Wipro Ltd is a Bangalore-based lobal Information technology, consulting and business process services (BPS) company. It is the 4th largest Indian ITES behind TCS, Infosys and HCL Technologies. WIT is listed both in India and in the United States via a US dollar-denominated ADR offering. Global investors can buy this stock in dollars.

Wipro Limited was founded in 1945, as Western Indian Palm Refined Oils Limited. It was a processor of a vegetable oil called Vanaspati. It had been founded in Amalner in rural Maharashtra by MH Hasham Premji and has been listed on the Bombay Stock Exchange in 1946. Premji owned 74% of the company. Many residents of Amalner, including farmers and shopkeepers, were given shares in Wipro as part of their employment or through community investments. Many has invested just INR100 in the early days. They received stock certificates and probably forgot about them for a few decades. Other locals had bought small amounts over the decades.

In 1966, Hasham Premji died suddenly of a heart attack and his 21-year-old son Azim Premji had to cut short his studies in Engineering at Stanford and came back as Chairman and CEO. He inherited a 74% stake in the company.

Under Azim Premji’s leadership, Wipro underwent a strategic transformation. Premji diversified the company to bakery fats, toiletries, hair care soaps, baby toiletries, lighting products, and hydraulic cylinders. In the 1980s, the company recognized the potential in the emerging IT sector and diversified into technology services. WIT started growing rapidly and the original non-IT businesses account for less than 1% of revenue.

By the late 1980s and early 1990s, many small shareholders in Amalner were worth over $1mn US dollars. Some entrepreneurial Mumbai brokers went to rural Maharashtra to proclaim the good news, find the many newly wealthy shareholders and grab their business.

We have already looked at India’s ITES companies with notes on Infosys and TCS. Wipro is a smaller player in the same sector and has similar business model. It has followed a more acquisitive strategy than TCS or Infosys. All of these acquisitions have been outside India with a fair number in the USA. Most of them have been small. There have been a few exceptions to this- the most notable was CAPCO – a risk management and technology consultancy focused on the banking industry- which was acquired in 2021 for $1.45bn.

Like the others, Wipro has maintained a strong balance sheet, exhibited stable operating margins and combined healthy cash flows with steadily rising dividends. Its growth rates and profitability have lagged those of TCS and Infosys.

The company had a total of ~1,300 active customers. There is some significant concentration of large clients and a large tail of smaller clients. The top 5 and top 10 clients contributed 14% and 22% of revenues respectively.

The company has ~234,300 employees.

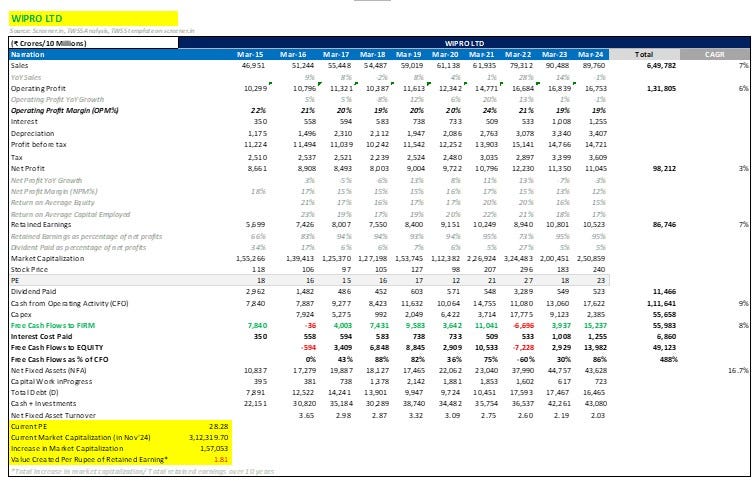

WIT 10-years Financial Summary

The slide above gives a good snapshot of select WIT numbers in the last ten years

The numbers are in Indian Rupees but the final column, which shows the CAGR percentage growth rates, is easily understandable.

In the last ten years Revenues and Operating Profit have grown at CAGR of 7% and 6% respectively. Over the same period, Net Profit has grown at a CAGR of 3%. This is a noticeably worse performance compared with TCS and INFY.

Cash Flow from Operations have grown at CAGR of 9% over the last ten years.

The second last column (in the slide above) shows the ten-year cumulative data for select items on the Income Statement.

The cumulative ten-year Net Profit is INR 98,212 crores ($11.3bn). (A crore is 10mn). The cumulative cash flow from operations is also shown in this column and it is INR 111,641crore ($13bn), higher than the cumulative net profit figure. This indicates WIT has been able convert more than 100% of net profits into operating cash flow.

Operating Profit Margin is around 19% while Net Profit Margin is 12%.

Return on Equity and Return on Capital Employed reached 15% and 17% respectively in FY 2024.

Again, both these numbers are noticeably lower than those achieved by TCS and Infosys

Towards the bottom of slide above, we see at WIT’s total debt of INR 16,655 crores ($1.9bn) is higher than Infosys debt but it is below the Cash and Investments which are INR 43,080 crores ($5.1bn) so WIT, like INFY and TCS, has negative net debt.

We also highlight the last unit in the slide which is highlighted in yellow. This shows the value created per each rupee of retained earnings is 1.8 rupees. This metric is based on a Warren Buffett idea. He outlined the circumstances in which a company should retain earnings beyond those needed for necessary capex, rather than distribute it to shareholders.

“For a number of reasons, managers like to withhold unrestricted, readily distributable earnings from shareholders – to expand the corporate empire over which the managers rule, to operate from a position of exceptional financial comfort, etc. But we believe there is only one valid reason for retention. Unrestricted earnings should be retained only when there is a reasonable prospect – backed preferably by historical evidence or, when appropriate, by a thoughtful analysis of the future – that for every dollar retained by the corporation, at least one dollar of market value will be created for owners. This will happen only if the capital retained produces incremental earnings equal to, or above, those generally available to investors.”

If we apply this test to WIT, we can see that over the last ten years, WITI has retained and reinvested INR 86,746 crores ($10.0bn). Over the same period, the market cap has increased by INR 157,053 Crore ($18bn or 1.8x). Hence our assertion that each Rupee retained by WIT has created 1.8 rupees of value for investors. This 1.8x meets the Buffett test but it is much less than the 7x plus shown by TCS and Infosys.

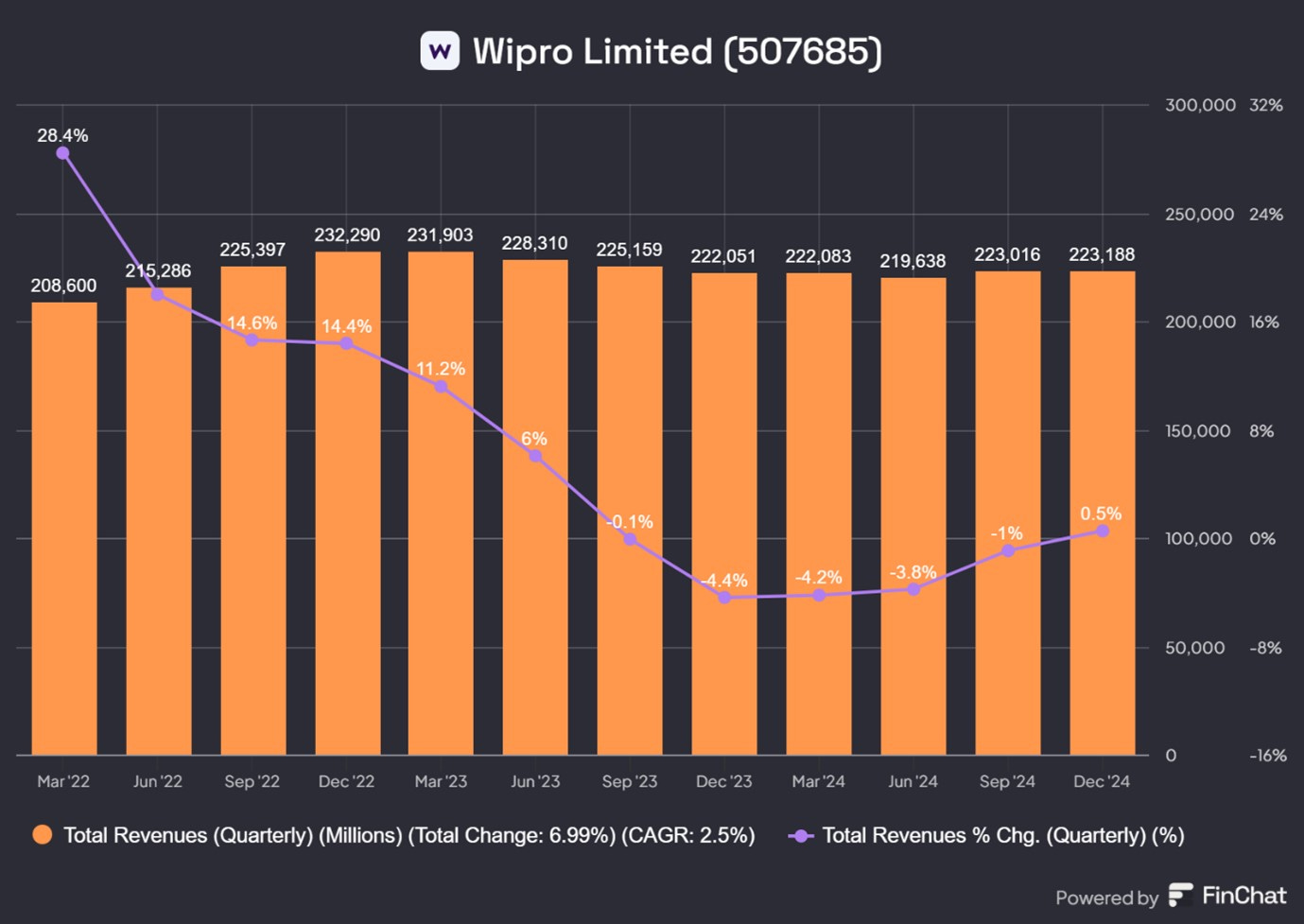

Since 2022, the rate of growth in revenue has been slowing sharply and fell into negative territory. The company has been struggling to grow quarterly revenue for some time.

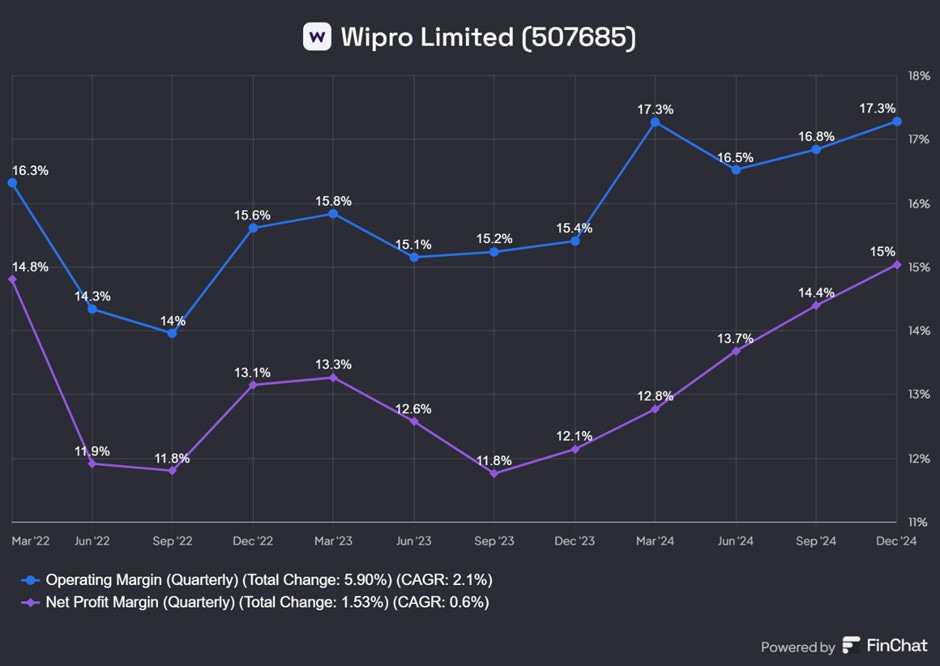

Profits were weak in 2022 and 2023 but have recovered since then in line with the growth in margins.

The company was struggling at that time and was probably a factor in the resignation of previous CEO Thierry Delaporte in April 2024.

Q3 Quarterly Results

Client budgets are usually decided in January / February and ITES companies only have visibility in March. The 3rd quarter (to end December) is a seasonally quiet quarter. Even If budgets are constrained, there may nevertheless be some discretionary spending especially if there have been some great than expected savings elsewhere.

Revenue growth was just 0.5% (y/y) but Operating Profit growth and Net Profit growth was much higher at 8.1% and 24.7% respectively.

The reason for this differential performance was the growth in margin with Operating Profit Margins were up 125bps (y/y) and Net Profit Margins rose 307bps. Therefore, Wipro continued the recent trend of subdued earnings growth but improving margins.

Highlights of the Earnings Conference call

Overall Summary

They gave a very modestly optimistic tone on revenue but are more bullish on AI.

“FY 2025 looks more hopeful and resilient. Our clients are cautiously optimistic and discretionary spending is slowly coming back. While cost optimization remains key, we expect significant growth in AI spending.”

“We are committed to driving innovation for our clients by leveraging the transformative power of AI.”

Margins have been strong

“Our operating margins came in at 17.5 percent, an expansion of 0.7% quarter on quarter and 1.5% year on year. This is a 12-quarter high.”

The BFSI consulting business, CAPCO, is performing well above the average.

“Our Capco business (large US acquisition from 2021) consulting space continued to see improved demand. Order book grew by 9% (y/y) and revenue grew 11% (y/y).”

America is strong but the rest of the world is not.

In our strategic market unit performance, we saw steady growth in demand across Americas, while Europe and APMEA remained soft for us.

Growth was primarily led by health and technology and communication sectors.

Health maintained its momentum, growing 6.7% sequentially and 4.5% year on year.

BFSI grew 3.4% year on year.

New Order Pipeline is strong

“In Q3, we closed 17 large deals with a total value of $1bn across markets and sectors.”

The largest accounts are growing fast.

“In Q3, we achieved a sequential growth of 7.3% in our top account. Top 5 and top 10 accounts grew 3.7% and 1.8% respectively.”

Financial numbers

Let me cover the financial highlights for the quarter in a few key points.

as a result of the strong in quarter execution, we delivered above the top end of our revenue guidance range, growing 0.1% quarter on quarter in constant currency terms.

our operating margins are at a 12-quarter high of 17.5%. This marks an expansion of 0.7% quarter on quarter and 1.5% (y/y). Let me also add that this was achieved after absorbing 2 months of incremental wage division. With this, the wage division impact that we did as of September 24 is fully behind us.

our EPS and net income grew 24% year on year and 5% sequentially. This was on the back of the margin expansion.

AI

They are winning deals due to their AI capability and they gave two examples.

I would like to give you two examples in this context.

1. We won a vendor consolidation deal with a leading American retail and distribution company. As a strategic partner, we will transform their merchandising, sales and supply chain functions. In fact, our AI led approach across engineering, digital, infrastructure and application services was crucial in helping us win this deal.

2. My second example is a leading airline in the Middle East that has partnered with us for end to end technology modernization. As part of a long-term contract, we will design and implement a customized cloud-based solution to improve operational agility and resource utilization. Again, using AI powered industry solutions, we will enhance employee productivity and customer experience for them. We continue to focus on our large accounts in our core markets and priority sectors.

They are gearing up to meet the anticipated growth in AI-driven demand

At Wipro, we continue to invest in AI education. 50,000 of our employees now hold advanced AI certifications. Beyond skilling, we are also investing in AI tools and platforms across the software development cycle and our own internal processes. At Wipro, we are early adopters of Agentic AI, which will be delivering impactful results for our clients.

This technology goes beyond traditional productivity assistance. While many of these applications are still experimental, we see use cases emerging in areas like customer service and supply chain management. Building talent at scale is a key strategic priority for us. We remain focused in building a globally diverse team with a high-performance culture. While we are promoting strong internal talent, we are also bringing in top external talent.

Current order pipeline.

Our current large order pipeline is robust and we are seeing good traction across geographies. Our strongest traction in large deals remain in Banking, Financial Services and Insurance (BFSI) and Energy, Manufacturing and Resources (EMR).

Margin expansion

The margin expansion occurred despite a wage hike and seasonal weakness

If you look at what were the factors in Q3, we started the quarter with 2 incremental months of salary wage hike to absorb. We also had a seasonally weak quarter. A lot of the improvement that we did to offset the increase and also expand the margins came from the on the back of improved execution rigour both in our core and in the consulting business.

If you look at rising Capco and the core business, all of that has done very well. Now we had a set of levers which are traditional in terms of the utilization offshoring and the fixed price productivity that played out. We also did a very conscious reduction in terms of our overheads including G and A,

Now these are conscious reductions as we drove and they have also yielded into the margin improvement. Where do I look at is there a revised aspirational band? We've got to 17.5% that we had shared and it's a 12-quarter high. So in some sense, we are very conscious that we should sustain it.

Mining vs hunting

They have increased the percentage of revenue gained from the largest clients. This give rise to a mining vs hunting debate where the latter is the attempt to get more revenue from existing clients and the latter is hunting new clients.

We have done reasonably well when it comes to growth in top 10 clients. It's up 15% year on year, whereas ex of that, our revenues are still declining at a 5% rate.

We do look at mining our top 10 clients or top 25 or top 50 as a show of strength and that's something that we focused on. We remain committed to investing and scaling our large accounts, demonstrating client centricity by driving greater value, increasing wallet share and expanding into new business new lines of business.

Hunting remains a very, very key lever for us and we are very, very focused on winning more new accounts.

Hiring

They are looking to hire up to 12k new people which is about 5%. There will be some attrition so the net addition will be less than that but they would not be hiring if they were not confident about revenue growth.

We have called out that for the next fiscal, we will be going every quarter to campus and hiring about 10,000 to 12,000 people. Over and above that, we'll have lateral hiring happening. And we also see our attrition coming down in the coming quarter because our net resignations have been coming down.

The company and the sector face a revenue growth challenge. This is especially acute for Wipro as they have seen actual revenue declines

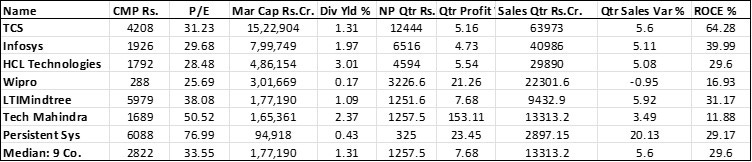

Relative Valuation

The table below shows some valuation parameters for some large and mid-sized Indian It companies.

Wipro has the second lowest ROE of the above companies and is trading at the lowest P/E.

Summary

WIPRO has faced significant revenue and margin challenges since 2022. Margins have improved in the last few quarters.

The BFSI consulting business of its subsidiary CAPCO is doing well but the company overall is struggling to increase revenues. The company has talked of a strong pipeline and future revenue will grow if they can convert this

Valuation

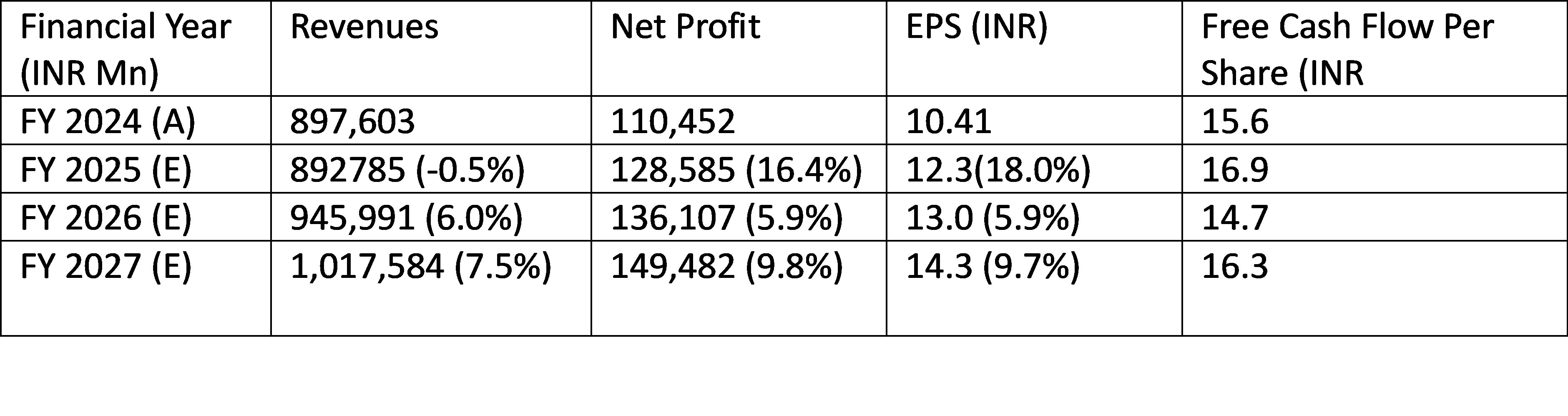

The consensus among analysts is that revenues will again grow in FY 2026 and 2027 and give rise to proportionate increases in net profit and EPS.

Wipro share price currently is INR 320 and that implies a two year forward P/E multiple of 24.6X. This implies a two-year forward earnings yield of 4.1%.

The current two year forward Price to Free Cash Flow Ratio of 21.7X. which implies a free cash flow yield of 4.6%.

This appears to be slightly expensive fair valuation even if we assume likely revenue growth of 6%-9% CAGR and likely ROE/ ROCE of 16% to 18%.

Conclusions

The conventional wisdom for some time has been that Infosys and TCS should be preferred to WIT in the Indian ITES as the former were fundamentally more profitable and better run businesses. This has been the correct view. Wipro needs to maintain the improvement in margins as well as increase the rate of revenue growth.

We will continue to monitor a few companies in this sector including Wipro. However, given the general overvaluation of Indian stocks we will not have any exposure expect for a long standing position in the Infosys ADR.