The Indian Stockmarket

An overflowing bath?

I am currently working from India and watching CNBC-TV18 – the local CNBC TV affiliate- and looking at summary financial data on large Indian companies. The valuations, based on my quick and dirty analysis, look very high and have the effect of making the inflated US stock market look cheap.

Imagine a bath with plastic ducks and other floating toys. The tap is open and water is flowing out at a steady, heavy rate. The bath plug is in place so water cannot escape. The water level is rising and all the plastic toys are floating up.

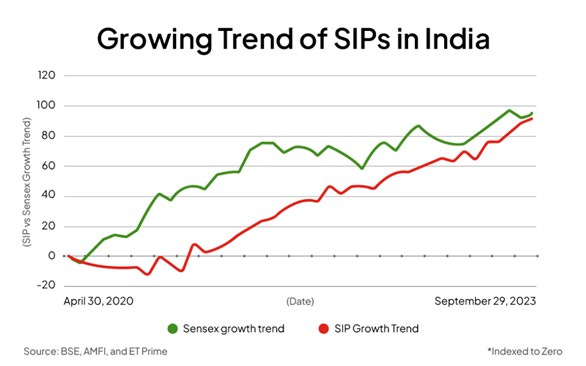

This is a description of the Indian Market. The flow of water is the flow of money into mutual funds principally, through Systematic Investment Plans (SIP). SIPs are plans where investors sign up to invest a fixed amount each month into Mutual Funds (mostly equity Mutual Funds). The amount involved can be as little as US$ 5.00 per month. Today there are over 100mn SIP accounts and the number is growing steadily as indicated by the chart below.

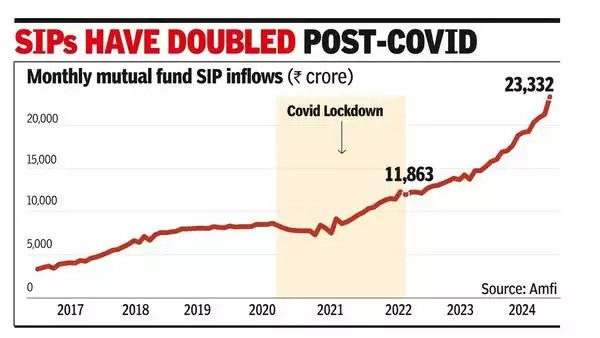

The value of monthly inflows from SIP accounts are growing fast and are currently at the equivalent of US$ 3bn a month. At the current rate, that implies about $ 36bn is flowing into the market through Mutual Fund SIPs. The net figure is lower due to some SIP Redemptions. The chart below shows the monthly inflow in mid-2024 as 23,332 crore rupees. A crore is 10mn.

This money comes in every month and the fund managers have to invest in local markets as their ability to keep cash is limited. The rising water pushed up all the toys higher. The liquidity pushes up all shares and stock valuations are very elevated.

The bath is plugged as the flowing liquidity cannot be invested outside India. The Central Bank, the Reserve Bank of India, is concerned about the currency and effectively limits how much Indian mutual funds and residents can invest outside India. There a couple of local rupee-denominated Nasdaq ETFs in India, which cannot create new units, and they trade at a 17% premium to NAV(!).

Our analogy of the bath is not quite accurate. The bath does have some leaks.

There are foreign institutional investors in the market. They are called FPIs (Foreign Portfolio Investors) and they can sell to offset the SIP-driven local buying. However, for the last two years, FPI selling has been overwhelmed by SIP-driven local buying, and markets have traded higher.

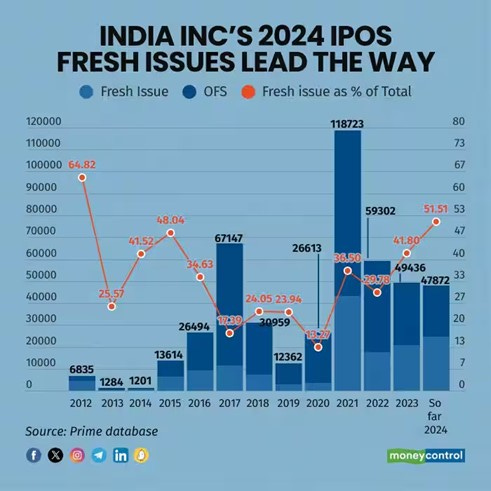

Another potential leak on the bath is new supply. The number and value of IPOs has increased greats. There seems to be a few new issues and ongoing offers for sale (OFS) by listed companies every week.

In 2023, INR 49,436 crore (US$5.8bn) was issued and so far in 2024 it its estimated INR 160,000 crore (US$19bn) worth of new supply has appeared in the market. This included a US$3bn issue by Hyundai India where the Korean parent took advantage of high valuations in India to take some back home.

Supply has increased dramatically and this will probably slow down the rise in stocks. Supply will probably grow relative to demand in the next two years. Valuations are expensive and the Indian stocks could suffer a price correction or a time correction.

However, there are over 5,506 companies listed in India and there must be some companies which offer good value in absolute terms and many others which offer value in relative terms.

I am going to try to write about some Indian companies in this Substack. However, most of my subscribers can’t access the market. The only foreigners currently allowed to invest in India are the FPI and non-resident Indians (NRIs). Only about 30% of my subscribers are based in India. Nevertheless, there will be some value in exploring the opportunities.