Microsoft (MSFT)

Q2 2025 Results

We have reported on Microsoft on a number of occasions and it has been a top 5 holding on our portfolio for 5 years. Our most recent report can be found here. We revisit the company again as it reported Q2 2025 results two weeks ago.

The background to the release was as follows: markets had fallen sharply at the beginning of the week as analysts focused on DeepSeek, which had launched an LLM on par with the leading US models from companies such as OpenAI, Google, Anthropic and so on. However, DeepSeek said they had developed the model for about $6mn, a tenth of the cost the US companies would typically incur. Market commentators fretted that cheap Chinese AI demolishes the logic for the tens of billions of dollars of investments in AI Datacentres made by large US companies, including Microsoft.

The key MSFT numbers were

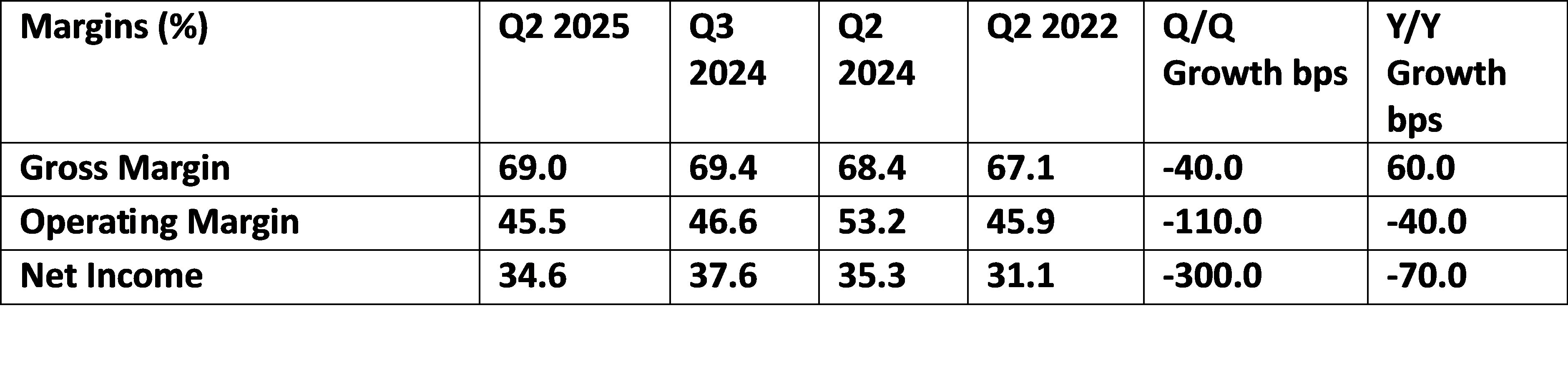

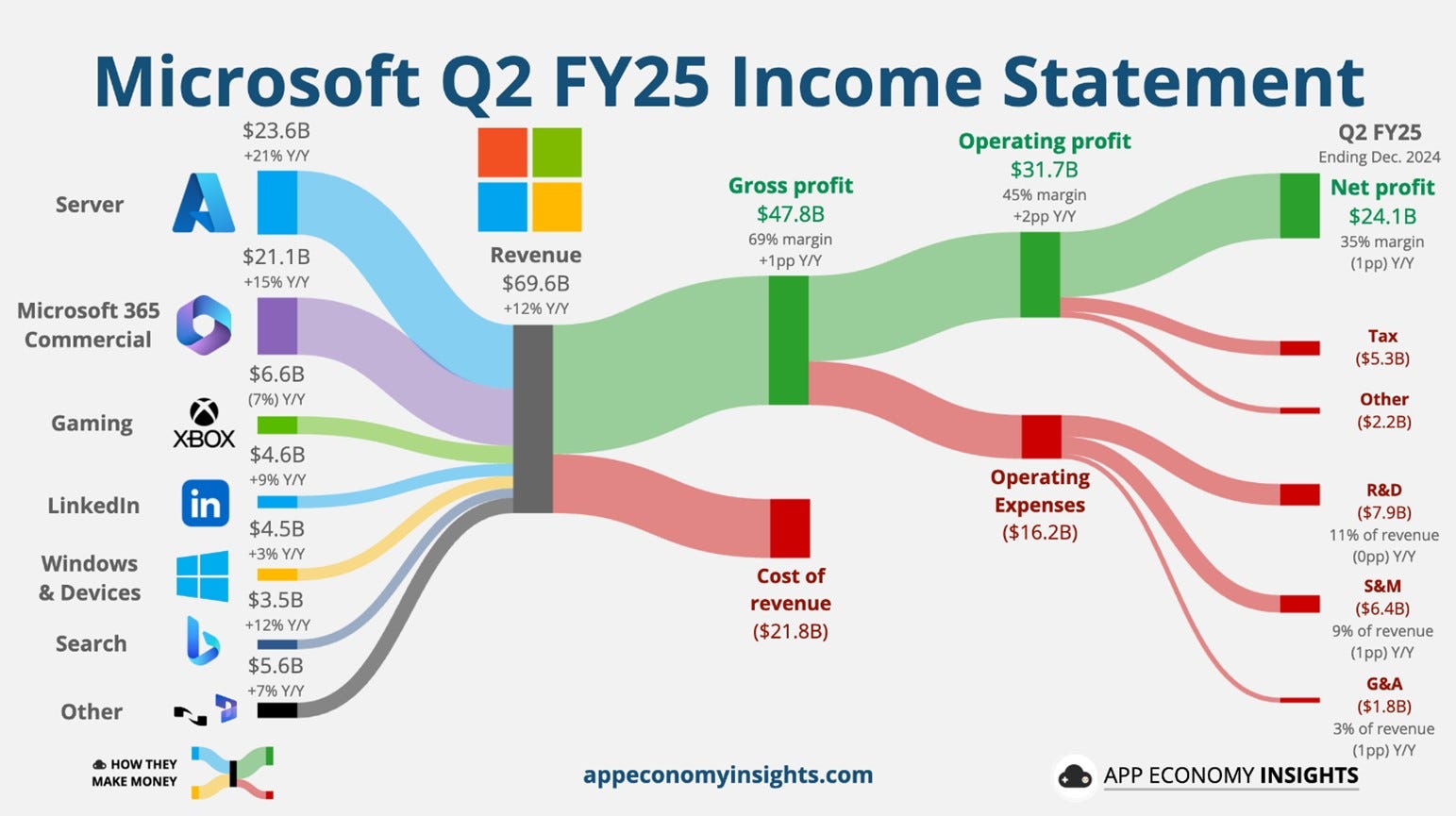

Revenue was $69.6 billion and increased 12%

Operating income was $31.7 billion and increased 17%

Net income was $24.1 billion and increased 10%

Diluted earnings per share was $3.23 and increased 10%

Operating Revenue growth at 17% (y/y) was higher than revenue growth.

Net Income margins were lower, in part due to the incidence of higher taxes at the net profit level. Margins overall are impressively high.

Segment Growth

In terms of segment growth, the trend of the last five years, where the Cloud and Enterprise business have been strong, while the consumer facing businesses have underperformed, has continued.

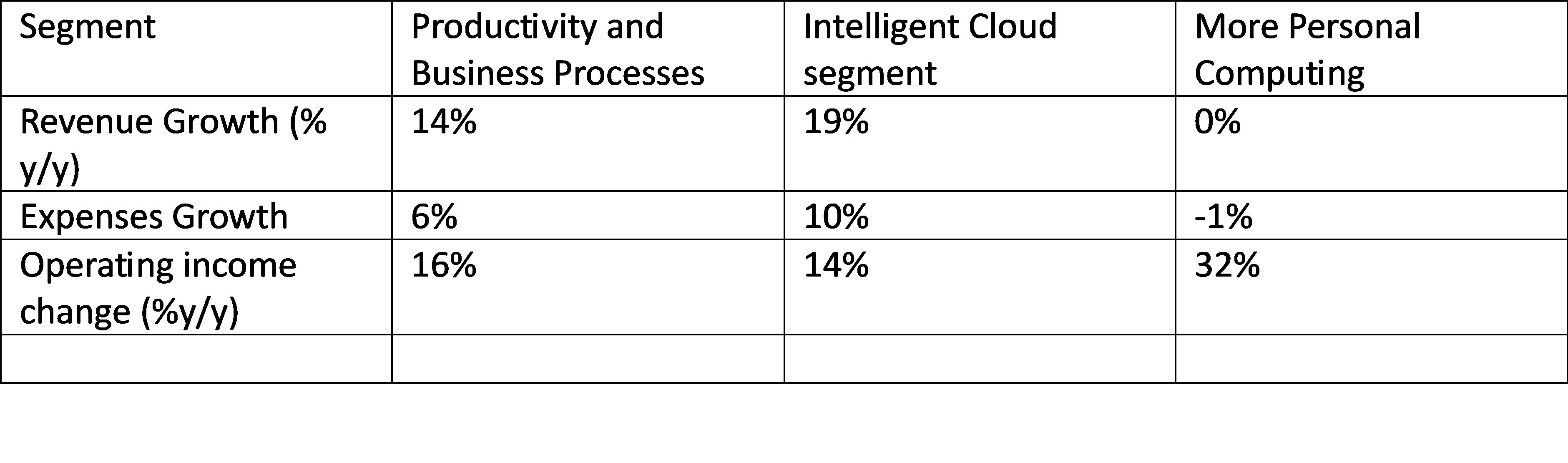

Revenue in Productivity and Business Processes was $29.4bn and increased 14%.

Revenue in Intelligent Cloud was $25.5bn and increased 19%,

Revenue in More Personal Computing was $14.7bn and was relatively unchanged.

At this point of their presentation, companies often highlight segments which have shown exceptional growth.

Our AI business has surpassed an annual revenue run rate of $13bn, up 175% year-over-year.”

Microsoft Cloud revenue was $40.9bn, up 21% year-over-year.

Productivity and Business Processes (overall up14%)

Microsoft 365 Commercial products and cloud services revenue increased 15% driven by Microsoft 365 Commercial cloud revenue growth of 16%.

Microsoft 365 Consumer products and cloud services revenue increased 8% driven by Microsoft 365 Consumer cloud revenue growth of 8%

LinkedIn revenue increased 9%

Dynamics products and cloud services revenue increased 15% (up 14% in constant currency) driven by Dynamics 365 revenue growth of 19%

Intelligent Cloud (overall up 19%)

Server products and cloud services revenue increased 21%

Azure and other cloud services saw revenue growth of 31%

More Personal Computing (overall flat)

Windows OEM and Devices revenue increased just 4%

Xbox content and services revenue increased just 2 %

Search and news advertising revenue excluding traffic acquisition costs increased 21% (up 20% in constant currency) but from a very low base.

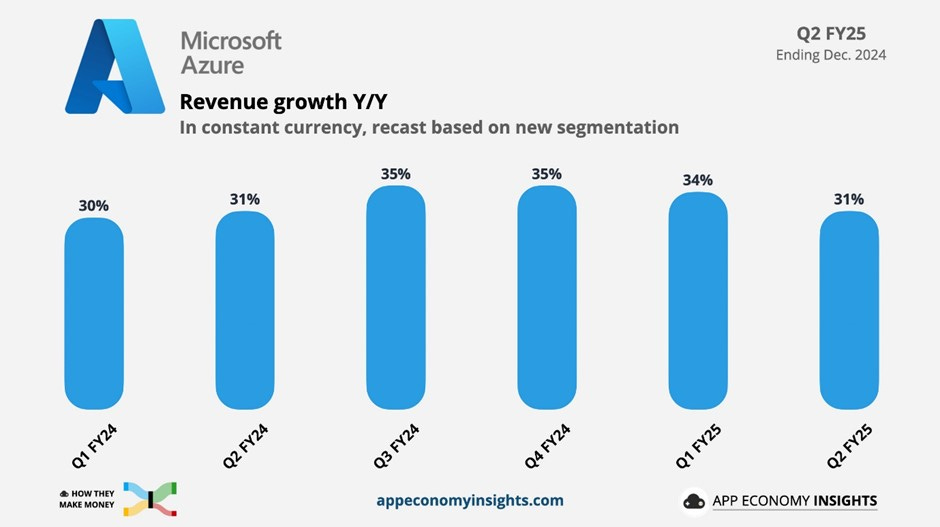

Microsoft Chief Financial Officer Amy Hood said Azure would grow between 31% and 32% in the current fiscal third quarter, below the 33% Wall Street expectations.

Microsoft's Azure unit reported revenue growth of 31% in the quarter, missing estimates of 32%. The market was especially disappointed by this and analysts asked questions about it. They were not convinced by CFO Amy Hood’s convoluted answer which suggested a focus on AI Cloud growth had led to a neglect of non-AI Cloud growth.

Microsoft's capital expenditures hit $22.6bn, above analysts' already high consensus estimate of $20.95bn.

Microsoft also posted 67% growth in what it calls commercial bookings, a measure of new contracts signed with large customers and this was largely driven by OpenAI’s commitments to use Microsoft Azure cloud network in the future. This data was released for the first time.

Highlights of Earnings Conference Calls

Continued strength in Microsoft Cloud, which surpassed $40bn in revenue for the first time, up 21% (y/y).

Enterprises are beginning to move from proof of concepts to enterprise-wide deployments to unlock the full ROI of AI.

AI business has now surpassed an annual revenue run rate of $13bn, up 175% year over year.

Given the news about DeepSeek’s cut-price AI model two days before, the CEO of Microsoft was keen to emphasise how their AI models and processes are getting more efficient.

AI scaling laws continue to compound across both pre training and inference time compute. We ourselves have been seeing significant efficiency gains in both training and inference for years now. On inference, we have typically seen more than 2x price performance gain for every hardware generation and more than 10x for every model generation due to software optimizations.

When token prices fall, inference computing prices fall, that means people can consume more and there'll be more apps written. And it's interesting to see that when I reference these models that are pretty powerful, it's unimaginable to think that here we are in sort of beginning of 2025 where on the PC you can run a model that required pretty massive cloud infrastructure. That type of optimizations means AI will be much more ubiquitous. And so therefore for a hyperscaler like us, a PC platform provider like us, this is all good news.

As AI becomes more efficient and accessible, we will see exponentially more demand.

From now on, it's a more continuous cycle governed by both revenue growth and capability growth, thanks to the compounding effects of software driven AI scaling laws and Moore's Law.

Our datacentres, networks, racks and silicon are all coming together as a complete system to drive new efficiencies to power both the cloud workloads of today and the next generation AI workloads.

We continue to take advantage of Moore's Law and refresh our fleet as evidenced by our support of the latest from AMD, Intel, NVIDIA as well as our first party silicon innovation from Maya, Cobalt Boost and HSM.

In any case, the DeepSeek R1 Model will be offered on the Microsoft platform. Microsoft said it had added DeepSeek, the breakout Chinese AI model, to its offerings on Azure just before the release of the results.

DeepSeek's R1 launched today via the model catalogue on Foundry and GitHub with automated red teaming, content safety integration and security scanning.

Satya Nadella had talked of the Jevons Paradox which states that ”In the long term, an increase in efficiency in resource use will generate an increase in resource consumption rather than a decrease.”

If AI become cheaper and ubiquitous to the extent it will run on most PCs and laptops, they believe they will benefit as a leading provider of Cloud hosting and software running on PCs.

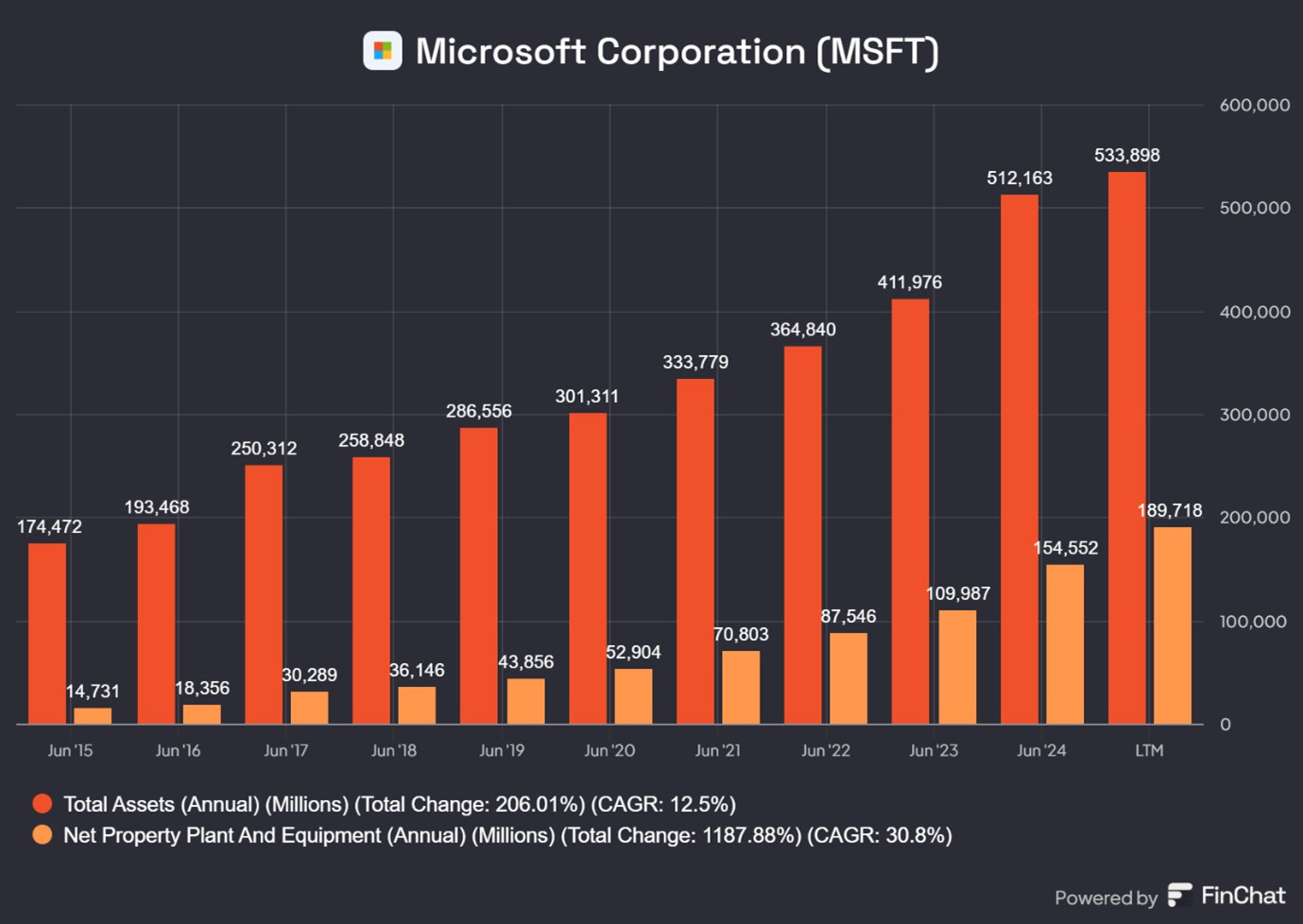

Capital Intensity

Once upon a time Microsoft was a capital light software company. However, with all the investments made in Cloud infrastructure and more recently in AI Data centres, that is no longer the case. The CEO kept talking about the “fleet” in much the same way as the CEO of UPS might talk about his fleet of vans, trucks and aircraft.

The core thesis behind our approach to how we manage our fleet and how we allocate our capital to compute.

As we have done with the commercial cloud, we are focused on continuously scaling our fleet globally and maintaining the right balance across training and inference as well as geographic distribution.

These comments indicate that MSFT and, perhaps Google, are not capital light any more.

The chart above shows Microsoft Net Property Plant and Equipment (PPE) has risen from about 8% of total assets in 2015 to about 38% currently, a big change.

Billions of dollars of investments have been made and will continue to be made.

Azure is the infrastructure layer for AI. We continue to expand our datacentre capacity in line with both near term and long-term demand signals. We have more than doubled our overall datacentre capacity in the last 3 years (26% CAGR). We have added more capacity last year than any other year in our history.

The growth of AI is seeing a huge increase in AI apps which are greatly boosting demand for the Azure platform, Cloud hosting services and many, many other products and services.

The MSFT CEO noted demand for Fabric is growing. Microsoft Fabric is an end-to-end analytics and data platform designed for enterprises that require a unified solution. It encompasses data movement, processing, ingestion, transformation, real-time event routing, and report building. It offers a comprehensive suite of services including Data Engineering, Data Factory, Data Science, Real-Time Analytics, Data Warehouse, and Databases.

At the data layer, we are seeing Microsoft Fabric breakout. We now have over 19,000 paid customers from Hitachi to Johnson Controls to Schaeffler. Fabric is now the fastest growing analytics product in our history. Power BI is also deeply integrated with Fabric with over 30mn monthly active users, up 40% since last year.

We are seeing new AI driven data patterns emerge. If you look underneath ChatGPT or Copilot or Enterprise AI apps, you see the growth of raw storage, database services and app platform services as these workloads scale. The number of Azure Open AI apps running on Azure databases and Azure app services more than doubled year over year, driving significant growth in adoption across SQL Hyperscale and Cosmos DB.

Azure AI Foundry features best in class tooling, runtimes to build agents, multi agent apps, AI ops, API access to thousands of models. It only been running two months but we already have more than 200,000 monthly active users and we are well positioned with our support of both OpenAI's leading models and the best selection of open-source models and SLMs.

Our 5 family of LLMs has now been downloaded over 20mn times.

And we also have more than 30 models from partners like Bayer, Page AI, Rockwell Automation, Siemens to address industry specific use cases. With AI, how we build, deploy and maintain code is fundamentally changing.

And GitHub Copilot is increasingly the tool of choice for both digital natives like ASOS and Spotify as well as world's largest enterprises like HP, HSBC and KPMG. We've been delighted by the early response to GitHub Copilot and Versus Code with more than 150mn developers, up 50% over the past 2 years.

We are thrilled Open AI has made a new large Azure commitment. Through our strategic partnership, we continue to benefit mutually from each other's growth. OpenAI's APIs are exclusively running on Azure, customers can count on us to get access to the world's leading models.

In the last month or so, there has been a very public fight between the CEO of Microsoft, Satya Nadella and the CEO of Salesforce, Marc Benioff. Both companies want their software to be used by knowledge workers as the gateway/ platform through which AI work is done.

Salesforce makes CRM software as well as Slack, Tableau, and others. Its CEO Marc Benioff has talked about how CEOs will no longer lead all-human workforces. Millions of workers will have AI agents who will be their co-workers. Salesforce has launched Agentforce in their CRM. Knowledge workers can use Agentforce to quickly create Agents to do much of their work for them.

Salesforce describes Agentforce as follows: “Agentforce engages customers autonomously across channels 24/7 in natural language. It can resolve cases swiftly and accurately because every answer is grounded in trusted data. Set up a set of prebuilt skills to empower Agentforce to support customers in minutes or customise fast with low-code.”

Agentforce introduces fully autonomous agents. These agents don't just offer suggestions—they can complete tasks independently. For example, they can handle customer inquiries, troubleshoot issues, and even make sales recommendations without human intervention.

Benioff has publicly criticised Microsoft 365 Copilot saying it a very poor product and Agentforce produced agents are much better. They do the work for humans rather than just help humans do their work which they argue is the copilot modus operandi.

In the earnings conference call, Satya Nadella, the MSFT CEO, said Copilot is the de facto user interface works for AI. He believes, Copilot will be the User Interface (UI) for AI and is seeing huge demand from paying customers.

Microsoft 365 Copilot is the UI for AI. It helps supercharge employee productivity and provides access to a swarm of intelligent agents to streamline employee workflow. We are seeing accelerated customer adoption across all deal sizes as we win new Microsoft 365 Copilot customers and see the majority of existing enterprise customers come back to purchase more seats. When you look at customers who purchased Copilot during the Q1 of availability, they have expanded their seats collectively by more than 10x over the past 18 months.

To share just one example, Novartis has added thousands of seats each quarter over the year and now have 40,000 seats. Barclays, Carrier Group, Pearson and University of Miami all purchased 10,000 or more seats this quarter. And overall, the number of people who use Copilot daily again more than doubled quarter over quarter.

Employees are also engaging with Copilot more than ever. Usage intensity increased more than 60% quarter over quarter and we are expanding our TAM with CoPilot chat which was announced earlier this month.

The adoption of Copilot has been aided by the launch of Copilot Studio

With Copilot studio, we are making it as simple to build an agent as it is to create an Excel spreadsheet. More than 160,000 organizations have already used Copilot Studio and they collectively created more than 400,000 custom agents in the last 3 months alone, up over 2x quarter over quarter. We've also introduced our own first party agents to facilitate meetings, manage projects, resolve common HR and IT queries and access SharePoint data. And we also continue to see partners like Adobe, SAP, ServiceNow and Workday build their 3rd party agents and integrate with Copilot.

The reason for the success of Copilot is due to the large amount of data that is stored in the various components of Microsoft software and applications.

What is driving Copilot as the UI for AI as well as our momentum with agents is our rich data cloud, which is the world's largest source of organizational knowledge.

Billions of emails, documents and chats, hundreds of millions of Teams meetings and millions of SharePoint sites are added each day. This is the enterprise knowledge cloud. It is growing fast, up over 25% year over year. More broadly, what we are seeing is Copilot plus agents disrupting business applications and we are leaning into this.

Copilot is already being automatically incorporated in many new PCs.

15% of premium price laptops in the U. S. this holiday were Copilot Plus PCs and we expect the majority of the PCs sold in the next several years to be Copilot Plus PCs. And they will soon be able to run DeepSeek's R1 digital models locally on Copilot Plus PCs as well as the vast ecosystem of GPUs available on Windows. And beyond Copilot Plus PCs, the most powerful AI workstation for local development is a Windows PC running WSL2 powered by NVIDIA RTX GPUs.

Results were driven by strong demand for our cloud and AI offerings, while we also improved our operating leverage with higher-than-expected operating income growth. … our AI business annual revenue run rate surpassed $13bn and was above expectations.

Microsoft’s order books have continued to grow.

Commercial remaining performance obligation increased to $298bn up 34%. Roughly 40% will be recognized in revenue in the next 12 months, up 21% year over year. The remaining portion recognized beyond the next 12 months increased 45%.

In all segments, expenses growth was less then revenue growth

As noted above, Azure growth included 13 points from AI Services, which grew 157% year over year and was ahead of expectations even as demand continued to be higher than our available capacity.

Let me spend a little time on that, about what we saw in Q2 and give you some additional background on the near-term execution issues that we're talking about. First, let me be very specific. They are in the non-AI Azure component. Our AI Azure AI results were better than we thought due to very good work by the operating teams pulling in, some delivery dates even by weeks.

When you're capacity constrained, weeks matter and it was good execution by the team and you see that in the revenue results. On the non-AI side, really the challenges were in what we call the scale motions. So think about primarily these are customers we reach through partners and through more indirect methods of selling. And really the art form there is as these customers, which we reach in this way, are trying to balance how do you do an AI workload with continuing some of the work they've done on migrations and other, fundamentals. We then took our sales motions in the summer and really changed to try to balance those two.

As you do that, you learn with your customers and with your partners on sort of getting that balance right, between where to put our investments, where to put the marketing dollars and importantly, where to put people in terms of coverage and being able to help customers make those transitions. And I think we are going to make some adjustments to make sure we are in balance because when you make those changes in the summer, by the time it works its way through the system, you can see the impacts and whether you have that balance right. And so the teams are working through that. They're already making adjustments.

Growth in our non-AI services was slightly lower than expected due to go to market execution challenges, particularly with our customers that we primarily reached through our scale motions as we balance driving near term non AI consumption with AI growth.

This was not a clear explanation but it suggests an excessive focus on AI cloud growth constrained non-AI cloud growth.

Capital expenditures.

We expect quarterly spend in Q3 and Q4 to remain at similar levels as our Q2 spend. In FY 26, we expect to continue investing against strong demand signals, including customer contracted backlog we need to deliver against across the entirety of our Microsoft Cloud.

However, the growth rate will be lower than FY 25 and the mix of spend will begin to shift back to short lived assets, which are more correlated to revenue growth. As a reminder, our long-lived infrastructure investments are fungible, enabling us to remain agile as we meet customer demand globally across our Microsoft cloud, including AI workloads.

Outlook for FY 2025

For the full fiscal year, we continue to expect double digit revenue and operating income growth as we focus on delivering efficiencies across both COGS and operating expense. And given the operating leverage that we've delivered throughout the year, inclusive of efficiency gains as we scale our AI infrastructure and utilize our own AI solutions, we now expect FY 25' operating margins to be up slightly year over year.

OpenAI has historically had a close relationship with Microsoft but had just announced a new venture called Stargate in collaboration with Softbank, Oracle and the US Government. The funding size has been reported to be up to US$ 500bn but Microsoft is not involved.

We remain very happy with the partnership with OpenAI. They have committed in a big way to Azure and even in the bookings what we recognize is just the first tranche of it.

Summary

In one sense this was just another normal set of results at Microsoft. The Cloud and Enterprise business continued to perform well while the consumer facing business again struggled.

In another sense, it was completely new scenario because of the widespread realisation that the DeepSeek model was performing in par with the leading models but had cost a small fraction to develop.

This suddenly raised important question about the huge AI investments the big five companies (Microsoft, Google, Amazon, Meta and Oracle) and others such As OpenAI and Anthropic are making in AI infrastructure. Does the DeepSeek announcement, taken at face value, mean that these massive investments will turn out to be a very poor use of capital.

MSFT for one is not worried. The big companies are committed to continue to make investments in AI and at this point, we have to give them benefit of the doubt. Time will tell whether their investment decisions were the correct ones.

Markets were disappointed that Azure growth at 31% (y/y) was lower than the 33% expected and the company did not give a good explanation of the shortfall. The MSFT share price fell over 5% after the results and have declined further since then. They are now 10% below the level prevailing before the results came out. They are only up 2% in the last twelve months. Microsoft shares have underperformed other large-cap tech stocks in the last two years.

Valuation

At the current share price of $415 per share, the stock is trading at a two-year forward P/E ratio of 27.9 X which is a reasonable level for a company with an ROE of +34% and a likely earnings growth of 11% to 14% on the next two years.

However given the rapid increase in the capital intensity of the business, there must be some fears that the ROE will perhaps fall in the future below 30% and tends towards 25% and therefore returns on the stock will tend to gradually reduce in the future

Conclusions

MSFT looks well placed to benefit from the unfolding AI revolution. The company continues to perform well but it is not firing on all cylinders as the consumer performing business continue to underperform.

The company is likely to generate low double digit percentage revenue and net profit growth in the next two years. The stocks Is more reasonably priced after the 10% decline following the earnings release.

We give the management the benefit of the doubt and continue to hold the stock.