Interactive Brokers (IBKR)

Pre-eminent technology-driven global brokerage.

IBKR Description

“IBKR is an automated electronic broker. It specialises in executing and clearing trades in stocks, options, futures, foreign exchange instruments, bonds, mutual funds, and exchange-traded funds, as well as offers custody, prime brokerage, securities, and margin lending services. Interactive Brokers Group serves customers globally.”

(Source: Hoover's Inc., a Dun & Bradstreet Company)

OVERVIEW

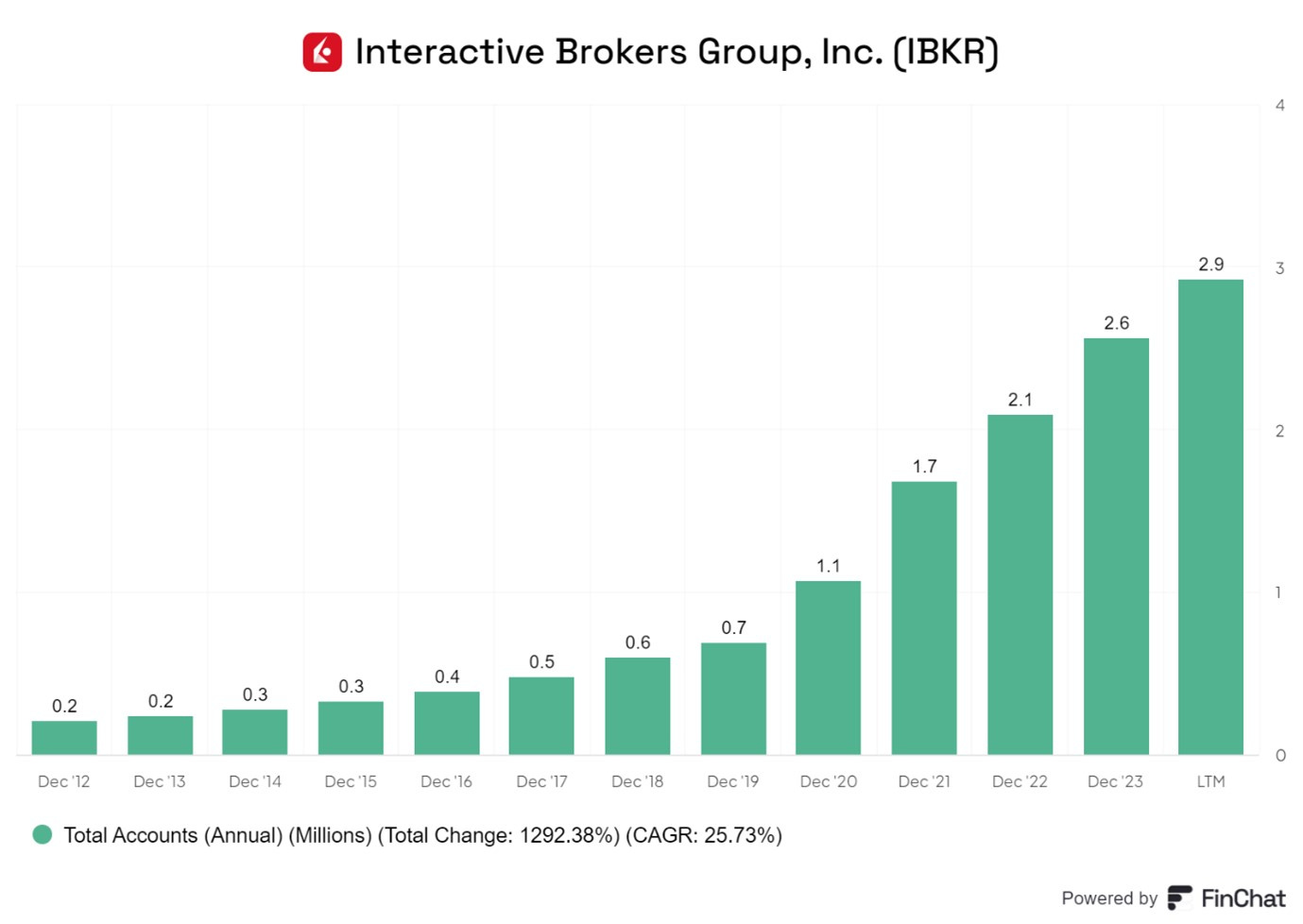

In essence, IBKR helps anyone buy and sell multiple different assets through their platform. With 2.8 million accounts worldwide, IBKR provides access to over 150 markets in 27 currencies in 34 counties and serves customers in more than 200 countries. The platform is known for its low prices, broad market access, and advanced trading tools.

IBKR services accounts for hedge and mutual funds, exchange-traded funds (ETFs), registered investment advisors (RIAs), proprietary trading groups, introducing brokers (IBs) and individual investors.

The company also licenses its trading interface to large banks and brokerages through white branding agreements. IBKR operates worldwide but generates about 70% of its revenue in the US.

“Since our inception, we have focused on developing proprietary software to automate broker-dealer functions. We have been a pioneer in developing and applying technology as a financial intermediary to increase liquidity and transparency in the capital markets in which we operate. The proliferation of electronic exchanges and market centres has allowed us to integrate our software with an increasing number of trading venues, creating automatically functioning, computerized platforms that require minimal human intervention. Over four decades of developing our automated trading platforms and automating many middle- and back-office functions have allowed us to become one of the lowest cost providers of broker-dealer services and to significantly increase the volume of trades we handle.”

IBKR Operations

Interactive Brokers offers three principal products

1. IBKR Pro,

2. IBKR Lite and

3. IBKR Integrated Investment Account.

IBKR Pro is the traditional IBKR service designed for sophisticated investors. It offers the lowest cost access to all classes of financial instruments. This product is aimed at Institutional Investors, Funds and Professional trading firms.

IBKR Lite provides unlimited commission-free trades on US exchange-listed stocks and ETFs as well as low-cost access to global markets without required account minimums or inactivity fees to participating US customers. This is targeted at smaller active traders. IBKR Lite was introduced in 2019 in response to the trend of commission-free trading. It operates on a zero-commission basis, earning revenue through payment for order flow (PFOF). With PFOF the broker, like Robinhood or IBKR, receives compensation for routing the orders they receive to market makers (like Citadel Securities, Jane Street and Flow Traders).

BKR Integrated Investment Account include Interactive Brokers Debit Mastercard, Bill Pay, Direct Deposit and Mobile Check Deposit, Insured Bank Deposit Sweep Program, Investors' Marketplace, Mutual Fund Marketplace, Bonds Marketplace, Fractional Trading. This product is directed at smaller individual investors and the firms that service them.

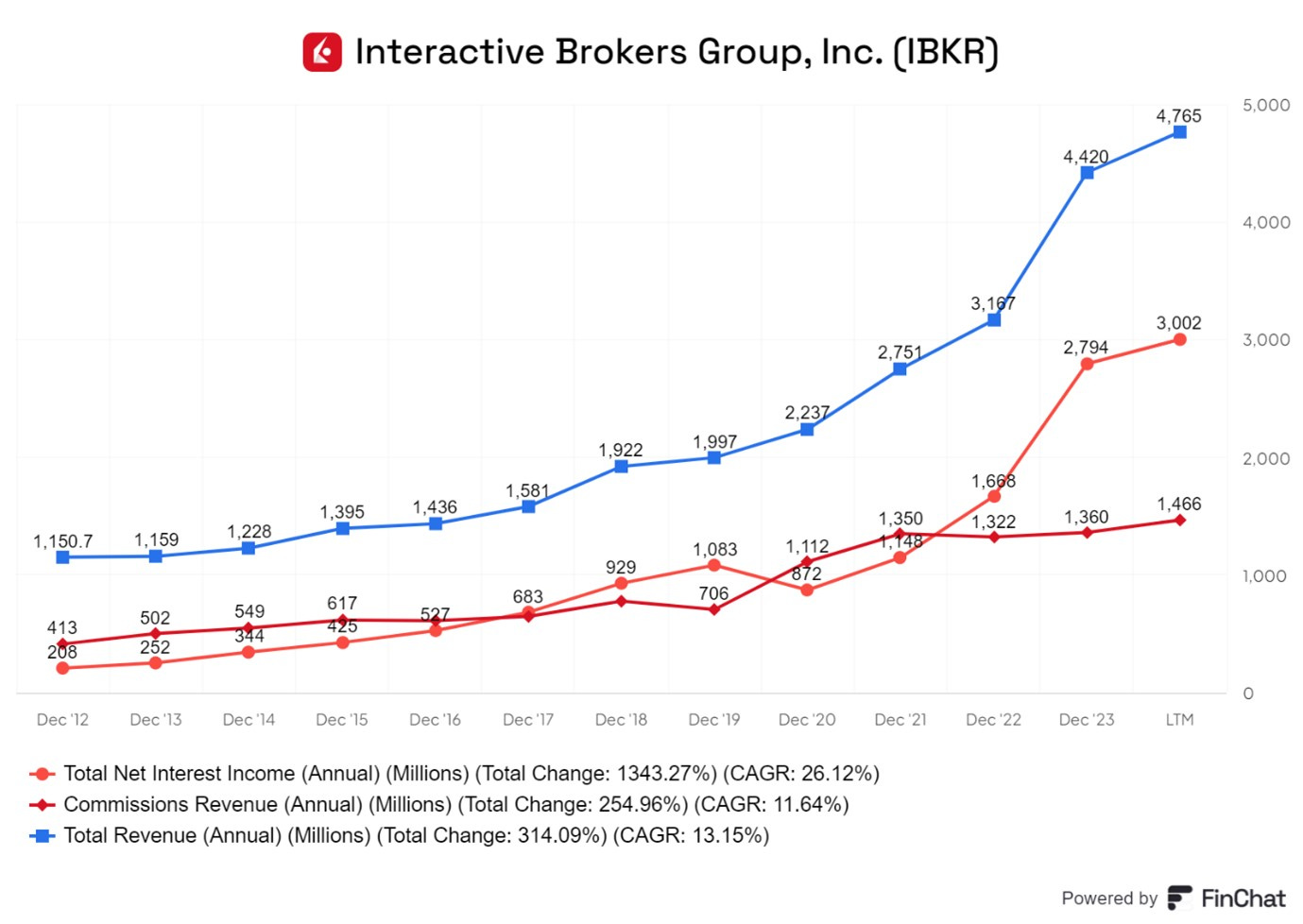

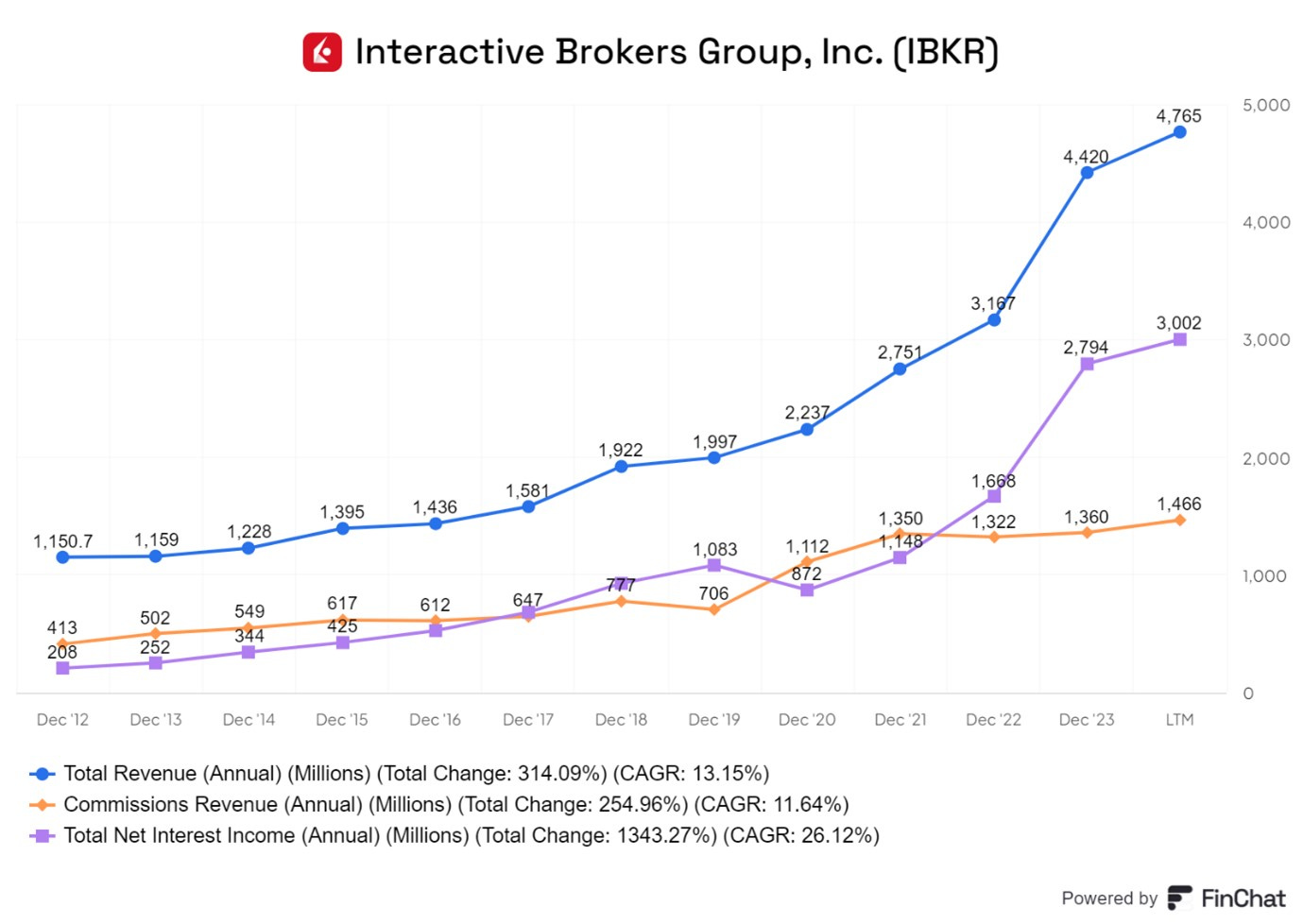

IBKR gains the bulk of its revenue from interest income and commissions.

The two categories were equal contributed to a similar degree until December 2021. In 2022/23, the US Federal Reserve increased interest rates five times in rapid succession and IBKR total net interest income has grown rapidly since then. Net Interest Income now accounts for 2/3 of total revenues while commissions account for 1/3.

Geographic Reach

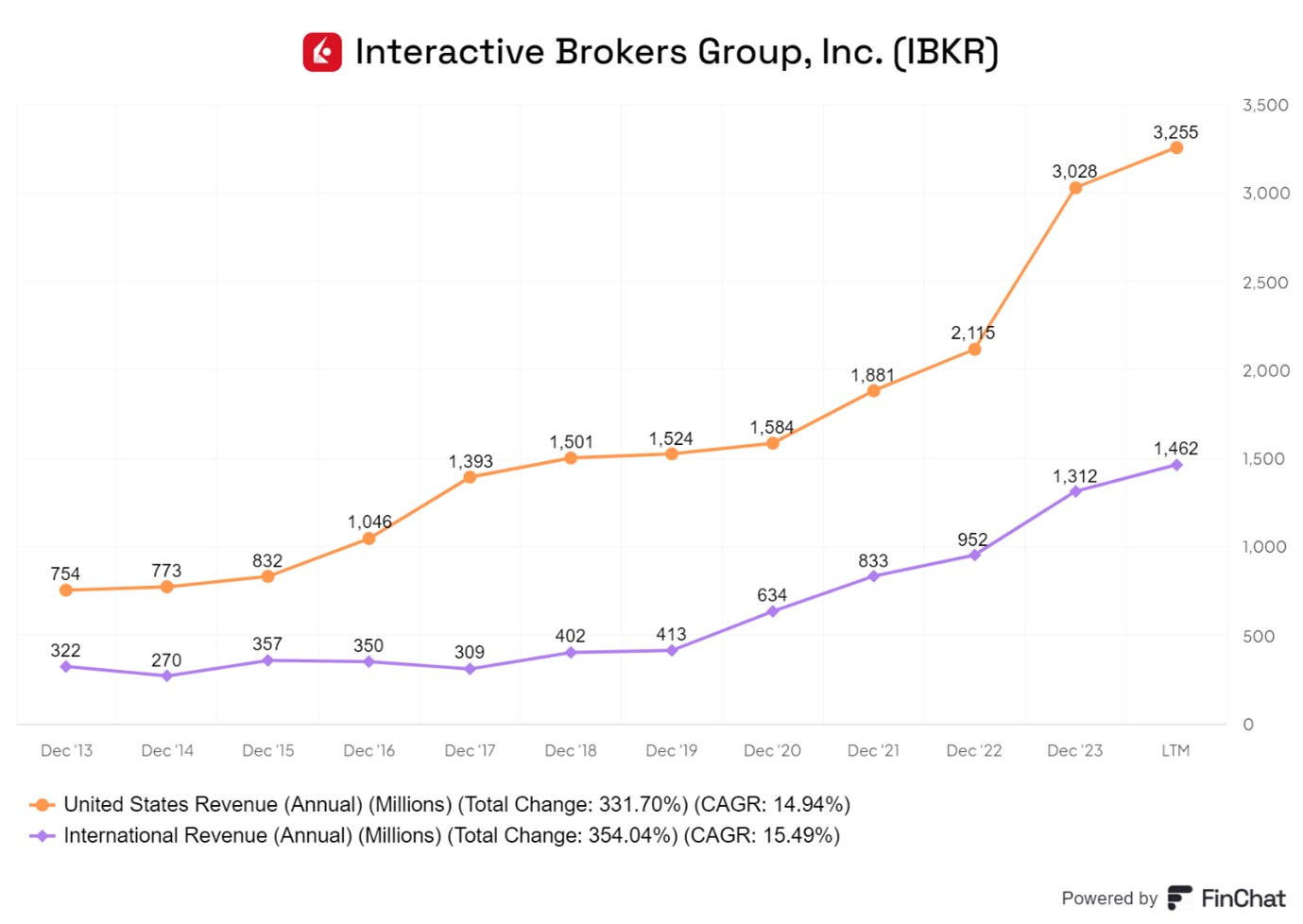

IBKR has customers in more than 200 countries and territories. It has US offices in cities including Chicago, Illinois and nine other locations. The company's overseas offices are in Canada, the United Kingdom, Ireland, Luxembourg, Switzerland, Hungary, India, China (Hong Kong and Shanghai), Japan, Singapore, and Australia. The US generates about 70% the company's revenue while international countries generates for about 30%. As the chart below shows, international revenues have grown slightly faster than US revenues.

Sales and Marketing

IBKR categorizes its clients into the 2 groups: cleared customers and non-cleared customers (or trade execution customers).

Cleared customers include small group and individual market makers, institutional and individual traders, introducing brokers, financial advisors, and hedge funds.

Non-cleared customers who use IBKR for excursion but clear with another prime broker or custodian bank. Non-cleared customers include online brokers and commercial bank customer trading units.

Company Background

IBKR was founded by 79 year old Thomas Peterffy who is currently the Chairman.

Thomas Peterffy

Peterffy started the company in 1978 as T.P. & Co. Peterffy was a pioneer of digital trading in the 1980s, he was the first to build computer systems able to trade financial assets electronically, independent of direct human intervention.

In 1977, he became a member of the American Stock Exchange. He built the first automated market-making firm for stocks, options, and futures, which later gave rise to IBKR. The company has grown from 200k customer accounts to 3mn. Long-Term Investing is a customer.

Customers

Cleared customers are the vast majority of their customers. IBKR’s USP to clients is simple: they offer the best possible execution for trades at the lowest price and have competitive interest rates on client balances and lending to clients. Other selling points are IBKR’s the conservative financial policies and the solid balance sheet. Clearing Clients leave assets and cash with brokers. The financial soundness of the broker is an important consideration.

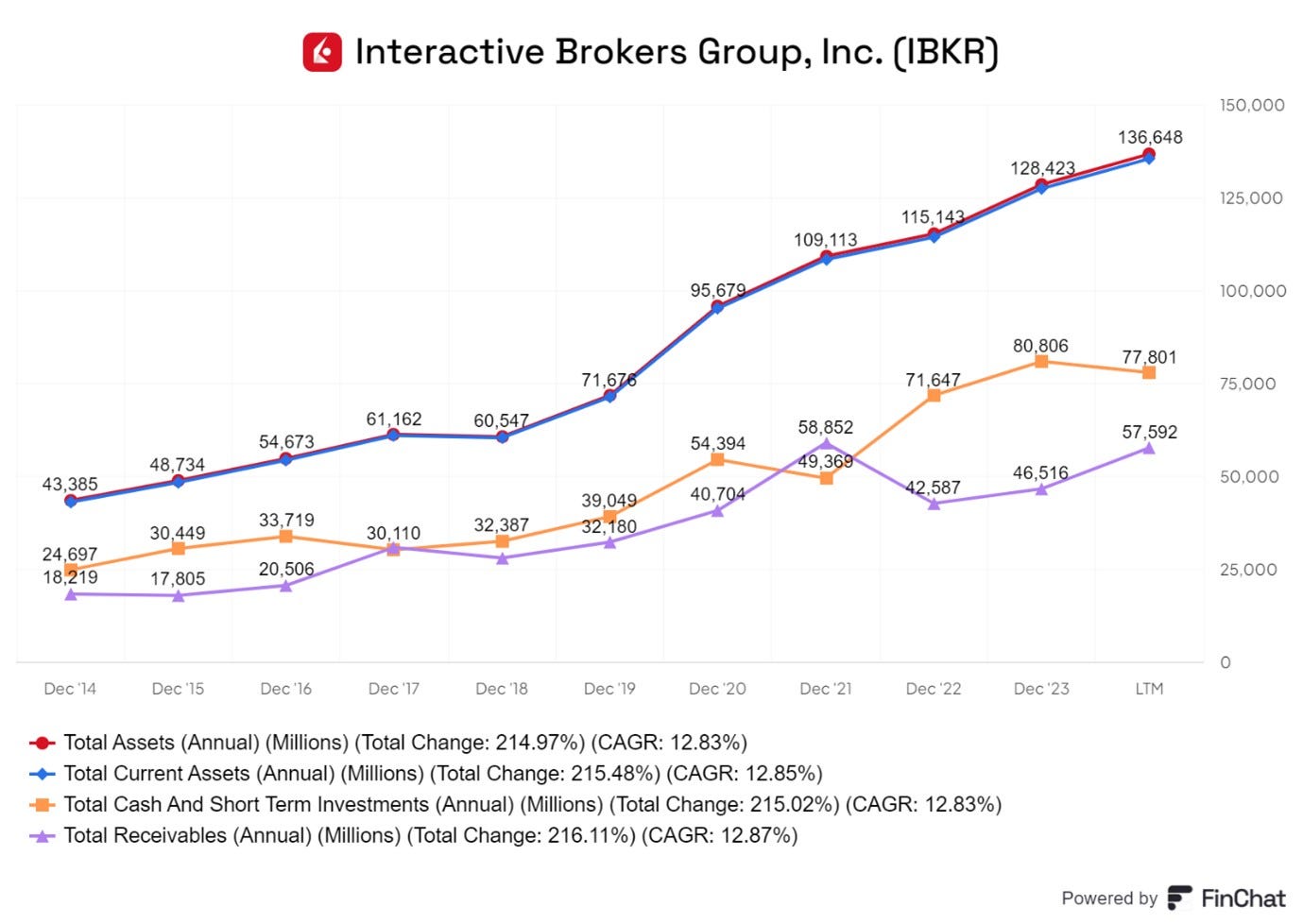

IBKR total assets are currently about $136bn and all but $200mn of these are current assets. $77bn consists of cash and short- term investments and $58bn are receivables. The latter occur where clients have sold shares and the transactions have not settled and money is due to be received. Given the nature of the business, current assets and liabilities will be a large part of the Balance Sheet. IBKR has no long-term debt. It has a sound and liquid balance sheet.

In 2023, there was a banking crisis when Silicon Valley Bank collapsed (third largest bank failure in US history) and this was followed by the demise of Signature Bank and Silvergate Bank. Shares of Charles Schwab (SCHW) came under great pressure at the time. SCHW is a major broker and competitor of IBKR.

The failed institutions had invested customers’, depositors’ and their own money to a in long-term Treasury Bonds and other government securities as long as 15 years.

In 2022/2023, the Federal Reserve raised interest rates rapidly from 0.5% to 5.25%. Bond prices fell. Bond mathematics dictates bonds with the longest maturities and durations will fall the most in response to rising interest rates. As a result, the firms sustained huge mark to market losses on their extensive bond holdings and this led to a loss of confidence and their eventual collapse after a run on deposits. IBKR mainly invests in short-dated paper which as almost no market risk. IBKR has always been conservative and did not make the losses in 2023 their rivals suffered.

IBKR’s Position in the market

As many exchanges stopped opened outcry trading formats and became electronic in the 1980s, there was need for an electronic platform for professional traders who did not want to miss out on the growing electronic liquidity. It was a professional platform from inception.

IBKR appeals to professional traders including Hedge Funds who are unable to secure Prime Brokerage relationships with the likes of JP Morgan, Morgan Stanley or Goldman Sachs. These Funds may be too small, or their investment strategies do not require the high levels of trading the big banks demand.

IBKR stands somewhere in the middle between the large investment banks on the one hand and the retail targeting entities such as Charles Schwab, Robin Hood, Fidelity or Raymond James on the other. SCHW has a $118bn market cap and it is a diversified company which is an S&L (Savings and Loan) as well and an asset manager and advisor. Robinhood has a market cap of $20bn and IBKR which has a $16bn.

When compared with the investment banks, IBKR offers an equally professional platform as a Goldman Sachs (global access to 150 global markets). However, unlike the large firms, IBKR is not involved in equity research, corporate finance or asset management.

Like the retail brokers, IBKR offers access to smaller individual investors and traders. However, compared with other retail brokers. IBKR does not actively chase smaller clients and does not offer credit cards or advisory services which would be appeal to them.

In summary, IBKR’s clients are somewhat smaller than those targeted by the bulge-bracket firms but are much more sophisticated than those targeted by the retail brokers. The Company is very focused on its niche and wary of diversifying into adjacent business

“We will not go into asset management because we do not want to compete with the asset managers who are our customers.” This comment was made by Thomas Peterffy in an informative podcast interview which can be can be heard using the link below.

IBKR does not have its own advisers as it wants Independent Registered Investment Advisers (RIA) to trade on the platform.

“So many firms have done. I think they made an error when they did that, such as Fidelity and Schwab have their own asset management and have their own RIAs on their platform who are employees of the firms. So as a result, many independent RIAs see Schwab and Fidelity as competitors while they are also on their platform.”

“There is a large sophisticated and growing customer base that wants our type of service and outside of the United States worldwide, we have practically no competition.”

“We have about 160 exchanges on our platform, 27 different currencies. We're going to continue to add other new exchanges, other new currencies, other new products, and that's how we are going to keep growing. I think we'll have tens of millions of customers in the very near future.”

Summary Financial Numbers

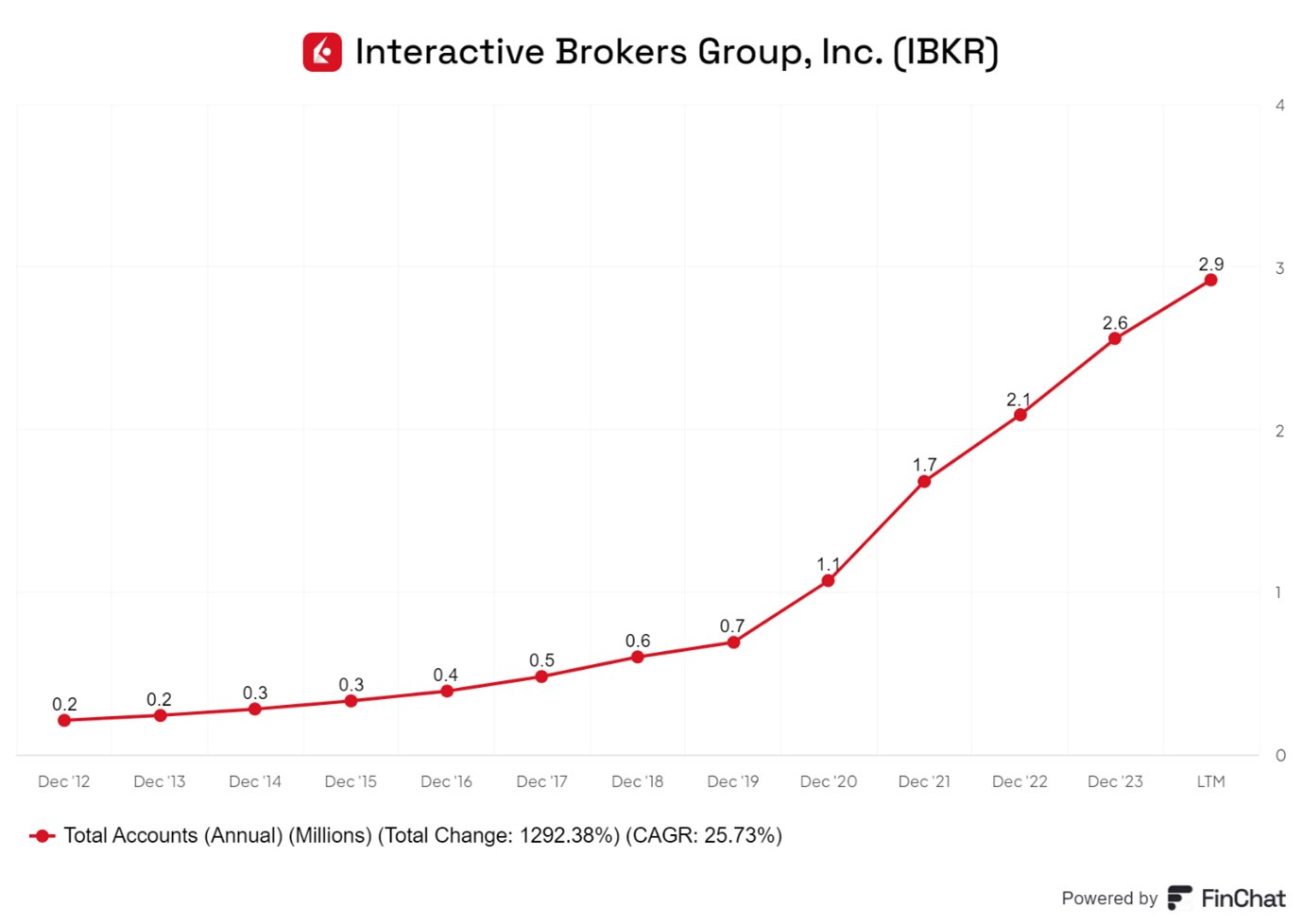

Total number of accounts from 200k in 2012 has grown to 3mn currently. This represents at a CAGR of 25.7%.

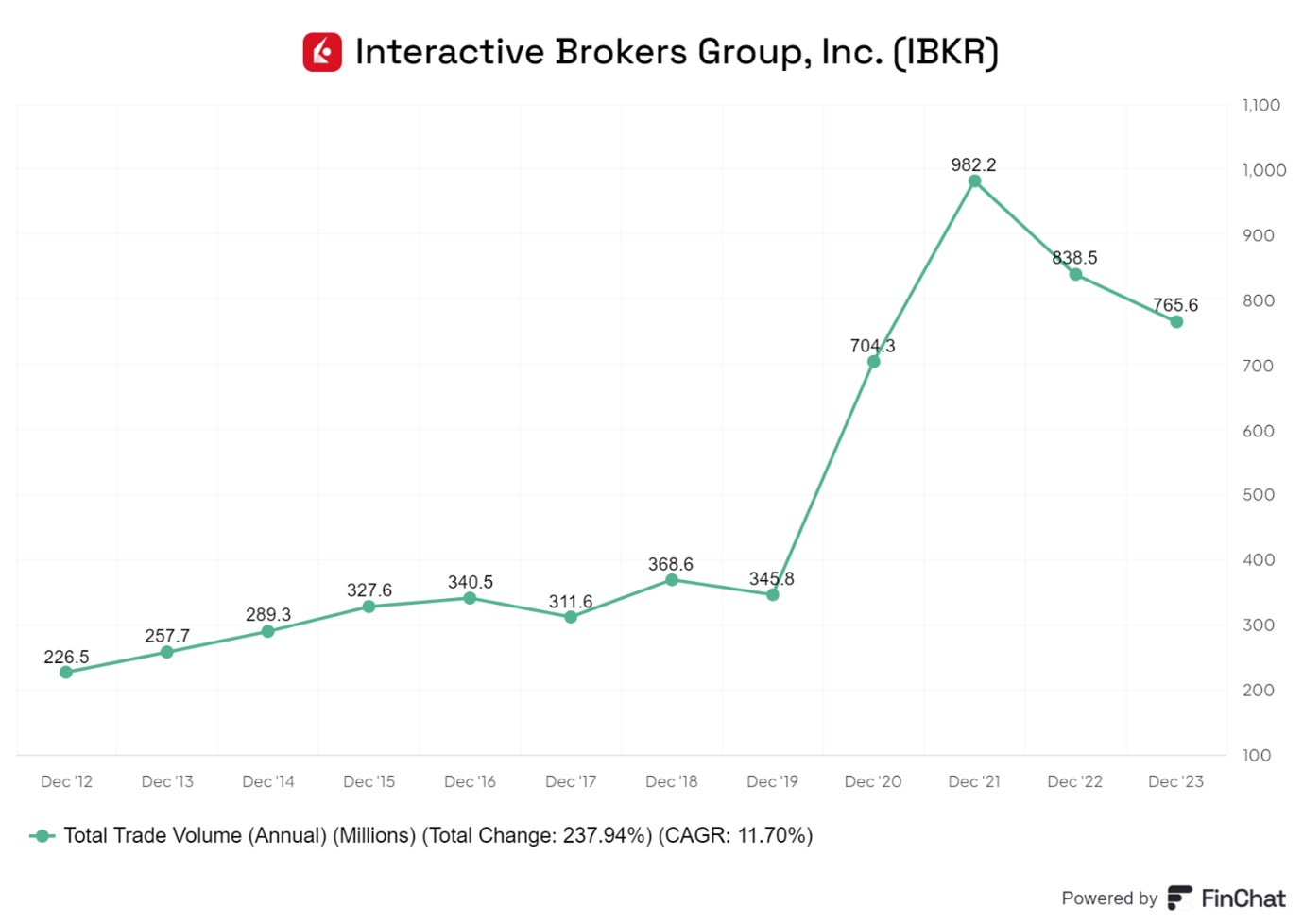

Total revenues have grown at a CAGR of 13.15%, slower than the growth of customers numbers. This is a cyclical business, but IBKR has navigated it well and commission revenue has never fallen over a two-year period.

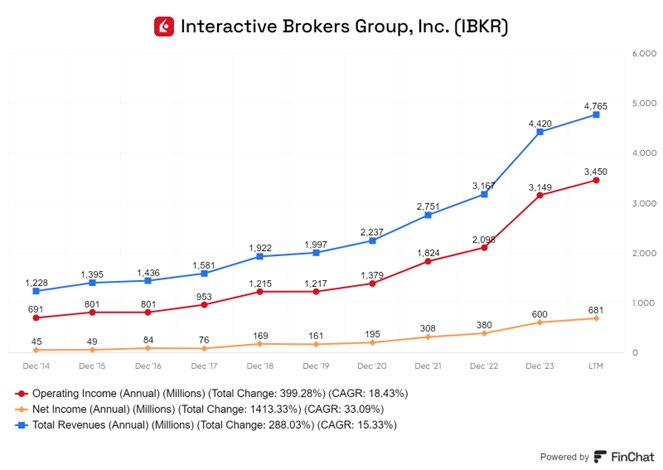

Operating Income has grown faster (18.4% CAGR) than operating revenue indicating some measure of operating leverage in the business. Net Income has grown much faster than operating income (33% CAGR).

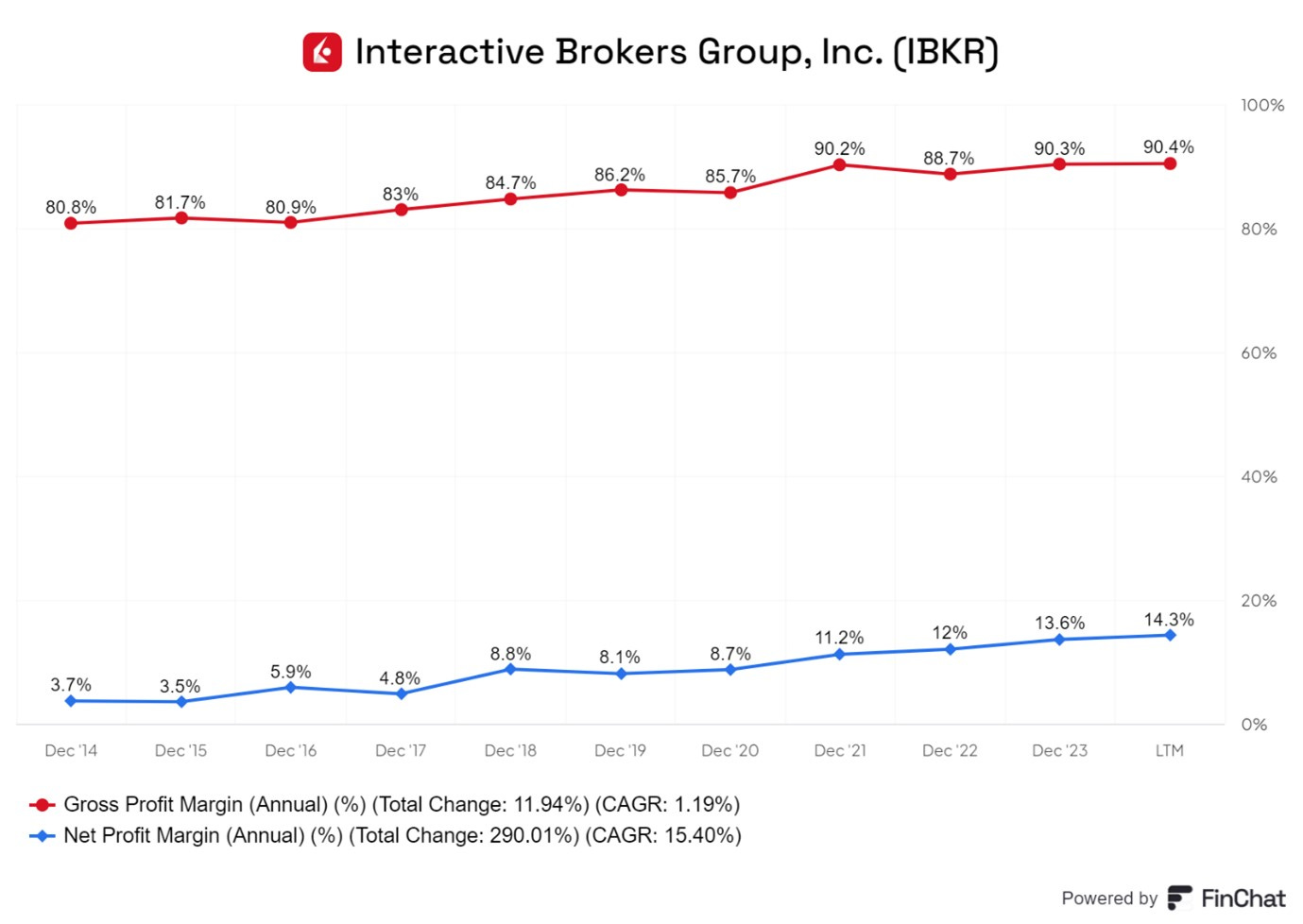

IBKR has high very high Gross Margins of about 90% which indicates very low costs. Operating Margins are about 70%. Net Profit Margins are lower due to the shareholding structure company which will be discussed later.

Current Assets and Liabilities given the nature of the business. The two items have grown in line but current assets have always been greater than liabilities as shown below.

Over the last 17 years, the stock has given a CAGR of 9.3%.

Over the last 3 years, the stock has given a CAGR of 27.2%.

Over the last 1 years, the stock has given a CAGR of 68%.

IBKR shares have performed strongly in the last year and therefore, it is likely to be trading at a high valuation.

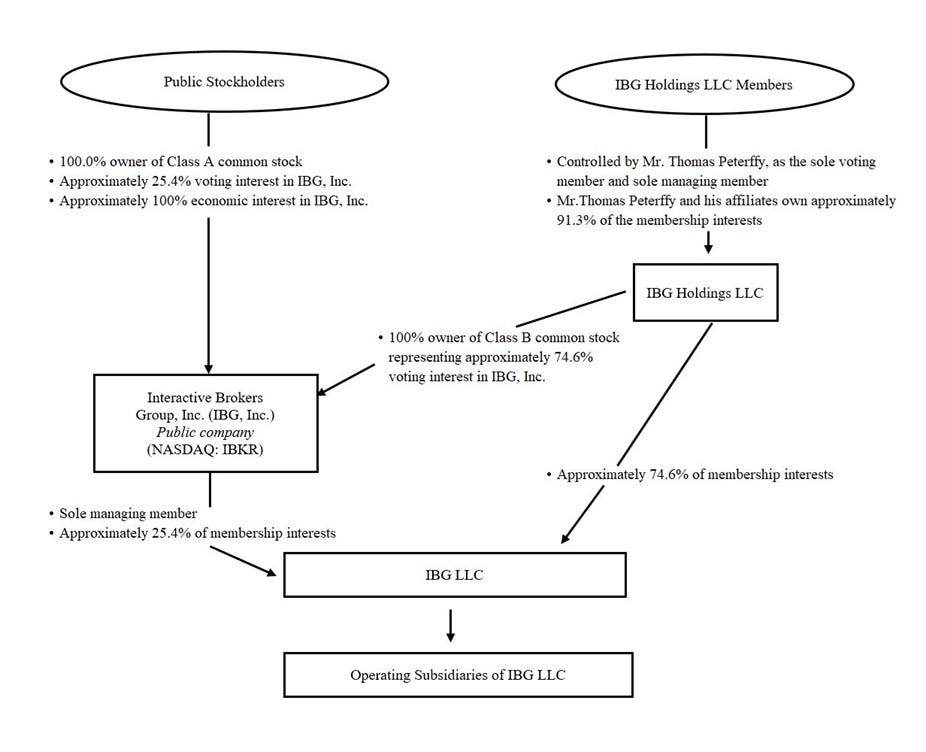

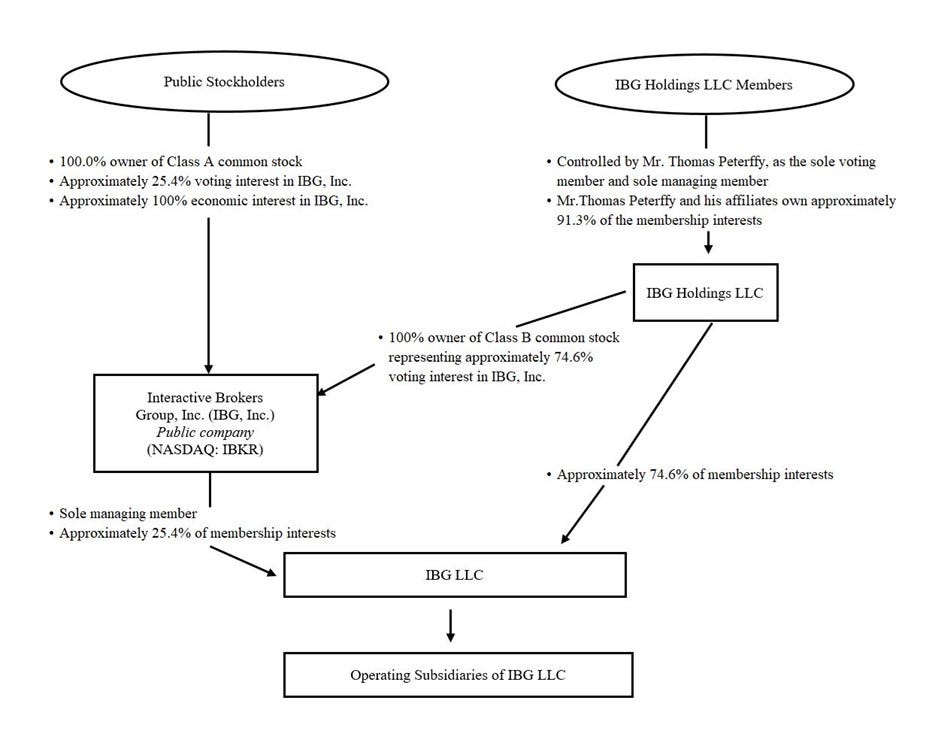

Dual share structure

IBKR has a complex dual share structure as illustrated in the diagram below.

IBKR, IBG Holdings LLC and IBG LLC are Holding Companies.

IBKR aka IBG Inc has two classes of shares

Public shareholders hold 100% of the Class A shares and this amounts to a 25.4 % shareholding in IBG Inc and IBG LLC.

IBG Holdings LLC a vehicle controlled by Thomas Peterffy holds 100% over the Class B shares of IBKR which gives at 74.6 % shareholding or “membership interest” in IBKR and IBG LLC.

This dual structure means the Company is under the effective control of Mr Peterffy. The structure reflects the fact that Mr Peterffy and associates owns 74.6% of IBKR. We are not too worried about the unusual structure as Mr Peterffy has proved to be skilled and rational manager and capital allocator over many decades.

Technology

One of the key differentiating factors of IBKR is technology. Almost all of the IBKR technology has been developed in-house and is optimised for automating processes and ensuring fast and efficient execution. Majority of senior management are software engineers, committed to automating as many brokerage processes as possible.

All processes from account opening through the entire transaction lifecycle are automated. Functions such as real time risk-management, securities lending and short stock availability are embedded in the platform and automated. IBKR integrates their technology with electronic exchanges and market trading venues, and this leads to transparency, liquidity and efficiencies of scale.

As a customer, Long-term Investing can vouch for the quality of their products and the excellence of the low- touch service they provide.

Sources of Income

Commissions

Customers pay brokerage for stock trades they execute on the platform. IBKR Pro uses the traditional brokerage model, charging commissions on trades. IBKR Commission rates are competitive. Commission income moves in line with total client assets and trading volumes.

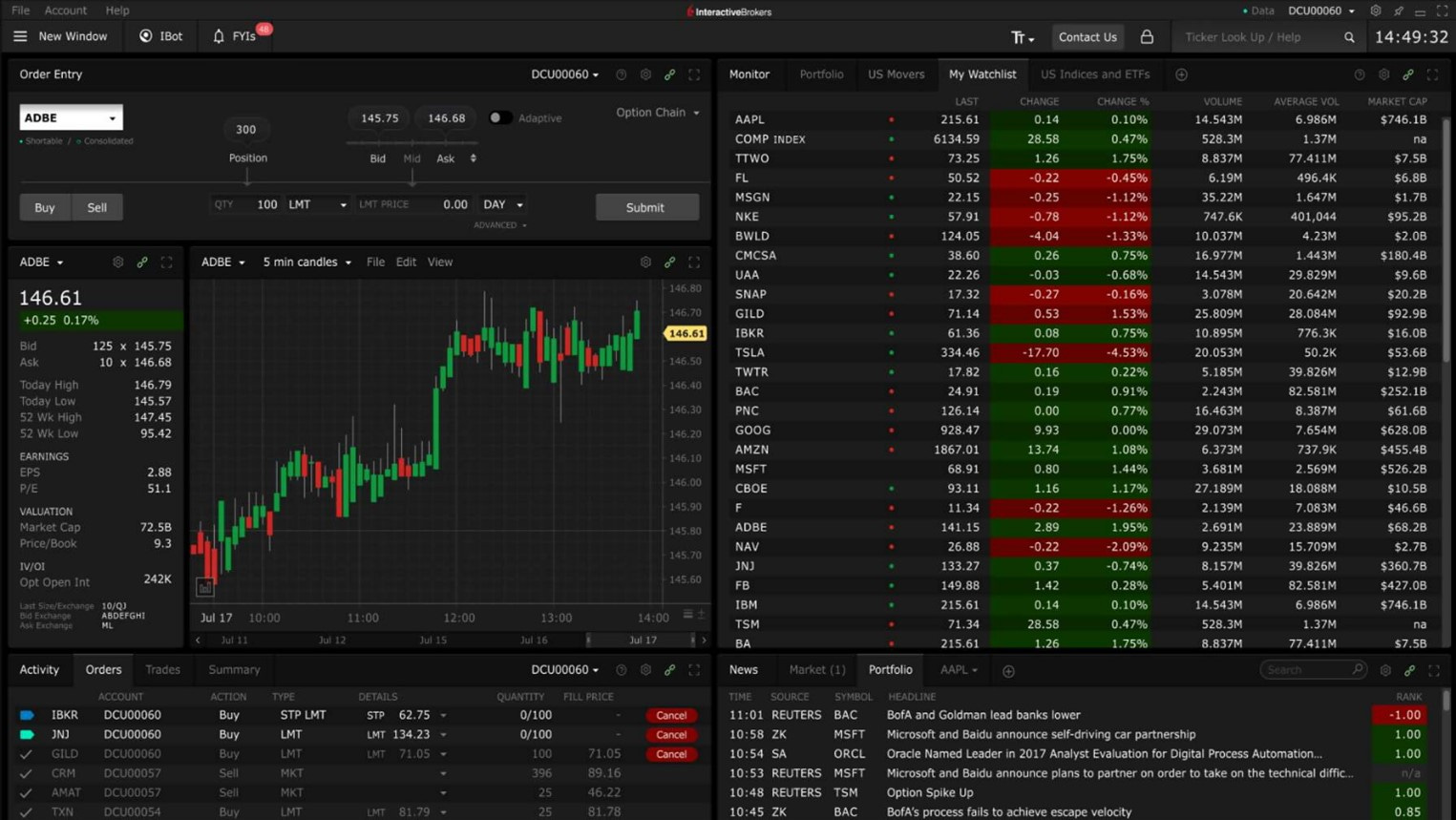

Screenshot of IBKR Trader Workstation.

IBKR Lite was introduced in 2019 in response to the trend of commission-free trading. It operates on a zero-commission basis, earning revenue through payment for order flow (PFOF). Robinhood which offered “commission free” trading was growing fast in 2019 and IBKR felt compelled to respond with IBKR lite. However, there is no free lunch and investors who opt for commission-free trading tend to pay higher prices. Over 90% of IBKR’s clients use IBKR Pro.

Interest Income

IBKR earns interest income on margin lending as they lend money to clients to leverage their portfolios. They earn an interest spread on customer cash balances. This is the difference between the interest they pay on balances and the interest they receive by lending out money in the wholesale markets or to leveraging clients. IBKR also makes interest income on securities lending to investors who have gone short securities and need to borrow securities to settle transactions.

The bulk of interest income comes from margin lending. As interest rates rose sharply in 2022, the spread between borrowing and lending rose and IBKR interest income rose dramatically

Geographical split of Income

Although a high percentage of current income comes from the USA, 80% of new customers coming from outside the US. In the last decade, international income grew at 15.5% CAGR compared 14.9% CAGR for domestic income.

Retail investors (individuals) make up 68% of their customer base but only account 43% of client equity.

Hedge Funds make up 1% of customers but generate 7% of commissions and account for 7% of client equity.

Trading Groups are 2% of customers but generate 16% of commissions.

Institutions and Trading Groups are more profitable than retail investors and IBKR focus on the former makes sense. One important category of client are Introducing Brokers (IB). IBs are brokers who have their own client bases composed of relatively small clients.

A division of HSBC Bank acts an IB and offers IBKR platform to its trading clients.

IBs keep the client relationships but allow their clients to trade on a platform which is labelled or badged as the IB’s but the back-end is 100% IBKR. This arrangement is a win-win for all concerned. The introducing brokers (IB), manage their own marketing and customer service while offering their clients a global service by utilising IBKR's backend for trading and clearing operations. They keep the clients and maintain their business.

The clients get to use a professional grade platform. As far as IBKR is concerned, the IBs are the client. IBKR does not have the burden of maintaining the (often small) client relationships. The IBs pay standard commission rates and pay or receive interest on cash or borrowings before marking them up to their end clients.

IBKR’s Competitive Advantages

Does IBKR have significant competitive advantages? Does it have anything which can be described a Moat?

The industry has gone through a significant consolidation and many small and large players have disappeared. IBKR has survived and prospered and is now one of the largest players. Given these trends, there is not much incentive for new entrants into the industry. Therefore, barriers to entry are high. IBKR has its own niche and does not compete directly with either the large investment banks or the retail-focussed brokers.

Key features of the IBKR business model.

Low Costs

IBKR claims the lowest cost in the industry. IBKR’s DNA is leveraging technology to automate as much as possible, which drives down costs. A large part of the workforce and most of the senior management have a technology and systems background.

“Our core software technology is developed internally, and we do not generally rely on outside vendors for software development or maintenance."

This low-cost technology combined with growing scale means they have highest Gross Margins (90%) and lowest costs in the industry. This enables them to offer the customer, the lowest trading charges, the most competitive interest while continuing to maintain a high operating margin (71%)

In the past, we have referred to a concept called “Scale Economies Shared or SES” which was first articulated by the fund manager Nick Sleep. Sleep discussed it with respect to companies like Amazon and Costco. We discussed SES in detail in our note on Amazon which can be seen here.

SES is where companies use their position of the lowest cost producer to offer the lowest prices and win market share and use the scale to win further market share. In this way, a strong moat is further strengthened over time. IBKR follows the SES strategy.

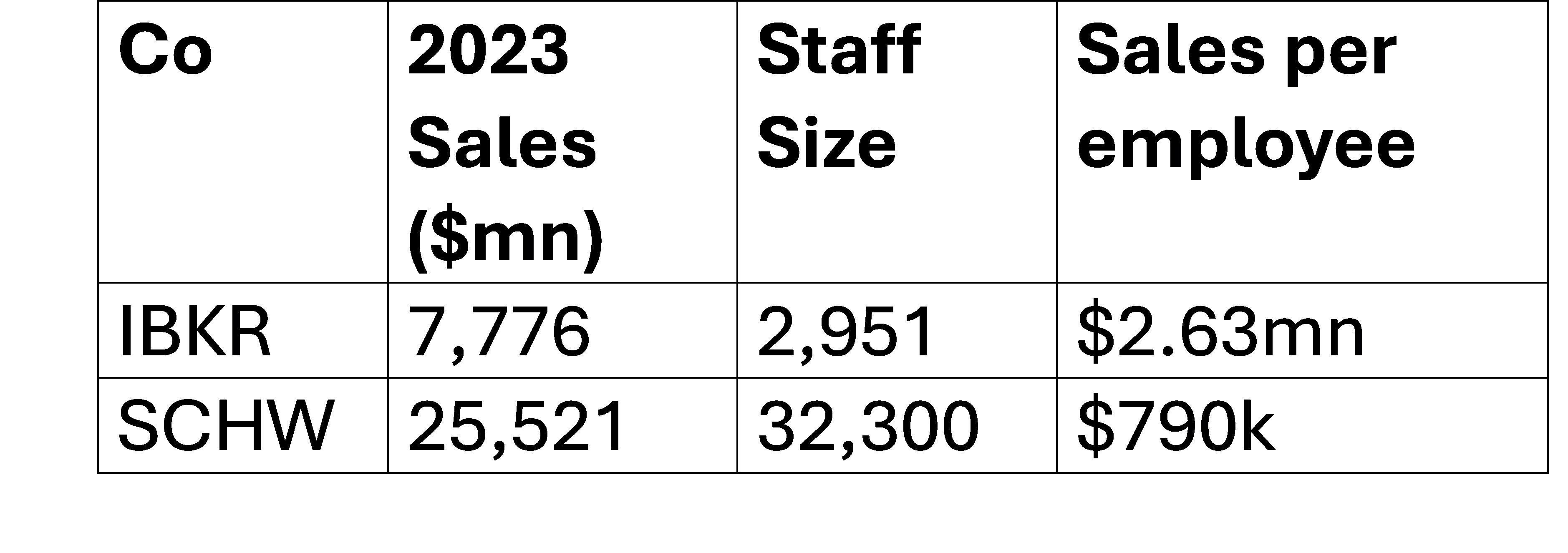

IBKR generates much higher revenue per employee compared with SCHW. This, in part, reflects a different business mix and approach but also reflects the efficiency that accrues to IBKR due their technology platform.

Product offering

For their targeted client base, IBKR offers everything and is a one-stop shop. Customers can trade everything from bonds to futures, foreign exchange, and derivatives with IBKR. IBKR serves customers from over 200 countries and offer trading on more than 150 electronic exchanges. IBKR covers 27 different currencies. This much more than competitors offer.

IBKR also offers some advanced institutional trading tools that other brokers do not and are usually the preserve of large banks and institutional brokers. These include various types of order types, extended trading hours, algorithms and platform APIs. These are irrelevant for retail brokers but appeal to Trading Groups and Funds who are the most profitable customers.

The choice of customers

IBKR focuses on customers who trade the most volumes as well as those who trade the most frequently. It also means not actively chasing the resource-intensive small, and relatively inactive, retail clients. Robinhood has nine times more customers than IBKR but only 25% of client assets. In terms of revenue, Robinhood 2023 revenue number was $1.8bn compared with IBKR’s $7.7bn.

Growth Potential

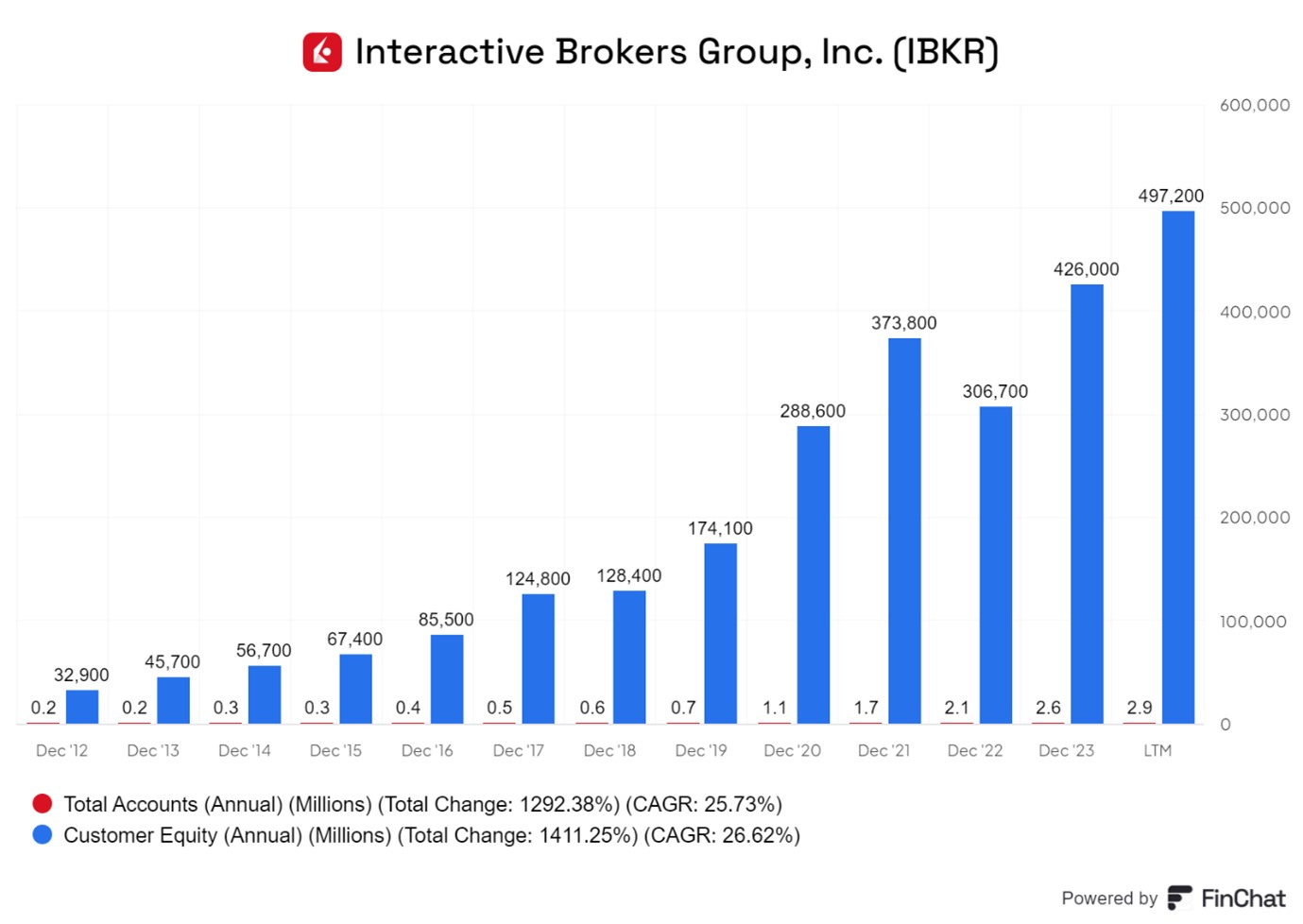

IBKR’s number of accounts has grown by about 25% CAGR in the last ten years. Customer equity has also grown impressively grown in line at about 26.62% CAGR.

What is the likely growth in the future? One of the major trends in investing in the last few years has been the massive growth of passive investing through vehicles such as ETFs. Individual Investors who buy ETFs rather than assembling portfolios on their own, are less likely to need a broker and are unlikely to trade frequently. However the ETFs need to use brokerages to manage their investment activity. Companies like Jane Street have grown rapidly on the back of this ETF trading. This is an important market for IBKR.

Industry data indicates that the brokerage industry has been growing worldwide along with the rise in passive investing. According to Mordor Intelligence, the electronic brokerage market is expected to grow by 6.5% annually until 2030.

In particular, with recent the growth of information systems online directed at DIY investors, many new active investors are emerging, particularly in the emerging economies. IBKR currently has $380bn in AUM, which is less than 1% of retail equity holdings. They have been growing faster than the market for many years and are likely to continue to do so.

During, the pandemic, many investors opened accounts with zero-commission brokers like Robinhood in the USA and Zerodha in India, among others. These brokers rely on other sources of income such as Pay for Flow (PFOF) where they get paid for directing orders to chosen market makers.

The EU plans to ban PFOF starting in 2026, and if the US follows suit, the zero-commission brokers could face significant challenges. The vast majority of IBKR’s business does not rely on PFOF.

As noted above, IBKR generates revenue through interest on margin loans and commissions on trades and are profitable on this basis. This makes them more robust and less vulnerable to regulatory changes regarding PFOF.

Another growth driver for IBKR are Introducing Brokers (IB). About 22% of IBKR’s customer accounts come from IBs. As millions of retail investors sign up with local brokers in emerging countries, some local brokerages will look to become IBs to IBKR to facilitate global trading for their clients.

IBKR has recently signed two new IBS in Hong Kong and China. Just in the last two weeks, there has been a huge surge in Chinese retail investors opening brokerage counts. Analysts estimate that individual investors opened 1.5mn-2mn stock accounts during the national holiday. Individual investors account for around 50% of market cap and 60% of trading volume in China’s A-share market. While there’s a lot of competition for IBKR in North America, globally there’s less competition among brokers. This suggests significant potential for continued international growth.

Inorganic growth

Another potential rout for growth for IBKR is via the acquisition of rival brokers. The CEO was asked about this and his response is given below:

“So, as you know, we have significant cash reserves, significant amounts of capital that we could deploy and would like to deploy. We have been looking for possible acquisition targets. They are all in our industry. They tend to be brokers who are less efficient than we are. We have closely looked at a number of them. We either find the price to be too high for acquisition or find that the acquisition would represent a very significant amount of work in terms of the integration. So far, we have not found any target that we would actively go after. But we hope that that will change in the future.”

IBKR is looking for brokers to acquire but have not found that matches their exacting criteria. The strong selectivity is indicative of prudent capital allocation.

Management

IBKR is led by its founder and largest individual shareholder, Thomas Peterffy. He retired as CEO at the age of 75 but remains the Chairman. It is sometimes argued, companies with owner-operators focus more on long-term value creation compared to those with professional managers. We concur with this statement.

Peterffy founded the company and has actively steered it for decades. He created a long-term conservative culture that we find appealing. IBKR retains most of its earnings and maintains a strong and conservative balance sheet. Over his long career, Thomas Peterffy has experienced many financial crises, his overriding priority is that IBKR should be a safe-haven during market downturns.

During financial crisis, attention is focused on counterparty risk and investors try to switch to the safest institution. This happened after the collapse of Lehman Brothers and the collapse of Silicon Valley Bank.

Balance Sheet strength.

IBKR has $14bn in equity on their balance sheet with no long-term debt. As of December 31, 2023, aggregate excess regulatory capital for all of the operating subsidiaries was $10.2 billion. IBKR’s capital was $10bn more than the minimum required by the regulators.

Other Key Management

CEO: Milan Galik joined in 1990 as a software developer and has been CEO since 2019.

CFO: Paul Brody joined in 1987 and has been CFO since 2003.

CIO: Thomas Frank joined in 1985 and has been CIO since 1999.

The proxy statement notes "Our named executive officers have an average of 38 years tenure with us."

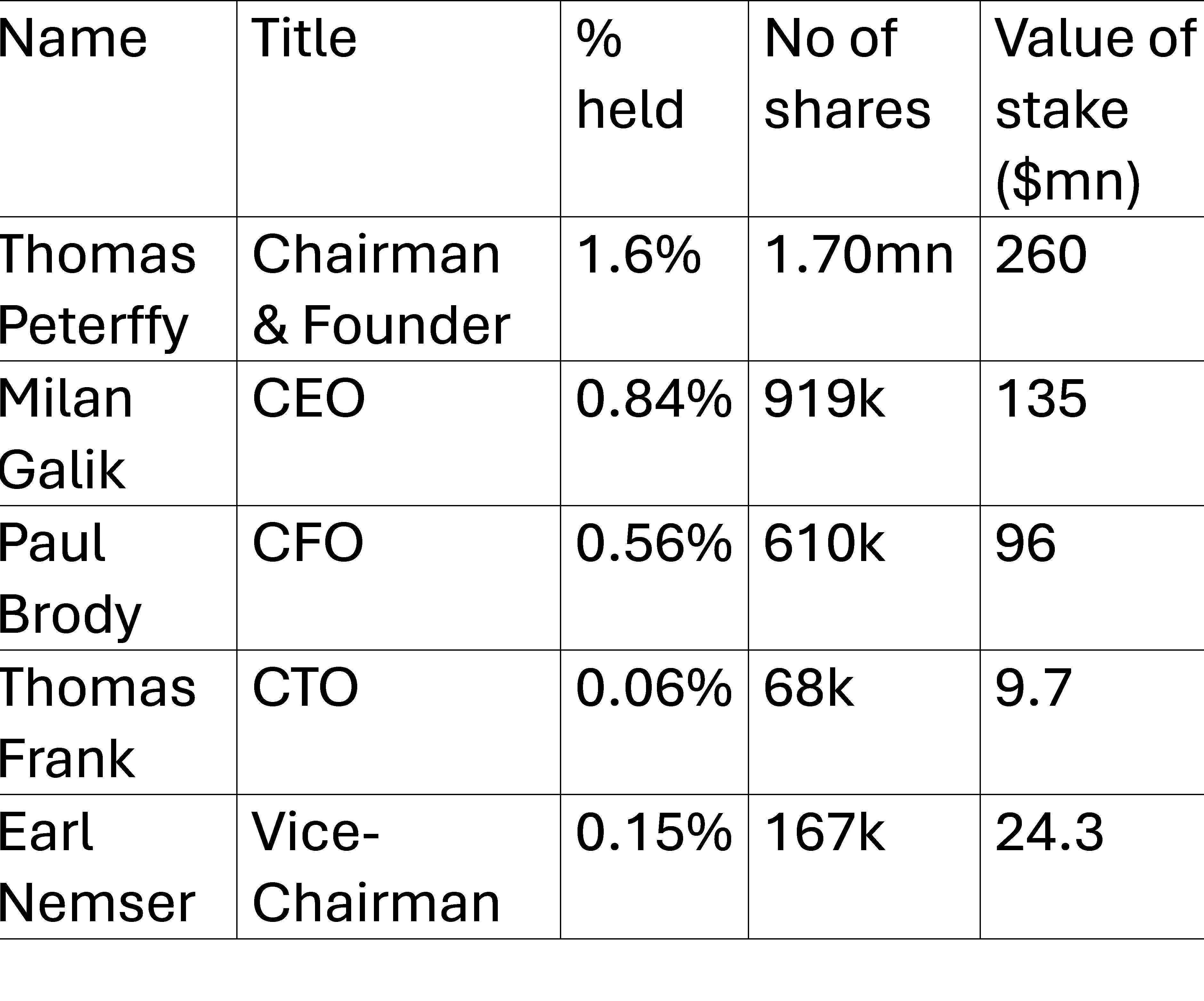

This indicates long-term experience and impressive stability at the top. Peterffy has a 75% interest in the company through the Class B controlling shares. In addition, the senior managers have substantial holdings in the Class A shares as shown in the table below:

Senior management have “skin in the game”.

We can also look at their approach to compensation. According to the proxy statement, "The Compensation Committee has traditionally set Mr. Peterffy’s compensation as salary only, capped at 0.2% of IBG LLC’s net income…We have never issued stock options to our employees,"

The company does not buy back shares even though it has huge cash reserves. In fact, there is a significant increase in the number of share outstanding as shown in the chart below.

In the last ten years the number of share outstanding has doubled, an increase of about 6.8% CAGR.

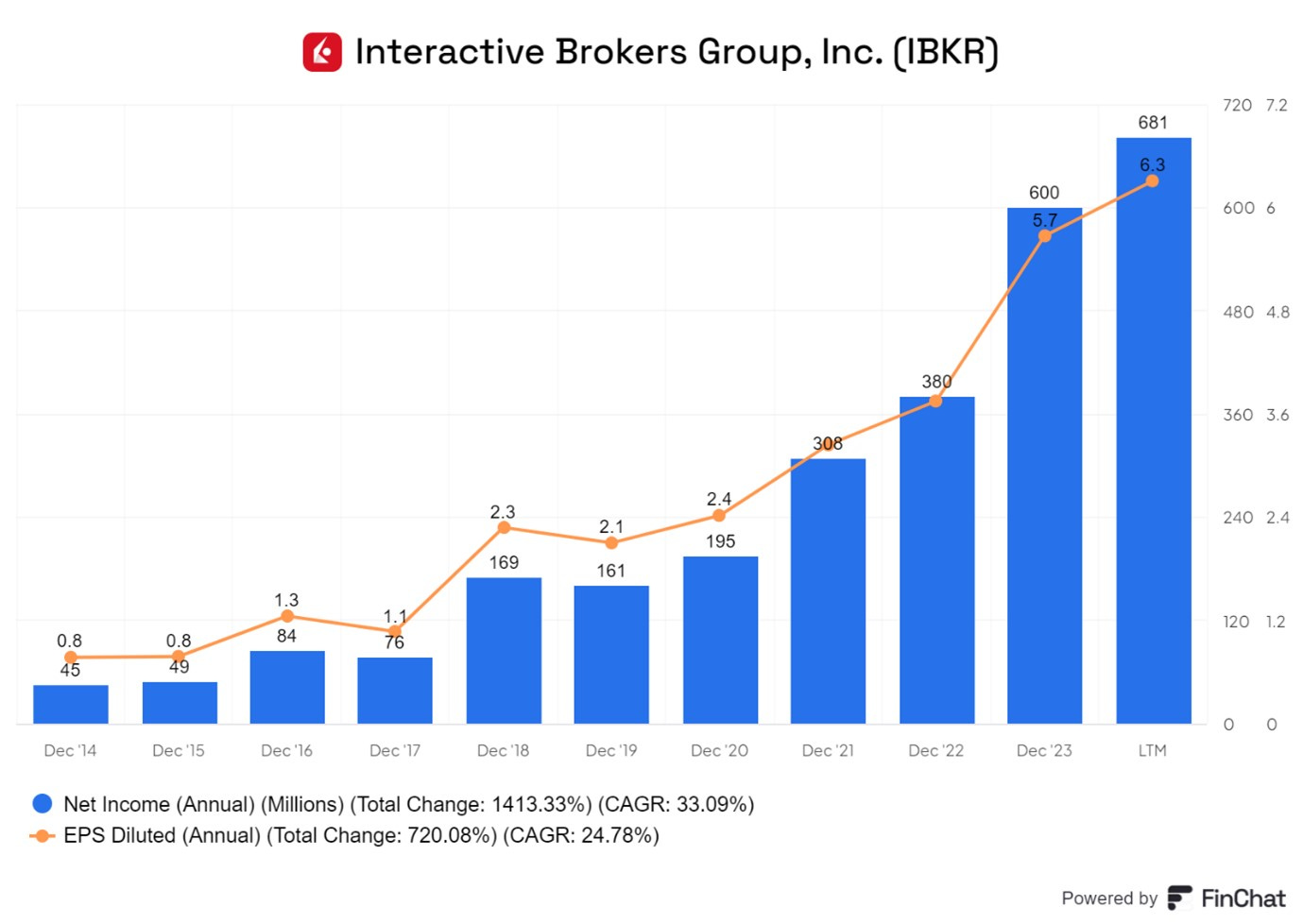

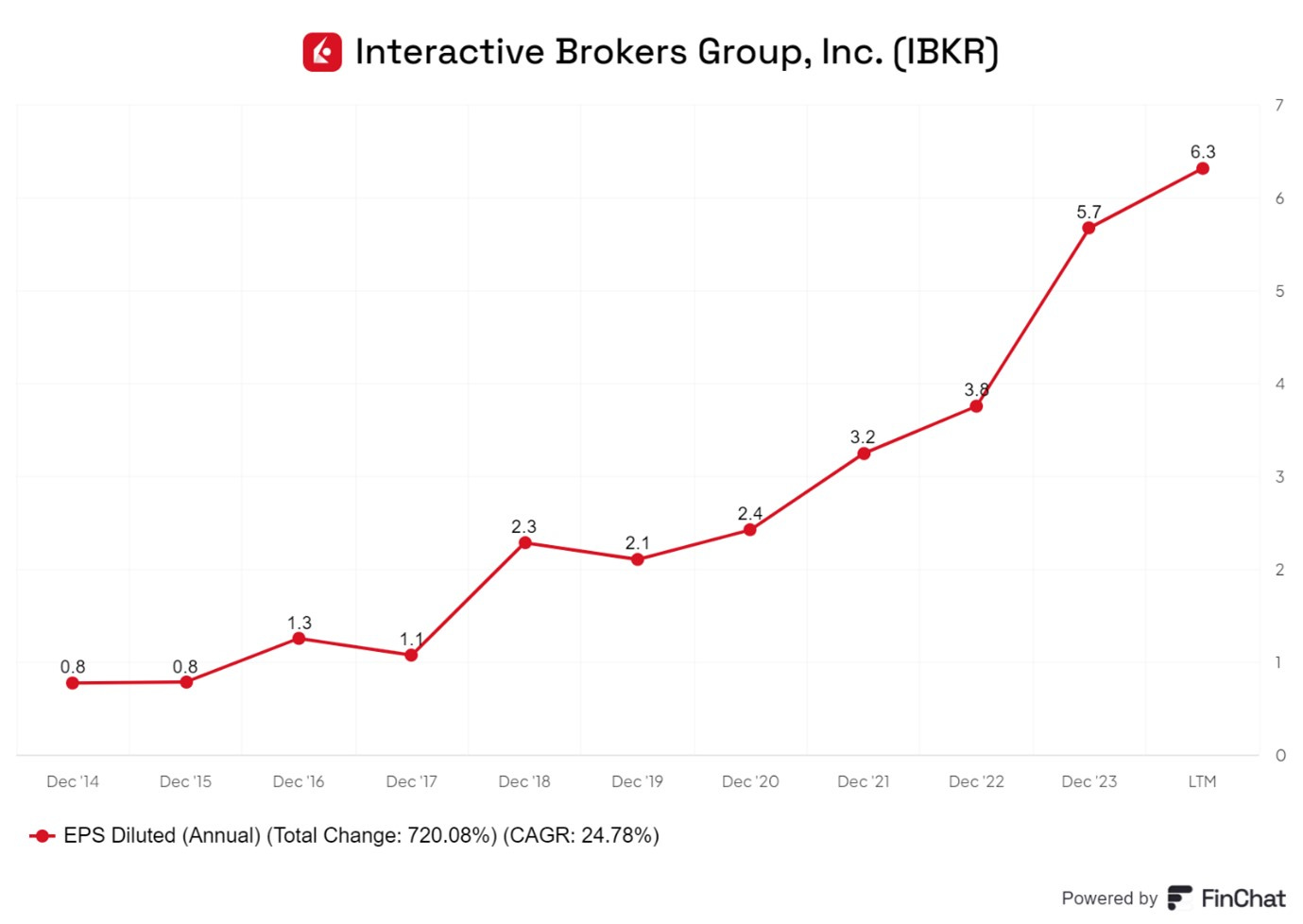

The chart below shows that while Net income has grown by 33.0% CAGR, EPS has only grown by 25% CAGR. The difference is explained by the consistent issuance of new shares.

We need to discuss the reason for the growth in the number of shares outstanding. It relates to the dual structure of ownership of IBKR which was disclosed above and is shown in the diagram below.

Public Shareholders own 25.4% of IBG LLC. IBG Holdings LLC owns 74.6% of the holdings of IBG LLC.

There is exchange agreement which “provides that the Company may facilitate the redemption by IBG Holdings LLC of interests held by its members through the issuance of shares of common stock through a public offering or directly to Holdings in exchange for the interests in IBG LLC being sold by Holdings.”

Therefore, under this agreement IBG Holdings can gradually sells it economic interest in IBG LLC in return for shares in IBKR. This means overtime, the number of shares issued by IBKR will increase. To the extent, the newly acquired shares in IBKR are sold in the market, the public percentage holding in IBKR will increase.

“From 2011 through 2023, the Company issued 40,111,445 shares of common stock (with a fair value of $1.9 billion) to Holdings in exchange for an equivalent number of shares of member interests in IBG LLC.”

It could be argued there is a headwind for shares in that the major shareholder is a potential major seller over the next few years. On the other hand, the exchange agreement can be seen as stable, predictable way by which the founders’ 74 % controlling owners’ stake can be reduced.

What are the risks of investing in IBKR?

The earnings of IBKR depend on the market. If markets fall consistently, trading volumes will fall and this will directly affect IBKR’s revenues. Volatile markets are good for trading volumes especially in options. Therefore, a reduction in volatility can reduce IBKR’s revenues.

IBKR lends money to investors and is at risk if customers default after losing money, during financial crises or big market events. IBKR has excellent technology and processes to monitor markets and collateral values and trigger margin calls. However, these can still fail to prevent losses during periods of higher market volatility.

IBKR lost $104mn when oil prices went negative in 2020 and $120mn during the Swiss franc event in 2015. IBKR has strong risk management and a huge $10bn in excess capital to cushion potential losses. However the risk remains.

IBKR has key man risk as Thomas Peterffy, the founder and largest shareholder, is aged 79. He owns 75% of the company. There is a long-term plan in train to reduce his stake gradually. The senior management has been in place for a long time and has done a good job over decades. The key man risk is more apparent rather than real.

IBKR is exposed to the interest rate cycle. Its Interest income rose strongly after the US Federal Reserve increased interest rates in 2022/23. High-interest rates are currently benefiting IBKR, but the Fed has now started cutting interest rates. Hence, IBKR’s net interest income might fall. However, given the strength of the economy and ongoing inflationary pressures, interest are unlikely to fall much lower. In any case, lower rates might boost stock trading activity and support IBKR’s revenues. This would help to partially offset the fall in interest income.

Summary

IBKR is a pre-eminent technology-driven global brokerage.

It has been an owner operated company for all of its life.

Senior management have a technology background and have all been with the company over three decades.

IBKR has always been conservatively managed with a strong balance sheet.

It has regulatory capital significantly in excess of what is required by the regulators’ frameworks.

IBKR has a long track-record of operating efficiently and have very high gross and Operating Margins.

The company has been a survivor in a consolidating industry.

There is an exchange arrangement which allows for a potential systematic reduction of the 75.4% stake owned by the founder Chairman.

This should result in the share count increasing by 7% year and the IBKR increasing its economic interest in the operating companies by the same proportion.

IBKR is likely to see steady revenue growth in US in the next few years. Overseas revenue is likely to grow faster due in large part to growth in emerging markets.

Valuation

The fully-diluted EPS has grown strongly in the last 10 years. Recent growth has been due to the increase in interest income after the large rise in interest rates in 2022/23.

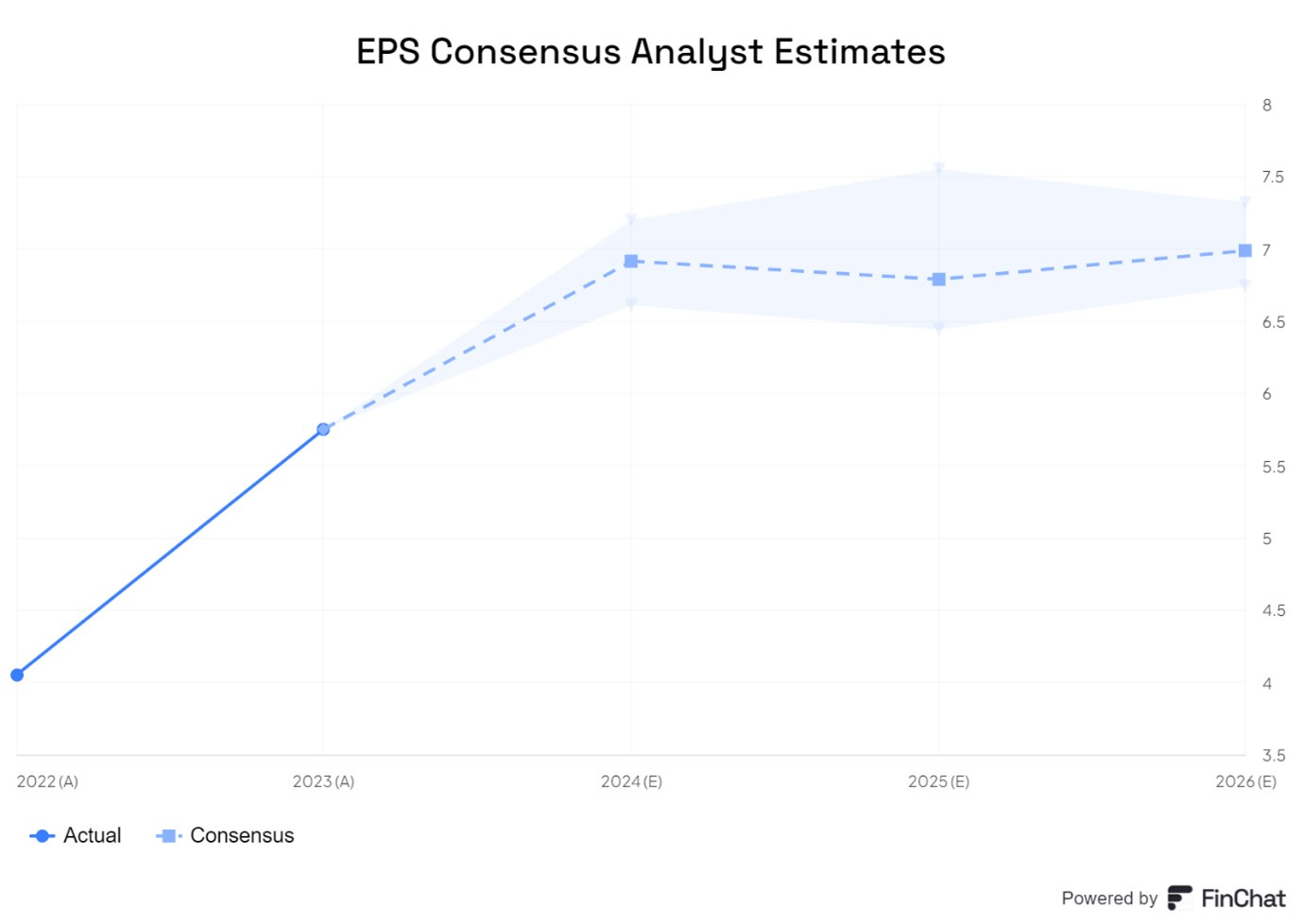

The analysts’ consensus estimates for EPS are $7 per year for the next three years. Analysts expect EPS to plateau in the next three years. This may be a little conservative.

At the current price of $151 per share, IBKR is on a forward P/E of 21.6X. This implies an earnings yield of 4.62%. This feels fairly valued for a cyclical business with a ROE in the mid to high teens. IBKR stock is not a bargain currently.

This a common situation for US stocks currently. This is not surprising, given markets are at an all-time high and may be an indication stocks are overvalued and further advances may be difficult to achieve.

Conclusion

We believe there is small but not insignificant chance that future EPS will be higher than the current analysts’ forecasts.

We will open a 1.0% position in our portfolio for IBKR and look to double it, if the stock price fall to the $120 per share level.

There is another factor to consider:

For the past 15 years, we have seen the longest bull run in stock market history, marked by periodic bumps, including the COVID-19 pandemic, none of which managed to derail its momentum. Tjhis was driven primarily by extraordinary monetary policies driving real interest rates below zero and expanding money supply, but there were other reasons, see: https://rockandturner.substack.com/p/the-4-of-companies-worth-holding

Money was so easy to make during this period, often referred to as the "everything bubble," that nearly everyone fancied themselves a financial expert with the Midas touch. In truth, even a monkey could have made money during this time.

This caused a huge increase in trading activity which was the wave which all of the brokerage businesses have enjoyed riding, including IBKR.

That period is largely behind us now. Valuations look stretched across asset classes which means that stagnation of valuations, or a downside correction, are more likely than a continuation higher. In such circumstances it is likely that people get burned and either lessen their trading activity or else withdraw from active investing and instead put their money to work in managed funds.

Modelling the future on a linear basis by looking at the past for these businesses ignores the pendulum effect that is far more likely.

PS - I use IBKR for most of my trading and I have found them to be best in class. The business model is great, the culture is superb, there is nothing wrong with the business. I am just calling out macro-economic factors that may impact all businesses in this space over the next 5-10 years.