Tata Consultancy Services (TCS) and Infosys

Quarterly Results

The Quarterly Results in India kicked off with results from two bellwether stocks, TCS and Infosys.

These companies are in the important Information Technology Enabled Services (ITES) sector. As the Indian Economy opened up in the 1990s, it was the first sector to demonstrate global competitiveness. For the background to this, you can read our note from 2023 on Infosys which can be found here.

These are the largest ITES companies. Infosys has ADRs listed on the Nasdaq so global investors can invest in the stock. The third and fourth ranking companies, HCL Technologies and Wipro also reported quarterly results. The latter also has an ADR listed in the USA.

These companies were engaged in global labour arbitrage. India has had a huge supply of software workers for decades and the companies grew by employing large numbers of software engineers to provide IT services for global clients in the B2B space. They maintained legacy mainframe systems, wrote software code, helped companies transform and monitor IT systems. They got a significant boost due to Y2K issues in the late 1990s when companies had to overhaul IT systems to deal with the Millenium Bug. The large banks who have been among the larger spenders on IT in the last three decades have been important customers for the Indian ITES companies.

For decades, they earned 70% of their revenues from US companies and institutions with the balance coming from the rest of the world. Indian customers accounted for a negligible share.

These companies along grew very strongly in the last three decades. They enjoyed high sales growth, and very high margins and generated huge free cash flows. They gave excellent returns for shareholders over the decades.

As they grew, they became major recruiters of students in STEM subjects in India and had to give generous salary packages and increments as they battled rampant attrition.

In the last three decades, the ITES sector has employed 4mn young professionals and created huge wealth both through high incomes but also share price appreciation.

The success of these companies was widely applauded. They were seen a symbol of the new capitalist India and its first globally competitive industry.

There were, however, some criticisms. One line of argument was that they just provided software coolies and only interacted with the IT people in the client’s hierarchy. The higher value technology consulting work was still done by the likes of Accenture, Booze Allen and Bain who had deep business relationships with the CEOs and Senior Management.

Their success encouraged large global companies such as Accenture (ACN), IBM, Cognizant (CTSH) and many others to establish large operations in India. IBM and Accenture now employ about 300,000 people each in India. Cognizant has 200,000.

Indian ITES companies are currently facing significant revenue headwinds in 2024.

These companies have been slow to upgrade themselves for the job skills required in an AI-driven world. Companies like Accenture have been quicker off the mark.

The growth for AI is changing technology work fundamentally and fewer people are required. The optimists argue that these companies will adopt and place themselves in a position where they will be able to capture AI -related workflows.

The growth of the cloud and the emergence of Saas many old-style customer-developed software us being developed by a readymade software packages such as Zoho, FarEye and Workon Grid. This means the armies of coders needed to maintain and code and enhance the software are no longer needed. This is a big headwind for the ITES companies.

Companies across the world are cutting expenditures and new transformational IT projects which are considered discretionary are under pressure. They are likely to wait for greater certainty before approving the discretionary expenditure.

Demand growth has slowed. The hiring environment has changed significantly, and attrition rates have fallen greatly. Companies have reduced hiring and may have to look reduce payrolls in the future, perhaps for the first time in their history.

Some summary numbers on ITES companies

As the data above shows these are substantial companies.

TCS has a market capitalisation of US$ 168bn and over 600,000 employees. It has 60 clients whose annual revenue to TCS is more than US$ 100mn. You can find more information on TCS here. Infosys has a presence in 60 countries and serves 183 of the Fortune 500 companies. Their current investor presentation can be found here.

The Results

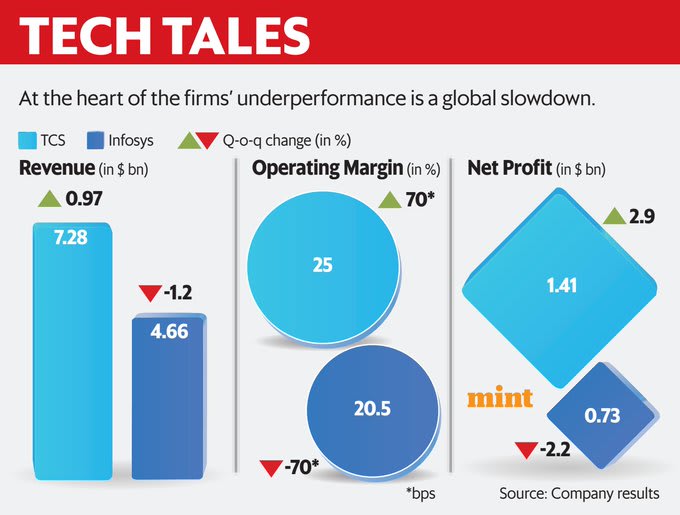

TCS grew faster than Infosys and beat estimates but both companies are on track to record the lowest growth numbers in many years.

Tata Consultancy Services reported a better-than-expected increase in third-quarter revenue, helped by the strong performance in the U.K.

Consolidated revenue rose 14.6% to INR 605bn ($7.30 bn) in quarter compared with

INR 582bn in the same quarter a year earlier. Analysts were expecting revenue of INR 601 bn rupees. However, analysts noted that if we ignore one exceptional deal with Indian state telecom company, BSNL, the revenue growth was much more subdued. Since listing in 2005, TCS has achieved a CAGR revenue growth rate of 14.7%

TCS Revenue in its U.K. market grew 8.1%, but declined 3% in North America, due to

extended furloughs and clients cutting discretionary spending amid macroeconomic challenges. TCS secured deals worth $8.1 bn in the quarter, down from the $11.2 bn in the July-September quarter.

Infosys reported revenue just 1.3% higher to INR 388 bn. Analysts were expecting revenues of INR 387bn. In the last five years, revenues have grown at a CAGR of 12.9%.

The EPS was INR 14.74 lower than the same quarter last year, when it was INR 15.7. Analysts were expecting EPS of 14.9 per share.

The combined workforce for Infosys and TCS declined by 11,728 workers in the three months to December.

Both HCL Technolgies and Wipro surpassed quarterly revenue expectations.

HCL revenues rose 6.3% compared with the same quarter in the previous year. In the last five years, HCL revenues have grown at a CAGR of 14.9%

HCL Technolgies beat quarterly profits helped by its deal with U.S telecom

company Verizon and strength in its products and platforms business.

The company's net profit rose 6.2% to INR 43.5 bn ($525 million) for the December quarter. Analysts had expected INR 41.5bn.

Wipro revenues fell -1.7% but net profits rose 1.7% in a surprise advance as Wipro restricted the impact of lower revenue on operating margins. In the last five years, Wipro revenues have grown at a CAGR of 10.8%.

Wipro maintained new deal momentum with new order wins of US$ 3791mn similar to the US$ 3785 mn in the previous quarter. The size of the above US$ 3bn for three successive quarters. The revenue growth forecast was raised a little to - 1.5% to 0.5%.

Summary

The large Indian ITES companies are currently facing revenue headwinds as large clients delay transformational IT spending. However, these companies have significant strengths in terms of their depth of extensive client relationships, a strong profile of existing highly profitable and cash generative business. They also have fortress balance sheets.

IT stocks rallied strongly after these results were released as markets overall were strong and analysts are forecasting a pick-up in IT spending in 2025. We are invested in the Infosys ADR and will continue to hold. The forward P/E multiples do not look too high given the margins and profitability of these companies and the share prices are likely to advance if the current demand uncertainties fade and discretionary IT spending resumes a growth trajectory.

Global investors can look at Infosys and Wipro ADRS while investors in India can look at all these companies as well as smaller more specialised players such as L&T Tech, Tech Mahindra and Cyient.