Paychex (PAYX)

Outsourced Human Capital Management (HCM) to SMBs,

Paychex (PAYX)

if you run a small or mid-size company employing anywhere from a few people to a few thousand in the US, a lot of time and effort will be required for managing the human capital. You need to ensure people are paid correctly and all benefits and allowances etc are taken into consideration. Rules and regulations related to employment have increased greatly in volume and complexity. Keeping compliant with a myriad of requirements is a full-time job. Managers must try and do this at the same time as the main task of running the business.

There are integrated human capital management (HCM) companies to whom some or all these tasks can be outsourced.

Paychex, Inc (PAYX) is an HCM company which provides solutions for

payroll,

human resource (HR),

retirement and

insurance services

PAYX’s clients are small- to medium-sized businesses in the US. Clients who often do not have the resources or expertise, to adapt to the constantly evolving environment.

Effective HCM is vital to any organisation and requires both resources and expertise. Organisations face continuous evolution in employer-employee relations including: an increasing number and complexity of federal, state, and local regulations; changing workforce dynamics; and challenges attracting and retaining talent.

The workplace is rapidly changing as employees increasingly

become mobile,

work remotely, and

expect a user experience like consumer-oriented applications.

PAYX offers integrated HCM solutions from hire to retire for businesses and their employees. They customize the offering to match the client's business.

The key features are:

A comprehensive cloud-based platform optimized to meet the HR and payroll needs of small- and medium-sized organisations.

Expertise in HR and payroll with their technology backed by approximately 250 compliance experts and over 650 HR business professionals.

Streamlined workforce management that combines technology with flexible, tech-enabled support options.

Modern, mobile, and intuitive user experience with self-service capabilities.

Scalable and customizable platform that allows clients the ability to add services as they grow;

Software as a service, or “SaaS”, delivery model that reduces total cost of ownership for our clients; and

Advanced data analytics and artificial intelligence (“AI”) capabilities powered by large data sets.

Over 50% of PAYX’s revenues are from solutions other than payroll processing.

These companies are sometimes known as PEOs or Professional Employer Organisations. PEOs offer the full range of HCM services, but they are a co-employer for tax and insurance purposes. They handle various HR functions, as if they were the employer. This allows businesses to focus on their core operations.

PAYX is the second largest PEO. The largest player is Automatic Data Processing (ADP) which currently has a market cap of $125bn compared with $53bn for PAYX.

PAYX has recently consolidated its position by taking over the much smaller Paycor.

The payroll-related ancillary services and human resource service (HRS) offerings often leverage the information gathered in the base payroll processing service, allowing PEOs to provide outsourcing services covering the HCM spectrum. The PAYX platform unites HR, payroll, time and attendance, and benefits processes to maximize efficiency and savings.

Clients can choose to have PAYX personnel do all the work, or they can use software such as Paychex Flex to do some of all of it themselves.

After the retirement stage, PAYX provides retirement benefit administration services. PAYX is also among the top 20 largest insurance brokers in the U.S.

Paychex offers two Saas solutions called Paychex Flex® [1]and SurePayroll® respectively. Both allow users to process payroll when they want, how they want, and on any type of device (desktop, tablet, and mobile phone).

The medium-sized clients generally have more complex needs. They can opt for an integrated suite of HCM solutions, which allows them to choose the services and software that will meet the needs of their businesses.

The company emphasises the flexibility and scalability of their solutions. Their service agreements and arrangements with clients do not have specified contract periods and may be terminated by either party with 30-days’ notice of termination.

Despite this, client retention rates are about 80% to 85%. PAYX has 800,000 Payroll Clients and 2.5mn HR Outsourcing client worksite employees.

The company’s go-to-market strategy involves cultivating long-standing relationships with channel partners such as brokers, accountants and banks,

Financial summary of the company in Charts

This is not the type of high growth industry we normally look at. It is a relatively mature industry. Most companies that are likely to be potential clients already have an HCM services provider.

Revenue growth for PAYX will be driven by factors such as the nominal economic growth and the rate of the formation of new enterprises. Underlying revenues growth for PAYX is likely to be less than 10% per annum.

However, this is still of potential interest as it is consistently profitable and a reliable generator of cash flow. Free Cash flow has been e latter is relatively high as the company has an asset-light operating model.

Total Revenue

Total Revenue has grown at a CAGR of 7.3% over the last decade to about $5.57bn in FY25.

Management solutions Revenue (73% of total revenue) grew at a CAGR of 5.3% over the last decade

PEO and Insurance Solutions (24% of total revenue revenue) grew 15.6% CAGR over the last decade. The latter has been an important source of growth.

Operating Income and Net Income grew at a CAGR of 8.2% and 9.1% respectively over the last decade. This suggests the business model has a low degree of operating leverage as ten-year CAGR profit growth was only slightly higher than equivalent period revenue growth.

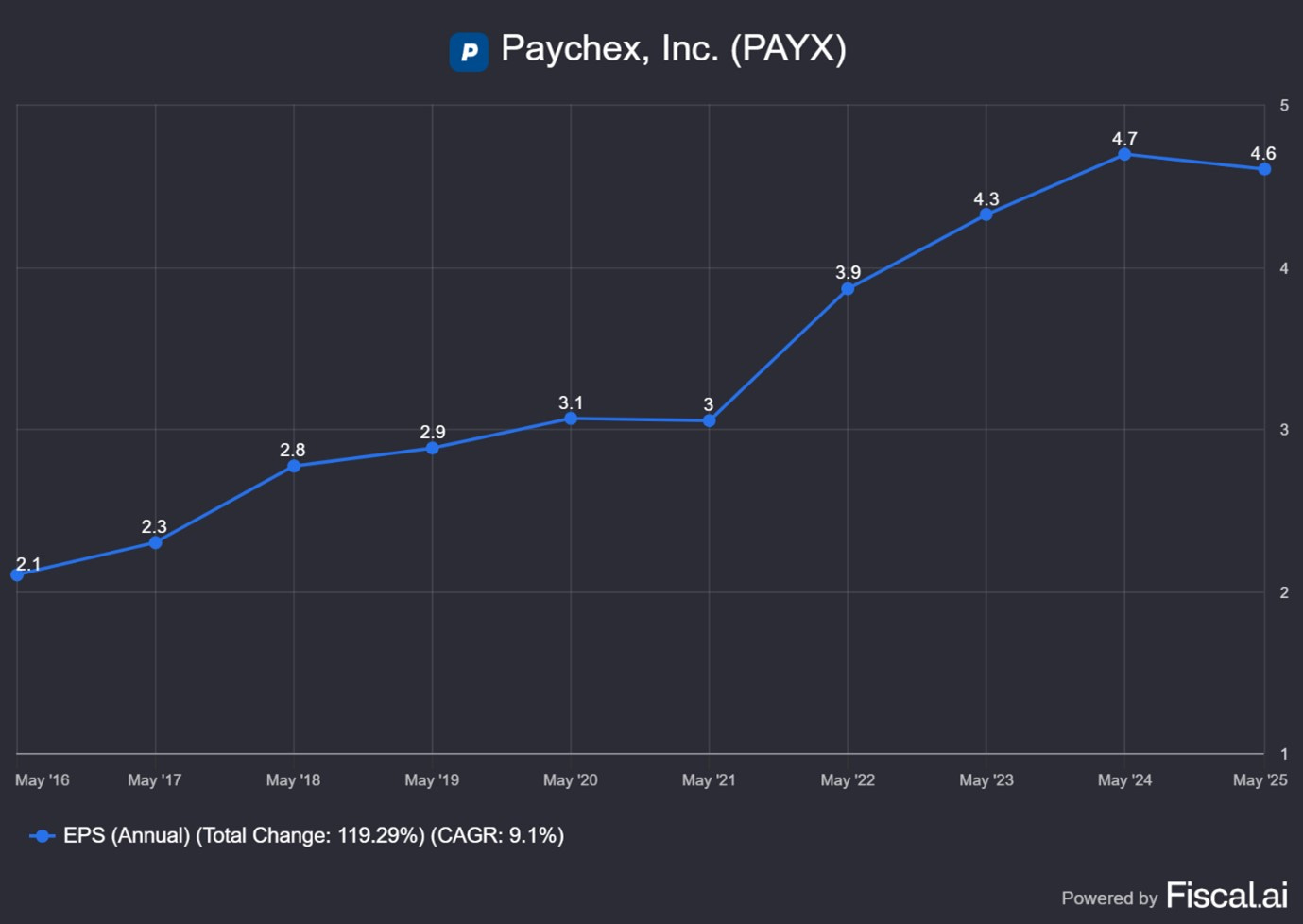

Earnings per Share has increased at a CAGR of 9.1% per annum in the last decade.

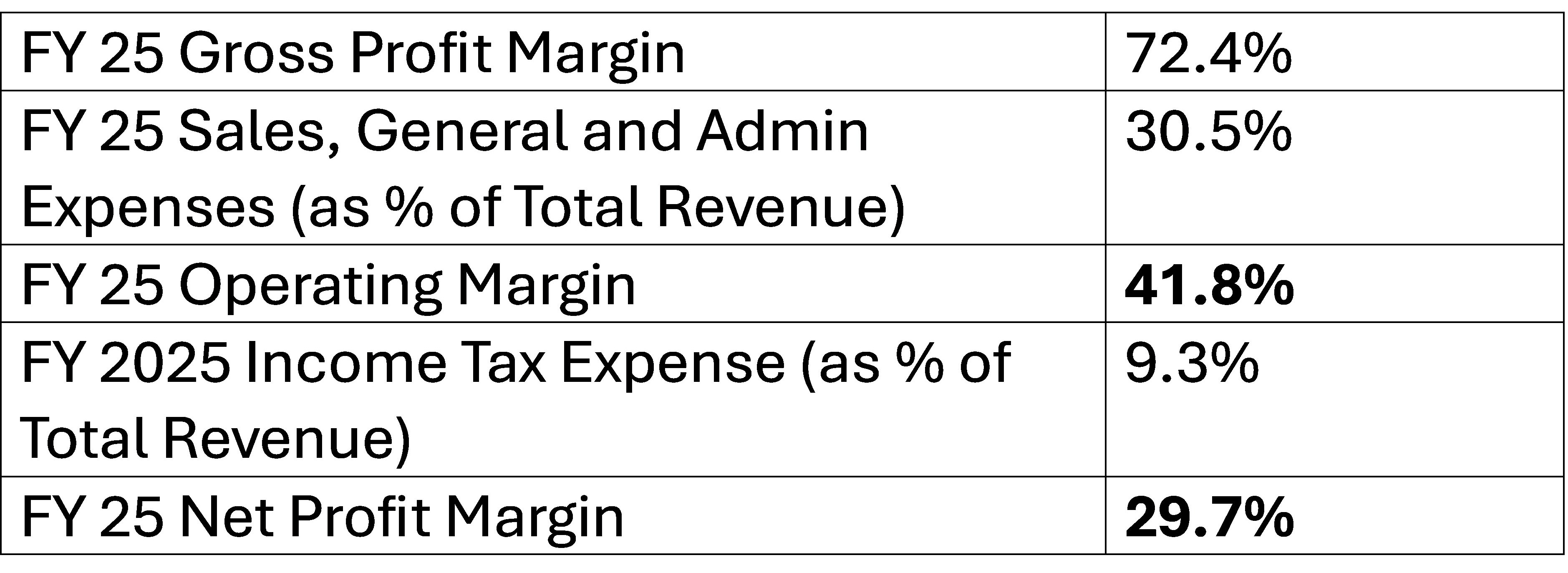

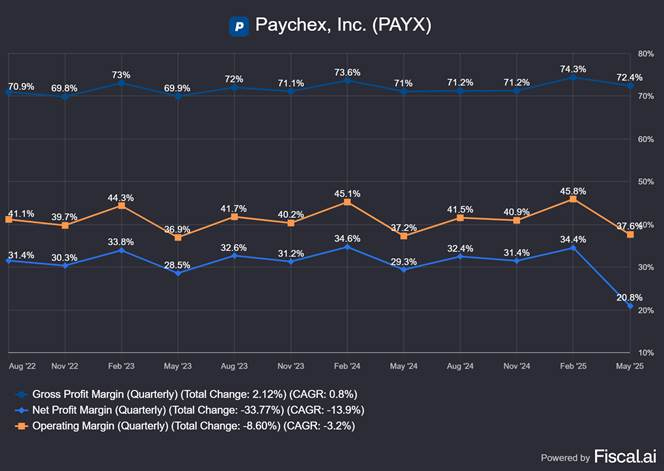

There has been a slight increase in both Operating and Net Profit Margin in the last decade. These stand at 41.8% and 29.7% respectively.

Operating Cash and Free Cash Flow have grown consistently at a CAGR of about 7.5% over the past decade.

The company has little capital expenditure and has an asset light model.

Capital Intensity (defined as Net Plant and Equipment as a percentage of Total Assets) has declined and is currently just 4%. Capital Scale (defined as Capex divided by Total Revenue) is also a low 4%.

Profitability

We looked at both ROE and ROIC to assess PAYX’s profitability.

Return on Equity (ROE) and Return on Invested Capital (ROIC) are both key measures of a company's profitability, but they focus on different aspects of capital and offer distinct insights.

ROE= Net Profit /Equity

ROIC = Net Operating Profit at Tax (NOPAT) / Total Capital Employed.

ROE at about 41% is much higher than ROIC (16.3%).

A significant difference between the two can often be explained by high leverage. High leverage raises the ROE. This is because debt can be used to boost Net Profit but it is not included in the denominator of ROE which is composed of only equity.

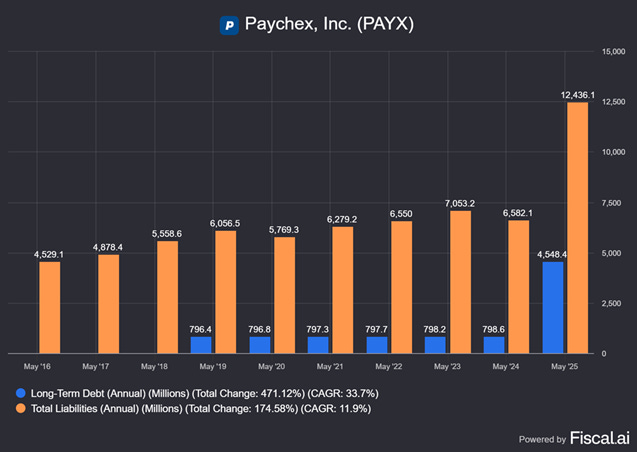

However, this is only a partial explanation as PAYX did not have too much debt until the most recent quarter.

For long-time, long-term debt was only about $700mn

There may well be another source non-equity capital which is deployed in the business and is helping to boost Net Profit and ROE.

One possible answer is” float”. PAYX has a float which arises from short period holding of client funds before they are paid out for payroll and related services.

When clients send money to Paychex for payroll processing, Paychex temporarily holds these funds (the before disbursing them to employees or tax authorities. During this holding period, Paychex invests the float and earns interest income. This interest income increases the company's net income

As Return on Equity (ROE) is calculated as Net Income divided by Shareholders’ Equity. Since the float generates additional interest income without requiring additional equity investment, it increases net income while equity remains unchanged, thereby boosting ROE.

The difference between ROE and ROCE can be explained by a combination of float and leverage.

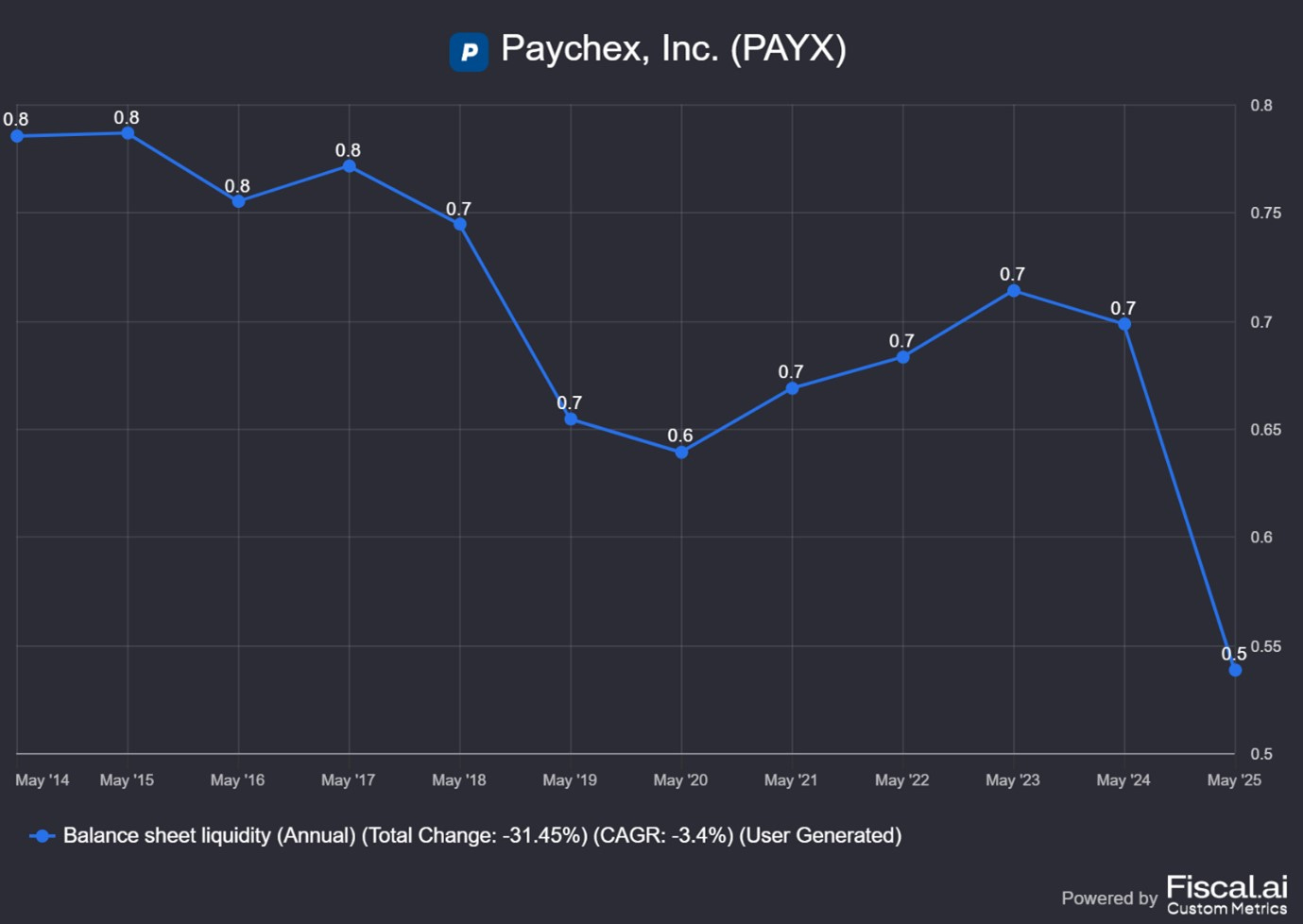

Balance Sheet

Historically the company has had a strong balance sheet

Long-term debt has been low (until Q4 2025) and a small part of total liabilities.

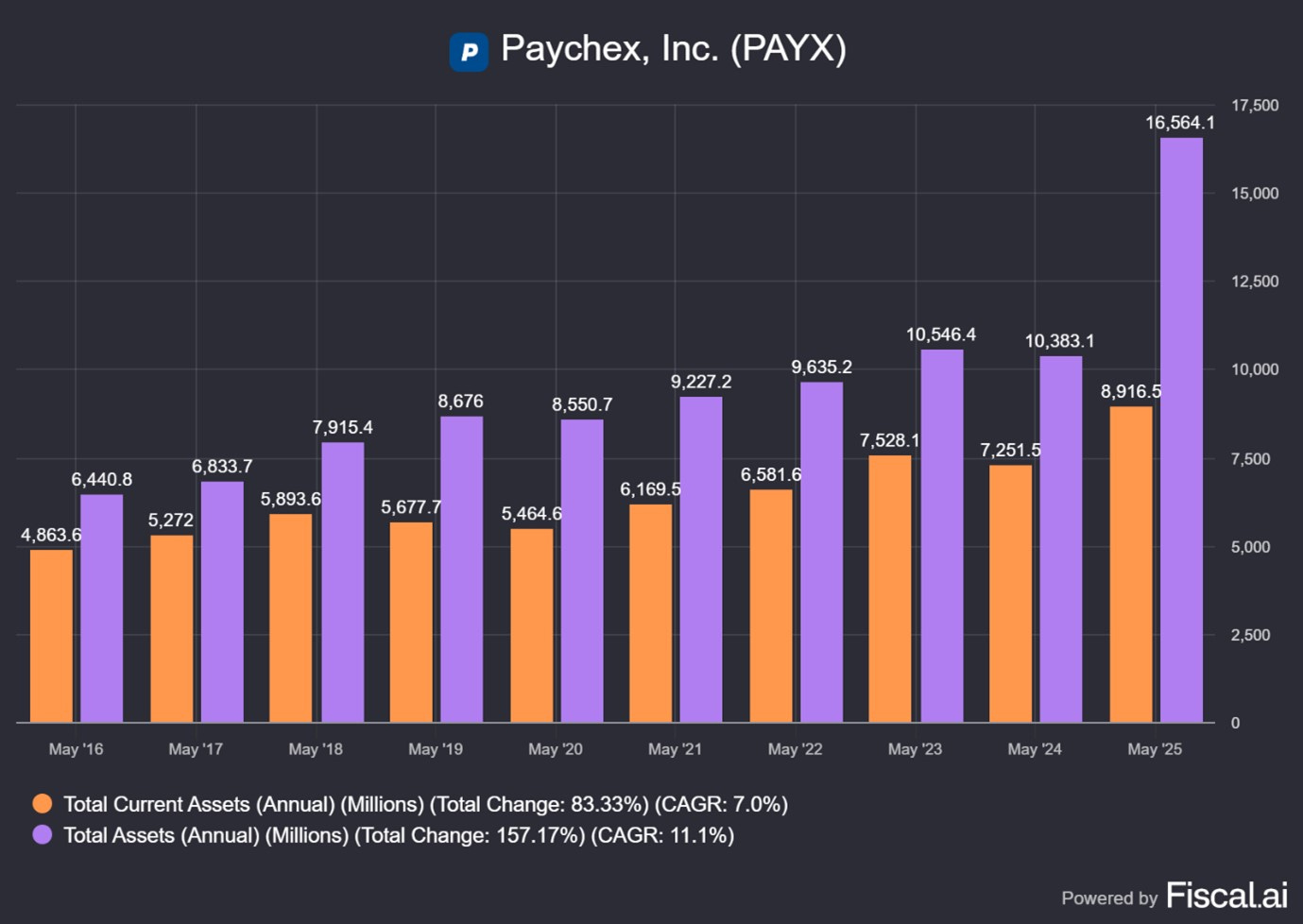

Balance sheet has been liquid historically with current assets accounting for 70% of total assets.

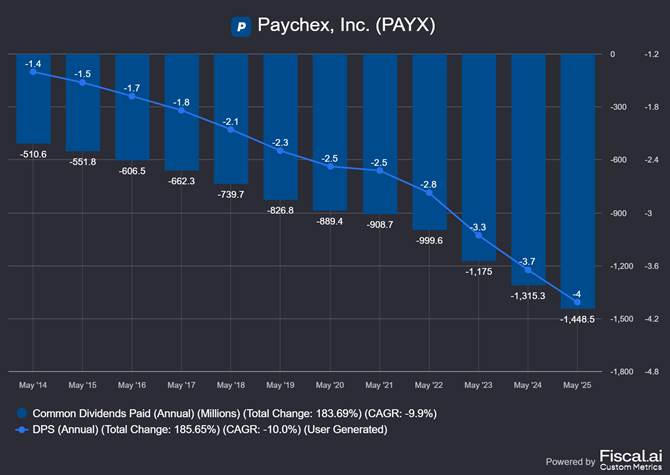

PAYX has been a consistent payer of increasing dividends.

Total dividends paid has risen from $510mn in 2014 to $ 1.44bn in 2025.

The Dividend Per Share has increased from $1.4 to $ 4 over the same period (a CAGR growth of 10%). These are both shown in the chart below. They are illustrated as negative bars as they represent a cash outflow,

Historical Returns from the PAYX stock

In the last 24 years, the PAYX stock has given total return at about 9.8% CAGR.

In the last five years, the PAYX stock has given a total CAGR return of 15.7% CAGR.

This suggests that ROIC rather than the higher ROE is a better indicator of likely shareholder return over the medium to long term

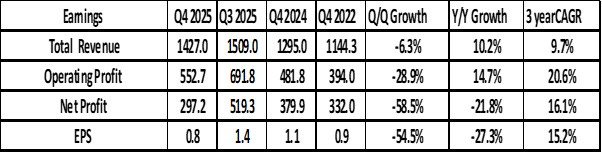

Q4 2025 Results

PAYX saw 10% revenue growth (y/y) in the fourth quarter. Company, reflecting continued execution across the business and the addition of Paycor. Operating Profit grew at 14.6% (y/y)

For FY 2025, they achieved 6% revenue growth and 6% growth in diluted earnings per share.

Management solutions grew 12% (y/y) which was much faster than the growth in PEO and Insurance solutions.

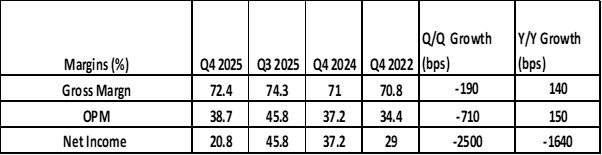

Margins have been stable over long periods. However, there was a notable decline in operating and Net Profit margins in Q4 2025. The decline in margins reflect the Paycor acquisition (see below).

Highlights from the Q4 2025 Earnings Conference Call

Acquisition of Paycor

In May 2025, the company issued $4.1bn of debt and the proceeds were used to acquire Paycor. It was an all-cash acquisition of 100% of Paycor for $22.50 per share, representing approximately $4.1 billion of enterprise value.

This led to a meaningful increase in the long-term debt of the company, from about $800mn to $4.5bn.

Paycor is a much smaller company than PAYX. The management is optimistic about this non-dilutive acquisition for several reasons.

They argue the combined offering will be the most comprehensive HCM portfolio in the industry.

They expect annual cost synergies of more than $80mn in FY 2026 and substantial revenue synergy opportunities over the next several years

They expected the deal to be accretive to adjusted diluted EPS in FY 2026.

According to the management

“The acquisition of Paycor is highly complementary. It will enhance our capabilities up market, broaden our suite of AI driven HR technology capabilities across the platforms and provide new channels for sustained long term growth. Our customers will benefit from an expanded suite of technology and advisory solutions designed to help them address their HR challenges and Paycor's customers will benefit from our broad product set of HR advisory and employee solutions and from the scale and tradition of operational and service excellence that Paychex is well known for in the marketplace.”

“We have made significant progress on the Paycor acquisition, surpassing our expectations and setting a strong foundation for future success. We are raising our cost synergy expectations to approximately $90mn in fiscal year '26.”

Customer Focus

The Paycor Platform will target the larger companies in their customer base

“Paychex Flex will focus on companies with up to 99 employees, Paycor platform will target the upmarket enterprise segment above 100 employees.”

Re-organisation of sales coverage

We also completed a comprehensive territory assessment and reassignment review across the sales teams that aligns to these market segments.

We have expanded and optimized our sales coverage nationwide in the fourth quarter.

We are encouraged by how sales hiring, retention and tenure developments are trending going into the fiscal year.

We continue to believe the biggest opportunity is the cross-sell of Paychex retirement, ASO and PEO solutions into the Paycor base of more than 50,000 clients.

We also believe there are opportunities to take Paycor's capabilities into the Paychex client base in the years ahead.

Working with channel partners

Their go-to-market strategy involves cultivating long-standing relationships with channel partners such as brokers, accountants and banks.

More than half of our new business originates from channel partner referrals.

One of the key channel partners in the US are brokers. These are insurance brokers, PEO brokers, benefits brokers and retirement plan brokers. They often have long- term business relationships with enterprises targeted by PAYX.

Brokers

We introduced the Paychex Partner Plus program to brokers to foster relationships and drive mutual growth.

Together, we now have a broader suite of solutions to offer brokers, which can supplement their offerings to clients.

Over 1,000 brokers are enrolled in the Partner Plus program, and we are hearing positive feedback, which we believe indicates a strong foundation for retaining and expanding this important referral channel.

Accountants

Another key type of channel partners are Accountants who work with enterprises.

We also recently launched Paychex Partner Pro platform, a new portal designed to provide accountants quick access to critical data, reporting and insights for their clients using Paychex Flex.

This innovative platform transforms how CPAs manage their portfolios by providing a centralized hub for accessing client payrolls and HR data, resolving issues and identifying missing information. This is empowering them to really operate with greater efficiency and proactively serve their clients.

Recession Risk

The hard data continues to indicate that small businesses remain fundamentally healthy despite the headlines.

Our small business employment watch revealed stable employment levels with moderation in hourly wage inflation in the recent months. Our data does not currently show any signs of recession.

However, it may be the calm before the storm.

We also see our interactions in the market that the uncertainty is prompting businesses to exercise caution when making decisions and being cautious about how much they are spending on products and services

We have also seen an increase in bankruptcies and financial distress in the micro end of the market and in our client base in the fourth quarter.

Many businesses, I think, on the edge of failure may have decided not to fight that new headwinds they see in front of them. We also saw losses due to increases in business combinations and mergers increase more than typical.

We continue to see moderate growth in small business hiring. …we probably saw slower growth than we would have expected in the mid-market, but it wasn't astronomical. It wasn't recessionary and we've really not seen any signs of recession. There's a high degree of uncertainty, and I think a lot of people are frozen right now.

A recession will hit small business hard, and this will be a significant headwind for PAYX.

Paycor acquisition was needed to boost growth.

The numbers show growth would have been challenging without the contribution of Paycor.

Excluding Paycor, total revenue increased 3%.

Excluding Paycor, Management Solutions increased 3% in the quarter.

PEO and Insurance Solutions revenue increased 4% to $340 million for the quarter, driven primarily by solid growth in the number of average PEO worksite employees.

·Interest on funds held for clients increased 18% to $45 million for the quarter, primarily driven by the inclusion of Paycor balances.

Excluding Paycor, interest on funds held for clients increased 3%.

Adjusted operating margins reduced by Paycor acquisition.

Operating income margins for the quarter were 30.2%. Excluding Paycor, adjusted operating income margins expanded by approximately 110 basis points.

Paycor expected to boost FY 26 growth.

Total revenue for fiscal '26 is expected to grow in the range of 16.5% to 18.5%.

We expect the recent Paycor acquisition to contribute approximately 12 to 13 points of that growth.

Paycor will boost revenue initially, but the combined entity will face growth challenges. They are pinning hopes on revenue synergies due to cross selling etc.

We expect revenue synergies to build over the next several years. And in fiscal '26, we expect revenue synergies to contribute 30 to 50 basis points of the growth we are forecasting.

They expect some organic growth and some price increases.

We're going to continue to focus on our growth formula as a company, which includes 1% to 3% organic client growth across the combined businesses. We're going to continue to focus on driving product penetration.

And we're going to continue to exercise the pricing strength that we have, the value, the ability for us to pass value on to our customers as well.

We're still assuming that Paychex is going to -- or Paycor is going to be a strong double-digit grower business. I mean certainly, there's an element of conservatism, I would say, overall, in the guide.

Capital Allocation

They are going to continue to invest in the business and pay out growing dividends.

We feel like we're well positioned to continue to maintain our dividend policy. Certainly, our #1 focus is investing into the business. We're going to continue to do that. And to the extent that we have excess cash, our primary way to return that to shareholders is through dividend versus share buybacks.

Debt has increased because of the transaction. They will de-leverage gradually as maturing debt will be repaid and not re-financed.

if you look at the balance sheet, you'll see there is a current portion of long-term debt. We do have some of our long-term debt coming due within the next 12 months, and we would look to pay that down. So, the combination of those 2 things over the next 12 months will deleverage the balance sheet.

The cost of integrating Paycor and the required restructuring of the company has already occurred.

A lot of the restructuring stuff, to be honest with you, is behind us. We got a lot of that behind us, a lot of the onetime costs related to the transaction.. When you look at kind of the adjustments going forward, they're mostly noncash related. You have the amortization of the intangibles, and you have some of the rollover equity.

On Macro uncertainty

There's been a lot of things hit the market that drive uncertainty in the fourth quarter. I think we all have been living through that, including global conflicts.

Our assumptions is that we're going to have a more consistent macro environment that we saw in the first 3 quarters, which was, moderate growth in small businesses and a little bit more stable, what I would say environment for businesses to be able to make decisions about future investments in capital

The value proposition that the PEO brings to the marketplace has never been in more need. There is a health inflation issue out there, and we have solutions to solve that problem. And when you look at it on the aggregate basis, we increased the number of people participating in our PEO health plans across the country and continue to see strong demand for the product and service

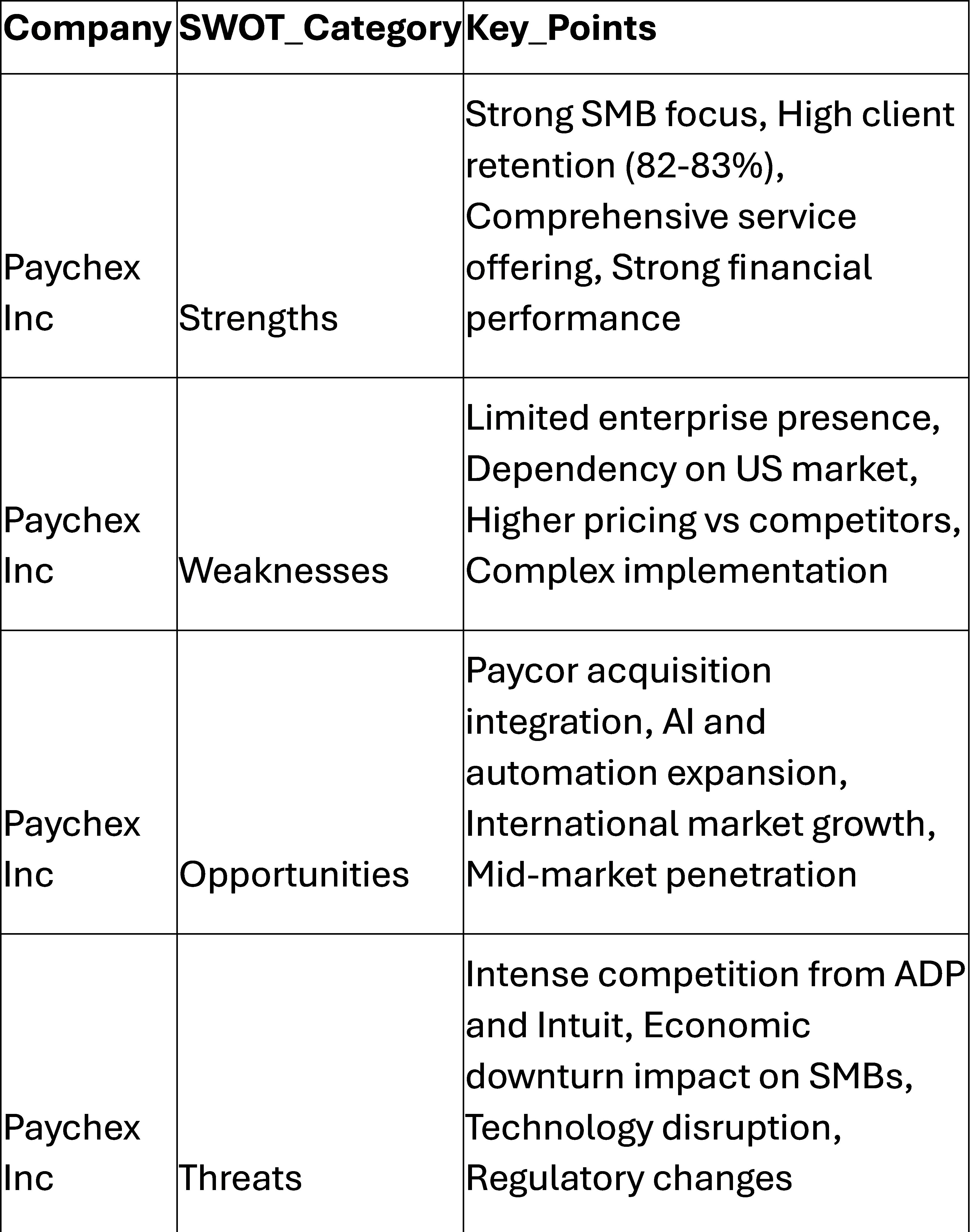

We asked an AI LLM to generate a SWOT analysis for PAYX. This was the output.

Summary

Paychex is a leading PEO and Human capital Management (HCM) company.

It offers services to small and mid-sized companies relating to HCM including Payroll, HR, insurance and retirement benefit services.

This is a mature industry, so it is difficult to generate sales growth above single digit percentage growth rates.

The industry is consolidating as reflected in Paychex takeover of Paycor.

It has been a consistently profitable and cash generative company over many years

Valuation

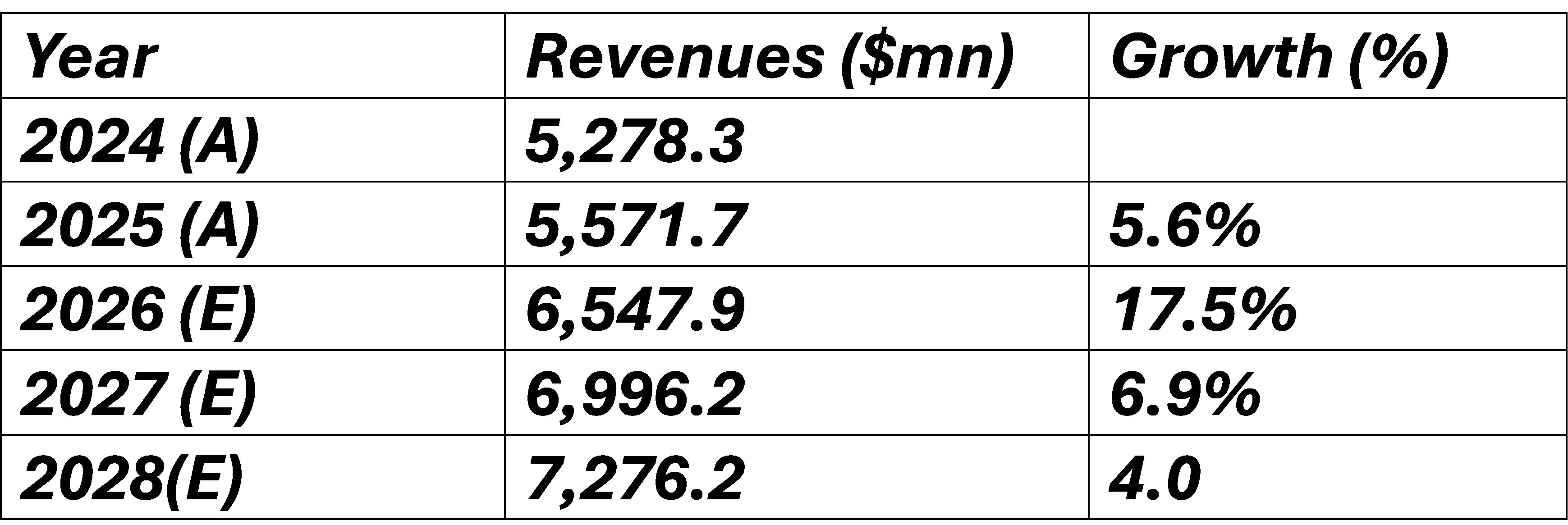

The consensus analysts’ forecasts for revenues are as follows:

Source: fiscal.ai

FY 2026 Revenues will grow by 17.5% reflecting the full year of growth post the Paycor acquisition. However, analysts expect revenue growth to slow in FY 2027 and FY 2028.

The analysts’ forecasts for EBIT are as follows:

Source: fiscal.ai

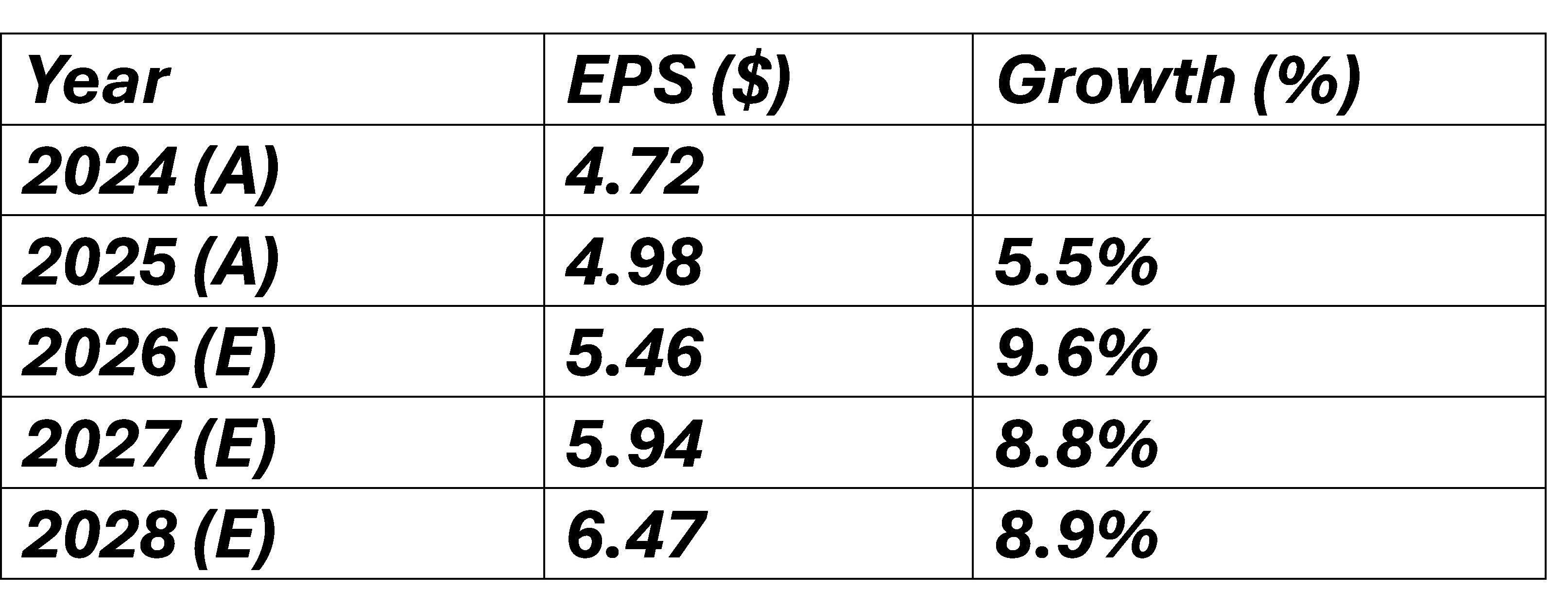

The analysts are assuming EBIT margins will plateau at recent levels. The analysts’ forecasts for fully diluted EPS are as follows:

Source: fiscal.ai

Source: fiscal.ai

Currently, the PAYX share price is $147 per share and the market capitalisation of $52bn. This means it is currently on a two-year forward Price /Earnings Ratio of 23.9X and Price to Free Cash Flow Ratio of 24.1X.

This implies a two-year forward earnings yield of 4.2% and two-year forward free cash flow yield of 4.1%.

On the face of it this suggests that PAYX stock is fairly valued given the fundamentals of the company noted above and the conservative assumption used.

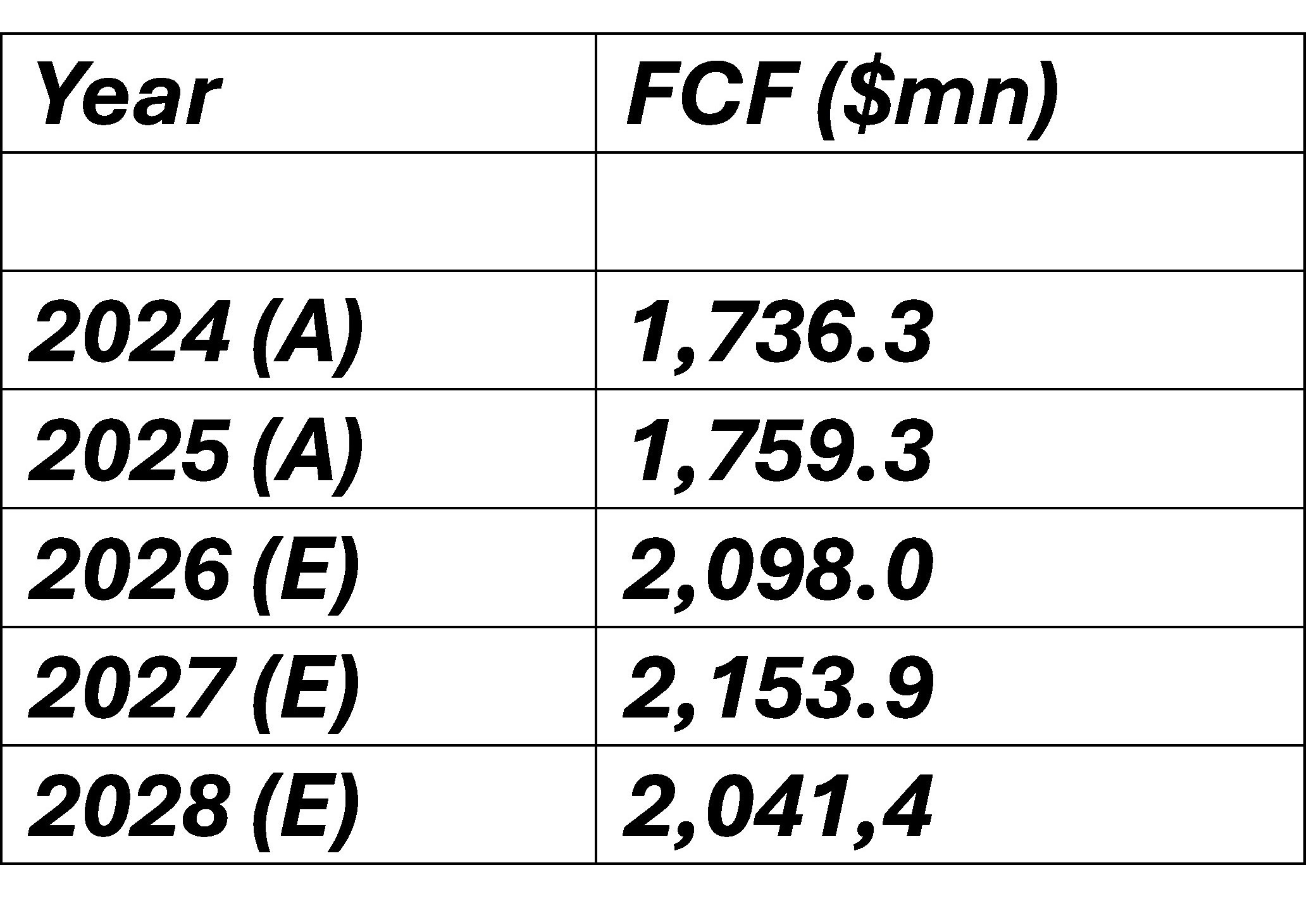

We conducted a Discounted Cash Flow (DCF) Calculation to double check this view. Using analysts’ consensus figures and some additional assumptions, we sought to value the stock.

The risk-free rate is currently of 4.0% and the Market Risk premium of 5.0%. The Stock Beta is 0.9. The Weighted Average Cost of Capital (WACC) is 7.9%.

We use the analysts’ consensus’ numbers noted above.

In addition, we assume total revenue will increase by 8% in FY 2029 which is the terminal year.

We also assume that FY 2029 EBIT margin will be 42.8%.

In addition, we assumed that at end-2029, the terminal exit EV/FCF multiple is 35X. The current EV/FCF multiple is 33X.

With these assumptions, we calculated a theoretical PAYX stock value of $136.3 – the current price of $142 is 7% higher than the estimated fair value.

If we increase the terminal exit EV/FCF multiple to 37X, we get a theoretical value equal to the current stock price. This suggests the stock is slightly overvalued currently.

Conclusion

Our best guess is that the stock should earn a minimum average return of 7% to 9% CAGR over the next five to seven years. This is not high enough.

At $147, the valuation is a little too rich, and we will not re-establish a position at this time. We will look at the stock if the price falls below $125.

[1] Paychex Flex features more than 25 HR self-service options and helps organizations manage recruiting and hiring, onboarding, performance management, and benefits such as a 401(k) plan and group health insurance. -an integral part of flexible job markets.

Solid list! Which mistake do you think hurts new investors most — chasing trends, averaging down too early, or focusing only on value/growth?