work and workflow and work artifacts. Customers continue to adopt Copilot at a faster rate than any other new Microsoft 365 suite …A record number of customers returning to buy more seats.

Barclays, for example, will roll out Microsoft 365 Copilot to 100,000 employees globally following a successful initial.

Many other MSFT businesses have huge scale:

We now have nearly 1.5mn Security customers and continue to take share across all major categories we serve.

LinkedIn is home to 1.2bn members with four consecutive years of double-digit member growth.

In Gaming, we have 500mn monthly active users across platforms and devices.

Reason for Accelerated Cloud Migration

The MSFT management were asked about the strength of the migrations of workloads to the Cloud.

There are three things that are really happening.

One is the migrations whether it's VMware migrations or migrations of SAP or even just our own server migrations, they're pretty healthy. And as it turns out that we're still not anywhere close to the finish line.

The second thing that's also happening is cloud native applications that are scaling. This is even excluding all of the AI stuff, just the classic cloud native e-commerce company, let's say. These are scaling in a big way. And some of those customers were not on Azure previously, but now they're increasingly there because they have come for AI perhaps, but they now stay for more than AI.

And thirdly of course there are the new AI workloads. So those are three things that are all in some sense building on each other, but that's kind of what's driving our growth.

Rationale for higher capital expenditure

They were asked for the rationale for higher capital expenditure which is expected to hit $90bn in FY 2026. The answer is the current backlog and prospective demand.

We have $368bn of contracted backlog we need to deliver not just across Azure, but across the breadth of the Microsoft cloud. The spend that we're making is correlated to basically contracted on the books business that we need to deliver and we need the teams to execute at their very best to get the capacity in place as quickly and effectively as they can.

Our investments, particularly in short lived assets like servers, GPUs, CPUs, networking storage, is just really correlated to the backlog we see and the curve of demand.

We are still seeing demand improve. We are focused on building backlog, building business and delivering capacity, which we are seeing has a good ROI today in terms of our ability to get that done.

Summary.

This was a very strong set of numbers from Microsoft both for Q4 25 and the full year to end June 2025.

Despite its large size, the company continues to generate high teen percentage growth in Revenues, Operating Profit and EPS.

The company has maintained high margins and has been a steady producer of Operating Cash and Free Cash Flow.

With investment expenditure growing faster than operating cash flow, free cash flow growth has been slowing.

The company has continued to be a major purchaser of its own shares and has raised its dividend consistently. With slower free cash flow growth , the company may be more constrained in the amount of cash that it can return to shareholders.

The growth of Azure and other Cloud services at 39% (y/y) was impressive.

The main issue of concern is the high level of capital investment. The company claims it is investing to meet backlog and likely demand. However, other large tech companies are also stepping up investment and it may lead to aggregate overinvestment,

This would mean returns could be poor or even negative. In this case there would be write-offs and MSFT would suffer.

Will management be able to achieve high returns on the new investment. Their track record on capital allocation has been strong, and we give them the benefit of the doubt.

Valuation and Conclusion.

At the current share price of $513 per share, the stock is trading at a two-year forward P/E ratio of 33.9X, which is either fair value or a little expensive for a company with an ROE of +33% and a likely earnings growth of 13% to 14% on the next two to three years.

MSFT is our second largest holding (after Nvidia).

The valuation is not expensive, but it is hard to argue it is a bargain. Our best estimate for the fair value of the stock, based on a DCF Model is $430 to $ 510. However, we will continue to hold to our 4% position, as it is a good quality, low-risk company.

As the second largest company in the world by market capitalisation, it is unlikely to grow very fast. We think there is a good prospect of a minimum return of 8%-9% over the next few years.

Forgot to mention . End June also marks the end of the fiscal year. The Fiscal Year 2025 Results showed consistent 15% -17% growth across key items.

• Revenue was $281.7 billion and increased 15%

• Operating income was $128.5 billion and increased 17%.

• Net income was $101.8 billion and increased 16% (up 15% in constant currency)

• Diluted earnings per share was $13.64 and increased 16%