Reliance Industries Limited (RIL)

India largest conglomerate

Reliance Industries Limited (RIL) stands as one of India's largest and most diversified conglomerates, with significant presence across petrochemicals, retail, telecommunications, and digital services. RIL has a current market of about US$ 200bn. It is listed in India but also trades in London as a Global Depositary Receipt (GDR). One GDR is equal to four local rupee-denominated shares.

The original company was founded in 1966 by Dhirubhai Ambani as a small textile trading company. It has transformed into a global powerhouse through strategic expansion, significant backward integration and large-scale diversification.

Dhirubhai Ambani had migrated to Aden in the Middle East as a young man and worked as a Petrol Pump Attendant for a BP Service station. He established Reliance Commercial Corporation in 1966 as a small textile trading business in Mumbai. Ambani began by exporting spices and textiles to Yemen. His strategic insight led to the company's first significant expansion in 1966 when he set up a textile manufacturing unit in Naroda, in Ahmedabad, Gujarat, marking Reliance's transition from trading to manufacturing.

Initially the Naroda plant was making synthetic fabrics. Synthetic i.e. manufactured textile materials are made mostly from non-renewable coal and oil, which are converted into monomers and then polymerized. They don't break down rapidly and may be made in any length (continuous filament) and thickness for any purpose. Manmade fibres are used to create synthetic textile fabrics. Clothes made from synthetic textiles are perhaps less comfortable than cotton but crucially in the Indian context they were much more affordable and durable for the emerging middle class and the masses. In 1975, the company expanded its business into from unbranded fabric into branded textiles, with "Vimal" as the main brand. As part of this forward integration, Vimal branded stores were established to retail the textiles.

Dhirubhai Ambani (seated) with his sons Mukesh Ambani (left) and Anil Ambani.

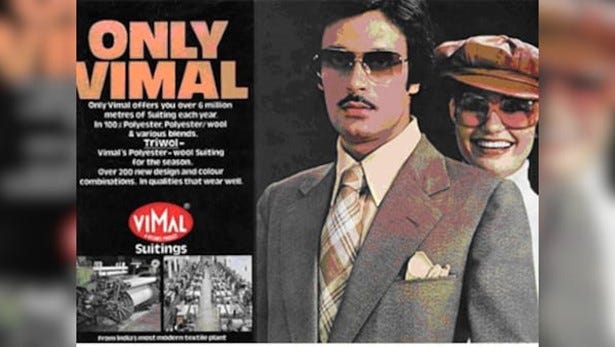

1980s advertisement for Vimal “Suitings.”

Vimal “Suitings and Shirtings”. Fabric materials which your local tailor could turn into a shirt and suit cheaply.

In 1977, Reliance Industries went public with an IPO that was a significant milestone in the Indian capital markets. The issue was oversubscribed seven times and 58,000 investors applied for the shares. Many of the early AGMs were held in sports stadiums. It introduced many first-time retail investors to the stock market.

The main raw material synthetic fabric require is Polyester Filament Yarn (PFY). Large-scale industrial production of PFY made from Polyethylene Terephthalate (PET). So Polyester Fibre is also called PET Fibre. Going further back in the chain, PET is formed from two intermediates derived from crude oil or natural gas.

Polyester Filament Yarn (PFY) Reels

In the 1960s and 1970s, PFY was not manufactured in India and Reliance and others had to import it. Later some scale manufacturing was done by ICI India and IOCL.

In 1980, RIL set up a PFY plant with financial and technical collaboration with EI du Pont de Nemours & Co. of the USA. By 1992, the PFY capacity was 145,000 tonnes per annum.

RIL was now a vertically integrated textile manufacturer, controlling processes from PFY to textile retailing. The company's innovative financial strategies, including the introduction of convertible debentures, created new financial markets in India.

The next logical step was to integrate backwards into Petrochemicals (to manufacture PET). In the 1990s, RIL set up their third manufacturing plant at Hazira. It was a Naphtha cracker. Naphtha is a flammable liquid hydrocarbon mixture made from oil, gas condensates and petroleum distillates. Naphtha can be used to make PET and is a feeder to RIL fibre intermediates, plastics and polyester plants. Reliance now had the synthetic textile value chain from Naphtha to PET, PYF and PSF to fabrics and all the way to the “Vimal” retail shops selling textiles.

The next backward integration step was going to go into a new industry, Oil Refining and Oil and Gas exploration. Construction of what later became the world's largest refining complex at Jamnagar, started in 1999. Jamnagar is strategically located on India’s west coast facing the Persian Gulf.

RIL’s Jamnagar Refinery

What does an oil refinery do? An oil refinery is an industrial process plant where Crude Oil is refined into products such as gasoline (petrol), diesel, fuel oils, heating oil, kerosene, LPG and the aforementioned Naphtha.

Following the death of Dhirubhai in 2002, a succession dispute between his sons, Mukesh and Anil Ambani, led to a family settlement in 2005. This resulted in a division of assets, with Mukesh Ambani retaining control of Reliance Industries' core petrochemical business and oil and gas exploration operations. Anil Ambani got the Financial Services company, the energy, the telecommunications and the infrastructure assets.

Under Mukesh Ambani's leadership, RIL underwent significant transformation. The company expanded its petroleum operations, commissioned a second refinery at Jamnagar, and entered retail business through Reliance Retail in 2006.

The discovery of significant gas reserves in the Krishna-Godavari basin marked Reliance's successful entry into natural resource exploration. This was a further backward integration into Oil and Gas Exploration.

The Petroleum and Refinery Assets are highly cash generative and RIL used the cashflow to diversify into new higher growth areas, notably telecommunications, digital infrastructure and retail. Reliance has become a consumer facing business to much greater extent than was the case before.

Digital Revolution and Retail Expansion

In 2016, Reliance launched Jio, revolutionizing India's telecommunications sector with affordable 4G services. The company's aggressive pricing strategy and extensive network coverage disrupted the market, leading to widespread digital adoption across India. Jio is now the leading telecommunication and data provider in India. Having used aggressive prices to land customers at scale, it is now raising prices. The current wireless mobile market revenue share is Jio (46%), Bharti Airtel (37%) and Vodaphone Idea (17%).

In the last eight years, Reliance Retail expanded dramatically, becoming India's largest retailer by revenue.

The Reliance business around 2019 is shown above. After the expansion into oil refining, Reliance went into petroleum retailing in partnership with BP. The footprint has expanded into many other industries including media, digital services, e-commerce and payments.

Reliance Retail has expanded significantly and built retail chains based on many global and Indian brands.

Recent Developments

Jio Financial Services (JFS) was demerged from RIL in 2023. RIL shareholders were given shares in JFS and RIL now has no stake in JFS.

JFS was created with the aim of entering India's financial services sector, leveraging the massive customer base and digital infrastructure of Reliance Jio's telecom network. The company aims to provide a range of financial services including lending, insurance, payments, and digital financial solutions. In 2024, it launched a joint venture with Blackrock to offer retail financial services in India.

New Investments

RIL is making new investments in renewable energy. They plan to offer a fully integrated end-to-end renewables' energy ecosystem to customers through solar, batteries and hydrogen. They will set up solar manufacturing plants in Jamnagar in the next two years. After that they will target battery manufacturing. Recently they have announced they will invest in large AI datacentres in Jamnagar. The plan is for a 3GW AI datacentre, which is much larger than the largest established unit of this type.

Historic Returns

Revenues, profits and cash flows have grown strongly in the last four to five decades and the share price has advanced strongly from about INR 60 per share in 2006 to INR 1230. A 20X return over about 20 years. This implies a 16% CAGR share price return in INR terms. This would translate to about 13% CAGR in US$ terms. The total returns have been higher due to dividends and returns from demergers such as JFS.

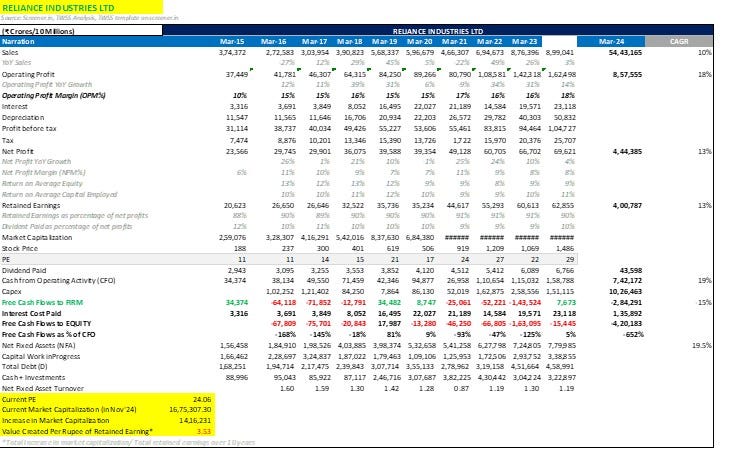

RIL : Summary 10-year Financial Results

In the last decade, Revenues and Net Profits have grown at a CAGR of 10% and 13% respectively. Over the same period, operating cash flow has grown at a CAGR of 19% indicating the strong cash generating potential of the business.

In the last ten years, the company’s cumulative retained earnings have been INR4trn (US47bn). Over that period the increase in market capitalisation has been INR 14trn (162bn) or 3.5 times. Each rupee of retained earnings has created more than 3.5 rupees of increase in market capitalisation. This is a good performance for a company in a capital-intensive business. It passes the Warren Buffett described below:

“Unrestricted earnings should be retained only when there is a reasonable prospect – backed preferably by historical evidence or, when appropriate, by a thoughtful analysis of the future – that for every dollar retained by the corporation, at least one dollar of market value will be created for owners. This will happen only if the capital retained produces incremental earnings equal to, or above, those generally available to investors.”

The composition of the Revenues has changed significantly in the last ten years. Today Retail and Telecom account for 34% of Revenues and 50% of EBITDA, respectively compared with about 1-4% ten years ago.

In FY 2024, Total Revenue was INR 9.1trn (US 105bn) and net profit was INR 696 bn ($ 8.1bn). The current market capitalisation is about $192bn.

Summary of Core Business Segments

Oil to Petrochemicals (02C)

The Refinery has sophisticated crude processing capabilities. The O2C segment continues to generate substantial cash flows, though its contribution to overall profits has gradually decreased as newer businesses have matured. Refining is a high fixed-cost business: billions of dollars have to be invested before a single barrel of oil can be refined. They key metrics are the capacity of the refinery, the capacity utilisation and the Gross Refining Margins (GRM).

For Reliance the metrics are as follows

Refining capacity: 1.45million barrels per day

Gross Refining Margin (GRM): Historical average of $9-11 per barrel

Petrochemical production capacity: 38.2 million tonnes per annum

Jamnagar is the largest and most complex refinery in the world with Nelson Complexity index score of over 21. To build the word’s largest and most complex Oil Refinery in a remote location was a very impressive engineering achievement.

The definition of

GRM = Value of Refined Products - Cost of Crude Oil

For example:

If a barrel of crude oil costs $80

And the refined products from that barrel can be sold for $95

The dollar GRM is $15.

The GRM = ($15/$95) × 100 = 15.8%

The net earnings of a refinery will be the GRM minus operating costs, maintenance, labour, and other expenses. The operating expense per barrel which is about US$ 1.7 to US$2. To derive the real operating margin of the refining operation you have to subtract the operating expense per barrel from the dollar GRM per barrel. In the above example, the operating income per barrel would be $ 15 minus $ 2 = $13.

In 2024, the GRM was about $9. The operating income per barrel would have been around be $7 ($ 9-$2). So annual estimated refining operating profit would have been approximately $7 * 360 days * 1.45mn barrels a day which equals to $3.6 bn or INR 306bn. Analysts expect GRMs to rise to about $11 in FY 25 and FY 26.

Refinery earnings are heavily dependent on GRMs because:

Processing costs are relatively fixed - The main operational costs (labour, maintenance, energy) don't vary much with production levels

Direct correlation to profits - Higher GRMs generally translate directly to higher profits since most other costs are fixed.

This raises the question as to what determines GRM? GRMs are determined by a number of factors which are mostly beyond the control of the refiner.

GRMs depend on

Global oil prices

Regional demand for specific refined products

Available refining capacity in the market

Seasonal factors (like higher gasoline demand in summer)

This most efficient refineries focus heavily on:

Optimizing their crude oil selection

Maximizing production of higher-value products

Maintaining operational efficiency

Managing their costs carefully

In the Industry, the most widely quoted GRMs benchmarks are the Singapore GRMs. These are averages. Reliance achieves much higher GRMs than the benchmark. This reflects the higher technical complexity of the Refinery, the greater than average scale of operations and the integration advantages. These are explained in greater detail in Annex 1.

As the most complex refinery in the world, Reliance is able to maximise production of the higher value products. It also has the best safety record of all large refineries.

Refining performance is vulnerable to volatile crude oil prices and refining margins. The transition toward renewable energy poses a long-term structural challenge to growth prospects. However, RIL is also investing in renewable energy at scale.

Potential Catalysts for Oil and Chemicals business

Partnership with Saudi Aramco, Sabic and other strategic partners –

Expand into downstream chemicals

Carbon Capture and Utilisation Services (CCUS) and alternative energy investments.

Jio Platforms

Jio was launched in 2016 and has revolutionized India's telecommunications sector. The platform has nearly 480 million wireless and wired broadband subscribers. It is number one mobile service provider in India with 47% market share and Bharti Airtel which has 37%. The third player, Vodaphone idea has 13% but it is financially troubled and losing ground. The market is becoming a duopoly with Reliance as the dominant player. this bodes well for price increases, margins and profitability.

The most important metrics are the number of subscribers and the Average Revenue per User (ARPU). The former is about 480mn. In January 2024, Reliance Jio's ARPU (Average Revenue Per User) was Rs 178.8 (US$2) per subscriber per month.

An approximate calculation for Jio subscription revenues in US dollars will be 480mmn * $2* 12 months = $ 11.5 bn or INR 990.

A Jio Retail Unit

Operational Metrics:

Subscriber base: 480+ million

ARPU: INR 179

Network coverage: 99% of India's population

Data consumption per user: 25GB per month

Analysts covering the stock are assuming that ARPU will increase by about 12% due to an increase in tariffs and subscriptions will grow by 4-5%.

Potential Future catalysts for Jio Platforms

Market share gains

ARPU expansion due to tariff hikes –

5G adoption –

Possible IPO of Jio Platforms –

Monetization of Jio Platform services

Retail Operations:

Reliance Retail is India's largest retailer by revenue, operating across formats including grocery, consumer electronics, and fashion. The company's omnichannel approach and extensive physical presence may provide competitive advantages in India's rapidly growing retail market. In the last year, the company has been closing some stores in the loss-making segments including Grocery.

Potential Catalysts for Retail Operations

Digital commerce ramp-up

New commerce strategy

Private labels &FMCG partnerships –

Margin expansion from scale

IPO of Reliance Retail

Summary of Current Market Position

Competitive Advantages

Integrated operations across the energy/ synthetic textiles value chain

Extensive retail distribution network

Strong telecommunications infrastructure with dominant market share

Robust balance sheet enabling strategic investments

First-mover advantage in several digital initiatives

Investment Considerations

Strengths

The company's diversified revenue streams provide stability while offering exposure to India's growing consumer market. Reliance's strong market position and financial resources enable it to capitalize on emerging opportunities and weather economic challenges.

Risks

Regulatory changes in telecommunications and retail sectors

Global oil price volatility affecting refining margins

Intense competition in retail and digital services

Environmental regulations impacting petrochemical operations

Valuation

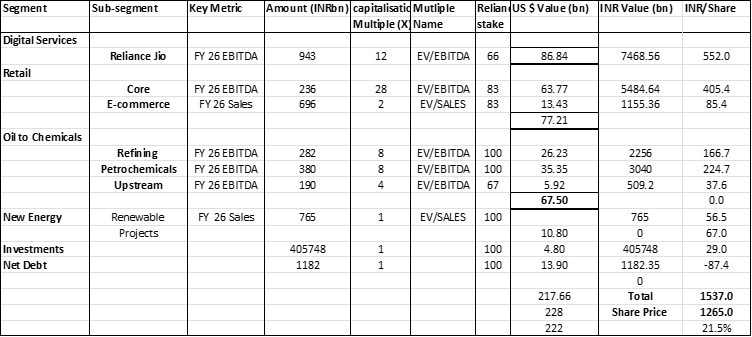

Reliance is a giant conglomerate with significant businesses in three large unrelated segments. Such as company can be valued using a Sum of the Parts (SOTP) calculation. We will attempt such a calculation to arrive at an estimated valuation.

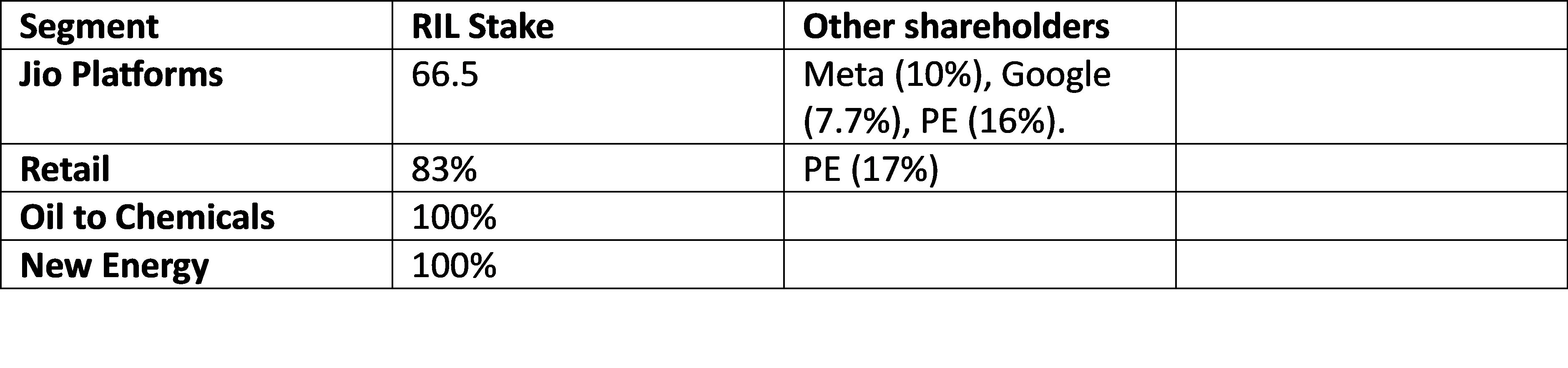

RIL does not own 100% of all the business segments as noted below:

Our estimate of the valuation is shown below. Each segment is valued based on estimated FY 2026 EBITDA or Sales.

The Sales and EBITDA numbers were taken from company data and research reports from two reputed brokerages. For each segment we worked out an appropriate capitalisation multiple to derive the Enterprise Value. We then adjust the EV valuation for the percentage owned by RIL. Finally, we divide by the number of shares (13.5mn) to get the per share valuation in INR terms.

Retail Division Valuation

Enterprise Value: $70bn

Valuation Method: 25x EV/EBITDA multiple

Key Comparable Companies: Avenue Supermarkets (50X – too high), Walmart (20x)

Oil to Chemicals Valuation

Enterprise Value: $67bn

Valuation Method: 8x EV/EBITDA multiple

Key Comparable Companies: Saudi Aramco (7.6X), ExxonMobil (7.3x)

Digital Services Valuation

Enterprise Value: $86bn

Valuation Method: 15x EV/EBITDA multiple

Key Comparable Companies: Bharti Airtel (14.6X), Vodafone Idea (16.1X)

SOTP Calculation

Per Share Valuation:

Number of shares outstanding: 13.5mn

Implied value per share: INR 1537

Sensitivities

The valuation is very sensitive to many assumptions including:

Changes in GRM margins due to oil price volatility

Digital services ARPU growth trajectory

Retail business expansion pace and profitability

Overall market conditions and industry multiples

Conclusions

The estimated valuation that we have derived is INR 1537 per share which is a 21% premium to the current share price of INR 1265. Conglomerates trade at a discount to the SOTP value.

In mature markets such as the US, conglomerates have become less common than their heyday in the 1960s and 1970s. The reason for this was a change in focus in management science to core activities and shareholder value. This led managements to re-focus on the core and shed non-core activities.

In a high capital cost and low trust society like India, there may be more room for multi-division corporation with activities across a range of unrelated segments. A conglomerate with cash rich business division may be more willing to provide capital to new growth businesses at a lower cost than the market would be.

In the West, conglomerates are not well looked upon by the market and trade at significant discounts to analysts’ SOTP estimates. Often the only way to narrow this discount is to have a value realisation or value unlocking event. For example, value could be realised for RIL if there was an IPO of Reliance Retail or Jio Platforms, or better still, a demerger where existing shareholders are given a pro-rata share in a newly-listed Jio Platforms or Reliance Retail

However, in the absence of these events, some discount is likely to persist. We will continue to track RIL. At the moment our tentative conclusion is the stock appears to be fairly priced and may perhaps be a little cheap.

Annexe 1

The Jamnagar Refinery has much higher GRMs than the benchmark Singapore GRMs. There are a number of key reasons for this. These include

Higher Complexity Index: Reliance's Jamnagar refineries are among the most complex refineries globally, with a Nelson Complexity Index over 21. This allows them to:

Process heavier, more sour (high sulphur) crude oils which are cheaper

Produce a higher proportion of valuable light and middle distillates

Be more flexible in adjusting their product mix based on market demands

Scale Benefits: The Jamnagar complex is the world's largest refining hub, which provides:

Better purchasing power for crude

Lower per-barrel operating costs

More efficient logistics and operations

Integration Advantages:

Integration with petrochemical operations allows for optimizing product streams

Strong infrastructure for importing crude and exporting products

Ability to shift between domestic and export markets based on pricing

You say "Following the death of Dhirubhai in 2002, a succession dispute between his sons, Mukesh and Anil Ambani, led to a family settlement in 2005. This resulted in a division of assets, with Mukesh Ambani retaining control of Reliance Industries' core petrochemical business and oil and gas exploration operations. Anil Ambani got the Financial Services company, the energy, the telecommunications and the infrastructure assets."

But I would like to know more about the management today.

Is the business still run by the brothers?

Is there still a grievance in the family?

Is nepotism an issue? In my experience, there are 7 billion people in the world and the chances that the son of the founder being the best choice to lead the business is about 7 billion to one! Brunello Cuccinelli once told his daughter, 'you may inherit my business, but don't assume that you will inherit the ability to manage it'. These are wise words. The father was saying that if you want to protect the asset I leave you (the business), find the best person to run it. Founders that don't follow this advice generally see their offspring destroy much of what they had built.

With this in mind, I would like to better understand the management here.

Also, their growth by acquisition style seems to be a scatter gun approach rather than being focused like a sniper. How do they determine which companies to acquire and what is their record on divestments?

Thank you in advance.