Alphabet

Review of Q2 Results

On 5th May 2023, we wrote a detailed rep[ort on Alphabet (GOOGL) in the light of Q1 results. This can read here

In this report, we noted “Google has grown strongly through its dominance of internet advertising. It has used its cashflow to make some brilliant acquisitions which have also boosted revenues in both advertising and in unrelated areas.

Google has been much less successful where it has used its cashflows to incubate new businesses. These businesses are primarily in Google Cloud Platform (GCP) and Other Bets.”

We noted that 71% of Revenues come from advertising (Search and YouTube) with Google Play and Cloud accounting for 15% each.

Our conclusions at the end of May were as follows:

“Advertising revenue growth is slowing significantly at Google. In part, this reflects cyclical factors as the economy slows down. However, it also partly reflects the size and scale of Google’s advertising which means faster growth from this level is much more difficult.

In either case, it shows the urgency of significant cost cutting. This requires a fundamental change in the mindset and culture of the company and is unlikely to be achieved quickly or easily. It may need a much tougher manager than the current CEO

This is our biggest issue with respect to Alphabet/Google. Revenue growth will slow and costs may not be controlled and this will lead to sustained fall in profits and free cash flow.

The current analysts’ consensus is for 17% in the next two years. I think there is a risk that this may not be achieved and the share price could come under further downward pressure.”

Since then the stock has risen by 20%

The recent Q2 results showed that, after all the talk of the last two or three quarters, Alphabet is finally cutting costs. This was the first quarter for a long time where revenue growth was greater than cost growth. Operating Revenue in Q2 grew 12% but Operating Cost only grew 4%. Headcount rose about 4.4% Y/Y. The company emphasised this will continue in the next few quarters at least. Profits will benefit from operating leverage and grow strongly

The lower costs reflect the implementation of the job cuts announced in Q1, reduced levels of hiring, consolidation of the property estate and aggressive deployment of teams to the most productive tasks.

We will review the Q2 Results in detail:

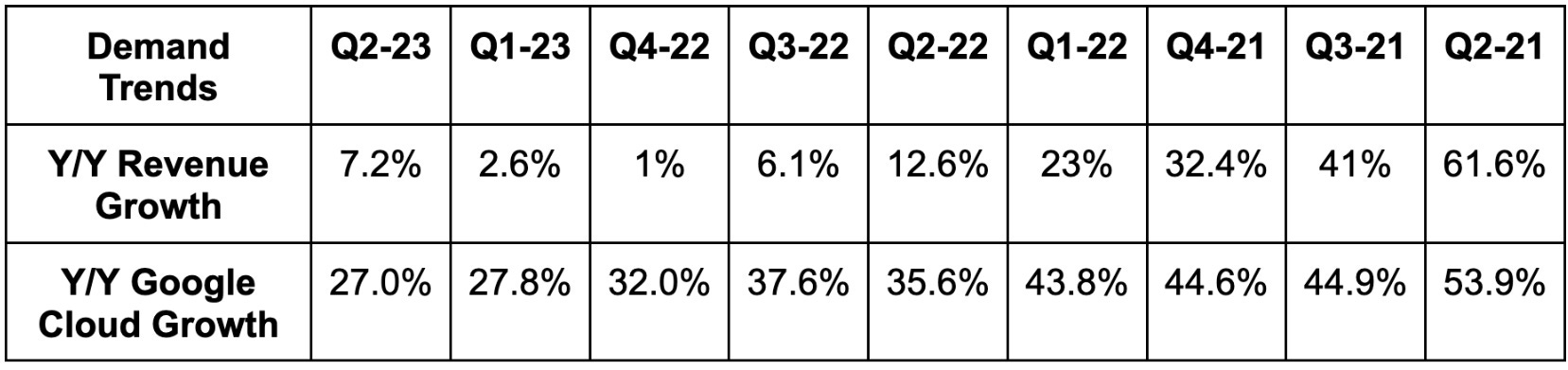

Source : The Stockmarket Nerd

Overall growth was 7.2% with a slowdown in advertising growth (both Search and You Tube) but Cloud continued to grow strongly at 27%

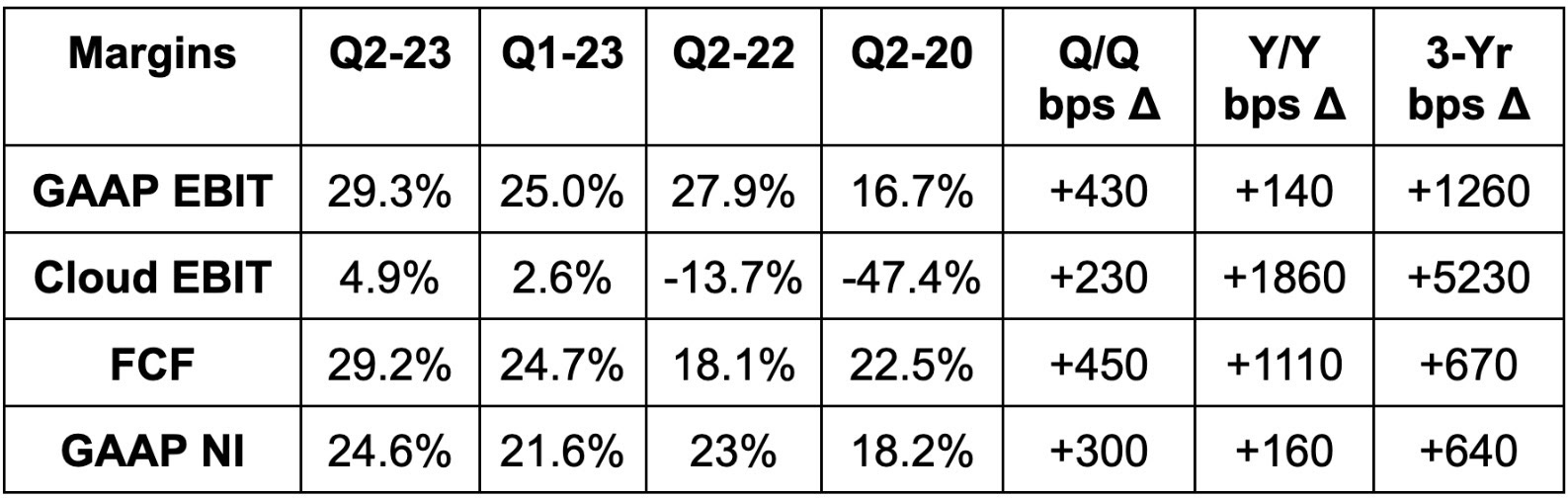

Source : The Stockmarket Nerd

Margins improved across the board. Google has been playing catch-up with Amazon and Microsoft in the Cloud business. It is continuing to improve its profitability, with EBIT margins at 4.9% having been -13.7% a year ago. Free Cash Flow (FCF) generation continues to be impressive with the FCF Margin hitting 29.2%. Every US$ 3 of revenue translates into US$1 of FCF.

Earnings Conference Call highlights

Sunder Pichai CEO hosted the Conference Call from London and set the tone by saying this was the 7th year in which Alphabet was operating as an AI company.

He noted that AI and Large Language Models (LLM) are enabling Alphabet to change their products and service. Search is now re-badged Search Generative Experience (SGE). SGE enables more natural search and has been shown to enhance the quality of query results. Since launching in May, SGE has already cut query response time by 50% and has generated positive user feedback.

Google Bard is a product for conversational AI- It is constantly improving and is now available in 40 languages. Alphabet will soon launch Gemini as its foundational language learning model (LLM).

AI is being used to improve the core advertising business. For example, the Gemini LLM and Performance Max (its AI-driven campaign creation tool) is being used by YouTube to boost advertising. 80% of advertising on Alphabet now use at least one AI ad tool.

70% of generative AI Unicorns are Google Cloud (GCP) customers.

The demand for more AI-driven workloads is boosting the Cloud business. Generative AI cloud customers are up 15x Q/Q (from a very low base). They are seeing strong demand to use one of their 80 plus AI models including third party models. AML AI for example helps clients such as HSBC tacker money laundering.

Generative AI gives opportunity to sell to 9mn Google Workspace customers as well as target new customers.

GCP (Google Cloud Platform) revenues grew by 28% (slightly more than Microsoft Azure but from a smaller base).

YouTube continues to perform impressively at scale. YouTube shorts has 2bn monthly average users vs. 1.5bn (33% growth). YouTube is now in the process of adding Shorts inventory to Google’s overall advertising supply. YouTube reaches 150 million people (!) through connected TV in the U.S.

Other Bets’s Revenues were US$ 285mn but operating losses were US$ 813mn. These Blue Sky bets continue to deliver large losses and probably need to be looked at more critically.

Restructuring and cost cutting

Alphabet has incurred US$ 2bn in YTD restructuring charges due to layoffs and an additional US$ 564 million costs to a reduction in its real-estate footprint. These should not recur going forward.

The cost-cutting action has been more vigorous than we expected. The company has implemented the layoffs announced in the first quarter, has slowed hiring and consolidated premises. Teams of workers have been moved to more productive tasks. For example, Google Brain was combined with Google Deepmind.

The company emphasised they need the cost cuts to partly fund rising investment in Datacentre, AI Infrastructure and chip development.

CFO Ruth Porat will move on to become the President and Chief Investment Officer at Alphabet. She will continue to be the CFO until 2024.

Summary

This was an encouraging set of quarterly numbers.

The efforts to keep costs in check is beginning to bear fruit. Anecdotal evidence indicates that there is a lot of excess fat in the business that can still be trimmed.

Although advertising revenue growth is slowing due to tough economic conditions, the Cloud business continues to strongly

Margins and profitability have improved greatly

The company has moved fast to use generative AI to improves its products and services offering.

After years of investment as Alphabet tried to catch up with Amazon and Microsoft in the Cloud hosting, GCP is now a new source of reliable EBIT. GCP is beginning to see a strong boost due to growth in AI workloads. It is likely that the growth of AI will be a greater boost to Google and Microsoft’s Cloud business than it will for Amazon’s AWS. The next data point on this will be AWS growth in the Amazon results.

Conclusions

The company continues to be a strong generator of profits and free cash flow.

Cost cutting will ensure the profits will grow faster.

AI will require significant additional investments but should ensure higher future profits and free cash flows in the medium to long term.

The current forward P/E multiple of 21 times looks attractive given likely 22%-25% ne profit growth, 25% operating margin and about 24% ROE.

We had an underweight position in GOOGL and would look to add to it at the current price.