Ulta Beauty (ULTA)

A short write up

I have been writing this Substack for over 18 months and there are over 160 articles. I like to write the company deep dives, but these takes a long time and the frequency of output is lower than I would like.

Going forward, I will write some short company write ups. These are companies which look interesting to me but detailed work has not been done.

These short reports should not be taken as investment recommendations. In fact, no report should be taken thus. Rather, they should be seen as the starting point for further work, evaluation and consideration.

Introduction

Ulta Beauty, Inc. was founded in 1990 as a beauty retailer at a time when prestige, mass, and salon products were sold through three distinct channels

Department stores for prestige products.

Drug stores and mass merchandisers for mass products.

Salons and authorized retail outlets for professional hair care products.

Ulta developed a distinctive specialty retail concept that offers a broad range of brands and price points, select beauty services, and a convenient and welcoming shopping environment.

They define their target consumer as a beauty enthusiast, “a consumer who is passionate about the beauty category, uses beauty for self-expression, experimentation and self-investment, and has high expectations for the shopping experience.”

They estimate that such female beauty enthusiasts represent approximately 60% of shoppers and 75% of spend in the U.S. beauty category.

They provide a differentiated assortment of more than 25k beauty products from 600 (!) brands across all categories, including their own private label. They cover a very wide range of price points as well as a variety of beauty services. The latter are offered in a full-service salon in every store featuring hair, skin and brow services.

Ulta has more than 1,400 stores in 50 states predominantly located in convenient, high-traffic locations.

They also have a digital offering delivered through our website, ulta.com, and mobile applications.

Ulta also has a loyalty program that enables members to earn points for every dollar spent on products and beauty services and provides them with deep, proprietary customer insights.

It claims to be the only national beauty retailer of prestige, mass, and salon products and services under one storefront.

They have historically used cash flow for new, remodelled, relocated, and refreshed stores, supply chain investments, short-term investments, and investments in information technology systems.

Key aspects of Ulta Beauty’s business include:

Large Store Footprint

Ulta Beauty maintains an average size per store of over 10,000 sq. ft. This have an open and spacious design, inviting customers into the store. These stores are open 7 days a week, 11hrs a day. Within each store there is a 1000 sq. ft Salon as well, offering services to its consumers.

Ulta Beauty Salon

The Salon is an important feature as it encourages regular customers trips to the Stores.

Loyalty Program:

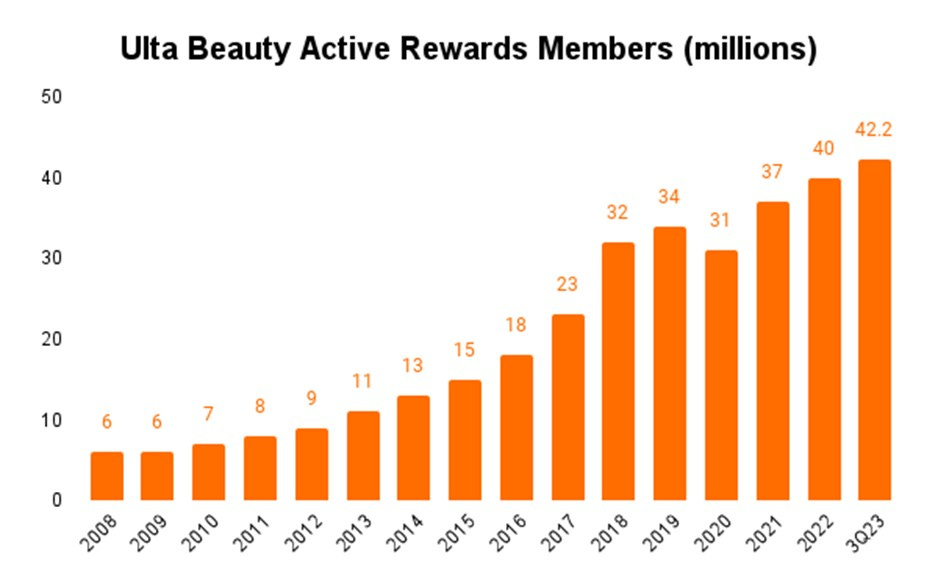

The Ultamate Rewards loyalty program plays a pivotal role in Ulta Beauty's customer engagement strategy. Members earn points for purchases which can be redeemed for discounts on products or services. This program, which accounts for over 95% of the company's total sales, supports Ulta Beauty in gathering insights into customer preferences and tailoring experiences and promotions accordingly. It has 43.3 mn members.

Leveraging insights from over 43.3 million Ultamate Rewards members, Ulta intends to foster deeper connections with beauty enthusiasts.

Their member data suggests our guests prefer to transact in physical stores, where they can discover and interact with products and other beauty enthusiasts. In FY 2023, 76% of their 43mn loyalty members transacted solely in their stores.

Brand partnerships

They have active relationships with brand partners such as L’Oréal and Estée Lauder among others,. These brands represent represented 55% of total net sales. They believe the brand partners view them as a significant distribution channel for growth and brand enhancement.

Store location and structure

The stores are in smaller shopping centres called Power Centres which have several national brand stores. Ulta relies on the footfall that the latter generate. The stores are 10,000+ square foot in size

In terms of staffing, each store has four managers and ~28 full- and part-time associates. These include four to eight prestige consultants and five to ten licensed salon professionals.

The management team in each store reports to the General Manager (GM). The GM oversees all store activities including salon management, inventory management, merchandising, cash management, scheduling, hiring, and guest services.

The Company believes they have the potential to grow the store footprint to between 1,500 to 1,700 freestanding Ulta Beauty stores in the United States.

In addition to the large standalone stores, Ulta has a collaboration with Target where it implements a “shop-in-shop” model. The employees will be trained by Ulta but are on the payroll of Target. This 1000 sq. ft. shop will be made to look like the Ulta Beauty stores and placed right next to the cosmetics section of Target.

Store Economics

The average investment required to open a new Ulta Beauty store is approximately $2mn, which includes capital investments, net of landlord contributions, pre-opening expenses, and initial inventory.

The stores are leased. The leases have a fixed minimum annual rent and generally have a 10-year initial term with options for two or three extension periods of five years each, exercisable at Ulta’s option.

Supply chain

The company has evolved a supply chain to distribute products efficiently

These include 4 regional distribution centres (RDCs) that support both stores and e-commerce demand, and two fast fulfilment centres (FFCs) that support e-commerce orders only.

In 2023, Ulta opened their first market fulfilment centre (MFC), which are smaller than RDCs MFCs focus on the most productive products and supports e-commerce sales and store demand, improving service and responsiveness, especially in markets with high store and population density. In addition, 400 stores fulfil e-commerce orders as part of their ship-from-store program.

Inventory is shipped from our suppliers to RDC, FFC and MFCs. These use warehouse management software systems to manage inventory to support product purchase decisions. They deliver to stores using a broad network of contract and local pool (final mile) carriers.

Like many brick and mortar retailers, they are building an Omnichannel with multiple online channels. Ulta also multiple pickup and drop-off options such as home-delivery, kerbside delivery, store pickup and Store-2-Door.

Company believes the omnichannel experience is 3x more valuable since along with driving sales, it offers a chance to communicate with customers and drive customers to stores.

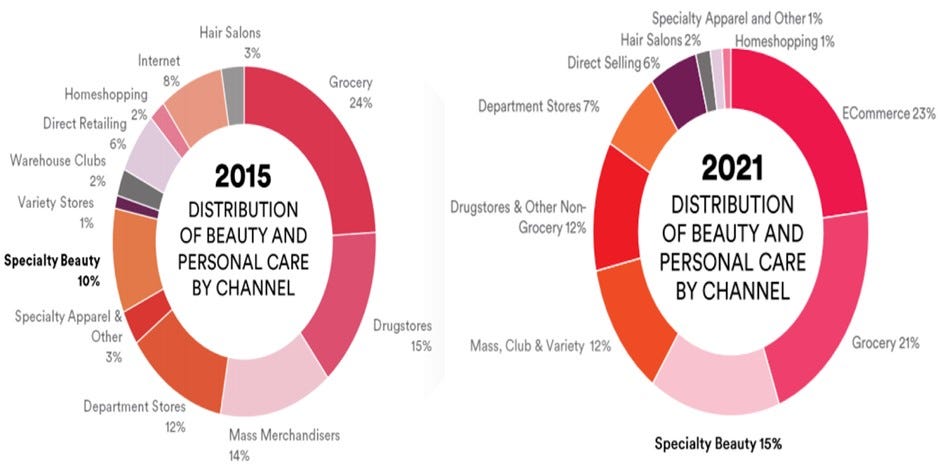

Size of the market

The beauty products and services market in the USA is over $181bn per annum. Products are about $120bn per annum while salon services account for $49bn. Ulta has a ~6% market share.

The rest of the market is quite fragmented as seen in the graphic above as Speciality Beauty Stores only have a 15% share. This suggests that Ulta has room to win market share.

When Ulta listed in 2008, the market was estimated to represent about $35 billion in retail sales. The addressable market has grown at ~7% CAGR over the past 16 years.

Ulta also has full-service hair salons in its stores and estimates that it has less than 1% share of that market. Only about 3% of Ulta’s revenue in FY22 came from the services category.

Private Label Collection

In order to further monetise its extensive store presence and understanding of consumer behaviour, Ulta launched its own private label line known as Ulta Beauty Collection. This collection along with its permanent tie-ups for exclusive products from brands accounts for 4.5% of total sales.

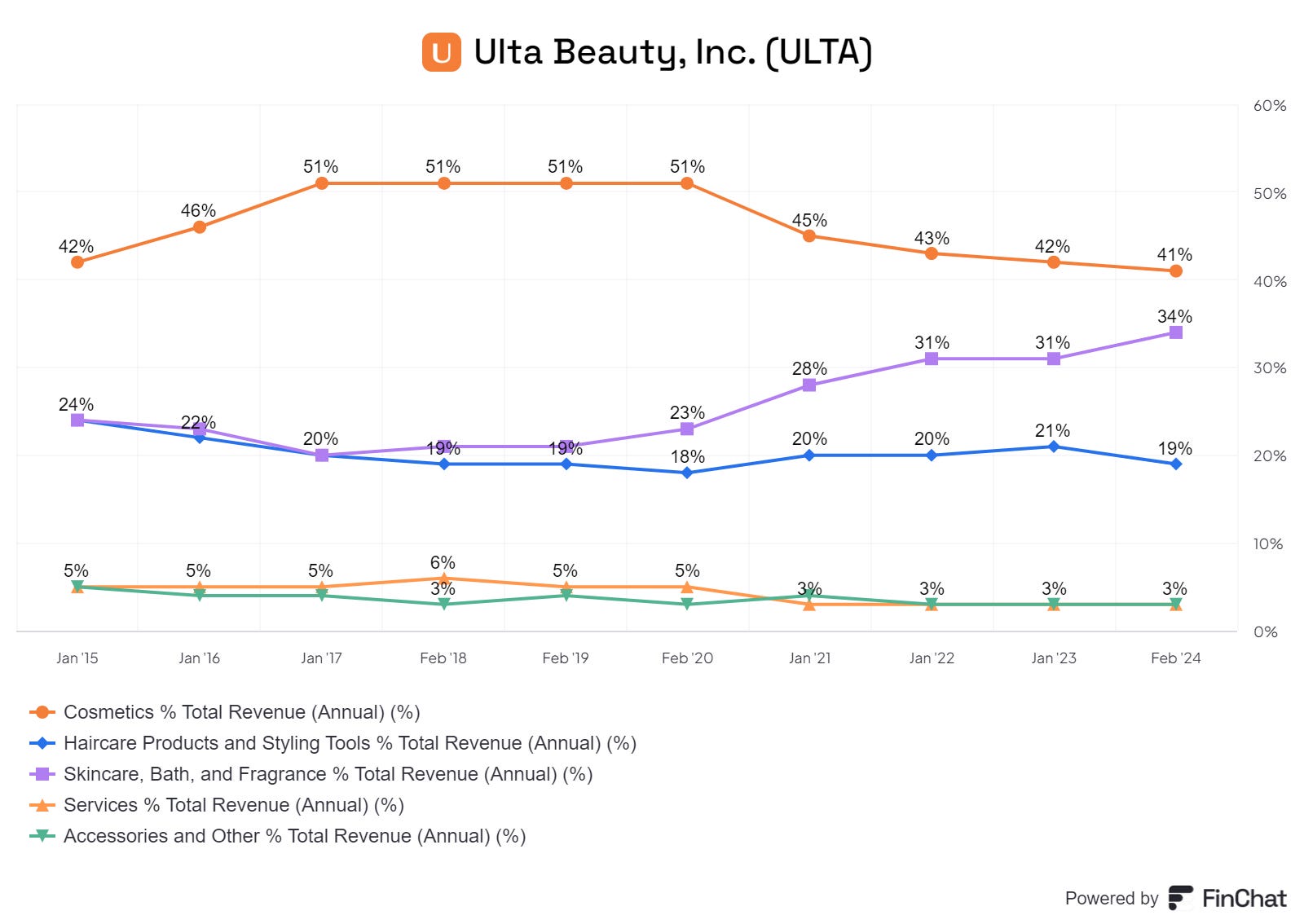

Sales breakdown

The broad categories of types of sales are

Cosmetics (41%)

Haircare (19%)

Skincare, Bath and fragrances (34%)

Omnichannel Experience Evolution: Recognizing consumers' preference for physical store interactions alongside the convenience of digital channels, Ulta seeks to blur the lines between these experiences. Plans include expanding physical store presence, enhancing service offerings, and leveraging digital innovations to create a seamless omnichannel journey.

Digital Engagement: Ulta Beauty's online platforms, including its website and mobile applications, are designed to offer engaging, interactive, and personalized shopping experiences. In FY 2023, 18% of loyalty members shopped both in-store and online. The digital platform serves dual purposes: generating sales and driving traffic to various Ulta channels. Omnichannel customers, in particular, are highly valued, spending significantly more than those who shop exclusively in retail

Competition

Ulta faces a lot of competition. For beauty products, competitors include traditional department stores, specialty stores, grocery and drug stores, and both the online operations of national retailers/brands and pure-play e-commerce entities such as Amazon.

Their most similar competitor is Sephora, which is owned by LVMH. It is a global player and has over 400 stores in the US and in-store tie ups with JCP Penney (450 locations) and Kohl’s (soon to be 100 locations). This article compares the consumer experience between the two stores.

By 2023, Sephora at Kohl’s has surpassed $1.4 billion in sales and sales projection for 2025 is more than $2 billion. Sephora total 2023 sales in the US were nearly $ 8bn compared with $ 10bn at Ulta.

The salon services and products market is highly fragmented, and competition is from both chain and independent salons.

Historically, beauty products were primarily sold at large grocery retailers and department stores such as Macy’s. However, the industry has seen a channel shift over the past few decades with more of the sales coming from e-commerce and specialty beauty retailers – between 2015 and 2021, specialty beauty retail grew from 10% to 15% of channel distribution while grocery declined from 24% to 21% over the same frame. Ulta has been a beneficiary of this trend in the last ten years.

International Expansion

Ulta Beauty announced plans for international expansion into Mexico in 2025 through a joint venture with Axo. This move aims to leverage Ulta Beauty's differentiated value proposition in the sizable and growing Mexican beauty market. This is seen as an incremental long-term opportunity to grow its international footprint and introduce its differentiated retail model to new consumers.

Key Financial Metrics

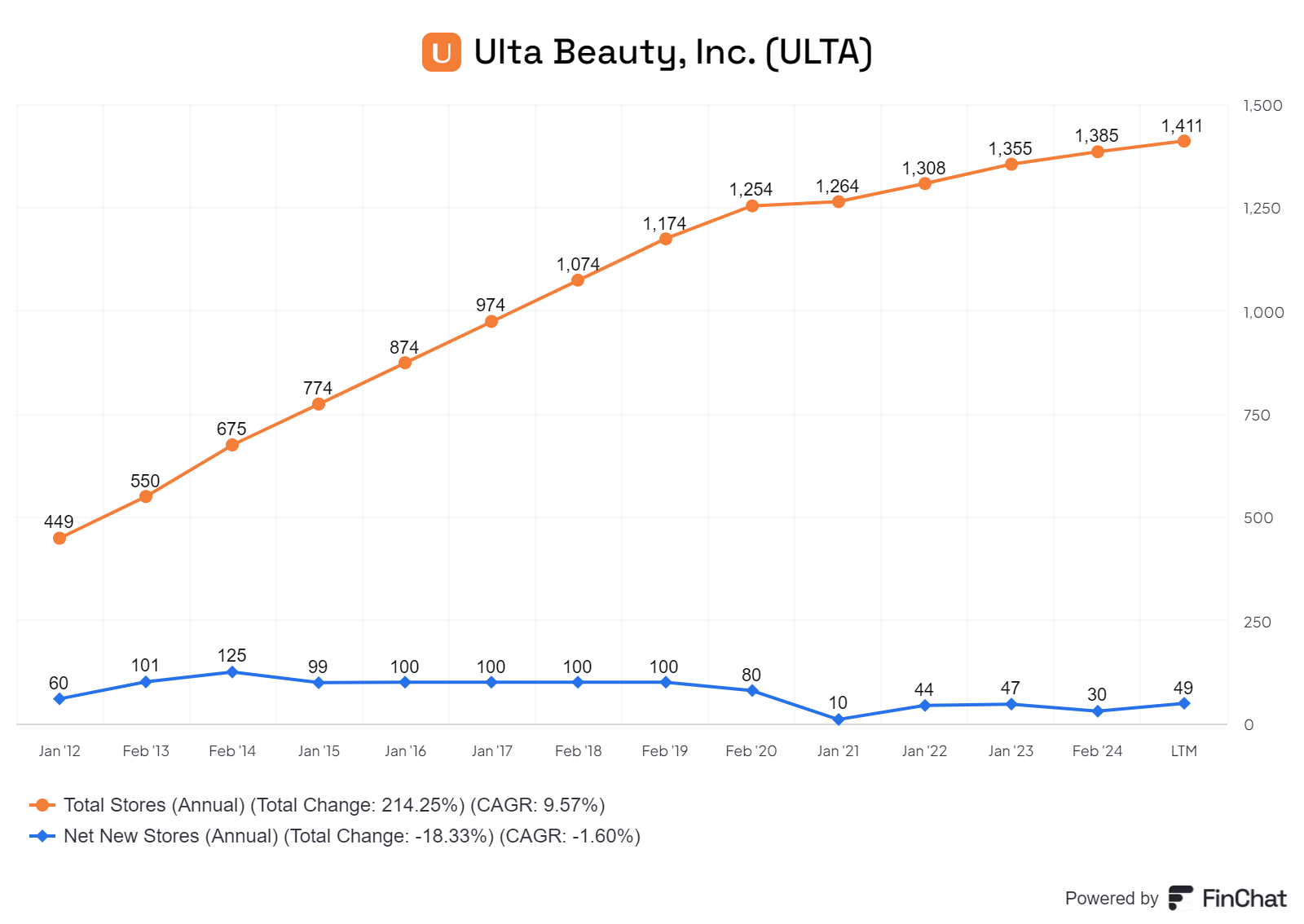

The chat below shows the growth of Ulta stores.

The company has gone from 450 stores in 2012 to 1411 currently. They have added ~ 1000 stores in 12 years. In recent years, it has been adding about 30-50 stores a year. (~2% to 3% a year).

The company estimates they will hit market saturation with 1500 -1700 stores. At the current rate of expansion, saturation will be reached in 2 -5 years.

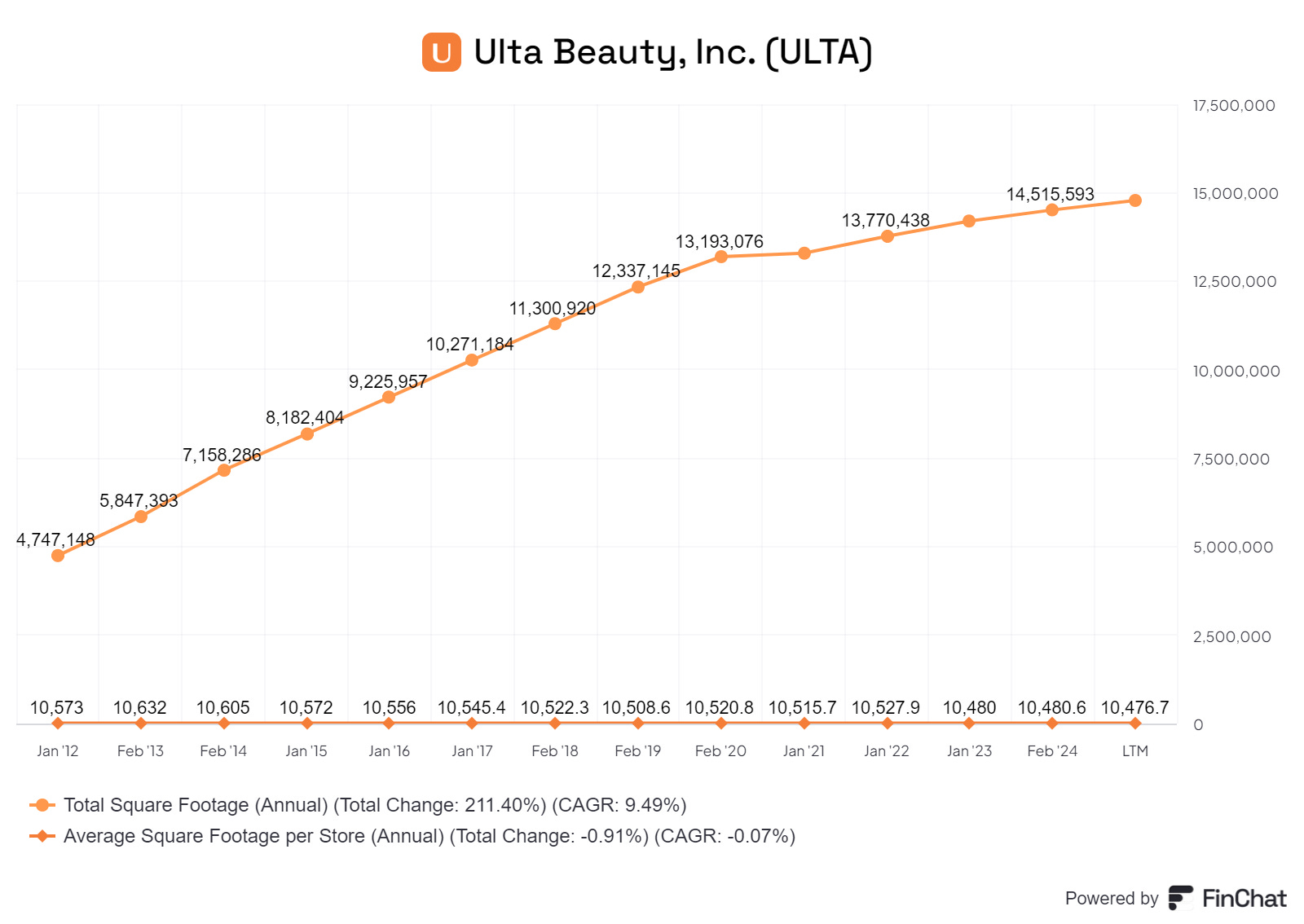

Each store is about 10,500 square foot. In 12 years, the total square footage has increased from 4.7mn to 14.5mn square feet and may peak at between ~15.75mn and ~17.9mn sq. ft.

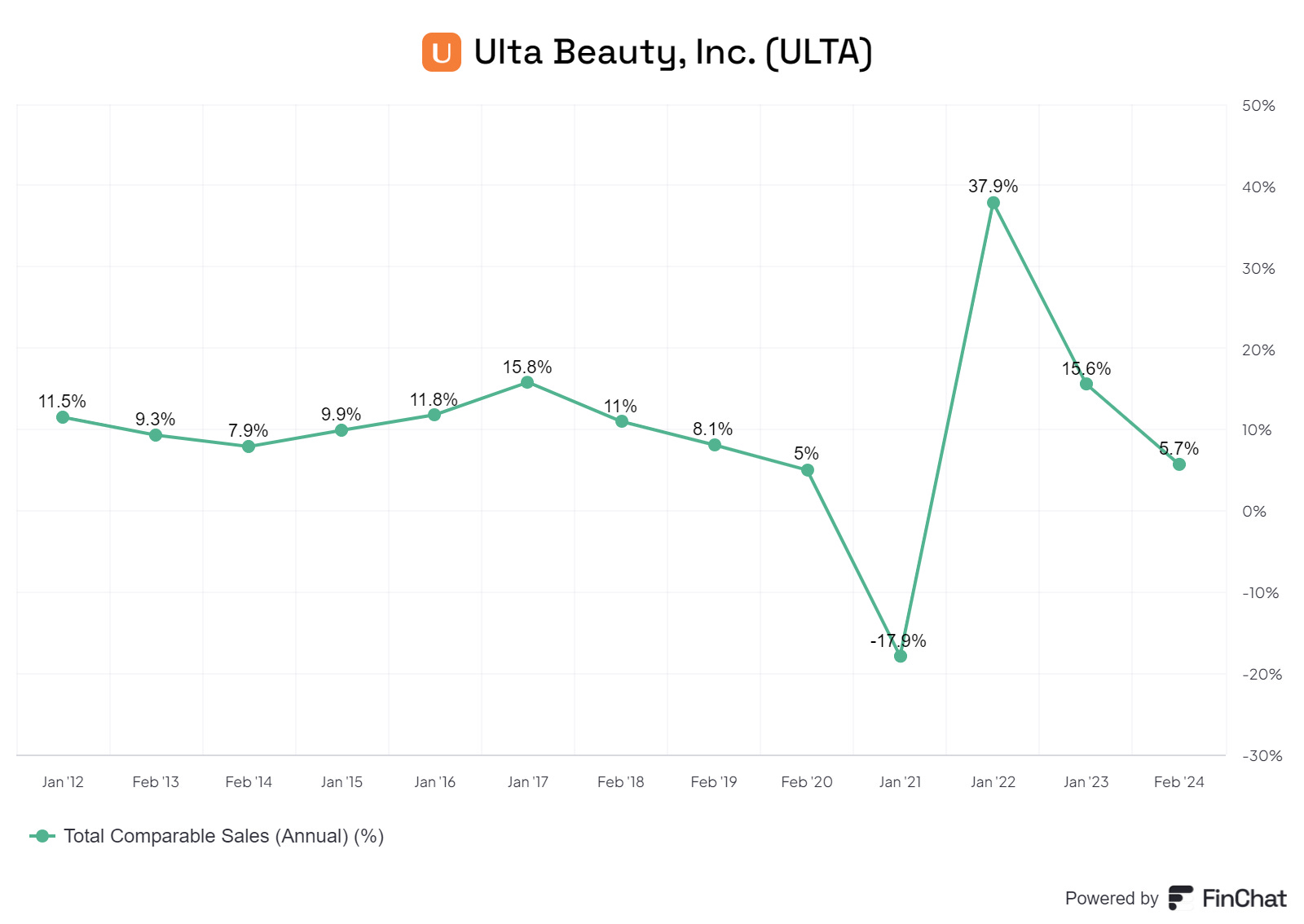

Every year, there will be some increase in sales simply because new stores are added. We want to tease out underlying same stores sales growth; i.e the growth in established stores only. We understand this data is captured by comparable sales growth and this is shown in the chart below.

Sales were hit hard in 2020/21 during the Covid 19 Pandemic. There was a strong subsequent recovery as sales normalised after lockdowns ended. Comparable sales are at 5.7% and could fall back to the 5% level seen in 2020.

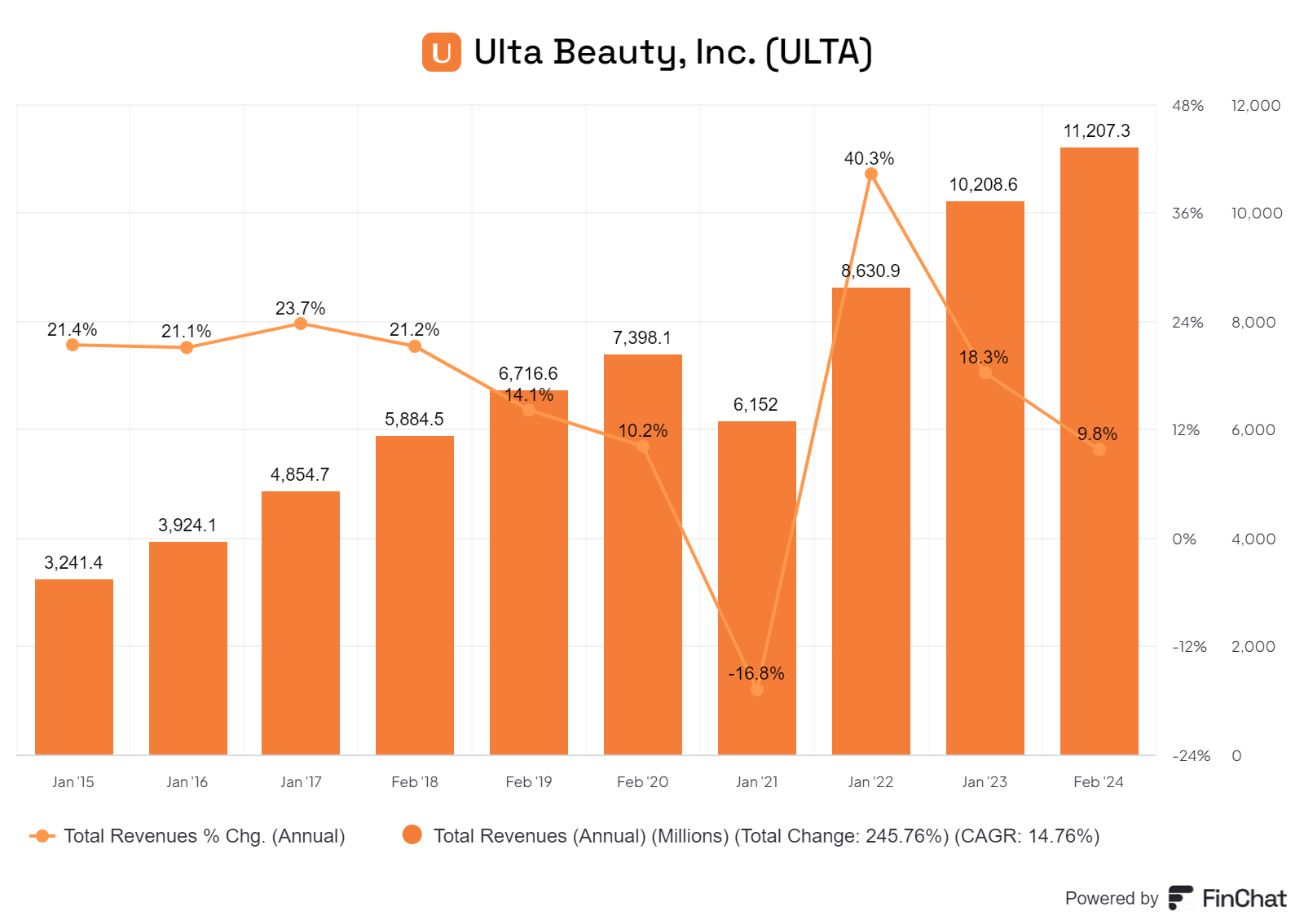

Total annual sales have risen from $ 3.2bn in 2014/15 to $11.bn in 2023/24. The chart shows the Covid19 dip in 2020/21.

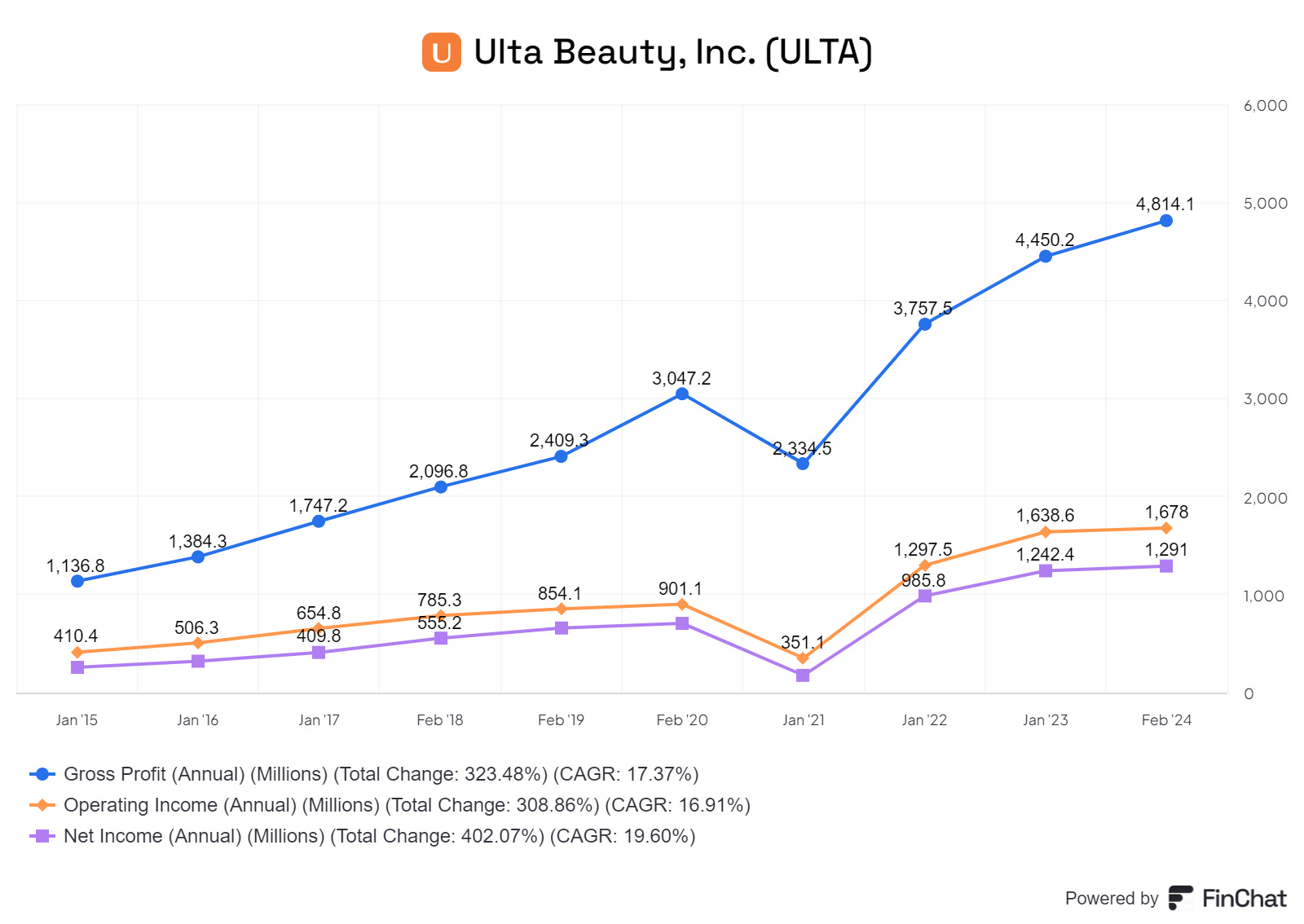

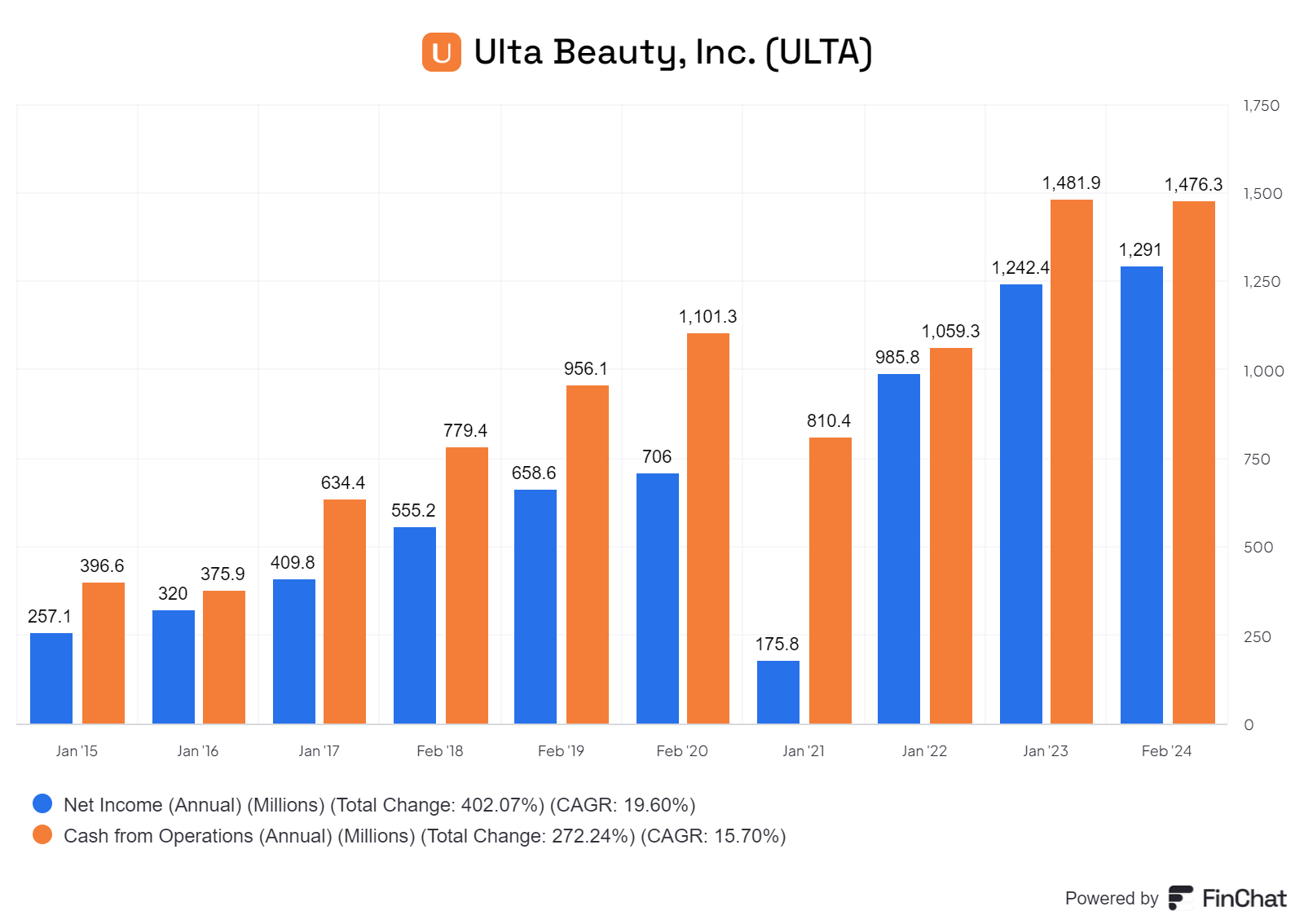

Profits at the Gross, Operating and Net level have grown steadily in the last 10 years.

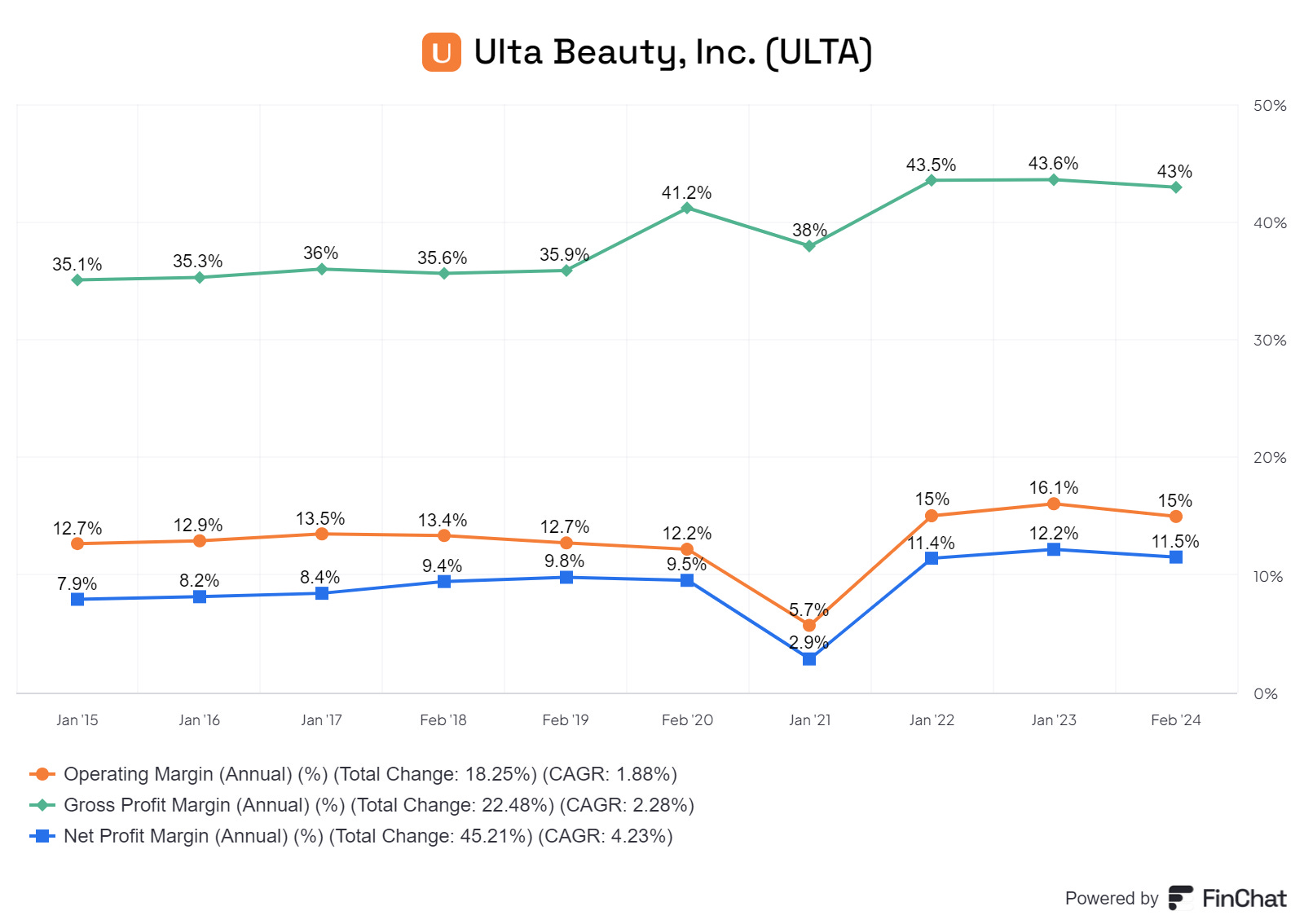

The data shows the net margin trends. Operating margins at 15% are much higher than the 3% - 4% of general volume retailers such as Walmart, Target or Costco but are like those of Tractor Supply – a specialist retailer that we wrote about here.

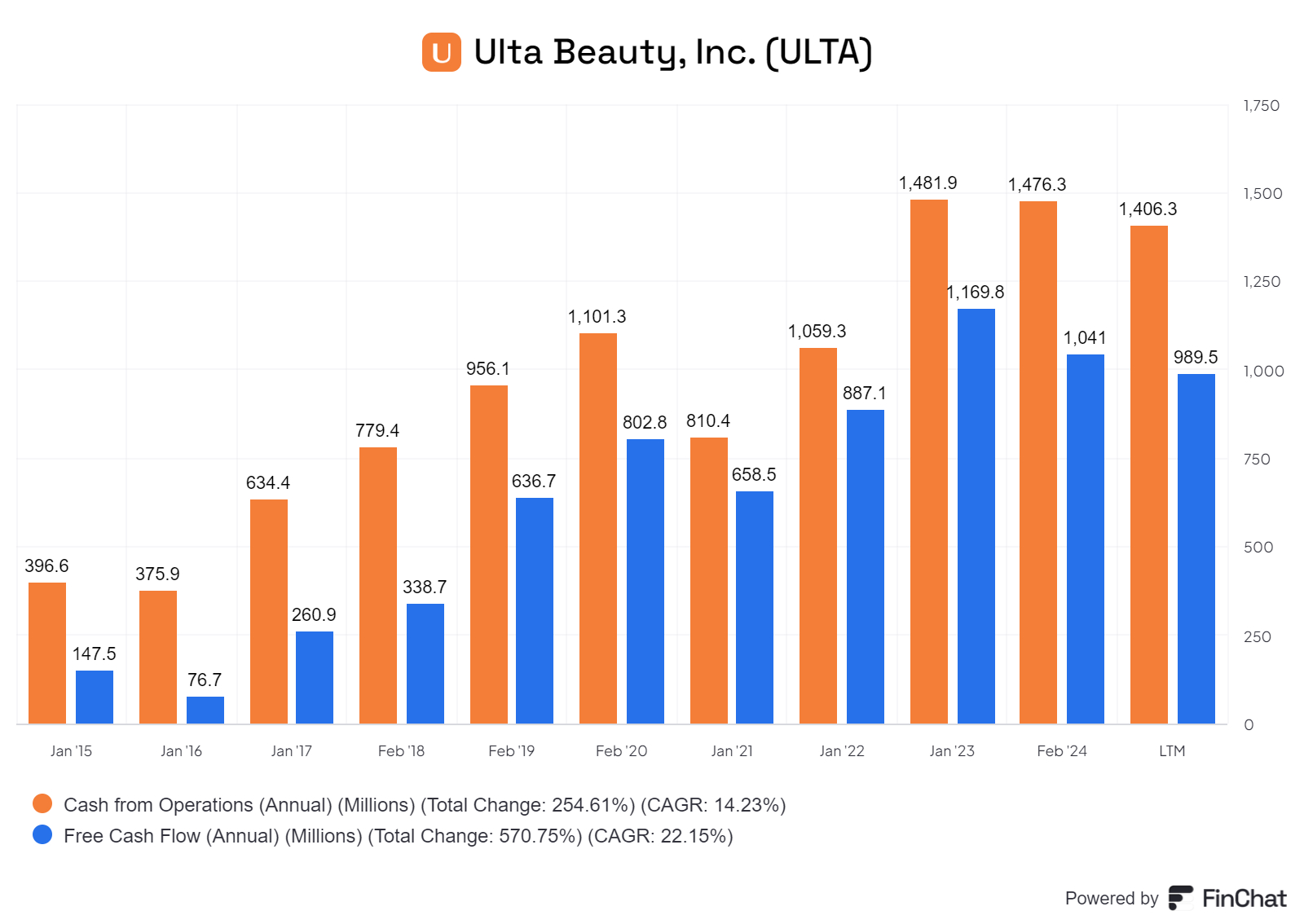

Profits and operating cash have grown steadily in in lock step in the last ten years.

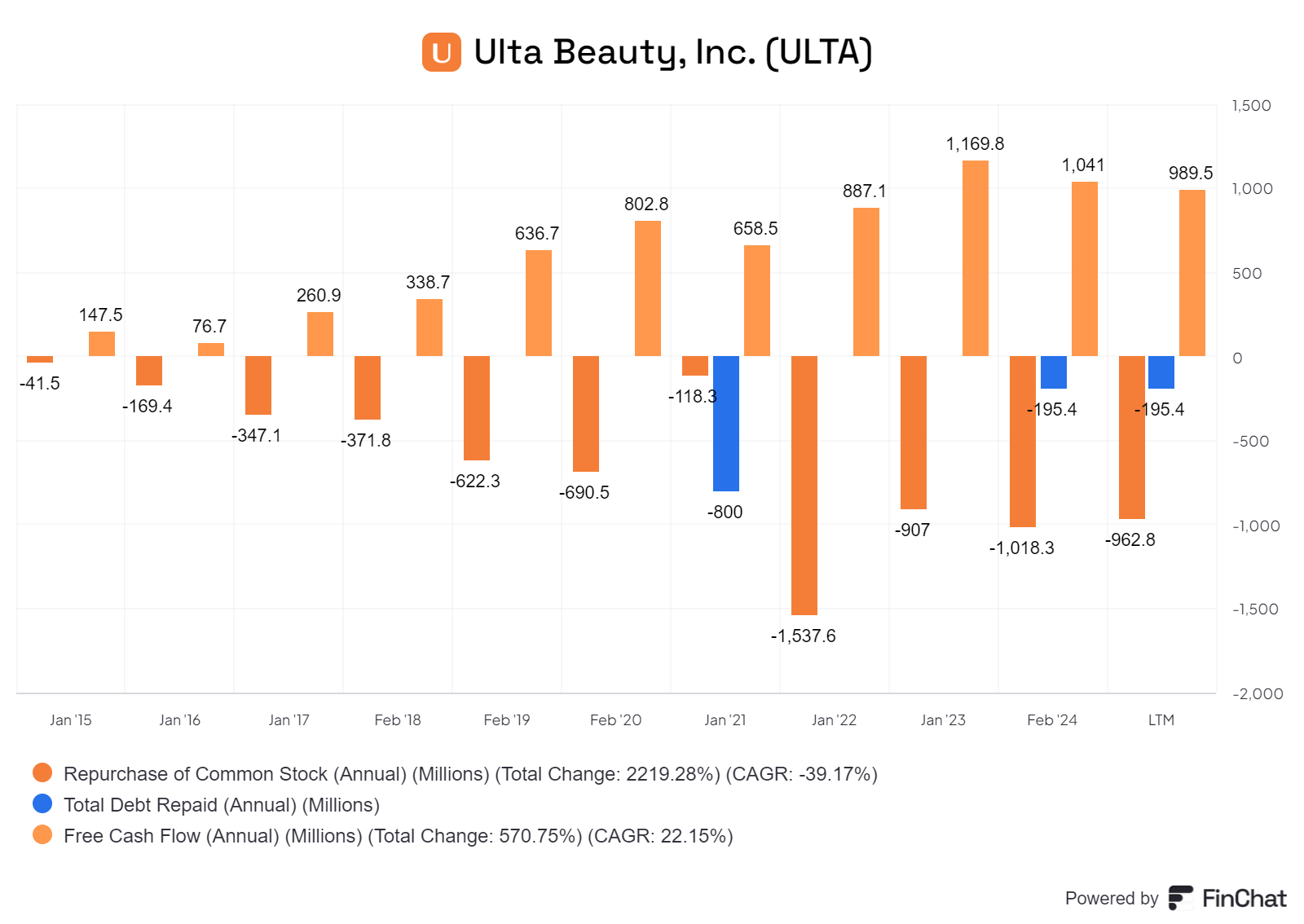

Free cash flow has also risen steadily in the last ten years. The company used most of the available free cash flow to buy back shares. Ulta no longer has any debt (other than the store leases) and does not pay a dividend.

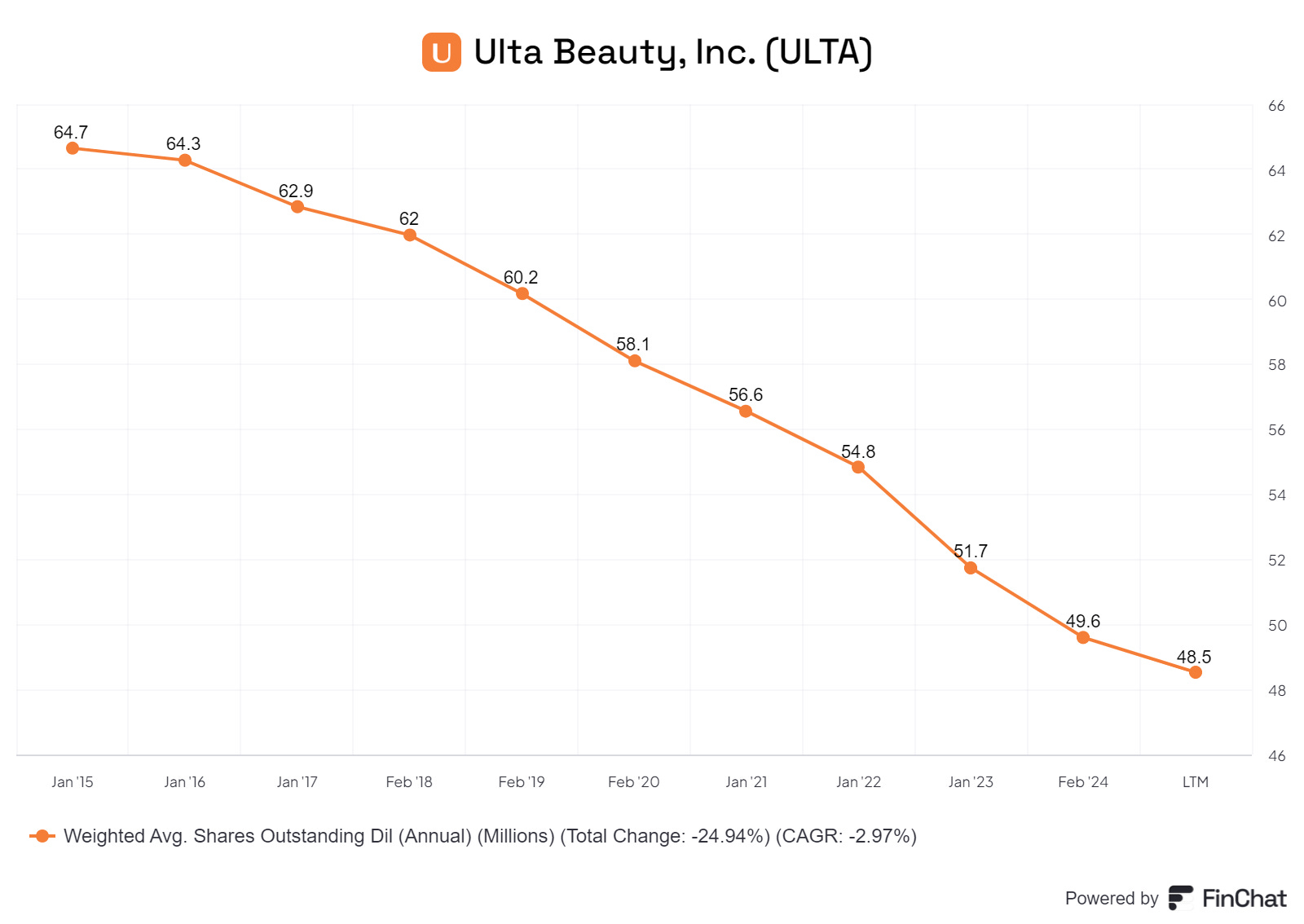

There has been steady decrease in the average number of shares outstanding from 65mn to about 48.5mn in the last ten years.

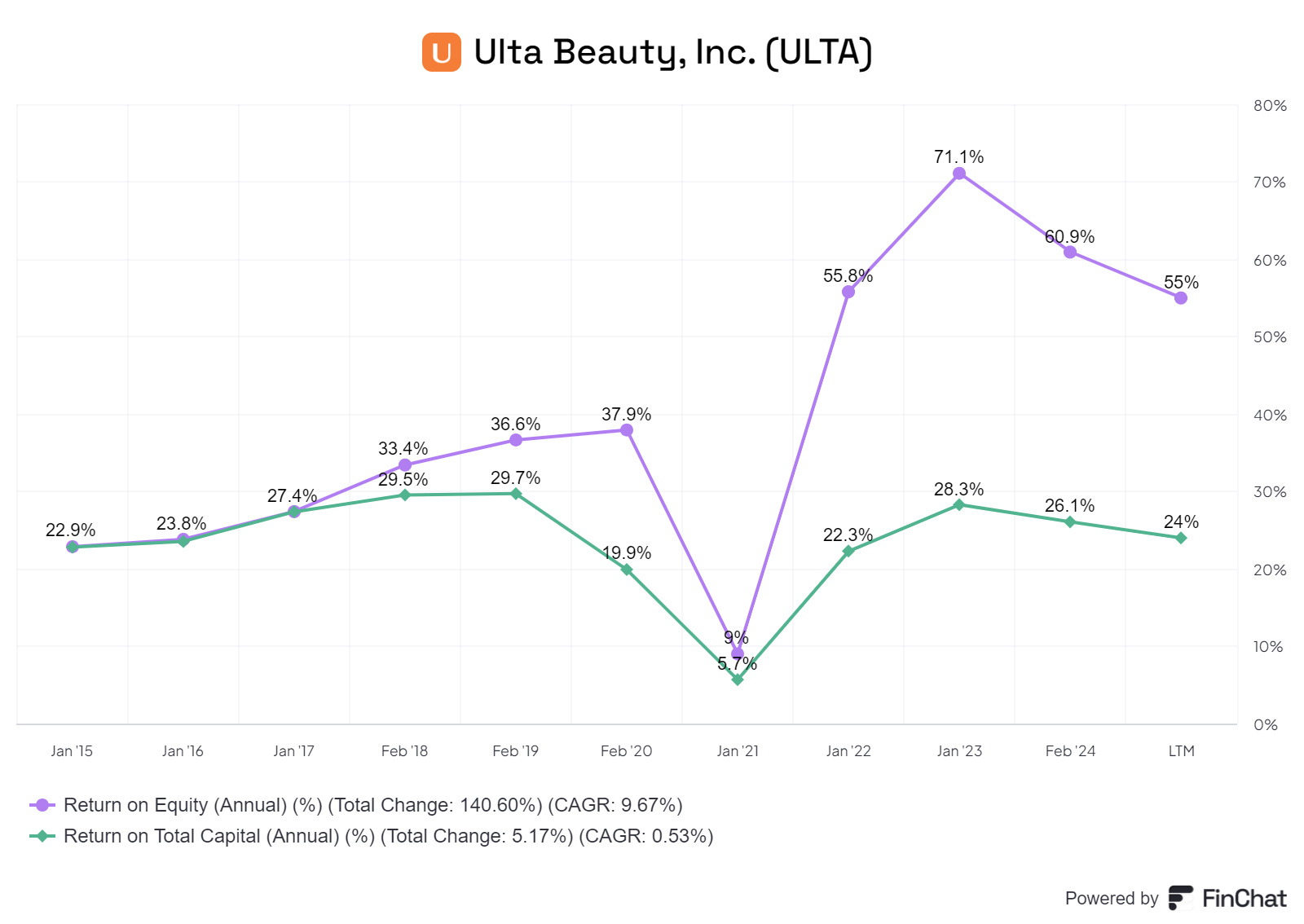

The company has been become more profitable in recent years with an ROE of 55% and the Return on Total Capital of 24%.

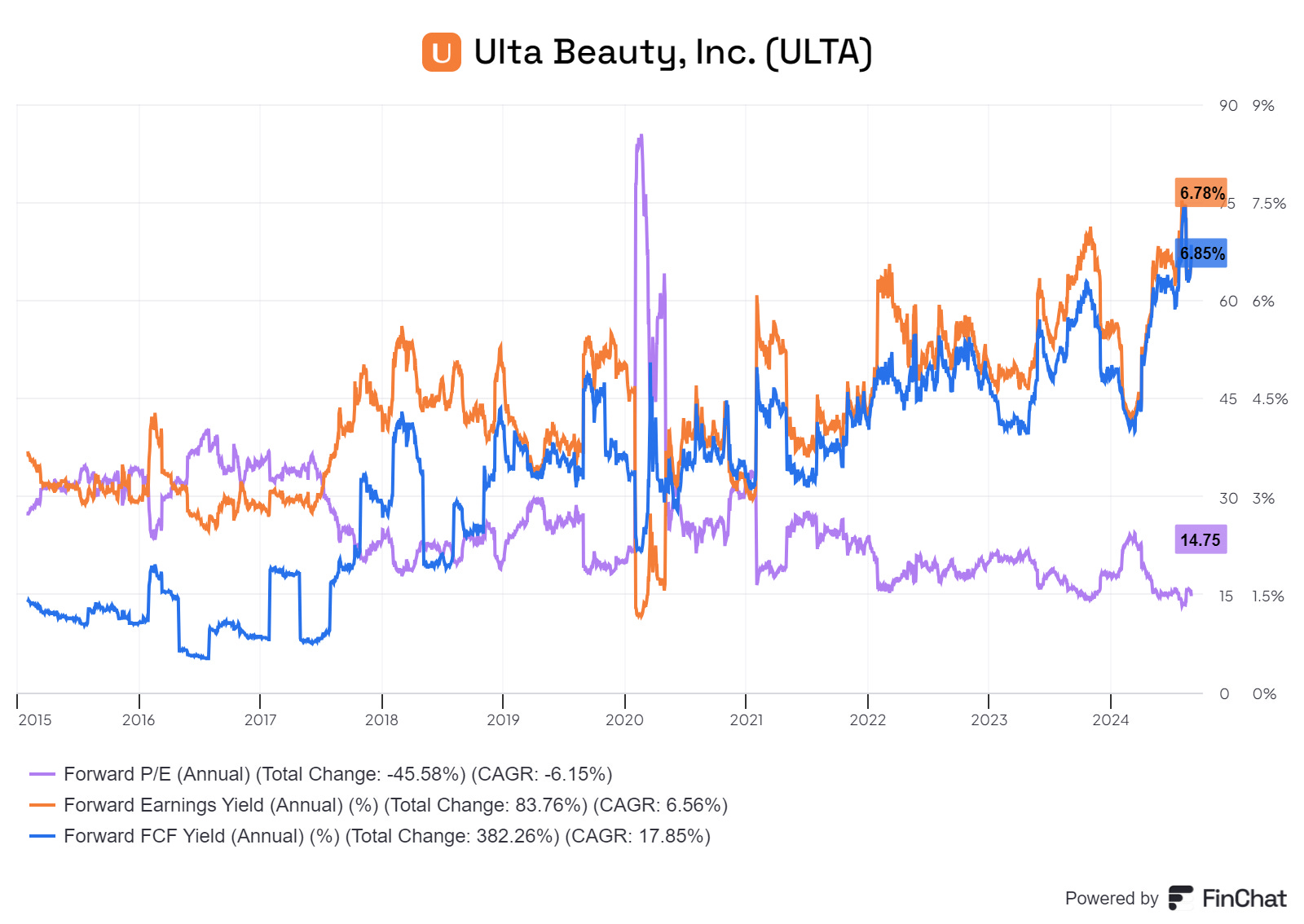

The 1-year P/E multiple of the company has trended lower and is currently at about 14.5X. times- very much at the lower end of the historical range.

Ulta Beauty has consistently increased its revenue and income in recent years. The company has consistently increase Operating Cash and Free Cash Flow (FCF). It has sustained high margins and profitability, as evidenced by its margins and the high ROE and ROTC.

Detailed Analysis

If we step back and look at this industry, the clear value lies in the Brands. These are owned by companies such as L’Oreal, Unilever, Proctor and Gamble, LVMH Estee Lauder, Revlon and so on.

LVMH and L’Oreal brands: LVMH brands include Christian Dior and Guerlain and their retailer, Sephora is competitor to Ulta Beauty.

The pricing power and high returns are often achieved by brand owners esp in the premium segment of the market.

Retailing is more competitive. The brands have the upper hand and the sector has low barriers to entry and a lot of competition. However, Ulta has done relatively well in a tough sector and has given CAGR 15.8% total returns in the last 17 years.

The company seems to have a successful formula- it stands out as a high-quality business. One source of its strength is the loyalty programme called Ultamate Rewards, Customers deeply value the customer experience and a large number of them have become loyal participants in the membership programme.

The programme allows Ulta Beauty to gather valuable customer data, which is used to enhance the customer experience and drive achieve financial returns. Ultamate Rewards has 42.2 million active members, and 95% of total sales comes from rewards members. The programme also allows Ulta to convert customers that typically only buy in-store into multi-channel shoppers. This is important as omni-channel shoppers spend 2.5 times to 3 times more than single channel shoppers. Importantly, the increase in spend is largely incremental rather than cannibalistic.

Another factor in the success is that Ulta has steadily gained access to more prestige brands as it has become a nationally recognized retailer. E.g. MAC Cosmetics started to sell its products in 25 Ulta Beauty stores as well on Ulta’s e-commerce platform in 2017. Today, MAC Cosmetics are in nearly every Ulta location. The story is similar for brands like Clinique and Estèe Lauder as well.

An Ulta store stocks more than 600 brands compared to a Sephora carries only around 200 brands (Sephora focus much more on Premium brands). Ulta customers have a larger assortment and across multiple price points.

The strategy is to get customers through the door and spending. Overtime some will migrate towards the prestige brands. That requires customer retention, and the rewards programme works here. The in-house Salons also generate regular visits to the stores.

Another factors is Ulta Beauty Collection which are the private label brands. These have probably contributed to the growth of margins. Private label products have allowed Ulta to deliver differentiated products and packaging that adds to its value proposition of having more products and brands compared to competitors.

Store openings

As noted above, Ulta has used operating cash to invest in new stores over the years. The pace of store building has slowed down in recent year to about 30-50 stores per annum.

The company estimates that they will hit market situation with 1500 -1700 stores. At the current rate of expansion saturation will be reached in 2 -6 years. Once it is at saturation, growth will slow and depend on overall market growth and market share gains (if any).

The company is expanding in Mexico, but it is difficult to know how many stores will be opened there as they intend to expand there slowly.

The years of sales growth due to new store openings are almost over. The cessation in new stores will lead to higher free cash flow levels but lower sales growth.

Lower store opening means a reduction in capex and an increase in free cash flow. The company could increase amounts returned to shareholders either by increasing the pace of share re-purchases or by initiating dividend or both.

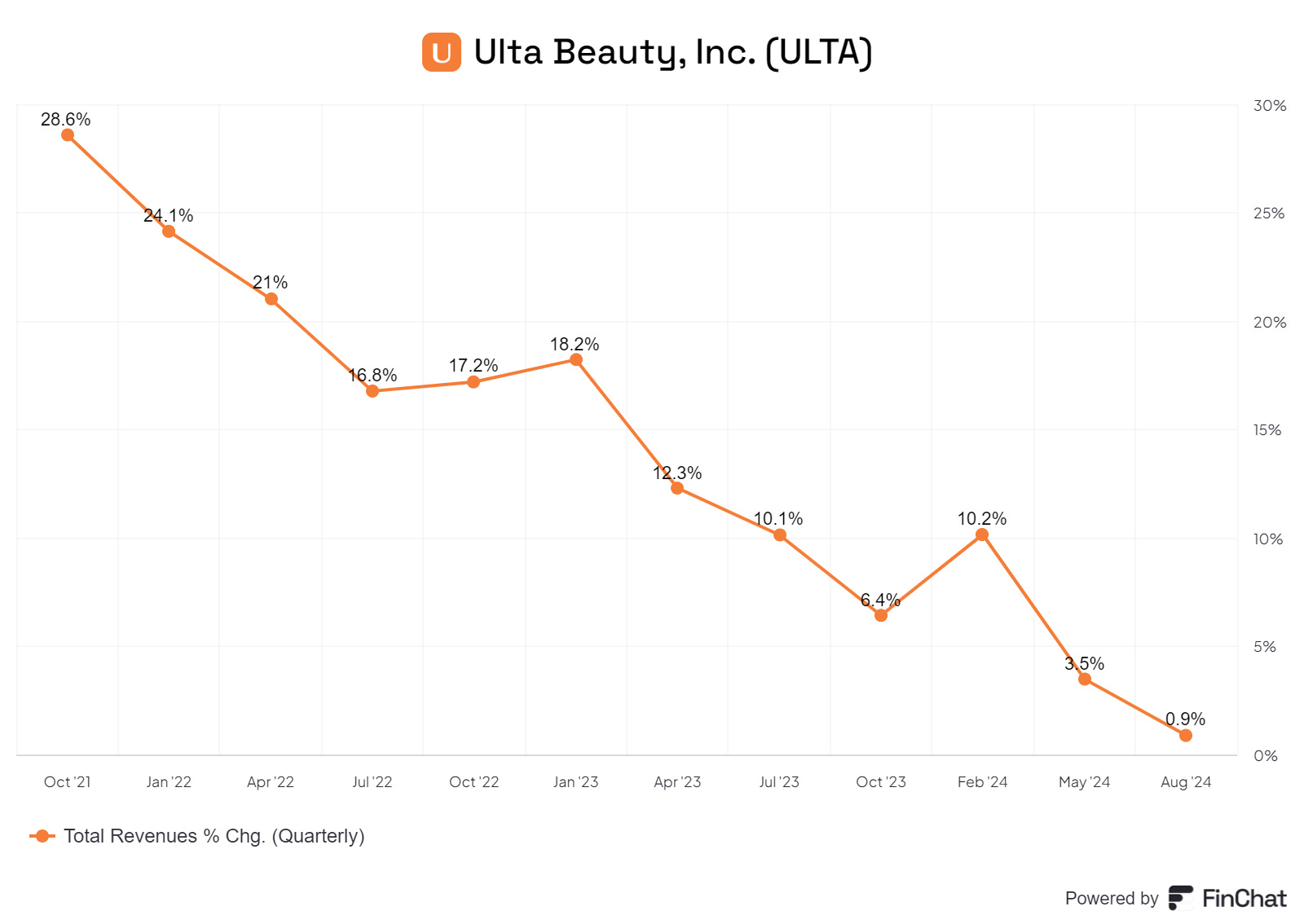

As new store openings slow, overall sales growth is likely to fall towards the comparable sales growth. The latter is at 5.7% and on a declining trend.

Give these perspective changes in capital allocation, the historical returns on capital may not be a good indicator of the future.

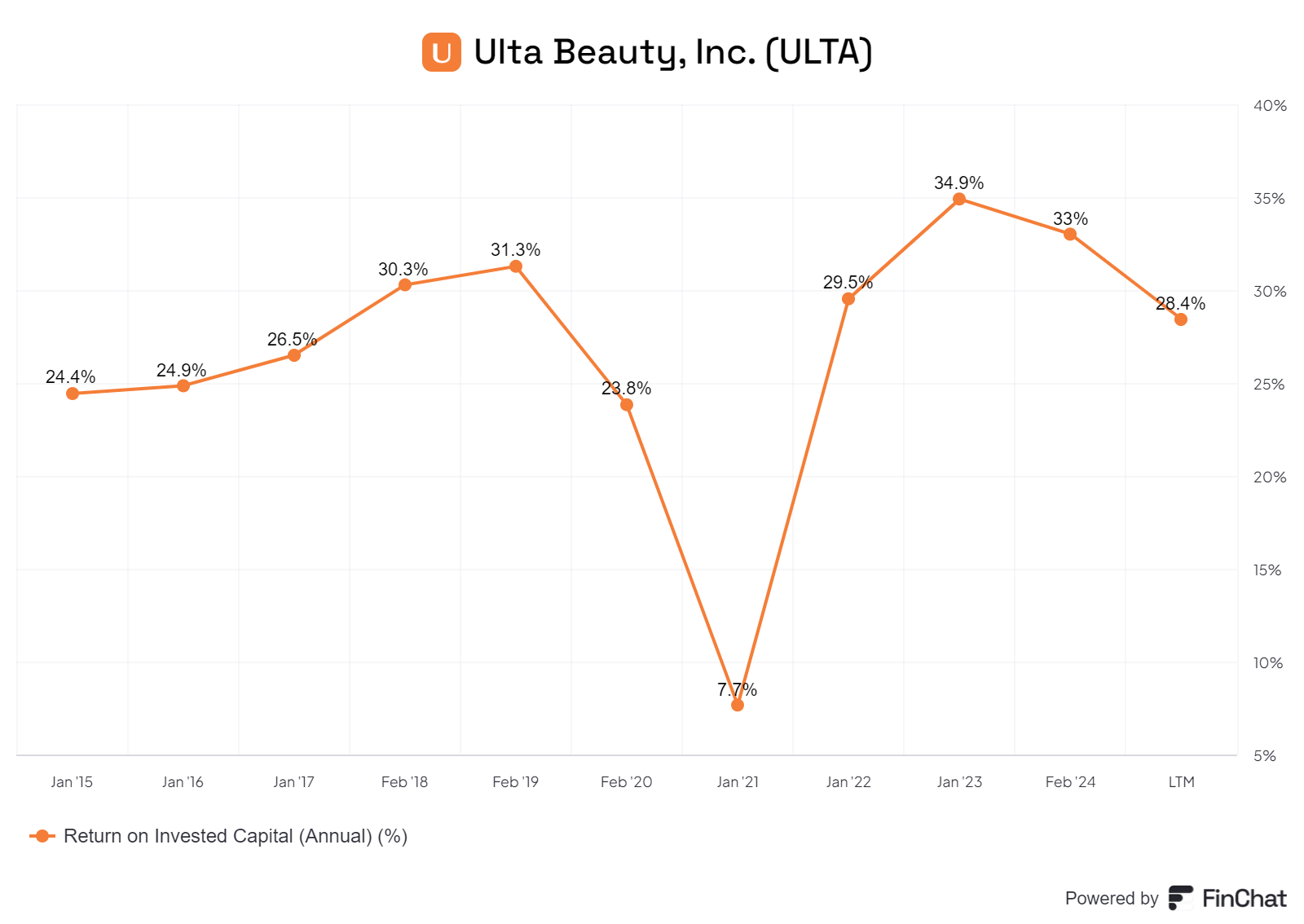

Let us consider Return on Invested Capital (ROIC).

.

ROIC is currently 28%. Management has shown that they can find attractive capital allocation opportunities, but it is likely to be difficult to maintain the current high returns over the medium-term.

Share price performance

Ulta’s share price has fallen 32% in the last year and by 41% in the last six months.

It is currently trading on a Forward P/E ratio of 10.2X and a forward Price/ FCF ratio of 12X. This implies an earnings yield of ~10% and Free Cash Flow Yield of ~8.5%.

This raises two questions.

Why has the share price been so weak ?

Are the current low valuations compelling?

Weakness of the stock price.

The weakness of the stock price may reflect several factors. These include

Negative sentiment towards the industry: Share prices of companies such as Estee Lauder, L’Oreal and LVMH have also declined significantly in 2024.

Worries about the US consumer. :There are widespread fears that US consumers have run down the cash reserves that they built up during the pandemic and are facing more difficult. Many consumer stocks have reported poor results and have commented on the weakness of consumer sentiment.

Slowing sales growth at Ulta: Quarterly sales growth have been on a declining trend and the most recent quarterly sales growth was just 0.9% (q/q).

The company discussed these issues during their most recent earnings conference call.

“net sales increased 0.9 percent to $2.6bn and comparable sales decreased 1.2%...Although we anticipated the headwinds experienced in the Q1 would continue, our results were short of our expectations, driven by a decrease in comp store sales, specifically comp store transactions.”

“There was a 1.2% decline in comparable sales. (This) was driven by a 1.8% decline in transactions, which was partially offset by a 0.6% increase in average ticket.”

Ulta argued there three reasons for the poor performance.

Growth normalizing after 3 years of unprecedented gains.

There is a change in consumer behaviour as consumers increasingly focus on value and become more cautious with their spending.

“U. S. Beauty growth slowed to approximately 3% through H1 2024, with Prestige Beauty experiencing high single-digit growth and mass beauty maintaining low single-digit growth.”

Competition intensity seems to have increased.

“Today, there are significantly more places to buy beauty, especially prestige beauty with more than 1,000 new points of distribution opened in the last 3 years.”

“More than 80% of our stores have been impacted by 1 or more competitive opening in recent years, with more than half impacted by multiple competitive openings”

“We now expect next sales for the year will be between $11bn to $11.2bn with comp sales in the range of down 2% to flat.”

Concluding Thoughts

The short to medium term out looks challenging for this impressive company.

However, the valuation looks very attractive.

If the company can go back to comparable sales growth of 3%-5%, Ulta should be able to generate high and growing Free Cash Flow which can be paid out to shareholders as dividends or be used to reduce the share count and thus boost EPS.

We need to evaluate the numbers to consider the future trajectory of earnings and free cash flow. This will help us do a valuation to determine whether the stock is at a good entry point.

Good compilation, as usual. My 20+ daughter says that new make-up stuff is bought better at stores as she could try it out, but repeat buys would be online. In the former (store purchase) case, pharmacies offer potentially cheaper prices. So it's a mix between Ulta, a local pharmacy and online. If this was true (and I asked her if she represented most women in her age group, she said yes) Ulta's future growth would be driven by fresh customers, existing customers moving up the income curve and new stores making it convenient for them to visit one. Too complex to predict profit growth then?

Hi Sanjiv, nice writeup. Writing as a shareholder here. Something to consider - if consumer preferences for purchasing cosmetics moves more online rather than in store, what stops the consumer from shopping directly from L'Oreal or Estee Lauder whom make up 55% of sales, or other smaller brands? Presumably it's cheaper with faster shipping to shop directly from the manufacturer. In this case Ulta could lose the shoppers that know what they want, or that just need to restock on what they already have.