On 27th April 2023, we published a note on Enphase Energy (ENPH) and SolarEdge Technologies (SEDG). This can be found here.

It is a useful introduction to the Residential Solar industry, global trends in solar energy in general and renewables in particular. It is also a good introduction to the two companies.

At the time the company was trading at $174 a share. Today it is at $118, having been as low as $75 on December 8th.

Something went wrong with the sector and our investment thesis. There is more to be gained from doing a post-mortem on our losers rather than celebrating our winners. In this sprit, we look at what went wrong in this case.

In the April article, we went into a great deal of detail into the global growth of renewables especially solar. We looked at the technology of Microinverters (which Enphase manufactures), batteries (which it distributes) and energy management software (which it designs and offers).

The company designs, manufactures (through outsourcing partners) micro converters and sell to distributors.

The distributors on-sell to Installers who are involved in installing residential solar.

The problem was we missed the wood for the trees and the key issue was demand and sales.

The problem was that as soon as the note was written, there was evidence of demand slowdown.

Households choose to install solar panels because they will save money in the long run. They have a 7–9-year break even on an asset which many last up to 25 years.

However, for most people, installing solar panels requires a major capital outlay upfront. They often must take a loan to finance the installation.

With hindsight, we can say that demand fell for three reasons.

The sharp rise in US interest rates as the US Fed funds rate went form 0.125% at the beginning of 2022 to 5.25% in July 2023 led to much higher borrowing costs.

In December 2022 California approved a new net metering policy (NEM 3.0) which came into effect on April 15th, 2023. Among other things, the NEM 3.0 reduced the amount that was paid to householders who export electricity to the Grid.

In the April note, we wrote:

“The NEM 3.0 will reduce the average export rate in California to US$0.05/kWh to US$0.08/kWh compared to current average of $0.25/kWh to $0.35/kWh. This is a substantial reduction “.

We had noted the importance of California in the residential solar market in the United States.

“California has been an important Solar due to the size and wealth of the state, the abundance of sunshine and the magnitude of state incentives. About 1.5 million California homes and businesses have solar systems with a capacity of more than 12,000 megawatts of renewable power, or the equivalent of 12 nuclear reactors. According to Bloomberg NEF, the Golden State accounts for about one-third of all US residential capacity installed.”

The combination of higher interest rates and lower tariffs in California was a double blow to economics of domestic solar installation in 2023. Demand plummeted as a result.

Both of these were flagged as risk factors in our report, but we did not do a sensitivity analysis of their combined impact.

In addition, Enphase also saw poor sales in Europe. It is active in Germany, Netherlands, and France. A poor economy led to fall in demand.

Enphase sells to distributors who then sell to the installers. Distributors already had significant inventories on their books. When they saw demand was falling, they probably reduced their orders to Enphase sharply. The cut in orders was of a greater percentage magnitude then the decline in end-demand.

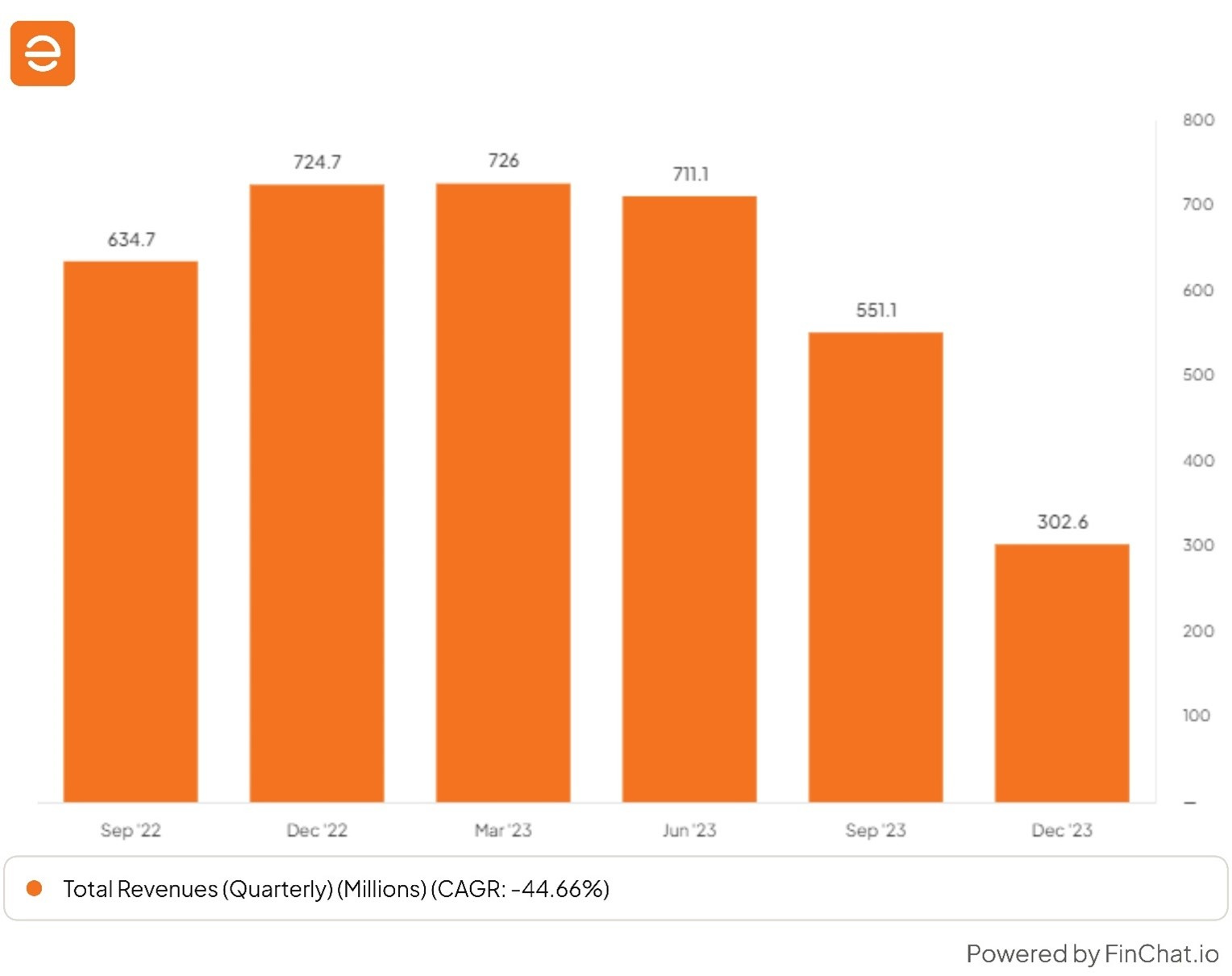

We can see the impact of this in the chart for quarterly revenues below:

December quarterly sales were $ 302mn compared with $ 726mn in March 2023.

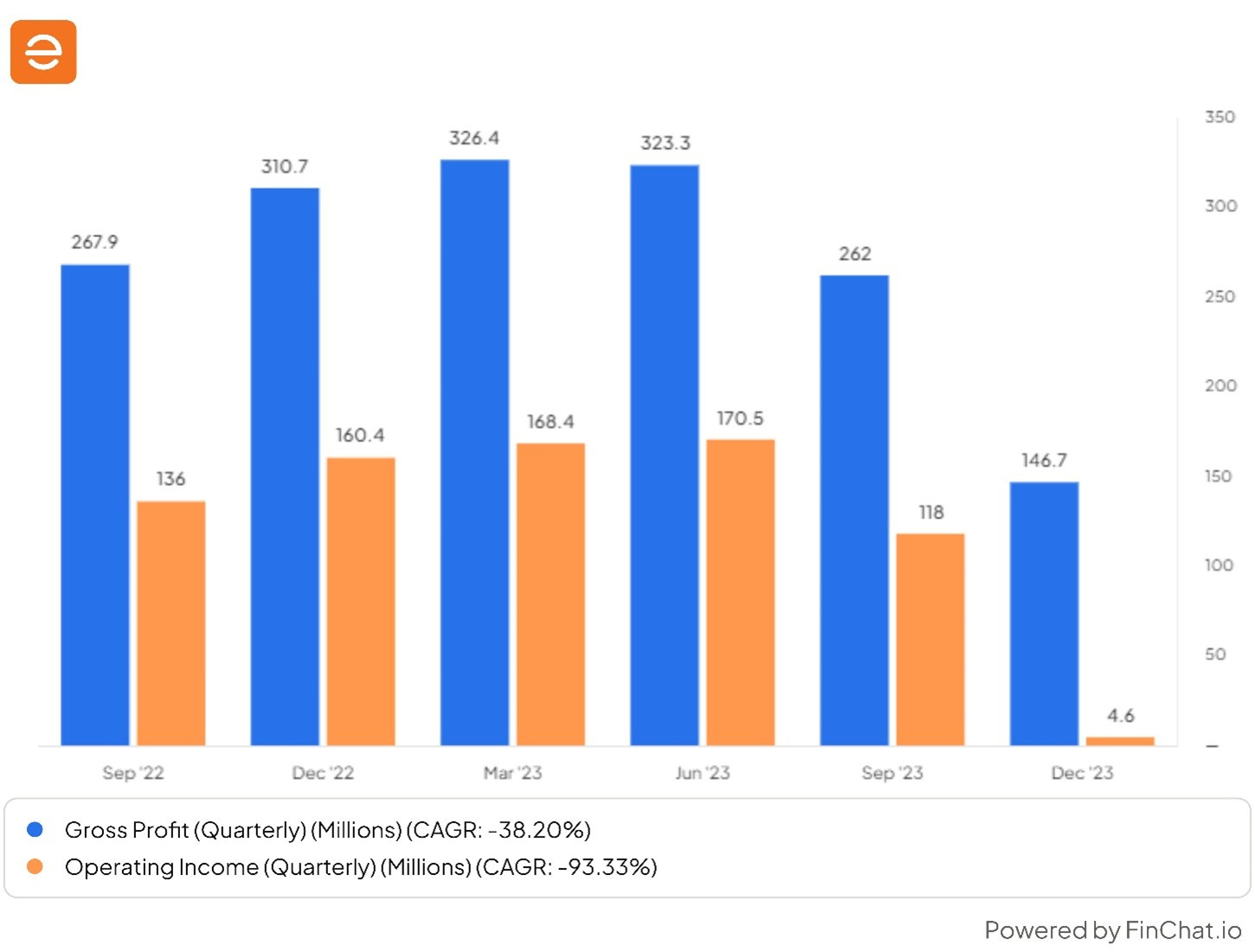

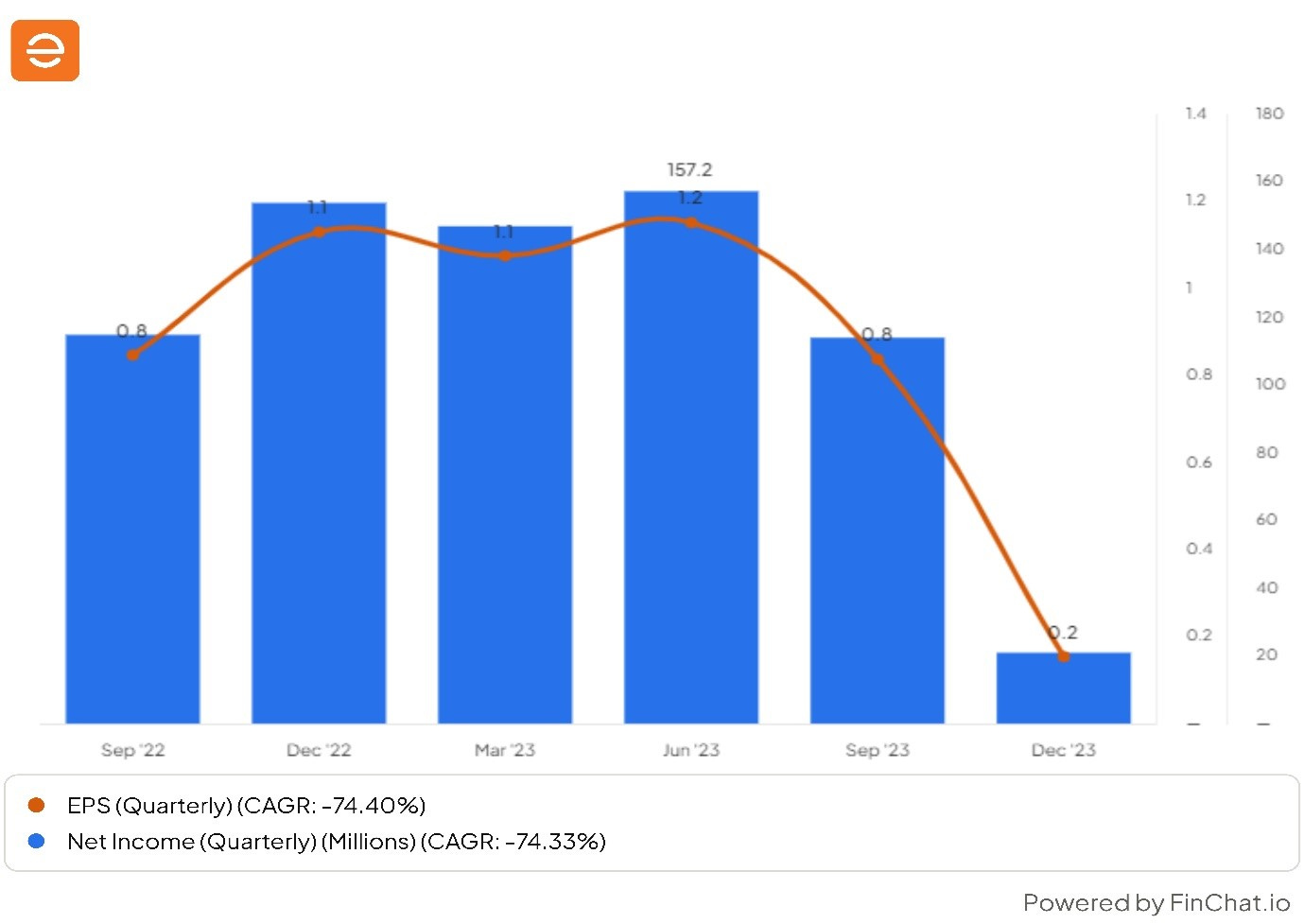

This was a substantial decline in sales which led to corresponding falls in Gross, Operating and Net Profit and EPS.

Enphase did not respond to the fall in demand by cutting prices and therefore preserved Gross Profit Margins. However, the pre-tax (operating) margin and the net profit margin fell significantly.

This demonstrates of operating leverage in reverse as revenues falls.

On December 8th, the company announced a plan to cut operating costs by reducing the workforce by 10%, by having a hiring freeze and instructing their partners to stop production in two plants. This should help to boost operating and net margins.

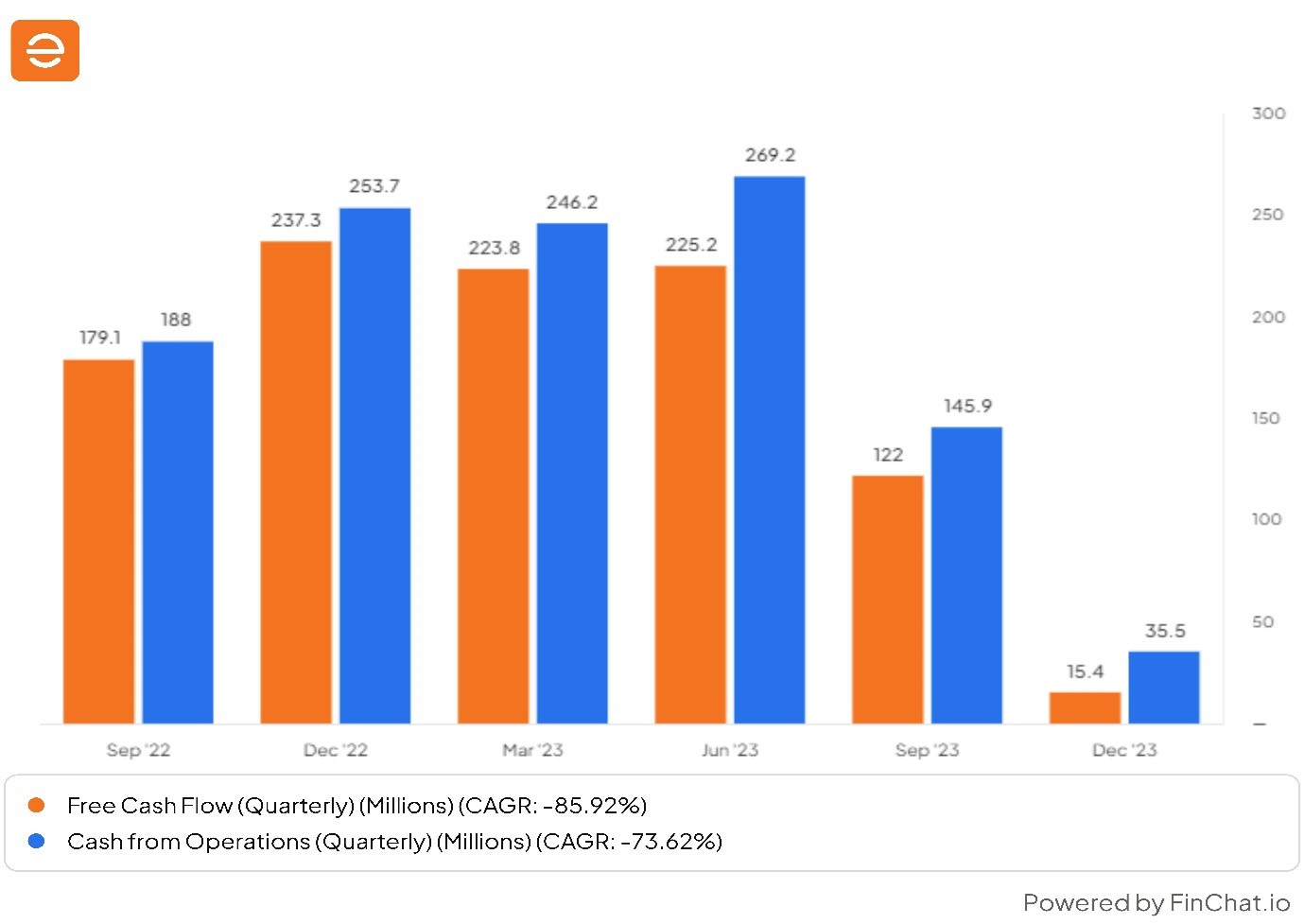

Cash flow from operations and Free Cash Flow fell significantly but remained positive in Q4.

The market cap fell from the December 2022 peak and so did the P/E Ratio.

Enphase announced their Q4 Quarterly Earnings on 7th February. The stock rallied after the numbers and the conference call. Comments during the call were interpreted as Enphase calling an end to the downturn in demand.

Q4 Results

Enphase's Q4 revenue was $302.6mn, which compares with analysts' expectations of $327.9mn. The revenue level was below expectations.

Gross margin was 50%

Operating profit was a loss of $ 10mn compared with a profit Of $ 157mn in same quarter in the previous year.

So, the numbers continued the recent negative trend.

However, the detailed explanations behind the numbers offered some encouraging explanations.

On the previous earnings call, they said they would reduce channel inventory in the quarter by approximately $150 million. The actual reduction of $147 million in Q4.

Though Enphase revenues were $ 303mn, total demand for Enphase product sales in the quarter were $ 450mn (303mn plus 147mn).

The total amount sold to the market (450mn) is called the sell through. Enphase sales were only $ 303mn and therefore they undershipped by $ 147mn.

“The overall sell-through of our micro inverters and batteries in the U.S. was down 9% in Q4 compared to Q3.”

In Q1, the current quarter, they expect an undershipment of $130 million. Therefore, in the six months to end March 2024, they should have reduced inventories by $ 277mn ($130mn + $ 147mn).

These two quarters are the northern winter and there is lower demand for installations. There is a seasonal pick up from Q2 onwards.

They expect sell through demand to pick up after April 1st and given the exhaustion of inventories, this should feed through to an increase in demand for Enphase as the year progresses,

The breakdown of sales between US and non-US is 75% to 25%. The non-Us is mostly Europe.

The earnings conference call went into a lot of detail about the current demand situation and why demand should pick up strongly in second half of 2024.

We can only offer a summary here. Interested reader should read the full transcript.

Enphase Energy current supplies its own microinverters and buys batteries from China and distributes them. From the 3rd quarter, its long-term manufacturing partners will be able supply US-made batteries. These will benefit from subsidies arising from the Inflation Reduction (IRA) Act passed by the Biden administration.

Non-US California

“For non-California states, our overall sell-through was only down 1% in Q4 compared to Q3.”

Non-California demand is flat essentially.

“The sell-through of our microinverters was flat and the sell-through of our batteries was down 8% in Q4.”

Non-California demand has been flat. With lower inventories and the Q4 seasonality boost in the Spring, they are confident that demand will pick up in Q2 and this will be clear in the second half the calendar year.

Europe

Currently Enphase is only three markets in Europe: France, Germany and Netherlands

“The overall sell-through of our microinverters and batteries in Europe was down 20% in Q4 compared to Q3.

The sell-through of our microinverters was down 23% and sell-through of batteries was down 2% in Q4 compared to Q3.”

France: France demand decline in negligible. France is well placed to see a pick-up in demand.

Germany: “In Germany, our overall sell-through in Q4 was down 32% compared to Q3.”

Netherlands: “In Netherlands, our overall sell-through in Q4 was down 37% compared to Q3.”

There are special circumstances in both these markets. In the earnings conference call, the company has given a detailed explanation as to why demand will pick up in the second half of 2023 in both these markets.

In addition. the company is going into new markets such as the UK and Italy in Europe. In the longer-term Asia and South America are promising areas of growth.

California

The company described California as a wild card. The implementation on NEM 3.0 has hit demand sharply in the short run.

NEM3.0 is designed to encourage residents to buy batteries so they can store the power their panels have produced rather than exporting all unused power to the GRID. This can overwhelm the system during long hot spells.

The problem is batteries are expensive relative to Panels or Microinverters and greatly increase the total installation cost. The up-front cost is much higher when a battery is attached. This increases consumers reluctance, especially if the cost of borrowing remains elevated. This is particularly applicable in California, where homes are large and the sun shines a lot and so the largest, most expensive batteries are required.

The company estimates that the California payback period for a solar plus battery system is currently about 7 years which compares with component life of 15 to 25 years.

There will be a big need to educate and train installers about this and the benefits of added batteries and the EV charger the company has designed.

The company believe NEM 3.0 will eventually be positive for battery sales and for demand for microinverters.

Summary

Our original report focused too much on the macro factors such as the growth of renewables and solar worldwide and technological sophistication of the products and software offered by Enphase.

We ignored the effect on demand of rising interest rates and the falling rates paid by California NEM3.0. This was a costly mistake as the share price fell sharply in 2023.

We also were not aware of the risks posed by the build-up of inventory both on the company’s balance sheet and in the distributor channel.

The company is confident that demand will pick up in the second half of the year and is effectively calling a bottom in demand.

The big question is whether sales will recover to a $ 700mn quarterly run rate by 2026.

Annual sales peaked at 2.3bn in 2022.

Quarterly sales peaked at US$ 726mn in Q1 2023.

The current consensus is for sales of $ 2.3bn in 2025 with a net profit of $ 725mn and an EPS of 5.45.

At the current stock price this implies a two year forward Price/ Earnings ratio of 21.2 times.

This does not look expensive given the historic ROEs and margins the company has achieved.

However, the events of the last year have probably weakened investors’ confidence and markets may want to see more evidence of a recovery in demand before pushing it higher.

We are sitting on a 38% loss on our position which makes it our worst performer by far. However, we will hold on for now.

I have bought both Enphase and Solaredge, after their big decline.