Oracle Inc ( ORCL)

Giant debt raising done. Giant equity raising ahead?

In our recent notes, including one written yesterday, we noted that Oracle needs to raise money. In our note on September 11th (found here.) we observed the following

“However, as we noted in our earlier note Oracle carries a lot of debt about $82bn which rises to $96bn if long-term leases are included. Oracle’s ability to service its debt has fallen sharply if we take capex out of the question. Oracle is unlikely to be able to borrow from the debt markets. Oracle’s long-term debt is rated BBB by S&P Global and Fitch, and Baa2 by Moody’s as of September 2025. S&P’s outlook is currently negative due to high capital expenditures and rising leverage. Moody’s also revised Oracle’s outlook to negative mid-2025 amid aggressive investment for cloud and AI expansion.

The debt outlook is negative and Oracle risks being downgraded to junk if there is two-notch downgrade. A trigger could perhaps be if leverage exceeds 4.0x debt/EBITDA for a prolonged period. Our data indicates this number is at 3.9X. Oracle has little scope to increase debt.”

Yesterday we noted the following

“Oracle needs money to execute the new ramp up in business coming from OpenAI and others. However, Oracle is highly indebted and unable to take on much more debt. There were also some questions about OpenAI’s ability to pay Oracle.”

Well, we underestimated Oracle needs for cash and their determination to get it. They launched a US$ 15bn in seven tranches including a long 40-year tranche yesterday. The issue was amongst the largest in recent memory and was increased to nearly $26bn (!) because of the strong demand. This is an impressive, opportunistic fund raising. This reflects the current high risk appetite in the debt markets.

Tech companies have raised about $157 bn so far this year in the US public bond markets alone, up some 70% from what they issued in the same period last year. The appetite for investment-grade bonds is so strong that spreads have been pushed to near their lowest in 27 years, with investors seeming willing to accept the lowest yield premium for taking the credit risk.

Oracle already had total long-term debt of $85bn and total long-term liabilities of $114bn.

With this fund raising, those numbers will go to $111bn and $140bn respectively.

We stated in our earlier note that Oracle’s debt outlook is negative with the main Credit Rating agencies. There is a risk there will be a one notch downgrade after this large fund raising.

A further large debt raising would risk an additional downgrade which would mean Oracle debt would no longer be Investment Grade, and therefore will be classified as Junk or the less pejorative high yield. We assume Oracle management would not be willing to risk such an outcome.

A trigger for a descent into Junk bond territory could be if leverage exceeds 4.0x net debt/EBITDA for a prolonged period.

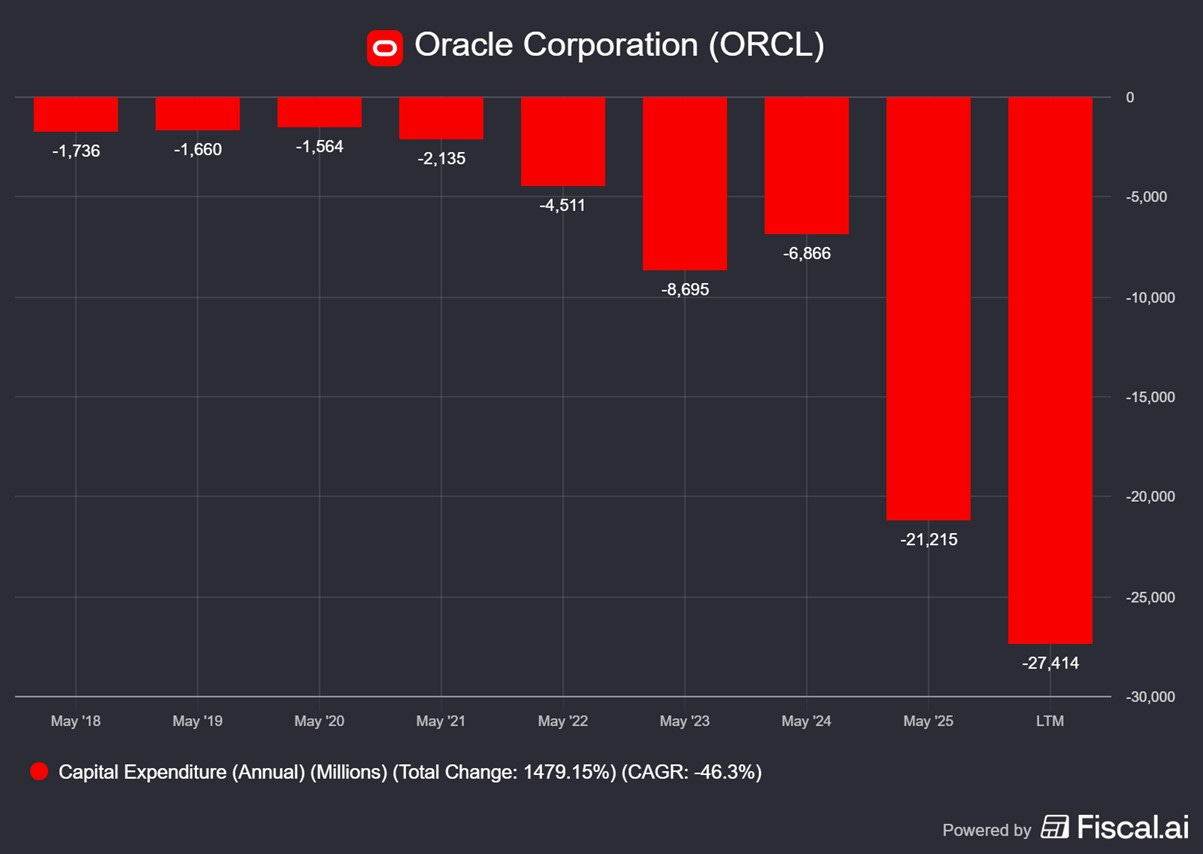

Oracle has indicated that its Capex plan on the next twelve months is $35bn. How can this be funded?

As the chart above shows, the total cash and cash equivalents are about $11bn. With the $26bn raised today the company has about $37bn which will be enough to cover about 12 months of Capex.

The company has an operating cash flow of $21bn. As the following year approaches, that will be available for some of the likely capex in the following year ending May 2027 but there is no question money will be tight and the debt market will be closed. What about an equity raise?

We also looked at Oracle’s past share buybacks. Around 2000, the share count peaked at around 6bn shares (adjusted for splits since). They steadily repurchased them over the next 15 years, and then between 2018 and 2022 they aggressively bought back almost 40% of the outstanding shares.

This was done between when the share price is in the low $40s and about $90.

After that, they did minimal buybacks — not enough to offset Stock based compensation-so the total number of shares outstanding increased slightly (see above)

Capex increased sharply(see below) so there was no money for buybacks.

Today they need money for even more capex to finance their cloud building to meet demand for orders received from OpenAI.

With the shares at price at $290, they could perhaps do a huge rights issue at $250 per share. That would be quite a trade-buy a 40% of the shares at between $50 and $90 and issue them all back again at $250!

Perhaps the market is afraid of this and this is why the stock is down nearly 6% today!