Oracle Corporation (ORCL).

Cloud Revenue Take-off is here?

We wrote about ORCL on Mar 15, 2024. That report can be found here. It is worth reading if you want to understand the business and how it achieved its present structure.

We look at Oracle again in the light of their Q4 results published yesterday

In the last earnings call, Oracle Cloud Infrastructure (OCI) was described thus:

“Oracle Cloud is the first public cloud built from the ground up to be a better cloud for every application. By rethinking core engineering and systems design for cloud computing, we created innovations that solve problems that customers have with existing public clouds. We accelerate migrations of existing enterprise workloads, deliver better reliability and performance for all applications, and offer the complete services customers need to build innovative cloud applications.”

We also noted the following:

In the last 15 years there has been a huge growth in the Cloud. The emergence of large-scale cloud hosting companies has meant that IT infrastructure is no longer an upfront fixed cost but a pay as you go, variable cost.

Many tech companies established in the last 20 years are cloud-native and older companies and organisations are moving more of their workloads, data and applications to the Cloud.

We concluded our note with a section called

“The coming explosion in Cloud Revenues”

We noted the following:

Orace has developed a cloud offering that seems to be more flexible, faster and more cost effective than the existing players. It has also developed industry-specific Cloud offerings targeted towards the Financial, Healthcare and Telecom sector among others.

Oracle was not an early leader in the Cloud, but its persistent development efforts, large footprint within IT, and sizable wallet share give it a unique position of account leverage.”

As the Cloud business ramps up, the revenue profile will become becomes less volatile. The software license transactions are generally perpetual in nature and recognized as revenues up front at the point in time when the software is made available to the customer to download and use. The timing of a few large transactions can substantially affect the quarterly revenues due to the point-in-time nature of revenue recognition. This is very different to the revenue recognition pattern for cloud services and license support revenues as revenues are recognized rateably over the contractual terms.

The recent quarterly results indicate that this boost in Cloud Revenues is beginning to happen, perhaps in a big way.

Q4 Quarterly Results

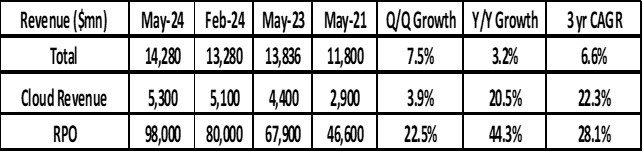

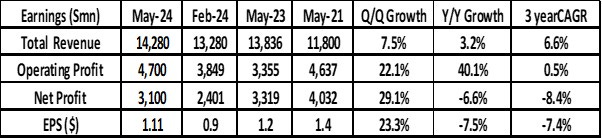

Q4 total quarterly revenues were up a relatively subdued 3% (YoY) to $14.3bn. However, within that, Cloud Revenues rose 20.5% (YoY)

The RPO (remaining performance obligations) which measures the value of contracts for which revenue has not yet been recognised is now $98bn and up 44% (YoY).

These two factors (subdued top line growth but increase RPO) are to be expected given the change in the revenue recognition policy.

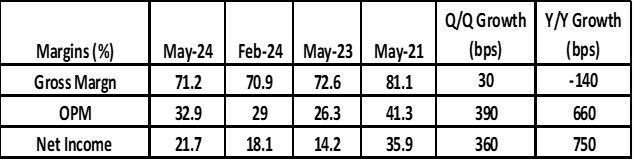

Q4 operating income was $4.7bn up an impressive 40%. Operating margin was 33%, up 660 bps (YoY).

Net income was $3.1bn.

Operating cash flow was $18.7bn during fiscal year 2024, up 9% (YoY)

Fiscal year 2024 total revenues were up 6% in USD to $53.0 bn.

The most impressive thing was the growth in Operating Income, which itself, was greatly boosted a rise in Operating Margin

The Q4 Earnings Call Highlights

The key feature of the quarter was the demand for Cloud Services,

“Q4 was powered by the enormous demand for our cloud services, and they showed up in RPO.”

“Oracle signed the largest sales contract in our history, led by huge demand for training large language models as well as record levels of sales for OCI, Autonomous, Fusion and NetSuite.”

“RPO was $98bn up $18bn from Q3 and up 44% year over year from $68bn.”

As noted in our March report, Oracle are changing the revenue recognition process from upfront revenue recognition to a pro-rata revenue recognition on the life of the contract. This makes revenue more stable and means any contracts signed now will contribute to revenue over their lifetime.

“We are trading one-time non-recurring license revenue in return for much bigger strategic customer commitments for multi-year cloud revenue from which we expect to further accelerate our revenue growth rates. “

“This is exactly what we've been targeting, and it bolsters my confidence that our overall revenue, earnings and cash flow performance as well as our growth rates will only get stronger and accelerate.”

“Q4 marks the full emergence of our high growth cloud businesses.”

“Both operating cash flow and free cash flow, which of course we report on a trailing 12-month basis, were each declining 10% 4 years ago. This year they grew 9% and 39% respectively.”

“In total, we signed over 30 AI contracts for over $12bn.”

In our March report, we noted that they had signed an agreement with Microsoft Azure where Oracle software and services are available on Microsoft Azure cloud where they can used on a time basis with no upfront costs. This quarter they signed a similar agreement with Google Cloud Platform

“We've signed another multi cloud partnership this time with Google. OCI and Google Cloud Network Interconnect is available immediately in 10 regions and we will be live with Oracle Database at Google Cloud in September where customers can get direct access to Oracle database services running on OCI deployed in Google Cloud Data Centres.”

They believe their offering is more comprehensive and more flexible. In terms of the former, Oracle is the second largest seller of enterprise software after Microsoft.

“We have the most secure, complete and cost- effective set of enterprise applications and infrastructure cloud technologies of any vendor.”

“Not only are our cloud technologies vertically integrated to work together, but we offer flexible deployment models like public cloud, multi cloud, sovereign cloud, dedicated cloud or any other way our customers ask us to deliver.”

Total cloud revenue was up 20% (YoY) at $ 5.3bn

Within that IaaS revenue of $2.0bn up 42% (YoY) on top of last year's 77% growth.

“The gross margin for cloud services and license support was 77%. This is a result of the mix between support and cloud in which cloud is growing much faster. Gross margins will go higher as more of our cloud regions fill up. We monitor our expenses carefully to ensure gross margin percentages expand as we scale.”

“The operating margin was 47%, up from 44% last year as we continue to drive more efficiencies in our business.”

“As we continue to benefit from economies of scale in the cloud, we will not only continue to grow operating income, but we will also expand the operating margin percentages.”

Net profit and EPS growth was less impressive (YoY) than Operating Profit growth as ORCL had a much higher tax rate this year.

“Had we had the same tax rate last year as this year, net income would have grown 14% and EPS would have been 11% higher.”

The Q4 quarter also marked the end of the financial year. Thus, they presented at the full fiscal year numbers as well.

“For the full fiscal year, Total Cloud services and license support revenue, which is entirely subscription based and accounts for nearly 75% of total revenue, was $39.4 bn up11%.”

IaaS and Cloud Infrastructure revenue was up 50% to $6.8 bn year.

The RPO is now $98bn up 44%.

“Approximately 39% of total RPO is expected to be recognized as revenue over the next 12 months and this reflects the growing trend of customers wanting larger contracts as they see firsthand how Oracle Cloud Services are benefiting their businesses”

They are capacity constrained and working to increase capacity as fast as they can.

“We are working as quickly as we can to get cloud capacity built out given the enormity of our backlog and pipeline”.

“We have 76 customer facing cloud regions live with 47 public cloud regions around the world and another 19 being built.”

“We have 11 databases at Azure sites live and more locations with Microsoft coming online soon. And we will have 12 Oracle database at Google Cloud sites live this year.”

“We also have 13 dedicated regions live and 15 more planned. We have several national security regions and EU sovereign regions live with increasing demand for more of each.”

So, there is lot of capacity waiting to come on stream.

FY 2025 Guidance

The following are some excerpts from the guidance the company gave:

“I expect continued strong cloud demand to push Oracle sales and RPO even higher and result in double digit revenue growth this fiscal year.”

“I expect fiscal year 2025 Cloud Infrastructure Services to grow faster than the 50% we reported this year.

“Beyond this fiscal year, I remain firmly committed to our fiscal year 2026 financial goals for revenue, operating margins and EPS growth.”

“However, given our strong bookings results, I believe some of these goals might prove to be too conservative given our momentum.”

“So, who are the companies choosing to use Oracle Cloud Services and Oracle Datacentres?”

Well, here are a few names NVIDIA, Microsoft, Google, xAI, OpenAI, Coherent and dozens More. the world's largest cloud companies and the world's most successful and accomplished AI companies. “

Why are they working with Oracle?

Because Oracle's Gen 2 cloud infrastructure is different.

“OCI's RDMA network moves data much faster. And when you charge by the minute, faster also means less expensive.”

“OCI trains LLMs several times faster and at a fraction of the cost of other clouds.”

“OCI's critical cloud software, the operating system and the database are fully autonomous. At OCI, human beings do not run the operating system or the database. Autonomous software robots do. No one else has this level of autonomy in the cloud. Eliminating human labour eliminates human error. Almost all cloud security breaches begin with human error. Eliminating the possibility of human error is the only way to make certain your cloud data is not stolen.”

“These customers have done a lot of the analysis and the engineering in advance and have tested us or competed us against our competitors and have chosen us very already understanding how we work and they're just waiting for us to give them more capacity.”

The believe they can let customers start with very small datacentres and scale up to the largest possible size.

“We've talked for a while about our ability to build very small datacentres, one you could put in a ship or a submarine or a full Oracle cloud… So virtually any one of our customers could choose to have the full Oracle Cloud in their datacentre with every service, every service in the cloud. And they could scale that up quite extraordinarily large.”

“We're also building the largest datacentres in the world. We're now bringing 200-Megawatt data centres online. And some of the datacentres we have that we're planning are actually even bigger. There are some are getting very close to, dare I say it, a gigawatt, which is a pretty good sized city.”.

The datacentres we're building include the power plants and the transmission of the power directly into the datacentre and liquid cooling. And because these modern data centres are moving from air cooled to liquid cooled and you have to engineer them from scratch.”

They also comment on rationale for the connected cloud arrangements with Microsoft Azure and Google.

“We think we should be interconnected to everybody. And that's what we're attempting to do within our multi cloud strategy. We'll get rid of these fees for moving data from cloud to cloud, and all the clouds will be interconnected, and customers can pick their favourite service from their favourite cloud and mix and match whatever they want to use and do it easily and seamlessly.”

They believe their strength is scalability, flexibility and security

“We had the advantage of seeing what all the other guys did, and we took a different road. It took us a bit longer, but we think we're better off in terms of security. We're better off in terms of scalability. By the way, that means the ability to go down in size and up in size. It allows us to get to every corner of the globe and provide a level of privacy, for your data that other cloud providers cannot provide.”

This has appeal to countries who want to create Sovereign AI , large scale datacentres on their own soil.

“And for most governments, they don't want their data in the public cloud out and about. They want to have it sovereign to their country. And so no compromises, no compromises on the services and no compromises on security.”

Automation helps scalability and data security

“Our cloud was designed not for hundreds of regions, but for 1,000 or possibly even tens of thousands of datacentres and regions. That's why we had to do it, put in a high degree of automation. There is no way we can run these we could run these datacentres manually.”

“There are too many of them, and we're building them too fast. We couldn't hire people fast enough and train people fast enough. And the risk of them making a mistake, an error is the risk. They start exposing our customers' data. So, they are highly automated.”

People talk loosely about the huge computer capacity requited to train Large Language Models (LLMs). Oracle pointed out that these models are increasingly being trained on images not just text o it is not quite correct to call them Language models

“They're neural networks, and they're trained not just with language, but masses of images as well. For example, Oracle is very involved with taking biopsy slides and using microscopes to read biopsy slides, recording those images, and then using AI to diagnose cancer from these biopsies.”

“Tesla is very close to getting full service driving authorized in China. In order to train a car to do full self-driving, you train it on vast amounts of images, because the car has to look at these images and then decide what it's going to do next... So everyone's going to be training their models on imaging. That's a huge amount of additional data. It's a huge amount of additional training. And we're right in the middle of it.”

The rationale for the Azure tie up is that Customers will be able to use Oracle databases on a pay as you go basis on the Azure Cloud.

“The database at Azure, those centres are just going live now. So even though we are selling quite a bit of ARR there, these are small and growing very, very fast. The revenue in Q4 of let's say Azure was very small. Q1 will be 10 times as much, Q2 will be potentially 30 times as much. So, it is extremely incremental to our current run rate.”

The Revenue growth coming from their new AI contracts will also be incremental to their current run rate.

“These contracts that we are signing that we've signed at the end of Q3 and that are signed at the end of Q4 are so much larger in size that they will be incremental to everything you saw this past year.”

Summary

Oracle shares are trading 12.8% higher after the quarterly results.

The company seems to be offering a good proposition to enterprises and countries who wish to move their core enterprise software and GenAI workloads to the ground.

It is working with Azure and Google to offer a hybrid cloud which will have some appeal to customers who are wary of cloud Vendor lock-in.

Oracle proposition does seem to have appeal to customers who are cost sensitive and seeking flexibility (e.g. start-ups) as well as customer concerns about data security.

Valuation

The company is currently trading at a two year forward P/E ratio of ~22 times.

However, analysts may raise the EPS estimates significantly after these results.

The share price is likely to move higher as the company grows over the next few years and may give a satisfactory return over the next few years.

There is some concern about the current high level of debt and low interest expense coverage ratio. However, the latter will improve as the operating cash flow will rise over the next few years.

Conclusion

Our conclusion in March was as follows:

“We think there is a good case for allocating 1-2% of the portfolio to Oracle. We will track it with a view to increasing this to 3% to 4% over time.”

We did allocate 2% of the portfolio to Oracle at the time. They had traded sideways to a little lower since then underperforming the market.

Given the strong earnings number yesterday. We increased our allocation to 3% today. We will track it with a view to increasing this to 4% over time.