The Trade Desk Inc (TTD)

A data and technology-driven platform for buyers of advertising

The Trade Desk (TTD)

The Trade Desk, Inc (TTD) is a technology company. It provides advertising purchase and campaign management software aimed at media buyers, planners, and advertising agencies.

As anybody who has watched the TV programme “Mad Men” which was based in 1960s, will know, advertising is a strange industry. Many years ago, the UK boss of Unilever said something like "I know 80% of my advertising budget is wasted. The problem is I do not know which 80%." In other words, he did not have the data to know the return on his investment in advertising/ marketing. He could not answer the question as to which campaigns were winners, and which were losers? People who spent their money on advertising were essentially shooting in the dark and hoping for the best.

Those days have gone-the world is now awash with data of all kinds. Google and Meta have lots of it and make most of their money from advertising. Snapchat, Pinterest, and many others base their business models on advertising revenues. As we noted in our recent note, Amazon makes nearly 10% of its revenue from advertising, which is its fastest growing revenue segment.

The detailed data big tech companies have on you, means advertisers can target particular groups. They can receive detailed data such as how many people clicked on advertisements and whether they bought the product. This data can be used to better target future advertising spend and improve the ROI on it.

More and more advertising is digital -on computer screens, mobile phones and in Apps rather than in Print, TV or roadside hoardings. The rise of big data and digital advertising has completely transformed the advertising industry. Old Media (newspapers and magazines) have lost out while New Media companies such as Google and Meta have become among the largest in the world. The next battle is between Linear TV and Connected TV (CTV). The former is conventional TV while the latter is Streaming TV accessed through internet-connected devices.

The best way to think about advertising is as a financial market (e.g.- exchange -traded derivatives).

First, on one side, there is the buy side. These are companies, brands, and their agents (Advertising Agencies) who are looking to spend money and buy advertising.

Second, on the other side, is the sell-side. They are the owners of advertising who are looking to sell advertising slots or space. They are newspapers, website owners, TV companies, cinema operators, roadside hoarding owners etc.

In between these two entities, are a variety of intermediaries, exchanges and platforms who make a living bringing the buyers and sellers together. The products, to varying degrees, are perishable. Adverts must be sold before the TV programme is broadcast, or before the magazine is printed or before the eyeball stops looking at the website. The diagram below shows a stylised diagram of the advertising market eco-system.

The Advertiser is the buyer and is on the extreme left. The Publisher (say a Magazine or TV company) is the seller and is on the right. They have the attention of the consumer, who the advertiser wants to reach.

In between, there are various platforms and intermediaries which help bring buyers and sellers together quickly and efficiently. There are Ad Networks, Ad Servers, data sellers and managers, DSPs (Demand Side Platforms) and SSPs (Supply Side Platforms). DSPs and SSPs facilitate real- time bidding (RTB).

The Trade Desk (TTD)

TTD provides a self-service platform that enables the buy-side (brands, advertising agencies) to purchase and manage digital advertising campaigns across various advertising formats. TTD only serves one side of the transaction, the buyer. Unlike others, they do not make money from the sellers (media, publishers, websites etc) as well.

The TTD platform enables a media planner or buyer at an advertising agency to:

purchase digital media programmatically on various media exchanges and sell-side platforms.

acquire and use third-party data to optimize and measure digital advertising campaigns.

deploy their client's own first-party data to optimize campaign efficacy.

link digital campaigns to offline sales results or other business objectives.

access other services, such as its data management platforms and publisher management platforms.

use its user interface and application programming interfaces (APIs) to build their own technology on top of the Company's platform.

TTD can be thought of as the DSP in the diagram below:

TTD is a DSP. It integrates 3rd Party data with the Brand’s own data and provides a platform which helps buyers achieve the best results and maximise the ROI on their advertising spend. TTD uses proprietary software, data, and intelligence to do so. TTD’s business model is very different to the way Google operates. Google’s model is shown below:

Google operates across the ecosystem and serves both the buy side and the sell side. They have very large market shares (~90%) at both ends of the spectrum with both Publishers and Advertisers and are dominant DSP and SSP as well. Google and the other large companies like Meta are closed Gardens. They thrive,in part, because they reduce choice. For example, in order to access YouTube’s ad space, one must use Google’s own DSP. Unlike SSPs, Google won’t provide data to help advertisers to value their ad inventory. Therefore, it is difficult to value ad space on YouTube (relatively speaking) compared to ad space somewhere else.

This creates an inherent conflict of interest when an advertiser uses a DSP owned by a major Internet Publisher like Google. Google is incentivized to sell its own inventory over a competitor’s. Any company that competes with Google will be reluctant to share its customer data (and metadata) with them.

These high market shares and inherent conflicts of interest have not escaped the attention of the authorities. The diagram below was produced by the US Department of Justice (DOJ) when they announced a case against Google in January 2023. It is designed to highlight Google’s market power.

The DOJ complaint alleges “that Google monopolizes key digital advertising technologies, collectively referred to as the “ad tech stack,” that website publishers depend on to sell ads and that advertisers rely on to buy ads and reach potential customers. Through this monopolization lawsuit, the Justice Department and state Attorneys General are seeking seek to restore competition in these important markets and obtain equitable and monetary relief on behalf of the American public.” We quote extensively form their press release below.

“As alleged in the complaint, over the past 15 years, Google has engaged in a course of anticompetitive and exclusionary conduct that consisted of neutralizing or eliminating ad tech competitors through acquisitions; wielding its dominance across digital advertising markets to force more publishers and advertisers to use its products; and thwarting the ability to use competing products. In doing so, Google cemented its dominance in tools relied on by website publishers and online advertisers, as well as the digital advertising exchange that runs ad auctions.” “It alleges that Google has used anticompetitive, exclusionary, and unlawful conduct to eliminate or severely diminish any threat to its dominance over digital advertising technologies,” said Attorney General Merrick B. Garland.

“In pursuit of outsized profits, Google has caused great harm to online publishers and advertisers and American consumers. This lawsuit marks an important milestone in the Department’s efforts to hold big technology companies accountable for violations of the antitrust laws.”

“The Department’s landmark action against Google underscores our commitment to fighting the abuse of market power,” said Associate Attorney General Vanita Gupta. “We allege that Google has captured publishers’ revenue for its own profits and punished publishers who sought out alternatives. Those actions have weakened the free and open internet and increased advertising costs for businesses and for the United States government, including for our military.”

“Our complaint sets forth detailed allegations explaining how Google engaged in 15 years of sustained conduct that had — and continues to have — the effect of driving out rivals, diminishing competition, inflating advertising costs, reducing revenues for news publishers and content creators, snuffing out innovation, and harming the exchange of information and ideas in the public sphere.”

“Google now controls the digital tool that nearly every major website publisher uses to sell ads on their websites (publisher ad server); it controls the dominant advertiser tool that helps millions of large and small advertisers buy ad inventory (advertiser ad network); and it controls the largest advertising exchange (ad exchange), a technology that runs real-time auctions to match buyers and sellers of online advertising.

The case is set for trail in September 2023.

Google clearly have huge conflict of interest. Will they really try to find the best advertising slots for the advertise or just sell (stuff) the inventory of advertisement slots they happen to have in stock? The US authorities have already made up their mind. The key question when considering the investment prospects for TTD, is whether it can compete against such powerful players.

How efficient is the market for digital advertising?

Let us go to microeconomics 101 and state the criteria for an efficient market. The textbooks would point to the following:

There are many buyers and sellers. This ensures that there is a lot of competition and that prices are driven by supply and demand.

Information is freely available. This means that all investors have access to the same information, so there is no advantage to any one participant.

Transaction costs are low. This means that it is not expensive to buy and sell assets, so investors are not discouraged from trading.

On this basis, the market for digital advertising is not very efficient.

There are too many intermediaries standing firmly between the buyer and the seller, each of whom take a cut, so transaction costs are high.

Information is not freely available, and the market is opaque. Buyers and sellers do not have enough information about the quality of the product or the prevailing prices.

There are many end buyers and end sellers but there are one or two dominant players in the middle, namely Google who control a very large share of the market.

The market works very well for Google, Facebook, and Amazon as intermediaries and as sellers of advertising slots on their valuable sites. The market works badly for other sellers of advertising (the rest of the internet) and for all the companies/brands who are the buyers of advertising. As noted above, TTD works only with the buyside who are especially disadvantaged in the current system.

The Global Advertising Market

We will now discuss recent trends in the advertising industry before looking at TTD in detail.

In 2022, the global advertising market was worth an estimated US$ 615.2 billion. This number is expected to grow to US$834.9 billion by 2028.

The most authoritative source of data on the global advertising market is the World Advertising Research Center (WARC). It publishes an annual report on the global advertising market, which provides detailed information on spending trends, advertising channels, and advertising formats.

Here are some key findings from WARC's 2022 report:

The global advertising market grew by 10.4% in 2022, reaching an estimated $615.2 billion.

Digital advertising accounted for 53.6% of global advertising spending in 2022, up from 48.6% in 2021.

The top five advertising markets in 2022 were the United States ($223.1 billion), China ($139.6 billion), Japan ($72.8 billion), the United Kingdom ($60.8 billion), and Germany ($58.3 billion).

The global advertising market is expected to continue to grow in the coming years especially outside the USA. The rise of digital advertising is a major driver of this growth. Digital advertising is more targeted and measurable than traditional advertising, which makes it a more attractive option for advertisers (buyers). The chart below shows the relative decline in traditional advertising in the US.

In the US, Digital is on the march and digital advertising is expected to be 68% of the market in 2024. There may be a similar trend globally.

Digital Advertising Growth

Digital advertising is a form of marketing and advertising which uses digital channels such as the Internet, mobile phones, social media, email, and interactive television to deliver promotional marketing messages to consumers. Digital advertising includes email marketing, search engine marketing (SEM), social media marketing, many types of display advertising (including web banner advertising), and mobile advertising.

Digital advertising has grown rapidly in recent years, as more people use the internet and mobile devices. This growth is driven by several factors, including:

The increasing popularity of online media: More people are spending time online, and this is creating a larger audience for digital advertising.

The growing use of mobile devices: Mobile devices are becoming increasingly popular, and this is opening new opportunities for digital advertising.

The effectiveness of digital advertising: Digital advertising can be very effective at reaching target audiences and driving results.

The future of digital advertising is bright. Advertisers will be able to reach even larger audiences with more targeted and effective messages. Most surveys estimate that digital advertising will grow between 11% -15% in the next few years.

Here are some of the trends expected to shape the future of digital advertising:

Programmatic advertising: where software to automates the buying and selling of digital advertising space. Programmatic advertising is becoming increasingly popular, as it allows advertisers to reach their target audiences more effectively and efficiently. We will discuss it in more detail below.

Native advertising: Native advertising is a type of digital advertising that is designed to blend in with the surrounding content. Native advertising is becoming increasingly popular, as it is seen as a more effective and less intrusive form of advertising.

In-app advertising: In-app advertising is a type of digital advertising that is delivered within mobile apps. In-app advertising is becoming increasingly popular, as it allows advertisers to reach their target audiences when they are already engaged with their mobile devices.

Video advertising: Video advertising is becoming increasingly popular, as more and more people are watching videos online. This included advertising on internet-connected TV (CTV) such as Netflix. Video advertising can be very effective at reaching target audiences and driving results.

The Trade Desk (TTD)

As noted above, The Trade Desk provides buyers with a self-serve platform for buying and managing advertising campaigns.

As a contrast to the large internet publishers, who let advertisers purchase ads for their own properties (e.g. Google (Ad Exchange or DSP/SSP) enabling Coca Cola (advertiser) to buy ads on YouTube (publisher) or Amazon (publisher) enabling Coca Cola (advertiser) to buy ads on Amazon website (Publisher) ), TTD offers advertisers the ability to buy ads for the “Rest of the Internet”.

TTD earns revenue by taking a fee based on a percentage (20%) of a client’s total spend on advertising. TTD also generate revenue from providing data and other value-added services.

Key features of the TTD platform are:

• Auto-Optimization. -allow buyers to automate their campaigns and support them with computer generated modelling and decision making. In addition, by giving clients full reporting, budgeting, and bidding transparency, clients can take control of targeting variables when desired, and apply algorithmic automation when appropriate.

• Advanced Reporting and Analytics Tools. A comprehensive view of consumers’ interactions with the ads purchased through the platform with robust reporting of performance insights across multiple variables, such as audience characteristics, ad format, site category, website, device, creative type, and geography. Better reporting results in better learning, often leading to better campaign optimization and outcomes.

• Data Management. The platform enables clients to license a broad selection of data from third-party vendors in a seamless way, allowing them to further optimize their campaigns with the most relevant data.

• Koa Artificial Intelligence. Koa AI helps platform users make data-driven decisions without sacrificing control or transparency. Koa makes recommendations for campaign optimizations based on its analysis of rich data sets. Advertisers can then choose which optimizations make the most sense for their campaigns.

• Media Planner. An omnichannel solution designed for digital media professionals to generate, analyse, and launch data-driven, programmatic media plans. This tool analyses the actions of existing core audiences with the data with the data across the open internet to deliver a fully transparent, performance-focused, and ready-to-activate campaign.

• Private Marketplace Support. For clients who wish to transact directly with individual publishers, TTD also offers some specific services including a user interface for discovering and transacting via a wide variety of private contracts.

The key elements of TTD's technology are:

• Scalable Architecture. The infrastructure is hosted in data centres in eight countries around the world. On average, TTD's real-time bidding technology evaluates more than 790 billion ad opportunities per day, reaching over 819 million devices per day on a global basis. The core bidding architecture is easily adaptable to a variety of inventory formats, allowing the platform to communicate with many different inventory sources. Scale is important in advertising as there are significant economies of scale.

• Predictive Models. They use the massive data captured by the platform to build predictive models around user characteristics, such as demographic, purchase intent or interest data. Data from the platform is continually fed back into these models, which enables them to improve over time as the use of the platform increases.

• Performance Optimization. During campaign execution, the optimization engine continually scores a variety of attributes of each impression, such as website, industry vertical or geography, for their likelihood to achieve campaign performance goals. The bidding engine then alters bids and budgets in real-time to deliver optimal performance. Additionally, the platform enables clients to set multiple, simultaneous optimization goals for their advertising.

• Real-time Analytics. the platform continuously collects data regarding inventory availability. Real-time campaign delivery and spend totals are used to manage campaign budgets and goal caps, as well as campaign reporting. This data is fed back into optimization engine to improve campaign performance, and into machine-learning models for user demographic predictive modelling. They report over 200 performance measures across 300 measurable variables to Clients.

For TTD, the key to growth is to get more advertisers on board. The flywheel or virtuous circle for TTD would be as follows: as more advertisers come in the platform, that will attract more sellers and therefore more inventory. There will be more transactions, better ROI and outcomes and more advertisers will be attracted.

Advertising is a scale business. Since larger DSPs have larger scale than their smaller competitors, they have lower costs per unit (i.e.per ad campaign). As a result, they are likely to provide better bids (and monetize their advertiser’s ads more cheaply) compared to their smaller DSP competition. At the same time, SSPs prefer to send impressions to the DSPs who are more likely to win the auction (rather than working with too many DSPs). If an ad spot isn’t monetized, neither side gets paid (wasted ad spots are like hotel rooms that remain unoccupied overnight). Therefore, SSPs prefer working with larger DSPs because they are more likely to monetize an ad impression. As a result, smaller DSPs have less inventory to choose from over time, which lowers the quality of inventory they can make available to their advertisers.

The advertising industry is being changed by several factors including Programmatic Advertising, Connected TV (CTV), Retail Market Networks (RMN), Privacy-concern driven actions against Cookies.

Programmatic Advertising

Definition: Programmatic advertising is a system that automates the processes and transactions involved with purchasing and dynamically placing ads on websites or apps. It makes it possible to purchase and place ads, including targeted advertising content, in less than a second. The speed with which this happens is mind boggling and it means that the whole process is automatic, there can be no human intervention as that would be too slow.

How does this lightning-fast process work? I believe it is as follows though I am not an expert and may have misunderstood it. When you click on to a website which has an advertisement slot, your profile (age, gender, location, interest etc), based on cookies and browsing history, triggers an auction and various advertisers through the SSPs bid on it (based on your data the system has). The winning advertisements is on the website in a second. The advertiser will pay, the DSPs and Ad exchanges get their cut and Publisher receives a net amount for hosting the advertisement.

If you click on the advertisement, that generates additional data points, and more data points might be generated if you go ahead and purchase. A simple example: during the pandemic I wanted to buy a car and watched lot of car reviews on YouTube. After that every website I visited and ever programme, I watched on More 4 (a streamed TV channel in the UK) seemed to be full of Car advertisements.

Before programmatic advertising, it was difficult for advertisers to access Ad inventory. This meant that 60% of publisher ad space went unsold. Automation helped to solve the problem by making it much easier to understand and buy ad inventory.

For advertisers, the benefits of programmatic advertising include:

Ability to scale. Programmatic advertising allows advertisers to reach a large audience by purchasing ad space from any ad inventory available.

Real-time flexibility. Advertisers can make real-time adjustments to ads based on their impressions, and they can take advantage of a broad range of targeting criteria.

Targeting capabilities. With programmatic targeting, an advertiser's budget can be put to better use and spent more efficiently.

Efficiency. The process is more streamlined, and more relevant ads are served through targeting. Access to a large pool of publishers means advertisers can get a better ROI, while publishers can maximize their revenue too.

The cost of programmatic advertising can vary because it is priced using CPM. This means cost per 1,000 ad impressions.

Definition: In online advertising, an impression is counted each time an ad is displayed on a user's screen. Whether the ad is clicked on or not is irrelevant. Impressions are a common metric used to measure the reach of an online advertising campaign.

On average, programmatic CPMs tend to be a cheaper option than social media advertising methods and significantly better value than traditional offline approaches.

With the right tools, programmatic advertising protects publishers and can keep their readers in mind by hosting ads that are much more relevant to them.

For publishers, the benefits of programmatic advertising include:

Simplicity. Programmatic advertising makes it so much simpler to sell advertising space. Publishers can optimize their ad sales with automation tools that reduce the time required to find advertisers.

Communication. Publishers can communicate and collaborate with advertisers with ease, ensuring both the publisher and the advertiser benefit.

Relevancy. When visitors come to a publisher's site, they will be served with ads that are relevant to them because they are part of the target audience of the advertiser. Programmatic advertising enables advertisers to access a range of publishers, removing the need for phone calls, emails, or other slow forms of negotiation.

Efficiency. Programmatic advertising can lower costs and raise margins for publishers, helping them to earn more from their available ad space especially as the unsold inventory problem is much reduced.

While plain digital advertising hopes to have a wide reach and find the correct audience, programmatic advertising uses precise targeting tactics to segment the audience with real data. Programmatic advertising combines the best elements of tech advancements, human knowledge, and expertise to make it easier to buy, place, and optimize ads.

As AI continues to develop, it will be able to combine the mapping of ad viewing metrics with user data so that ads can be placed more accurately, resulting in lower costs.

Connected TV (CTV)

TV advertising is the new battleground in advertising and the big opportunity for TTD. CTV is non-linear TV. Linear TV is traditional TV when the broadcaster forces you to watch when they want you to watch. There is a good chance you will sit passively sit though the advertisements as well. CTV is where you control where you watch - thanks to Netflix, ROKU, Disney, and other streaming service through an internet connected device. Cord cutting and Netflix/ Amazon Prime/Disney Plus have been killing linear TV.

The industry is excited about digital video ads run against premium content on Internet-connected TVs as these can be targeted in a way which was not possible in linear TV. Linear TV (broadcast + cable) still dominates total consumption hours despite steady declines in cable penetration in recent years. Investors are anticipating a growth in CTV advertising reminiscent of the S-curve of growth exhibited by mobile advertising from 2012-2016.

Consider people watching a programme on linear terrestrial TV. Everybody sees the same advertisement. If the same programme is shown on a Connected (Streaming) TV – in theory, all advertisements could different as they could be targeted to the individual viewer.

Streaming has been gaining ground. In May 2022, streaming accounted for 32% of total TV viewing, up from 26% in May 2021. It is forecast to account for more than 50% of total TV viewing in the US by 2025. In this context, Netflix decision to have a cheaper ad-supported offering is significant. The value of total annual spending on advertising on Linear TV in the USA is estimated to be around US $66 billion. If only 10% of that would move to CTV, that would be a US$ 12bn opportunity for TTD. Targeted programmatic advertising account for 75% of all advertising on CTV in the US (See below) .

CTV will be transformational in showcasing the power of the open internet to advertisers. There are several players such as Netflix, Amazon Prime, Paramount, Disney, HBO, WarnerBros Discovery etc. There is no one dominant player like Google is in digital advertising. There is little chance a walled -garden approach can prevail here. As CTV users have to their e-mail address to access, it is a 100% authenticated audience and so attractive to advertisers. It is a more efficient market than digital advertising and TTD has already grabbed significant market share.

Retail Media Networks (RMN)

In 2012, Amazon launched its retail media network (RMN) and successfully started selling advertisements space on its websites. Other retailers have followed suit, from Walmart and Target to specialty retailers such as Sephora (Beauty) and even app-based delivery services like Instacart. For a retailer running their core business on a 2% to 4% percent margin, the prospect of setting up a RMN at 40% net margin is very attractive. RMNs began in the U.S. and China, European and Latin American retailers are currently seeing consistent growth, with Tesco in the UK and FairPrice in Singapore prominent.

RMN is a vehicle for marketing to customers at the point of purchase at the point of choice. In the old days it consisted of activities such as product sampling or in-store displays where a supplier pays the retailer to have a more prominent location in the store. RMN is an advertising platform maintained by a single retail entity and established across its owned channels and digital properties, both online and in-store.

Each RMN has

a self-serve advertising portal that allows brand advertisers to place their media buys,

a range of retail media advertising types and formats to choose from

a method for campaign managers to upload and store advertisements.

a method to manage product details like description etc and

a campaign reporting module to monitor performance of active media promotions.

Retailers often partner with one or more ad tech service providers for development and advertising needs to accelerate their progress and better meet the demands of brands.

RMNs can also incorporate vast amounts of first-party customer data, sourced from a retailer’s brick-and-mortar and digital ecosystems e.g., customer cards. They can do search, pay-per-click, display and more ad tricks, just like the big media players – with the advantage of not relying on cookies: this is important given heightened privacy concerns.

RMNs are also attractive to brands. Brands are looking to RMNs and retailer data to make up for the data lost due to the ban on cookies and engage with customers at the “digital shelf moment”. This will help improve ROI analysis on advertising investments. RMNs can be large. Best Buy claims to have three billion customer interactions a year and can generate a deep level of insight into those transactions, not just from the point of view of the purchase but also from the research people do before they buy, the installation or the after-sales service. Walmart has data on the 240mn customers who visit weekly either in-store or online.

RMNs face some challenges but will continue to grow in volume and bring welcome relief to retailer profitability if brands perceive and quantify the value that comes from the retailer’s intelligent use of first one customer data – and customer data from loyalty programmes –in an ecosystem where digital and physical interactions are increasingly interconnected and customer data protection regulation is advancing across most geographies. Retailers realize they cannot maximize the value of their shopper data by building walls around it. They stand to drive much greater growth by opening their data up to advertisers in a privacy safe way.

Brands want to access the retailers’ customers. Coke is activating campaigns across more than 25 retail media networks, including Kroger, Target, Walmart, Amazon, DoorDash, and Instacart. Since Coke started building out its retail media strategy a few years ago, it has seen a major uptick in return on ad spend and incremental reach, as well as its ability to determine overlapping audiences across more than 130 million households in the United States. This approach has helped the company better pinpoint audiences in targeted channels like programmatic display, Connected TV, and social media. A Coke spokesman said "Retail media networks know so intimately the behaviours of these consumers that their predictive models, their data, really help us identify what are those right touch points when we are able to say, this is a great time to remind you that there's a Coca-Cola product for you." In RMNs, advertisers win when they can apply data to their campaigns and because of this, like CTV, a walled garden will not be the right strategy.

TTD claim they provide access on their platform to about 80% of the leading retailers in the United States and they are now rapidly growing their international footprint with partnerships with Tesco in UK and FairPrice, the largest grocery chain in Singapore. More recently, they have signed up Macy’s which is a diversification away from the general grocers like Walmart and Target to higher-end merchandise.

UID2

A cookie is a file a website saves on a computer or mobile device when one visits the site. It enables the website to remember your actions and preferences (such as login, language, font size and other display preferences) so you don’t have to keep re-entering them whenever you come back to the site or browse from one page to another.

There are two main types of cookies:

First-party cookies: These cookies are created by the website you are visiting. They are used to store information about your preferences and browsing activity just on that website.

Third-party cookies: These cookies are created by a third-party website, such as an advertising network. They are used to track your browsing activity across multiple websites.

Websites can make money from cookies in a few ways:

Retargeted advertising: This is when a website shows you ads for products or services that you have previously viewed on other websites. This is done by tracking with third-party cookies.

Behavioural advertising: This is when a website shows you ads that are based on your interests and demographics. This is also done by tracking your browsing activity with third-party cookies.

Conversion tracking: This is when a website tracks how many people click on its ads and then go on to make a purchase. This information can be used to improve the effectiveness of the website's advertising campaigns.

Google announced in January 2020 that it would drop third-party cookies from Chrome by the end of 2022. The company cited privacy concerns as third-party cookies are used by advertisers to track users across multiple websites. In July 2022, Google said it would delay the removal of third-party cookies until 2024 as it has not come up with an alternative. Cookies present valid privacy concerns, but many websites earn the bulk of their revenue from the ad targeting powered by cookies. When Chrome drops third-party cookies, advertisers will lose the precise targeting that makes web advertising such a valuable channel.

Unified ID 2.0 (UID2)

UID2 is an initiative sponsored by TTD to address the concerns about privacy and cookies. Many publishers, DSPs, SSPs and Data Providers and Managers have joined the initiative. It is a privacy-focused, unencrypted alphanumeric identifier created from a user's email address or phone number. It is independent of third-party cookies and supports advertisers' need for running personalized ads that are targeted to specific consumers without compromising their privacy.

UID2 can provide a privacy-compliant identifier to power the advanced data targeting coveted by advertisers. Unlike cookies, Unified ID 2.0 will require users to directly provide consent to a publisher by providing their email address before a publisher can create a UID2 identifier. Publishers will need to explain to the user the value-exchange of the open Internet and why creating a universal identifier for the ad tech ecosystem is crucial in providing the free content users want.

UID2 extends and upgrades the targeting abilities of TTD by creating an always-on identifier to better understand who is behind the impression the advertiser is buying. TTD expects 75% of its gross spend to be UID2-tagged by Q2 2023 vs. 15% as of the end of 2021. UID2 adoption will allow TTD to “effectively solve the identity-matching challenge for the entire open internet beyond anything cookies ever accomplished with more privacy and consumer control.”

UID2 has also already won acceptance from key data infrastructure players like Amazon AWS, Snowflake, Salesforce, and Adobe. These integrations paired with TTD’s aggregated data indicate exactly what individual customers want to see.

UID2 is delivering 12X more relevant audience reach for a Disney+ advertiser (Unilever) using it.

Paramount Advertising (Paramount, CBS etc.) integrated with UID2 during the last quarter.

UID2 doesn’t directly drive revenue. It simply enhances the value of each Ad impression value and uncovers more impression buying opportunities. That, in turn, eventually drives incremental TTD revenue.

OpenPath:

OpenPath allows opted-in publishers to connect directly to TTD’s demand. TTD does not work for the sell side. OpenPath allows publishers who want to perform their own supply side functions like yield management to do so. OpenPath cuts out a lot of the middlemen and unnecessary fees from the supply chain by enabling direct demand and supply matching. This ability to “clean up the supply chain” reduces the number of intermediaries and improves transaction economics.

The largest players in digital advertising are shown below wither 2022 market share.

Company Market Share

Google 28.6%

Facebook 23.7%

Amazon 7.1%

The top three players are walled gardens. Is there room for a company like TTD which is not a publisher, does not have any inventory of its own but which can buy advertisements in “the rest of the internet”? This is the key question for any potential investors in TTD must ask. The quick answer would be that the three leading players are too big and dominant for a small company to survive let alone prosper.

TTD has emerged as the largest independent DSP, as smaller players have exited the market. If there is room for an independent player, TTD is a good candidate as it is the largest player and Brands would not want multiple independent DSPs.

The rise of Programmatic Advertising, CTV, RMNs and UID2 have created a great opening for TTD. Advertisers have realized that buying ads online in a programmatic, data-driven way improves their ROI. As a result, the programmatic advertising is currently growing at ~20% a year and digital advertising is growing at 11% to 14%. TTD has been growing at 40% CAGR for the last five years. This data suggests there is room for an independent player like TTD.

Programmatic ad buying is a win-win model, as it improves transparency, price discovery, and precision, all at scale. It creates transparency for advertisers because they can now know where their ads are being placed and for publishers because they can know who is buying their inventory. It creates efficient pricing, for ad impressions, by matching the supply and demand between ad buyers and sellers. Lastly, data and AI enable precise targeting and attribution at scale, something both advertisers and publishers value.

According to Google, there are over 1.1bn websites on the Internet today. There is a lot of interest on the part of advertisers outside the walled gardens of Facebook and Google especially outside North America. There is no shortage ad inventory outside the walled gardens and Advertisers want easy access to this.

Connected TV advertising will be a big growth story as both Disney Plus and Netflix have realised. There are a number of other players, and a walled garden will not work. Programmatic advertising works very well in CTV and this plays to TTD’s strengths. CTV accounted for 37% of The Trade Desk's revenue in 2022. This is up from 29% in 2021 and 19% in 2020.

Amazon’s success shows the importance of RMNs. Other retailers have grown their own RMNs both in the USA and abroad. TTD has access to 80% of the RMN inventory and this shows their offering is especially competitive in this space. TTD has partnerships here with Walmart, Target, Home Depot, Kroger, Meijer and many more. Recently, it has added Tesco & FairPrice (two large international grocers) to the large roster.

Google was planning to end 3rd party cookies on its Chrome Browser in 2022. However, this has been delayed to 2024 as Google has not come up with a solution which does not harm it own business model. In the meantime, TTD has come up with UID2 which has been widely accepted in the industry. UID2 addresses privacy concerns while allowing targeted advertising. UID2 is already achieving good results for advertisers.

TTD has scale. Most large advertisers in the world feed 1st party data to its algorithms to combine with ample available 3rd party data. This means it can infuse more relevant insight into each impression purchasing decision and can segment individuals in a more precise manner. This results in much higher ROI.

TTD cuts booking costs in half, and routinely delivers triple digit ROI. As a result of more successful, higher return advertising campaigns, publishers can also enjoy higher impression bid prices so they can lower ad frequency, improve the customer experience and lower churn.

Above all advertisers need an able partner who can be trusted. TTD is in a good position to be a trusted partners as they don’t own any inventory themselves. They are simply a middleman helping advertisers most cost effectively reach the “Rest of the Internet’s” ad space. TTD is the largest independent DSP. Advertising is a scale business. TTD is benefiting from the economies of scale and is winning market share.

TTD’s percentage take is 20%. This looks high but it has been at this level for nearly a decade. Buyers see value in the offering. The world’s largest advertisers seem to be happy as it has a retention rate at 95%.

Advertising is a cyclical business. TTD is not fully immune to macro headwinds but given tailwinds it is more insulated than most.

Summary Financial performance of TTD.

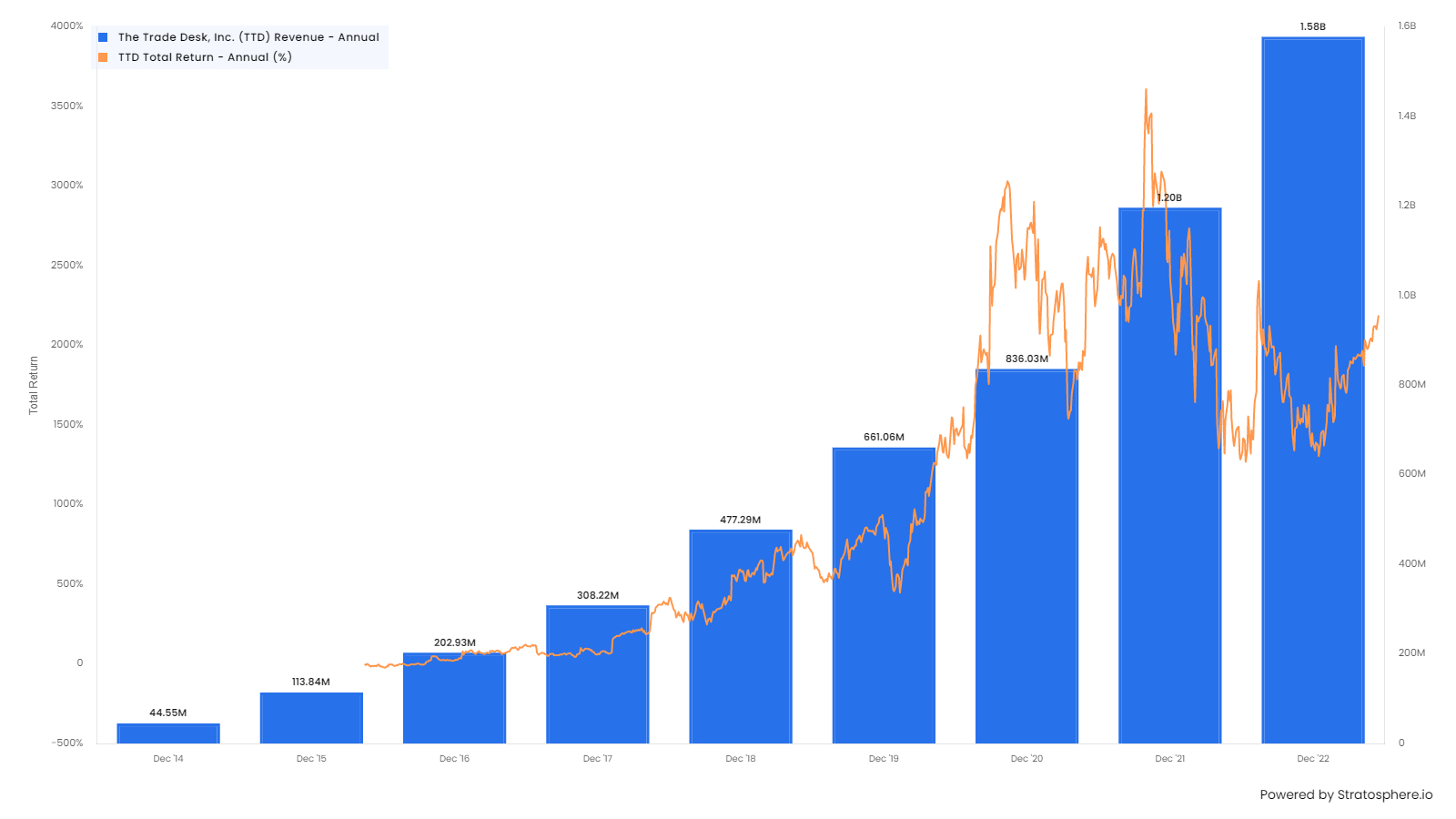

Chart 1: TTD Revenue and Stock Return (US$ Million and %)

Source: stratosphere.io

TTD total revenue has grown from just US$ 45mn in 2014 to US$ 1.5bn in 2022. Growth in the last five years has been at a CAGR of 38%. The stock has given a return of 20x since the IPO in 2016.

Chart 2: TTD Take Rate as % of Gross Spend.

Source: TSOH Investment Research Service

Despite the growth in revenues, the take rate has been stable as 20% of Gross Spend.

The take rate is calculated by dividing the company's net revenue by the total amount of advertising spend that flows through its platform. US$ 20 for every US$100 of advertising that flows through TTD’s platform. It has been argued that this too high and that the company is taking advantage of its market position to charge excessive fees.

In its defence, TTD offers a wide range of services, including ad serving, audience targeting, and campaign management. These services require a significant amount of investment in technology and infrastructure. TTD has a large and growing customer base which is prepared to pay and it uses its size as leverage in negotiating with publishers and ad exchanges. In the future this high take rate may come under pressure or regulatory scrutiny

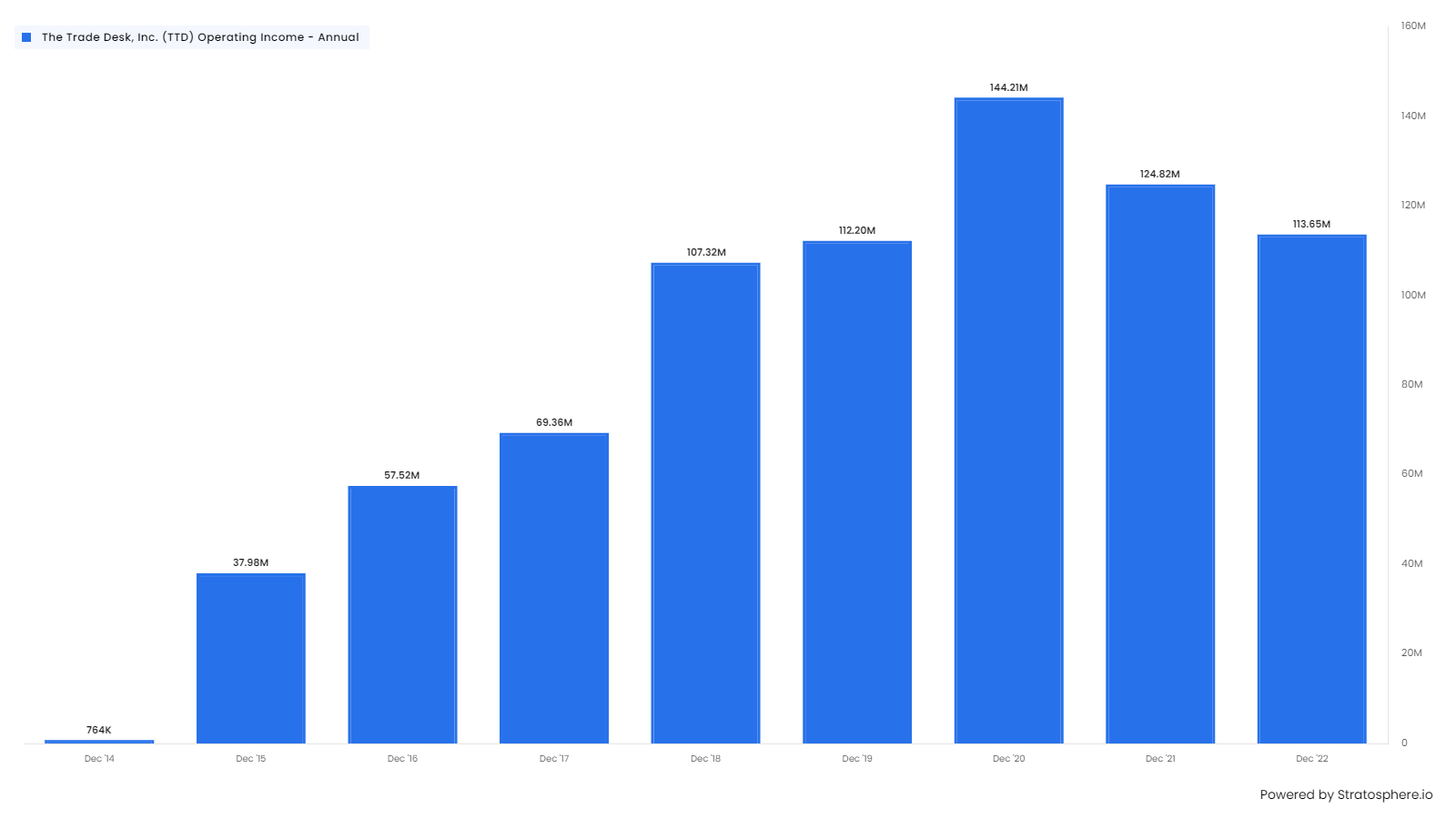

Chart 3: TTD Annual Operating Income. US$ Millions.

The growth in Operating Income has been less than growth in Revenue as seen below. US$ Millions

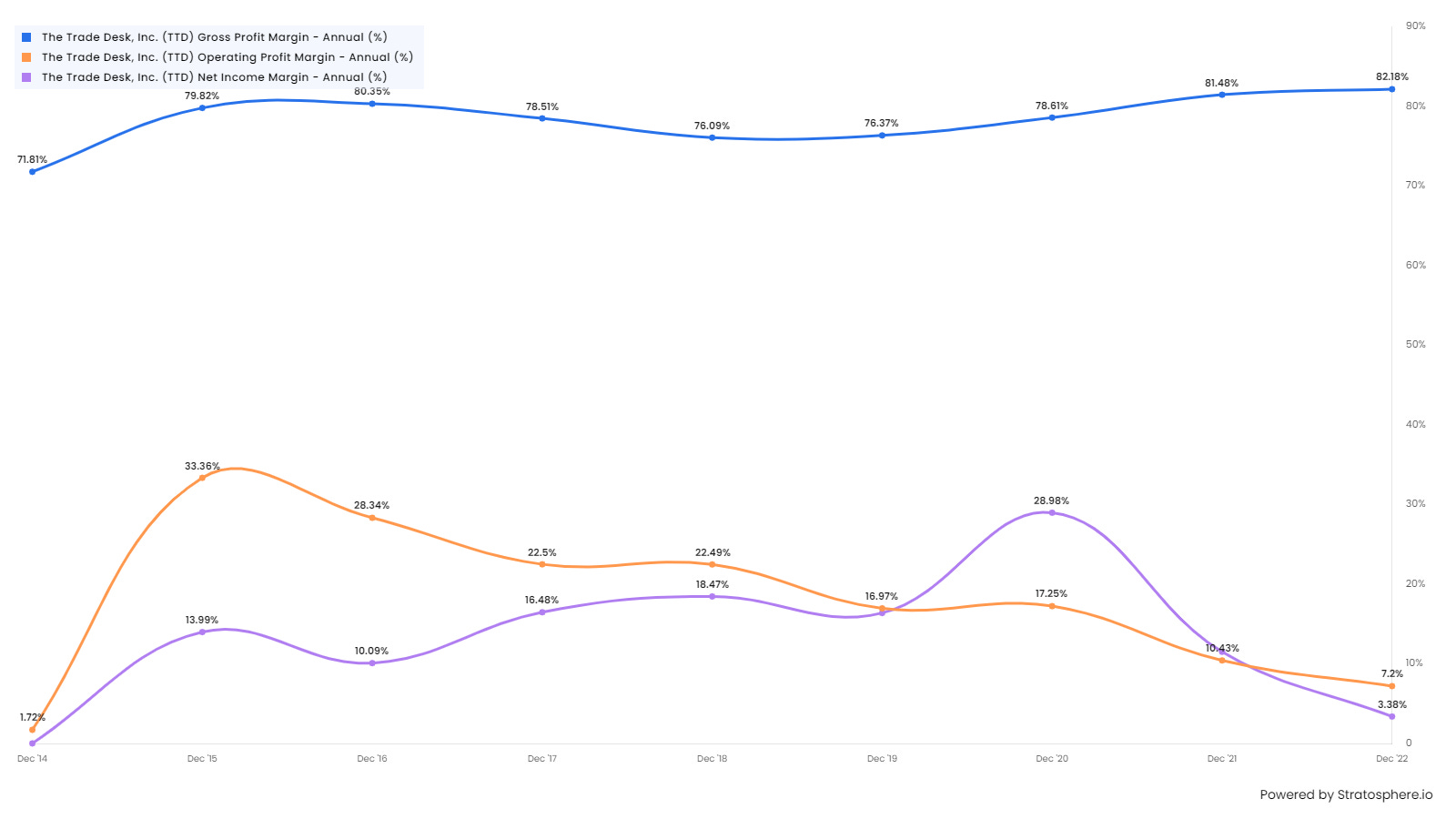

Chart 4: TTD Gross, Operating Profit Margins and Net income Margins (%)

While Gross Margin has been strong and stable at around 80% Operating and Net Margins have fallen noticeably to single digits (see above).

Chart 5: TTD Margins: SSGA expenses and R&D Expenses (the latter are the orange bars in the chart below). US$ Millions.

Source: Stratosphere.io

The recent decline in Operating and Net Margins is explained in part by the growth of SSGA expenses and R&D expenses (orange bars) shown above . The company has been investing in people and technology to develop their product offering.

Chart 6: TTD Operating Cash Flow and Free Cash Flow (in Orange Bars) US$ Millions.

Source: Stratosphere.io

This chart shows the impressive growth in both Operating and Free Cash Flow since 2019. The company seems to have hit an inflection point in 2020 to much higher cash generation.

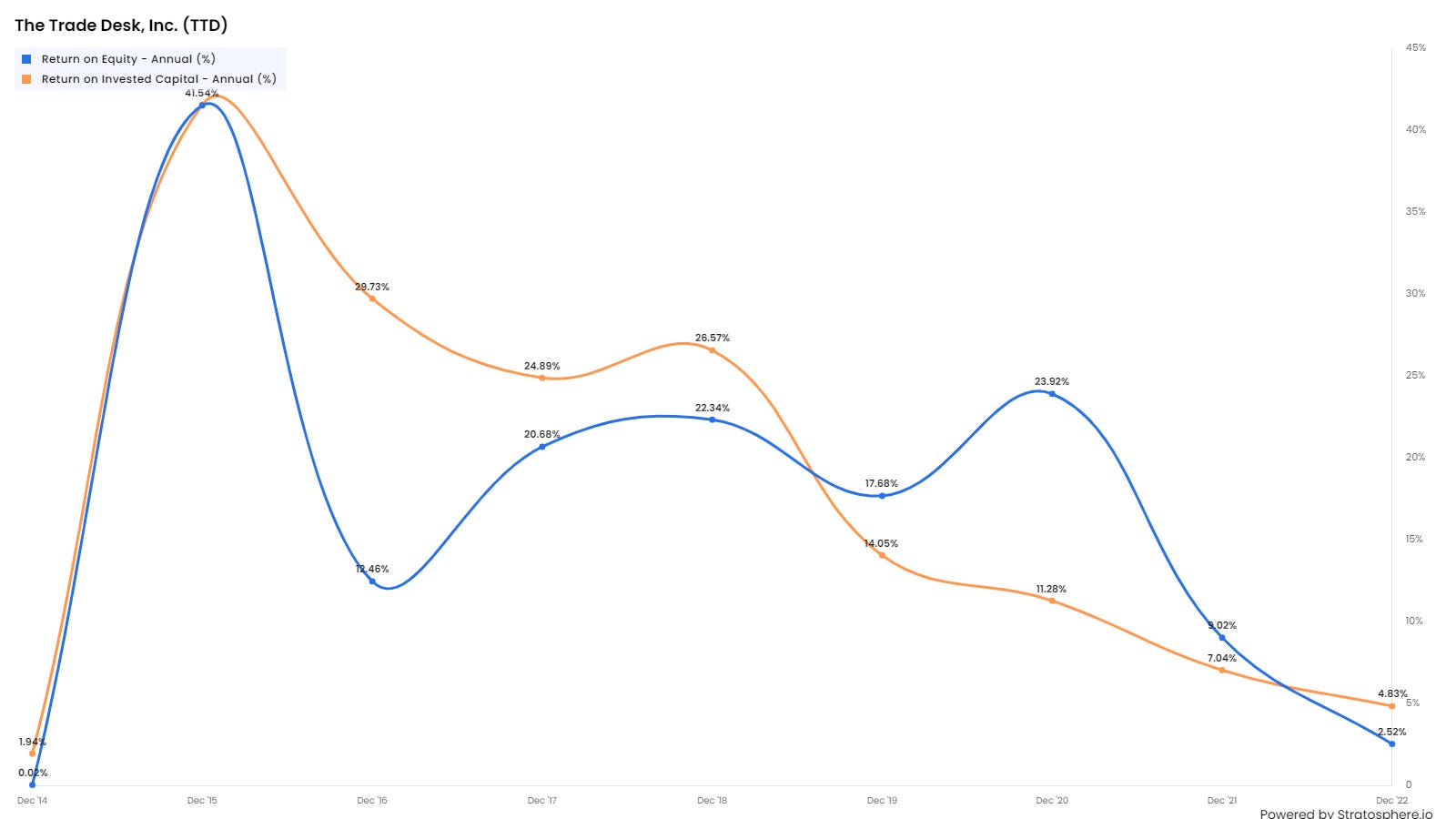

Chart 7: Return on Equity (ROE) and Return on Invested capital (ROIC) (%)

ROE has fallen in recent years as higher operating expenditures has tended to reduce profits in line with the decline in net and operating margins.

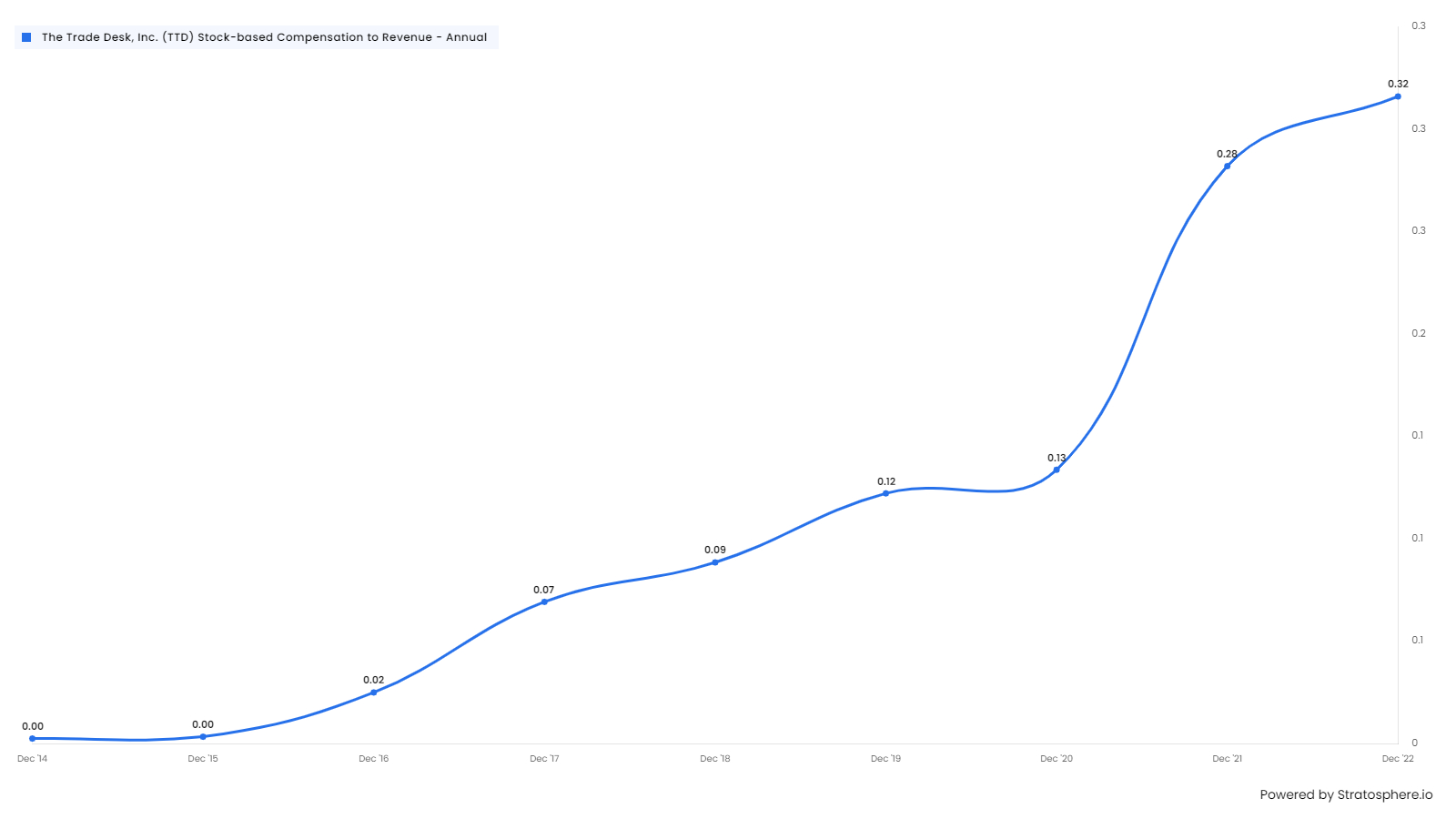

Chart 8: Stock-based Compensation as a percentage of revenue.

As company has boosted revenues. , stock-based compensation as a percentage of revenues has increased significantly from 0 in 2014 to 32% in 2022. This needs to be investigated more closely.

Chart 9: Average Total Shares Outstanding (millions)

The number of share outstanding has increased in the last five years. In the most recent quarter, the company has started buying back shares and noted that the new higher level of Free Cash Flow will allow them to both invest and buyback shares. Therefore, hopefully the share count will fall steadily from now. However, Stock compensation and capital allocation policies needs to be investigated further.

Extracts from the most recent two TTD results conference call with management.

“…as has been in the case in the last few quarters, we continue to significantly outperform the digital advertising industry. We are gaining market share as advertisers embrace the precision and relevance of data-driven advertising on the open Internet via our platform.”

“Our clients trust that we represent their interest alone and we continue to innovate our platform to bring maximum value and ROI for their brand and agency campaigns.”

“…the shift to CTV is driving significant change, not only in TV advertising but also in omnichannel advertising. In other words, our whole business. Many campaigns are now starting with high-value CTV impressions with carefully monitored reach and frequency.”

“The shift to decision CTV was reinforced at our recent Forward '23 CTV event in New York City, where most of the major streaming media companies joined us on stage to talk about how they are innovating in CTV to bring value to the world's top advertisers.”

“Even Netflix, a company who just launched their advertising business model at the end of last year, highlighted on their earnings call a few weeks ago that the ad-funded subscriber is more valuable to them than the ad-free subscriber.”

“…We are so excited about our position in the advertising ecosystem when it comes to AI. We look at over 10 million ad requests every second. Those requests, in sum, represent a very robust and very unique dataset with incredible integrity. We can point generative AI at that dataset with confidence for years to come. We know that our size, our dataset size and integrity, our profitability and our team will make Koa and generative AI a promising part of our future.”

“In the future, you’ll also hear us talk about other applications of AI in our business. These include generating code faster; changing the way customers understand and interact with their own data; generating new and more targeted creatives, especially for video and CTV; and using virtual assistance to shorten the learning curve that comes with the complicated world of programmatic advertising by optimizing the documentation process and making it more engaging.”

“The Department of Justice has clearly done their homework, which I'm encouraged by. I know there's some at Google suggesting that we've been through this 3-4 times before. I do believe that this is fundamentally different. And part of that is just because of how detailed I think the case is… We will win regardless of the outcome. We’ve won in an unfair market. Imagine what we can do with more fairness.”

As a reminder, the DOJ is suing Google over its involvement in both the supply and demand side of ad-tech. They claim it unfairly pushes advertisers to un-optimal impressions for its own gain because it makes more profit when those impressions are matched with its own supply or certain partners. Other complaints involve it reporting return metrics in intentionally opaque ways.

Across the board, UID2 is accelerating as the primary currency or CTV decisioning. As we've discussed previously, biddable marketplaces are inevitable for media companies to maximize demand and compete in the CTV content arms race. This only becomes more true as the streaming wars intensify each year. By the way, this also makes integration with The Trade Desk somewhat inevitable for all major streaming platforms as they scale because they need as much demand as possible to their platforms.

With a critical mass of premium CTV inventory available across a wide range of platforms, our advertising clients are eager to embrace the power of decisioning in their TV campaigns and many of them are working with us to drive new innovations in CTV to get the maximum value from their investments.

AI has always been a very strategic focus of The Trade Desk and we're confident that once again, we're in a leading position. In our original business plan, we said that our technology had to be a fusion of human and machine.

Last quarter, I said we expect 75% of the third-party data ecosystem to be activating on UID2 by the middle of the year. I'm proud to report today that we are now right at that level with most major third-party data providers leveraging UID2s on our platform.

OpenPath was born of an advertiser interest in a more clear and transparent path to publisher inventory…. Advertisers have long been aware that there are quite a few hops in the advertising supply chain and neither the price nor the value of each hop has ever been completely clear.

OpenPath, is very consistent with our long-term commitment to make supply chain optimization and efficiency a reality. Advertisers' eagerness for more transparency came at a time when publishers were becoming increasingly frustrated in their ability to manage yield in the complex world of programmatic. Indeed, many of them were starting to do it themselves, with some even launching their own ad servers.

Many publishers representing thousands of media properties across CTV, mobile and display have already integrated with OpenPath. And our advertisers are increasingly prioritizing direct channels, where they have a clear view of value. OpenPath is a product that directly integrates with publishers and content owners so that they can see the demand that we're bringing. It is not us getting into yield management, where we're providing the service to publishers and content owners to get them the highest CPM possible. Because for the most part, we're trying to get lower CPMs on behalf of buyers.

The growing adoption of UID2 by major advertisers and publishers speaks to the value that is placed on identity in the open Internet ecosystem.

Video which includes CTV represented a mid-40s percentage share of our business and continues to grow rapidly as a percentage of our mix. Mobile represented a mid-30s percentage share of spend as growth was again solid across in-app and mobile video. Display represented a low double-digit percent share of our business and audio represented around 5%.

Geographically, North America accounted for 88% of our Q1 spend, with international representing the remaining 12%. We're pleased to report that international growth slightly outpaced North America during this period, with particularly strong performance in EMEA. Our CTV business in Europe grew well into the triple digits year-over-year in Q1.

In Q1, we repurchased 5.1 million shares of Class A common stock for an aggregate amount of $293 million.

Summary

Advertising has been an imperfect market. The big problem for years was a lack of data on the exact impact of the advertising spend which mean the ROI was impossible to calculate and there was poor feedback loop into future strategy.

In recent years, data has proliferated. The growth of the internet, mobile and store cards etc has created an explosion in data and in data-driven targeted advertising. Digital advertising as grown much faster than old media advertising and is now widely believed to be more than 50% of all advertising.

The market for digital advertising is not very efficient. There are too many intermediaries, and this leads to elevated transaction costs. It is dominated by three large players including Google who operate walled gardens which restrict choice for buyers and creates opacity. The big players’ position mean they have significant conflicts of interest. Advertisers must trust them and cannot independently verify their claims.

The authorities are alert to this, and the DOJ have launched an anti-trust case against Google this year.

TTD has been battling in this unfair market by investing in technology, software, and AI. It only acts for the buyer and does not have its own advertising inventory.

TTD has grown revenues much faster than the market in the last five years and in the last three years has started to generate significant Operating and Free Cash Flow.

Operating and Net profit have not grown in line with Revenues as company has made significant investments in people and product.

New growth opportunities such as CTV and Retail Media Networks (RMN) are not structured to favour a walled garden strategy and present a more level playing field for TTD.

CTV has become TTD’s bread and butter as it dominates this space on the buy side and will benefit from the fact that Netflix, Disney, and HBO among others are looking at adding Ads in their offering in 2023.

Another growth vector for the company is Retail Media Networks (RMNs). The company has partnered with most large retailers active in this space and have started to look abroad.

TTD makes over 80% of its revenue in the USA and international growth is another strong opportunity.

Concluding Remarks

Growth companies are often difficult for the value investor as they often look expensive and can fall dramatically if the growth projections prove too optimistic.

We believe that TTD has a good chance of continuing to see sustained revenue growth with much higher profitability.

It is a worthy addition to our watchlist.