Yesterday marked both the end of March and of the first quarter of 2025. It has been a remarkable quarter. The summary: US stocks have fallen sharply while non- US stocks, especially in Europe and China, have risen.

The S&P 500 and the Nasdaq Composite endured their biggest falls since 2022. In March, the S&P 500 was down 4.6%, the worst quarter since the third quarter of 2022. Nasdaq lost 10%, the worst quarter since the second quarter of 2022.

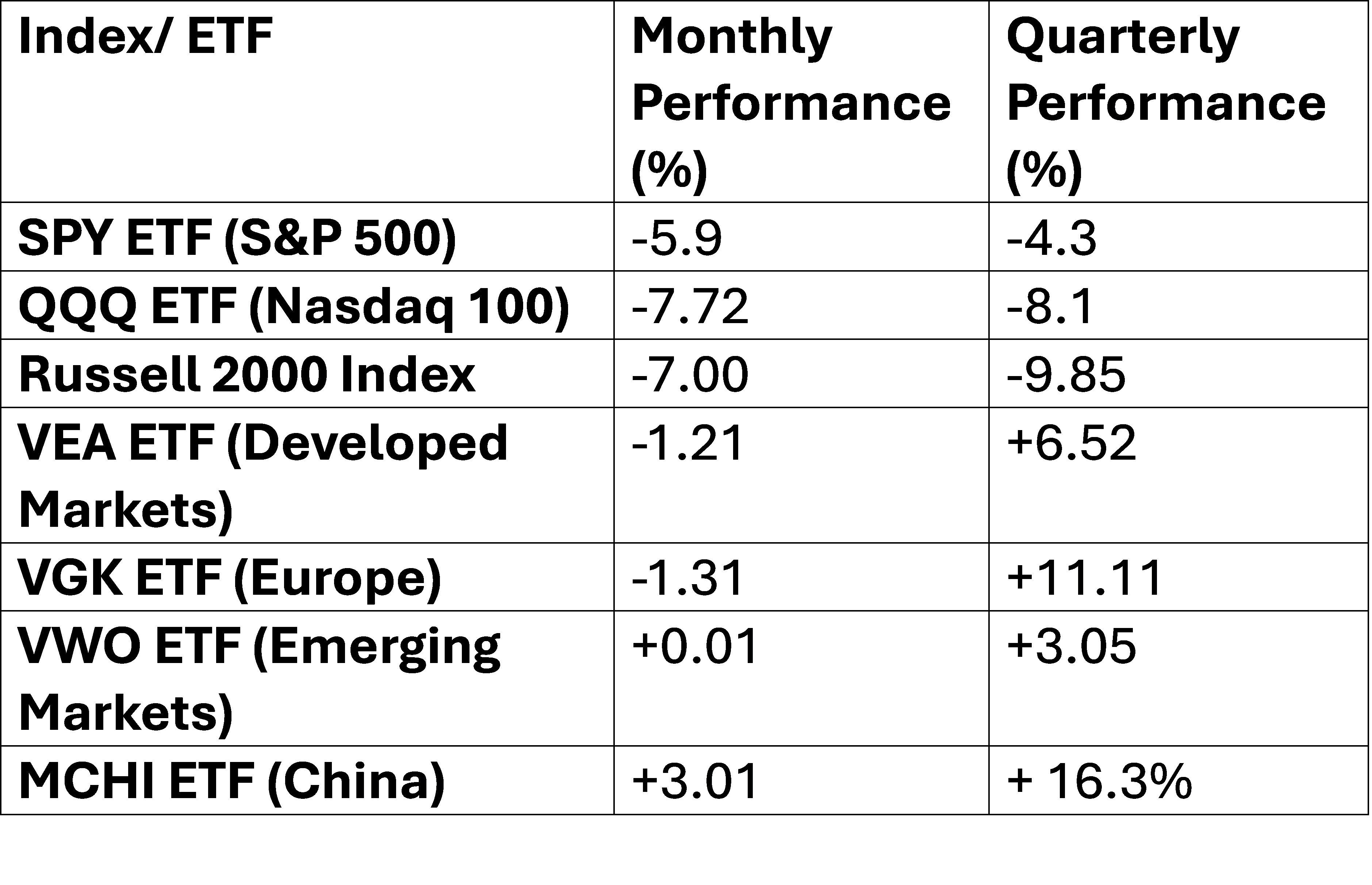

The S&P 500 is on track for its worst quarter compared to the rest of the world since the 1980s, according to Bloomberg. This was because non-US markets advanced in the quarter. The standout in this was Germany's DAX. It was up 11%, the strongest quarter since early 2023.

Monthly and Quarterly Performance of Key Equity Index ETFs

Our portfolio was down 3.6% in GBP terms. The GBP rose by 2.33% over the month against the US$.

In US$ terms, our portfolio fell by 1.3%. The bad news is this was a decline but the good news it outperformed the US Indices.

For Q1 2025, the Portfolio is down 2.0% in GBP terms. Over the quarter, the GBP has appreciated 5.7% against the US Dollar. Therefore, in US dollar terms the portfolio has advanced about 3.7% in 2025.

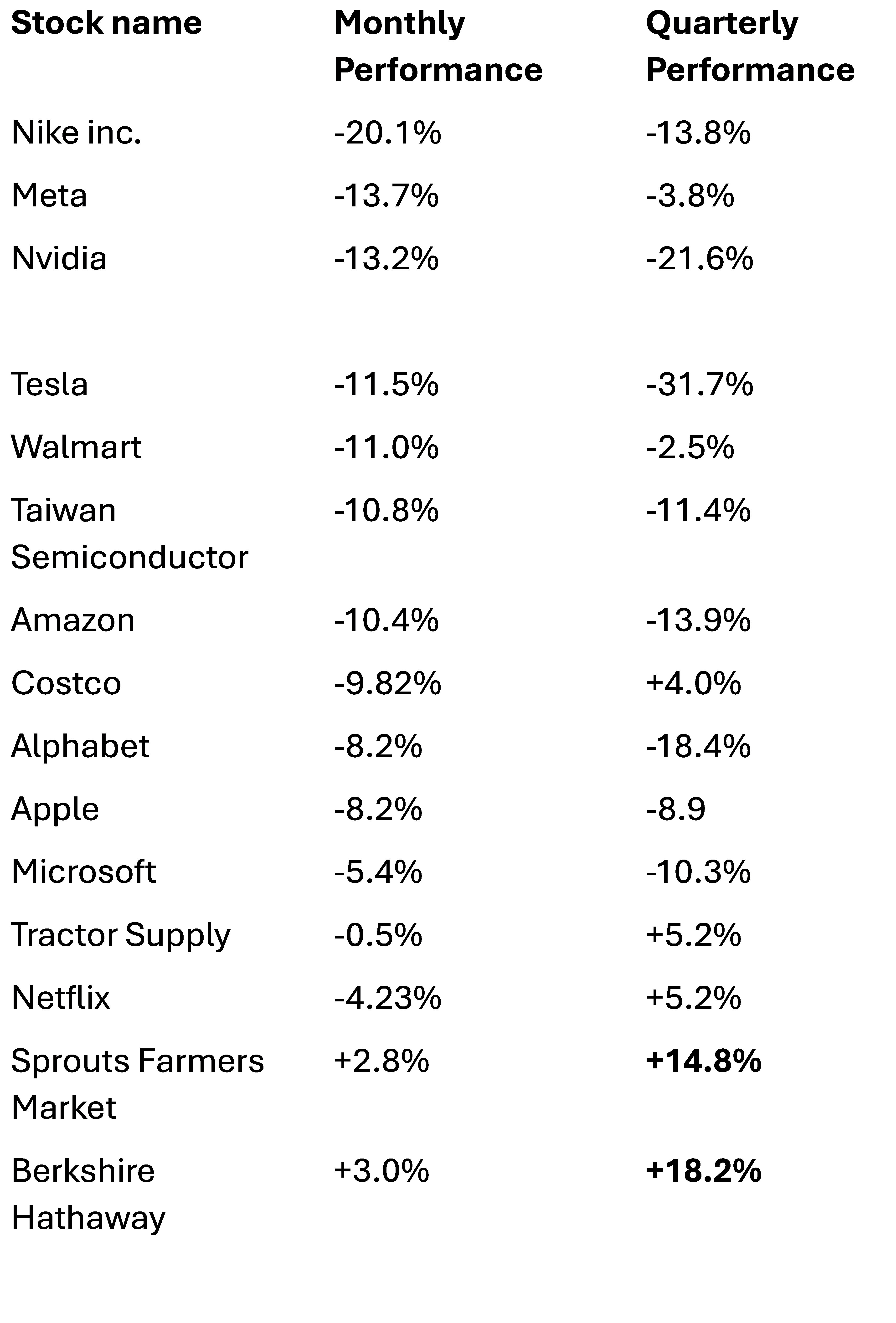

The table below shows the performance of key shares, including many held in our portfolio.

This table makes sobering reading. Favoured stocks are down sharply over the first quarter. Tesla, Nvidia and Alphabet have fallen 32%, 22% and 18.4% respectively. On the other hand, Berkshire Hathaway is up 18.2% in 2025.

Our largest holding, Berkshire Hathaway rose 3.0% in March but many other stocks fell.

In January, we wrote two notes expressing concerns about the euphoric conditions in the market, rising bond yields and the high valuations of stocks. These can be found here and here.

We concluded the second of these notes with the following comments:

“Therefore, we are looking at the valuations of some of the companies in our portfolio. We are reducing our holding in some of them, even though we continue to believe they remain fundamentally good companies and increasing the percentage of our portfolio in cash.”

In mid-January, we increased the cash holding in our portfolio to 30%. This was a big change as we have been 90%-95% invested in equities since 2020. The move to cash hurt us a little as the market rose for another week but protected us in the sharp decline since then.

In our last update we noted “we believe too many US stocks are fully valued or overvalued, so some corrections had to be expected at some point…We are going to work at trying to identify new names in the next few months but given current high valuations, economic and political uncertainty, we are not going to be in a hurry to deploy capital unless some outstanding businesses at compelling valuations are identified.”

Towards the end of the month, we bought (perhaps mistakenly) into some stocks and our cash holding has declined to about 22%.

Looking back how do we explain the performance of Q1 2025. In January stocks were overvalued, and a correction was overdue. The Trump bounce did not sustain, and the economy is showing signs of a slowdown. Sentiment has also been affected by the on-off nature of tariff s and other economic policy announcements by the new administration.

Fast forward to today and markets have corrected significantly. The S&P 500 is 8.4% below its February 19 peak which was also an all-time high. The equivalent decline for the Nasdaq 100 is 13.0%.

Valuations are much more reasonable, but it is hard to find many stocks which are compelling purchases at this level. We are looking for attractive companies which are priced attractively but are not in any hurry to deploy capital.

A six-week correction is nothing when compared with a 2 ½ year rally. So, we are hesitating and waiting.

One reason for this is, we are considering the possibility the rules of the game have completely changed. It may be that what worked in the last 16 years, and perhaps even the last 45 years (buy the dip and hold on!), may no longer work.

It may be that investors are playing checkers while the US government are playing (3-D) chess, a completely different game.

It is possible the US government wants to fundamentally change the structure of the economy and this requires:

a recession in the short to medium term,

higher inflation

a lower dollar and

eventually much lower interest rates and bond yields.

A recession, higher inflation and lower dollar would be a deadly combination for (foreign) investors in stocks.

A lower dollar and higher inflation would be good news for the US government as it has 35 trillion dollar of debt and about 25% of that is held by foreigners.

It would also be good news for holders of gold and perhaps Bitcoin. I note in passing, the Trump family has invested in a Bitcoin business.

Why would a government deliberately want to engineer stagnation and inflation? This is a combination known as stagflation which was last seen in the 1970s and early 1980s.

A slowdown will be useful for reducing imports and the trade deficit.

Inflation and a lower dollar would reduce the real value of the US government’s US$ 35.5trn dollar debt.

Lower bond yields would make refinancing that debt easier.

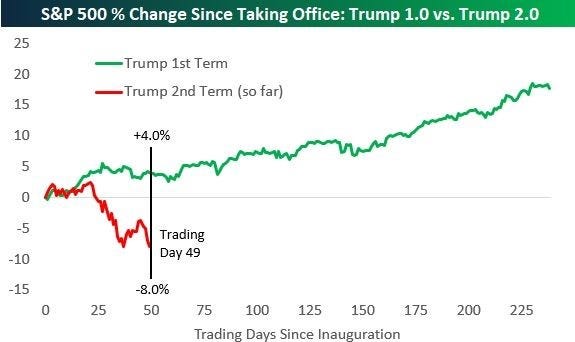

If, and it is a big if, this is the government’s strategy, the chart below makes a lot of sense.

This also means stocks could fall a lot lower.

One final thought.

In Omaha sits a very successful and wise 94-year-old investor. He manages US$1trn dollar of assets including wholly owned subsidiaries which he will never sell. He has US$325bn of assets in Cash and 3-month treasury bills. He is waiting patiently for much lower valuations so he can deploy the money and make one last great killing as he did in 1974 and 2008.

1/04/2025