Microsoft

Quarterly Results

On May 1st 2023, I wrote a detailed note after Microsoft published its Q3 quarterly results and this can be read here. Our conclusion at the time was as follows:

“The current valuations (Forward P/E ratio of 29 times and Free Cash Flow Yield of 2.5%) do not indicate that the stock is cheap but given the profitable growth opportunities, we may add a little to our position.” The MSFT stock has appreciated 27% in the three months since then.

The Bloomberg headlines on the most recent results yesterday were as follows:

Microsoft reported revenue for the fourth quarter that beat the average analyst estimates both on the top line and the bottom line.

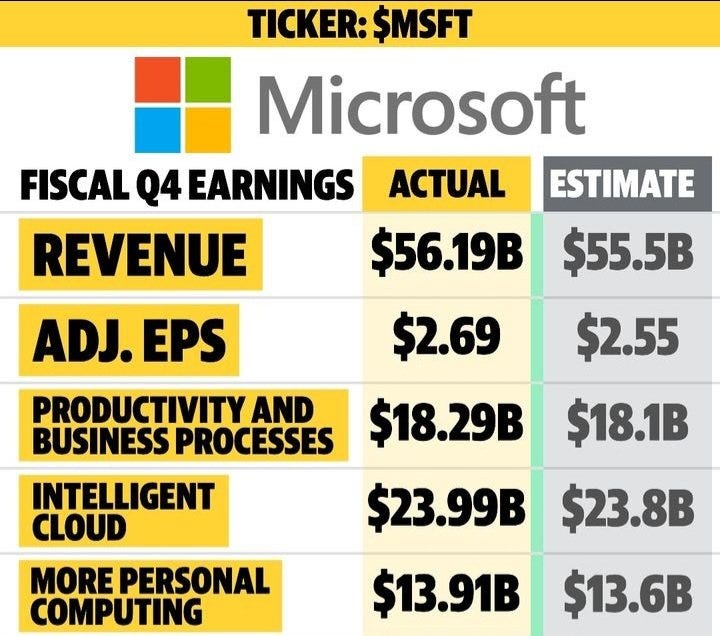

Q4 RESULTS

Revenue $56.19 billion, +8.3% y/y, estimate $55.49 billion (Bloomberg Consensus)

Productivity and Business Processes revenue $18.29 billion, estimate $18.1 billion

Intelligent Cloud revenue $23.99 billion, estimate $23.8 billion

More Personal Computing revenue $13.91 billion, estimate $13.58 billion

Microsoft Cloud revenue $30.3 billion, estimate $30.05 billion

EPS $2.69 vs. $2.23 y/y, estimate $2.56

Operating income $24.25 billion, estimate $23.28 billion

Capital expenditure $8.94 billion, estimate $7.85 billion

Revenue at constant currency +10%, estimate +8.52%

In the last five years, total revenues have risen at a CAGR of 15.5% and eps growth has been 24.3%. In Q4, revenues grew by just 8.3% but net profit and diluted EPS grew 23%.

In terms of the three segments, recent trends were maintained

Intelligent Cloud grew 17% ( Cloud Gross Margin remained at 72%). Azure grew 23%. This Azure growth continues the recent downward trend, as the effect of large numbers due to previous five years strong growth has an impact, but 23% is still an impressive number for what is now a very large business (US$ 67bn top line annual run rate)

Productivity and Business Processes grew 12%

Personal Computing fell by 3% (due to declines in Windows and Devices revenues).

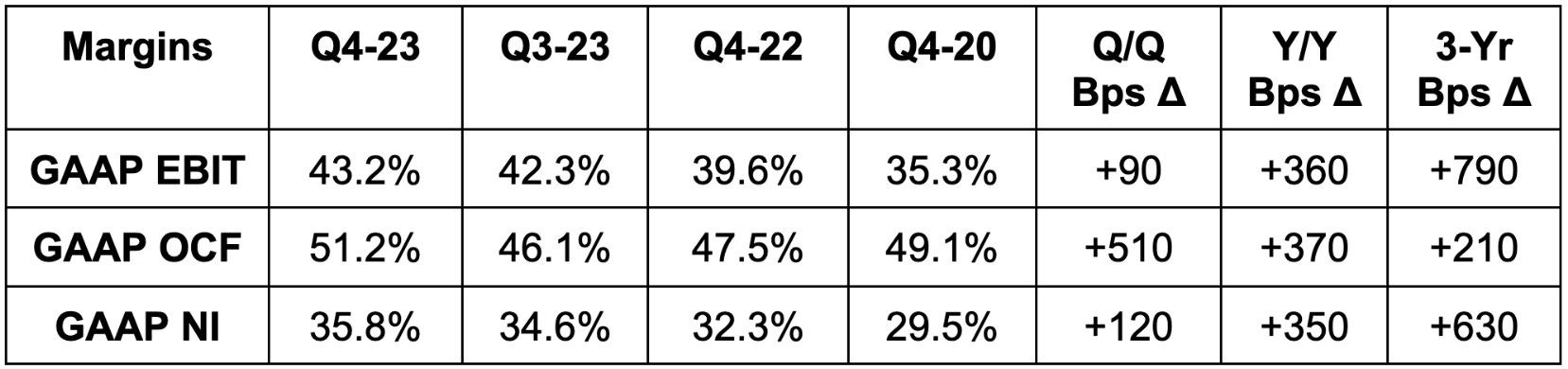

The already impressive margins have been increased a little further:

Source: The Stockmarket Nerd

MSFT guidance was margins will be flat for FY2024 . Market was pricing in a modest expansion in margins .

MSFT reduced deprecation expense by US $3.7 billion in avoided depreciation by extending the useful life of servers and equipment in the last twelve months. This benefit will be lower in 2024

Capital Expenditure will rise in 2024 due to investments in AI infrastructure.

Highlights of the Earnings Conference Call

Azure, the cloud hosting business continued to take market share. The company is still dealing with the workload optimization affecting the Cloud industry. During the pandemic as WFH spread, companies spent heavily on Cloud. In the last three quarters they have been looking to optimise and make the most of the capacity they have already bought rather than spending much more .

MSFT said they expect the optimisation headwind to continue for another six months but Azure demand growth should pick up after that. The Average contract value for Azure set a new record this quarter.

The momentum in Azure is being driven by Azure Arc and AI.

Azure Arc is its multi-cloud management platform to let a customer access Azure services on-premise and on the edge.Azure Arc customers rose 150% Y/Y & 20% Q/Q to reach 18,000.

Azure AI is adding 100 new customers per day during the quarter. Azure Open AI, developed by Open-AI, the not for profit supported by Microsoft, already has 11,000 enterprise users.

The existing business continues to perform strongly. The new momentum is expected from AI and Copilot in particular. Copilot is Microsoft’s new AI powered virtual assistant which will power code writing, email sending and productivity.

365 Copilot has been trialled by 600 early release customers who call it a “game changer” for knowledge workers productivty.

27,000 organizations have signed up to use GitHub Copilot to automate source code processes within the DevSecOps (development-security-operations) world. That represents 100% Q/Q growth. Anecdotal reports suggest huge growth in which developers can produce code.

One noted developer was quited as saying “ with GitHub Copilot X, developers can be made ten times more productive, which means ‘ten days of work, done in one day. Ten hours of work, done in one hour. Ten minutes of work, done with a single prompt command’”. He added “ it will help a new generation of developers learn and build at the speed of thought.”

This week they announced the pricing for 365 Co-pilot. Users will be charge US$ 30 per month on top of current 365 payments,

Summary

This was another predictably strong quarter for Microsoft.

Some products are weak such as Devices or consumer 365 but other businesses particularly Azure continue to grow strongly. The company impressively continues to grind margins higher.

The next two quarters maybe a little subdued as Azure optimisation is a drag and Co-Pilot launch is prepared. However , in six months, Copilot revenues will start to show up in a meaningful way and this is likely to be combined with re-acceleration growth in Azure at that point.

MSFT is about to enter a period where a huge growth in AI revenue will occur as a very large percentage of its installed base of customers start spending more.

Conclusions

Microsoft continues to justify its position as our largest holding. The company will continue to show double digit revenue and profit growth with significant operating leverage. It will continue to generate huge free cash flow some of which will be used to buy back shares. The development of AI has led to new products and services being developed and this will start a new acceleration of revenue within the next six months.

The current forward P/E ratio of 32 does not seem too expensive for a stock with such prospects and a current ROE of 38%. We would look to add to our position.