Amazon Inc

Q2 Quarterly Results

On 12th May, I wrote a detailed piece on Amazon.com which can be accessed here.

The recent quarterly results provide us with a timely opportunity to look again at the company.

Any undertaking to study Amazon.com leads quickly to Jeff Bezos Day 1 Letter. It is a remarkable document and the quotes below only give a small indication of its power.

“We believe that a fundamental measure of our success will be the shareholder value we create over the long term. … The stronger our market leadership, the more powerful our economic model. Market leadership can translate directly to higher revenue, higher profitability, greater capital velocity, and correspondingly stronger returns on invested capital. Our decisions have consistently reflected this focus.”

“We first measure ourselves in terms of the metrics most indicative of our market leadership: customer and revenue growth, the degree to which our customers continue to purchase from us on a repeat basis, and the strength of our brand.”

“We have invested and will continue to invest aggressively to expand and leverage our customer base, brand, and infrastructure as we move to establish an enduring franchise.”

We will continue to focus relentlessly on our customers.

We will continue to make investment decisions in light of long-term market leadership considerations rather than short-term profitability considerations or short-term Wall Street reactions.

We will make bold rather than timid investment decisions where we see a sufficient probability of gaining market leadership advantages. Some of these investments will pay off, others will not, and we will have learned another valuable lesson in either case.

When forced to choose between optimizing the appearance of our GAAP accounting and maximizing the present value of future cash flows, we’ll take the cash flows.

We will balance our focus on growth with emphasis on long-term profitability and capital management. At this stage, we choose to prioritize growth because we believe that scale is central to achieving the potential of our business model.

These few extracts illustrate the key elements of the company’s business model. Investing heavily to gain customer and market share, build up revenue growth and focus on the long run. Such an approach puts less emphasis on Profitability, Earnings and Free Cashflows.

For many investors, including myself, valuation ratios such as Price to Earnings or Price to Free Cash Flow always indicated that Amazon shares were trading at too expensive a level.

One investor who took a large stake in Amazon in the early 2000s, and held the stock for over a decade, was Nick Sleep of the Nomad Investment Partnership. He bet on Amazon soon after the dotcom bubble when they were trading at less than US$30 per share. Regulatory filings show by 2007 Nomad held 1.4m shares in Amazon, then worth US$55.2m. By 2014 —the year it closed— Nomad held 2,926,232 shares, worth US$1.2bn.

Nick Sleep had two great insights with respect to Amazon

First, conventional analysts when modelling long-dated earnings or cash flows were reducing (or fading) the growth rate after a few years as this was conventional and reasonable approach for brick and mortar retailers. However, Sleep argued that this does not necessarily make sense for an internet retailer.

“… if the rate of growth in internet retailing is a product of attitude, rather than assets, then, the fact that a firm is quite large already does not necessarily tell you that its growth rate is set to slow. The widely held presumption that regression to the mean begins the moment the analyst picks up their pen, risks being wrong footed as a result. Two years of forty percent revenue growth, for example, will result in revenues doubling in twenty-four months and regression to the mean-based estimates would be out by almost a factor of two! That did not take long. In other words, although some online retailing firms may be quite large, they may also be quite young.”

Second, Sleep had an insight with a model called Scale Economies Shared (SES) which was developed after his analysis of Costco Inc.

As we wrote in our note, “Due to scale and buying power, Costco is able to extract a higher margin. It shares a large part of this with customers. As is well known, Costco makes over 90 % of its net profit from membership income (which has a 100% Gross Margin) and limits its overall Gross Margin to just 13% by reducing prices to customers. This does not make sense in the short-run but does in the long-run, as the lower prices drive higher volumes, generate future economies of scale and in turn lead to further reduction in prices.”

Sleep realised SES also applied to Amazon. Amazon’s business strategy was articulated by Jeff Bezos in his letter to investors in 2005 which is also worth reading in full.

“Our judgment is that relentlessly returning efficiency improvements and scale economies to customers in the form of lower prices creates a virtuous cycle that leads over the long-term to a much larger dollar amount of free cash flow, and thereby to a much more valuable Amazon.com.”

Nick Sleep made money because he looked very deeply at the qualitative aspects of the business model while conventional investors focused more on standard quantitative ratio analysis.

As Charlie Munger once said “People calculate too much and think too little.”

Amazon reported its second quarter results last week. This is how Bloomberg reported them:

“Here are the most important numbers that Amazon reported, as compared to analysts' expectations compiled by Bloomberg:

Net sales: $134.38 billion actual versus $131.63 billion estimated

EPS: $0.65 versus $0.35 estimated (estimate was greatly guided down by management and beating is not much of a surprise.)

Amazon Web Services (AWS) net sales: $22.14 billion versus $21.71 billion estimated

Operating margin: 5.7% versus 3.46% estimated. Impressively higher operating margins.

Operating income: $7.68 billion versus $4.72 billion estimated

Q3 net sales outlook: $138 billion-$143 billion versus $138.3 billion estimated

In Q1, Amazon guided to Q2 net sales of $127 billion to $133 billion.”

In general, the numbers were much better than expected.

Source: MBI Deep Dives

In the last five years, revenues have grown at a CAGR of 20.5%.

In the most recent quarter, the growth was just10.8%: within this, the “core” first party (1P) Amazon retail business only grew at 4.3%. The average was boosted by higher growth in Ads (22.3%) and third party (3P) retail (18.1%).

In terms of business mix, the last quarter was significant. As indicated in the last column, 1P retail accounts for less than half (43.2%) of Amazon’s total revenue and faster growing services businesses account for 55%.

These consist of services to other retailers (3P), consumers (Subscription) and enterprises (AWS and Ads). This ongoing change in business mix should have a positive impact of profitability as the faster growing services businesses have much higher margins.

Source: MBI Deep Dives

AWS revenue growth (QoQ) has recovered after a rare decline in the last quarter.

Source: MBI Deep Dives

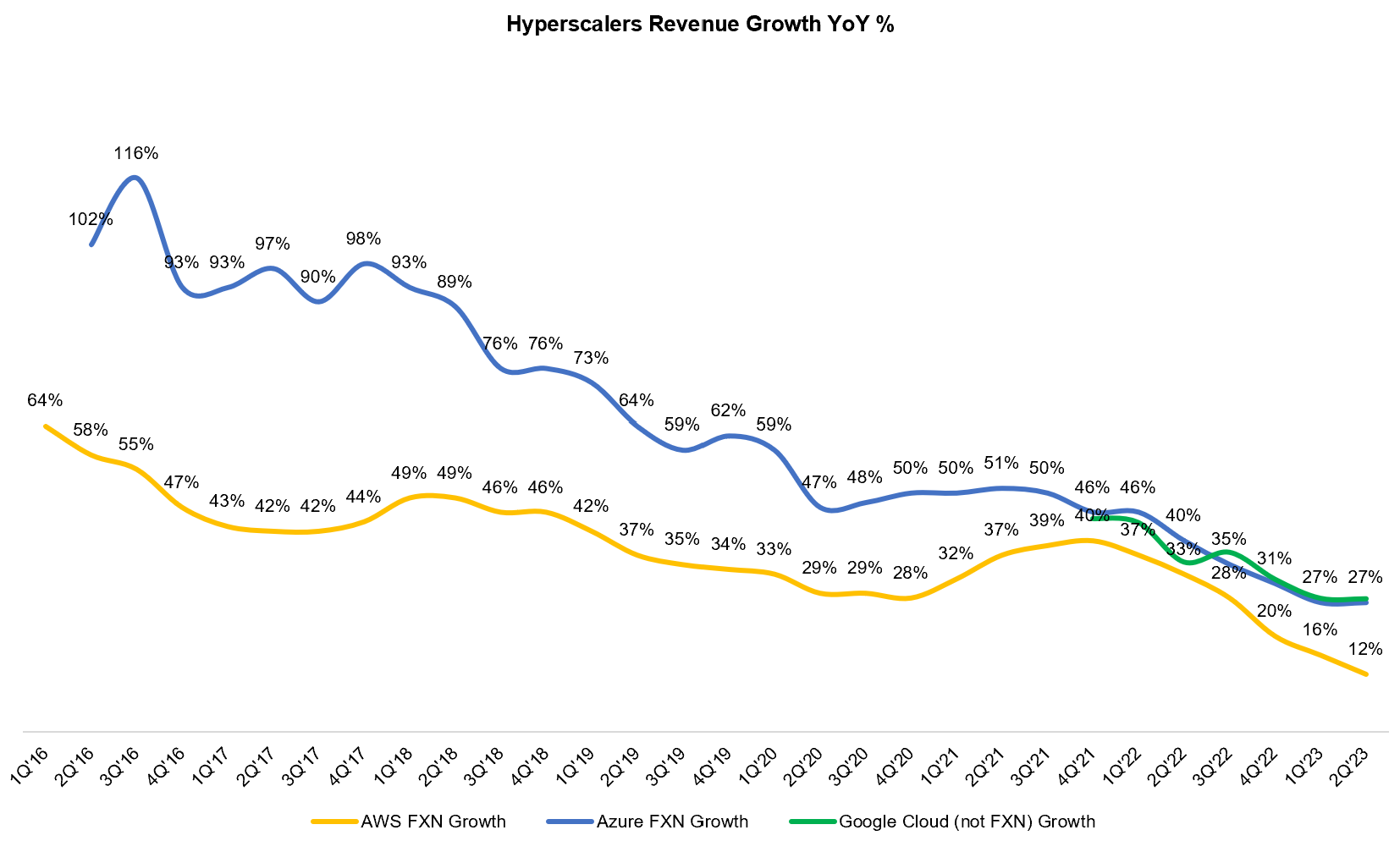

Revenue growth at all three hyperscalers (AWS, Microsoft and GCP) continues to slow. AWS, the largest of the three grew at 12%in the most recent quarter, while the other two recorded higher growth in the range 26% to 28%.

Source: MBI Deep Dives

The Operating Margins in AWS have stabilised at 24.2%.

Source: MBI Deep Dives

Operating margins in the Retail business have recovered in both North America and the International segment though the latter remains loss-making at the operating level.

Source: Stockmarket Nerd

Margins generally rose across the board except in AWS where they were stable.

Source: App Economy Insights

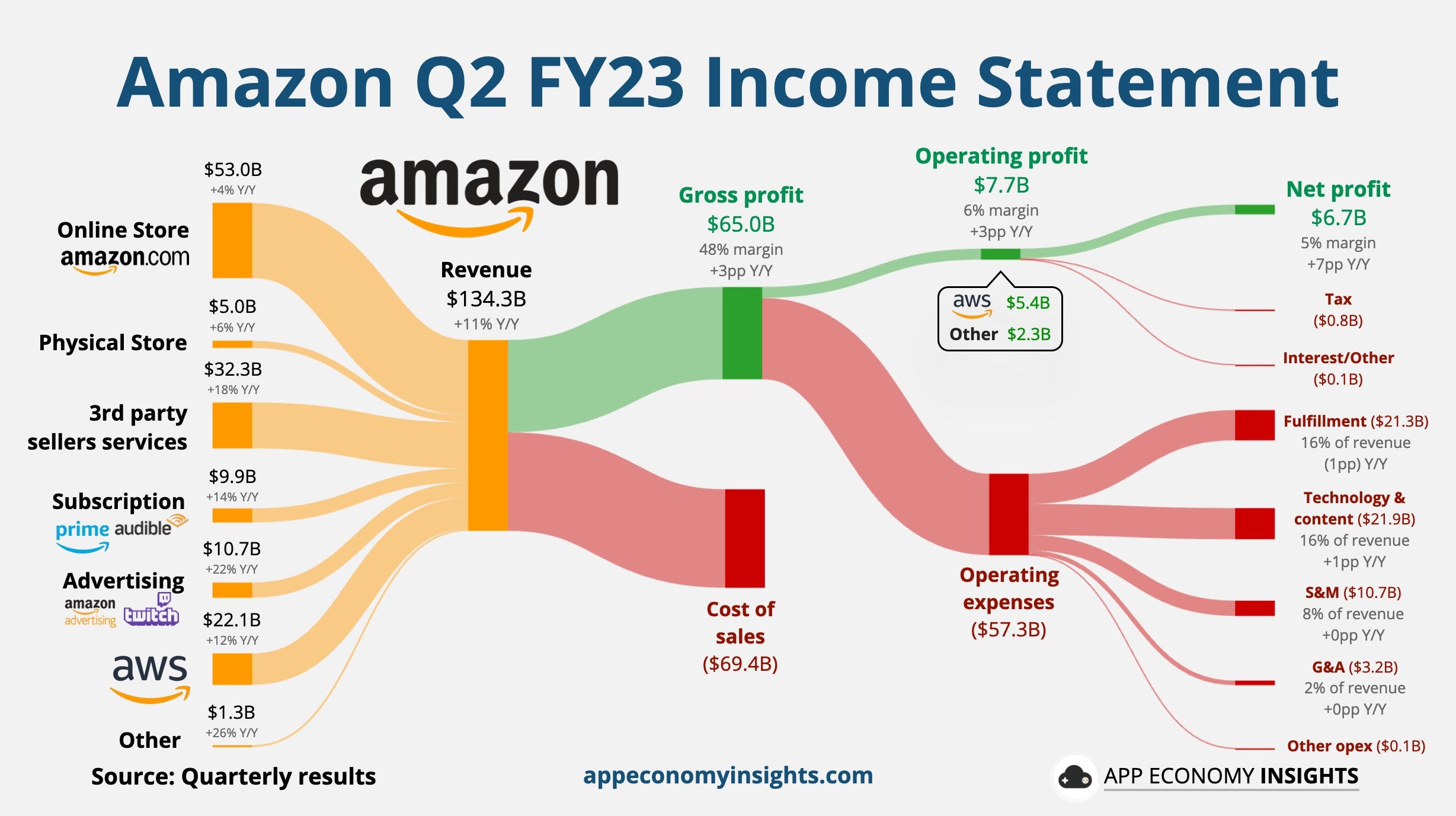

AWS accounts for 70% of total operating profit (US$ 5.4bn/ US$7.7bn) but only 16.5 % of revenues

Earnings Conference Call Highlights

Introductory comments

Today, we are reporting $134.4 billion in revenue and $7.7 billion (5.7% margin) in operating income, both of which exceeded the top end of our guidance ranges. We're encouraged by the progress we're making on several key priorities, namely:

lowering our cost to serve in our stores business;

continuing to innovate on and improve our various customer experiences; and

building new customer experiences that can meaningfully change what's possible for customers in our business long term.

Strategy for lowering costs in stores

Central to our efforts has been the decision to transition our stores' fulfillment and transportation network from one national network in the United States to a series of eight separate regions serving smaller geographic areas. We keep a broad selection of inventory in each region, making it faster and less expensive to get those products to customers.

Regionalization is working and has delivered a 20% reduction in number of touches for our delivered package, a 19% reduction in miles traveled to deliver packages to customers and more than 1,000 basis point (10% point) increase in deliveries fulfilled within region, which is now at 76%.

Changing customer experience

First, customers care a lot about faster delivery. We have a lot of data that shows when we make faster delivery promises on a detail page, customers purchase more often, not just a little higher, meaningfully higher. It's also true that when customers know they can get their items really quickly, it changes their consideration of using us for future purchases too.

This ability to have shipments closer to customers is the result of a lot of work and invention on the regionalization side, placement logic and local in-stock algorithms. It's also driven by our development and expansion of same-day fulfillment facilities, which is our fastest fulfillment mechanism and one of our least expensive, too.

Our same-day facilities are located in the largest metro areas around the U.S., so our top-moving 100,000 SKUs, but also cover millions of other SKUs from nearby fulfillment centers that inject selection into these same-day facilities and have a design that streamlines getting items from order to being ready for delivery in as little as 11 minutes.

The experience has been so positive for customers in our business that we're planning to double the number of these facilities. We believe that we are far from the law of diminishing returns and improving speed for customers.

“So far this year, we've delivered more than 1.8 billion units to U.S. Prime members the same or next day, nearly 4x what we delivered at those speeds by this point in 2019.”

“Lowering our cost to serve allows us not only to invest in these speed improvements, but also add more selection at lower price points.”

“In particular, we're growing our selection in everyday essentials, enabling customers to avoid going out to get these items and increasing both basket sizes and the frequency with which customers choose to shop with us. We now have more than 300 million items available with U.S. Prime free shipping, including tens of millions of items with free same-day and 1-day delivery.

We're continuing to focus on providing great value with tens of millions of deals that help customers stretch their dollar a little more. For instance, in Q2 of '23, we offered customers 144% more deals and coupons than we did in Q2 of 2022. Prime Day was similar.

Building new customers experiences

“Amazon offered more deals than any past Prime Day event with a wide selection across millions of products. Prime members purchased more than 375 million items worldwide and saved more than $2.5 billion across the Amazon store, helping make it the biggest Prime Day ever.”

This is really bad news for rival retailers who still survive. Amazon is already at a very efficient level in terms of speed of delivery. However, they are not resting on their laurels but are looking for more ways to reduce (logistics) costs and reduce prices to get more revenue and market share.

AWS

“AWS remains the clear cloud infrastructure leader with a significant leadership position with respect to number of customers, size of partner ecosystem, breadth of functionality and the strongest operational performance. These are important factors for why AWS has grown the way it has over the last several years and for why AWS has almost double the revenue of any other provider.

As the economy has been uncertain over the last year, AWS customers have needed assistance cost optimizing to withstand this challenging time and reallocate spend to newer initiatives that better drive growth. We've proactively helped customers do this. And while customers have continued to optimize during the second quarter, we've started seeing more customers shift their focus towards driving innovation and bringing new workloads to the cloud.”

During the pandemic as WFH spread, companies spent heavily on Cloud. In the last three quarters they have been looking to optimise and make the most of the capacity they have already bought rather than spending much more . All three of the large providers have commented on this optimisation which is leading to slower sales. MSFT said they expect the optimisation headwind to continue for another three to six months but Azure demand growth should pick up after that. AWS is perhaps being a little more positive in saying they are already seeing some signs that clients are looking to migrate more work to the cloud.

“The AWS team continues to innovate and change what's possible for customers at a rapid clip. You can see across the array of AWS product categories where AWS leads in compute, networking, storage, database, data solutions and machine learning, among other areas..”

Their investment in producing their own CPU chip design (branded as Graviton) seems to be paying off .

“Today, more than 50,000 customers use AWS' Graviton chips and AWS Compute instances, including 98 of our top 100 Amazon EC2 customers, and these chips have about 40% better price performance than other leading x86 processors.”

The big increase in demand for AWS is likely to come from the migration of AI workloads. Amazon characterise the Generative AI space in three layers.

“At the lowest layer is the compute required to train foundational models and do inference or make predictions. Customers are excited by Amazon EC2 P5 instances powered by NVIDIA H100 GPUs to train large models and develop generative AI applications.”

However the cost and periodic shortages of Nvdia Chips “prompted us to start working several years ago on our own custom AI chips for training called Trainium and for inference called Inferentia that are on their second versions already and are at a very appealing price performance option for customers building and running large language models. We're optimistic that a lot of large language model training and inference will be run on AWS' Trainium and Inferentia chips in the future.”

“We think of the middle layer as being large language models as a service (LAAS(?))”

“Companies do not want to spend hugely to develop their own LLMs. Rather, they want access to them, want to customize them with their own data without leaking their proprietary data into the general model, have all the security, privacy and platform features in AWS work with this new enhanced model and then have it all wrapped in a managed service. This is what our service Bedrock does and offers customers all of these aforementioned capabilities with not just one large language model but with access to models from multiple leading large language model companies like Anthropic, Stability AI, AI21 Labs, Cohere and Amazon's own developed large language models called Titan.”

“Customers, including Bridgewater Associates, Coda, Lonely Planet, Omnicom, 3M, Ryanair, Showpad and Travelers are using Amazon Bedrock to create generative AI applications.”

They want to offer Generative AI as lower cost option at scale in the same way they have offered cloud services.

“What we're doing is democratizing access to generative AI, lowering the cost of training and running models, enabling access to large language model of choice instead of there only being one option, making it simpler for companies of all sizes and technical acumen to customize their own large language model and build generative AI applications in a secure and enterprise-grade fashion, these are all part of making generative AI accessible to everybody and very much what AWS has been doing for technology infrastructure over the last 17 years.”

They believe Amazon’s experience in handling data will give them an advantage in hosting and servicing AI workloads in the Cloud.

“..the core of AI is data. People want to bring generative AI models to the data, not the other way around. AWS not only has the broadest array of storage, database, analytics and data management services for customers, it also has more customers and data store than anybody else.”

In our previous note we devoted some space to Amazon’s advertising business and noted that is had quickly become a US$ 10bn quarterly revenue business. It has continued to grow strongly.

“Advertising revenue remained strong, up 22% year-over-year. Our performance-based advertising offerings continue to be the largest contributor to our growth. Our teams worked to increase the relevancy of the Ads we show to our customers by leveraging machine learning and improve our ability to measure the return on advertising spend for brands.”

The 3P business to 1P business ratio in Retail is now nearly 60%. “Third-party unit mix increased to 60% during the quarter, the highest level we've ever seen, and we're continuing to see good growth in the number of sellers and the unit sold per seller. We're making steady progress on improving our worldwide stores profitability.”

Margins continue to improve as shipping and fulfilment costs grow less than unit growth.

“Since North America segment operating margins bottomed out in Q1 of 2022, we have seen 5 consecutive quarters of improvement, with second quarter operating margin of 3.9%. This is an improvement of 620 basis points over these past 5 quarters. One of the largest drivers of this operating income improvement in the stores business has been reducing our cost to serve, with shipping costs and fulfillment costs continuing to grow at a slower pace than our unit growth. Most recently, regionalization is an important contributor.”

Capital expenditure overall will be lower than before but AI investments will be higher.

"…investments were $54 billion for the trailing 12-month period ended June 30, down from $61 billion in the comparable prior year period. Looking ahead to the full year 2023, we expect capital investments to be slightly more than $50 billion compared to $59 billion in 2022. We expect fulfillment and transportation CapEx to be down year-over-year, partially offset by increased infrastructure CapEx to support growth of our AWS business, including additional investments related to generative AI and large language model efforts."

Source: Stratosphere.io

Capital expenditure at US$ 50bn is a lot less than the US$ 61bn and US$ 63bn in the previous two quarters. As shown in the chart above (It is shown as a negative as it is a cash outflow). Perhaps Capex has peaked and will be at a lower pace going forward. This would be positive for future Free Cash Flow.

The company the increase in AI-driven investments in AWS is a good thing.

“ …one of the interesting things in AWS, and this has been true from the very earliest days, which is the more demand that you have, the more capital you need to spend because you invest in data centers and hardware upfront and then you monetize that over a long period of time. So I would like to have the challenge of having to spend a lot more in capital in generative AI because it will mean that customers are having success and they're having success on top of our services.”

Summary

This was a good quarterly report. The company easily beat analysts expectations. There were many positive factors.

Revenue growth slowed but was positive. Core 1P sales was the slowest growing category and higher margin services are growing much faster. As a result the business mix continues to change rapidly. The services mix increased from ~40% in 2018 to ~60% currently and this trend is likely to continue. This will improve overall profitability over time.

Within services, the likely highly profitable Ads business continues to grow strongly and already accounts for 10% of total revenue.

Margins have improved across all segments except AWS where they have stabilised.

AWS is the largest cloud hosting business but its growth has slowed more than its two main rivals. However, the company believes the consolidation of demand phase is over and they are well placed to win orders for new AI-driven workloads.

Capital expenditure will be lower going forward and this will be positive for free cash flow.

Conclusions

The recovery in margins in the last five quarters and the growth in services businesses have been an important positive development.

The company increased capital expenditure rapidly, after the huge boost to demand during the pandemic showed capacity constraints. The fact that capital expenditure will be lower going forward is an important positive.

Time will tell when, and to what extent, AWS growth will pick up. AWS has an EBIT margin of nearly 30% so above average growth in AWS will be very positive for overall profitability. AWS currently already accounts for 70% of total operating profit. Cloud is likely to grow rapidly due to generative AI from Q4 2023 onwards and AWS, as the market leader, should benefit from this.

However we are back to the same problem on Amazon. The forward P/E ratio of 55.5 times looks optically too expensive for a business where revenue grows at about 20% CAGR and a steady state ROE is around 30%.

We are mindful of the Scale Economies Shared (SES) playbook that Nick Sleep attributed to Amazon and the fact that this is going to a feature of the retail business going forward.

As value investors we are reluctant to commit capital, however there seems to be good momentum in the business. We will consider investing 2% of the portfolio in Amazon now and look to add up to 3% more on significant pullbacks in the share price (if any).