Sprouts Farmers Market (SFM).

Fast Growing Health Food Retailer

We first looked at SFM about a years ago but were not able to look in detail due to lack of time. The stock has doubled in the last year. Is it too late to get on board?

Sprouts Farmers Market, Inc. is a food retailer. It was founded in 1943 and is headquartered in Phoenix, Arizona. The company started as a single market stall.

SFM is a grocery store that offers fresh, natural and organic food that includes fresh produce, bulk foods, vitamins and supplements, packaged groceries, meat and seafood, deli, baked goods, dairy products, frozen foods, body care and natural household items etc. It tries to target consumers interested in health and wellness and those with specific dietary requirement or allergies.

The company is driven by the rapid growth rise of the health-conscious customers and the customers with specific dietary needs.

“SFM offers a distinct grocery experience with an open layout with fresh produce at the core. SFM claims “it inspires wellness naturally with a carefully curated assortment of better-for-you products paired with purpose-driven people. We continue to bring the latest in wholesome, innovative products made with lifestyle-friendly ingredients such as organic, plant-based and gluten-free.”

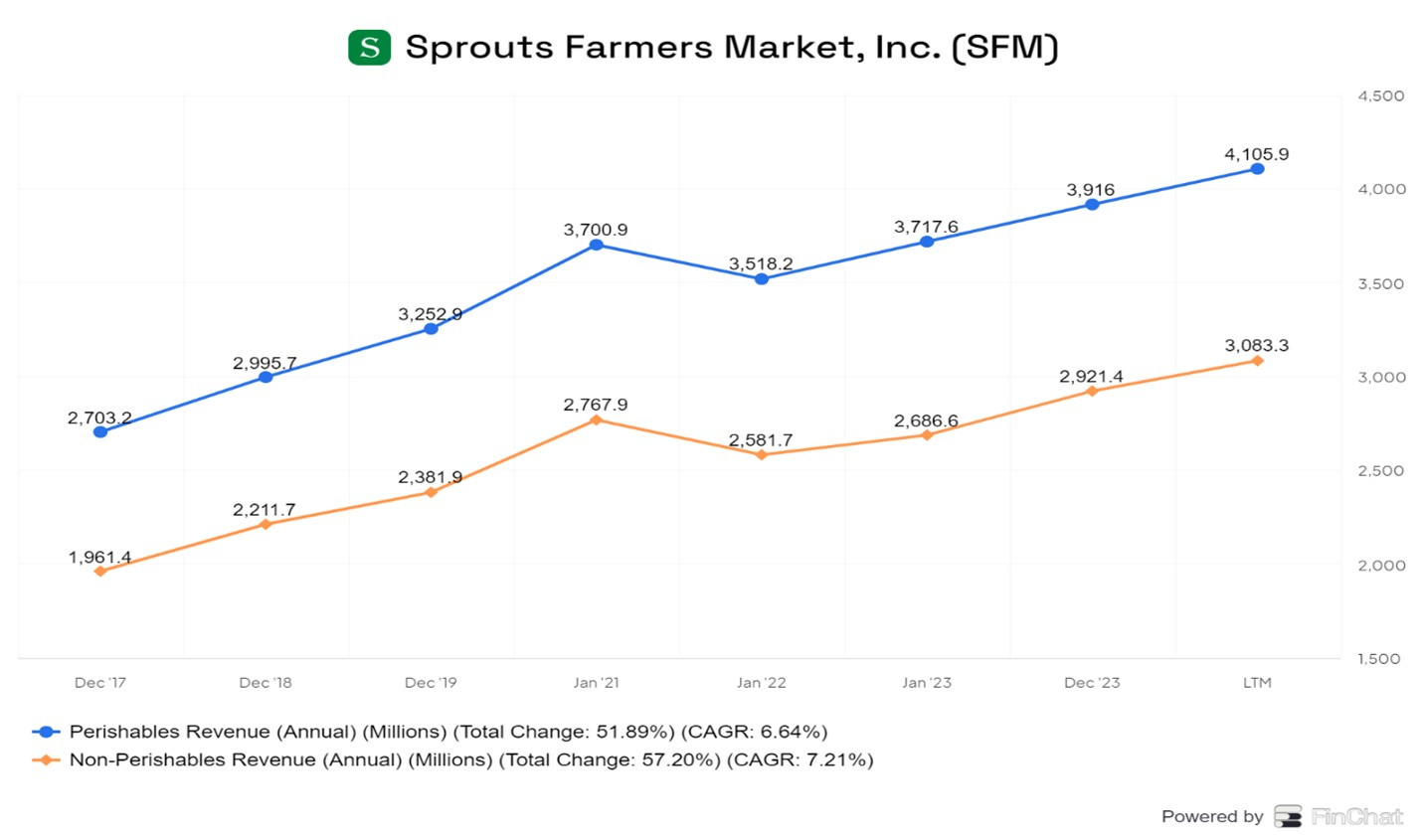

SFM categorises the products it sells as perishable and non-perishable.

Perishable product categories include produce, meat, seafood, deli and bakery.

Non-perishable product categories include grocery, vitamins and supplements, bulk items, dairy and dairy alternatives, frozen foods, beer and wine, and natural health and body care.

Perishable account for 57% of total revenue (see below) but non-perishables have grown a little faster in the last five years.

SFM has 407 stores in 23 states at end and claims to be the “fastest growing specialty retailers of fresh, natural and organic food in the United States.”

The company has grown steadily and profitably in recent years and shareholders have enjoyed good returns.

In the last 10 years, shareholders have achieved a CAGR total return of 14.0%.

In the last 5 years, shareholders have achieved a CAGR return of 41.4%.

In the last 3 years, shareholders have achieved a CAGR return of 68.7%.

The stock has performed very strongly in the last 3-5 years

This can be attributed to the current CEO Jack Sinclair who joined in 2019. He changed the strategy in two critical ways.

· He decided on a policy of radical differentiation with trying to only offer products that are not available anywhere else.

· He also decided not to compete on price: this required an end to a reliance on discounting, flyers and coupons to bring the customer.

Another important element of Sinclair’s strategy was to reduce the size of new stores from about 33k square feet to 23k square foot. We will discuss the rationale for this below.

Sinclair had joined from Walmart and has seen that company from the inside and is a great admirer of it. However, he also realised that a smaller grocery company like SFM with a strong product overlap with Walmart or Target would be forced into an unwinnable price war. It is estimated that only 11% of merchandise overlaps with Walmart or Kroger.

Sinclair told a Goldman Sachs (GS) Global Retailing Conference on September 5th that he tries not to stock anything that Walmart is selling.

“When I see a product that Walmart are selling, my first instinct is let's make sure we're not selling that.”

Sinclair noted SFM are not chasing the $1.4trn Grocery Market but the $200bn health food market. Their competitor is not Walmart, Kroger or Target but Trader Joe’s, Amazon Wholefoods or perhaps, Costco.

A second and related element of Sinclair’s strategy is not to compete on price. He removed flyers and discounts. The aim point was to eliminate the customer who spends $10 on four jars of a heavily discounted item and has no interest in the rest of the offering.

A strategy of excluding customers may seem counterintuitive. It initially caused alarm among SFM’s staff who had a traditional grocery mindset.

“We probably lost about 500,000 customers overnight.” Sinclair told the GS conference. 500k customers was a not insignificant 20% of the customer base. The strategy was to drop 20% of the customers and focus on 80% of the most profitable customers.

“These are not the customers we want. We want somebody who values the unique merchandise in our stores.”

Selecting or targeting customers carefully makes sense. Charlie Munger who was Warren Buffet’s partner at Berkshire Hathaway was a great admirer of Costco and was on its Board of Directors for many years. Munger was asked why Costco did not remove its (relatively modest) membership fee and let in all comers. His answer was by liming to members, Costco eliminated those people who came to the store for a very few low-value items and probably eliminated nearly 100% of shoplifting.

We will describe the SFM business in detail before looking at the key historic financial numbers

The SFM Offering

As noted above the offering is very different from the large Grocers. Sprouts’ products have attributes that are not found in other places because the company is highly focused on its specialty market niche. The majority products sold in its stores are attribute-driven – e.g. Organic, Vegan, Paleo, keto, plant-based, and non-GMO.

“we've gone really unique and attribute based, the further the teams have gone, those are the categories that have really led the charge for us over the last, call it, 6, 8 quarters.”

Sprouts is also a big player in Vitamins. It has great people in its Vitamin Department. They know a lot about the products and can help customers select the right ones.

“When you go into our vitamin department, you get these people who have got such passion and such knowledge for customers, but they tend to have very interesting kind of hairstyles and nose rings and tattoos and that and really welcoming the difference in our company, the difference in our assortment, the difference in our stores that I have a passion for what we do.”

“When you get into our meat department, we don't have any conventional meat anymore. It's all grass-fed, no antibiotics, all the kind of dynamics that matter to our customers. And right across the store, that's what that team are bringing to us and making a difference for the customers.”

At the GS Conference, the CEO outlined some of the recent trends.

“Non-alcohol alcohol, which strikes me as a bit of a kind of misnomer, but that category, we're seeing a lot of innovation, a lot of differentiation. That's doing well for us.”

“Plant-based dairy, not so much plant-based meat, which saw a bit of a peak has come down.”

“Organic produce is now more than 45% of our produce sales. … when we double down on that in terms of bringing products in, we're seeing some real strength in there.”

The Store format

In 2019, Sinclair decided to reduce the size of new stores from about 33k square feet to 23k square foot. The larger store format had a lot of unproductive space and this is considerably reduced in the 23K sq ft store. SFM has been able to save on rent and achieve the same sales as in the larger store format.

The new stores are cheaper to build. They have a faster payback time but can still generate the same volumes. Over time, as new stores are added, they will become relatively more important and become a more significant driver of growth

“Returns on these smaller stores are probably higher with a low to mid 30% cash-on-cash return by year five.”

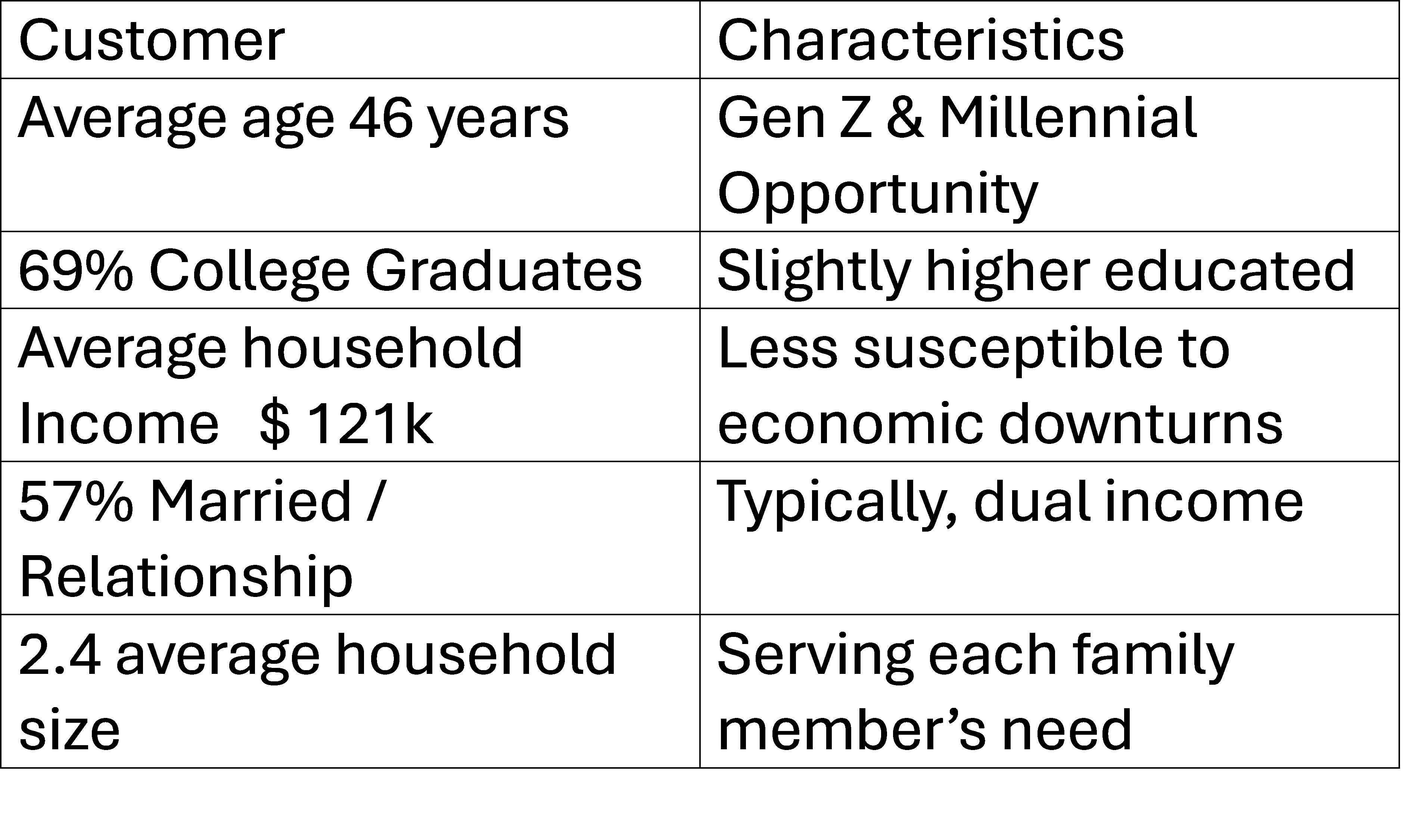

The target customer base

SFM have a particular customer target base. Their Investor Presentation outlines the demographic of their customer base. This is reproduced below:

SFM also describes their characteristics in the Presentation.

32% committed to buying organic

30% committed to dietary lifestyle

69% are concerned about the environment

41% review nutrition labels

28% are looking for Fairtrade /socially responsible

Another feature is that a lot of the customers are women and mothers. They understand the quality of the produce and are less likely to tolerate bad produce. They are also more likely to recommend by word of mouth.

“We are focusing attention on our target customers, identified through research as ‘health enthusiasts’ and ‘selective shoppers’, where there is ample opportunity to gain share within these customer segments.”

The customers are affluent and less likely to suffer in economic downturns.

“Sprouts’ customers go there for keto, organic, paleo, whatever. When the economy slows and they have to cut back, they might buy one less of those items, but they’re not going to switch to another store. They’ll maybe cut back the volume. You hang on to the customer.”

The customer attributes mean they are less likely to change consumption habits

“If you're a vegan, you kind of stick to being a vegan whether there's a lot of inflation or no inflation, there's a positive economy by the economy. You kind of stick to your diet.”

In summary, we can say that SFM has a distinct customers base who are less likely to change their consumer habits and switch to Walmart and Kroger. They are also less likely to trade down in the event of an economic downturn.

The omnichannel strategy

The Sinclair era had only just began when the Covid-19 pandemic hit. This was a tough period for brick-and-mortar retailers. They had to change to an omnichannel strategy

“When I joined the company, we had 2% of our sales on ecommerce through Instacart. Then the pandemic came along, and we went from 2% to 15% of our sales.”

They now have delivery partnerships with DoorDash, Uber Inc as well as Instacart.

“We've been really encouraged, all three partners. … seeing really strong growth in all three partners, which is really encouraging.”

One might have thought people would not order perishable produce online as they would want to inspect for quality and freshness.

However, SFM claim the ratio of perishable/non-perishable in the online orders is the same as in the in-store business. This indicates the customer trusts SFM to deliver quality produce.

“It's really unusual for an ecommerce business to have as equivalent mix in fresh produce as a bricks and mortar business. I don't know any other place that does that. And that says our customer trusts our produce and then therefore trusts the differentiated assortment.”

SFM believe the online orders have not replaced sales which would have otherwise happened instore but they are incremental.

We've been pleased with as we've added channels. It's been largely incremental, which just tells you there pools of customers out there that are in an omnichannel space looking for a different way to engage with us.

The new long-term strategy includes a laser-sharp focus on brand and marketing. Sprouts is embracing a digital marketing approach. It is highly focused on connecting with the customers, keeping them, understanding what they want, getting information about them, hanging on to them, and building a lasting relationship with them.

The supply chain

Sprouts sells perishable products where quality and freshness are key. They need a supply chain that will get the right products quickly and efficiently into the stores. The company has built out a series of distribution Centres (DC), located so each store is within 250 miles of them. This maximum distance ensures that perishable items can sent to stores in a timely manner.

“This 250 miles has been an important part, so that we're not shipping products from Atlanta down to Naples. We're actually trying to get ourselves into a place where the fresh food distribution supports a smaller store with produce at the center.”

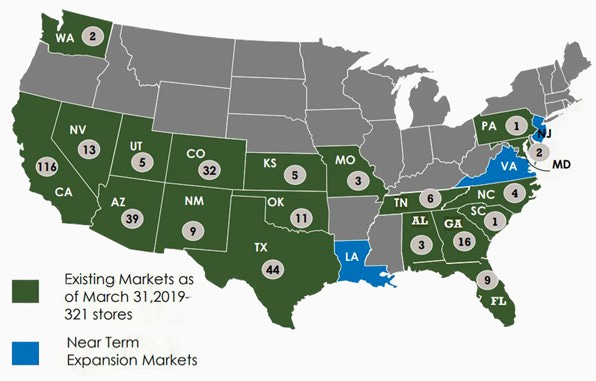

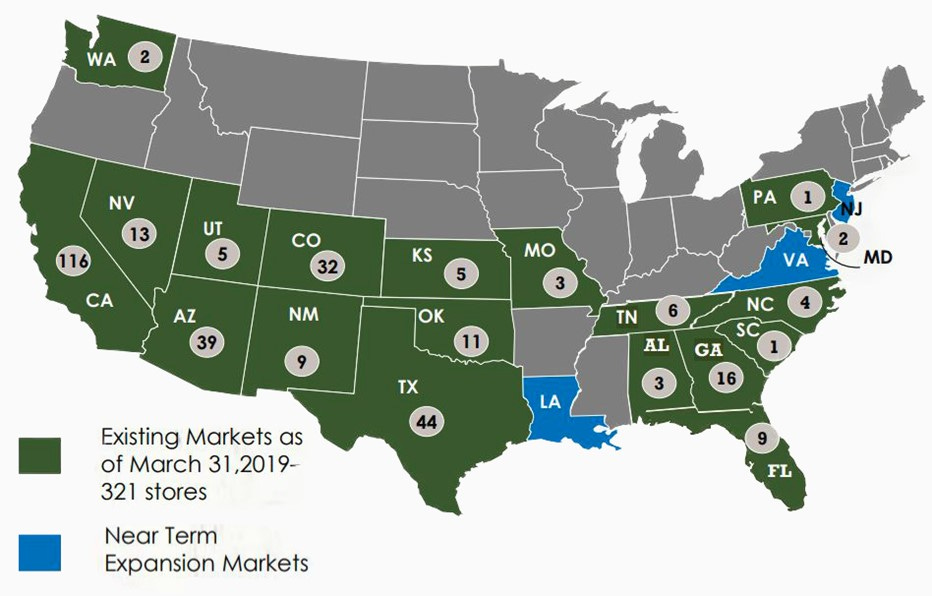

Currently the stores are located on the two coasts of the USA and through the Southern states. SFM is present in 23 states. California has 139 stores while Texas and Florida have 50 and 43 respectively. The company has no presence across the whole of the Mid West. The company estimates that the current network of DCs can support an additional 300 stores.

They plan the next DC in New England. The next one after that will be in Chicago to serve the mid-west.

“If we do get to the Midwest in due course, we'll need a distribution centre somewhere up towards Chicago somewhere at some point.”

The map above is dated and shows the store count and location in 2019. The numbers have increased but the geographical distribution remains the same.

Sprouts Account and the Loyalty programme

The company is designing a loyalty programme. A pilot is underway in 2 cities to do a bigger effort with your loyalty program.

“We're on a customer data journey. We're on a journey to try and as a specialty retailer as opposed to a mass retailer, understanding our customers better and better is going to be key to the future of how we evolve our merchandising, our marketing, our engagement with those customers.”

“This is about creating a kind of engagement and a loyalty that's the customer and we only need the customer to spend a little bit more with us. The whole point of the tests that we're doing in Tucson which is an established market and in Nashville which is a relatively new market to us.”

SFM KEY NUMBERS

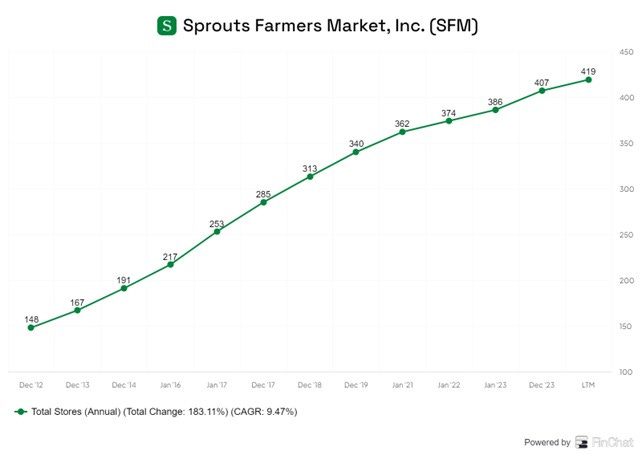

Growth in stores

The company has increased the number of stores steadily form 148 in 2012 to 419 currently. The CAGR growth rate has been 9.5%.

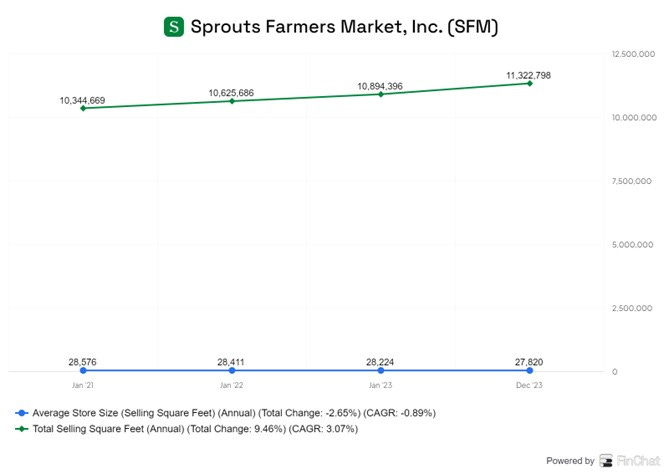

Growth in Square Footage

The total square footage has reached 11.3mn and the average sq ft per store has fallen from 28,500 in 2021 to 27,820 currently. This will continue to fall as new stores will be smaller.

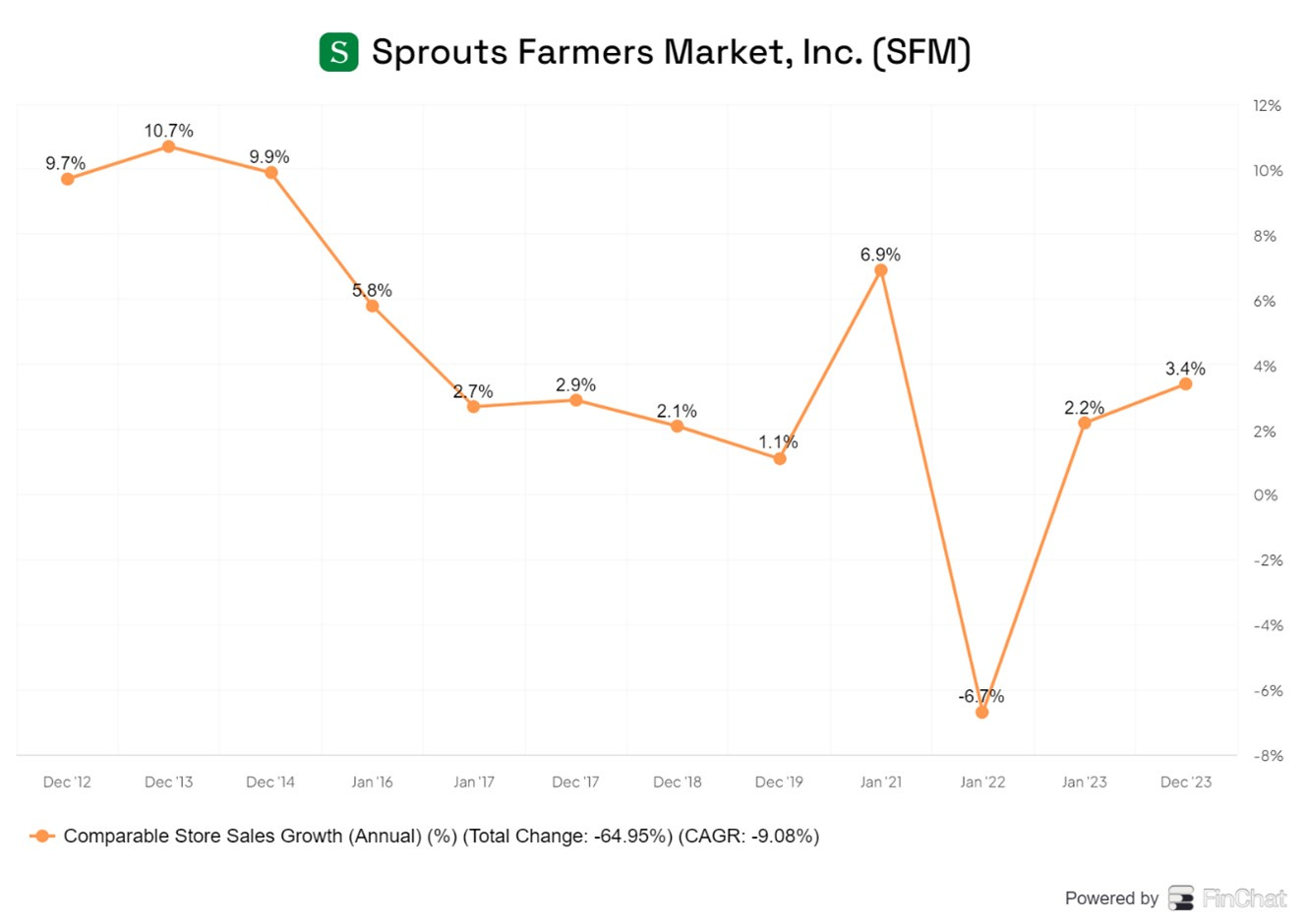

Same store sales

Comparable stores growth rate is about 2%-3% per annum. This is on the low side but management say it is stronger on the newer stores, so overall store sales growth should rise gradually over time.

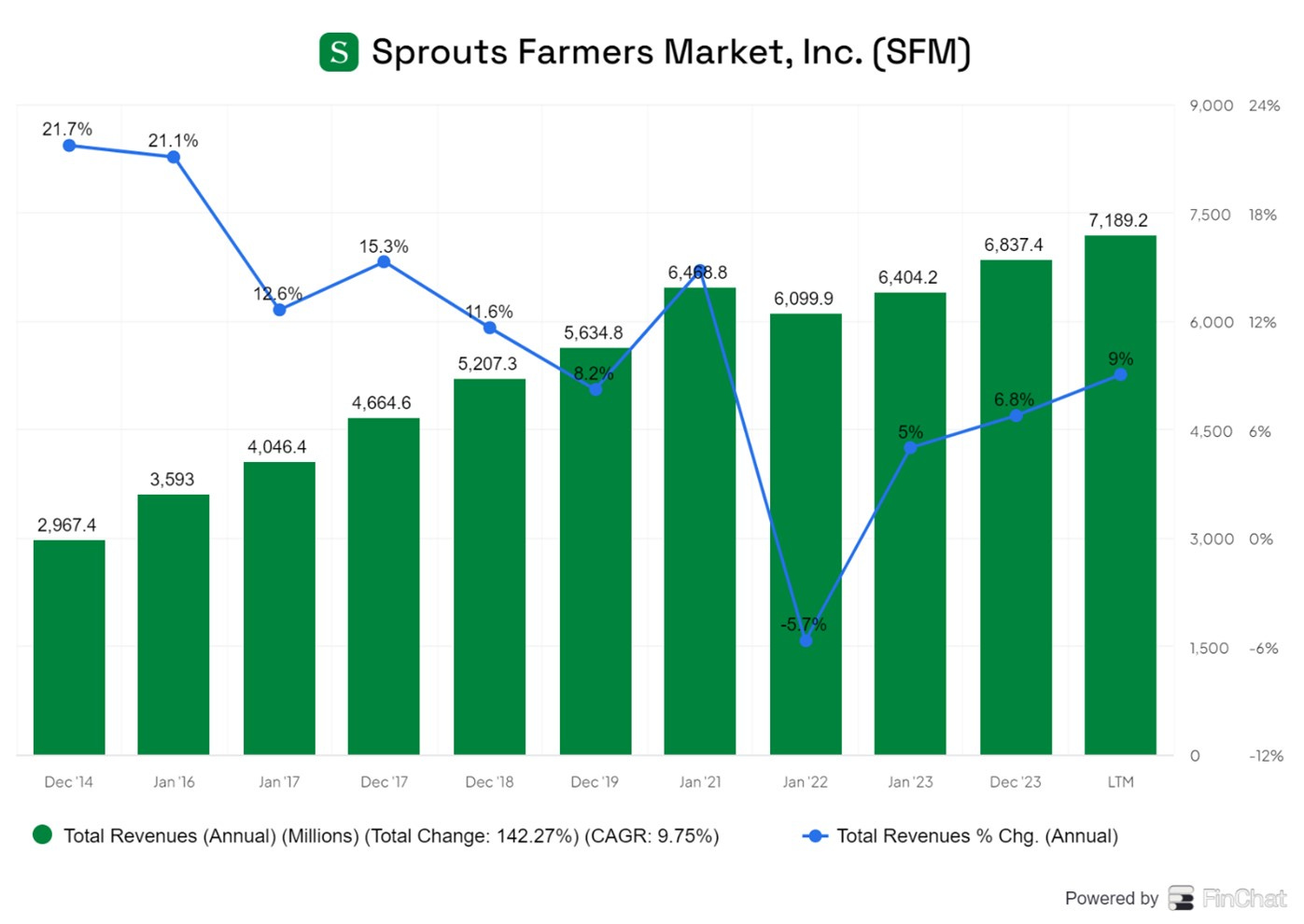

Revenue Growth

Total sales have grown from $3bn in 2014 to $ 7.0bn in 2023 -a CAGR of about 9.8%. Annual growth rates have slowed from 20% in 2014-2016 to about 7%-9% currently. There was a sharp dip in the Covid 19 era (2020-21).

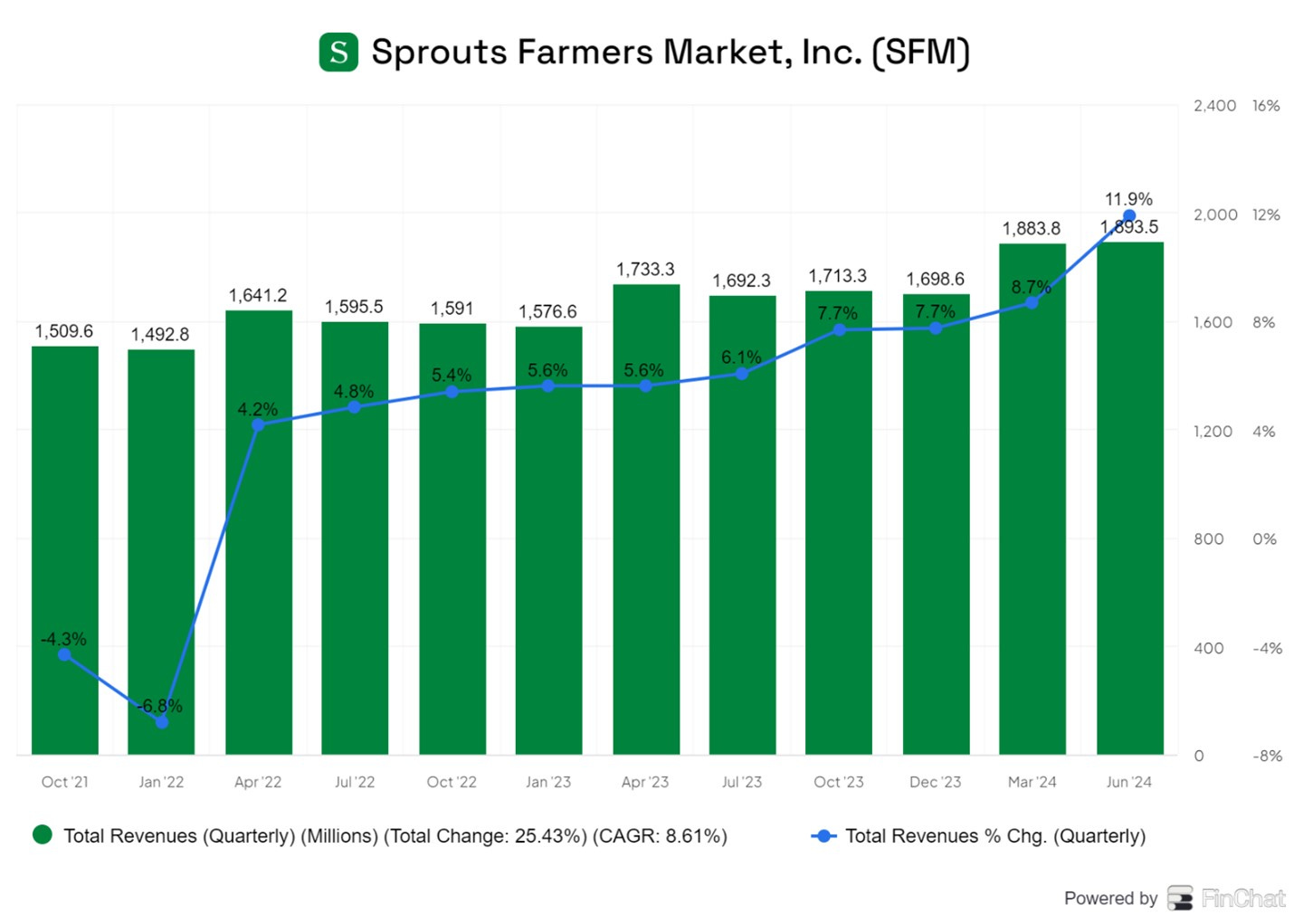

Looking at the quarterly numbers, we see the slow and steady recovery post the Covid dip.

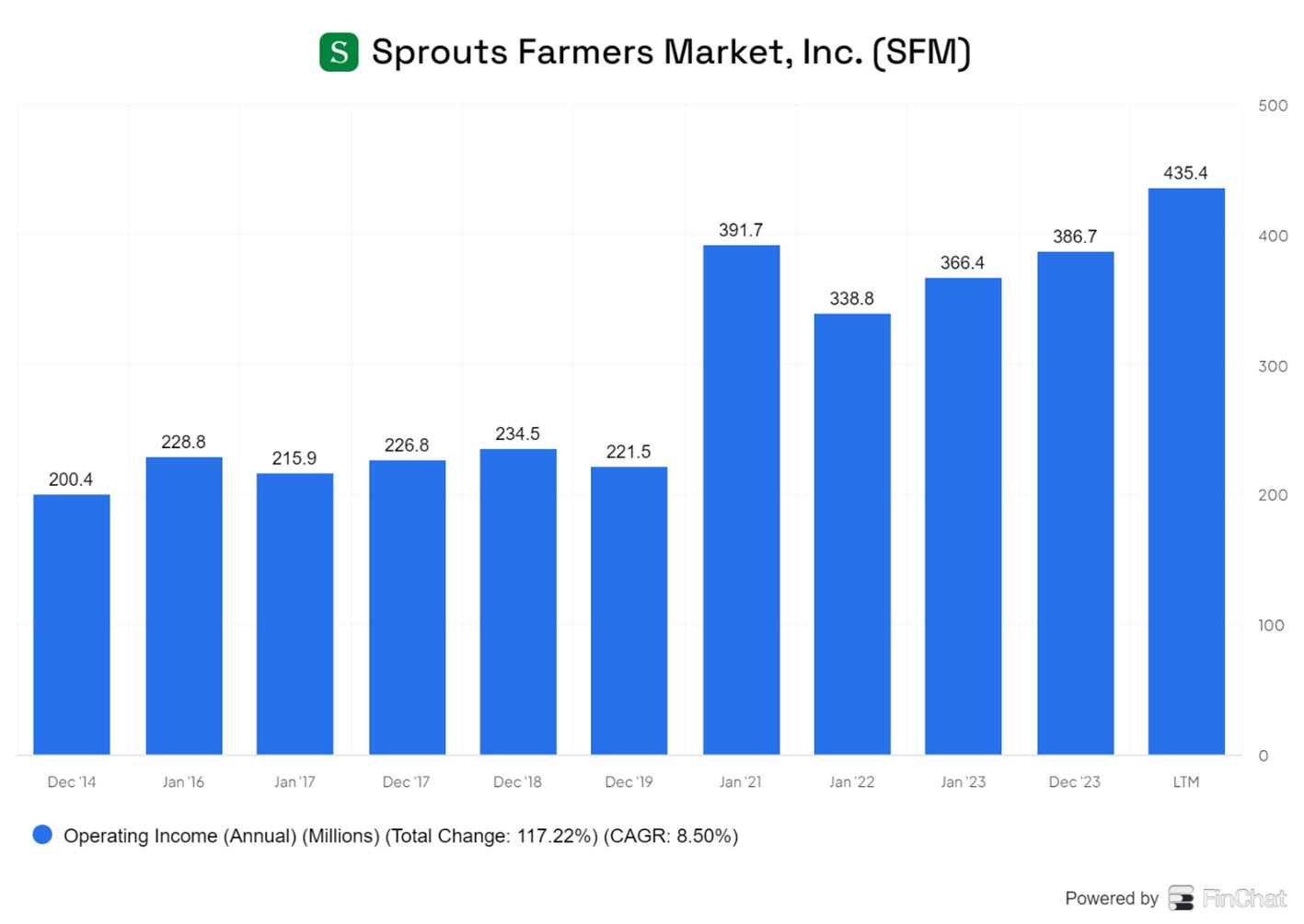

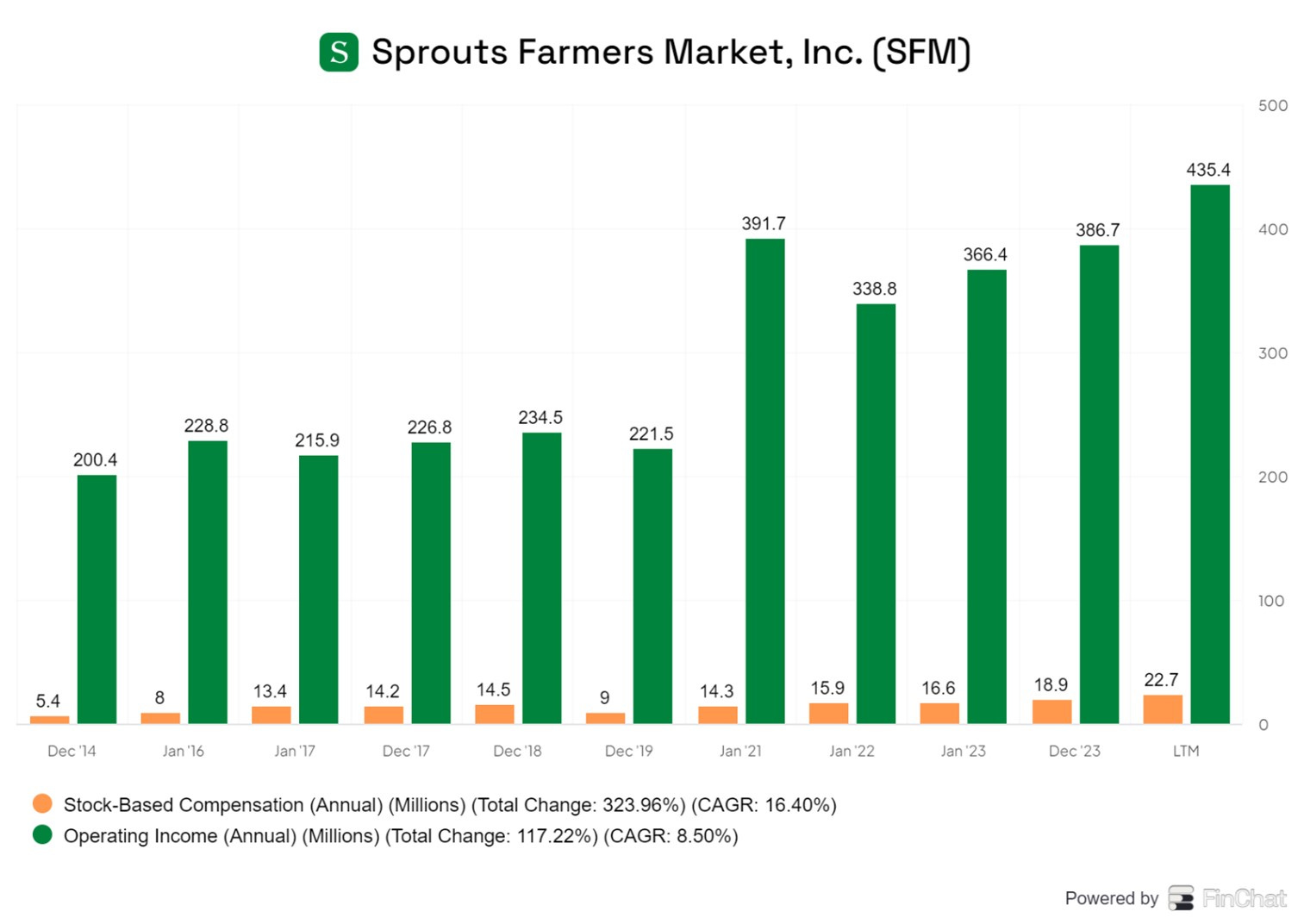

Operating Profit

Operating Profit has grown at a CAGR of 8.5% in the last 10 years.

Operating Cash Flow has grown by 10.8% CAGR. This is a little faster than operating than Operating Income.

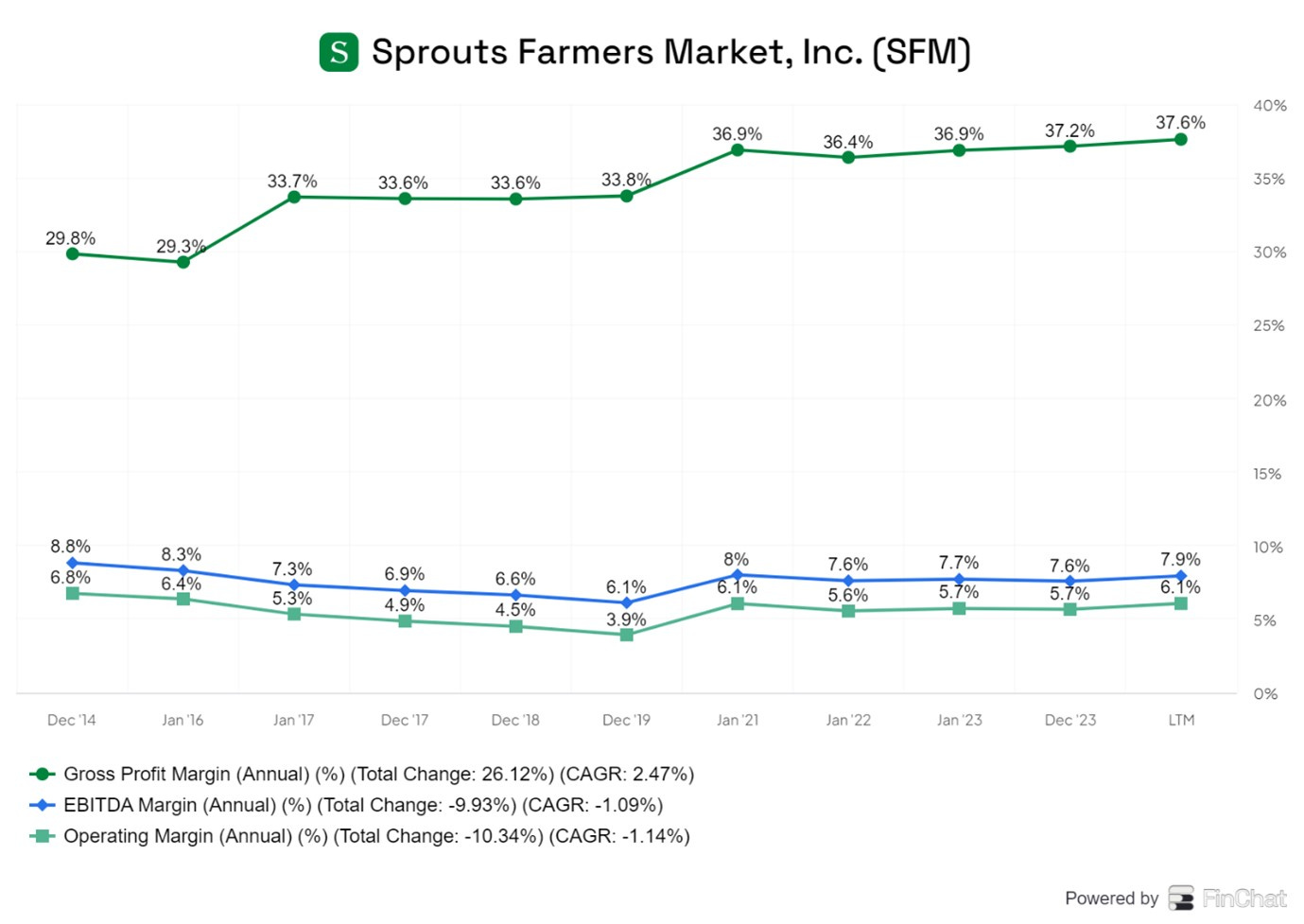

Margins

Margins have improved as company has eliminated discounting and reduced shrinkage.

Margins have been quite stable. This is by design.

“Our focus is really bottom-line stability. EBIT margin stands stable. And if we find gains as we have the last few years, we intend to keep them and maintain them.”

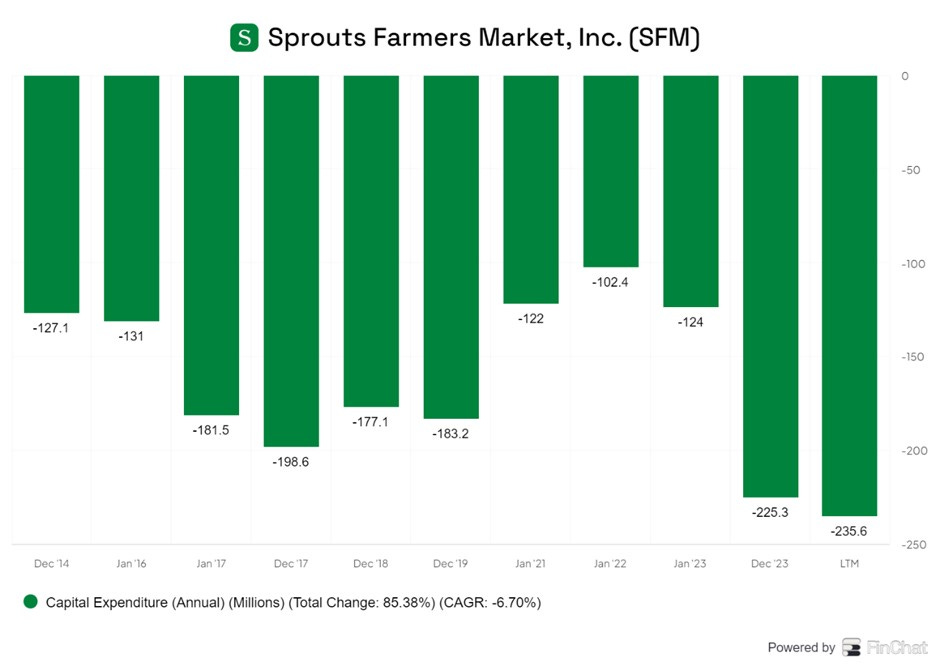

Capital Expenditure

Capital Expenditure is shown above as a negative figure as it is an outflow. It has grown by 6.7% and therefore by less than Operating Cash.

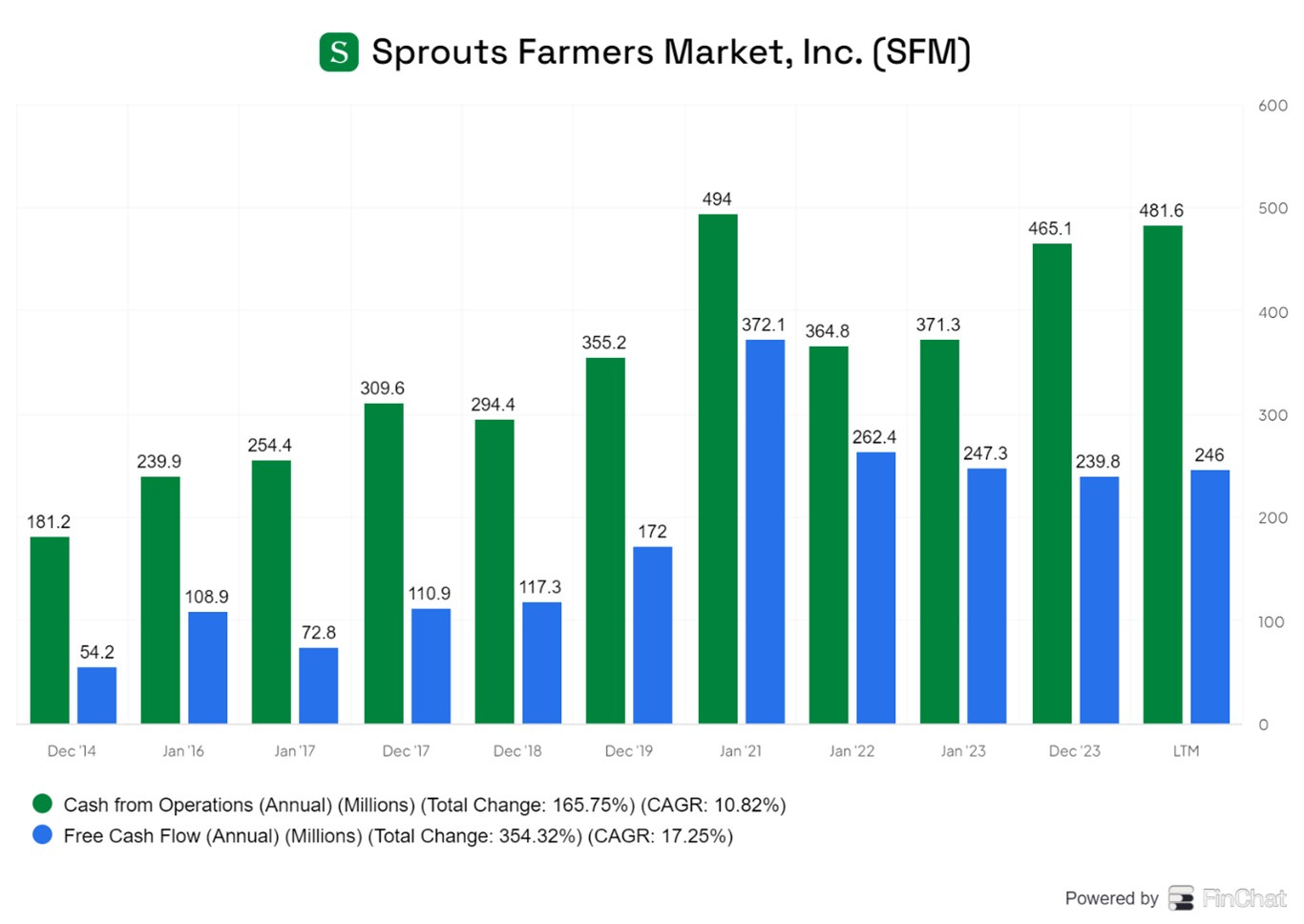

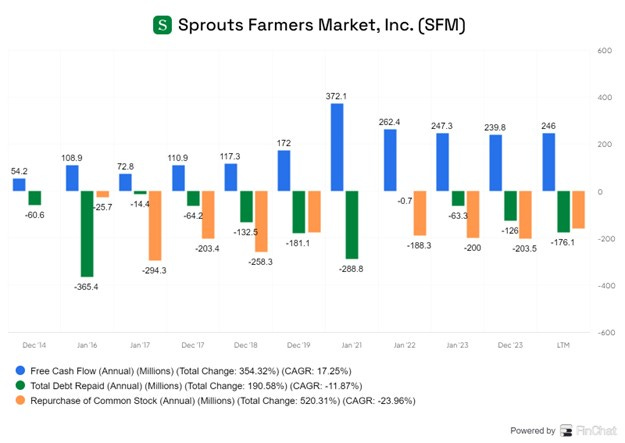

Free Cash Flow

Free Cash Flow (FCF) has grown by an impressive 17.23% CAGR. Future FCF growth may slow due to faster growth in capital expenditure.

Capital Allocation

In the past FCF has been used to repay debt and buy back shares. SFM does not pay a dividend.

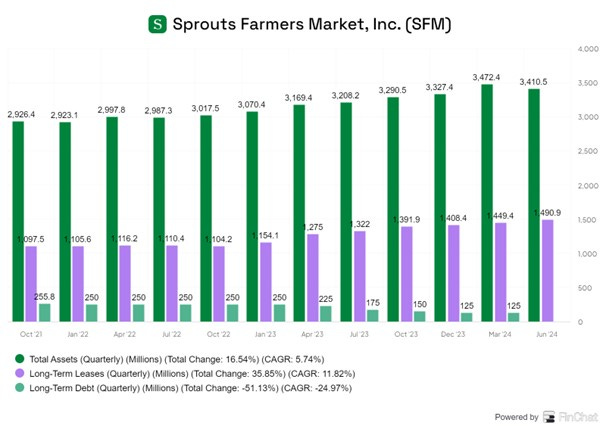

Long-term Debt

Long-term debt has fallen to zero, but Long-term leases have grown to $1.5bn. These are operating leases related to the growing number of Stores and Distribution Centres. The Stores generate a stable revenues which will grow in line and will cover lease payment obligations.

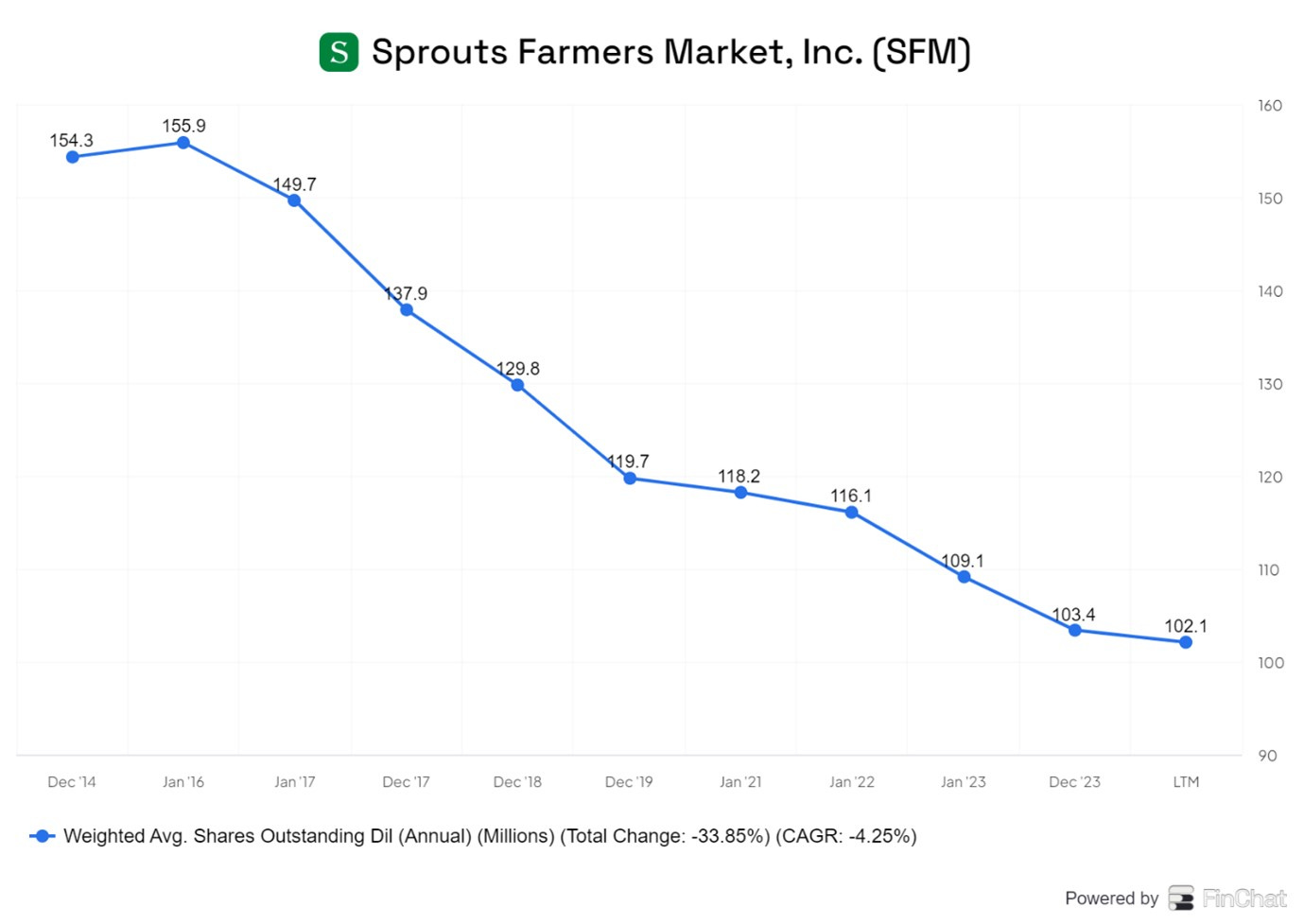

No of Shares Outstanding

Thanks to the share repurchases, the number of share outstanding have fallen from 154mn in 2014 to about 102mn currently- this represents a CAGR decline at an impressive 4.25%.

Stock-based Compensation

This is relatively low ($ 18.3mn in FY 2023) and seem to be constant at about 5% of Operating Income.

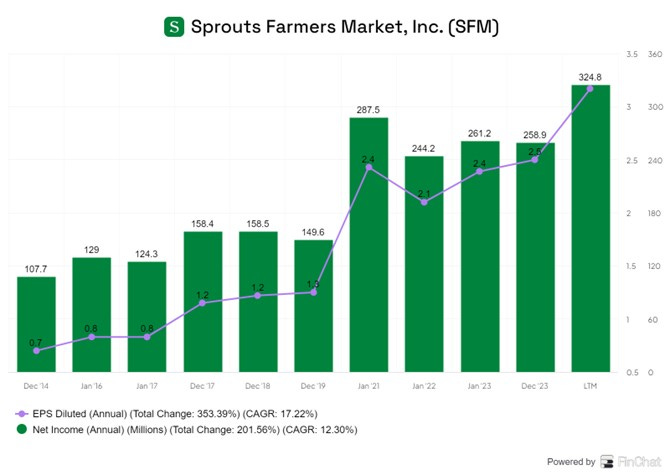

Net Income and EPS growth

Net Income has grown at a CAGR of 12.3% but EPS as grown faster at 17.2% CAGR thanks to the 4% CAGR reduction in number of shares.

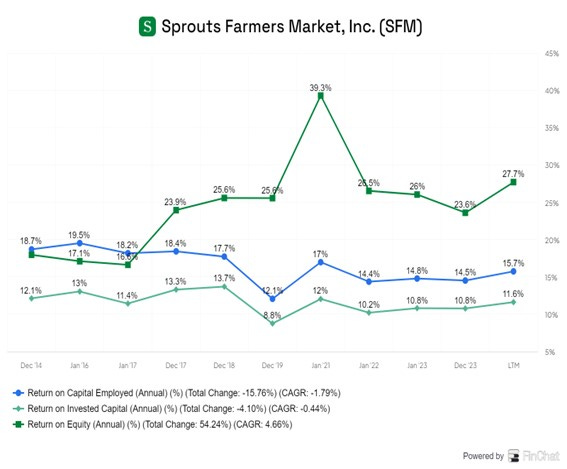

Profitability

The ROE of the company is currently at 27.7%

The company places an emphasis on Return on Investment Capital (ROIC)

“ROIC is an important measure used by management to evaluate our investment returns on capital and provides a meaningful measure of the effectiveness of our capital allocation over time.”

ROIC is at 15.7%

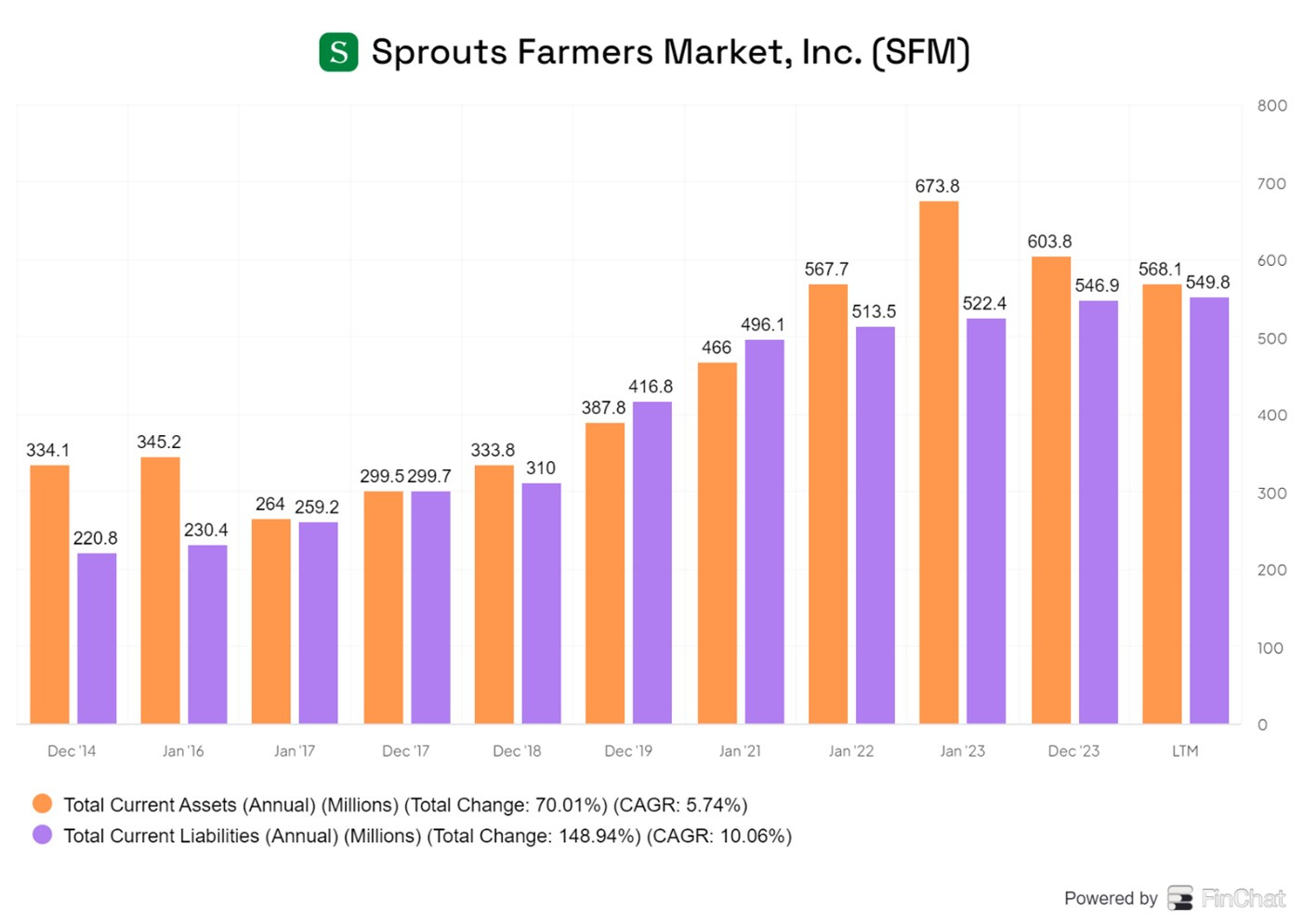

Balance Sheet

Current Assets are broadly in line with Current liabilities. As noted above, SFM has no long-term debt.

Summary of Numbers

In summary, the company has been a strong performer, steadily growing revenues, operating profits and free cash flow and achieving a high level of profitability.

Other aspects of SFM’s business

Competition and Pricing

Competition.

As noted above, the company tries to avoid competition with the large grocers such as Walmart and Kroger by having very little overlap with them in their offering or “assortment” as they term it.

More relevant competitors include Amazon Wholefoods, Trader Joe’s and perhaps Costco as well as many regional and local chains. As of March 4, 2019, Amazon Whole Foods has more than 500 stores in North America and seven in the UK.

This extensive post compares the two stores but struggles to find significant difference between them. Traders Joe’s (TJ) started in 1967 and has stores in 40 states and judging by the website, an active programme of regular new store openings. It is a privately-held company. They do not have an online offering and do not work with 3 parties like Instacart.

Like SFM, they do not have discounts of coupons. This post compares the two stores.

“Our Social Media Survey “Sprouts Vs. Trader Joe’s…Which is better” showed that both stores are pretty popular and LOVED for different reasons. Trader Joe’s takes the lead when talking about cheaper prices, variety, and accessibility (referring to more locations). Wine LOVERS also like Trader Joe’s wine! On the other hand, Sprouts Farmers Market takes the winning place for product quality.”

After some quick research on the internet, We concluded all three stores seems to have a similar offering.

SFM claims a price advantage on Organic products which account for 45% of their total sales.

“Our conventional produce gap are closer or significantly cheaper, but we're even more significantly cheaper on organic projects. when you're operating with a focus on conventional produce in the conventional supermarket space, you have to invest your margin in conventional, which means you have to make your margin up in organic, which creates a gap for us in the marketplace.”

Buying model

SFM has a hybrid produce-buying model, centralized in regional teams which allows some local flexibility in responding to market changes. SFM has developed meaningful farmer partnerships, which deliver new variety and favourable pricing to customers.

SFM is also involved in the “Rescued Organics “program, which is designed to reduce food waste and support farmers. In the GS Retail Conference they mentioned a new concept called the Foraging Team.

“The foraging team was we had this vision of the truffle pigs in the forest of Slovenia kind of sniffing about looking for product that nobody else can find….We've got a wonderful team of people who basically go out pitch to some … a lot of really innovative food entrepreneurs in the U. S.”

The also believe they are differentiated in the sourcing of Organic Products.

“Our organic sourcing projects are different, giving longer term commitments to growers, giving longer term commitments to the product is allowing us to get into this kind of three-way benefit. The customer gets a good deal on organic produce. The farmer knows how can make money because he's got longer term commitments and we can make a good margin at a competitive price and that's the kind of dynamic that we've got into an organic produce and feel very strong about that going forward.”

Own Brand

SFM has its own brand that it’s building up for some proprietary products. It appears to have built up the private-label brands penetration to a significant level. These products are exclusive to SFM.

Future Trends

They key future trend is more stores. The company believes they can expand from 417 stores to about 1100 stores in the United States. This is an additional 700 stores and is a huge runway

The immediate pipeline is strong.

“And we've got a really strong pipeline over 110 sites that we've approved already and 70 signed leases.”

The existing 407 stores is large footprint and this gives them an immediate brand recognition when they open in new locations. However, in other areas, they are still unknown and this is viewed as a positive factor.

“The biggest thing that's encouraging us is that the places where we're not that when we open in Arizona or we open in Southern California, a lot of people know who we are. When we open in places like Aberdeen, New Jersey, everyone goes, well, who are these guys?”

Their stores are located in the “smile” of America * (Both coasts plus the southern belt). They still have a lot of scope to put more stores in the “smile”.

“even though we have a lot of stores in California, there's still plenty of white space there. Mid Atlantic, for sure, will be a place that will be growing a lot in the next few years. And then there's still a lot of good infill opportunities, Florida, Texas, Arizona, Colorado, those are places where we still have stores to go. Miami, in particular, in Florida will be another good growth market for us.”

They estimate they have three years of growth in the “Smile” before they look at the mid-west.

“So the next, call it, 3 years, 3 years plus, we have a pretty good path in the smile of America... And then eventually, we'll need to get over into the Midwest, where there's a big white space opportunity for us as well.”

“And what's been really encouraging is we look at places like Florida where, call it, 4 or 5 years ago, we had 15 stores and we're approaching 50 now. We've seen really good performance and good results.”

SFM has long runway. If we assume they add 20-25 stores per annum on average they have at least 7-8 years of store growth as it would bring them to about 800 stores then. They assume that the US has room for 1100 stores and after that they can look at overseas expansion.

The planned expansion will require the capital expenditure programme to ramp up over time. That will lead to further revenue and cash generation.

Moat

Does SFM have Moat? If yes, what are the characteristics of the moat?

SFM probably does have a Moat but it is difficult to assess how strong it is. Let us consider the possible elements of the moat.

They have a large established presence in this market and have a known and trusted brand.

They have a strong cash generative business model where they can fund store growth and buy back shares without debt (other than leases)

SFM’s offering and store format seems to be attractive and effective.

The fact they have grown strongly despite competition from Amazon Wholefoods and Trader Joe’s is indicative of a Moat.

It is possible that Walmart, Kroger or Target could make an aggressive push in the health food and organic business. However, given the scale of their conventional groceries business, it is unlikely they will be able to develop different culture required.

SFM most likely has a sufficient moat to ensure many years of strong profitable growth.

The Analysts’ Views

According to Reuters, the average stock forecast for SFM in the next 12 months is $98.1. This price target corresponds to a downside of 11.14%. The range of stock forecasts for SFM is $43.4 - $131.3. Based on the ratings of 20 analysts, the consensus recommendation for SFM is Hold

Valuation

Let us build a “back of the envelope” valuation model for SFM based on recent historical trends and the information we have outlined above.

SFM is likely to grow new store numbers at about 5%-8% per annum and same stores sales are likely to grow at an average of 3% to 5%.

Total Revenues can easily grow at about 9-10% a year. Operating income is likely to grow at about 9-10% per annum.

Based on the performance of the last ten years, this is likely to translate to Net Profit growth of 12% to 14% CAGR.

Given that SFM buys back 4% of outstanding shares annually, EPS growth is likely to be 15% to 18% per annum

The consensus analysts’ forecasts for revenues are as follows:

The analysts expect total revenues to grow at about 9% to 10% per annum over the next three years.

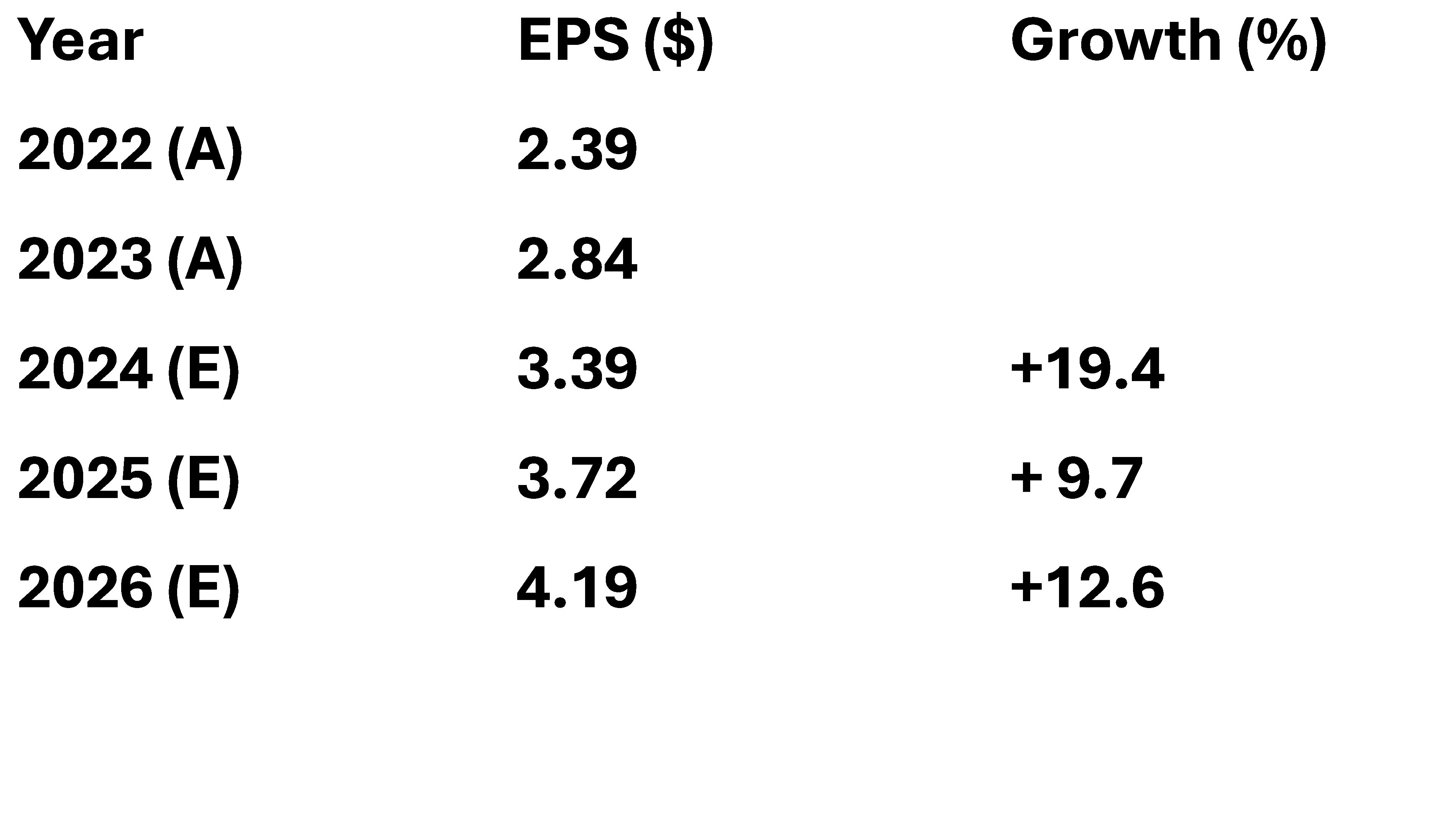

The consensus analysts’ forecasts for EPS are as follows:

The consensus analysts’ forecasts for Free Cash Flow (FCF) are as follows:

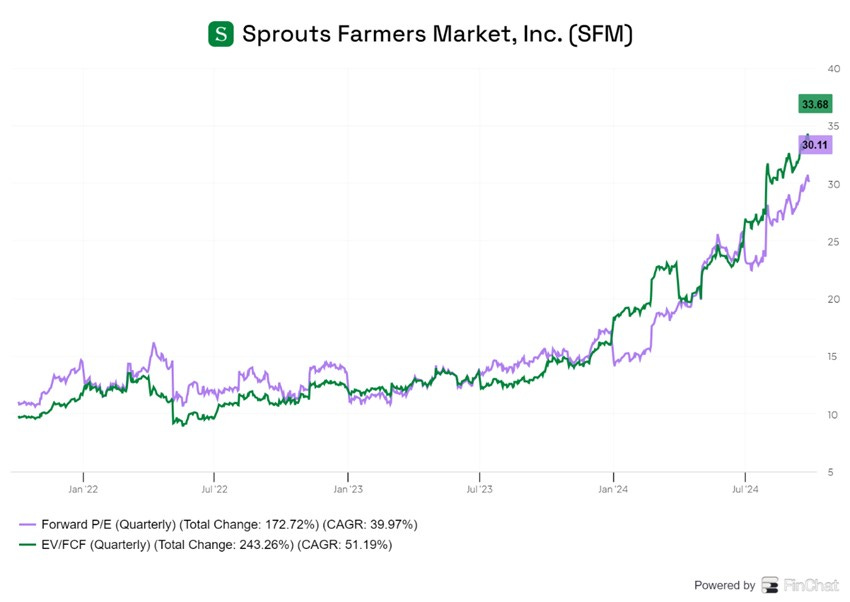

At the current price of $110, the SFM stock is trading at a three year forward P/E Ratio of 26X. This feels like it is fairly priced, given the ROE of 27.7%

At the current market cap of $11bn, the stock is trading at a two year forward Price to Free Cash Flow Ratio of 33X.

These numbers imply a three-year forward earnings yield of 3.8% and free cash flow yield of about 3.0%. These are reasonable yields given current interest rates but should ideally be a little higher and closer to 4%.

DCF calculation

We conducted a Discounted Cash Flow (DCF) Calculation.

Assumptions

We made following revenue assumptions.

We make the following additional assumptions. On operating margins, we assume the following:

We also assume a risk-free rate of 3.5% and a Market Risk premium of 5.0%. The stock Beta is 0.6 according to Finchat. These numbers imply a low Weighted Average Cost of Capital (WACC) of 5.5%. Finally, we assume that in FY 2028, the terminal exit multiple for EV/FCF is 26X.

DCF Results

With all these assumptions, we calculated a theoretical value of $ 89.2 per share – a 17% discount to the current value of the stock of $ 110.

If we increase the assumed EV/FCF to 32X , we get a theoretical value of $ 109 per share.

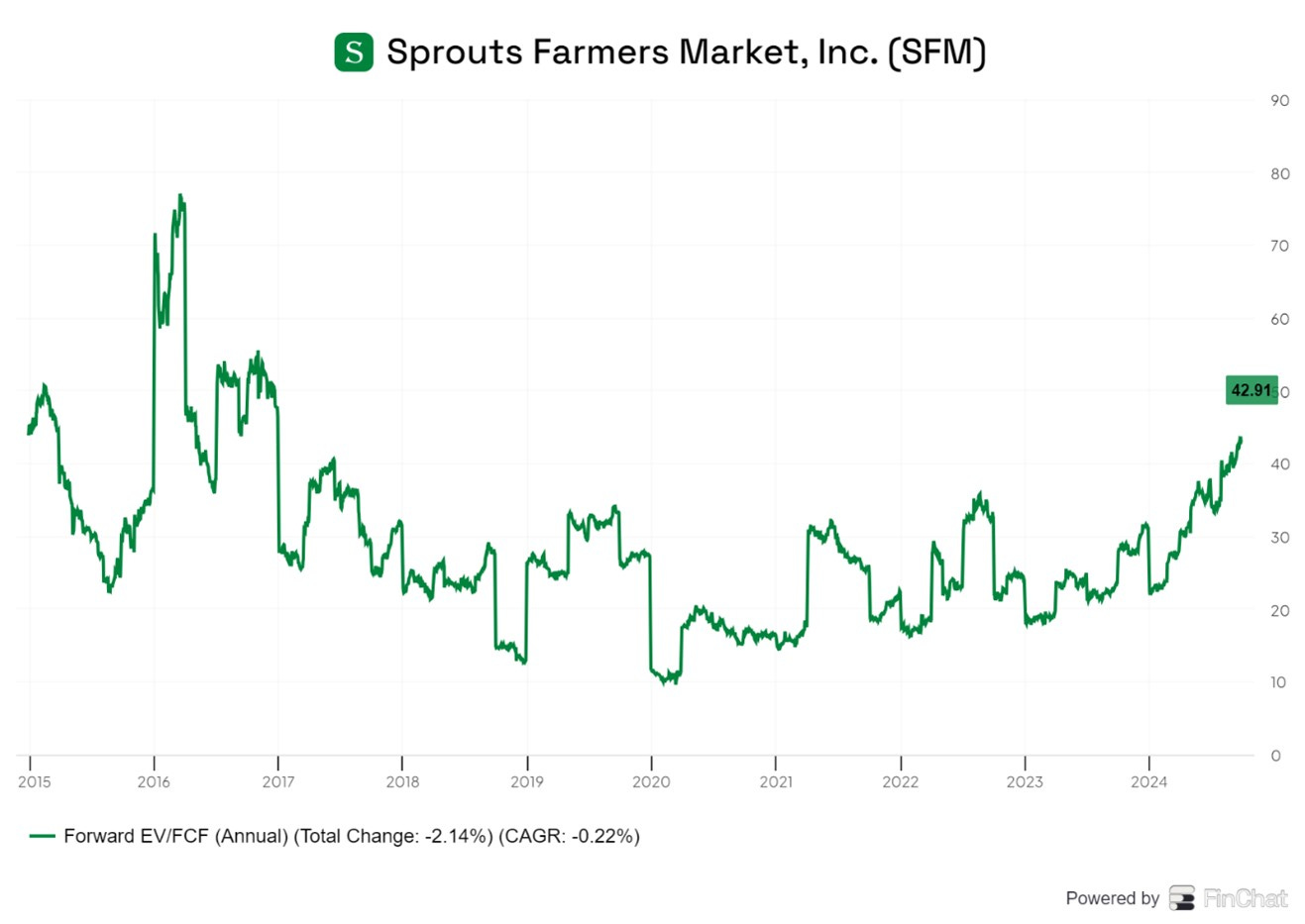

The chart below shows the historic trading level of the forward EV/FCF ratio. Based on this, our judgement is that an assumption of an EV/FCF ratio of 32x is a little aggressive. The originally assumed 26X is a much more reasonable level.

The stock has advanced 88% in the last 1 year and perhaps not surprisingly, the shares are now not trading at level which can be considered cheap.

Conclusion

In our view all fundamental equity analysis comes down to two questions.

1. Is the company under consideration, fundamentally a good business

2. If it is a good business, is it available at a fundamentally attractive price.

In the Case of SFM, the answers are Yes and Maybe respectively .

In this article, we have outlined why we think SFM is a good company.

However, the shares at $110 per share are trading at too high a level

One strategy would be to wait patiently (Patience is a virtue!) until the share price to fall back towards $ 90 per share.

The alternative strategy would be to buy a nominal 1% of the portfolio and look to add to the stock if it fall to $ 90 per share.

We have decided to follow the second approach and invested 1% of our portfolio in SFM.