Taiwan Semiconductor Manufacturing Company (TSMC) - US ADR (TSM)

Leading Leading-edge Chip Manufacturer to the World.

Introduction

This note on TSMC is one of a series on Semiconductor Companies. We will start here with a general introduction before we look at TSMC.

The Chip Industry

The Silicon Chip Industry has been one of the fast growing and technologically dynamic industries of the past 40 years. The speed of advances have been extraordinary, the pace of product development breath taking, and the rise in the complexity of manufacturing has been phenomenal.

I should refer here to Chris Millar and his book “Chip War” which is essential reading for anyone who want to understand the industry. Miller wrote the following:

“Last year, the chip industry produced more transistors than the combined quantity of all goods produced by all other companies, in all other industries, in all human history.”

In the early days, the chip industry was focused mainly on providing memory chips for mainframe computers which were often the size of a house. In 1981, after IBM introduced the first Personal Computer (PC), the industry was driven by providing Central Processing Units (CPUs) and memory chips for Desktop PCs. Later, specialist Graphic Processing Units (GPUs) demand increased as Gaming, through PCs and specialist consoles took off in a big way.

The advent of smartphones, the spread of the Cloud (and the consequent rise of huge Server Farms/ Datacentres) has driven demand for chips. The pace of change in the industry will only accelerate is not going to slow down due to several key trends:

· the increased digitalisation of work

· the growth of High-Performance Computing (HPC) driven by GenAI

· the development of the Internet of Things (IOT)

· the introduction of 5G mobile networks and

· the rapid growth of Electronic Vehicles (EVs) and Autonomous Vehicles (AV).

These trends will combine to greatly increase the demand for chips in the next 20 years. The pace of change in the industry is likely to accelerate. Chips will not be confined to our Computers, Phones and Games Consoles – they will be everywhere and in everything - we will truly be in an era of “Chips with Everything”

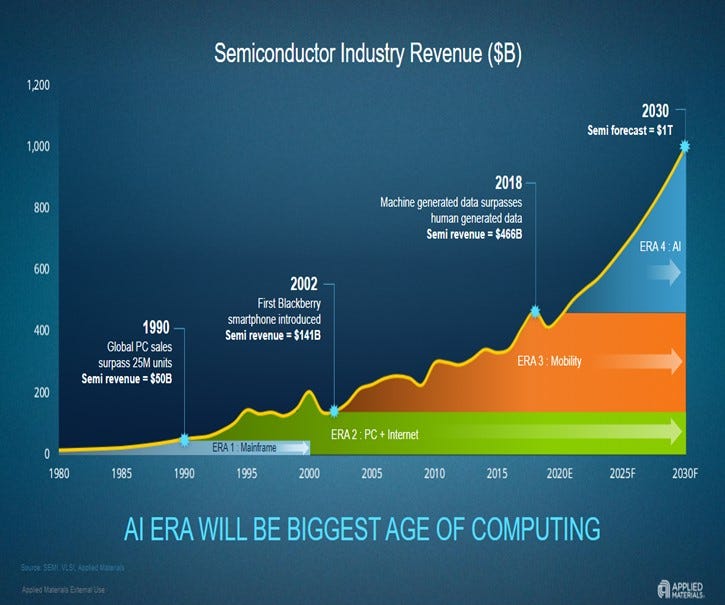

The US Chip capital equipment supplier, Applied Materials (AMAT) calls this period the “Fourth Era of Computing”. In their view, the first three Eras of computing were driven by Mainframe, PC (+ Internet) and mobile telephony, respectively. The Fourth Era will be driven by the application of Artificial Intelligence (AI). AMAT believes the Fourth Era will be the biggest and will drive semiconductor industry revenue from the 2020 level of US$ 500bn to US 1trn in 2030.

Source: Applied Materials Inc

The Chip Industry and its heroes

The chip industry has developed a broad ecosystem over the last five decades and spawned many interesting companies in a range of sub-sectors such as Chip Design, Chip Foundries, Capital Equipment, Testing, Yield Management, Electric Design Automation (EDA).

Today, the sector is characterised by limited manufacturing capacity and a hugely increased capital expenditure programme. Demand is set to grow more rapidly due to the reasons noted above.

The story of Chips has great heroes such as Robert Noyce, Gordon Moore, and Andy Grove who founded and powered Intel to become one of the most powerful companies especially in Computer Processing Units (CPUs). Morris Chang is another hero of our story. He worked with the Taiwanese government to found Taiwanese Semiconductor Manufacturing Co (TSMC) in 1987, which has become the largest and most technologically advanced manufacturer of chips. In its ascent, TSMC’s manufacturing capability has humbled the mighty Intel.

TSMC played an important enabling role in helping to transform the world in the last 25 years. It showed that contract manufacturing of the most advanced chips at scale was a viable business model. TSMC facilitated the creation of many new companies, as talented chip designers and engineers started new capital-light companies which could focus exclusively on innovation, chip design and development. This was possible as could to outsource the capital-intensive manufacturing to companies like TSMC and Samsung Electronics. The successes of companies like Nvidia, Qualcomm, Broadcom and Apple are, to an important degree, built on the success of TSMC.

Another hero is Jensen Huang of Nvidia which transformed the business of Graphic Processing Units (GPUs) and changed the experience for a growing army of computer gamers. Nvidia has subsequently successfully targeted datacentres, large companies and crypto miners and is riding the AI wave and anticipating the boom in Electronic Vehicles (EVs) and Autonomous Vehicles (AV)

Another hero or heroine is Dr Lisa Su, who has turned Advanced Micro Devices (AMD) from a perpetual runner-up to Intel in CPUs to a strong and credible competitor. Under Dr Lisa Su, who is Jensen Huang’s cousin, AMD has diversified away from its dependence on lower-end CPUs to develop advanced GPUs and CPUS for high-end servers and high-performance computers.

In the last four decades, the power and capacity of chips has increased exponentially without any increase in power consumption or chip size.

The cost and complexity of the manufacturing process has also increased exponentially. The process of manufacturing advanced chips is the most complex and technologically difficult manufacturing process. This has created opportunities for capital equipment suppliers to chip manufacturers such as Applied Materials (AMAT), Lam Research (LRCX) and KLA Corp (KLAC) (all USA) and ASML Holding (Netherlands) among others.

The story now increasingly has strong geopolitical aspects. Many governments and military experts have belatedly realised that a high percentage of the most valuable productive capacity in this strategic industry (Chips are vital for weapon and defence systems) is in China, Korea, and Taiwan -areas which are vulnerable to a more militaristically aggressive China.

The United States, The European Union, Japan, Singapore, Malaysia, and India are rolling out new policies to provide financial incentives to companies to invest in semiconductor manufacturing capacity within their borders.

China is also investing heavily to develop its own Chip industry as it seeks to reduce its dependence on the USA, Korea, Taiwan, and others. It has invested billions of dollars into many companies such as SMIC, Yangtze Memory and many others as it tries to build it capacity in all stages of chip development and manufacturing.

The current boom in investment is likely to be maintained for the next decade. I

In 2018, the amount of data generated by machines surpassed human generated data for the first time.

On the 14th March 2023, Chat GPT4 was first released to the world. This marked the beginning of the Gen AI boom.

Chat GPT4 was a huge improvement on its predecessors including improved understanding and Generation and better capacity to process and generate images as well as text.

It has kickstarted a boom in the creation of new Large Language Models (LLMs) from companies like Alphabet, Meta and a host of new start-ups such as Perpleixty.ai and xAI, founded by Elon Musk.

The unfolding GenAI revolution would not have been possible without chips, computers and software provided by Nvidia. The GenAI revolution will have a huge impact on the chip industry

“I've never seen any technology advance faster than this. Artificial intelligence compute coming online appears to be increasing by a factor of ten every six months. Obviously, that can’t continue at such a high rate forever …the chip rush is bigger than any gold rush that has ever existed.” Elon Musk

NVIDIA is already TSMCs second largest customer by revenue. The GPUs it builds are bound to play an outsized role in setting the foundry process and packaging technology cadence and roadmap at TSMC.

“There’s about a trillion dollars’ worth of installed base of datacentres. Over the course of the next four or five years, we’ll have two trillion dollars’ worth of datacentres that will be powering software around the world.” Jensen Huang, January 2024

In the last quarter, three large Cloud Service Providers SPs (Amazon, Microsoft, and Google) plus Meta Platforms, have announced plans for total capital expenditure of $ 200bn+ per annum for the next two years at least.

Most of this will be datacentre investment and will go principally into giant Datacentres which will require, among other things, Servers, Chips, Networking Tools and Services and Power Capacity.

In terms of Chips, the big winner has been Nvidia which has an 85% to 90 % market share in the GPUs for the new datacentres which will meet the exploding growth for GenAI workloads.

In summary, there are huge opportunities for investors in the next few years to make substantial gains as the use of GenAI and other technological progress drives the use of chips well beyond Computers, Mobile and Gaming Devices and Datacentres to the Connected Home, the Automated Factory and Power Station and Electric and self-driving vehicles. Fortunes will be made in both existing companies and emerging ones.

These are some key listed companies in the sector.

Advanced Micro Devices, ARM Computer, ASML, Broadcom, Entergis, Global Foundries, Infineon, Intel, KLA, Kulicke & Soffa Industries, LAM Research, ADI / Maxim Integrated, Marvell Technology, Microchip Technologies, Micron Technology, Motorola Solutions, Nvidia, NXP Semiconductors, Qorvo, Qualcomm, Renesas Electronics, Samsung Electronics, SK Hynix, Skywater Technology, SMIC, Synopsys, STMicroelectronics, Teradyne, Texas Instruments, Taiwan Semiconductor, Ultra Clean Holdings, United Micro Electronics, Yangtze Memory, Wolfspeed.

We hope to look at many of these in the coming days.

Taiwan Semiconductor Manufacturing Company (TSMC)

Nvidia may be designing the most advanced GPUs, computers and software, but their GPUs are manufactured by Taiwan Semiconductor (TSMC).

The history of TSMC is the history of one man. Morris Chang

Intel and AMD dominated the CPU industry in 1970s to 1990s with an integrated model where they both designed and manufactured chips. However, as chips became more powerful, and complex, the capital cost of manufacturing rose exponentially.

The various Intel/ AMD developed chips were “general-purpose” processors. Processors created for a specific task would, in theory, be much faster but it was a big gamble for a business to focus on “niche” chips given the greater uncertainly of demand and the small size of the market relative to high capital cost of manufacturing.

Morris Chang, a Taiwanese American, was a long-time executive at Texas Instruments (TI) which had been an early pioneer in integrated chips. Chang observed in the 1980s that it cost $50- $100 million dollars to start a new chip company, primarily because of the cost of manufacturing. You could sub-contract production to Intel, Texas Instruments or Motorola, but it wasn’t reliable — and they were also potential competitors who could steal your chip designs.

Morris Chang in 2017. Image Source: Wikipedia

In 1987, Chang was invited to Taiwan, and asked to put together a business plan for a new government initiative to create a semiconductor industry. Chang recalled later that he did not have much to work with. It is worth reproducing most of this interview.

“I paused to try to examine what we have got in Taiwan. We had no strength in research and development, or very little anyway. We had no strength in circuit design, IC product design. We had little strength in sales and marketing, and we had almost no strength in intellectual property. The only possible strength that Taiwan had, and even that was a potential one, not an obvious one, was semiconductor manufacturing, wafer manufacturing. And so, what kind of company would you create to fit that strength and avoid all the other weaknesses? The answer was a pure-play foundry.

In choosing the pure-play foundry mode, I managed to exploit, perhaps, the only strength that Taiwan had, and managed to avoid a lot of the other weaknesses. Now, however, there was one problem with the pure-play foundry model, and it could be a fatal problem which was, “Where’s the market?”

The approach was very much, build it and they will come

TSMC effectively created the market by

“Enabling independent, non- integrated organizations to sell, buy, and assemble components and subsystems.”

Specifically, Chang made it possible for chip designers to start their own companies as they could outsource the high capital cost of manufacturing to TSMC.

“When I was at TI and General Instrument, I saw a lot of IC [Integrated Circuit] designers wanting to leave and set up their own business, but the only thing, or the biggest thing that stopped them from leaving those companies was that they couldn’t raise enough money to form their own company. Because at that time, it was thought that every company needed manufacturing, needed wafer manufacturing, and that was the most capital-intensive part of a semiconductor company, of an IC company. And I saw all those people wanting to leave but being stopped by the lack of ability to raise a lot of money to build a wafer fab. So, I thought that maybe TSMC, a pure-play foundry, could remedy that. And, as a result of us being able to remedy that then those designers would successfully form their own companies, and they will become our customers, and they will constitute a stable and growing market for us.”

The large existing companies such as Intel and Motorola would only let you manufacture their wafers only when they didn't have the capacity, or when they didn't want to manufacture the stuff themselves anymore. When they didn't have the capacity, and asked you to do the manufacturing, then as soon as they got the capacity, they would stop orders to you, so it couldn't be a stable market. You only got the loss- making crumbs

So, the conclusion at that time, the conventional conclusion was that there was no market. Maybe this idea, this pure-play foundry idea, exploited the only strength you have, which is manufacturing, but there's no market for it. That's why it was so poorly thought of. What very few people saw, and I can't tell you that I saw the rise of the fabless industry, I only hoped for it. But I probably had better reasons to hope for it than people at Intel, and TI, and Motorola, etc because I was now standing outside. The fabless industry really started in about 1991 and 1992 and today there are hundreds of, maybe close to a thousand fabless companies in the world.

Despite all the uncertainty around the business model, the Government of Taiwan decided to fund half of the $220mn funding Chang decided to raise for his new company. 8% of the fund came from Philips, the same company that started ASML (a joint venture between ASM and Philips). The rest ~22% was raised from various business leaders in Taiwan who were essentially told by the government to invest in this new company. Taiwan Semiconductor Manufacturing Company (TSMC) was founded in 1987.

In the initial years, TSMC was mostly just manufacturing “leftover” orders from the IDMs, but it was the rise of fabless companies that truly turbocharged TSMC’s growth.

Today’s behemoths such as Nvidia, Qualcomm, and Broadcom all started after TSMC was founded and as none of them had their own fabs, they were looking to outsource their manufacturing to someone else. As the “Fabless” companies grew from just a handful to thousands, so did TSMC’s revenue. TSMC became publicly listed in Taiwan in 1994 at $ 4bn valuation. It later became listed in the US in 1997.

In 2005 when Chang was 74 years old, he decided to retire by handing over the leadership position to Rick Tsai. However, this retirement proved to be temporary as he decided to return to the helm of TSMC at age 78 during the summer of 2009.

While TSMC invested only ~$12bn cumulative capex during 2005-2009 period, they invested a huge ~$40 Bn cumulative capex during 2010-14 period following Chang’s return to the company. They also started a relationship with Apple, TSMC’s largest customer today, which generated ~$18bn of revenue for the company in 2023.

Apple’s COO, Jeff Williams recalls meeting Morris Chang in 2017

“We were not doing business with TSMC at that time, but we had a great conversation. We talked about the possibility of doing stuff together, and we knew the possibilities were great if we could take leading-edge technology and marry it with our ambitions. It seems obvious right now, but it wasn’t then, because the risk was very substantial. The way Apple does business is we put all our energy into products, and then we launch them, and if we were to bet heavily on TSMC, there would be no backup plan. You cannot double plan the kind of volumes that we do. We want leading-edge technology, but we want it at established technology volumes. On the TSMC side, that means a huge capital investment. It means ramping faster than the more careful yield plan that the industry is used to…Together, we decided to take the bet, to take the lead and Apple decided to have 100 percent of our new iPhone and new iPad chips — application processors — sourced at TSMC. TSMC invested $9 billion and had 6,000 people working round the clock to bring up the Tainan fab in a record 11 months, and in the end, the execution was flawless. We’ve gone on to ship over half a billion chips together in that short window, and I think TSMC has invested $25 billion — $9 billion on that first venture — there are very few companies in the world that would spend $9 billion in capital across everything, let alone a single bet. So for that, we thank you, Morris Chang, and everybody at TSMC. It’s been a wonderful partnership. The big challenge we had as we looked at the mobile revolution was this trade-off between performance and power. Even today, Apple is TSMC’s largest customer.

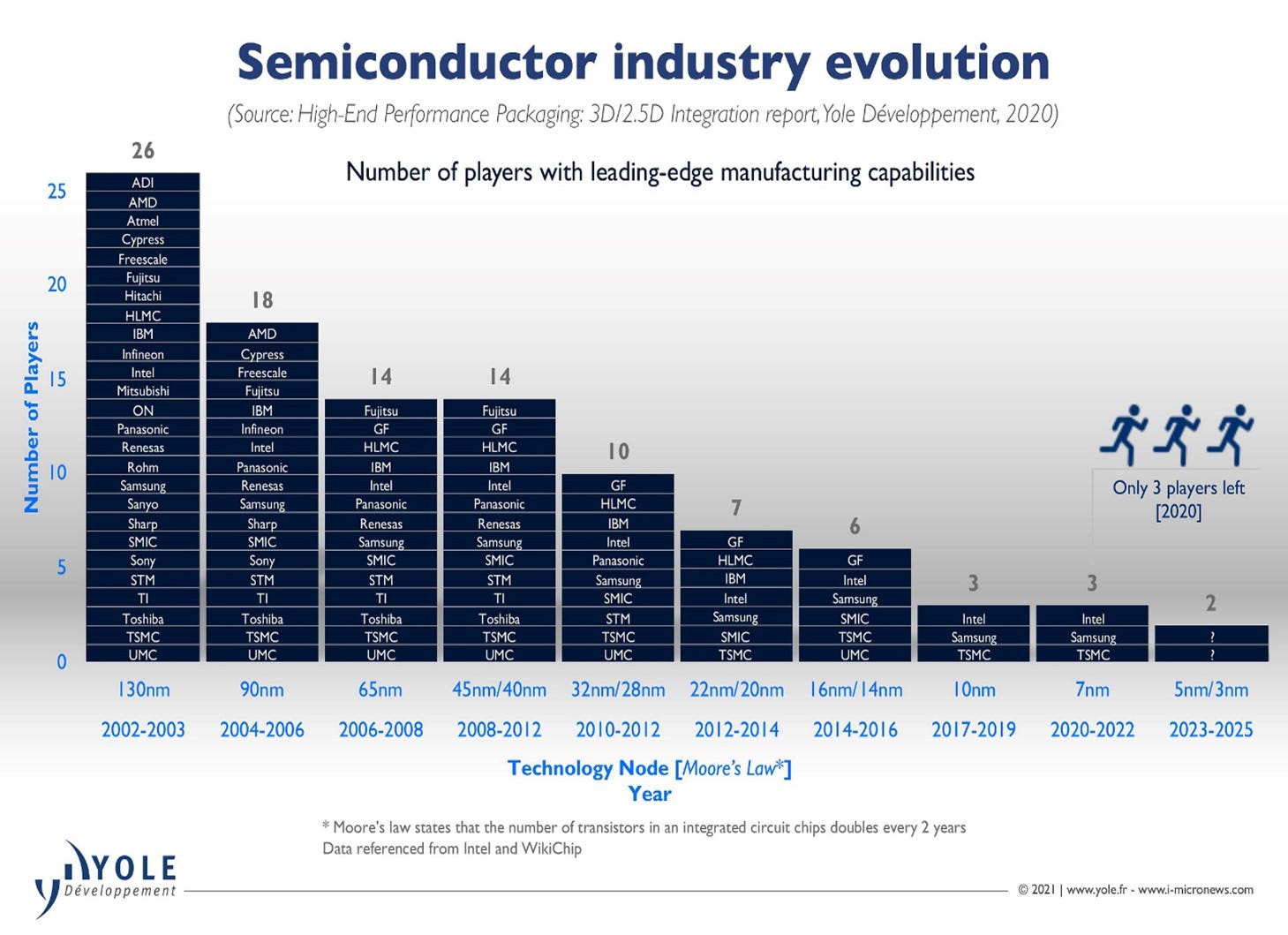

The chart below illustrates the gradual decline in the number of companies capable of manufacturing leading edge chips.

In 2002-2003 the leading edge was 130 nanometres (nm). A nanometre (nm) is one billionth of a meter, or a million of a millimetre. A microchip the size of your fingernail contains billions of transistors. Progress in chip design depends on the ability to squeeze in more and more transistors on the same area of silicon. Nanometre technically refers to the width of the gate on transistors. The smaller the gate. the greater the number of transistors that can be packed in

By 2020 the leading edge in chip manufacturing had shrunk to 7nm and only three players were able to manufacture leading edge chips. These were Intel, Samsung and TSMC.

In 2020, Intel engineering prowess stumbled and only two companies are left at the leading edge: Samsung of Korea and TSMC.

One of the reasons for the winnowing of manufacturers is the sheer complexity of chip manufacturing. For those who are interested, here are links to two videos which explains this in detail. You can watch them in just 20 minutes each at 1.25X speed.

The second related factor is cost. The capital cost of a single chip factory fab can be as high as $10bn and may have a life of no more than 4-5 years. Only the very largest companies can sustain such expenditures.

TSMC today

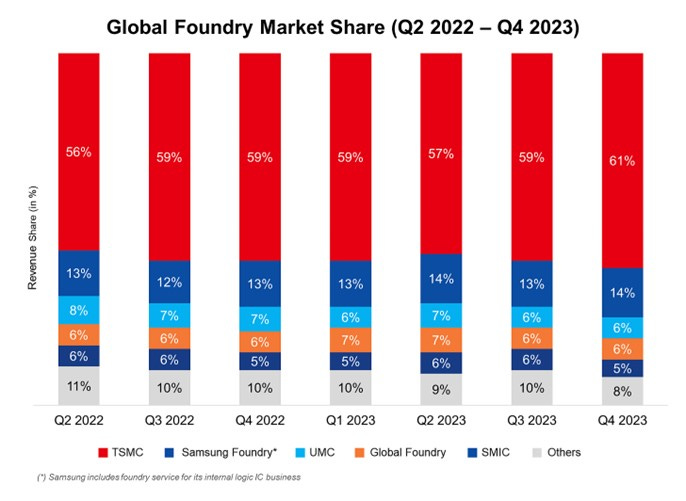

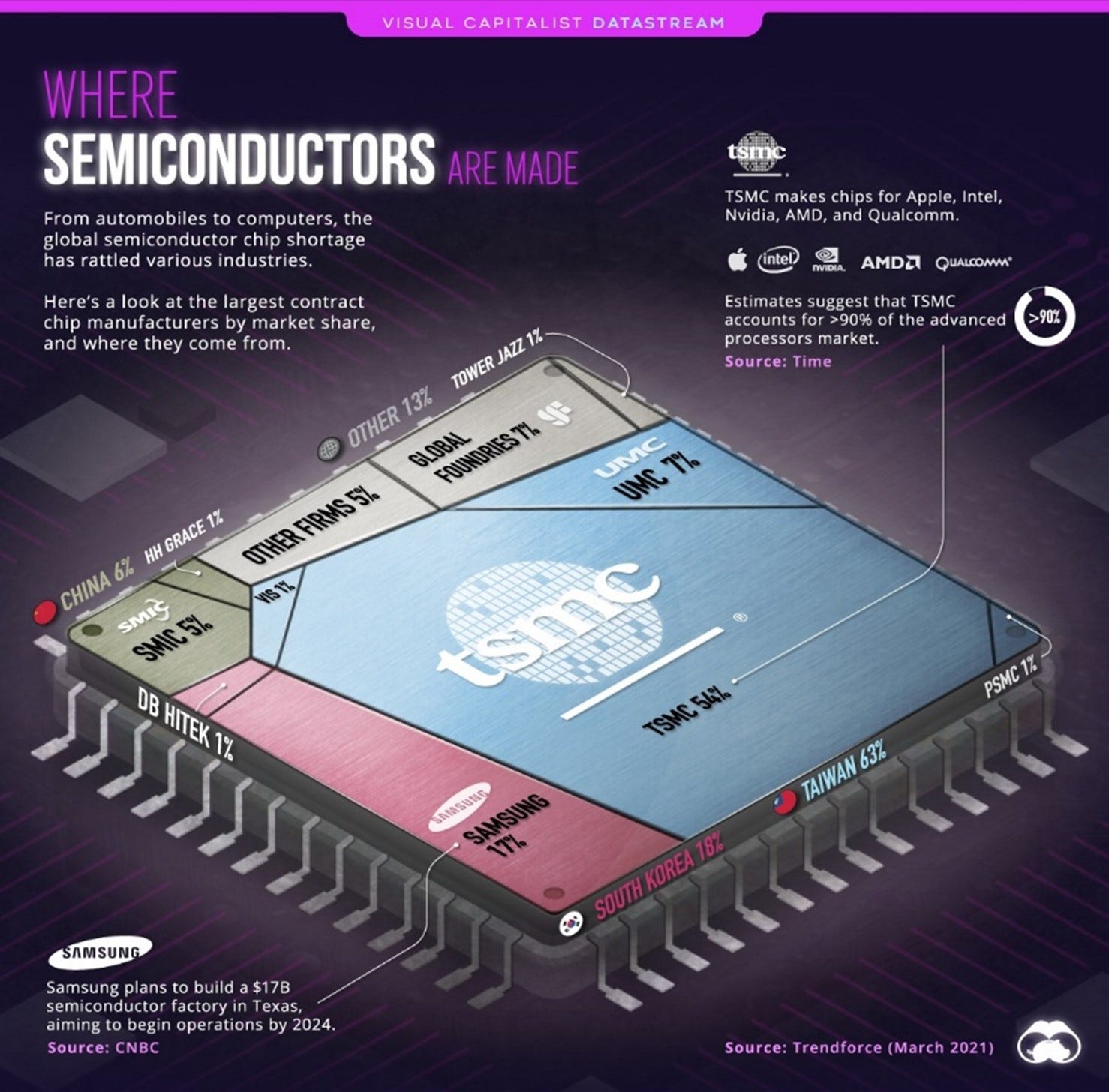

TSMC is the world’s largest contract chipmaker with a roughly 60% market share within contract manufacturing. TSMC share for the most advanced chips is much higher perhaps 85% or more.

Source: Mostly Borrowed Ideas

It is engaged in manufacture, sale and packaging test of integrated circuits and other semiconductor devices, the manufacture of photomasks, as well as the provision of computer-aided design.

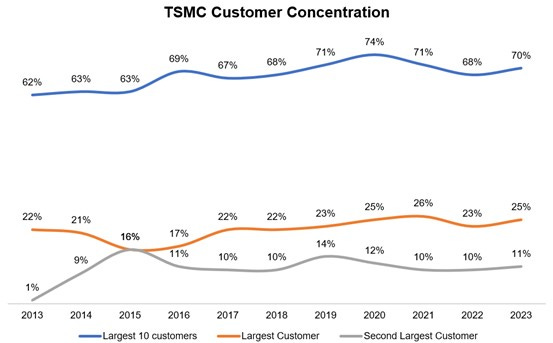

Overall, TSMC makes which make more than 10,760 products using more than 270 technologies for about 500 customers. TSMC customers include AMD, Broadcom, Nvidia, Qualcomm, Hisilicon Technologies Co., Ltd., and Intel. Apple has been a very important customer for the last 10 years and the two companies have grown strongly on the back of the Smartphone and Tablet computer boom. The top 10 Customers account for 70% of TSMC’s revenues.

Source: Mostly Borrowed Ideas

TSMC has factories in Taiwan, China, and the US, and US customers account for about 60% of revenue.

Big foundry competitors are UMC of Taiwan, SK Hynix, and Samsung of Korea and Global Foundries. UMC is a quarter of the size of TSMC, Samsung uses much of its chip output for its own devices while Global Foundries and SK Hynix are less advanced than TSMC.

The Company's products are used in PCs and peripheral products, information applications, wired and wireless communication systems, industrial equipment, consumer electronics such as digital video disc players, digital TVs, game consoles and digital cameras.

TSMC’s semiconductor foundry services and revenues focus primarily on leading-edge process technology (16nm or smaller) but the company also maintains a significant presence in the market for trailing-edge or mature process nodes (20nm or larger). In the latter case, the foundries are older but fully depreciated and are reliable cash-flow generators.

TSMC and Samsung Foundry are currently the only two foundries that offer leading-edge processes to customers. Intel is in the process of re-entering the foundry services market (i.e. providing the services of its foundry to other members) as part of the strategy outlined by CEO Pat Gelsinger.

TSMC has changed the composition of its revenues and moved up the value chain in recent years. In 2015, ~90% of revenues were from trailing edge. In 2021, 60%-70% of the revenues are from the leading edge.

While supporting customers at the leading-edge is more capital intensive, it has allowed TSMC to benefit from much higher growth rates, leading to outperformance vs peers and steady market share gains in the past few years.

Currently, the global chip industry faces a shortage of capacity and TSMC sees huge excess demand. Companies like Nvidia, Intel, AMD, Qualcomm, Apple, Amazon and many others are competing to get a share of TSMC’s capacity.

TSMC is planning for much higher capital investment. Chipmaking capacity does not come cheap – a new leading edge fabrication plant does not leave much change from $10bn.

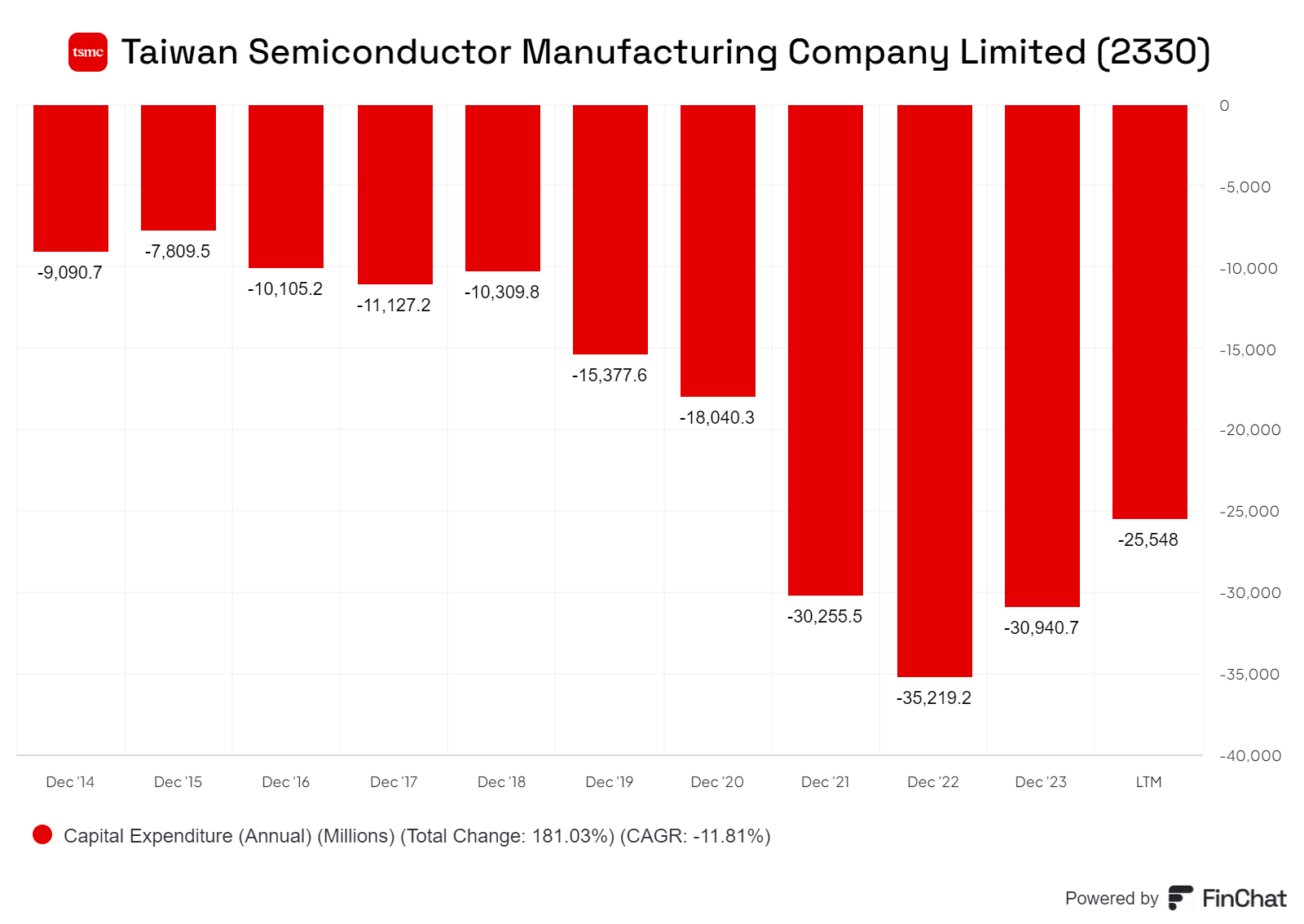

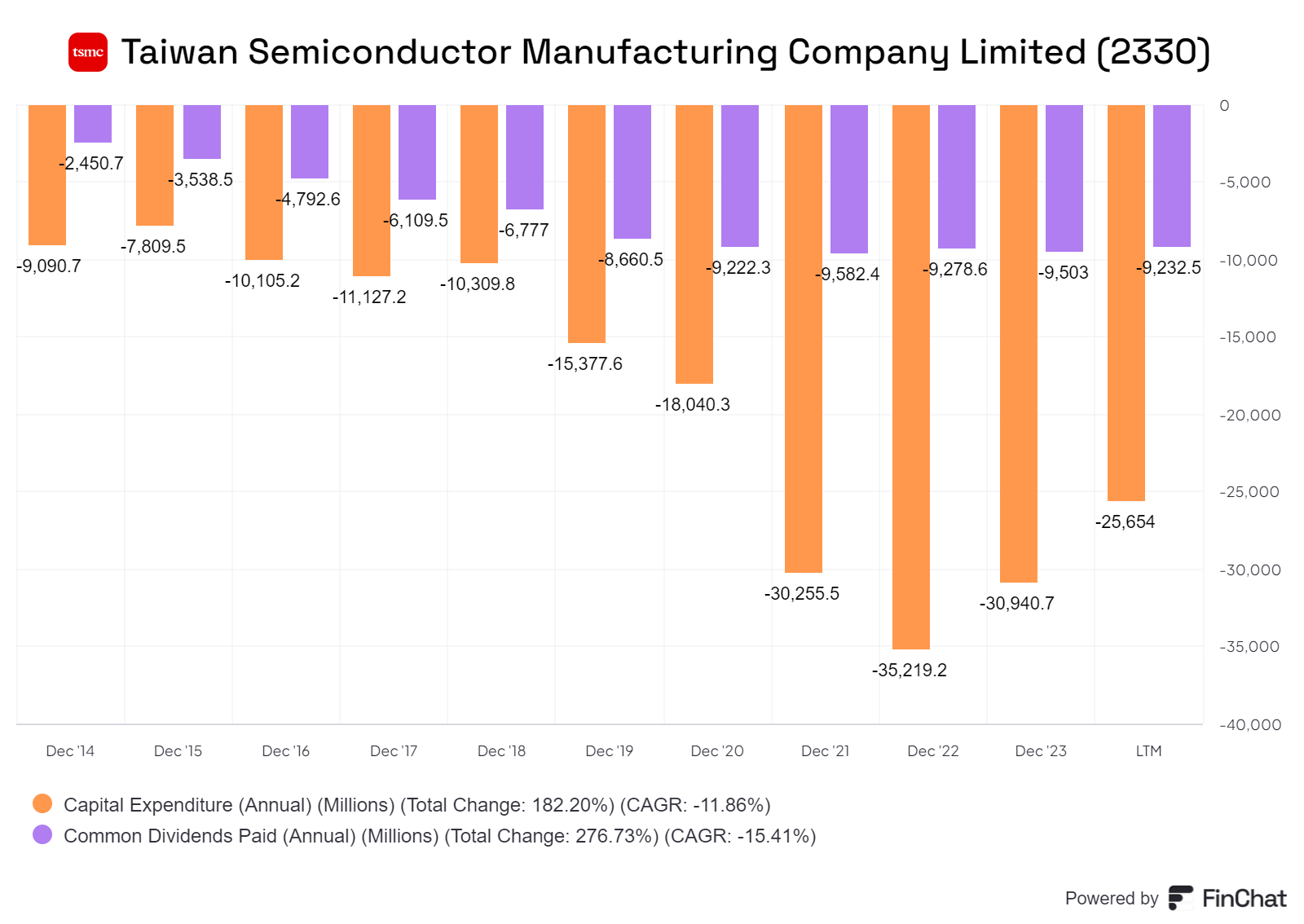

Since 2021, TSMC’s capital expenditures have been $30bn plus per annum with 80% allocated for the leading-edge. This is shown below. It is a negative number as it is a cash outflow.

The Performance of TSMC

From unpromising beginnings, TSMC has become the best contract chipmaker/pure play foundry in the world. Since October 1994, stock investors in TSMC have seen a CAGR return of 16.4% in US$ terms giving a total return 8828%. In the last ten year the return has been about 25%.

This is especially impressive when one considers the capital-intensive nature of their business. Their total annual revenues have increased from just USD 170mn in 1991 to about USD 70bn currently. Morris Chang’s creation has become one of the best corporate success stories in Technology. To learn more about Mr Chan and the history of TSMC, an Acquired podcast on this worth listening to. It can be found here. https://www.acquired.fm/episodes/tsmc

TSMC: A Financial snapshot

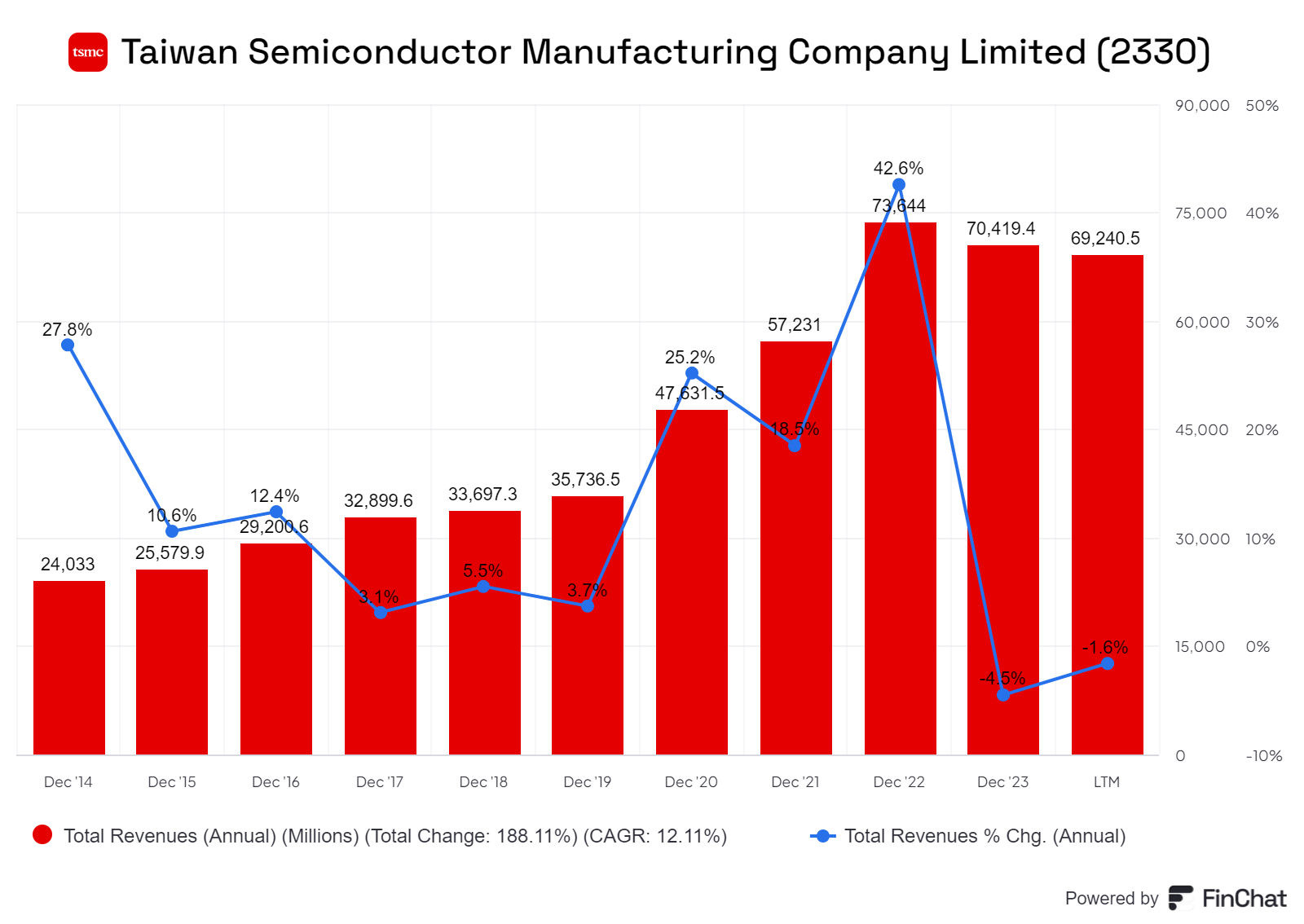

Annual revenues have grown from ~$24bn in 2014 to ~$70bn currently. CAGR growth of about 15%.

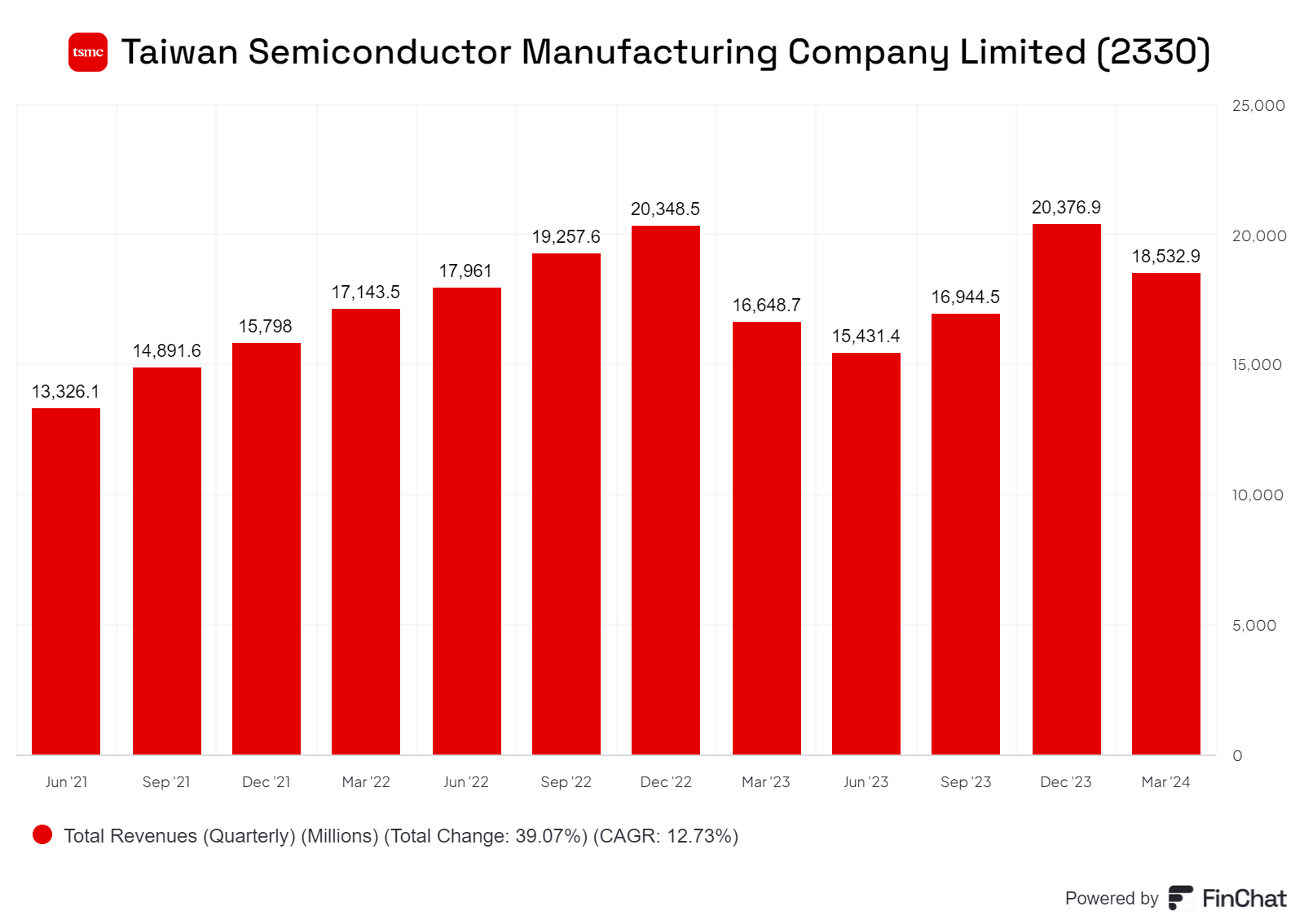

The quarterly run rate of revenue is about $ 18bn. There is some seasonality as the December quarter shows a peak (~$ 20bn).

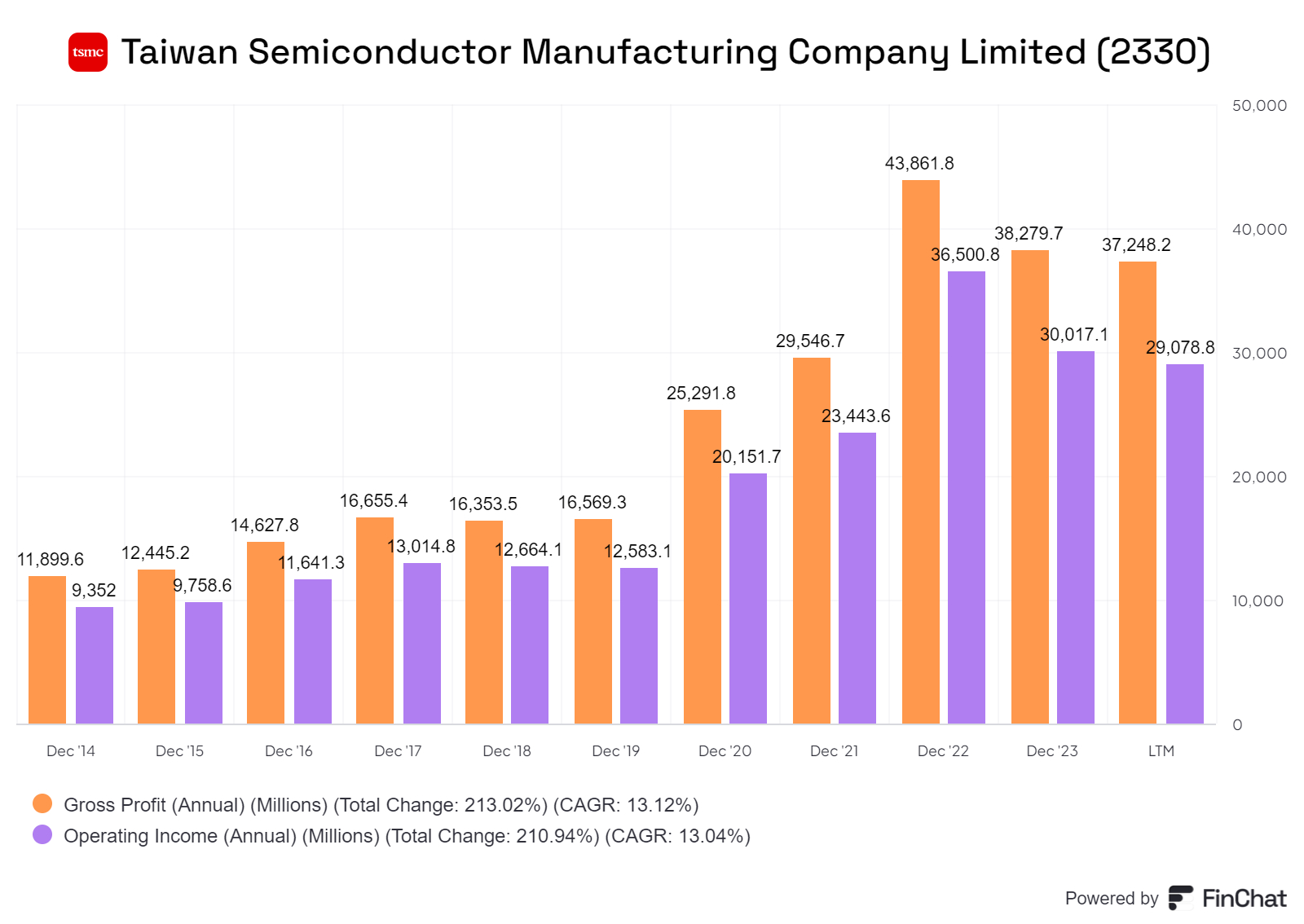

2023 Gross and Operating Profit were $38bn and $30bn respectively.

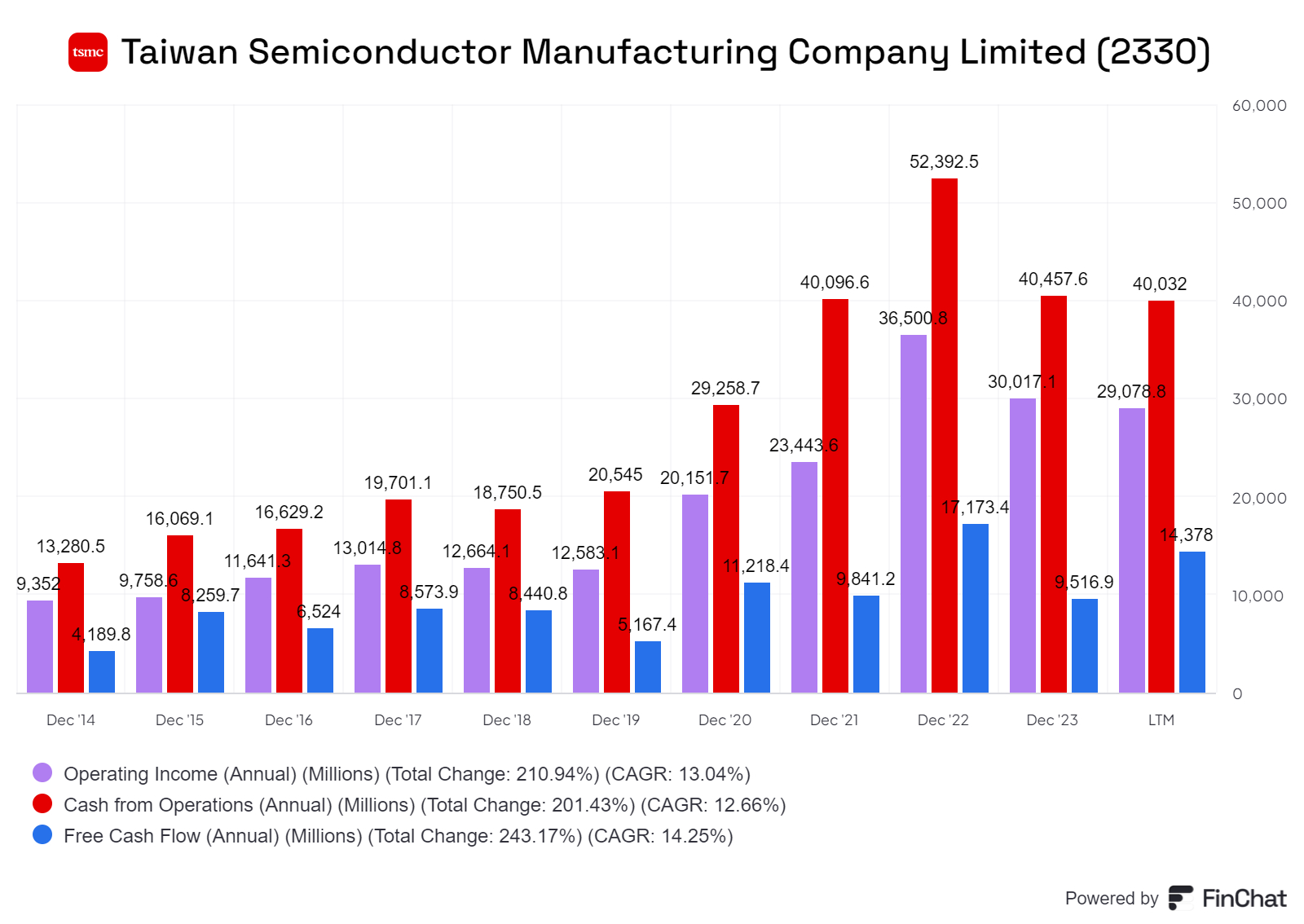

TSMC is a strong cash generator. 2023 Operating Cash was ~$ 40bn and Free Cash Flow was ~$9.5bn. The ~$30bn figure difference is of course capex.

The company has paid out most its free cash flow as dividends. Given the high return opportunities, I would prefer they do not pay dividends but retain all earnings and re-invest them. TSMC does not buy back stock. This is unfortunate as there will be times when this will be useful tool in their capital allocation strategy.

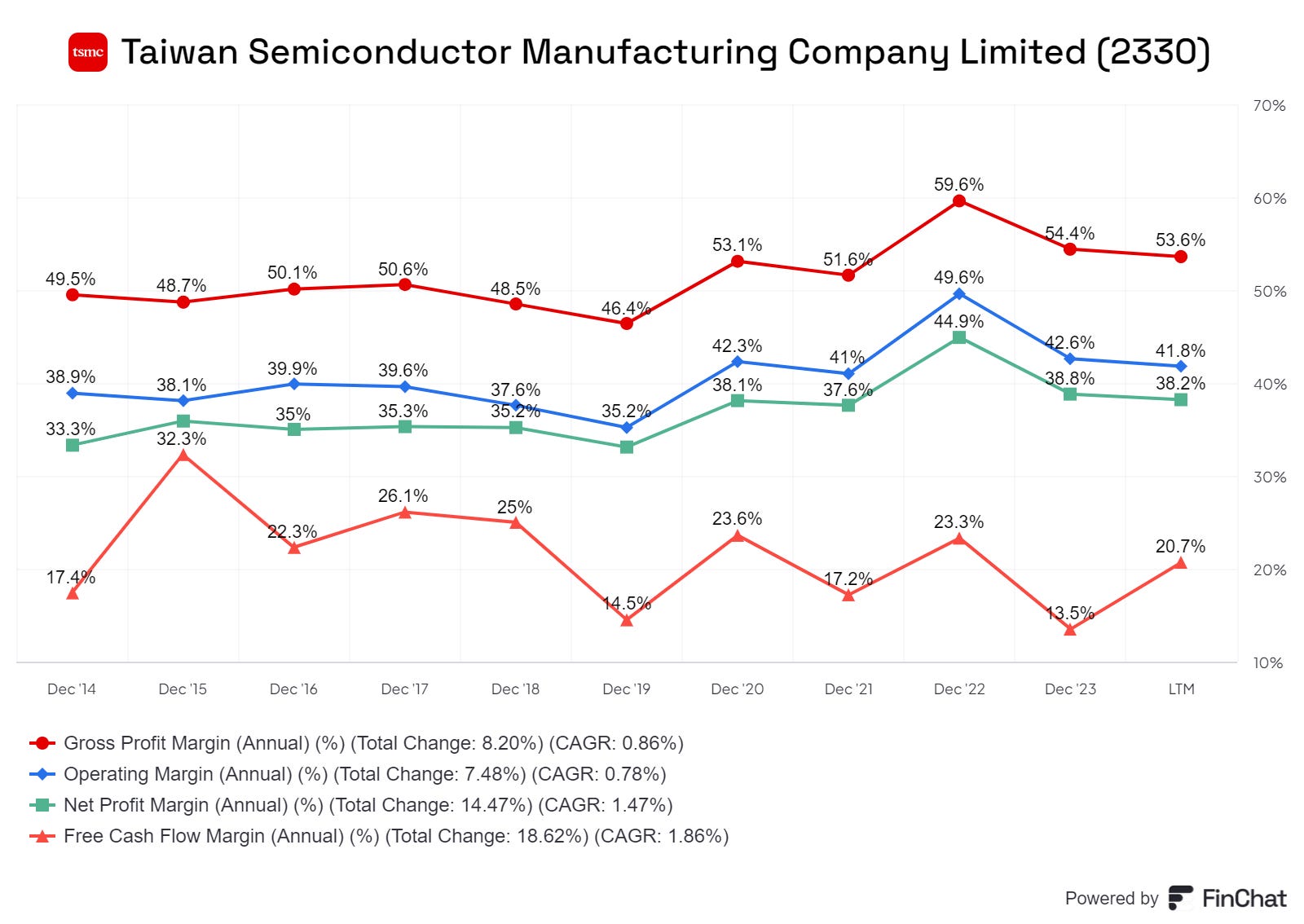

TSMC’s Gross Margin is ~ 52%. The operating margin is 41.3% which is remarkable for a manufacturing company and its operating costs are only 12% of revenues. Apple is a widely admired company but its operating margins are only ~30% and it outsources most of its manufacturing.

Although it operates in a highly cyclical and high fixed cost industry, the lowest operating margin TSMC ever posted in last 20 years was 25.3% back in 2003. After 2003, it never even posted less than 30% operating margin in any year. This indicates the remarkable operating efficiency of the company.

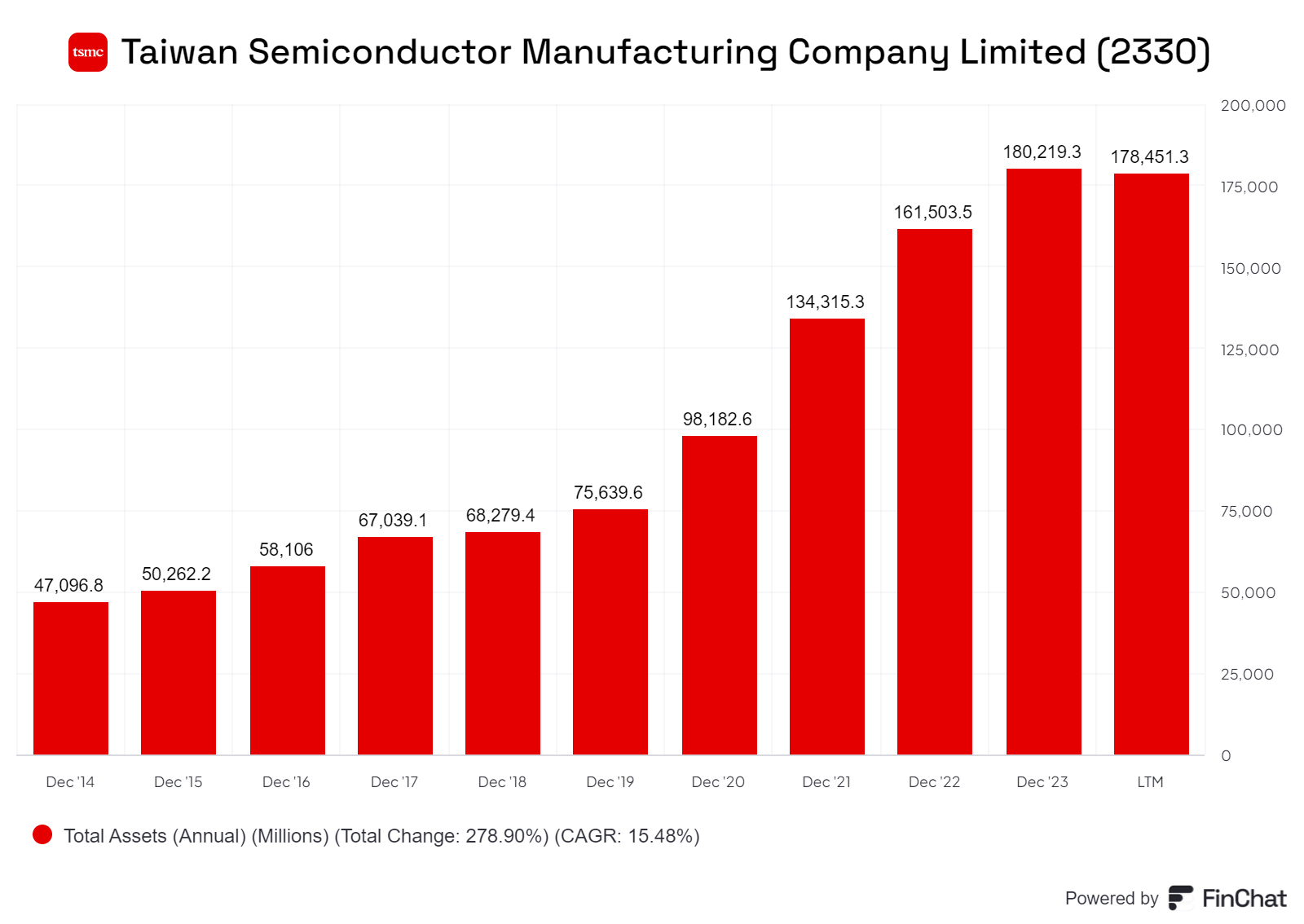

The scale of the company has increased greatly. Total assets have grown from below $ 50bn in 2014 to $ 180bn in 2023. A 22% CAGR.

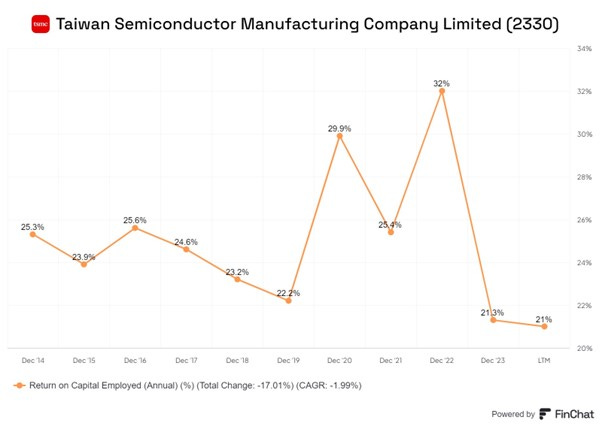

Despite huge increase in Capex and in Revenues, TSMC has maintained an ROCE of at least 20%. The RoE has consistently been in the range 25% to 27%. This is despite operating in a cyclical and high fixed-cost industry.

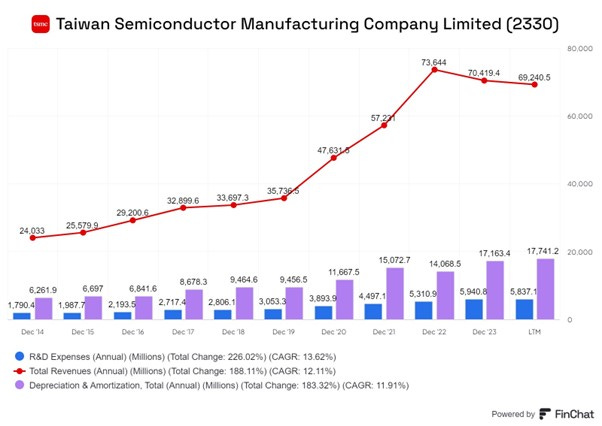

We noted above the high level of capex required to manufacture chips. This reflects the high costs for both designing chips and manufacturing them as shown below.

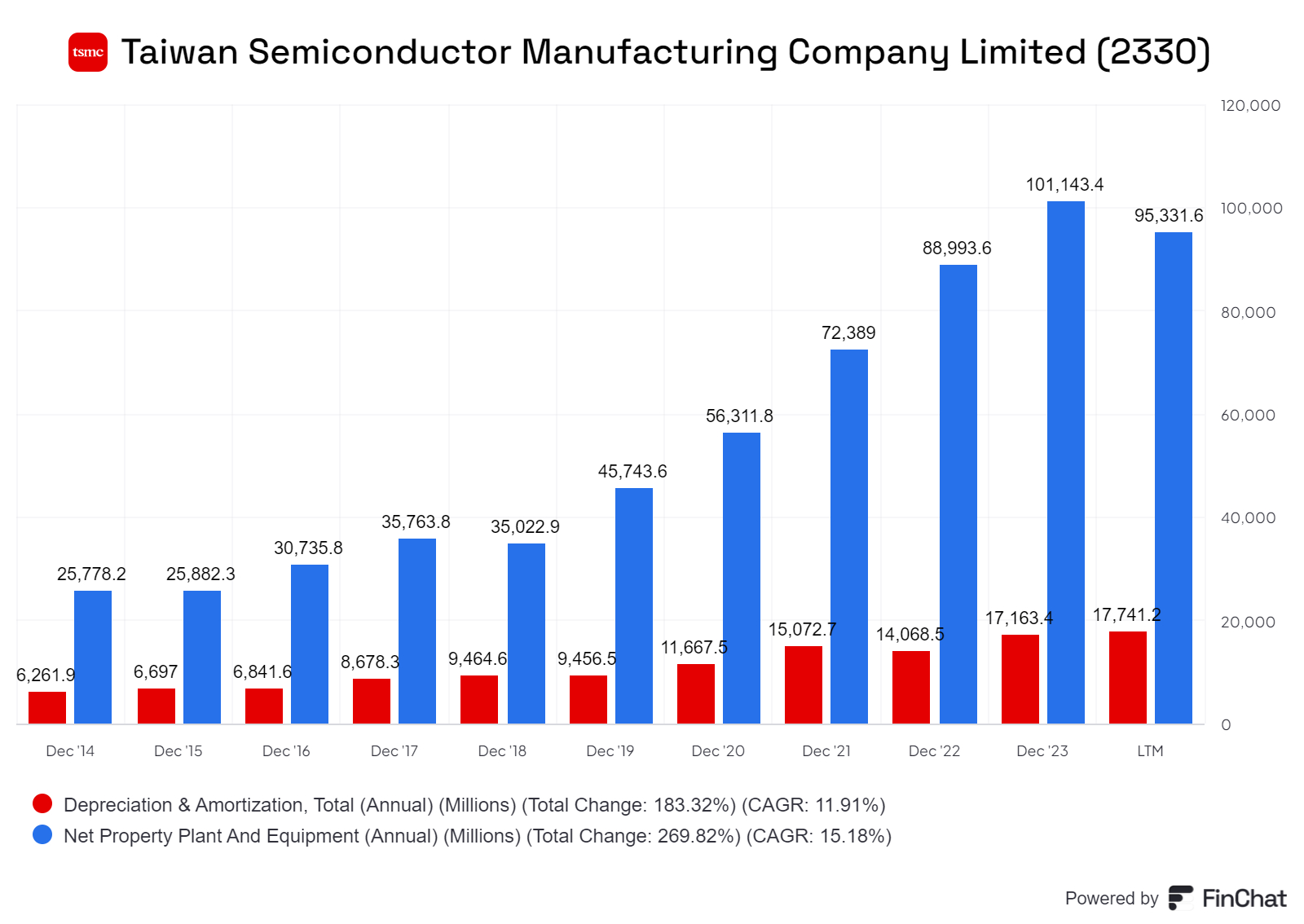

The depreciation rate for these plants can be exceptionally high.

Looking at last 10 years of data, ~25-40% of TSM revenue is just Depreciation & Amortization (mostly Depreciation) expense, and ~15-25% of its beginning PP&E is depreciated every year during the same time. For example in 2023, deprecation was $17bn or 25% of revenues.

2023 depreciation of ~17bn was ~17% of end 2022 Net PPE of $101bn.

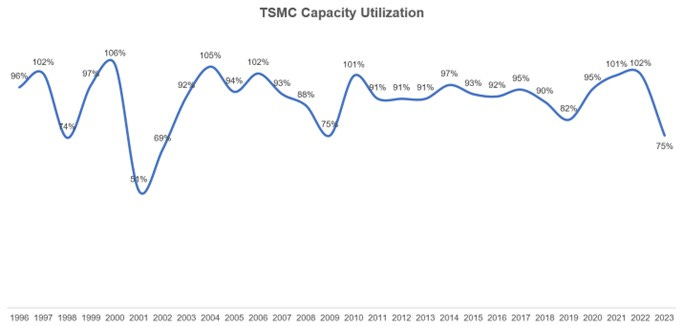

The company has high fixed costs, which must be paid in full before a single unit is produced or sold. This means that foundries have to be run at very high capacity utilisation levels with very high yields, otherwise large losses can occur very quickly . The chart below shows Capacity utilisation levels have been very high.

Source: Mostly Borrowed Ideas

Given the excess demand for Chips, foundries have changed the terms of trade a little to shift some risk to customers. The industry has moved to Long Term Agreements (LTAs) and Non-Cancellable, Non-Returnable (NCNR) policy with their customers. The fabs started to accrue and exercise some power over their customers.

The idea behind the NCNR is that customers should have to bear some of the risk and cannot cancel orders. Foundries and Fabs have managed to enter long-term agreements with most of their customers.

The last 30 year CAGR total return has been 16.4%. The 10 year CAGR total return has been 25.4% in US$ terms. This is broadly equal to the RoE, the company has achieved in recent years (see Chart above).

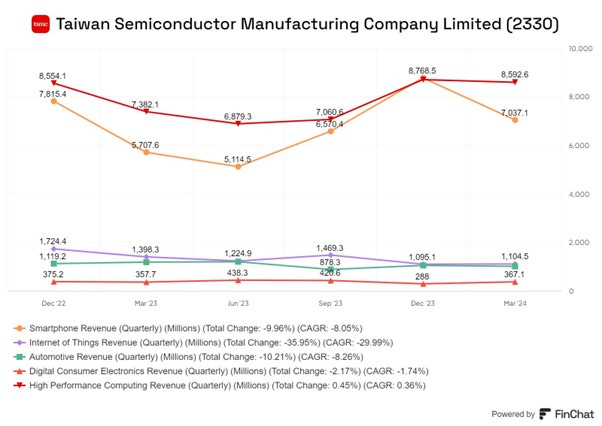

The chart above shows the segment breakdown of revenue. The March 2024 quarter total revenue was $18.5bn. $ 8.5bn (45%) was accounted for by High Performance Computing (HPC) which includes GPUs for GenAI driven investments in Datacentres. $ 7bn (38%) is accounted for by Smartphone Chips. The latter peaks in the December quarter and had an expected seasonal decline in March. Automotive accounted for 5.7%.

Highlights of the quarterly Earnings Conference Call

Q1 revenue decreased 3.8% in U. S. Dollars as our business was impacted by smartphone seasonality, partially offset by continued High Performance Computing (HPC) related demand.

Gross margin increased 0.1% points sequentially to 53.1%.

Total operating expenses accounted for 11.1 percent of net revenue, which is lower than the 12% implied in our Q1 guidance, mainly due to tighter expense controls.

Thus, operating margin increased 0.4% points sequentially to 42%.

Advanced Technologies, defined as 7nm and below, accounted for 65% of wafer revenue.

Current quarter guidance.

We expect our business to be supported by strong demand for our industry leading 3nm and 5 nm technologies, partially offset by continued smartphone seasonality.

We expect our Q2 revenue to be between US19.6bn and US20.4 billion dollars which represents a 6% sequential increase and 27.6% (YoY) increase at the midpoint.

Gross margin is expected to be between 51% and 53%. We continue to forecast a long-term gross margin of 53% and higher is achievable.

Operating margin between 40% and 42%.

We expect our overall business in Q2 of the year to be stronger than the first half and the revenue contribution from 3nm technologies is expected to increase.

We have a strategy to convert some 5 nm tools to support 3 nm capacity given the strong multi-year demand.

Our 2024 capital budget is expected to be between $28bn and $32bn as we continue to invest to support customers' growth.

· Between 70% 80% of the capital budget will be allocated for advanced process technologies

· About 10% to 20% will be spent for specialty technologies and

· about 10% will be spent for advanced packaging, testing, mask making and others.

AI related demand surge

The continuous surge in AI related demand supports our already strong conviction that structured demand for energy efficient computing is accelerating in an intelligent and connected world.

TSMC is a key enabler of AI applications. AI technology is evolving to use ever increasingly complex AI models, which needs to be supported by more powerful semiconductor hardware. Almost all the AI innovators are working with TSMC to address the accessible AI related demand for energy efficient computing power.

We forecast the revenue contribution from server AI processor to more than double this year and account for low teens percent of our total revenue in 2024. For the next 5 years, we forecast it to grow at 50% CAGR and increase to higher than 20% of our revenue by 2028.

We expect server AI processor to be the strongest driver of our HPC platform growth and the largest contributor in terms of our overall incremental revenue growth in the next several years.

Given the strong HPC and AI related demand, it is strategically important for TSMC to expand our global manufacturing footprint to continue to support our U.S. Customers' trust and expand our future growth potential.

In Arizona, we have received strong commitment and support from our U. S. Customers and plan to build 3 fabs, which help to create greater economies of scale.

Each of our fab in Arizona will have a cleanroom area that is approximately double the size of a typical logical fab. We have made significant progress in our first fab, which has already entered engineering wafer production in April with the N4 process technology. We are well on track for volume production in first half 2025.

Our 2nd fab has been upgraded to utilize 2 nm technologies to support the strong AI related demand…volume production is scheduled to begin in 2028.

We also recently announced plans to build a third Fab in Arizona using 2 nm or more advanced technologies, with production beginning by the end of the decade.

Together with our JV partners, we also announced a plan to build a second specialty fab in Japan with 6-7nm process technologies to support strategic customer for consumer, automotive, industrial and HPC related applications. Construction is scheduled to begin in second half 2024, with production targeted by the end of 2027.

In Europe, we plan to build a specialty technology fab in Dresden, Germany, focusing on automotive and industrial applications. With our JV partners, fab construction is scheduled to begin in Q4 this year.

Our overseas decisions are based on our customers' need and the necessary level of government support. This is to maximize the value for our shareholders.

These foreign plants will have higher costs. We plan to manage and minimize the overseas cost gap by pricing strategically to reflect the value of geographic flexibility and working closely with government to secure their support and third, leveraging our fundamental advantage of manufacturing technology leadership and our large-scale manufacturing base, which no other manufacturer in this industry can match.

Thus, even after factoring the higher cost of overseas fab, we are confident to deliver a long-term gross margin of 53% and higher and sustainable RoE of greater than 25%.

Our 2nm technology leads industry in addressing the accessible need for energy efficient computing, and almost all AI innovators are working with TSMC.

We are observing a high level of customer interest and engagement at 2 nm and expect the number of the new tape outs from 2nm technology in its 1st 2 years to be higher than both 3nm and 5nm in the in the first 2 years.

AI is producing a large profit pool at our customers and the HBM is also driving supernormal returns for memory players.

We will start 2nm production in the last quarter of 2025. We expect the meaningful revenue will start from the end of Q1 or beginning of the Q2 of 2026.

For TSMC, a higher level of capital expenditures is always correlated with higher growth opportunity in the following years. We work with our customers closely and our CapEx and capacity planning are always based on the long-term structural market demand profile. That is underpinned by the multiyear megatrends.

Why Has TSMC been so successful?

TSMC has a deep moat. Anybody whose products require leading edge chips, you have no choice but to buy from TSMC.

Samsung uses a lot of the chips it makes in its own devices. Therefore, you are currently greatly dependant on TSMC. Given their scale, it’s hard to compete with them on price. TSMC is not just one company, it is part of a complex value chain. Its relationship with ASML runs deep (from the very inception) which also makes it hard for another company to disrupt TSMC.

Morris Chang gave a talk at MIT in late 2023. He identified four factors that drove Taiwan’s/TSMC’s success in foundry business. The talk is 50 minutes long, but you can skip most of the lengthy introduction (join at about 5 minutes) and listen at 1.5X speed.

In the talk, Chang focused on the following key factors:

a) Talent: Taiwan had a ready supply of high-quality engineers, technicians, and operators. Many of them had studied in the USA, worked for an American tech company for a few years, and then came back home. The best engineers want to work for the best company, which in Taiwan is TSMC by a long distance. The cost for hiring engineers, technicians and operators are substantially less compared to the US/most western countries.

b) Low turnover rate: The US market had too many employers, staff turnover used to be 15% during recession and 25% during boom times at Texas Instruments (TI). This makes it very hard for chip manufacturing at scale as it takes almost three months to train someone. If trained staff leave, it becomes almost impossible to achieve high yield in chip manufacturing. Turnover was ~2% in the Japanese factories Chang used to run at TI; the implication is that TSMC had 2% turnover too.

c) Geographical concentration: Taiwan has major facilities in three cities, all of which are connected via high-speed trains. TSMC provides dormitories for their engineers to live in these cities. As Chang notes “it’s not a fun life, really, but it’s effective for the company.”

d) Experience curve theory: Manufacturing chips is perhaps the most complex manufacturing as noted above. It is difficult to achieve no fault production. In fact at the beginning the yield (percentage of flawless product) is very low but will hopefully improve with experience. TSMC decades of operations means it has more experience than almost anybody else.

Source: Mostly Borrowed Ideas

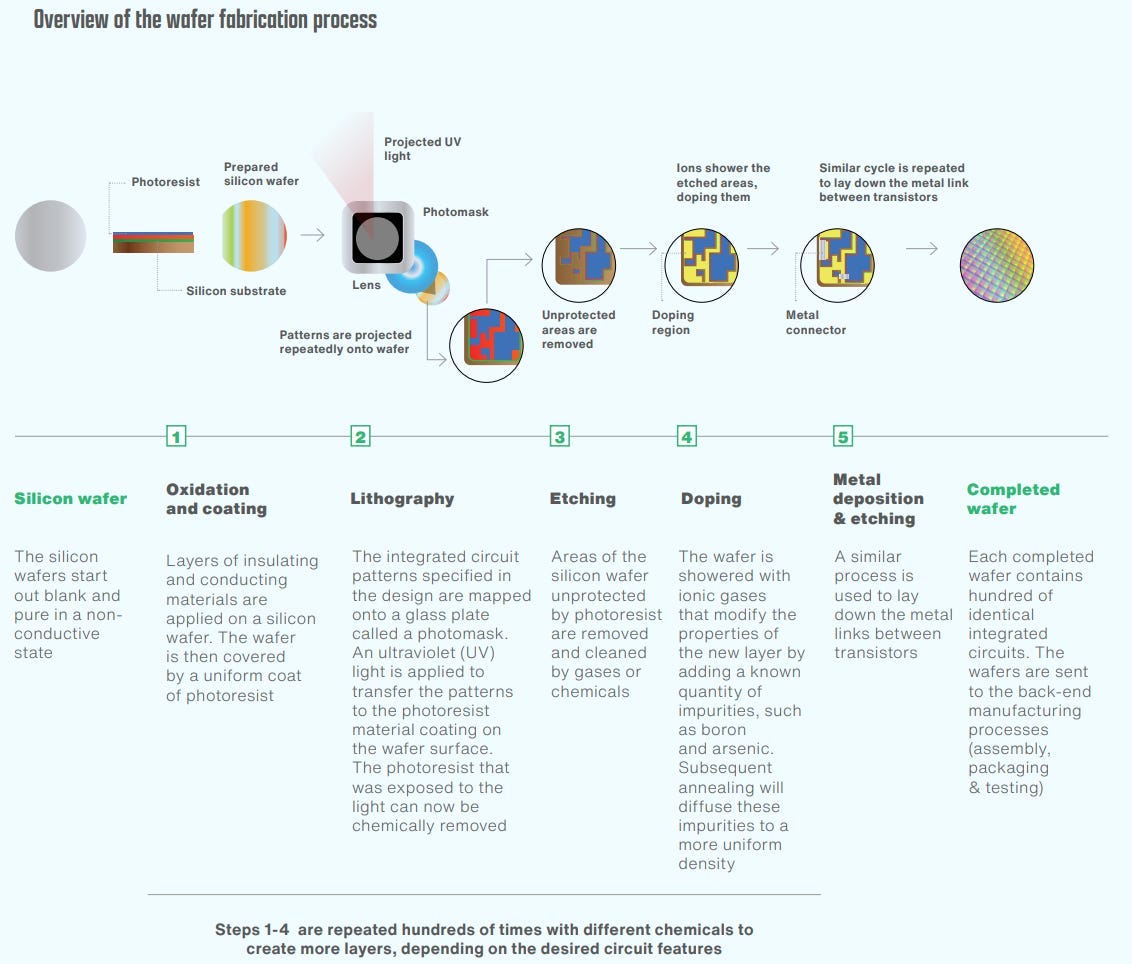

A single wafer undergoes hundreds of high-precision processes such as oxidation, coating, lithography, baking, etching, doping, and metal deposition as shown above .

Any tiny defect such a tear or a speck of dust will make the chip defective. The large number of intricate steps makes it hard to achieve perfection across all dies on a wafer. The need to pack more transistors onto each chip requires continuous scaling down of feature sizes to nm levels. This increases the complexity of fabrication processes like photolithography and etching, making it harder to maintain high yield.

At advanced nodes, defects tend to be systematic rather than random. Eliminating systematic issues requires extensive analysis, design fixes, and process tweaks. To make a functioning chip with billions of transistors you must achieve transistor failure rates measured in parts per billion. It must be close to perfection, yet cost-effective.

Achieving these near-perfect quality levels across billions of transistors on a single chip is an immense challenge. As a result, even if you have access to the technology, perfecting the manufacturing process and achieving high yield and maintaining elevated capacity utilization is a near impossible task.

This video below tries to explain the complexity of the manufacturing process and the challenges to achieve high yields, a process called yield learning. TSMC has more experience in achieving high yields and that advantage tends to be cumulative.

Political Risk

TSMC critical role in the vital chip industry is a source of weakness. 100% of its production is located on the Island of Taiwan which has been claimed by the People’s Republic of China for decades. Many analysts believe that a military invasion is inevitable at some point in the future.

The western world including the US Government have woken up to the dire risks represented by this geographical concentration of the manufacturing of the most advanced chips. This issue is well covered in Chris Millar’s book, “Chip War” and Financial Times Film called the Race for semiconductor supremacy which can seen here.

In Chip War Chris Miller puts it as follows:

“Taiwan produces 11 percent of the world's memory chips. More importantly, Taiwan fabricates 37 percent of the world's logic chips. Computers, phones, data centers, and most other electronic devices simply can't work without them, so if Taiwan's fabs were knocked offline, we'd produce 37 percent less computing power during the following year.

After a disaster in Taiwan, in other words, the total costs would be measured in the trillions. Losing 37% of our production of computing power each year could well be more costly than the COVID pandemic and its economically disastrous lockdowns. It would take at least half a decade to rebuild the lost chipmaking capacity. These days, when we look five years out we hope to be building 5G networks and metaverses, but if Taiwan were taken offline we might find ourselves struggling to acquire dishwashers.”

We all got a small sense of it during the pandemic when supply chains were disrupted and production of many good was affected.

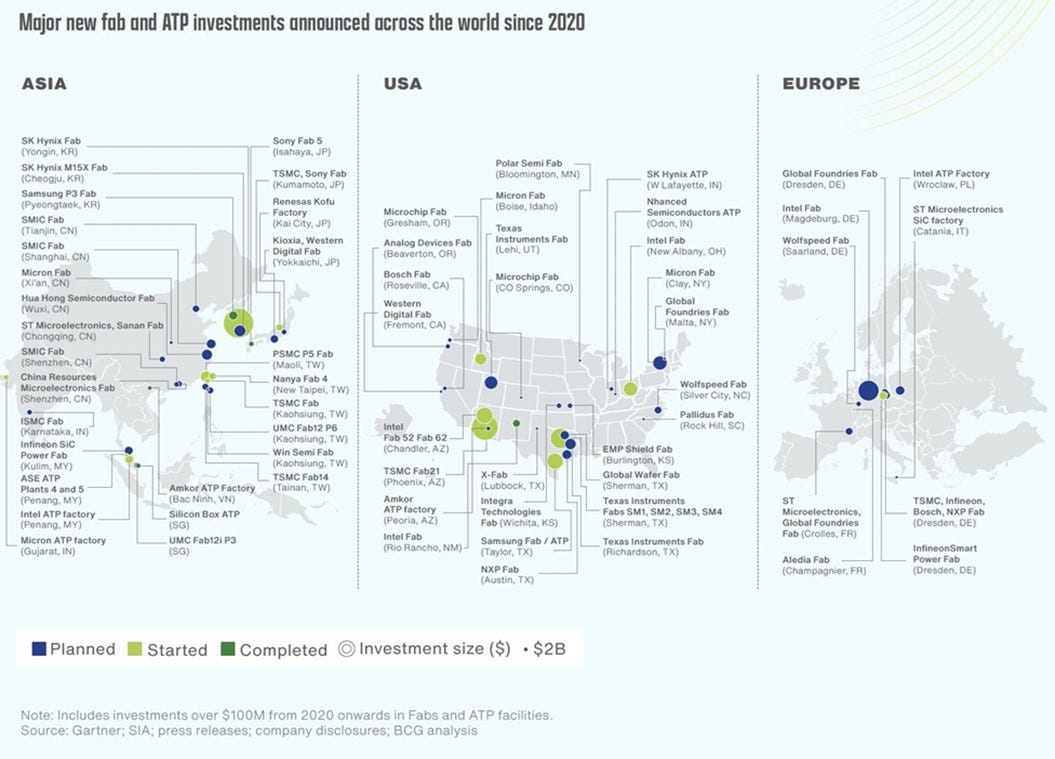

The CHIPS Act 2024 is the flagship legislation of President Biden’s Industrial policy. It includes $39 billion in tax benefits, loan guarantees and grants to encourage companies to build new chip manufacturing plants in the U.S. Additionally, $11bn billion would go toward advanced semiconductor research and development. The European Commission has earmarked 15bn Euros for public and private semiconductor projects by 2030. Countries like Japan, Korea, Singapore Malaysia and India have similar plans. China is also sponsoring huge investments though TSMC, like others , is restricted (by the US govt) in the technology it can transfer and the chips it can sell to China.

Already there is a huge increase in the planned Chip factory construction as shown in the chart below.

Source: Mostly Borrowed Ideas

TSMC is trying to build 3 fabs in Arizona and 2 in Japan. In addition, Samsung is building a new Fab in Taylor, Texas next to an existing facility. These are only some of the new capacity additions in all kinds of chips being planned globally, as shown above.

TSMC’s progress has been difficult due to labour shortages and culture clashes between Taiwanese management an American workers. These are covered in a April 2024 article at restofworld.org which is well worth listening to. It outlines its close knit military style hierarchical culture and the difficulties it causes in its new manufacturing operations in the USA.

https://restofworld.org/2024/tsmc-arizona-expansion

In the latest earnings call, the TSMC management indicated the plants will start production in 2025/26 and the third Arizona plant will start production in 2027.

Analysis

The foregoing analysis raises a couple of questions for us. It clear that TSMC has a dominant position and is in an oligopolistic situation if not a monopolistic one. Its customers are very profitable. Surely they could charge more and raise their margins from the current 52% to perhaps 60%. Our reading suggests the management views its customer relationships as long-term partnerships and culturally does not want to take advantage of market conditions to raise Prices and Gross Margins.

Having said that, the company is going to unchartered water in its overseas ventures. In Taiwan, they are naturally able to attract the best engineers, technician and operators and retain. They are able to work with a rigid, hard driving culture. This will not be possible as they expand into the US and elsewhere. They have noted that costs overseas will be higher than in Taiwan. They have said they will counter this by taking advantage of local subsidies (where available) and operational efficiencies ( where possible). However these measures may not be enough and TSMC may have to raise prices in order to maintain margins and profitability. This would obviously be a negative for Apple. Nvidia, Qualcomm and other fabless chip companies who are customers of TSMC.

Summary

TSMC is a remarkable company

It was founded in Taiwan at the behest of the Taiwanese Government even though the island had few competitive advantages in chip manufacturing.

It was grown strongly, profitably over three decades and has survived as one of only two companies which can manufacture the most advanced chips.

Despite the very high and increase complexity of the chip manufacturing process, TSMC has been able to maintain high and growing levels of output at high and rising margins and levels of profitability.

It real strength comes from the depth of engineering talent available to it in Taiwan, its relentless, hard-driving work culture and decades of experience of manufacturing leading edge chips.

Companies like Apple, Nvidia and many others could not operate without the TSMC.

TSMC’s critical role is a source of weakness. 100% of its production in Taiwan which has been claimed by the People’s Republic of China since 1949.

The CHIPS Act 2024 is the flagship legislation of President Biden’s Industrial policy. It includes $39bn worth of subsidies to encourage companies to build new chip manufacturing plants in the U.S. TSMC is planning three plants in Arizona in the USA, but construction progress has not been smooth. TSMCs unique operational and cultural strengths may be diluted as it shifts more production outside Taiwan.

TSMC two largest customers are Apple and Nvidia. AI datacentre workload demand for GPUs especially those designed by Nvidia have been going through the roof. This is a major of current and future source of demand for TSMC.

Demand growth is likely to remain very strong due to growth in Gen AI workloads in giant new datacentres, continued growth in smartphone sales and the rise of chip demand due to advances in automotive design, factory and warehouse automation and the rise of the Internet of Things (IoT).

Valuation

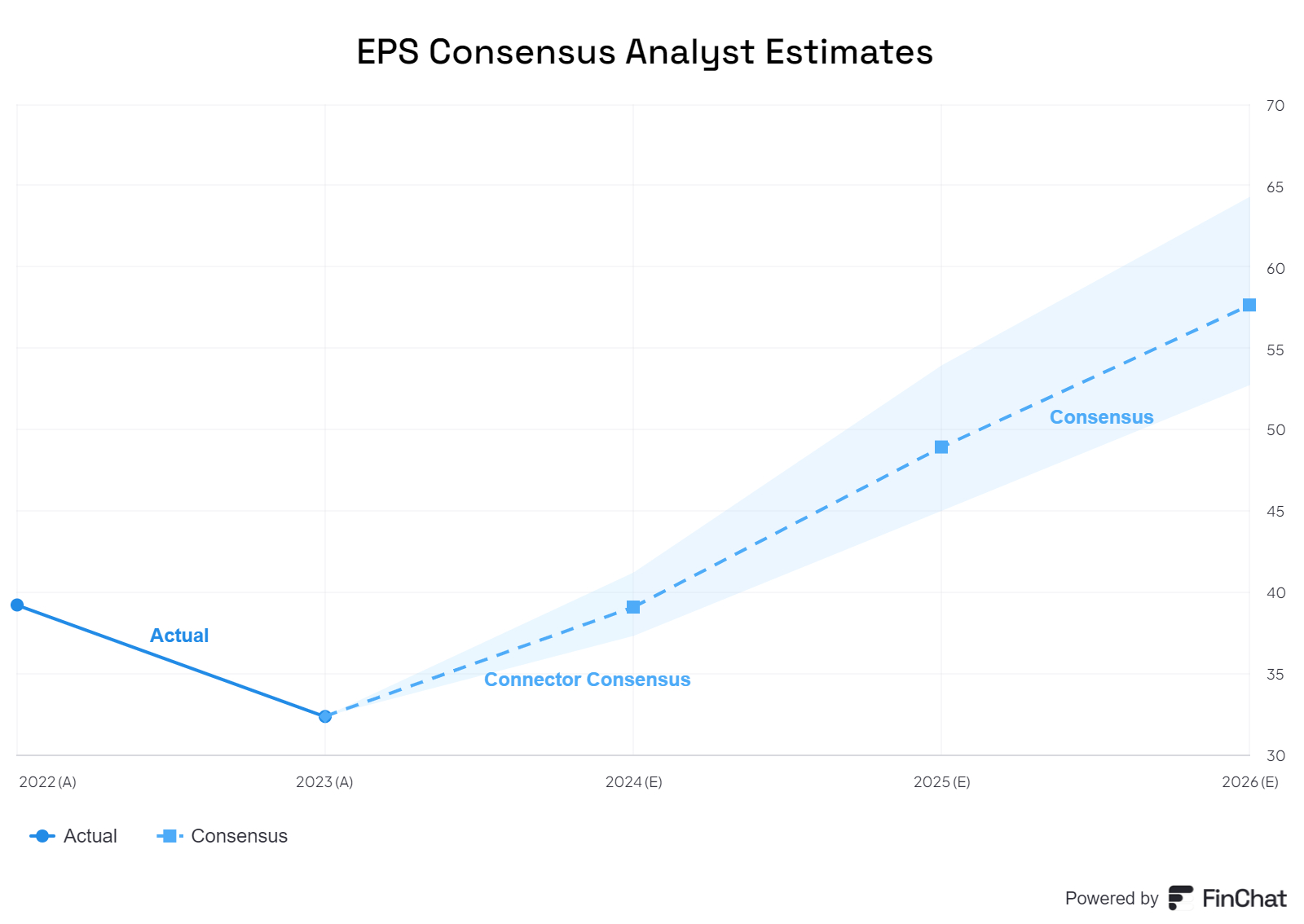

The analysts’ consensus expectations for EPS in FY2024, FY2025 and FY2026 are at $ 1.21 (TWD 39), $ 1.51 (TWD 48.9) and $ 1.76 (TWD 57) respectively. These are shown (in TWD) below.

TSMC has $ ADR where each ADR is a basket of five local shares. The ADR trades at $170 which implies a share price of $34 (170/5). This means the shares are trading at 22.5 times FY 2025 earnings and 19.3 times FY 26 earnings.

This seems cheap considering the growth potential and likely profitability of the company. It probably reflects a “China Invasion” discount to some extent.

The decision making is complicated as we do not know what discount to assign to the political risk of potential disruption in Taiwan due to China’s military assertiveness.

We will assume zero probability of it happening in our forecasting horizon but will note it as a key downside risk.

We can do a quick “back of the envelope” valuation calculation.

Let us assume that the analysts’ estimate,s which point to an EPS if US$ 1.76 noted above, prove to be accurate.

Let us further assume that this leads to EPS growth of 20% in years 4 and 5 for the next five years.

We can forecast 2028 EPS to be $2.54 ((1.2)^2) * $1.76)

If we assume in 2027 the forward P/E multiple will be 22, the share price in 2027 will be ~$55.8 per share or $ 279 per ADR.

This compares with today’s ADR price of $ 170 - a 64% discount.

A 64 % discount implies a CAGR return of 18% per annum for the next three years on the TSMC Stock. This seems attractive given the growth and profit opportunities available to the company.

We supplemented this “back of the envelope” evaluation with a Discounted Cash flow (DCF) calculation for which we made several assumptions. These include the following:

Revenue will grow between 22% in the next 5 years. Operating margins will be 44% for the next five years.

The weighted average cost of capital (WACC) is 10.9%.

The terminal EV/FCF multiple long-term growth rate is 25 times (compared with 50 times currently)

With these and other assumptions, we estimate the fair value of TSMC to be ~$ 221 per ADR, a 25% premium. As usual, we must state the caveat that these numbers are highly sensitive to the inputs. A small change in the inputs can lead to a very wide range of outputs.

Conclusions

We currently have a position of 2.5% of our portfolio in this stock to bring the weight to 3.5%.

We would note the big risk here is an invasion by China. However, we cannot meaningfully quantify it.

Given this risk, we are not planning to add more to this stock.

This is a very thorough post about TSMC and I linked to it in my links post for today: Emerging Market Links + The Week Ahead (June 24, 2024) https://emergingmarketskeptic.substack.com/p/emerging-markets-week-june-24-2024