Tata Consulting Services (TCS) is India’s largest (Market Cap $178bn) IT Enabled Services (ITES) companies. We discussed the sector before and that report can be found here. We also wrote about two of their competitors Accenture (ACN) and Infosys (INFY) recently and that report can be found here.

TCS is listed in India. Only Indian Residents, Non-Resident Indians (NRIs) and Foreign Portfolio Investors (FPIs) registered with the local regulator can invest in the Indian stocks. However, it is still worth looking at the TCS Results to see what insights it can give for stocks like CAN, INFY, CTSH and EPAM.

Introduction

TCS is India’s largest ITES company. It has over 600k employees, about a 100,000 less than Accenture (ACN). Most of its costs are in Indian rupees and most of its revenues are in foreign currencies, especially US dollars.

TCS is the flagship company and a part of Tata group which is the leading industrial group in India. It is an IT services, consulting and business solutions organization that has been partnering with many of the world's largest businesses in their transformation journeys for over 50 years. TCS offers a consulting-led, cognitive powered, integrated portfolio of business, technology and engineering services and solutions.

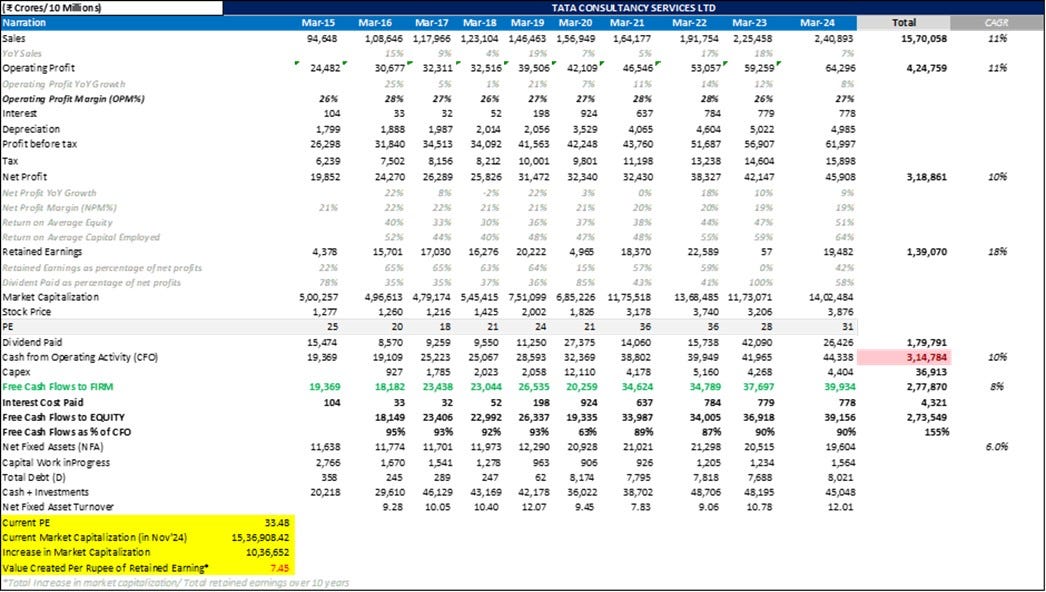

TCS 10-years Financial Summary

The slide above gives a good snapshot of select TCS numbers in the last ten years

The number are in Indian Rupees but the final column, which shows the CAGR growth rates, is easily understandable.

In the last ten years Revenues and Operating Profit have grown at CAGR of 11%. Over the same period, Net Profit has grown at a CAGR of 10%. As we noted in our report on Infosys, the industry model does not have significant operating leverage as you have to hire people if you want to grow revenue. Costs move up in line with revenues and operating margins are broadly stable.

Cash Flow from Operations have grown at CAGR of 10% over the last ten years, the same rate of growth as Net Profit.

The second last column (in slide above) shows the ten-year cumulative data for select items on the Income Statement. The cumulative ten-year Net Profit is INR 318,861 Crores. (A crore is 10mn). The cumulative cash flow from operations is also shown in this column and it is 314,784 Rupee Crore ($37bn), almost identical to the cumulative Net Profit figure. This indicates TCS has no difficulty in generating cash equal to reported net profit.

Operating Profit Margin is shown to be very steady at 26% to 27% while Net Profit Margin is in the range 19% to 20%.

Return on Equity and Return on Capital Employed reached an impressive 51% and 64% in FY 2024

Towards the bottom of slide above, we see at TCS’s total debt of INR 8021 Crores ($942mn) is dwarfed by Cash and Investments of INR 45,048 ($5.3bn) Crores so TCS has negative net debt.

We would also highlight the last unit in the slide which is highlighted in yellow. This shows the value created per each rupee of retained earnings is 7.5 rupees. This metric is based on a Warren Buffett idea. He outlined the circumstances in which the company should retain earnings beyond those needed for necessary capex, rather than distribute it to shareholders.

“For a number of reasons, managers like to withhold unrestricted, readily distributable earnings from shareholders – to expand the corporate empire over which the managers rule, to operate from a position of exceptional financial comfort, etc. But we believe there is only one valid reason for retention. Unrestricted earnings should be retained only when there is a reasonable prospect – backed preferably by historical evidence or, when appropriate, by a thoughtful analysis of the future – that for every dollar retained by the corporation, at least one dollar of market value will be created for owners. This will happen only if the capital retained produces incremental earnings equal to, or above, those generally available to investors.”

If we apply this test to TCS, we can see that over the last ten years, TCS has retained and reinvested INR 139,070 Crores ($16.4bn). Over the same period, the market cap has increased by INR 1,036 ,652 Crore ($122bn or 7.5X). Hence our assertion that each Rupee retained by TCS has created 7.5 rupees of value for investors – an excellent result.

Heavy Dividend Payouts

TCS has been a generous payer to shareholders and have paid 70% of its cash flows from FY05 to FY20.

Research & Development

TCS Research and Innovation is strongly aligned with the Company’s vision of Growth and Transformation. It continues to expand its foundational research in core computing areas. In FY20, the company applied for ~5,200 patents and has been granted ~1,350 out of them.

Its innovation labs are located in India and across the world and its R&D expenditure for FY20 was INR 1,867 crores ($220mn)

Clients Base

Clients include Google, Amazon, Microsoft Azure, Adobe, Intel, Bosch, IBM, Apple, Oracle, Symantec, etc. Currently, it has 64 clients who pay over $100 Mn per annum and about 140 clients who pays $50mn.

Q3 Quarterly Results

Client budgets are usually decided in January and the 3rd quarter (to end December) is a seasonally quiet quarter. If budgets are constrained there may nevertheless be some discretionary spending especially if there have been some great than expected savings elsewhere. Clients are currently (in January) deciding their budgets and the ITES companies will be awaiting the results of the decisions.

In terms of segments, Banks, Financial Services and Insurance (BFSI) companies have been large spenders on technology services and they account for 37% of revenues. However, BFSI budgets have been constrained the last 18 months as can be seen in the table above.

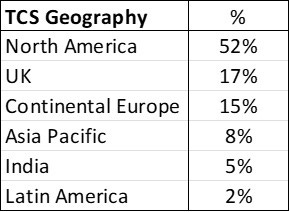

In terms of Geography, North America is by far the largest market followed by the UK and Continental Europe. Asia Pacific is quite small and India has grown rapidly in the last two years but is still only 5%.

TCS revenues grew 5.6% (y/y) and 4.5% (y/y) in constant currency to INR 63,973 crore ($7.5bn). This is less the historic CAGR for revenue growth of 11% noted above.

Operating margin was at 26.5% and net margin was at 19.3%.

Total Contract Value (TCV) for the quarter was $10.2bn with North America contributing $5.9 billion. TCV is measure of the value of the contracts signed in the quarter and company highlighted this number was exceptionally strong.

“We achieved significant large deal wins across various markets and industries, resulting in a double-digit growth in TCV (y/y). This performance is particularly noteworthy given the absence of any mega deal wins. Our strong deal pipeline and TCV gives us confidence as we look ahead.

As end 2024, they have more than 1,300 clients which contribute to $1mn plus annualized revenue. In Q3, three added three new client ’s in the $100mn plus band, bringing the total to 64.

It is sometimes argued that Indian ITES companies supply cheap coding talent in large numbers and their main competitive advantage is labour arbitrage. This is view is outdated and has not been accurate for many years. There are two reasons for this.

First, non-Indian companies employ large numbers of IT workers in India. For example, Accenture (ACN) has 50% of its 740k employees in India.

Secondly the leading Indian software companies have developed their own products and IP.

Below is a table of some of the product developed by TCS.

Three examples cited by TCS in the earnings conference call show the high level of the mission-critical work they do for clients

A leading American electronics retailer partnered with TCS to enhance customer engagement and drive operational excellence.

“TCS utilizes contextual knowledge to design and implement a scalable, unified contact centre platform that consolidates chat and IVR (Interactive voice response) systems, enabling seamless workflows across channels. The platform employs advanced natural language understanding and conversational agents for intent identification and handling of open-ended inquiries.”

“A real-time dashboard tracks critical metrics, including user containment rates, queue transfers, and system utilization, providing actionable insights for continuous optimization. Supporting over 30,000 daily chat conversations and 3x as many invoices, the system has achieved 90% intent identification, 3% user containment improvement rates, and enabled context-aware brand-aligned response, improved self-service, and reduced live agent transfers.”

A leading global life sciences company partnered with TCS for accelerated cancer drug discovery.

“The challenge was to design small molecules against a novel target protein of interest where no target-specific small-module dataset is available. The only available input was a target protein structure. The novel molecules must satisfy all drug-like properties.”

“We designed a GenAI-based drug discovery solution for identifying small molecules on a cancer target that takes the structure of the target protein as input and designs target-specific property-optimized small molecules. We generated around 1,300 molecules, optimized for five properties, and further the reduced set had to pass several proprietary filters on the client side and assess synthesizability against the client's in-house compound library.”

“A leading global bank partnered with TCS to build a first-of-its-kind AI-led real-time fraud detection solution, replacing its existing technology. TCS’s innovative predictive AI solution performs real-time transaction monitoring, detects customer behaviour anomalies, and generates risk scores. This delivered an 18% point improvement in fraud detection, reduced false positives by 25%, and improved fraud analysis response times by 50%.”

Highlights of post-earnings conference call

The historic 10-year sales CAGR 10%. Last year (FY24), growth was 7% and this quarter (a slow quarter), was just 5.6% (y/y). Sales growth has been slow and the company addressed this issue

“What happened during FY’25 was also the deferral of some projects going slow based on the ROI expectation which saw reprioritization. (We are) …seeing the revival in discretionary spend, early signs of revival, I don't want to say that it's recovered. Seeing the early sign of revival and the strong TCV win gives us more confidence in CY’25 and FY’26.”

They are seeing a revival on demand 2025 and 2026. Analysts are not convinced and the consensus of analysts’ views sees FY 2025 and FY 2025 revenue growth at 6% and 7% respectively.

They are confident they can maintain operating margins.

“Our margin aspiration remains 26% to 28%. Going forward, we will strive to get as close to our guiding band as possible.”

This is positive and suggests there is no pressure on operating margins

There were fears that the rise of AI might reduce demand for services and products of companies like TCS. Unsurprisingly TCS disagree,

“We think AI demand will be net positive rather than being negative. That is at least what we are seeing as of today”

They gave an insight as to clients are focusing on at the moment.

“Customer priorities continue to remain centred around cost optimization and business transformation. GenAI, AI and cloud services continue to see significant growth for us this quarter. Clients are investing in agentic AI adoption, building robust data foundation, and taking a value chain-based approach to AI and GenAI transformation.”

“Agentic AI represents the next step of maturity in the exponentially evolving space of AI. It allows us to orchestrate actual transactions inside business value chains using the rapidly improving planning and reasoning capabilities of large language models. We are now starting to go past the initial wave of chatbots and RAG deployments of GenAI, and more crucially, this will allow TCS to use our deep contextual knowledge of our customers' business to design, train, and deploy agents that solve high-value business problems.”

Management was asked about the prospect of higher spending from the key BFSI sector.

“..on the BFSI thing, as I said, GenAI adoption is very strong., From an overall technology modernization, code modernization, we are talking to some of our customers on large scale transformation as well. So, we do see a reasonable kind of either advanced discussions with our customers or early discussion, but technology modernization discussion is very strong.

“Client budgets are likely to be flat with some positive bias. At the same time, we are hopeful of discretionary spending picking up.”

Bullet point summary of the conference call.

Revenue in dollar terms was $7,539mn, with a year-on-year growth of 3.6%, translating to a constant currency growth of 4.5%

Net cash from operations was $1.54 billion, representing 105.3% of net income.

Free cash flows amounted to $1.45 billion, with invested funds at $7.28 billion.

Deal Wins and TCV:

Total Contract Value (TCV) for the quarter was exceptionally strong at $10.2 billion, with North America contributing $5.9 billion.

BFSI (Banking, Financial Services, and Insurance) accounted for $3.2 billion, while the consumer business contributed $1.3 billion.

Notable double-digit growth in TCV year-on-year was achieved without any mega deal wins, indicating a broad-based performance across various markets.

Workforce and Talent Management:

Workforce totalled 607,354 with 35.3% representation of women and 152 nationalities.

LTM attrition in IT services was reported at 13%.

Over 25,000 promotions awarded in the quarter, reflecting commitment to talent development.

Campus hiring is progressing as planned, with preparations for onboarding an increased number of hires next year.

Demand Trends and Outlook:

Customer priorities focused on cost optimization and business transformation.

Significant growth observed in GenAI, AI, and cloud services.

Early signs of revival in discretionary spending noted in BFSI and Retail.

Expectations of client IT budgets remaining stable with a positive bias for CY'25.

Management expressed cautious optimism for CY'25, anticipating better performance compared to CY'24 despite the tapering off of the BSNL contract.

Challenges and Headwinds:

The management acknowledged the impact of unresolved geopolitical issues, trade wars, and uneven growth forecasts as potential headwinds.

The BFSI sector is experiencing operational efficiency demands, with ongoing modernization initiatives.

Declines in specific sectors such as Communication and Media, Life Sciences, and Manufacturing were noted, with expectations for stabilization and recovery in the medium term.

Capital Allocation:

The Board recommended a dividend of ₹76 per share, including an interim dividend of ₹10 and a special dividend of ₹66 per share, consistent with the capital allocation policy of returning substantial free cash flow to shareholders.

Summary

TCS is the largest Indian ITES companies. Over the last two decades it has grown strongly with an effective cash generative business. In the last twenty years, the stock has given a CAGR total return of 22%. Given the Rupee likely average annual depreciation of 3% per annum, the CAGR total return to dollar investors have probably been around 19%.

The company has a very strong balance sheet and a consistent track record for both retaining earnings and returning capital back to shareholders in the form of dividends and share repurchases.

The company and the sector had a difficult time growing revenues in the last 18 months as client budgets have been flat in many cases and discretionary spending has been restrained. We noted in our report on Accenture on December 29th 2024 that their most recent quarterly earnings growth was just 2.7% and operating margins were about 15.4%, much lower than Infosys and TCS. TCS’s ROE and ROCE numbers are very high indicating a superior profitability.

Despite the revenue challenges, TCS remains a highly effective company which is well positioned to grow strongly.

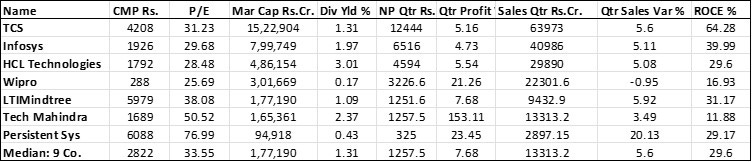

Relative Valuation

The table below shows some valuation parameters for some large and mid-sized Indian IT companies.

TCS has the highest ROCE but the P/E Multiple is also on the higher side.

Conclusions

The management is optimistic about future growth driven by strong deal wins and a robust pipeline, despite some sector-specific challenges. They expect to mitigate the impact of the tapering BSNL contract through new opportunities and improved discretionary spending.

Given the long track record of success, we are inclined to give the management the benefit if doubt. There is a good chance they can raise revenue growth to high single digit percentages and continue to grow profits. Over the long term it should reliably and steadily give total return of at least 15% per annum which means the share price should double in five years.

We will give TCS a 1.5% allocation in our Indian Equity Portfolio.

Annexe 1

This Annexe has some additional information on the various TCS Product Suites and the success they had in Q3 2025.

TCS Ignio™, our cognitive automation process suite saw 30 new deals wins and 9 go-lives. The ongoing trend in AI and GenAI are significantly driving investments in AI based systems and intelligent automation. These advancements are propelling ignio’s deal wins as an increasing number of customers embark on their journey towards becoming autonomous enterprises

TCS BaNCS™, our flagship product for financial services, continued its leadership with 4 wins and 7 go-lives during the quarter.

We signed a 15-year contract with Ireland's Department of Social Pension to implement and support the new Auto Enrolment Retirement Savings Scheme. This initiative will provide a comprehensive digital solution for automatic enrolment of nearly 800,000 workers in Ireland. This is a landmark deal for TCS in the geography and the first BPaaS implementation in Ireland. This further solidifies our leadership position in the UK and Ireland market for Life and Pensions.

We have migrated 800,000 UK Life and Pensions policies for Scottish Widows over 4 migrations in H2 of 2024. This now completes a highly complex migration of Life and Pensions for Scottish Widows comprising of over 500 products and resulting in 3 million UK L&P customers being serviced on TCS BaNCS.

Quartz, our innovation-led platform leveraging blockchain and AI, had one win and one go-live this quarter, including a strategic pilot for hybrid market infrastructure in Europe.

TCS iON, our platform for Digital Assessment and Exam Administration and Learning, had 38 new wins and 150-plus platform capabilities went live. Our assessment platform administered in-center exams for over 17 million candidates The Indian government's focus on industry participation in employability, internships and skilling should drive strong growth on the iON platform. Additionally, there is an increasing emphasis on reducing logistics work and shortening the results generation timeline.

TCS OmniStore™, our AI-powered Universal Commerce Suite, had one deal win and one go-live this quarter.

TCS Optumera™, our AI-powered Retail Merchandising Suite, went live for one client. • TCS TwinX™, our digital twin solution, has three wins and one go live. • And in Life Sciences, TCS ADD™ platform had three go-lives this quarter