Introduction

We have written three previous notes on Netflix (NFLX). The first was an “Initiating Coverage” type note from 8 April 2024 and can be found here. Our second note was written on 26 July 2024 and can be found here. We also wrote in November 2024 on the Q3 results and that note can be found here.

We made a 2% investment after the July note and the NFLX stock has advanced 56% since then. We added an additional 1% after the November 2024 note and the stock has advanced about 6% since then

In the last twelve months the NFLX stock has advanced 73% and it accounts for about 5% of our total portfolio and 7% of our equity portfolio. The difference is due to the current large cash holding in the portfolio.

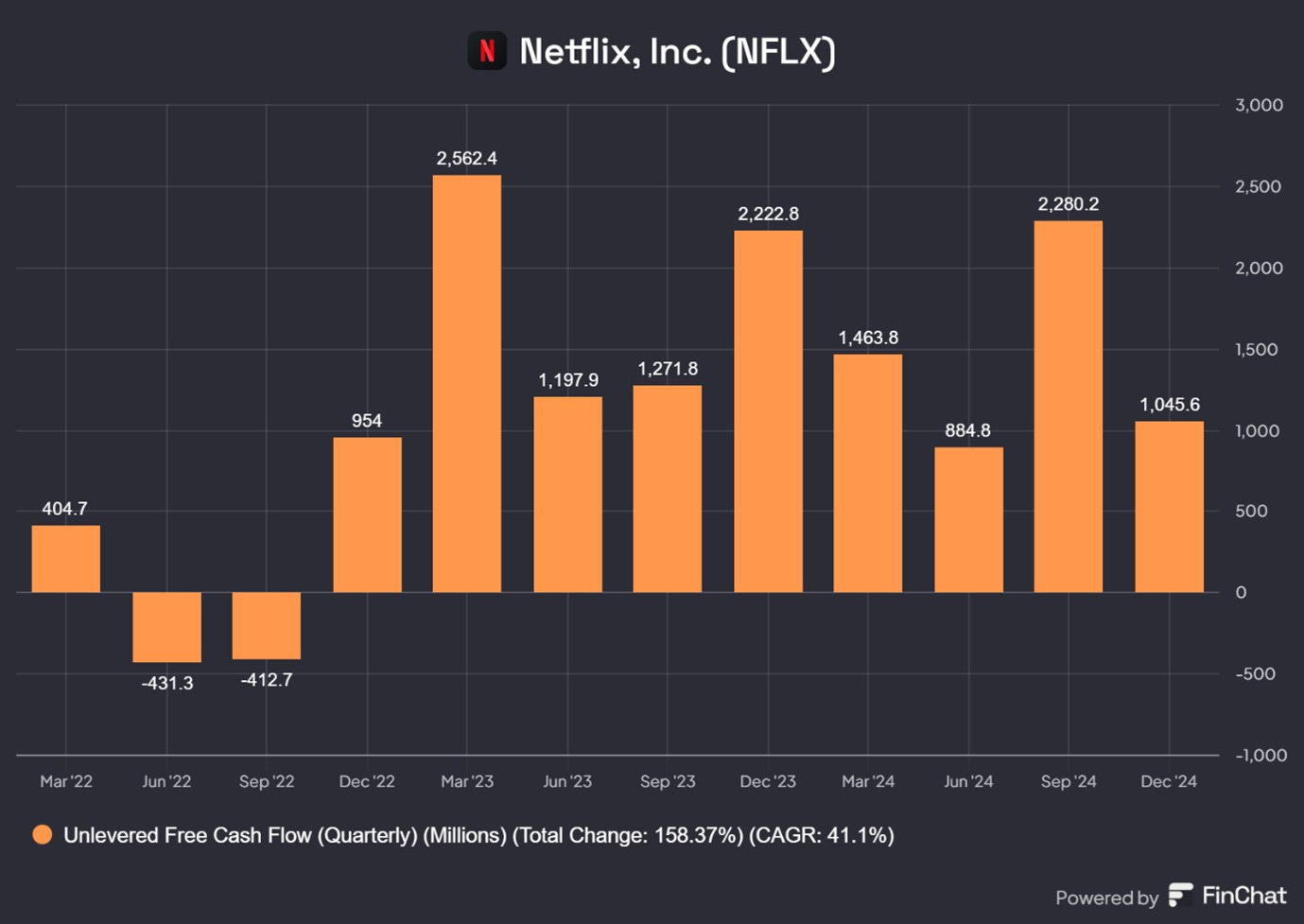

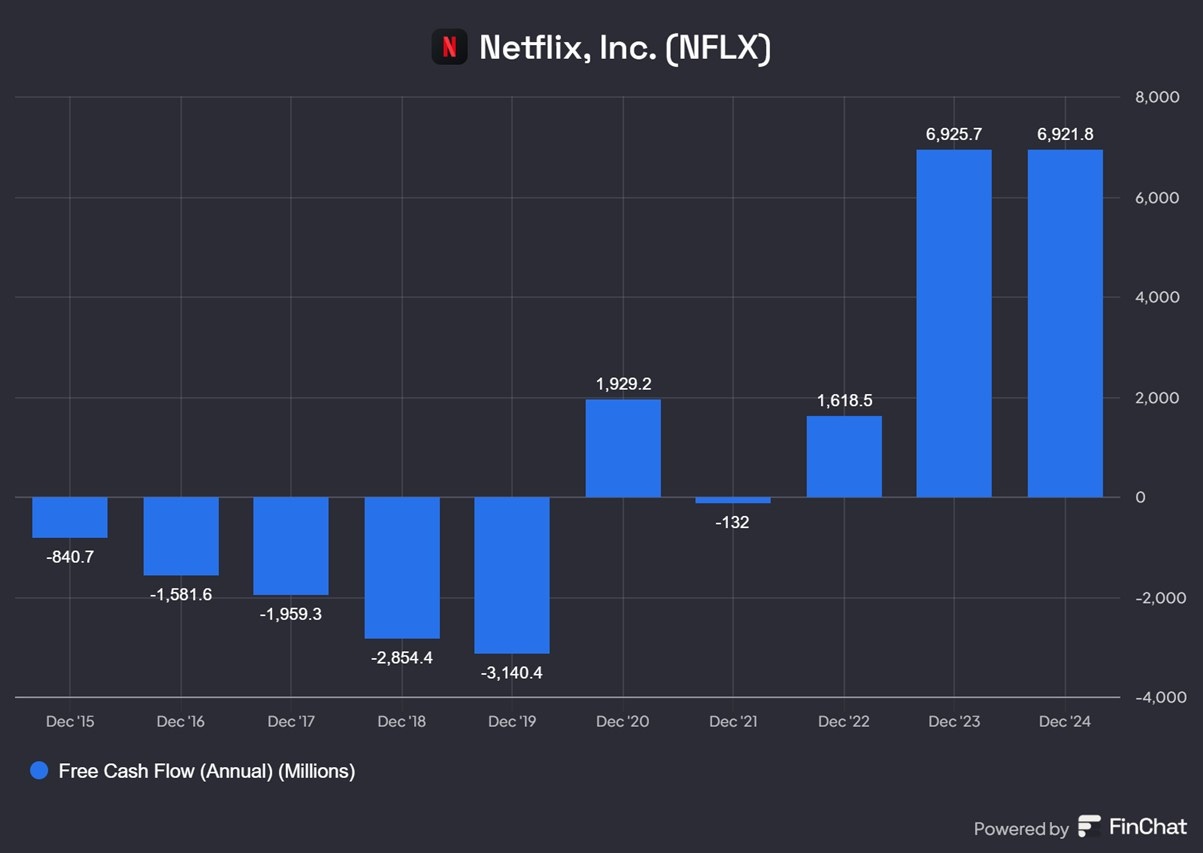

In our various notes we discussed how Netflix has spent the decade to about 2022 investing in content. This was financed by debt was marked by negative free cash flows. Since then, revenue growth as kicked and the company free cash flow turned positive.

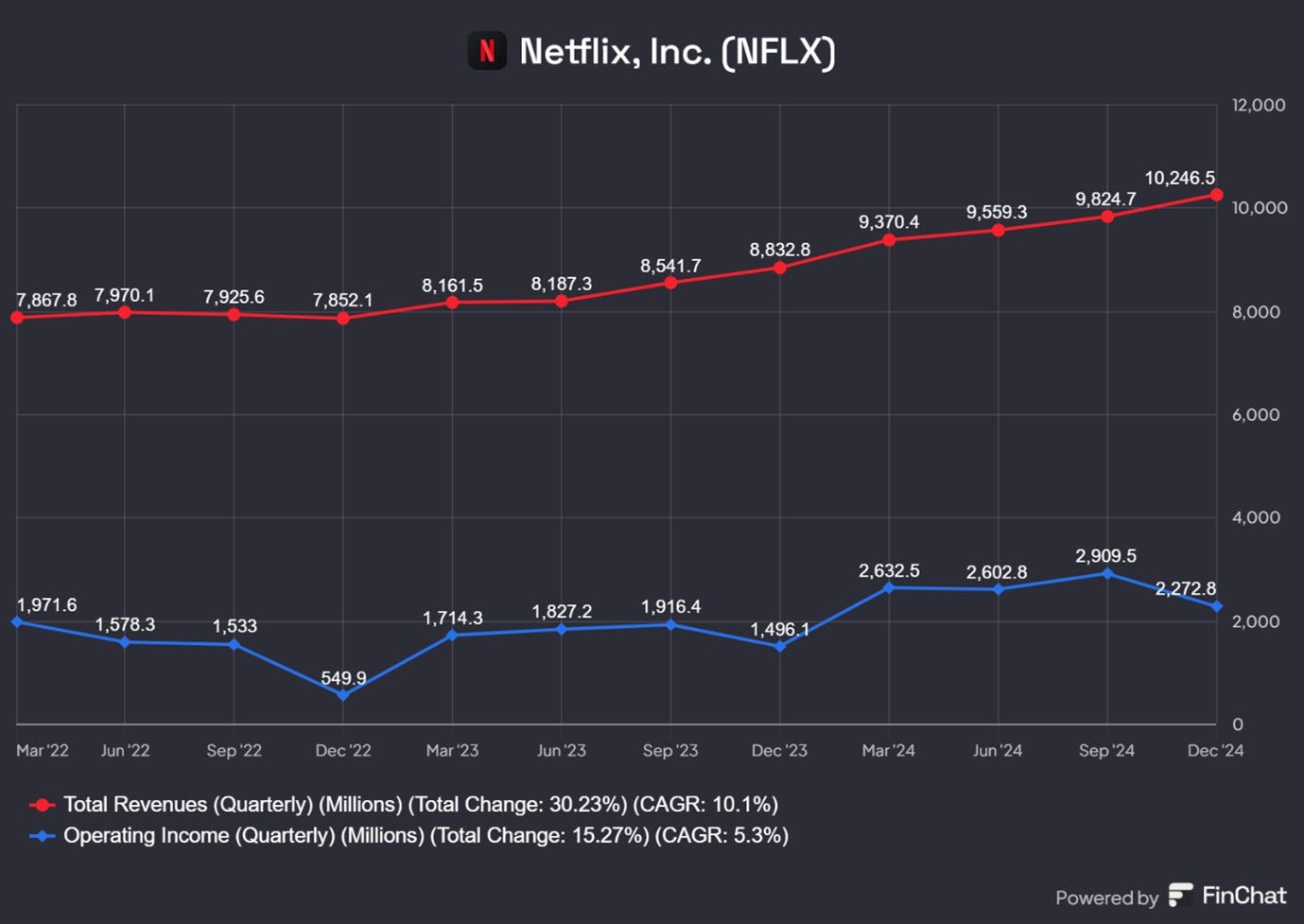

Revenue and Operating Profit has grown driven by an end to password sharing and the introduction of a cheaper ad-supported tier. (See Chart below)

Q4 Results

Take a moment to look at these astonishing numbers.

Total Revenue grew 4.3% (q/q) and 16% (y/y).

Operating Profit grew 51.9% (y/y)

Net Profit grew 99.2% (y/y/)

Earnings per Share (EPS) grew nearly 105%.

The business is clearly in a very sweet spot as regards operating leverage with 16% revenue growth being translated into 99% growth in Net Profit.

What drove the Revenue growth? All regions saw double digit percentage revenues growth. Leading the pack was Asia Pacific with 25.9% growth (y/y) and EMEA with 18% (y/y).

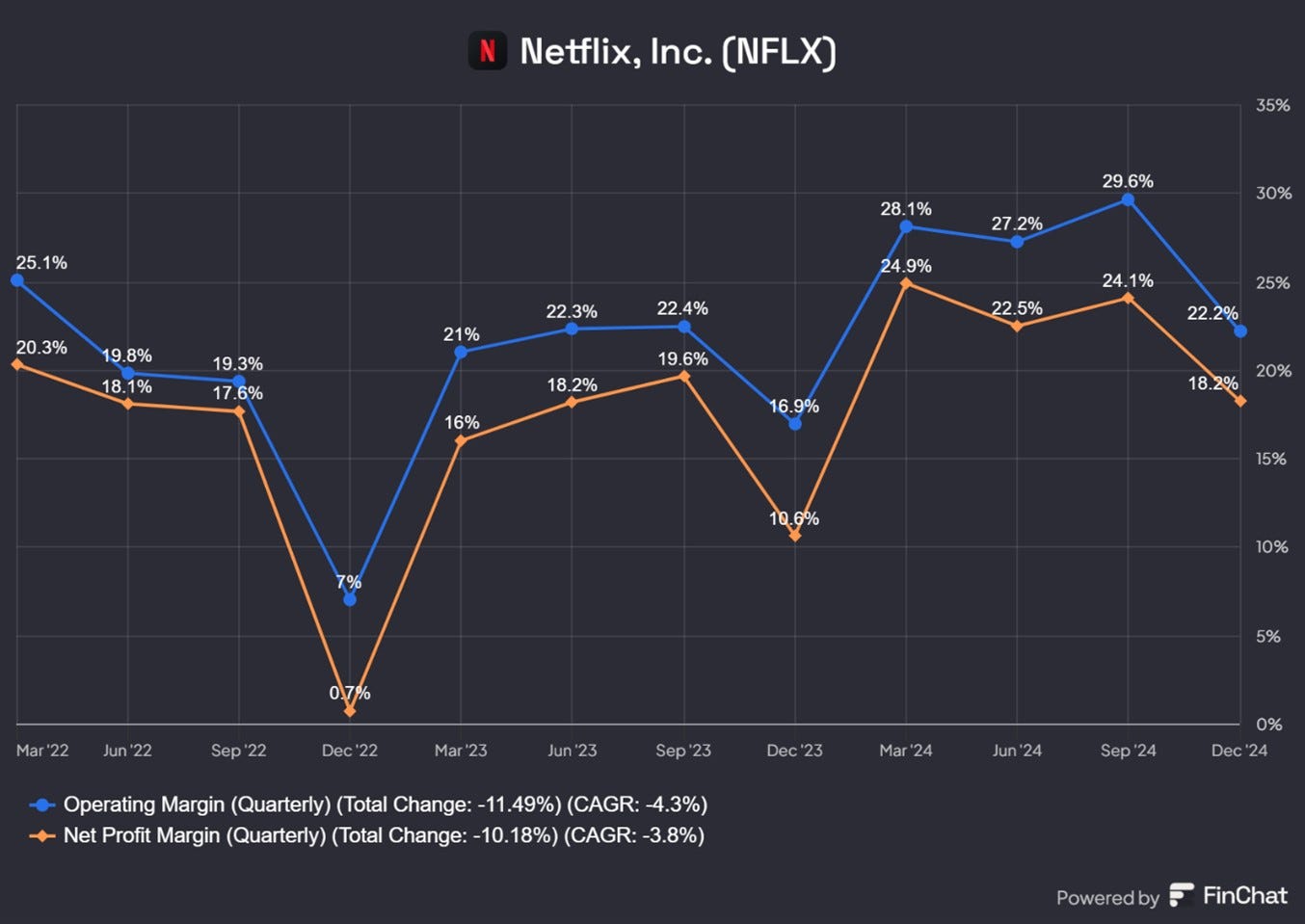

The huge expansion in margins explains the inflection in operating leverage noted above.

Operating Margins increased 430pbs to 22.2% (y/y)

Net Income Margins increased 761bps to 18.2% (y/y)

However, they did fall on a q/q basis suggesting a peak in margins in the previous quarter (q3 2024) or a big dip in margins in Q4 2023. The charts below suggest that both these factors apply and indicate a seasonal factor where margins dip in December. However, the general trend in the last two years has been of higher margins.

The main headline after the results was that Netflix paid subscriptions had hit 300mn for the first time. Paid Memberships grew 21.8% (y/y). This was led by APAC (+30%) while North America (UCAN) showed the slowest growth.

The more relevant membership data is Net Memberships which adjust for cancellations. Net Memberships grew by 18.9mn in Q4 2024.

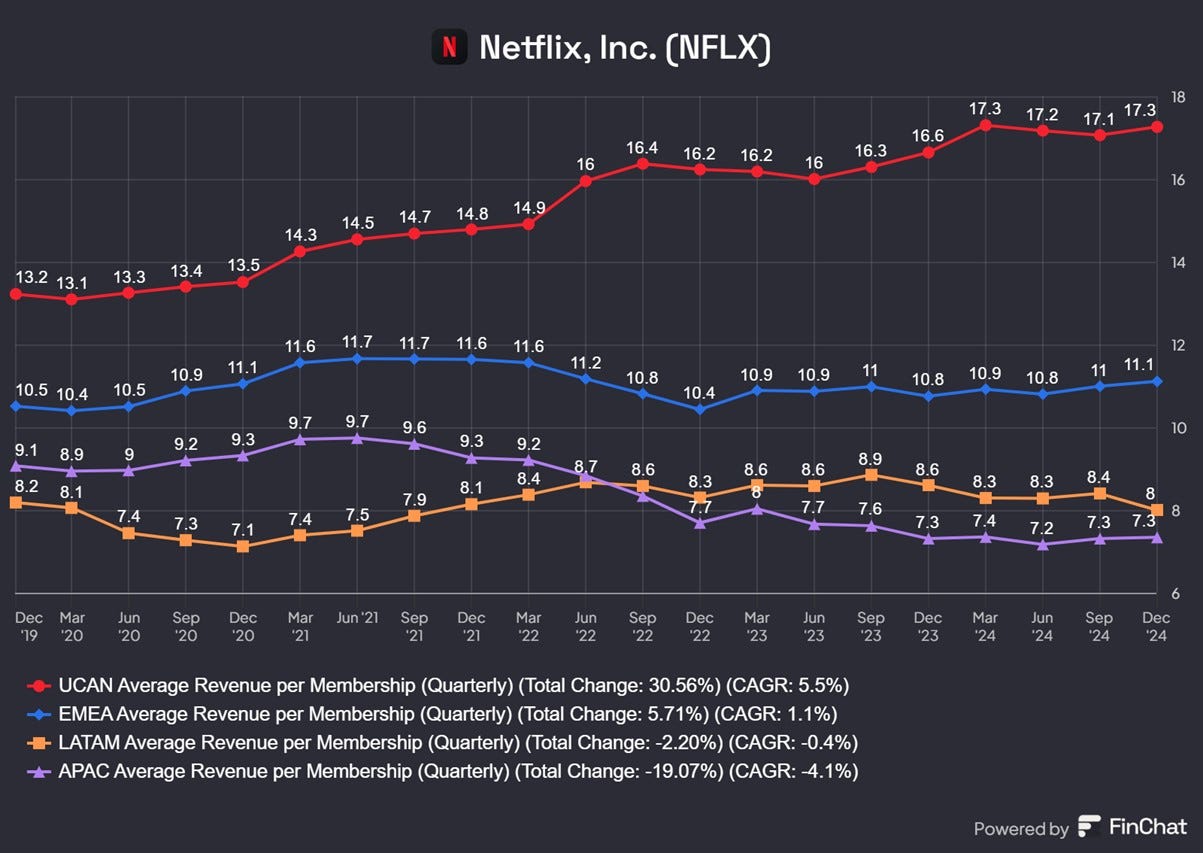

Not all memberships are equal as there are significant geographical variations in average revenue per user (ARPU).

Quarterly ARPU in UCAN at $17.3 is considerably higher than elsewhere and has also rose more than other geographies. APAC is at the lowest at $ 7.3 per quarter.

Key Numbers

NETFLIX Q4 REVENUE $10.25 BILLION VERSUS IBES ESTIMATE $10.11 BILLION- Revenue beat expectations

NETFLIX Q4 EPS $4.27 VERSUS IBES ESTIMATE $4.20- EPS Beat expectations

NETFLIX Q4 GLOBAL STREAMING PAID NET ADDITIONS 18.91 MILLION VERSUS IBES ESTIMATE 9.6 MILLION- double what was expected

NETFLIX OUTLOOK Q1 EPS $5.58 VERSUS IBES ESTIMATE $5.98- EPS Q1 outlook below expectations

NETFLIX OUTLOOK Q1 REVENUE $10.42 BILLION VERSUS IBES ESTIMATE $10.49 BILLION- EPS Revenue outlook below expectations

NETFLIX OUTLOOK FY 2025 REVENUE OF $43.5 BILLION - $44.5 BILLION VERSUS IBES ESTIMATE $43.64 BILLION

NETFLIX OUTLOOK FY 2025 OPERATING MARGIN OF 29%

NETFLIX: ADJUSTING PRICES TUESDAY ACROSS MOST PLANS IN US, CANADA, PORTUGAL AND ARGENTINA -Price rise coming in many markets

NETFLIX: APPROVED INCREMENTAL $15 BILLION SHARE BUYBACK PROGRAM

NETFLIX: INTRODUCING EXTRA MEMBER WITH ADS OFFERING IN 10 OF 12 COUNTRIES WITH ADS PLAN TO GIVE MEMBERS ADDITIONAL CHOICE

Highlights from the earnings conference call

The fourth quarter saw three key livestreamed events on Netflix. They livestreamed two NFL games including one on Christmas day which featured a halftime performance from Beyoncé. In November, there was a mismatched boxing match between Mike Tyson and Jake Paul. Both attracted huge audiences. In addition, the Korean drama, Squid Game Season 2 was broadcast.

The NFL games were the two most streamed NFL games in US history with an average audience of over 24M viewers each. The boxing fight was the most streamed sporting event in history. Over 108mn people tuned in to watch the event globally.

These three events boosted audiences but the company claims this was not the major reason for their success in the quarter.

At a high level, we've seen broad strength across content categories across all regions. We've seen it throughout the entire year. And as we've consistently seen across our history, no single title really drives the majority of our acquisition or engagement. So, even in an amazing quarter where we had three huge live events, our estimates for subscriber adds driven by those titles combined represent a small minority of our total member acquisition in the quarter. So, it's really the whole service that's working that delivered the upside that we saw this quarter. The vast majority of our net adds were driven by our broad slate in our portfolio globally.

It's great that all these big swings worked very well in the quarter, but for -- to be able to have that translate into revenue growth meaningfully, everything has to be working. The product, the pricing teams, the marketing, the advertising, all those things have got to be working well and we saw really strong execution across the board throughout the quarter and throughout the year.

Advertising Subscription Tier

The company launched a lower cost subscription with advertisements and this has been very successful in attracting those who may otherwise have left Netflix or those who would never have signed up for the higher cost no-ads tiers.

“We love our ads plan because it allows us to offer a lower-price point for consumers. That's more choice, good accessibility that is proving to be popular and it means that we obviously have more people that can sign-up and enjoy the growing range of entertainment that we've got to offer. It's also the reason that we've been successful in driving that first ads priority we had in our ads goals, our most primary ads goals, which were to get to sufficient scale. In Q4, ads plan represented over 55% of sign-ups across our ads’ countries. We've seen membership on those ads plan increase about 30% quarter-over-quarter. This last quarter that was on top of 35%, the quarter before, on top of significant growth the quarters before that.”

Not only are people signing up with the ad tiers but they are also engaging with the content

“Moreover, engagement of those ads members remains healthy. So, view hours per member on the ads plan is similar to engagement on our standard non-ads plan in our ads country, which is a really good marker that we're excited about. So, we've done the work, I would say, to meet our scale goals for advertisers in '25.

Now they have the audience in the ad-tiers, they need to monetise it by effectively targeting and selling advertisements. This is described as a priority for the next several years.

We've been able to shift more of our focus, more of our attention on making the offering better for advertisers to increase monetization of that growing inventory. This is going to remain a priority and part of our roadmap for at least the next several years, but we're making solid progress already. For example, we exceeded our ads revenue target in Q4, which was an exciting milestone to get. We doubled our ads revenue year-over-year last year. We expect to double it again this year. So that should give you a sense of the slope of monetization growth that we're on. And broadly, we think of this as we're making solid progress, there's considerable work ahead of us for sure. we think our path is relatively straightforward and we're confident we've got a significant runway to continue to grow that revenue.

Targeting and selling advertising in a Connect TV (CTV) context requires great technology and execution

A big part of that is standing up our own ad stack. We launched that in Canada and that's done well. We're testing, we're learning quickly as we prepare to then roll that out in 2025 across the rest of our 12 ads countries, starting with the U.S. in April. And the biggest initial benefit we have of using our own ad server is just enabling us to offer more flexibility, more ways of buying for advertisers, fewer activation hurdles, just improving the overall buyer experience.

“And we're already seeing the impact of those benefits in the revenue growth in Canada. So that's exciting and improves our optimism around it. And then, over time, the first-party ad tech platform allows us to deliver more critical capabilities to advertisers that we hear from them that they really need.”

We're talking enhanced targeting, we're leveraging more data sources, more measurement, more reporting, more incrementality studies. So, being on our own tech stack enables all those advertising features -- advertiser-facing features, but the other big benefit is it just creates a higher quality experience for our members, so it increases relevance. That's good for them, it's good for advertisers, it's good for us, it's good for everybody in the ecosystem, essentially. Just so, to reiterate, we got many years of building ahead of us. The roadmap is clear. We're committed to iterative innovation in advertising, just as you've seen us do in many other places.

Some analysts were concerned about the move in live sports broadcasting. They were worried that NFLX would get into bidding wars with large media companies to win the right to broadcast a season of games from various team sports or prestigious tournaments. The company seems aware of this risk and wants to stick to live events rather than a more extensive commitment.

it doesn't really change the underlying economics of full season big league sports being extremely challenging. So, if there was a path where we could actually make the economics work for both us and the league, we certainly would explore. we're going to be mindful of the bottom-line and it's really important that those economics do work and that the big-league sports, full league -- full season economics are very hard to make work. But right now, we believe that the live events business is where we really want to be and sports is a very important part of that, but it is a part of that expansion.

In addition, they have started live steaming World Wrestling Entertainment (WWE) programming which previously had been on linear television. They have increased the audience form this including the addition of viewers form outside the United States.

WWE is off to a great start. Our first week, we drew about 5 million views, which is about two times the audience that Monday Night Raw was getting in linear television. Pretty consistent with how we modelled it, how we'd hope to build the audience for the league. We also saw that the non-live viewings in the day after the live event viewing grew by 25%, mostly outside of the U.S. time zones. In the U.S., our viewing of Monday Night Raw was as big as the Monday Night Raw viewing has been in five years.

They were asked how signing up the women’s soccer world cup is consistent with this strategy?

Women's World Cup is a real TV event. It's totally consistent with what we're trying to do here. These matches set a bunch of viewing records in 2023, and women's sports have only become more interesting and more popular since. It's a month-long event filled with drama played by some of the greatest athletes in the world. We're thrilled to be the home for those games in -- starting in 2027, and we're thrilled to have the time to start telling the stories of these teams and these athletes like we've done so well with other sports, with our series and our documentaries.

The key thing is they are not just broadcasting the event but will boost it with related series and documentaries.

Carry-on is a feature film in the Thriller category which was huge success but did not have theatrical release. This is an example of the way Netflix continues to challenge norms in the film industry.

In less than two months Carry-On was well reviewed and has racked up 313 million view hours. And the film generated significant buzz across social media and is set to surpass Bird Box viewership. A movie born on Netflix that can generate an enormous audience and tons of buzz. One of the producers called me over the break to tell me that this is exactly what it feels like when I have a big movie in the theatres, which was a great thing to hear. Our social channels with over 1 billion subscribers that actually keep that conversation going. So, I think it's a really strong proof point that a movie born on Netflix can be a big hit and be the centre of culture as well.

Pricing Strategy

The philosophy is to consistently provide value and then gradually increase prices.

Our pricing philosophy hasn't changed. It's pretty much the same as we've talked about for the last several years. We look to continually provide more value to our members seeking to wisely invest to increase the variety and quality of our entertainment offering. We listen for signals like engagement, retention, acquisition, there's more secondary signals as well, all to tell us when we've achieved that increase in value. When we've done that then we ask them to pay a bit more to keep that virtuous cycle going. You've seen us take up price across a number of markets in EMEA and APAC and LatAm over the last couple of quarters across most plans and including ads too.And those changes have gone smoothly. You can see those in our results.

The longer-term monetisation runway

We feel really good about our long-term monetization opportunity. We earn right now only 6% of the revenue opportunity in the countries and segments that we currently serve. And as long as we continue to deliver on improving the variety, the quality of our TV and film slate, we gradually expand the offering with newer content types, we'll believe we'll be able to increase that share.

We're small in terms of view share and penetration everywhere around the world.

We're less than 50% penetrated into connected households. (many households in their markets do not have CTV services)

We're only capturing about 6% of our estimated revenue market. (they only account of 8% of the total streamed hours in the USA. They are a close second behind YouTube)

Future trend of spending on content

They spent $17bn on content is 2024 and this will increase to 18bn in 2025. In the financial statements, this spend is shown as a cash outflow in the Cash flow statement, a growing intangible asset on the balance sheet and a depreciation charge on the Income Statement.

I think we're a long way from equilibrium, as you say. We're taking up our cash content spend this year estimated from $17 billion to $18 billion. We set our growth based on our top-line growth and our margin targets and then we kind of allocate as we can across the business for highest impact. You've seen us do that in a responsible way where our cash spend and our content cash amortization is a 1.1 ratio roughly, between our content amortisation, which runs through the P&L, and the cash spend which runs through cash flow. And both are growing slower than our revenue growth. So, I think you should see us continuing to grow in that way for the foreseeable future as we continue to grow more and more engagement and please more and more hopefully growing audience around the world.

They expect to see operating margins to continue to expand as expenses will grow less than revenues

We're always kind of looking to balance our revenue growth with strategic investment into the business. And we think we've balanced that well this year. You see we guided to 12% to 14% top-line revenue growth. If you kind of do the read through in terms of based on our margin guidance, what that we would expect in terms of our implied expense growth, you can see it's sort of high single digit, 9% plus or minus expense growth expected for 2025.

Across the board, for the most part, we're driving margin improvement in a way that we think is appropriate for the business while investing into our growth.

Summary

These were a tremendous set of results for Netflix. The company has become the dominant player in the world of CTV and is seeing significant revenue growth combined with margin expansion. This is expected to continue in the near term.

NFLX has successfully introduced an ad- based tier and is set on a course likely to result in a significant boost in advertising revenue.

The company continues to invest heavily in content and is determined to ensure that revenues growth will be greater than the growth of spend on content.

Historically the company borrowed heavily to finance the spend on content but as revenues have grown, the path to lower debt has been established.

The company has firmly established a path of making operating profits and generating operating cash flow and free cash flow. Margins and profitability, measured by ROE and ROCE, are on a rising trend.

The company believes the runway ahead of them is still very long. They believe they have, and will continue to have. considerable scope for increasing subscribers, raising prices and boosting advertising revenues.

They believe they are only capturing 6% of the potential revenues that they could make in the territories they operate. This does give an indication of the runway they still have ahead of them

Valuation

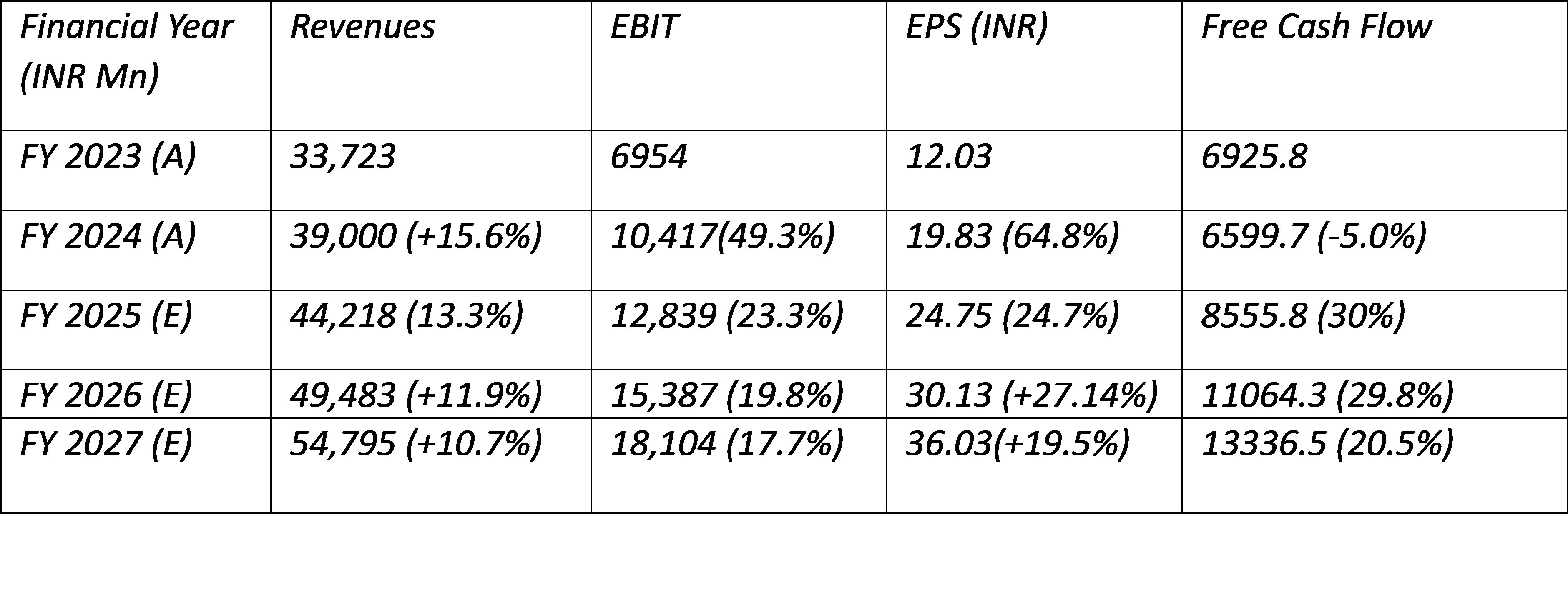

The consensus analysts’ forecasts for Revenues, Free Cash Flow and EPS are as follows:

The consensus analysts’ forecasts see low double- digit growth in revenues for the next three years with high double-digit growth in EBIT. The growth in EPS and Free Cash Flow is forecasted to be even higher than EBIT growth.

Free Cash Flow growth was negative in FY 2024 due to heavy capex but is expected to grow strongly in FY 2025 – 2027.

At the current price of $977 the NFLX stock is trading at a two-year forward P/E Ratio of 32X.

At a current market capitalization of $418bn, the two- year forward Price to Free Cash Flow ratio is 37.8X.

These numbers imply a two-year forward Earnings Yield of about 3.1% and a two-year Free Cash Flow Yield of 2.6.%.

These valuations are on the high side and the yields on the low side but reflect the high growth expectations embedded in the valuations. However the stock does not appear to be too overvalued given the company is likely to grow revenues at 11% with a likely ROE of 30% to 34%. It is hard to argue the stock is cheap, though that is a big ask in current market conditions.

We conducted a Discounted Cash Flow (DCF) Calculation.

For the DCF calculation, we had to make some additional assumptions about Revenue growth and Net income Margin in FY 28 and 29.

We assume Revenue growth in FY 2028 and FY 2029 at 11% and EBIT Margins of 30.0%. We also assume a risk-free rate of 3.75% and a Market Risk premium of 4.75%. The Stock Beta is 1.3. These numbers result in a Weighted Average Cost of Capital (WACC) of 9.5%. Finally, we assume that in FY 2029, the terminal exit multiple for EV/FCF of at the end of FY 29 is 34.

With these assumptions, we calculated a theoretical Netflix stock value of $800-about 18% below the current share price

If the terminal exit EV/FCF is reduced to a much more aggressive 32X, we get a theoretical value of $754 which is the 23% below the current share price.

These terminal exit EV/FCF multiples of between 32X and 34X may look a little high considering the good growth prospects for the company and the current profitability.

As we have noted before, the problem with all such valuation models is they are highly dependent on the inputs. If one makes small changes in the assumptions, there can be a wide range in the outputs. Therefore, all valuation estimates must be taken with a lot of salt.

It is however difficult to say the stock is valued at an attractive level. However, our best guestimate is that shareholders are likely to make 15% to 18% a year on average.

Conclusions

We have 5% of our total portfolio and 7% of our equity portfolio. We will carry on holding onto our position and we will continue to monitor the company.