The Trade Desk (TTD)

An additional note.

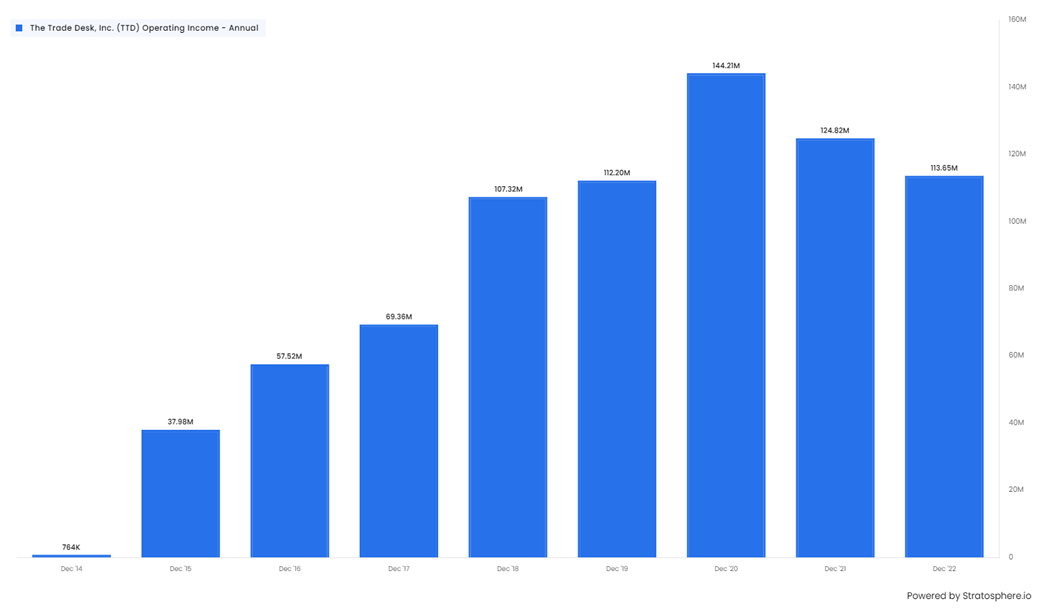

Last week we wrote a 7000 word note on The Trade Desk(TTD) . This can be accessed here . Our analysis highlighted these two charts showing total revenue and operating revenue and the divergence between the two after 2020 wherein the latter continues to rise but the latter fell.

Obviously the only reason for this is that operating costs have risen more than revenue. My suspicion was this had to do with Stock-Based Compensation (SBC) which has risen sharply as a percentage of revenue as shown below:

In 2022 stock-based compensation was a very high 32% of revenue.

We looked at the numbers in some more detail. The bottom line is SBC is too high and needs to moderate sharply in the future. If it does not, The Trade Desk may well do very well in business and financial terms, but shareholders will not necessarily enjoy the benefits as returns will be diluted due to excessive SBC.

2022 Gross Profit was US$ 1.3bn while operating profit was just US$ 113mn (see above) which implies total operating costs of about 1.2bn.

The breakdown of this is shown in the chart below:

All categories of expenses went up. R&D and Selling & Marketing Expenses doubled (in line with Revenues) and General Administrative Expenses more than tripled (!)

This is worrying as it shows excessive cost growth and suggests negative economies of scale.

Total operating expenses as a proportion of revenue increased from 83% in 2019 to 93% in 2022 with a corresponding 10% point decline in operating margin.

Operating Expenses are broken down into

Platform costs

Sales & Marketing

R&D expenses

General Administrative Costs

The first three have been constant at about 20-22% of revenues. As revenues have grown rapidly, one would have expected this number to fall to indicate some economies of scale/ operating leverage.

General Administrative expenses, however, have risen from 22% of revenues in 2019 to 33% of (much higher) revenues in 2022.

The 2022 10-k gives us some more information to the reasons for this.

“General and administrative expense increased by $151 million, or 40%, for the year ended December 31, 2022,…The increase was primarily due to increases of $138 million in personnel costs and $5 million in allocated facilities costs. The increase in personnel costs was primarily driven by a $104 million increase in stock-based compensation cost related to the CEO Performance Option, … and payroll related costs of $28 million due to hiring to support our growth, as well as return-to-office, travel and in-person event costs that did not occur in the prior year. “

There was a 104mn increase in the CEO compensation. SBC accounted for nearly US$ 500mn in 2022.”

The TTD CEO is one of the highest paid in the S&P 500. According to the March proxy statement, the company's CEO, received total compensation of $34,763,218 in 2022. This included a base salary of $1,000,000, a bonus of $15,000,000, and stock awards and options with a fair market value of $18,763,218.

Greene's compensation was significantly higher than the median compensation of $210,129 for all employees of The Trade Desk in fiscal year 2022. It was based on several factors, including the company's financial performance, his performance as CEO, and the competitive market for CEO talent. The Trade Desk's revenue grew by 46% in fiscal year 2022, and its stock price increased by 113%. Greene was also praised by the company's board of directors for his leadership and his ability to execute on the company's strategic plan. Mr Market’s (excessive(?)) enthusiasm for the shares has ensured a bumper payday for the CEO.

In order to understand the CEO’s compensation we need to look at the 2016 Incentive Award Plan. This stated that if certain specified target goals for the share price (ranging from $90.00 to $340.00 per share) the CEO’s continued service, the CEO may purchase up to 16 million shares, in eight equal tranches over a maximum term of 10 years i.e., until 2026). These target shares are subject to decrease or increase by up to 20% depending on the performance of shares for a maximum of 19.2 million shares.

The CEO Performance Option has an exercise price of $68.3 per share. As the share price is currently already US$ 75 we can assume that the CEO will be awarded up to 19.2mn shares at a price of 68.3. If we assume that price per share in 2026 is only today’s price i.e.,US$ 75, the options for the 19.2mn shares have an intrinsic value of intrinsic value of about US$ 128mn. However, these hugely understate the true value. The options have maturities of up to 2029. A large part of the value of an option come from the Time Value. Time Value can be so large and uncertain, that in the open market, nobody will willingly write long-dated options on an unhedged basis. Yet when it comes to SBC, companies do it almost without a second thought. As time goes on and (if the share price goes up), this (often significant) cost will hit the P&L evet year over the life of the options. This is what is happening with TTD.

Conclusions

TTD is a great business and should do well over the next few years.

It should be a good candidate for investment if the valuation is attractive.

However, investment is a partnership where management and large investors should treat minority investors as partners.

TTD fails on this and while the company may well do very well, shareholder returns (while positive) will get diluted to excessive SBC. The CEO and senior employees will get unfairly disproportionate share of the rewards.

There is large red flag for TTD we will not currently commit capital to it.

SBC is a complex issue, and we will cover it in more detail in a future note.