Heico Inc. (HEI)

We covered HEI in an earlier note which can be found here.

HEI is a leading aerospace parts manufacturer and distributor. About half of its business comes from the Flight Support Group (FSG), whose main business is FAA approved functional equivalent parts that are otherwise sold by original equipment manufacturers (OEMs) (Boeing Pratt& Whitney, Airbus etc). HEI sells parts below the price levels of the OEMs.

The customers (airlines and defence organisations and contractors) like that there is a second source for the aftermarket parts, as it keeps prices in check. The OEMs do not worry too much as HEI has vowed only to take 30% market share.

Another business within FSG handles parts distribution and repairs for domestic and foreign airlines and defence contractors.

The second business segment for HEI is the Electronic Technologies Group (ETG) which has many subsidiaries that manufacture electronic, microwave and electro-optical products. 66% of ETGs revenues come from the defence industry which is more predictable and less cyclical than the airline industry. ETG has customers in medical, telecommunications and electronic industries as well as the aviation, defence and space segments which are the mainstay of FSG demand.

The businesses (esp. FSG) have generated a lot of cash flows which, along with debt, have been used to acquire numerous smaller companies. Since 1990 when the present family management team took over, 90 acquisitions have been undertaken. 80% of the acquisitions have been in ETG.

The sellers of the companies stay on and retain some equity ownership (up to 15%) in their company and incentivised to ensure growth in their companies. HEICO a lot of autonomy to run their companies. HEICO intends to hold the business for ever. For founders and senior managers, HEICO is an appealing buyer, and it shares some similarities with Berkshire Hathaway in this regard.

Since 1990 the HEI stock has given a return of 21.1% per annum (CAGR) which is a 697X return. Over the same period, Berkshire Hathaway has given a return of 13.2% CAGR or 69X.

Forbes had an article on the company in 2020 which is worth reading and can be found here:

https://www.forbes.com/sites/abrambrown/2020/01/13/heico-mendelson/?sh=446198134b18

HEI recently reported their Q1 2024 Results. They have an end-October year end.

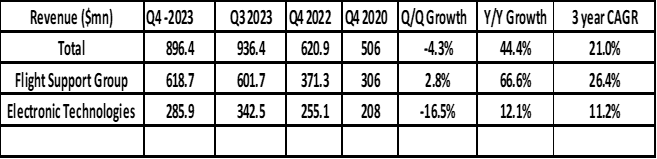

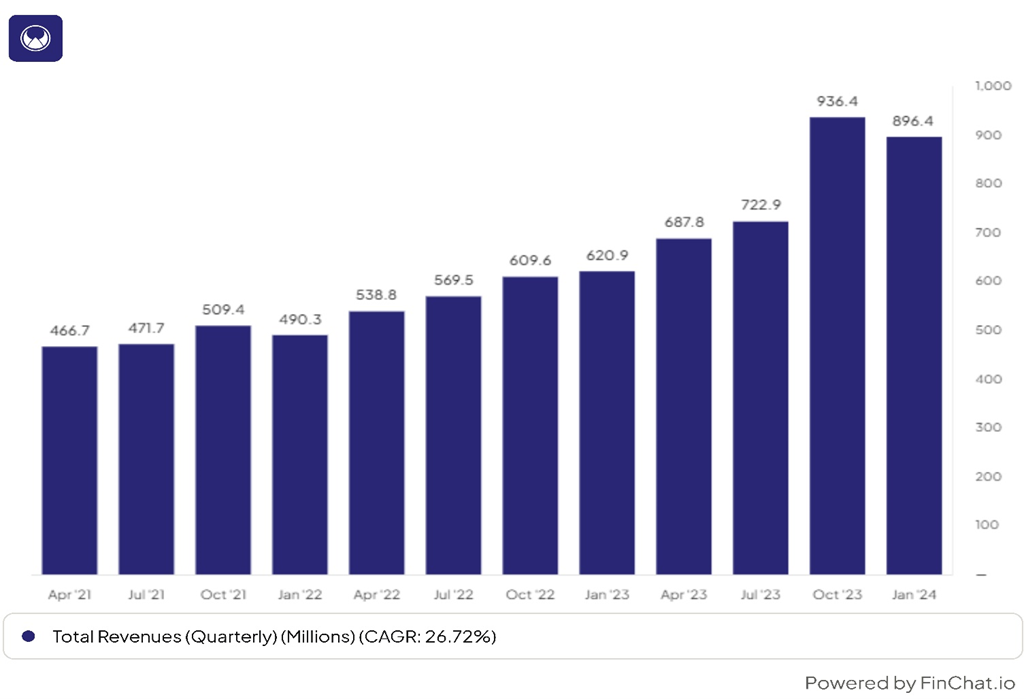

Total quarterly revenue was $896mn (+ 44% y/y but -4.3% q/q).

FSG performed well but ETG underperformed.

The Q!1 2024 quarterly revenue decline was the first for a while.

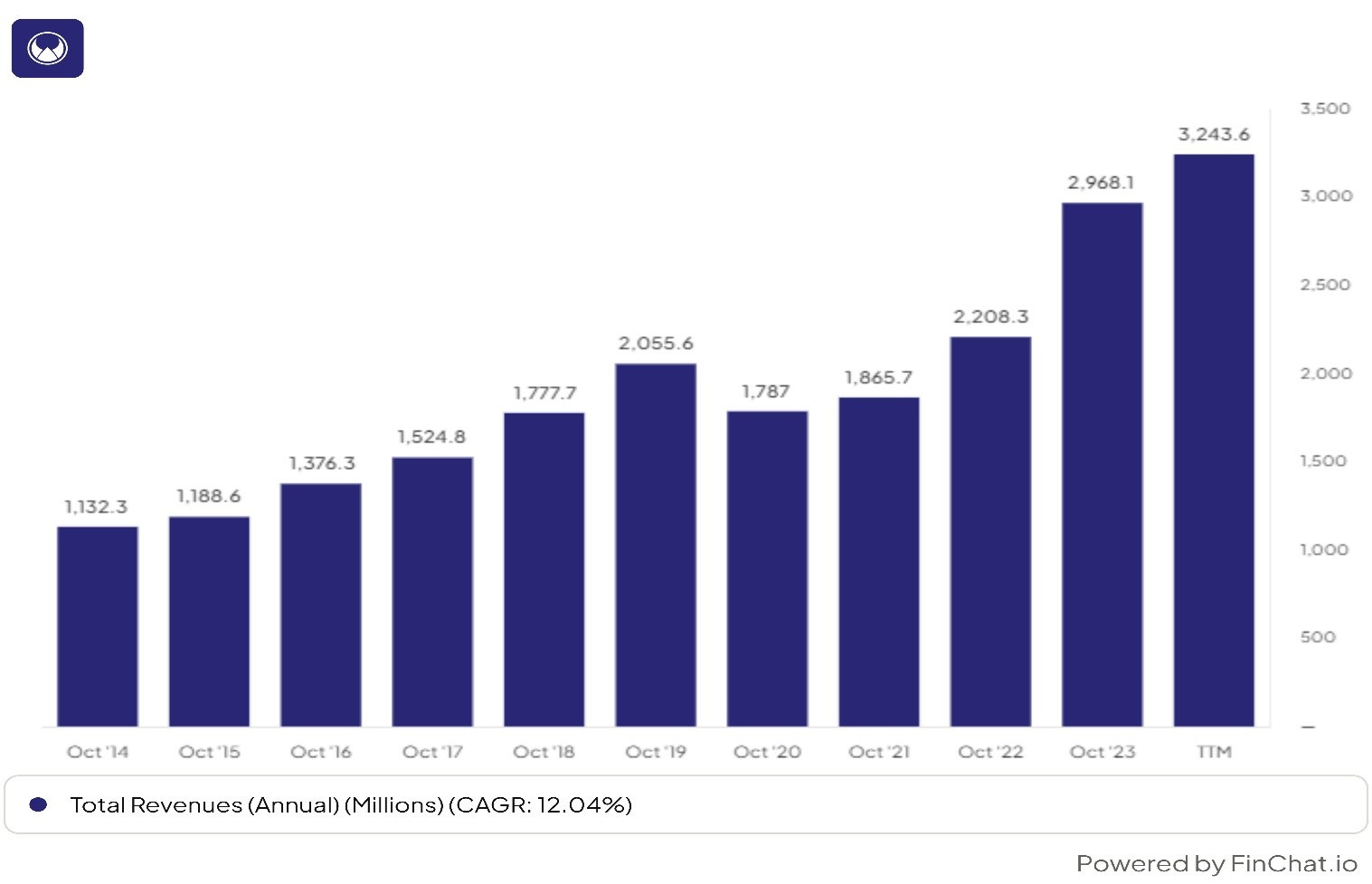

Looking at the annual numbers (above), revenues have recovered from the Covid Pandemic hit of 2020 and 2021.

Operating Profit grew 32.6% q/q and Net Profit Grew 23.3 q/q.

Ebit margins and Net Income margins declined a little.

Highlights from the earnings conference call

“The Flight Support Group (FSG) set an all-time quarterly net sales and operating income record in the first quarter of fiscal '24, improving 67% and 63% respectively…The increases principally reflect the impact from our fiscal '23 acquisition of Wencor and 12% organic growth mainly attributable to increased demand within our aftermarket replacement parts and repair and overhaul parts and services.”

Wencor was a large acquisition (value ~ $ 1.3bn) which was completed about a year ago. It accounted for most of the 66% increase in sales in FSG. Organic growth in FSG was a more sedate 12%.

“Cash flow provided by operating activities increased 46% to $111.7 million in the first quarter fiscal '24 …We continue to forecast strong cash flow from operations for fiscal '24.”

The more sedate performance in ETG is explained thus:

“The slight operating income decrease (in ETG) principally resulted from our subsidiary shipment schedules of our record backlogs with fewer shipment in the first quarter than scheduled in future quarters, something that was scheduled prior to the quarter start and is in line with our internal plan.”

“We are expecting a quite different result from ETG from the second quarter through the end of the year. …it is a lumpy business, and the sales and earnings should come through from the second to the fourth quarter.”

“I have said publicly that our goal is to grow net income 15% to 20% annually compounded. Over the last 30 to 33 years, we have done that, and the actual growth has been somewhere around 18% or 19%. I clearly am highly confident that we will attain that 15% to 20% growth in the current year and that without any future acquisitions which we might make.”

Summary

This was another set of reasonable results from a well-established company.

Since 1990 the company has given an impressive 21.1% return over 34 years which translates to a near 700X return.

FSG has a strong position in aircraft parts. Due to critical safety considerations, it is very difficult to get FAA approvals (called Parts Manufacturers Approvals or PMAs) to make aircraft parts and FSG has a good track record in this regard. HEICO is thought to command more than half of the PMA dollars in the aerospace market. Another company Transdigm (TDG) has a large part of the rest of the non-OEM parts market. New entrants would have to meet rigorous, very exacting FAA standards and therefore, new entrants are unlikely in the short to medium term.

Safety regulations regarding when to replace parts are very strict and Airlines must replace them on the prescribed replacement schedule.

HEI has produced over 11,500 PMAs to date and develops 350-400 PMAs per year. HEICO typically works with customers before a new PMA project, ensuring that there is ample demand for the product and the company typically gets order commitments before commencing manufacturing.

Adam Sessel in his book “Where the Money Is” writes about HEICO’s product runway.

“Despite this spectacular rise, HEICO today still has less than a 5% market share of aftermarket spares. After a generation in the business, HEICO now makes 10,000 generic parts, or one-half of 1% of the 2 million total parts on a plane. At its current rate of introducing seven hundred new parts annually, it would take HEICO 3,000 years to produce all those parts in generic form. Even if you took a conservative view and said that 75% of the parts were too complex to ever be genericized, it would still take HEICO seven centuries to manufacture the rest.”

Suffice to say, FSG’s PMA business has a very long, semi-protected, runway.

HEI has very successfully used the cash generated from the PMA business to acquire other companies. Almost all the Free Cash Flow has been used for acquisitions and the company has a 30 year-long track record of doing this successfully. HEI does not buy back shares, nor does it pay dividends.

The acquired subsidiaries usually have the existing management left alone to run the companies autonomously with meaningful incentives to perform. There is little of the usual talk about integration and synergies at Heico.

HEI management has credibility when they say they can grow revenues at 15% to 20% as they have done it in the last three decade. This growth is likely to be generated at an operating margin of 20%.

The HEI stock is currently trading at a two-year forward P/E ratio of 45 times. This seems expensive for a company growing at15%- 20% per annum with operating margins of 20% and a ROE of about 15% to 17%.

A significant adjustment has to be made for their very strong position in the aircraft parts /PMA business, but we are unsure as to how big this premium should be.

We will continue to watch this company. It is likely to perform very well in the long run, but it is hard to determine whether the current price is an appropriate entry point.