We try to look at the fundamentals of listed US companies and are beginning to look seriously at Indian companies now.

The S&P 500 has just completed two consecutive years of 20% plus returns. Bank of America researchers say this has happened only four times in the last 150 years. I am assuming they looked at data as far back as the 1880s and have no reason to disbelieve them.

India’s Nifty 50 Index was up in 2025 by about 8%. Rupee depreciation means the returns to foreign investors were a little less. However, it was the ninth consecutive year of a gain in the Nifty 50. I have not looked at the data of the Nifty or the older BSE Sensex Index, but I am pretty sure that nine consecutive up years has not happened before.

All this suggests we are living in unusual times.

For the last five years, we have been looking at US stocks. For at least the last eighteen months, we found most stocks very overvalued and virtually nothing looked cheap on a fundamental basis.

I thought US companies looked expensive until I started looking at the fundamentals of Indian companies. They generally look even more expensive even when you adjust for higher growth prospects and higher profitability (where relevant).

I do not know whether the S&P 500, the Nasdaq 100 and the Nifty will advance in 2025. They may well do so. I have covered some of the possible reasons in this Substack in the past. However the odds must be against it.

Stocks are valued at levels which build in a lot of optimism of future growth and profitability.

We do not know whether markets will correct and whether it will be time correction or a price correction.

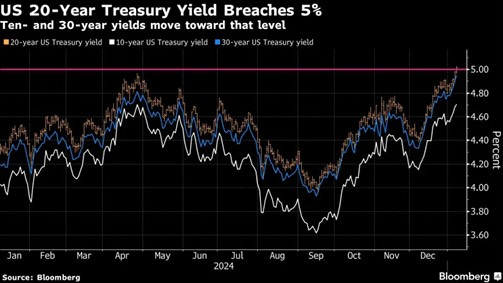

The balloon is full of air. What will be the pin to prick the bubble? Commentators are focused on rising US Treasury Bond yields and the possibility that the 10 year US Treasury Yield will rise to over 5%. The 20 year yield has just done so.

Nobody can reliably predict what markets will do . We certainly cannot. However, we do need to make a judgement on the probability of risks.

We currently believe (fear) that these are weighted to the downside. We need to preserve our capital.

Therefore we are looking at the valuations of some of the companies in our portfolio. We are reducing our holding in some of them, even though we continue to believe they remain fundamentally good companies, and increasing the percentage of our portfolio in cash.

Agree with the euphoria while there are so many dark clouds out there.

What is your view and data show about a philosophy that one should still stay in the market and participate with caution, not get out and keep waiting in the sidelines?