Arista Networks (ANET)

3rd Quarter Results

Arista Networks (ANET) reported Q3 2023 Results on the 30th of November 2023. We wrote a long piece about the company on 2nd September 2023 and re-read it again today. It is worth reading if you are not very familiar with the company. It can be found here.

The conclusions to that piece were as follows:

Arista Networks seems well placed to grow revenues by ~17% to ~25% for many years.

It is also likely to grow profits by ~20% to ~25% for many years.

This is likely to be achieved with profit margins of ~30% to ~35% and a return of equity percentage of a similar amount.

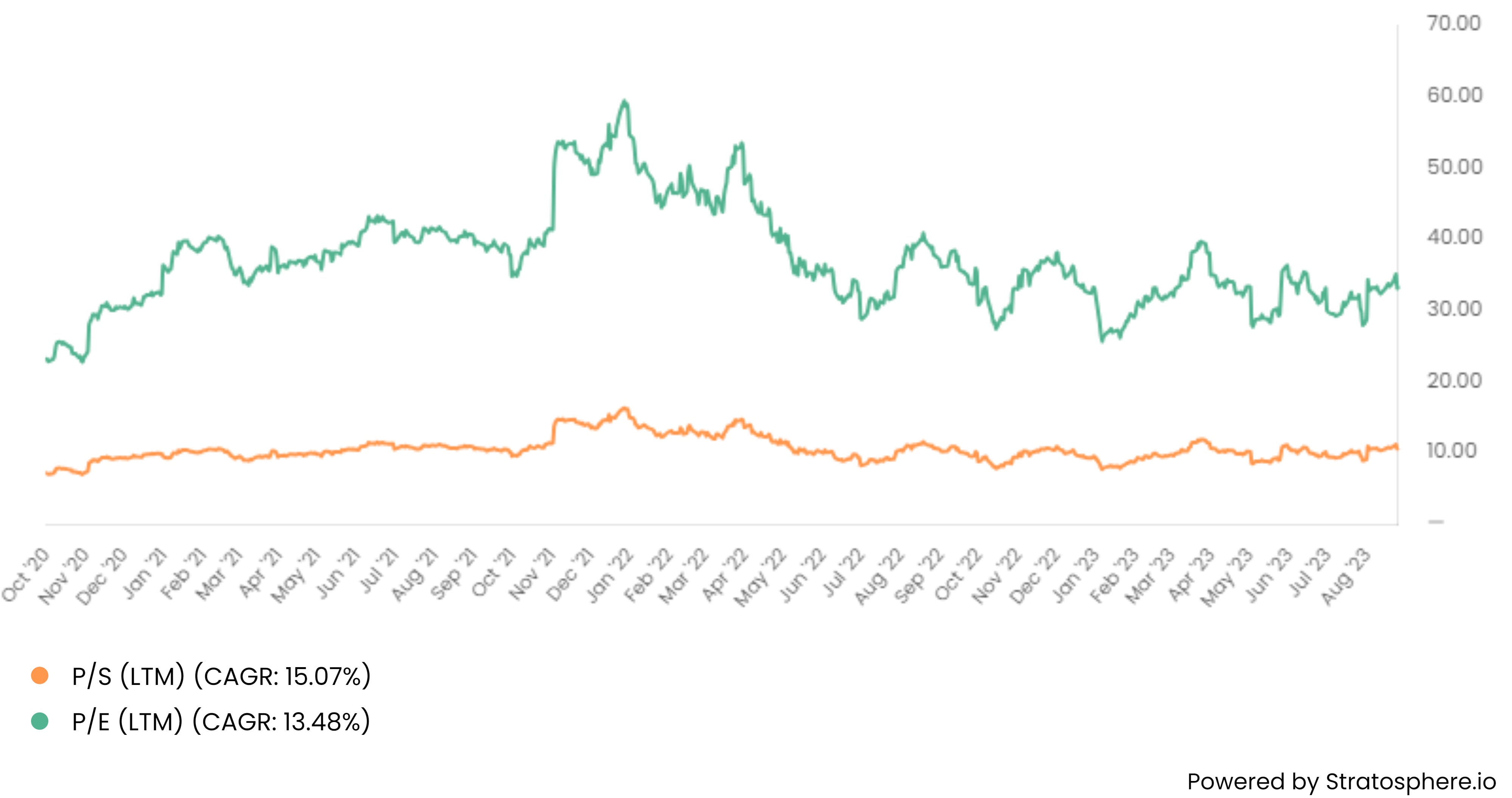

Given all this, a Forward Price/Earnings ratio of 36 times and Price to Sales Ratio of 10 times (see chart below) is not too expensive.

We don’t view the stock as a bargain at the current level but there is a strong chance that the company will grow strongly. It will therefore grow “into its multiples” and prove to be good long-term investment.

We will add to our current position in the company and continue to monitor it closely.

Since then, the stock has risen about 20% helped by a strong market for technology stocks.

The Results

The Results were better than expected.

Revenues were US$1.51 billion, a rise of 28.3%.

Gross Profit was US$ 942mn, a rise of 33%.

Gross Margin was 62.4% compared with 60.3%

Operating Profit was US$ 602mn, a rise of 44%.

Operating Profit Margin was 39.9% compared with 35.4%

Net Profit was US$ 545mn, a rise of 54%

Net Profit margin was 36.1% compared with 30.1%.

Non-GAAP earnings per share(eps) was $1.83. up 46.4%

There is good operating leverage in the business but the growth in eps (46%) is less than the growth in net profit (54%). This is due to the dilutive effects of stock-based compensation.

Outlook.

Revenues of approximately $1.5 billion to $1.55 billion in the current quarter.

A gross margin of approximately 63%.

An operating margin of approximately 42%.

The Conference Call

Some highlights

"Services and software support renewals contributed approximately 16.8% of revenue.”

“Non-GAAP gross margins of 63.1% was influenced by improving supply chain overheads and higher enterprise contributions. (Non-GAAP) gross margins have consistently improved every quarter this year and will stabilize next year in 2024.”

“Cash, cash equivalents and investments ended the quarter at approximately $4.5 billion”.

“We did not repurchase shares of our common stock in the quarter.”

“Arista's supply chain and lead times are improving steadily in 2023 and we expect it to normalize in 2024.” Supply chain disruptions wrought by Covid are finally going.

“The power of our one consistent software stack across a breadth of use cases, be the WAN routing, campus, branch, or data centre infrastructure, is truly unmatched by our industry peers.”

“International revenues for the quarter came in at $324.7 million, or 21.5% of total revenue, up from 20.9% last quarter. “- The 80/20 domestic /foreign revenue split remains.

“We expect to make incremental improvements to our 2023 outlook, which now calls for year-over-year revenue growth of approximately 33%.”

“In the last three years, we have made an investment and seen a significant uptake in enterprise customers wanting to do business with Arista. Historically, it's been the high-tech enterprise and the financials. And today, we're seeing a much better cross section of verticals, including healthcare, education.”

Overall, it was a routine conference with little that was new or striking. Perhaps this was because the company was scheduled to have an Analyst Day on November 9th and wanted to save new information announcements for that.

Conclusions

The company continues to perform well. This was a good set of results and consistent with the expectations outlined in our September report.

The share price has risen 20 % since September 2nd and by 14 % since the results.

Analysts are expecting about 10% growth in net profit and eps in 2024 and 2025. This is conservative but reflects the difficult comparisons due to the strong performance of recent years.

With a likely operating margin and return on equity next year of 37% and 34%, the stock looks fairly priced at a forward P/E multiple of 32.5 times.

We intend to continue to hold the stock but are not inclined to add to our holdings.

Arista often talks about non-GAAP numbers. These of course exclude stock-based compensation (SBC). As we noted in September, SBC is high at Arista. This is not uncommon for many technology companies.

Shareholders do not fully benefit from the performance of the company due to the dilutive effects of SBC. However, the company continues to offer good returns to investors even after adjusting for the impact of SBC.